Paper Dyes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

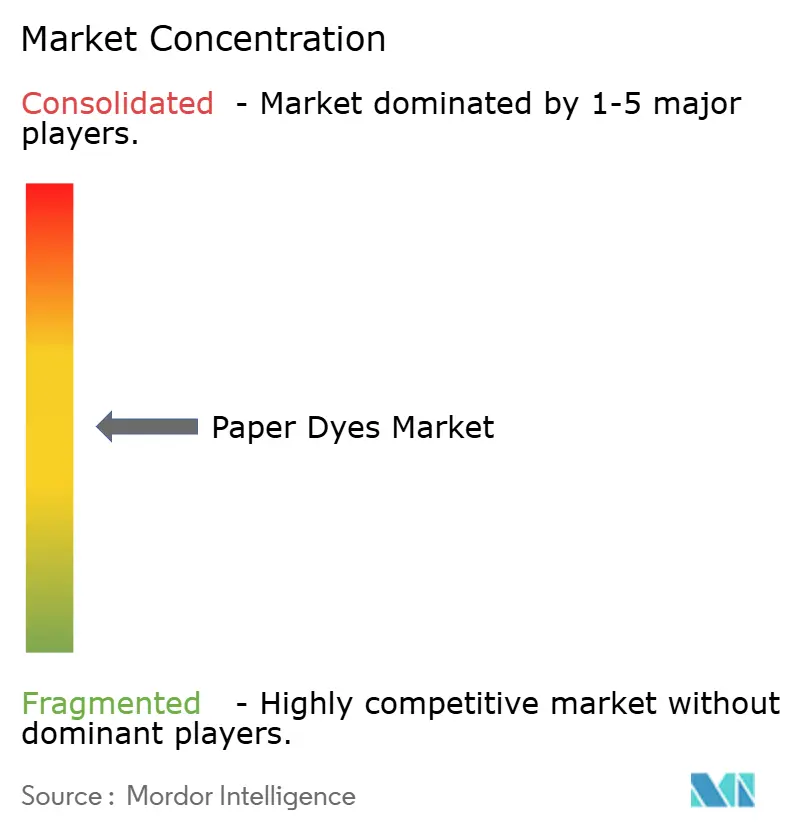

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Dyes Market Analysis by Mordor Intelligence

The Paper Dyes Market size was valued at USD 1.21 billion in 2025 and estimated to grow from USD 1.26 billion in 2026 to reach USD 1.54 billion by 2031, at a CAGR of 4.13% during the forecast period (2026-2031). This steady trajectory reflects the market’s resilience in digital-document substitution, supported by the structural migration from plastic to paper-based packaging and rising demand for vivid, brand-consistent graphics in e-commerce shipments. Liquid formulations that integrate seamlessly with modern inkjet lines are helping converters reduce downtime, while capacity additions by major dye makers keep raw material supply balanced. Regulatory tailwinds that restrict single-use plastics and brand owners’ preference for renewable substrates underpin an expansionary outlook even as graphic-paper volumes contract. Investments in lignin-compatible and nano-encapsulated chemistries further differentiate suppliers, positioning them to capture premium orders in food-contact and high-speed digital applications.

Key Report Takeaways

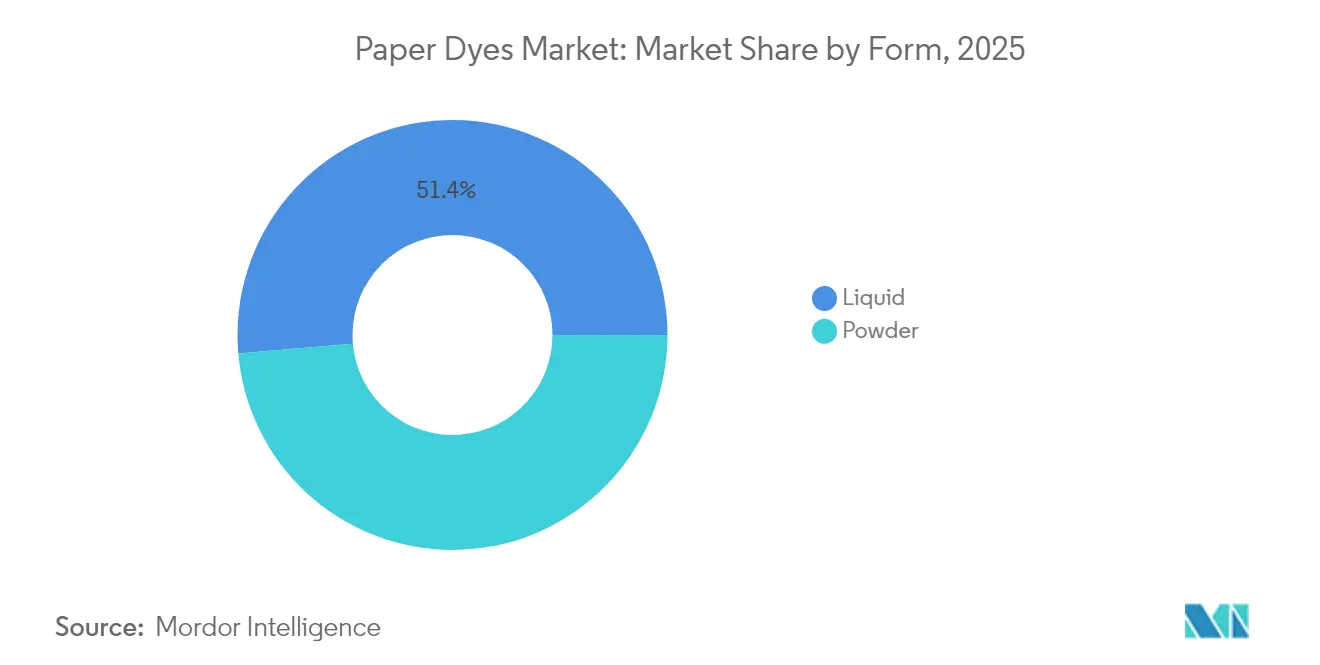

- By form, liquid products led with 51.38% of paper dyes market share in 2025 and are advancing at a 6.31% CAGR through 2031.

- By type, direct dyes captured 28.02% revenue share in 2025, while reactive dyes are projected to post the fastest 5.78% CAGR to 2031.

- By origin, synthetic grades controlled 69.64% share of the paper dyes market size in 2025; organic alternatives are expanding at a 6.96% CAGR.

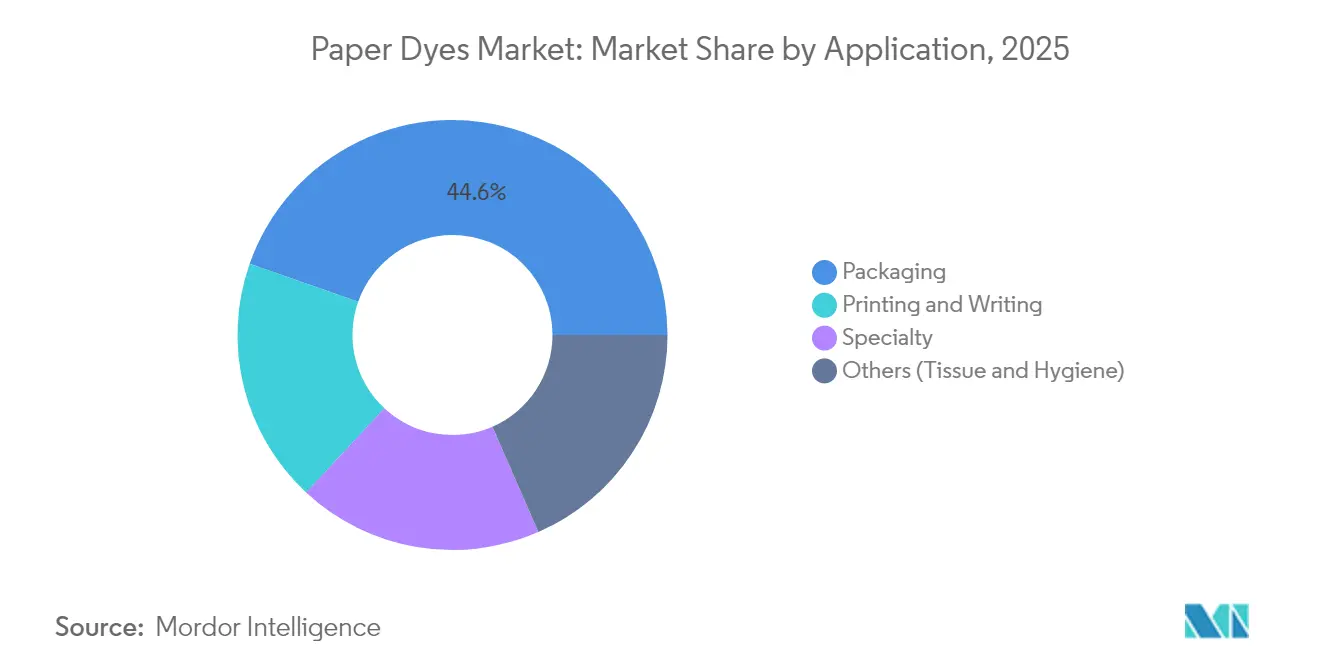

- By application, packaging accounted for 44.62% of 2025 revenue and is growing at a 6.62% CAGR to 2031.

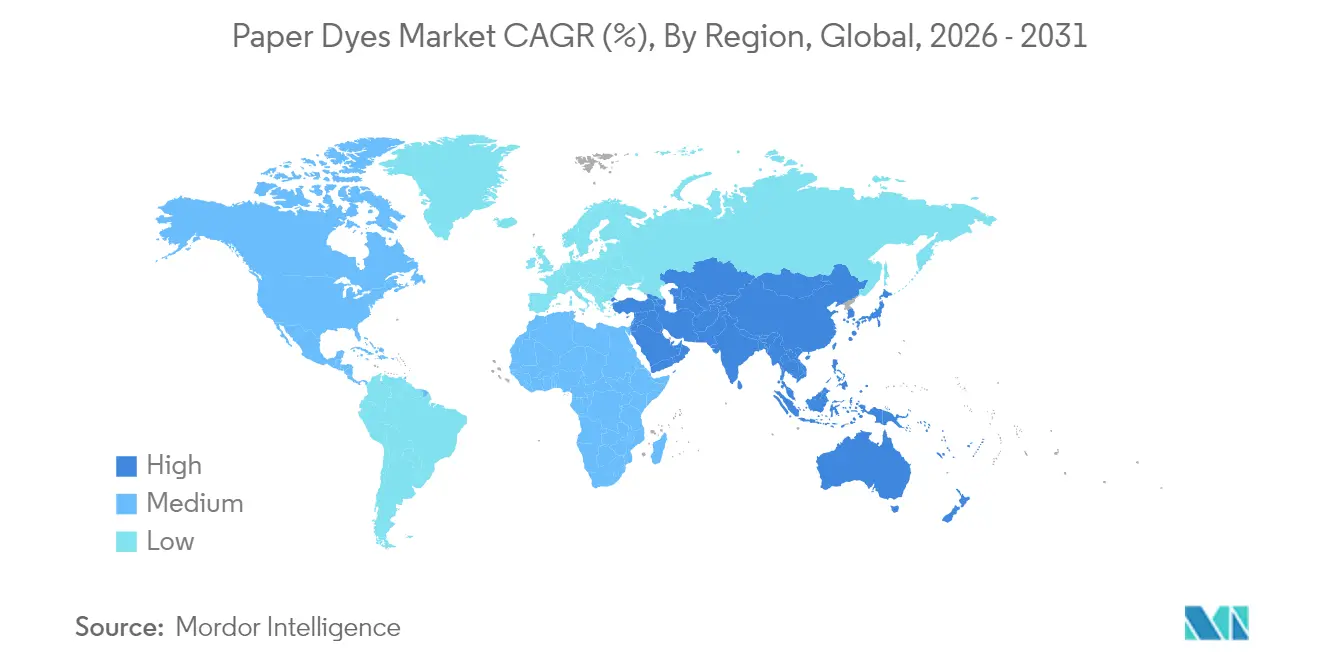

- By region, Asia-Pacific dominated with 44.25% of 2025 revenue, outpacing all regions at a 5.56% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paper Dyes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from plastic to paper-based packaging | +1.2% | Global, with strongest impact in North America & EU | Medium term (2-4 years) |

| E-commerce–fuelled boom in corrugated & mailer demand | +0.9% | Global, led by APAC and North America | Short term (≤ 2 years) |

| Capacity expansions by major dye manufacturers | +0.6% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Breakthroughs in bio-based lignin-compatible dyes | +0.4% | EU and North America, expanding to APAC | Long term (≥ 4 years) |

| Nano-encapsulated dyes enabling digital inkjet printing on paper | +0.3% | Global, technology-driven adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift from Plastic to Paper-Based Packaging

Retail brands continue to replace petroleum-based substrates with recyclable, fiber-based formats to comply with single-use plastic bans and to meet consumer preference for paper. Nestlé, Unilever, and other multinationals now eliminate up to 97% of plastic from certain SKUs, accelerating orders for high-performance dyes that remain stable through multiple recycling loops[1]Two Sides North America, “Why Well-Designed Paper Packaging Is Replacing Plastic,” twosidesna.org. Regulatory certainty created by the European Union’s Single-Use Plastics Directive supports capital investment in converters that require food-contact-compliant, migration-safe colorants. Consumer willingness to pay premiums for sustainable packaging has held steady, allowing dye producers to defend pricing for novel, colorfast formulations that tolerate alkaline de-inking and oxidative bleaching in recovered-fiber systems.

E-commerce–Fueled Boom in Corrugated & Mailer Demand

Over 80% of online orders ship in corrugated formats, and parcel volumes continue to rise—particularly in Asia-Pacific and North America—creating concentrated demand for vivid graphics that elevate the unboxing experience. Fulfillment centers require rapid-turn inkjet lines that run on liquid dyes engineered for low-maintenance printheads, enabling same-day personalization at scale. Building leases for packaging plants rose 45% above the 20-year average in 2024, a clear signal of structural capacity expansion that will sustain the paper dyes market over the forecast horizon.

Capacity Expansions by Major Dye Manufacturers

Archroma’s USD 750,000 upgrade in South Carolina targets paper-packaging clients with faster lead times and localized technical support. BASF commissioned a 260,000-metric-ton hexamethylenediamine complex in France that feeds intermediates for specialty colorants. Solenis inaugurated a USD 193 million polyvinylamine plant in Virginia, enabling captive supply of key wet-strength resins that synergize with dyes for label and board grades[2]Water Tech Online, “Solenis Opens USD 193 Million Production Site in Virginia,” watertechonline.com. These investments anchor regional supply chains, shorten transit times, and open capacity for higher-margin, bio-based innovations.

Breakthroughs in Bio-Based Lignin-Compatible Dyes

European consortia are scaling lignin-derived colorants that match the hue strength of synthetic analogues while lowering cradle-to-gate CO2 footprints. Researchers at the University of Borås improved lignin modification pathways, unlocking pH-stable pigments suitable for alkaline papermaking lines. Horizon Europe’s HORIZON-JU-CBE-2024-IA-05 project co-produces lignin aromatics, signaling institutional confidence in commercial viability[3]Celignis, “HORIZON-JU-CBE-2024-IA-05: Selective and Sustainable Co-Production of Lignin Derived Aromatics,” celignis.com. Laboratory trials demonstrate that lignin nanoparticles adsorb and re-release dyes 14 times more efficiently than untreated lignin, a breakthrough that could simplify effluent treatment while valorizing biomass waste.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Paperless office & digital documents adoption | -0.8% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Toxic amines & rising REACH compliance costs | -0.5% | EU primary, expanding globally | Medium term (2-4 years) |

| Volatility in wood-pulp availability & pricing | -0.3% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Paperless Office & Digital Documents Adoption

Graphic-paper demand contracted sharply after corporate and educational users accelerated digital workflows. The Confederation of European Paper Industries recorded a 13% fall in paper and board production in 2023, with graphic grades alone down 28%. Remote-work protocols that cut printing volumes by 50-70% remain in force, while e-signature platforms reduce the need for hard copies. Although packaging dyes offset some losses, graphic-paper contraction limits overall tonnage growth, particularly in mature regions.

Toxic Amines & Rising REACH Compliance Costs

The 2025 REACH revision imposes essential-use criteria for high-risk chemistries, including broader PFAS restrictions and enhanced data requirements for endocrine disruptors. Annual compliance outlays for polycyclic aromatic hydrocarbon limits alone approach EUR 3.4 million, disproportionately burdening small dye producers. Ten-year registration validity and new polymer filing mandates compel companies to scale or exit, hastening consolidation and channeling R&D toward inherently safer molecules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Dominance Drives Digital Innovation

Liquid offerings held 51.38% of 2025 revenue and are projected to expand at a 6.31% CAGR, reinforcing their pivotal role in high-speed inkjet lines that power versioned e-commerce packaging. Powder grades, although easier to transport in bulk, must contend with dust-exposure rules and slower dispersion times. Nano-encapsulated liquid systems now enable print-head duty cycles exceeding 1,000 hours, minimizing maintenance shutdowns and improving OEE for converters. Stable viscosity across temperature swings supports automated dosing, aligning with just-in-time production targets.

Ongoing advances in mini-emulsion and microfluidic encapsulation increase shelf life, preserving hue intensity for over 12 months when stored at 25 °C, compared with six months for standard formulations. As a result, converters see reduced write-offs from expired stocks. Powder suppliers respond with compaction and dust-suppressant technologies but still trail liquid rivals in digitally enabled plants.

By Type: Direct Dyes Lead Despite Reactive Innovation

Direct dyes, favored for cost-efficient exhaust processes, commanded 28.02% of 2025 sales, maintaining dominance in high-volume linerboard mills. Yet the reactive segment is advancing at a 5.78% CAGR on the strength of superior wash-fastness, an attribute prized by premium folding-carton users who require graphics to survive recycling. According to fiber-specific trials, cotton-fiber-rich specialty grades register dye uptake of 41.45% with reactivatives versus 35.68% for other chemistries.

Suppliers reduce typical reactive-bath temperatures from 90 °C to 60 °C without sacrificing fixation, lowering energy loads, and broadening adoption in mills constrained by decarbonization targets. Direct dyes remain a staple because they attach readily under neutral pH, but their market share is gradually ceded to higher-value chemistries that align with circular-economy mandates.

By Origin: Synthetic Dominance Faces Organic Challenge

Synthetic molecules still generated 69.64% of 2025 revenue, a testament to their broad chromatic range and competitive cost profile. Petroleum-derived intermediates benefit from global, integrated supply chains that stabilize pricing. However, organic entrants grow 6.96% annually as carbon-reduction commitments cascade across the FMCG and retail sectors. Pine-cone extracts rich in tannins now yield stable beige and brown shades suitable for tissue and kraft linings, offering biogenic carbon credits to converters.

Early-stage hybrid routes that blend lignin fractions with synthetic anchors deliver the color strength of azo dyes while cutting fossil feedstock intensity by 30%, aligning with scope-3 reduction targets of major packaging buyers. As supply scales, cost parity is expected within the decade, narrowing the premium gap currently limiting penetration.

By Application: Packaging Segment Drives Dual Leadership

Packaging captured 44.62% of 2025 revenue and is projected to post the fastest 6.62% CAGR, underscoring its central role in absorbing production from mills that retool away from declining graphic papers. Brand owners require shelf-ready displays and corrugated mailers with photorealistic imagery, a specification that favors high-gamut liquid systems. Graphic-paper volumes remain significant but continue their secular downtrend, while specialty niches such as moisture-indicator labels secure higher unit values but limited tonnage.

Tissue and hygiene papers in the “others” bucket gain from demographic expansion in South-East Asia and Africa, yet CAGR remains modest relative to the e-commerce packaging boom. Functional dyes that confer antimicrobial or odor-control benefits are gaining traction in tissue, creating incremental, innovation-driven demand within this segment.

Geography Analysis

Asia-Pacific retained leadership with 44.25% of 2025 revenue and is forecast to rise at a 5.56% CAGR to 2031, reflecting its status as a global manufacturing nucleus and fast-expanding consumer market. China’s chemical champions—Hengli, Wanhua, and peers—channel government incentives into fine-chemical projects that lift regional self-sufficiency. Vietnam, hosting 7,500 textile enterprises employing 4.3 million workers, boosts regional consumption of corrugated and specialty papers, translating into higher local dye usage.

North America ranks second by value, propelled by e-commerce fulfillment growth and aggressive plastic-reduction pledges from food and beverage multinationals. Archroma’s South Carolina site and Solenis’s Virginia complex provide localized supply, while regulatory clarity on PFAS pushes converters to adopt compliant, water-based systems. Although graphic-paper contraction tempers total tonnage, premium-grade orders that favor environmentally optimized dyes support above-inflation price realization.

Europe grapples with stringent REACH amendments and pulp-price volatility—Northern Bleached Softwood Kraft touched EUR 1,380 / t in April 2024—pressuring operating margins. Yet the bloc’s leadership in circular-economy regulation and R&D funding for lignin-derived colorants positions local suppliers at the forefront of high-value, eco-optimized offerings. Converters invest in closed-loop water treatment to meet discharge permits, raising demand for low-salt, high-exhaustion dyes that align with zero-liquid-discharge ambitions.

Regulatory Landscape

Regulatory requirements for paper dyes are tightening around chemical safety, food-contact migration, and discharge controls, which is influencing product selection across regions. In Europe, REACH (EC No 1907/2006) anchors registration and SVHC management, and the 2025 REACH revision cited in the report increases data and essential-use scrutiny for higher-risk chemistries, raising compliance costs for smaller dye producers. A new EU measure in 2026 adds another compliance layer for paper formulations used in consumer products with prolonged skin contact by restricting stilbene-based fluorescent whitening agents, pushing suppliers toward reformulation and requalification of compliant colorant packages for EU-bound grades.

Beyond legal requirements, paper mills and their chemical suppliers increasingly rely on standardized, audit-ready compliance tools to manage restricted substances and downstream declarations. The European Pulp and Paper Chemicals Group (EPCG) supports supply-chain transparency through its Harmonized Questionnaire and PIDSL, which sit alongside safety data sheets in procurement and qualification workflows. In North America, food-contact paper applications reference US FDA frameworks (including 21 CFR food-contact paper provisions), while environmental guidance such as the World Bank EHS Guidelines for Pulp and Paper Mills reinforces preference for water-based inks and dyes, alongside wastewater and occupational exposure controls.

Value Chain Analysis

The paper dyes value chain starts with upstream petrochemical and bio-based feedstocks and intermediates that feed into key dye chemistries (including direct, reactive, acidic, and basic systems). These are followed by specialized dye manufacturers that formulate powder and increasingly liquid products for wet-end and surface applications. Qualification and shade development are typically supported by application labs and pilot-scale testing, then routed through direct sales and chemical distributors to paper and paperboard mills, converters, and printing operations. Industry bodies such as ETAD and EPCG influence supplier behavior through safety and transparency practices, with EPCG tools (Harmonized Questionnaire and PIDSL) increasingly embedded in procurement and compliance documentation exchange.

Downstream, mills integrate dyes with retention aids, wet-strength resins, and functional additives to meet performance targets across packaging, specialty, tissue, and remaining graphic grades. Much of the value is created at the formulation and mill-application stages, where lot-to-lot consistency and shade matching are critical, and where digital color management and automated dosing reduce variability in high-speed lines. Bottlenecks tend to center on restricted-substance screening, documentation completeness for export markets, and process robustness under recycling and de-inking conditions. These constraints raise the importance of technical service, validated formulations, and reliable distribution networks for fast replenishment.

Competitive Landscape

The paper dyes market remains moderately fragmented. Archroma fortified its position by acquiring Huntsman Textile Effects, gaining technology synergies and a broader customer base in textile and paper circuits. European incumbents have consolidated to counter volume pressure from Asian suppliers, while mid-tier specialists carve niches in food-grade and security-print formulations.

Technology is a key differentiator: firms that commercialize nano-encapsulated and lignin-based systems win contracts with brand owners seeking circular credentials. Investments in regional technical-service labs help deepen mill relationships, reducing churn and enabling co-development of customized shades. Start-ups leverage computational-chemistry platforms to shorten development cycles and to model hue stability under alkaline recycling conditions, giving them latitude to compete despite limited scale.

Paper Dyes Industry Leaders

Archroma

BASF

Kemira Oyj

Atul Ltd.

DyStar Singapore Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity sits at the intersection of packaging conversion growth and tighter compliance requirements, where mills and converters need migration-safe, low-impurity colorants that retain fastness through recycled-fiber loops. Regulatory pressure and customer audits are pushing demand for traceable, standardized chemical declarations, benefiting suppliers that can support EPCG-style documentation, food-contact pathways, and mill qualification protocols alongside strong technical service. The report context also points to rising adoption of liquid systems for high-speed inkjet and personalization, which creates room for dye packages engineered for stable viscosity, low maintenance, and compatibility with modern printheads.

Investment activity in adjacent pulp and paper chemical infrastructure supports localized supply and faster technical response in core paper hubs, which can improve availability of compatible chemistries and enable bundled offerings for mills. In April 2026, Solenis broke ground on a 60,000-tonne-per-year production facility in Beihai, Guangxi, China, focused on functional and process chemicals used in pulp and paper operations, reinforcing regional supply chains that tie closely to coloration performance in packaging and board. In parallel, the report context on bio-based and lower-salt approaches to cellulosic coloration, including published 2025 research on salt-free dyeing routes, aligns with wastewater constraints and brand sustainability requirements without relying on traditional high-salt dye systems.

Recent Industry Developments

- June 2026: Vipul Organics announced an exclusive distribution partnership with Omya Group to supply SunTone and SunCoat pigment dispersions and powders across multiple European markets (excluding Switzerland and Poland). The move strengthens its route-to-market and local service coverage in Europe, supporting faster penetration into packaging and specialty paper coloration programs where converters increasingly require consistent dispersion quality.

- January 2026: Archroma installed three VCML pilot coaters from RK Print Coat Instruments at its Centers of Innovation in Mumbai (India), Prat (Spain), and Charlotte (North Carolina). The added pilot-scale capability accelerates development and qualification of sustainable materials for paper and packaging applications, tightening collaboration loops with mills and brand owners that need rapid proof-of-performance.

- October 2024: Archroma announced a EUR 20 million expansion plan at its El Prat de Llobregat facility to add 32,000 tonnes of annual capacity over three years. The capacity and logistics upgrade supports improved lead times and supply reliability for paper and packaging customers, while also providing a platform for scaling newer compliant colorant and sustainability-oriented product lines.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers dyes used to color paper and paperboard during manufacturing, including wet-end addition and surface sizing, measured as revenue from dye products supplied to paper producers.

Scope exclusions: Pigments, optical brightening agents, and dyes sold mainly for non-paper substrates are excluded from this sizing.

Segmentation Overview

- By Form

- Powder

- Liquid

- By Type

- Acidic

- Basic

- Direct

- By Origin

- Organic

- Synthetic

- By Application

- Printing and Writing

- Packaging

- Specialty

- Others (Tissue and Hygiene)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building the paper and paperboard demand context, then translating it into a realistic dye consumption pool. Public sources such as the UN Comtrade database, the World Bank, the US International Trade Commission data, and Eurostat were referenced to track trade flows and production signals, then link those to macro changes that affect paper output.

To keep assumptions grounded, we also reviewed technical references and standards bodies and public research, such as TAPPI resources, peer reviewed papers on paper coloring and retention, and regulator updates that influence dye selection and discharge norms. Company annual reports, investor presentations, and reputable press releases helped validate capacity changes and product focus. We used a paid subscription covering company financials and a patent database selectively to cross-check supplier direction. These sources are illustrative and not exhaustive, since many other public documents and datasets were also used for clarification and validation.

Primary Interviews and Surveys

Primary conversations were used to pressure-test how dye demand changes with paper grade mixes, shade requirements, and mill operating rates, and then to align pricing logic with real contract behavior. We spoke with stakeholders across dye suppliers, distributors, and paper manufacturers across APAC, EMEA, and the Americas, which helped fill gaps where public data does not clearly separate dyes from adjacent additives.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 17% | APAC: 44% |

| Mid tier: 46% | Functional/Unit leaders: 41% | EMEA: 33% |

| Smaller Players: 17% | Managers: 42% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where paper and paperboard output and trade are reconstructed by region, then converted into a dye demand pool using typical dosage ranges and the share of dyed grades. Once that spine is set, we corroborate totals with selective bottom-up checks, such as supplier revenue splits, channel feedback, and sampled average selling price by formulation multiplied by estimated tonnage.

Key inputs used in the model include paper and paperboard production volumes, packaging versus printing and writing mix shifts, import and export movements for paper products and for dyes, mill operating rates, and dye intensity factors tied to shade depth and grade requirements. Since prices can move with feedstock trends and contract resets, pricing was treated as a moving input rather than a fixed uplift, and currency conversions were aligned to the same time window as the base year.

For forecasting, scenario analysis was applied on top of trend models so we could reflect different paths for paper demand, packaging growth, and environmental compliance costs that affect product substitution. Where primary feedback showed thin visibility, gaps were handled with conservative ranges, then narrowed through follow-up checks until assumptions stayed consistent across regions and grades.

Data Validation & Update Cycle

Validation is done through several passes where outputs are compared against independent signals like paper production changes, trade direction, and supplier commentary on demand. When a region shows an unexpected jump or drop, we re-check unit conversions, pricing timing, and the underlying paper grade mix before it is cleared.

Before sign-off, the model and assumptions are reviewed by another analyst, and unusual variances trigger re-contact with selected interviewees for confirmation. The report is refreshed annually, and interim updates are made when material events occur, such as major capacity additions, regulatory shifts, or sharp feedstock moves. Right before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Paper Dyes Market Size Versus Other Published Estimates

Published market sizes can vary even when the topic sounds identical, because the definition of what is included, the price level used, and the time period used for currency and inflation are not always aligned. The table helps show how those practical choices create a visible spread in the stated numbers.

The table points to a key split between studies that stay within dyes used in paper and paperboard making versus those that may fold in adjacent colorants or use a different base year, and then scale forward. In Mordor Intelligence's model, pigments and optical brightening agents are excluded, and the value is tracked at end-manufacturer transfer pricing, which can pull the total away from estimates that use broader colorant baskets or different pricing bases.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.26 B (2026) | |

| Industry Publisher A | USD 1.27 B (2025) | Uses a different base year and may apply a straight CAGR bridge without fully re-anchoring to paper output and dyed-grade share by region, which can shift the starting point and price timing. |

| Global Publisher B | USD 1.20 B (2025) | Lower starting value is consistent with a slower growth curve and a longer forecast window, and it may reflect more conservative adoption and pricing assumptions across paper applications, especially when grade mix changes are not updated frequently. |

Taken together, the differences are mostly explained by scope boundaries, base-year alignment, and how pricing and demand drivers are refreshed. Our approach keeps the total traceable to paper production signals, dyed-grade participation, and realistic pricing steps, so the number can be reproduced and challenged with clear inputs rather than hidden uplifts.

Key Questions Answered in the Report

What is the current Paper Dyes Market size?

The paper dyes market stands at USD 1.26 billion in 2026 and is projected to reach USD 1.54 billion by 2031.

Which segment leads the paper dyes market by application?

Packaging dominates with 44.62% revenue share in 2025 and is expanding at a 6.62% CAGR through 2031.

Why are liquid dyes gaining traction in papermaking?

Liquid formulations offer dust-free handling, compatibility with high-speed digital printers, and stable viscosity, enabling converters to reduce downtime and waste.

Which region shows the fastest growth in the paper dyes market?

Asia-Pacific leads with a 5.56% CAGR, driven by its manufacturing base, rising e-commerce volumes, and supportive government policies.

Page last updated on: