Texture Paints Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

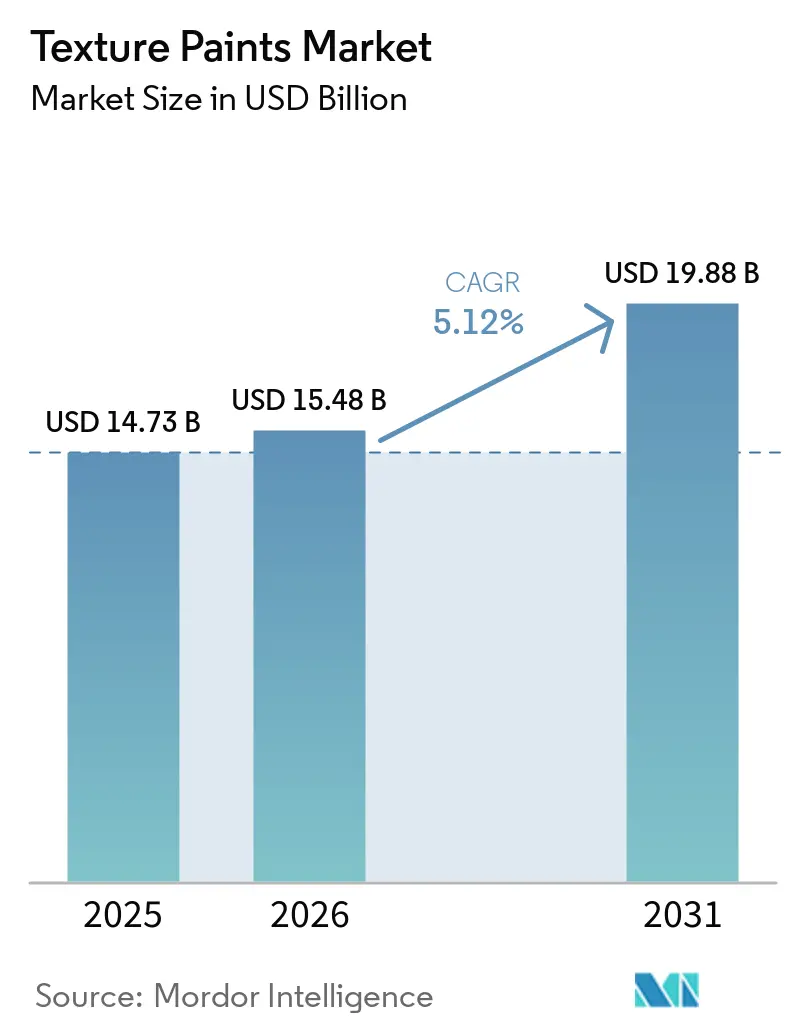

| Market Size (2026) | USD 15.48 Billion |

| Market Size (2031) | USD 19.88 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Texture Paints Market Analysis by Mordor Intelligence

The Texture Paints Market size is expected to grow from USD 14.73 billion in 2025 to USD 15.48 billion in 2026 and is forecast to reach USD 19.88 billion by 2031 at 5.12% CAGR over 2026-2031. Demand for low-VOC, thermally efficient coatings is growing as stricter green-building codes are implemented. However, rising raw material costs and a shortage of skilled labor continue to constrain profit margins. The adoption of micro-ceramic additives, AI-driven color-matching tools, and rapid urbanization in emerging economies are influencing purchasing decisions. Additionally, global supplier consolidation is accelerating as companies aim to achieve economies of scale in sourcing titanium dioxide and funding R&D for advanced binders. Climate policies, digital retail channels, and changing homeowner preferences are steering the texture paints market toward waterborne, roll-on products that offer easier application and energy efficiency.

Key Report Takeaways

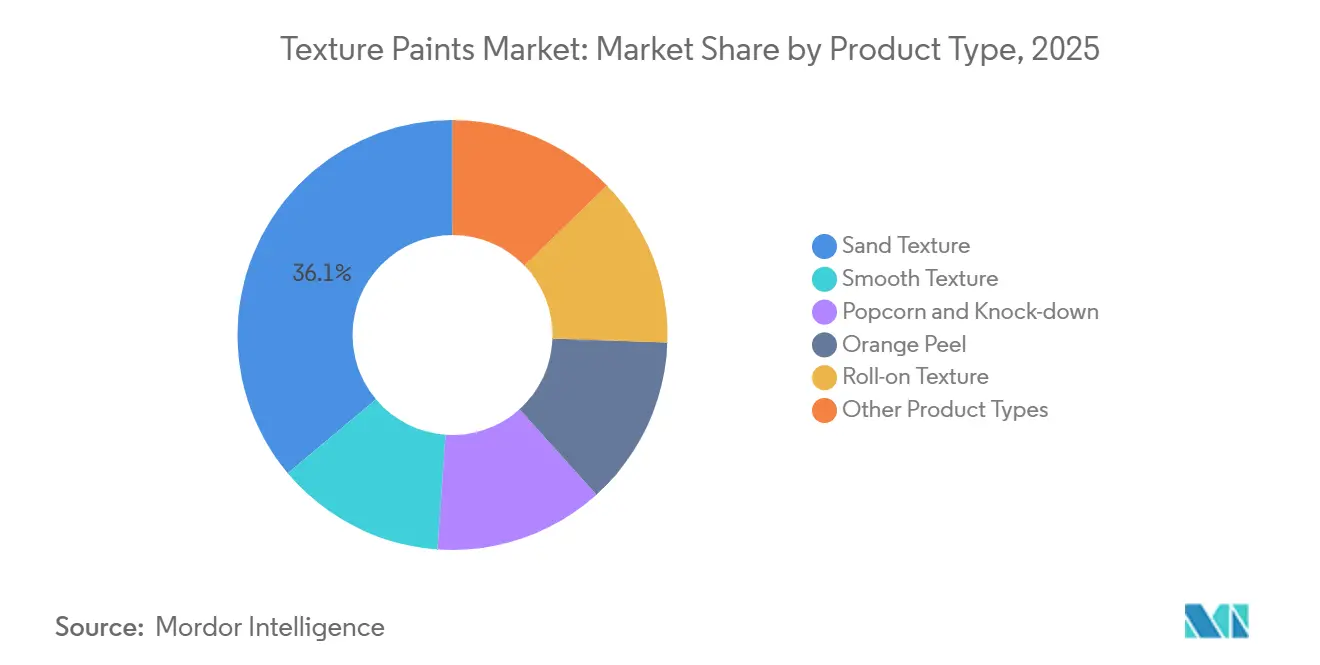

- By product type, sand texture led with 36.11% of the texture paints market share in 2025, while roll-on texture is forecast to advance at a 5.08% CAGR through 2031.

- By substrate, interior walls held 46.65% of the texture paints market share in 2025, while wood and metal surfaces are projected to expand at a 5.41% CAGR through 2031.

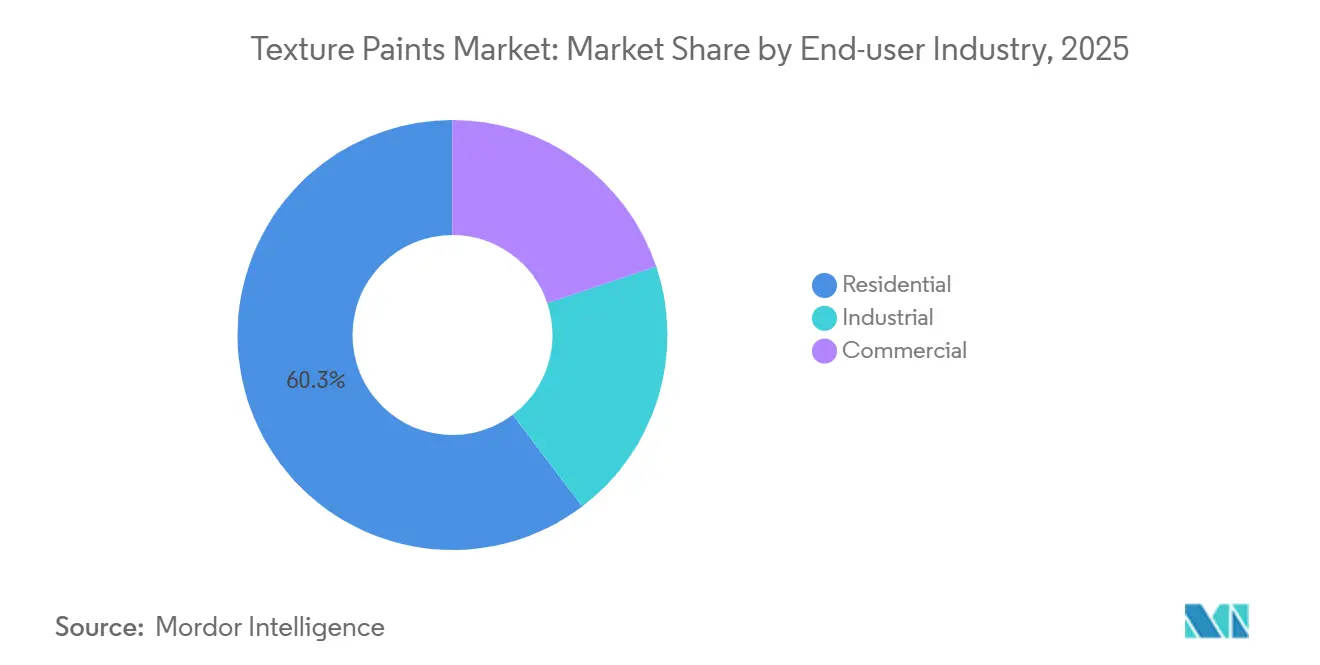

- By end-user industry, the residential segment captured 60.31% of the texture paints market share in 2025, while the commercial segment is growing at a 5.70% CAGR through 2031.

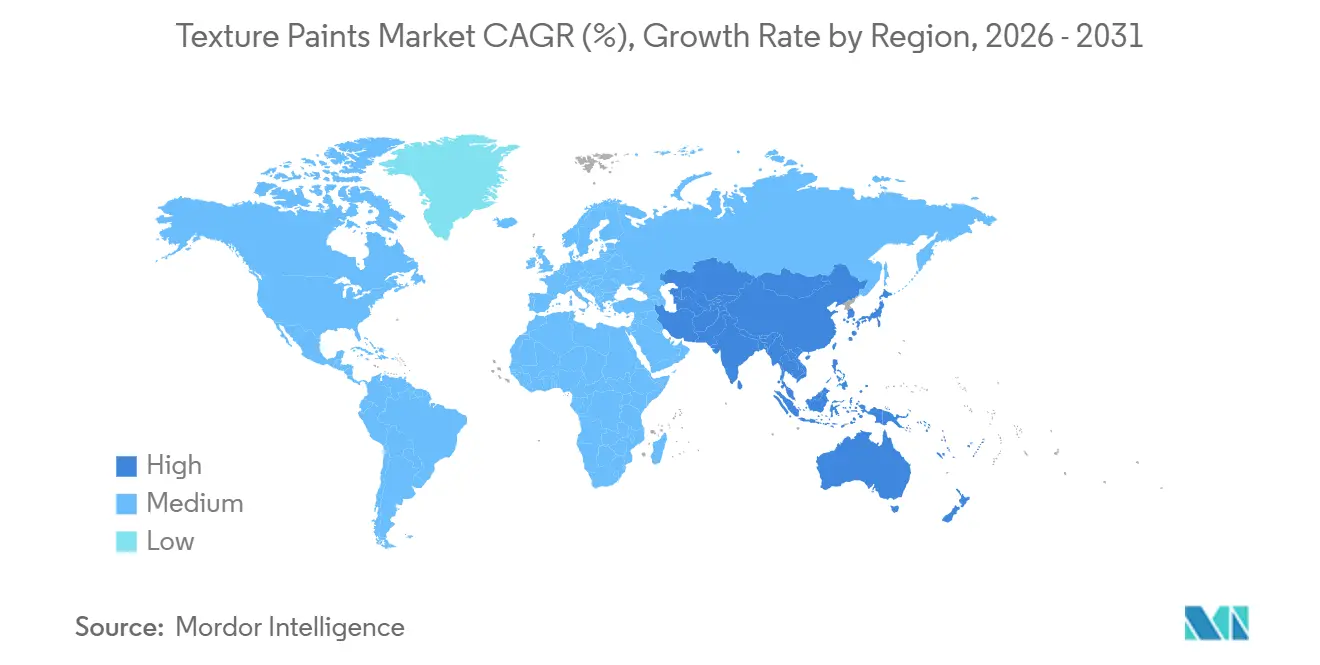

- By geography, Asia-Pacific accounted for 38.89% of the texture paints market share in 2025 and is set to grow at a 5.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Texture Paints Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-building certification driving low-VOC textures | +0.9% | Global, with early leadership in North America, EU, and select APAC metros (Singapore, Seoul, Tokyo) | Medium term (2-4 years) |

| Premiumization trend in millennial home ownership | +0.7% | North America, Western Europe, urban India, China Tier-1 cities | Medium term (2-4 years) |

| AI-powered color-matching tools accelerating DIY adoption | +0.5% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| Micro-ceramic additives enabling thermo-regulating textures | +0.6% | Global, with early adoption in Middle-East, Southern Europe, India | Long term (≥ 4 years) |

| 3D-printed interior panels requiring high-adhesion coatings | +0.3% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Green-Building Certification Driving Low-VOC Textures

Programs like LEED, BREEAM, and WELL now limit VOC content in interior paints to 30-50 g/L, leading to a shift from solvent-borne binders to waterborne acrylics and bio-based resins[1]U.S. Green Building Council, “LEED v4.1 Paints and Coatings Requirements,” usgbc.org. The EU Ecolabel has further tightened semi-volatile thresholds for 2026 and requires life-cycle disclosure of microplastics, effectively phasing out traditional acrylic copolymers. Products such as Arkema’s Synaqua 4804 dispersion and Sherwin-Williams’ Repacor SW-1000 system demonstrate the market's texture paints market's adaptation. Large contractors benefit from batch-level VOC certification, which helps clients earn green-building points. This has resulted in a two-tier pricing structure, with certified low-VOC textures commanding a 15-20% premium, while solvent-borne alternatives remain common in cost-sensitive emerging markets.

Premiumization Trend in Millennial Home Ownership

Homeowners aged 30-44 are driving demand for textured finishes like Venetian plaster, knockdown, and sand-swirl, which are priced 25-40% higher than flat finishes due to their tactile and aesthetic appeal. In India, the Pradhan Mantri Awas Yojana program has driven decorative paint volume growth of 4-5% in FY 2026, with textured finishes contributing significantly to value growth. Products such as Birla White Textura, launched in 2024, offer pre-mixed cement-based textures that reduce labor time by 30%. Distribution networks are expanding into tier-2 cities, transitioning texture paints from niche to mass-premium categories within the texture paints market. Manufacturers face the challenge of scaling production while maintaining margins against competition from private-label brands.

AI-Powered Color-Matching Tools Accelerating DIY Adoption

AI-powered platforms allow users to photograph a reference and receive precise texture-paint formulas, reducing the need for multiple store visits. Tools such as Sherwin-Williams’ ColorSnap and Benjamin Moore’s Color Portfolio apps have increased direct-to-consumer sales by 20-30% since 2024. Brands integrating AI tools into e-commerce platforms capture higher margins and gain valuable consumer data but must address application errors that could harm brand reputation. Instructional videos and texture kits are being used to mitigate these risks within the evolving texture paints market.

Micro-Ceramic Additives Enabling Thermo-Regulating Textures

Hollow ceramic microspheres reduce thermal conductivity by 15-25%, lowering interior wall temperatures by 2-4 °C in hot climates. Research indicates that electrospun ceramic nanofibers in acrylic binders achieve thermal conductivity of 0.045 W/m·K, comparable to rigid foam insulation, while maintaining adhesion. Middle-Eastern construction codes now recognize thermally efficient coatings, with Jazeera Paints leading regional production. Although ceramic fillers add USD 0.50-1.00 per liter, adoption is concentrated in commercial projects where energy savings justify the cost. Incentives under Saudi Arabia’s building code and the UAE’s Pearl system are expected to accelerate adoption within four to six years, further strengthening the texture paints market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and mineral-aggregate prices | -1.2% | Global, with acute pressure in Europe (anti-dumping duties) and North America (Venator capacity loss) | Short term (≤ 2 years) |

| Skill gap in spray-applied high-build textures | -0.6% | North America, Western Europe, with emerging pressure in urban APAC | Medium term (2-4 years) |

| Competition from peel-and-stick architectural films | -0.3% | North America, Western Europe, urban APAC metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ and Mineral-Aggregate Prices

Titanium dioxide prices are projected to reach USD 3,500 per ton in 2026, up from USD 3,200 in 2025, driven by Venator’s bankruptcy and the closure of Tronox’s plant. EU anti-dumping duties on Chinese TiO₂ imports further exacerbate cost pressures. A USD 300 price increase could reduce gross margins by 3-5% unless passed on to consumers. Manufacturers are responding by lowering TiO₂ content, sourcing from India and Turkey, or integrating pigment production. For example, Asian Paints’ USD 217 million Indore expansion includes new dispersion lines. Short-term volatility could push prices above USD 4,000 per ton by 2027.

Skill Gap in Spray-Applied High-Build Textures

In 2024, the U.S. reported approximately 650,000 construction vacancies, with trade-school enrollment down 40% compared to pre-pandemic levels[2]. Europe faces similar challenges, with 86-89% of firms citing a lack of skilled labor. Spray-applied textures require precise techniques, and errors can lead to costly rework. While large contractors are investing in airless sprayers and robotics, smaller firms face difficulties. This labor shortage is driving demand for roll-on products that require less expertise in the texture paints market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Roll-On Gains as DIY Confidence Rises

Sand texture accounted for 36.11% of the texture paints market share in 2025. Roll-on texture is anticipated to grow at a compound annual growth rate (CAGR) of 5.08% through 2031, supported by AI tools that simplify color selection and pre-mixed kits that minimize blending errors. Popcorn and knockdown textures are seeing a modest resurgence in multifamily housing due to their acoustic advantages, despite varying aesthetic preferences. Smooth finishes remain the preferred choice for premium interiors requiring seamless drywall, while orange peel textures dominate mass housing due to their cost-effectiveness in masking minor substrate imperfections. Regulatory trends favor waterborne chemistry, enabling producers with compliant roll-on lines to achieve incremental market gains.

Regional preferences significantly influence demand. Minimalist themes among millennial and Gen-Z buyers are shifting market share toward subtle textures. The EU Ecolabel regulations, effective since 2026, mandate waterborne binders, accelerating the phase-out of solvent-borne popcorn sprays in Europe. Similarly, California’s SCAQMD Rule 1113 imposes stringent VOC limits. Manufacturers that invested in low-VOC smooth and sand products now benefit from expanded shelf space, while others face reformulation challenges.

By Substrate Type: Wood and Metal Surfaces Accelerate on Thermal Innovation

Interior walls held a 46.65% share of the texture paints market in 2025. Wood and metal surfaces are projected to grow at a CAGR of 5.41% through 2031, driven by the adoption of micro-ceramic additives that enhance thermal performance on non-porous substrates. Exterior walls require elastomeric textures to bridge cracks caused by extreme temperature fluctuations, particularly in the Middle-East and Southern Europe. Ceilings continue to use popcorn and knockdown textures for acoustic damping, although the trend toward exposed ceilings in office designs is reducing demand in this niche. Emerging substrates, such as 3D-printed panels, necessitate high-adhesion primers, presenting future R&D opportunities.

Wood and metal textures command premium pricing due to their critical adhesion and corrosion resistance properties. Data centers and food processing facilities increasingly specify ceramic-enhanced coatings for energy efficiency, driving growth in this niche segment, which is expected to outpace the overall texture paints market as sustainability audits emphasize energy loss reduction.

By End-user Industry: Commercial Segment Prioritizes Lifecycle Value

The residential segment accounted for 60.31% of market texture paints market size demand in 2025, driven by remodeling activities and new-home construction. The commercial segment is projected to grow at a CAGR of 5.70% through 2031, as offices, hotels, and mixed-use developments adopt antimicrobial and pollution-resistant textures that extend maintenance cycles. Although industrial buyers represent a smaller volume, they pay premium prices for high-build epoxy or polyurethane textures designed to withstand heavy traffic and chemical exposure.

Lifecycle costing is a key factor in commercial real estate specifications. Antimicrobial coatings with silver or copper additives are gaining traction in hospitals and food facilities, while photocatalytic textures that break down grime are reducing cleaning costs in polluted urban areas. The residential segment remains price-sensitive but is gradually moving toward higher-end products influenced by social media design trends.

Geography Analysis

Asia-Pacific generated 38.89% of texture paints market revenue in 2025 and is set to grow at a CAGR of 5.45% through 2031. Despite a 9.4% year-on-year decline in China’s total coatings output in 2025, premium faux-stone and art textures gained market share, reflecting a shift toward higher-value products even amid volume contraction. Southeast Asia and the Middle-East are experiencing growth driven by large-scale projects specifying heat-reflective and bacteria-resistant coatings.

North America’s texture paint industry market is supported by commercial construction and stringent low-VOC regulations. California’s VOC limit of 50 g/L is accelerating the adoption of waterborne products. While economic uncertainty dampens demand, renovation subsidies in Germany and France are mitigating the impact of slower new construction. The Middle-East and Africa are benefiting from mega-developments in Saudi Arabia and the UAE. In Latin America, data coverage remains limited, but Sherwin-Williams’ USD 1.15 billion acquisition of Suvinil highlights optimism, particularly given Brazil’s local raw material base, which helps shield margins from global price fluctuations.

Competitive Landscape

The market exhibits low concentration. AkzoNobel and Axalta announced a USD 25 billion all-stock merger, combining 173 factories and 91 R&D sites, with an expected USD 600 million in cost synergies. JSW Paints acquired Akzo Nobel India for USD 1.5 billion, becoming the third-largest decorative paint player in India. Sherwin-Williams’ USD 1.15 billion acquisition of BASF’s Suvinil added two plants and a strong brand presence in Brazil.

Technology and sustainability are key differentiators for future market leaders. Companies investing in AI-driven color-matching and e-commerce platforms are bypassing traditional retail channels and gaining direct consumer insights. R&D budgets are increasingly focused on eliminating PFAS, reducing VOCs, and incorporating ceramic additives. Smaller producers face cost pressures from rising TiO₂ prices and complex regulatory requirements. Some are responding by specializing in local textures or partnering with additive suppliers to license ready-to-use formulations.

Texture Paints Industry Leaders

Akzo Nobel N.V.

Nippon Paint Holdings Co., Ltd.

PPG Industries, Inc.

The Sherwin-Williams Company

Asian Paints Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: JSW Paints Limited finalized the acquisition of a 61.2% controlling stake in Akzo Nobel India, gaining control of the Dulux brand. This acquisition impacted the texture paints market by enhancing JSW Paints' market share and intensifying competition.

- September 2025: Asian Paints Ltd. invested INR 1,500–2,000 crore to establish a new water-based paint plant in Indore, Madhya Pradesh, with an annual production capacity of 400,000 kilolitres. This investment strengthened its position in the texture paints market by enhancing production capabilities.

Global Texture Paints Market Report Scope

Texture paint is a high-consistency paint blended with materials such as sand, gypsum, or marble dust to produce a three-dimensional, rough-patterned, or decorative finish on surfaces. It is mainly used to enhance the visual appeal of feature walls and to conceal imperfections, including cracks or uneven surfaces.

The Texture Paints market is segmented into product type, substrate type, end-user industry, and geography. By product type, the market is segmented into sand texture, smooth texture, popcorn and knock-down, orange peel, roll-on texture, and other product types. By substrate type, the market is segmented into interior walls, exterior walls, ceilings, and wood and metal surfaces. By end-user industry, the market is segmented into residential, commercial, and industrial. The report also covers the market size and forecasts for texture paints in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Sand Texture |

| Smooth Texture |

| Popcorn and Knock-down |

| Orange Peel |

| Roll-on Texture |

| Other Product Types |

| Interior Walls |

| Exterior Walls |

| Ceilings |

| Wood and Metal Surfaces |

| Residential |

| Commercial |

| Industrial |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Sand Texture | |

| Smooth Texture | ||

| Popcorn and Knock-down | ||

| Orange Peel | ||

| Roll-on Texture | ||

| Other Product Types | ||

| By Substrate Type | Interior Walls | |

| Exterior Walls | ||

| Ceilings | ||

| Wood and Metal Surfaces | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the texture paints market?

The texture paints market size stands at USD 15.48 billion in 2026 and is expected to reach USD 19.88 billion by 2031.

Which product type is growing fastest through 2031?

Roll-on texture paints are projected to record a 5.08% CAGR through 2031.

Why are micro-ceramic additives important?

They lower the wall thermal conductivity by up to 25%, helping buildings cut cooling loads.

Which region holds the largest share in 2025?

Asia-Pacific captured 38.89% of revenue in 2025 and remains the leading region.

Page last updated on: