Rust Remover Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

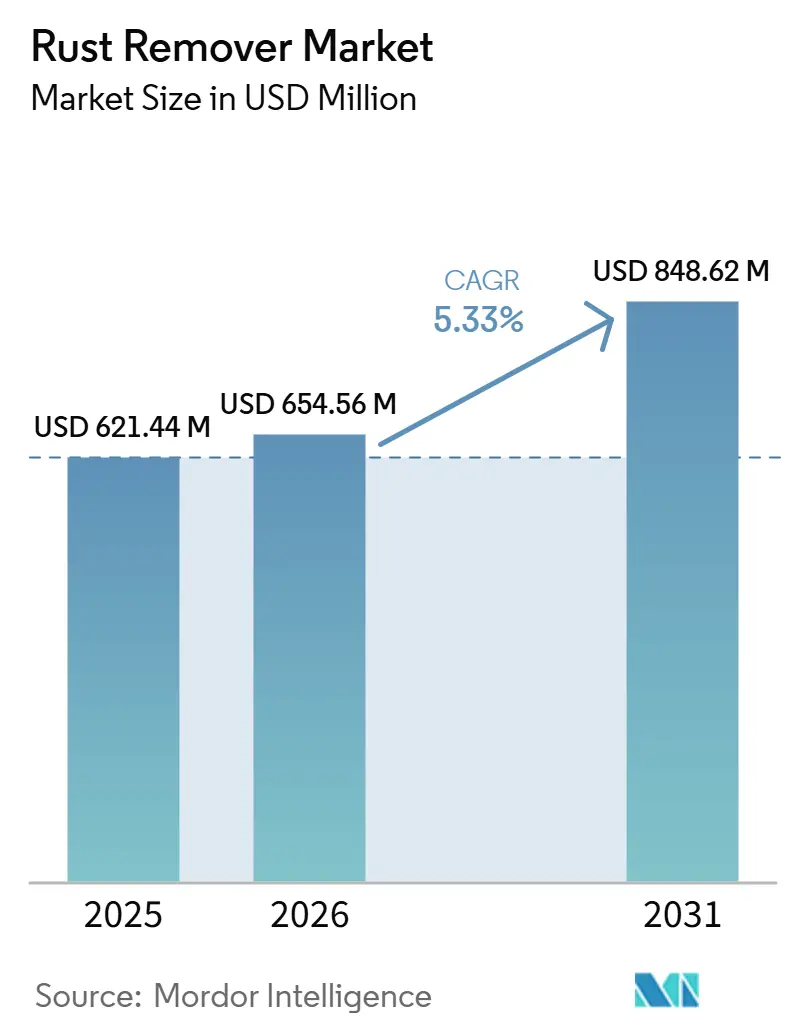

| Market Size (2026) | USD 654.56 Million |

| Market Size (2031) | USD 848.62 Million |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rust Remover Market Analysis by Mordor Intelligence

The Rust Remover Market size is expected to increase from USD 621.44 million in 2025 to USD 654.56 million in 2026 and reach USD 848.62 million by 2031, growing at a CAGR of 5.33% over 2026-2031. Surging maintenance outlays for bridges, industrial machinery, and aging vehicles are intersecting with regulatory curbs on volatile organic compounds, prompting a measurable shift from mineral-acid blends to bio-based and chelate chemistries. Formulators are racing to certify products under USDA BioPreferred and NSF Non-food Compounds while engineering flash-rust inhibition, primer compatibility, and low-reactivity propellants into the same bottle. Regional momentum tilts toward Asia-Pacific, where stimulus-backed infrastructure builds in India, Vietnam, and China, converging with relentless manufacturing expansion to keep demand for surface-preparation chemicals on an upswing. Meanwhile, North American and European buyers weigh total cost of ownership, access safety, labor, disposal, and lifecycle emissions more heavily than purchase price, rewarding suppliers that can validate durability and VOC performance with third-party lab data and transparent ingredient disclosures.

Key Report Takeaways

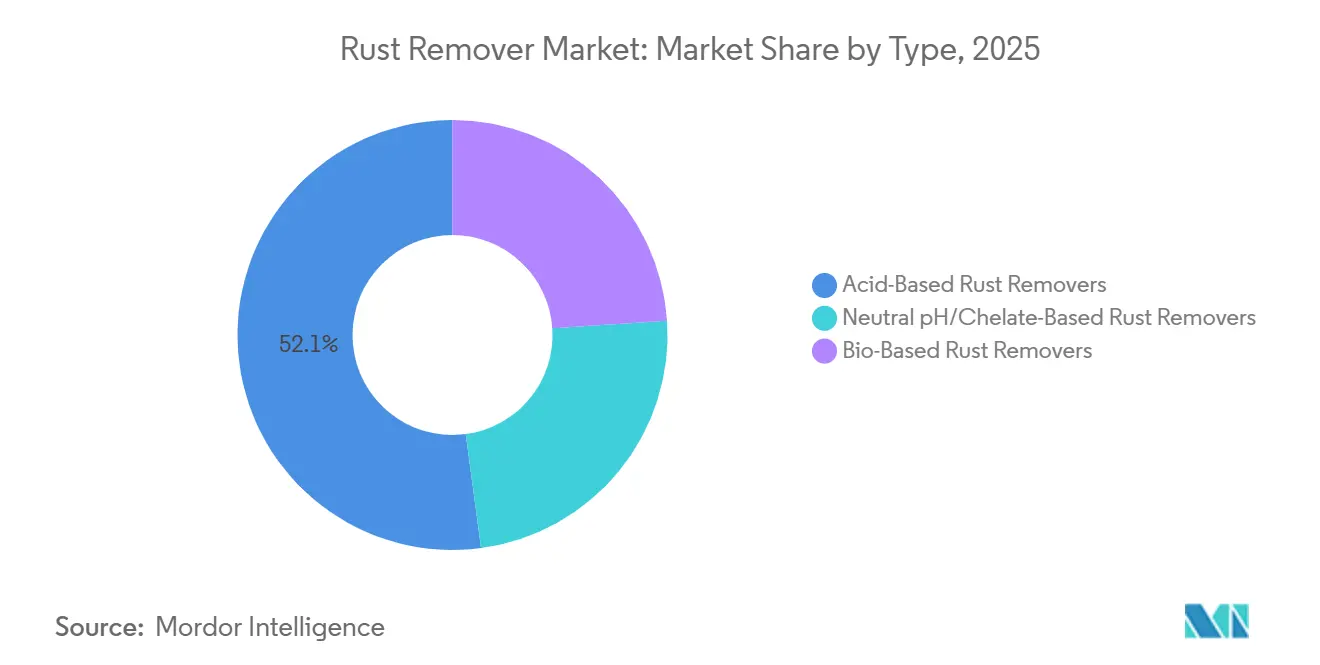

- By type, acid-based formulations captured 52.12% of 2025 revenue, while bio-based products are advancing at a 5.81% CAGR between 2026 and 2031.

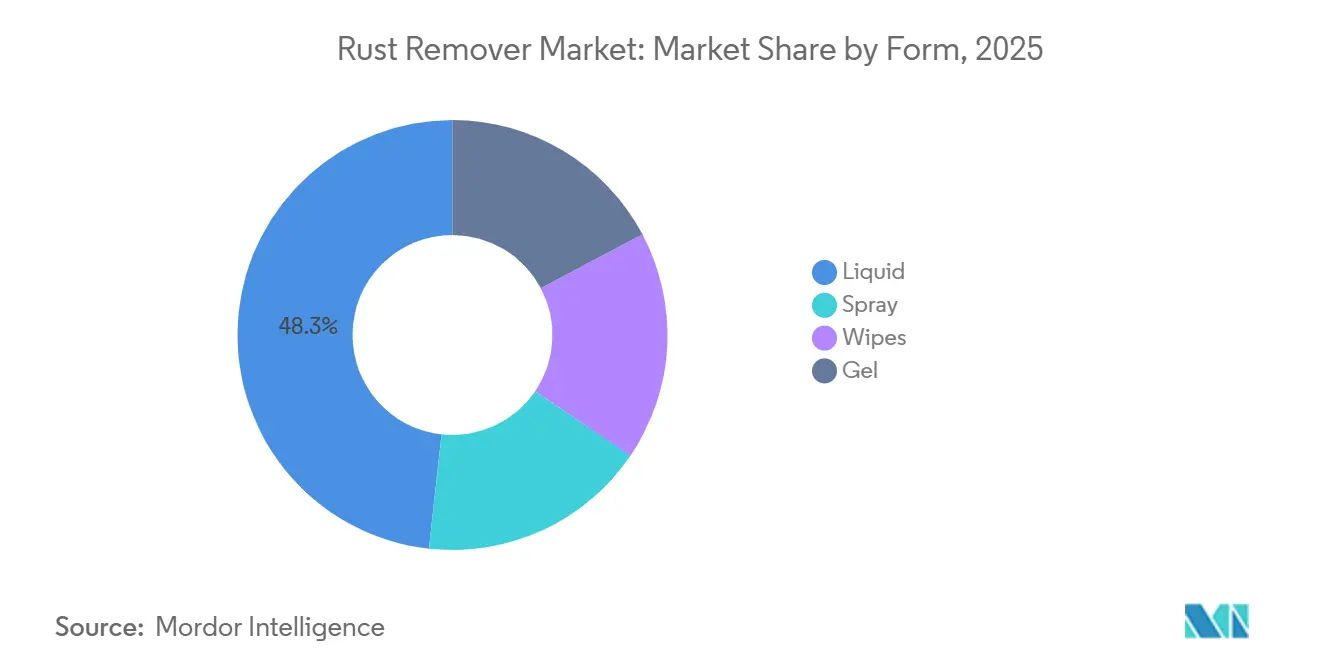

- By form, liquids accounted for 48.26% of the 2025 value; sprays are the fastest-growing format at 5.63% CAGR between 2026 and 2031.

- By end-user industry, industrial machinery led with 30.22% of 2025 demand, whereas the household/consumer segment is growing the quickest at 5.91% CAGR.

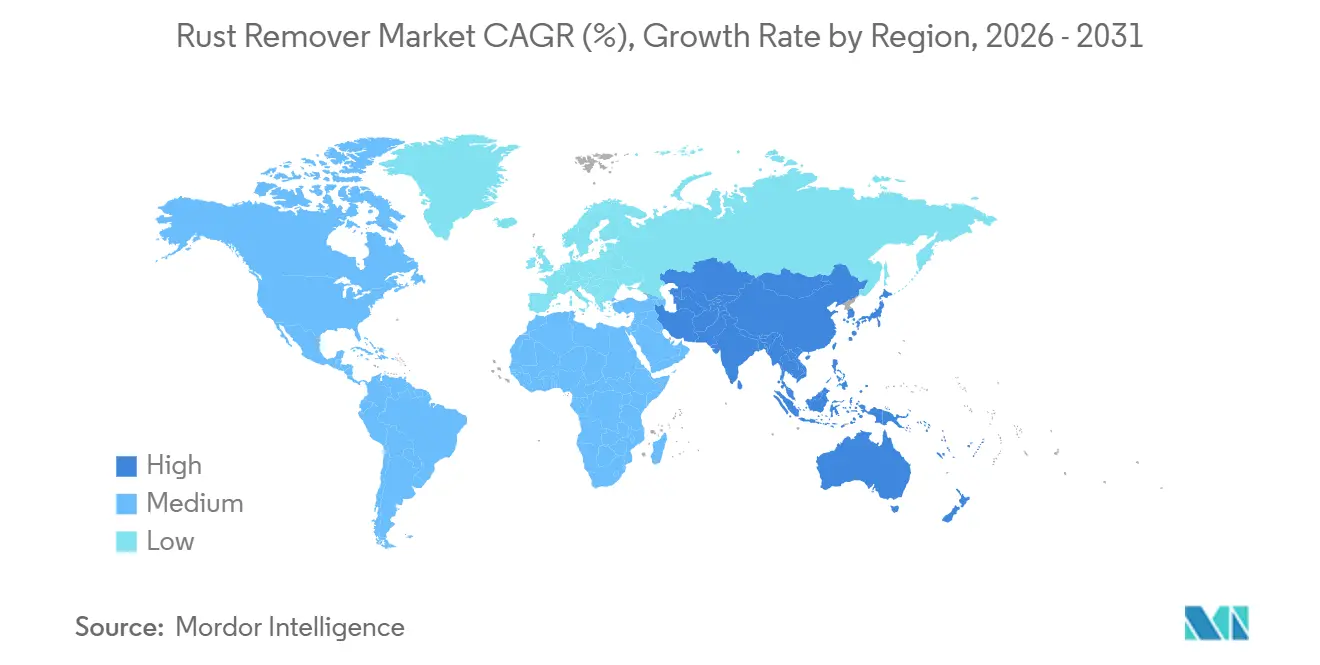

- By geography, Asia-Pacific dominated with 45.12% of 2025 sales and is poised for a 6.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rust Remover Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of manufacturing and infrastructure rehabilitation in emerging economies | +0.80% | Asia-Pacific (India, Vietnam, Indonesia), Latin America (Mexico, Brazil) | Medium term (2-4 years) |

| Regulatory push toward low-VOC and bio-based chemistries | +0.90% | Global, with early enforcement in North America and the EU | Short term (≤ 2 years) |

| Refurbishment of decommissioned offshore oil and gas platforms | +0.50% | North Sea, Gulf of Mexico, Southeast Asia offshore fields | Long term (≥ 4 years) |

| Pre-treatment demand for green-hydrogen electrolyzer components | +0.40% | EU, North America, select Asia-Pacific hubs (Japan, South Korea) | Long term (≥ 4 years) |

| Robotic and laser in-line rust-removal adoption in smart factories | +0.60% | North America, the EU, China, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Manufacturing and Infrastructure Rehabilitation in Emerging Economies

Industrial expansions in India, Vietnam, Indonesia, and Mexico are broadening the market for preventive surface treatments. In India, highway, metro, and port projects mandate corrosion protection for steel rebar and girders. This creates a consistent demand for liquid concentrates compatible with mobile spray rigs at job sites. Vietnam's electronics hubs deploy polyurea barriers to combat salt-laden humidity. However, they still require chemical rust removal during scheduled shutdowns. This is crucial, considering the region faces significant corrosion-related losses impacting its economy. In Mexico, the trend of near-shoring boosts the demand for tooling and mold maintenance. Meanwhile, in Brazil, tax incentives for domestically produced farming equipment ensure repair shops are well-stocked with gel products. These gels are particularly advantageous as they adhere to large castings without runoff. Together, these trends are strengthening the rust removers market, ensuring volume growth even amidst softening commodity prices.

Regulatory Push Toward Low-VOC and Bio-Based Chemistries

In January 2025, the United States Environmental Protection Agency introduced a new aerosol-coatings rule. This rule limits the product-weighted reactivity for rust converters and requires any volatile organic compound present above a certain threshold to be disclosed electronically. If a solvent is not listed, it automatically incurs a significant penalty, making many traditional hydrocarbon carriers impractical. On the other hand, citric-acid systems, derived from corn or cassava sugar, can achieve similar mill-scale removal. These systems produce minimal fumes and, when combined with xanthan gum, create drip-resistant gels suitable for a single vertical coat application. Meanwhile, tightening regulations under the European Union's Registration, Evaluation, Authorization, and Restriction of Chemicals and China's Ministry of Ecology and Environment standards further push global suppliers. They are increasingly moving towards unified formula portfolios that can meet the demands of various jurisdictions. This shift is reshaping the competitive landscape: now, having robust analytical reporting, meticulous volatile organic compound tracking, and access to biobased feedstocks are just as vital as pricing per liter.

Refurbishment of Decommissioned Offshore Oil and Gas Platforms

In the coming years, numerous steel platforms located in the North Sea and Gulf of Mexico are expected to be either removed or repurposed. Specifications require achieving a high level of surface cleanliness prior to the cutting and recycling process. In confined topside modules, where dust and noise regulations restrict abrasive blasting, heavy-duty liquid acid blends provide a suitable solution. While demand fluctuates based on contract awards, the aging fleet ensures sustained activity over an extended period. The offshore wind sector adds further complexity: during inspection cycles of monopiles and transition pieces, the use of neutral-pH chelating agents is essential. This method prevents hydrogen embrittlement in high-strength steels, supporting a premium sub-segment that remains unaffected by fluctuations in commodity prices.

Pre-Treatment Demand for Green-Hydrogen Electrolyzer Components

To meet the requirements of proton-exchange-membrane electrolyzers, which function under highly acidic conditions, Toho Titanium has started manufacturing porous sheets made of titanium. These sheets must be free of oxides before undergoing platinum electroplating. Additionally, global electrolyzer capacity is expected to experience significant growth over the coming years[1]International Energy Agency, “Global Electrolyzer Outlook 2024,” IEA.ORG. Despite the limited volume of chemical rust remover applied to titanium, buyers are willing to pay a premium price. This premium stems from the potential risks: downstream defects could threaten significant investments. The market is primarily dominated by neutral-pH, chelate-rich fluids that do not leave ionic residues. This creates a lucrative niche, allowing even mid-scale formulators, without petrochemical back-integration, to thrive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mechanical and coating-based substitutes | -0.70% | Global, with higher penetration in North America and the EU | Short term (≤ 2 years) |

| Geopolitical volatility in phosphoric and citric acid supply | -0.50% | Global, with acute exposure in regions dependent on China and Morocco imports | Medium term (2-4 years) |

| Rise of micro-abrasive and dry-ice cleaning technologies | -0.40% | North America, the EU, and select industrial hubs in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mechanical and Coating-Based Substitutes

Electric-vehicle battery enclosures are increasingly opting for powder coatings, which offer a zero-volatile organic compound application and generate nearly zero waste. This shift is enticing original equipment manufacturers to move away from traditional methods of sequential rust removal and repainting. A survey by AkzoNobel, encompassing manufacturers, revealed that a significant portion of electric vehicle producers now specify powder coatings, slightly outpacing the adoption rate seen in the broader automotive sector[2]Gustavo Carvalho, “EV Manufacturing Raising the Bar for Battery Protection,” Battery Technology Online, BATTERYTECHONLINE.COM. Plasmatreat's AntiCorr, a plasma-enhanced conversion coating, directly applies thin siloxane layers, completely sidestepping traditional chemical baths. With the growing adoption of galvanized steel and aluminum, the once-dominant inventory of bare ferrous surfaces central to the rust removers market has diminished, eroding the market's baseline volume.

Geopolitical Volatility in Phosphoric and Citric Acid Supply

China stands as a hub for citric acid production, while Morocco's phosphate rock takes the lead in supplying phosphoric acid. Factors like trade tensions, export limitations, or unexpected plant shutdowns can cause spot prices to rise significantly in a short period, impacting formulators without long-term contracts. Introducing alternatives like gluconic acid or ethylenediaminetetraacetic acid requires new efficacy trials and potentially fresh safety filings under the Toxic Substances Control Act or the Registration, Evaluation, Authorization, and Restriction of Chemicals framework, incurring both time and costs. While citric acid production through fermentation offers some buffer against petroleum price fluctuations, a concurrent rise in demand for food-grade citric acid can leave industrial buyers in a tight spot, scrambling for their share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bio-Based Formulations Gain as VOC Ceilings Tighten

Acid-Based Rust Removers maintained a 52.12% slice of 2025 revenue, while traditional methods anchor legacy maintenance manuals and facilitate heavy-scale removal, rising compliance costs tied to environmental regulations are steering buyers towards citric systems, proudly boasting a certification as fully biobased by the United States Department of Agriculture. Bio-based solutions are projected to expand at 5.81% CAGR between 2026 and 2031. Aerospace maintenance depots, wary of hydrogen embrittlement, are progressively boosting their share of the rust removers market. While still a niche, neutral-pH chelates are securing high-margin contracts in heritage preservation and electronics assembly, where the need for bare-metal precision compensates for their slower kinetics.

Over the forecast period, the market for chelate formulations in rust removers is projected to grow steadily, albeit from a modest base. While acid products continue to dominate heavy machinery refurbishment, the visible costs of additional personal protective equipment, fume extraction, and hazardous waste management are becoming evident in bid comparisons, tightening total cost of ownership gaps. Suppliers are now offering hybrid kits, combining acid pre-wash with chelate polish, to balance performance with regulatory comfort, easing the industry's shift away from a strong-acid-only approach.

By Form: Sprays Capture Convenience Premium in DIY Channels

Liquids products delivered 48.26% of the 2025 value. Backed by dip tanks and circulation systems in component rebuilding, the rust removers market for sprays is projected to witness significant growth during the forecast period, marking 5.63% CAGR between 2026 and 2031. As shelf-ready aerosol and trigger bottles take center stage in automotive aftermarket aisles, consumers are willing to pay a premium for the precision they offer. Whether it's for lug-nut threads, bicycle chains, or garden tools, the allure lies in their portability and straightforward application.

To meet volatile organic compound reactivity standards, manufacturers are shifting towards compressed air or nitrogen propellants. They're also incorporating flash inhibitors, which extend dwell time and reduce immediate re-oxidation. Gels are increasingly favored by shipyards and bridge contractors. Their thixotropic rheology minimizes runoff, reduces tarp preparation time, and decreases chemical waste. Wipes, enriched with chelate actives, effectively tackle light flash rust on stainless appliances and tools, making them a hit with homeowners who prefer a mess-free solution. By diversifying their product lines, brands can strategically place multiple stock-keeping units at each retailer, enhancing their market presence without overshadowing their flagship liquid products.

By End-User Industry: Household Segment Outpaces as DIY Culture Expands

Industrial Machinery and Equipment preserved its lead at 30.22% of 2025 demand. Predictive maintenance algorithms now schedule rust treatments during planned shutdowns. Scalable liquid concentrate systems circulate through computer numerical control coolant loops, effectively removing corrosion from iron chips before the next machining run. However, the rise of do-it-yourself enthusiasm, spurred by social media's how-to videos, has made waves in the industry, pulling household sales at 5.91% CAGR between 2026 and 2031. Big-box retailers prominently feature spray-on rust dissolvers for barbecue grills, lawn-mower decks, and bicycle frames at their end-caps, often pairing them with protective topcoats to boost sales.

As the global vehicle parc continues to expand, the automotive aftermarket revenue experiences a corresponding increase. Hobbyist restorers prefer gel products that adhere to vertical rocker panels without marring nearby paint. In marine settings, chloride-tolerant acids and inhibitors are essential to avert flash corrosion on stainless rails and aluminum hulls. Aerospace contractors, ensuring supply stability for aircraft lifecycles spanning several decades, opt for chelate fluids approved under military specifications. Thus, the rust removers industry caters to both high-volume consumer markets and specialized niches, necessitating tailored go-to-market strategies.

Geography Analysis

Asia-Pacific accounted for 45.12% of 2025 revenue and is on track for a 6.11% CAGR between 2026 and 2031. Chinese automotive production lines, which employ inline spray phosphates between welding and e-coating, drain significant volumes daily. Even a small shift towards bio-acids leads to an increase in volume. In India, contractors on the Bharatmala highway corridors, which use large amounts of reinforcing bar per stretch, specify rust treatments to align with the Ministry of Road Transport guidelines. Vietnam, dealing with substantial corrosion losses as a share of its economy, witnesses growing demand in its maritime sector for neutral-pH gels. These gels reduce diver time during hull maintenance. Meanwhile, foreign direct investment incentives from the Association of Southeast Asian Nations attract component suppliers. By adopting low-volatile organic compound liquids, these suppliers position themselves for European exports, advancing cross-regional formulation harmonization.

In North America, the Environmental Protection Agency's electronic-reporting mandate shifts market shares towards citric, gluconic, and other benign acids. Offshore decommissioning bids in the Gulf of Mexico now account for total lifecycle emissions, driving up chelate demands, even at a higher per-liter cost. Furthermore, a strong do-it-yourself culture in the United States sees social-media rust-hack videos translating into active weekend retail sales.

Europe, despite its maturity, remains focused on circular-economy metrics. A study from the Journal of Coatings Technology and Research pointed out that health, safety, and environmental access expenses dominate project spending. This trend nudges asset owners towards durable, low-maintenance coatings that reduce intervention frequency. Suppliers who offer rust removal alongside flash-inhibition gain a competitive edge, saving an extra scaffold cycle a significant advantage in European Union bidding.

While South America and the Middle-East and Africa command smaller market shares, they exhibit areas of rapid growth. In Brazil, soy harvesters face challenges with corrosive fertilizer dust. Meanwhile, in Saudi Arabia, desalination plants manage high-salinity stainless piping. Although political risks and currency fluctuations complicate forecasting, the emergence of localized blending plants offers a solution. These plants reduce import duties and lead times, granting nimble players incremental advantages.

Competitive Landscape

The Rust Remover market is moderately fragmented. Laser Photonics' CleanTech robotic cell operates efficiently without the need for consumables. Meanwhile, Plasmatreat's AntiCorr plasma technology applies nano-glass barriers directly onto electric vehicle battery housings, effectively replacing traditional wax baths. In response, chemical formulators are strategically positioning their liquids and gels as adaptable, flexible, and cost-effective solutions suitable for various geometries and on-site repairs. Certifications from the marine and aerospace sectors, such as those under the International Organization for Standardization or military detailed specifications, provide significant advantages; once suppliers achieve these qualifications, they can anticipate long-term reorder visibility.

Rust Remover Industry Leaders

WD-40

3M

Henkel AG & Co. KGaA

CRC Industries

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Japan's Environment Minister awarded AISIN and Kao Corporation for their eco-friendly rust remover. This innovation, which reduced CO₂ emissions by 73%, has revolutionized rust removal in the automotive sector. It is driving ongoing demand for sustainable solutions, cutting costs, and setting new global standards for eco-friendly practices.

- March 2024: ProXL, a part of Capella Solutions Group, introduced a revolutionary water-based rust remover for automotive repair. This eco-friendly solution removes corrosion without dismantling panels, reducing environmental impact and improving bodyshop efficiency. By reshaping rust removal practices, ProXL's innovation has driven demand for sustainable alternatives, challenged traditional methods, and transformed the competitive dynamics in the automotive repair market.

Global Rust Remover Market Report Scope

Rust removal is the process of eliminating iron oxide that forms when metal reacts with moisture and oxygen. It involves mechanical methods like sanding or scrubbing, and chemical treatments such as rust converters or acidic solutions that dissolve corrosion. Effective rust removal restores the metal’s surface, prevents further deterioration, and prepares it for protective coatings to enhance durability and longevity.

The Rust Removal Market is segmented by type, form, end-user industry, and geography. By type, the market is segmented into acid-based rust removers, neutral pH/chelate-based rust removers, and bio-based rust removers. By form, the market is segmented into liquid, gel, spray, and wipes. By end-user industry, the market is segmented into automotive, construction, marine, industrial machinery and equipment, household/consumer, aerospace, oil and gas, and other industries. The report also covers the market size and forecasts for the Rust Remover Market across 16 countries in major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Acid-Based Rust Removers |

| Neutral pH/Chelate-Based Rust Removers |

| Bio-Based Rust Removers |

| Liquid |

| Gel |

| Spray |

| Wipes |

| Automotive |

| Construction |

| Marine |

| Industrial Machinery and Equipment |

| Household/Consumer |

| Aerospace |

| Oil and Gas |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Acid-Based Rust Removers | |

| Neutral pH/Chelate-Based Rust Removers | ||

| Bio-Based Rust Removers | ||

| By Form | Liquid | |

| Gel | ||

| Spray | ||

| Wipes | ||

| By End-user Industry | Automotive | |

| Construction | ||

| Marine | ||

| Industrial Machinery and Equipment | ||

| Household/Consumer | ||

| Aerospace | ||

| Oil and Gas | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the rust remover market?

The rust remover market stands at USD 654.56 million and is forecast to reach USD 848.62 million by 2031 at a 5.33% CAGR from 2026 to 2031.

What strategic focus separates leading suppliers?

Differentiation through USDA-certified biobased content, multifunctional formulations, and early compliance with VOC reporting mandates secures margin and market access.

Why are sprays outpacing other forms in growth?

Ready-to-use aerosols and trigger bottles suit DIY applications, driving a 5.63% CAGR in spray revenues.

How are non-chemical technologies affecting demand?

Laser ablation and dry-ice blasting are replacing chemical removers in high-precision or environmental-sensitive settings, slightly restraining market growth.

Page last updated on: