Aluminum Pigment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

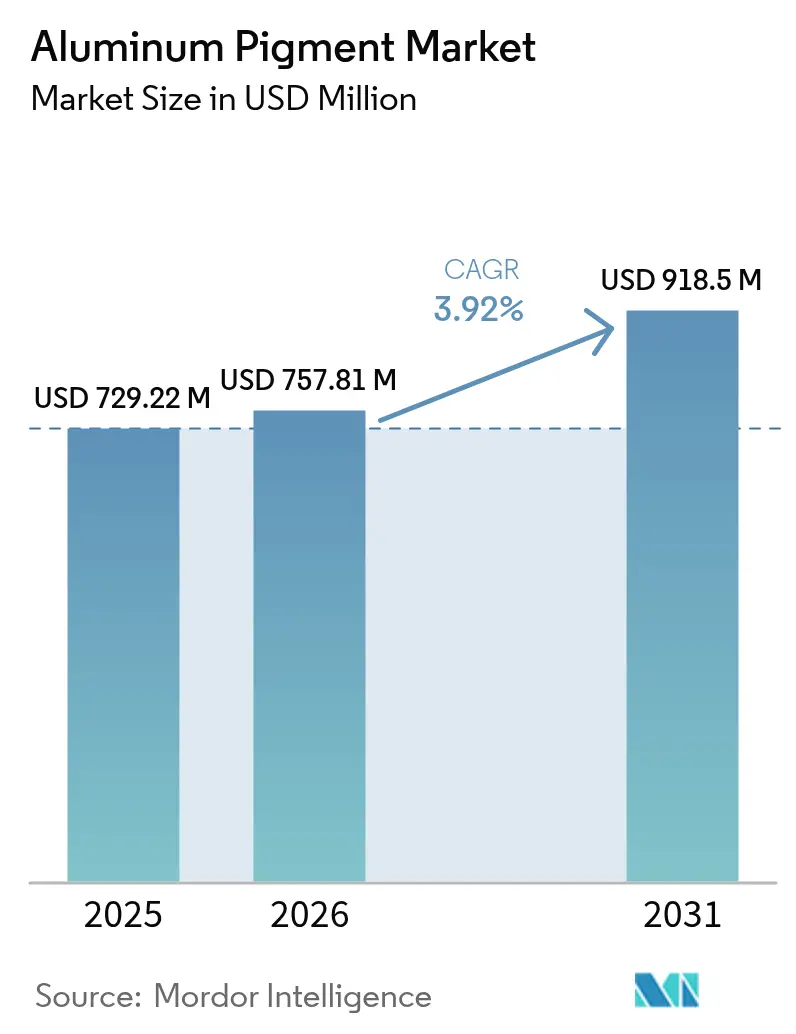

| Market Size (2026) | USD 757.81 Million |

| Market Size (2031) | USD 918.5 Million |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminum Pigment Market Analysis by Mordor Intelligence

The Aluminum Pigment Market size in 2026 is estimated at USD 757.81 million, growing from 2025 value of USD 729.22 million with 2031 projections showing USD 918.5 million, growing at 3.92% CAGR over 2026-2031. This steady trajectory is shaped by resilient demand for premium metallic automotive finishes, stricter global VOC rules that accelerate adoption of high-performance powder coatings, and expanding use of reflective pigments in cool-roof systems designed to curb urban heat. Larger producers that control upstream aluminum supplies are cushioning the impact of raw-material price swings and meeting the industry’s decarbonization targets with lower-carbon production routes. Meanwhile, sustained research and development spending on encapsulation and radar-transparent technologies is opening high-margin applications in autonomous vehicles and additive manufacturing.

Key Report Takeaways

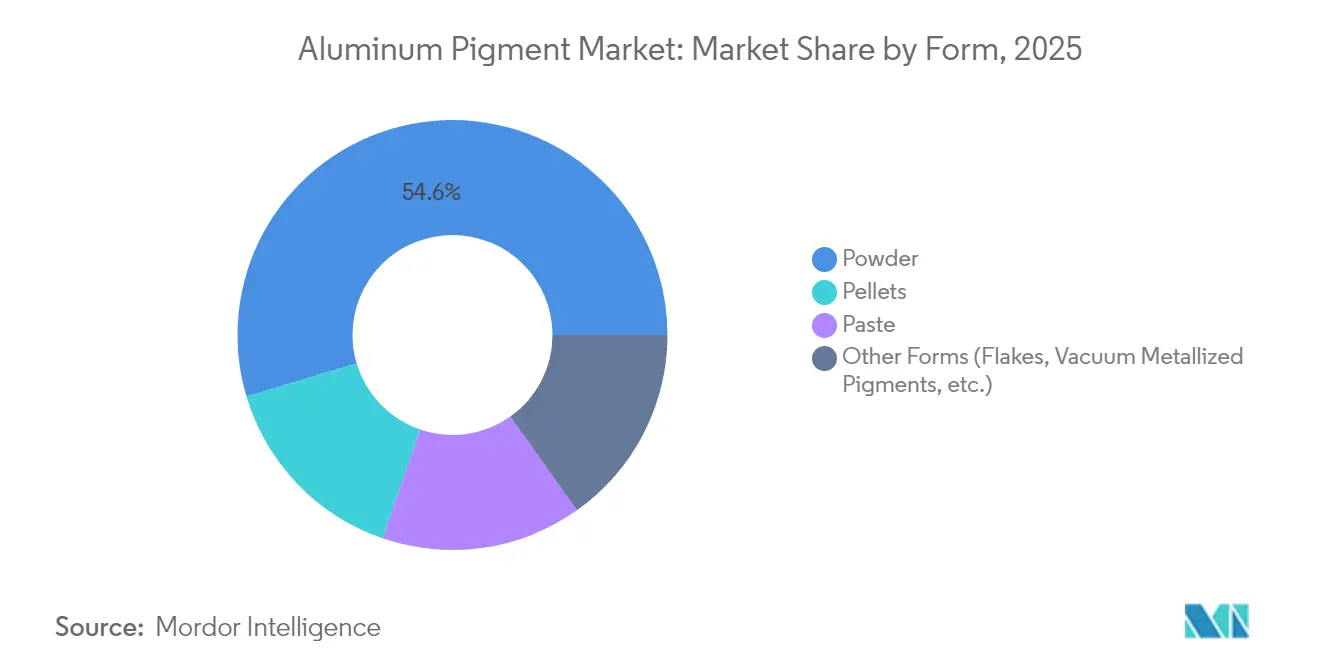

- By form, powder held 54.62% of the aluminum pigment market share in 2025, while other forms recorded the quickest 4.83% CAGR through 2031.

- By coating type, non-leafing accounted for 62.78% of the aluminum pigment market size in 2025, and leafing is advancing at a 4.58% CAGR through 2031.

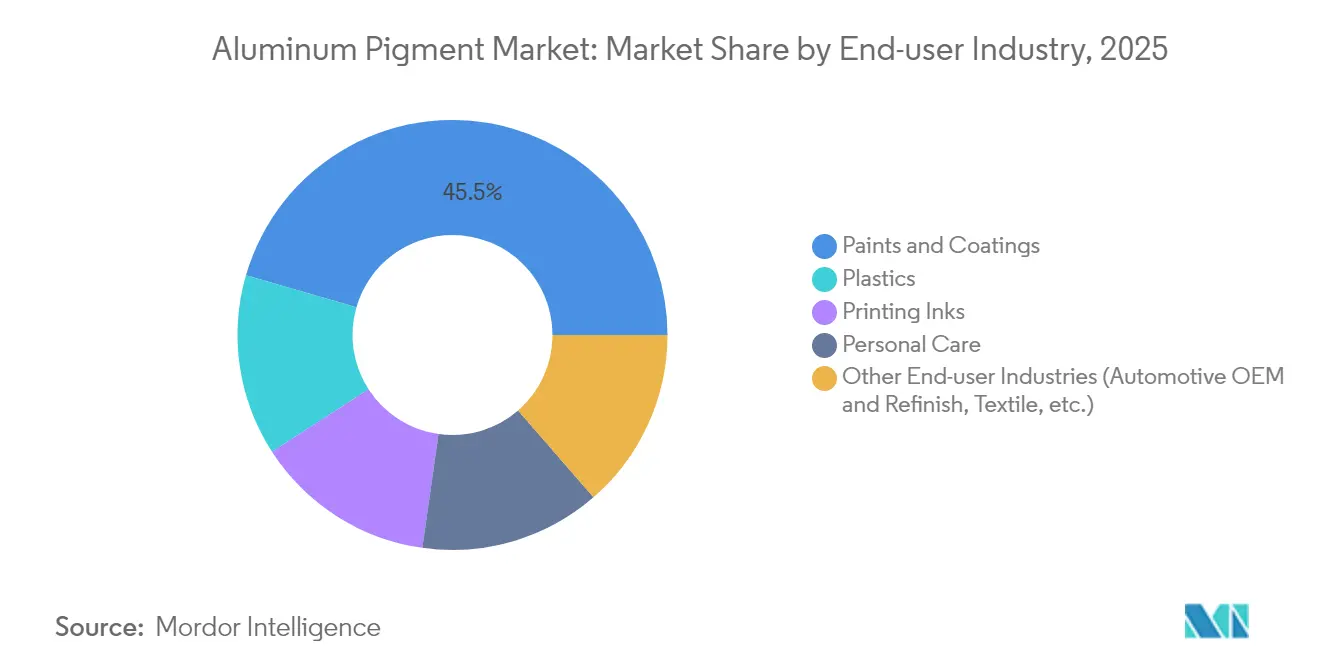

- By end-user industry, Asia-Pacific accounted for 45.52% of the aluminum pigment market size in 2025, and other industries are growing with a CAGR of 4.46%.

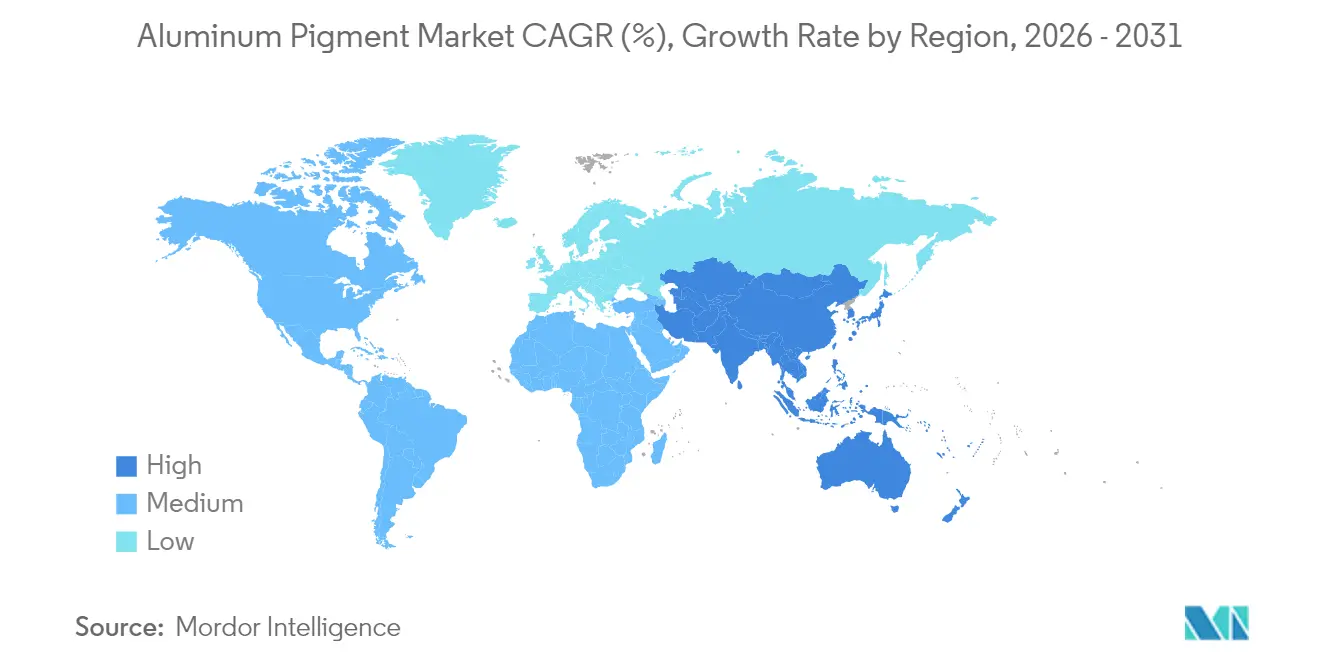

- By geography, Asia-Pacific captured 46.35% revenue share in 2025; the region is projected to lead growth at a 4.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aluminum Pigment Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for metallic automotive finishes | 1.2% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Rising adoption of high-performance powder coatings | 0.9% | Europe and North America core, expanding to APAC | Long term (≥ 4 years) |

| Expansion of personal care and cosmetics with effect pigments | 0.7% | Global, with premium markets in North America and Europe | Medium term (2-4 years) |

| Emerging use of aluminum flakes in additive manufacturing feedstocks | 0.5% | North America and Europe, early adoption in APAC | Long term (≥ 4 years) |

| Reflective cool-roof coatings for urban heat-island mitigation | 0.4% | Global urban centers, particularly hot climate regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Metallic Automotive Finishes

Regulatory limits on solvent emissions and consumer preference for premium styling push automakers toward metallic coatings that incorporate finely milled aluminum flakes. Electric-vehicle OEMs view these pigments as a dual-benefit material: they deliver eye-catching effects and improve thermal reflectivity, which lessens battery heat gain in warm climates. Autonomous-vehicle developers have added performance criteria around LiDAR and radar transparency, prompting suppliers to engineer narrow particle-size cuts that maintain reflectance without signal scatter. Automotive refinish suppliers also rely on aluminum pigments because repair jobs must match OEM shades while curing at temperatures low enough to protect plastic trims. Sector-wide, these requirements channel research and development budgets into tailored encapsulation methods that enhance corrosion resistance in waterborne formulations.

Rising Adoption of High-Performance Powder Coatings

Powder coatings eliminate VOC emissions, cut overspray waste, and offer single-coat coverage, making them the finish of choice for appliances, architecture, and wheels. Aluminum pigments enable bright metallic looks in these systems, but must retain brilliance after a 200 °C bake. Producers now suspend flakes in silica sol-gel or silicone shells to block oxidation, allowing glossy powder lines to pass salt-spray and humidity tests demanded by appliance brands.

Expansion of Personal Care and Cosmetics with Effect Pigments

North American and European beauty labels are moving beyond conventional pearl effects toward colored metallics that shift hues under diverse lighting. The U.S. FDA’s approval of aluminum powder for externally applied cosmetics, including eye-area products, gives formulators predictable safety rules and accelerates launch pipelines[1]U.S. Food and Drug Administration, “Regulatory Status of Color Additives: Aluminum Powder,” fda.gov. Encapsulation technologies adapted from industrial coatings protect the pigments from moisture and skin oils while preserving shimmer. Brands extend the metallic motif to recyclable aluminum packaging, reinforcing a premium, monomaterial aesthetic and nudging demand for effect pigments in both content and container.

Emerging Use of Aluminum Flakes in Additive Manufacturing Feedstocks

Laser powder bed fusion and binder-jetting methods are migrating from prototypes to serial aerospace and motorsport parts. Certified spherical aluminum powders with tight oxygen limits deliver crack-free prints and weight savings unattainable with cast alloys. Producers such as ECKART obtained DIN EN 9100:2018 approval in 2024 for aerospace-grade atomized powders, underpinning confidence among tier-one suppliers. Blend developers also add low-aspect-ratio flakes into photopolymer and composite filaments to impart electromagnetic shielding or heat-dissipation traits, broadening the aluminum pigment market beyond decorative roles.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EHS regulations on metal powders | -0.8% | Global, with stricter enforcement in Europe and North America | Short term (≤ 2 years) |

| Volatility in primary aluminum prices and supply | -0.6% | Global, with particular impact on cost-sensitive applications | Short term (≤ 2 years) |

| Energy-intensive production processes under decarbonization pressure | -0.5% | Global, with immediate impact in carbon-regulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EHS regulations on metal powders

Europe’s revised CLP Regulation and the U.S. OSHA dust-combustion rules require upgraded ventilation, inert-gas milling, and ATEX-certified packaging lines. Compliance costs escalate fastest for producers under 5,000 t/y, encouraging mergers that pool capital and engineering know-how. Updated U.S. Subpart RRR limits hydrogen chloride and particulate releases from secondary smelters, affecting pigment plants that tap scrap streams for greener inputs[2]U.S. Government Publishing Office, “40 CFR Part 63 Subpart RRR—National Emission Standards for Hazardous Air Pollutants for Secondary Aluminum Production,” ecfr.gov . In turn, the aluminum pigment market experiences a near-term growth drag until upgraded plants come online.

Energy-Intensive Production Processes Under Decarbonization Pressure

Producing 1 ton of primary aluminum still emits around 11 tons of CO₂ in coal-based regions. RMI calculates that the global aluminum chain requires nearly USD 1 trillion in capital by 2050 to hit net-zero. In pigment terms, higher Scope-1 and 2 charges under EU ETS Phase 4 and Canada’s carbon-pricing reforms raise operating costs for smelters that feed flake plants. While hydropower-rich smelters in Canada and Norway gain share, producers reliant on coal power face a medium-term capex burden, subtracting 0.5 percentage points from the growth rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Versatile Powder Steers Market Expansion

Powder held the largest 54.62% aluminum pigment market share in 2025 thanks to its ease of dispersion in automotive and industrial coatings. The aluminum pigment market size for powder formats is projected to grow steadily alongside high-performance powder coatings that cure faster and cut VOCs. In usage terms, low-oil-absorption grades enable thicker film builds without compromise on metallic sparkle, while dust-free granules improve worker safety during electrostatic application.

Other forms, chiefly flakes and vacuum-metallized pigments, represent the quickest 4.83% CAGR through 2031. Flakes mirror visible and near-infrared wavelengths efficiently, making them a staple in cool-roof and façade systems that demand both reflective function and design freedom. Vacuum-metallized pigments, produced by physical vapor deposition, deliver mirror-like brilliance prized in consumer electronics casings. Pellets and pastes remain niche but essential for waterborne or UV-cured formulations that need zero airborne dust.

By Coating Type: Non-Leafing Dominates while Leafing Gains Specialty Ground

Non-leafing pigments accounted for 62.78% of the aluminum pigment market size in 2025 because their surface treatment drives them into the coating matrix, affording abrasion resistance ideal for wheel rims and exterior appliances. Their orientation improves underlying substrates' chemical passivation, extending architectural panels' maintenance cycles.

Leafing grades orient at the surface, producing chrome-like sheen valued in decorative trims. Although smaller in volume, they will post the faster 4.58% CAGR to 2031 as sensor-compatible formulations for autonomous vehicles mature. Low-sparking varieties also find favor in marine topcoats that must balance metallic look with radar invisibility, giving suppliers another entry point to defense markets.

By End-user Industry: Paints and Coatings Anchor Demand

Paints and coatings absorbed 45.52% of revenue in 2025, with automotive OE, refinish, and architectural uses at the helm. Refinish shops, unable to bake panels at 180 °C, depend on readily dispersible aluminum pastes that flash at ambient temperatures yet replicate factory colors. Cool-roof policies add incremental tonnage in the construction sector, while clear-over-base systems in SUVs and pickups boost metallic loadings.

Other industries, led by electric-vehicle battery casings, plastic masterbatches for personal devices, and color-shifting cosmetics, deliver a 4.46% CAGR to 2031. Colored aluminum flakes in mascaras and highlighters satisfy consumer appetite for high-definition sparkle, showing how functional advances translate to lifestyle markets.

Geography Analysis

Asia-Pacific controlled 46.35% of 2025 sales and is set to expand at a 4.55% CAGR through 2031. India’s smelting output rose 11% to 4.016 million tons in 2024, underpinning domestic pigment feedstock security. Japan’s auto-grade aluminum demand recovery also supports higher-value pigments for premium brands.

North America benefits from a carbon footprint roughly 50% below the global average, thanks to hydroelectric smelters in Canada and widespread recycling. Europe mirrors this drive, with Hydro partnering with Porsche in 2024 to supply low-carbon aluminum across vehicle lines. These moves stimulate demand for sustainably certified aluminum pigments in luxury branding.

South America, the Middle East, and Africa collectively display emerging demand curves tied to rising infrastructure spending and light-vehicle assembly. GCC construction codes now reference solar-reflective index thresholds, opening doors for NIR-reflective grades. In Brazil and Mexico, pickup and compact-SUV output serves as a pull factor for local pigment blending houses, although currency volatility keeps imports sensitive to metal price shocks.

Mordor Intelligence provides coverage of the aluminum pigment market across other key regional markets. Detailed country-level analysis extends to France incorporating local coverage and market participation, as required.

Competitive Landscape

The market is consolidated in nature. Market consolidation quickened in 2024 when ALTANA acquired Silberline, inflating ECKART division sales by 24% to EUR 224 million and widening distribution in North America and Asia. Scale provides leverage for capital-intensive health-and-safety upgrades and greener energy purchases. Competitors with strong backward integration buffer aluminum price swings and secure recycled feed for low-carbon offerings. Technical differentiation centers on surface treatments. Silica sol-gel and silicone encapsulation protect flakes during waterborne curing and alkaline detergents.

Aluminum Pigment Industry Leaders

ALTANA

DIC CORPORATION -

SCHLENK SE

TOYO ALUMINIUM K.K.

Asahi Kasei Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: ALTANA formed a joint venture with Runaya to build a sustainable aluminum powder plant in India with aerospace and solar applications.

- January 2024: ALTANA closed the Silberline acquisition, integrating global manufacturing and distribution footprints for aluminum pigment through its subsidiary ECKART.

Global Aluminum Pigment Market Report Scope

The Aluminum Pigment report includes:

| Powder |

| Pellets |

| Paste |

| Other Forms (Flakes, Vacuum Metallized Pigments, etc.) |

| Leafing |

| Non-Leafing |

| Paints and Coatings |

| Plastics |

| Printing Inks |

| Personal Care |

| Other End-user Industries (Automotive OEM and Refinish, Textile, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Powder | |

| Pellets | ||

| Paste | ||

| Other Forms (Flakes, Vacuum Metallized Pigments, etc.) | ||

| By Coating Type | Leafing | |

| Non-Leafing | ||

| By End-user Industry | Paints and Coatings | |

| Plastics | ||

| Printing Inks | ||

| Personal Care | ||

| Other End-user Industries (Automotive OEM and Refinish, Textile, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the aluminum pigment market?

The aluminum pigment market size is USD 757.81 million in 2026 and is expected to reach USD 918.5 million by 2031.

Which region leads the aluminum pigment market?

Asia-Pacific holds the largest regional position with a 46.35% share in 2025 and is projected to grow at 4.55% CAGR through 2031.

Why are aluminum pigments important in electric vehicles?

They provide metallic aesthetics while reflecting heat, helping to keep battery packs cooler and improving vehicle efficiency.

How do environmental regulations affect aluminum pigment producers?

Strict VOC and dust-combustion rules force upgrades to encapsulation technology and plant safety systems, raising capital requirements and driving consolidation.

What is driving demand for aluminum pigments in building materials?

Urban heat-island regulations encourage reflective cool-roof coatings that use near-infrared-reflective aluminum pigments to reduce cooling loads.

Page last updated on: