Bleaching Agent Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

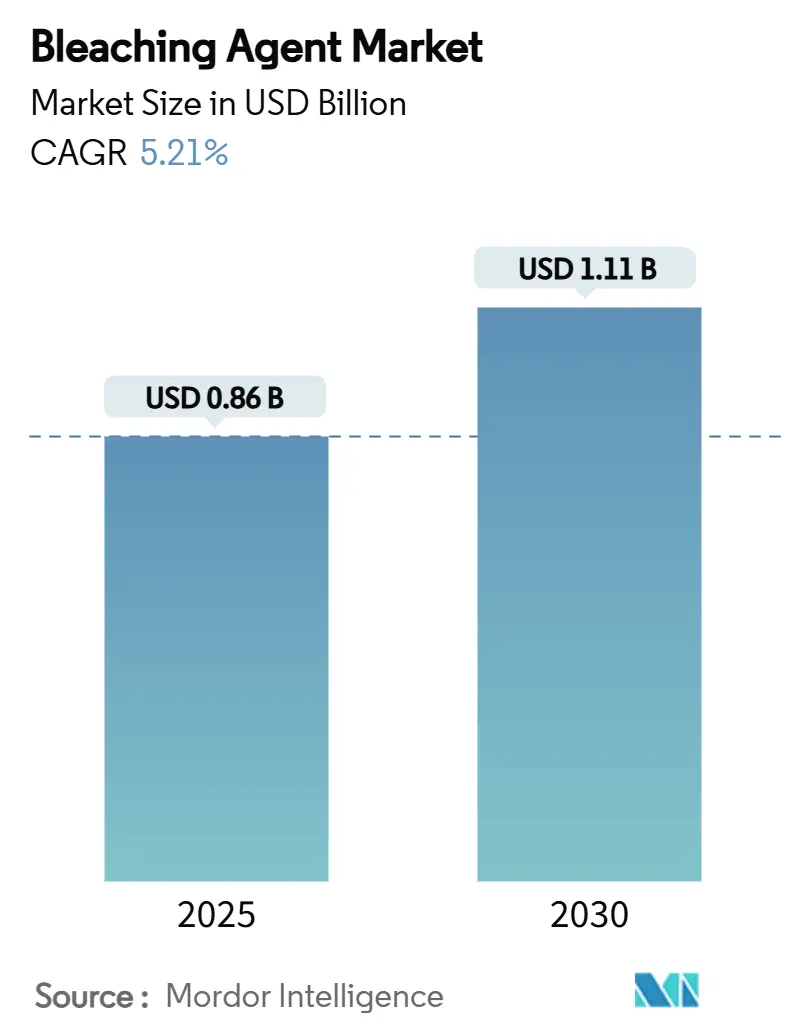

| Market Size (2025) | USD 0.86 Billion |

| Market Size (2030) | USD 1.11 Billion |

| Growth Rate (2025 - 2030) | 5.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bleaching Agent Market Analysis by Mordor Intelligence

The Bleaching Agent Market size is estimated at USD 0.86 billion in 2025, and is expected to reach USD 1.11 billion by 2030, at a CAGR of 5.21% during the forecast period (2025-2030). This projected expansion underscores a steady rise in the bleaching agent market size and the sector’s ability to adapt despite supply-chain disruptions and stricter environmental oversight. Persistent demand from municipal and industrial water treatment, continued preference for chlorine formulations because of cost and efficacy, and rapid uptake of on-site chlorine-dioxide generation underpin market momentum. Powder products, which offer logistical and dosing advantages, deepen manufacturers’ cost leadership, while Asia Pacific’s sizable production base and escalating consumption of bleaching agents in pulp, paper, and textiles keep the region at the forefront of growth.

Key Report Takeaways

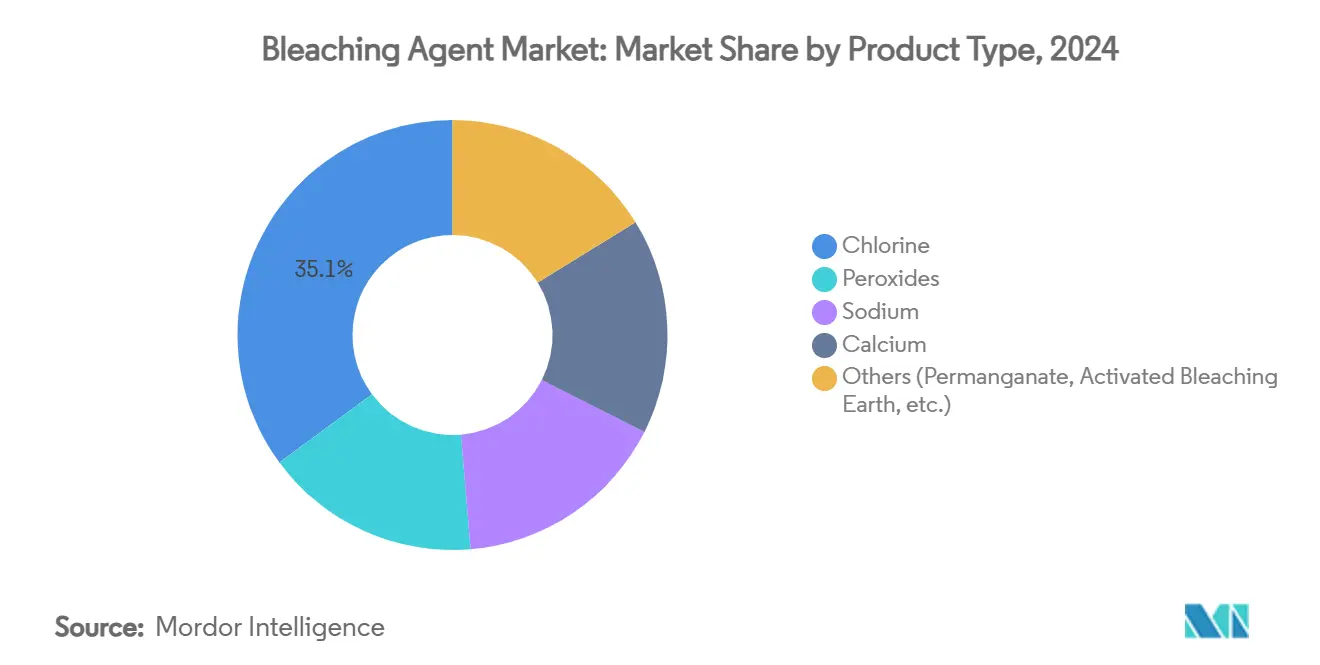

- By product type, chlorine held 35.11% of bleaching agent market share in 2024, whereas peroxide-based agents are poised for the fastest 5.76% CAGR through 2030.

- By form, powder formulations dominated with 61.18% share in 2024 and are expected to expand at a 6.04% CAGR.

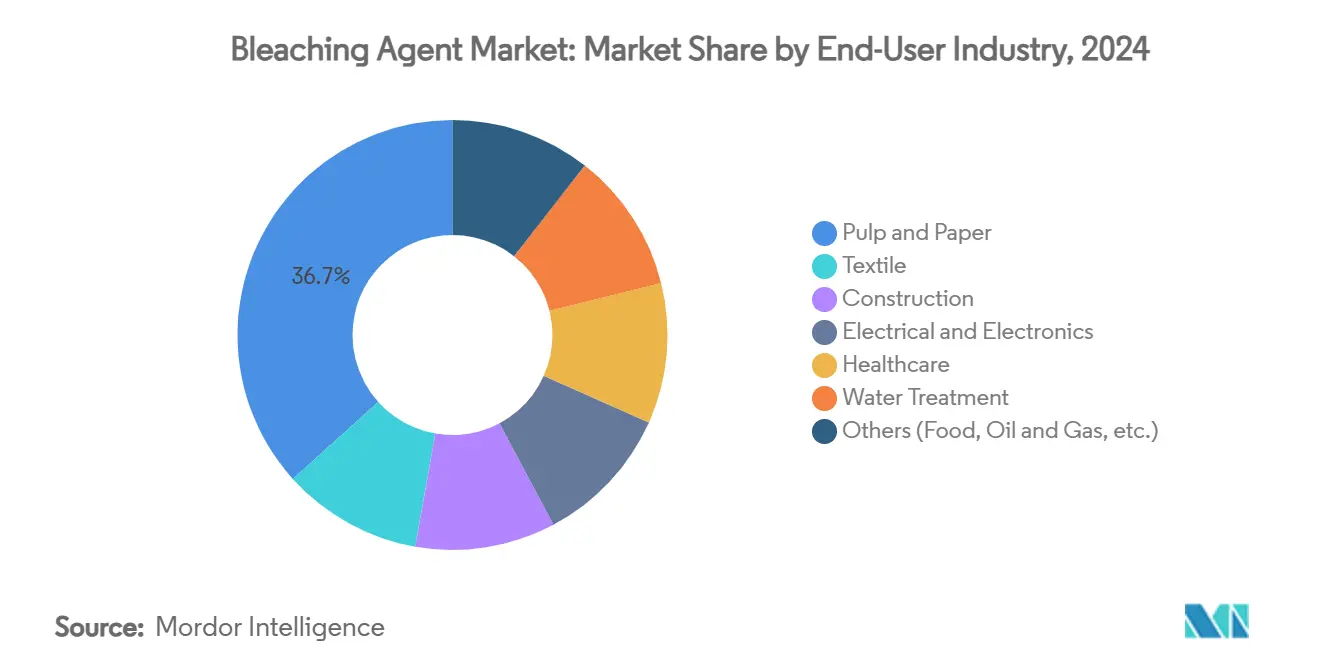

- By end-user industry, the pulp and paper segment accounted for 36.66% of the bleaching agent market size in 2024 and is projected to register a 6.13% CAGR.

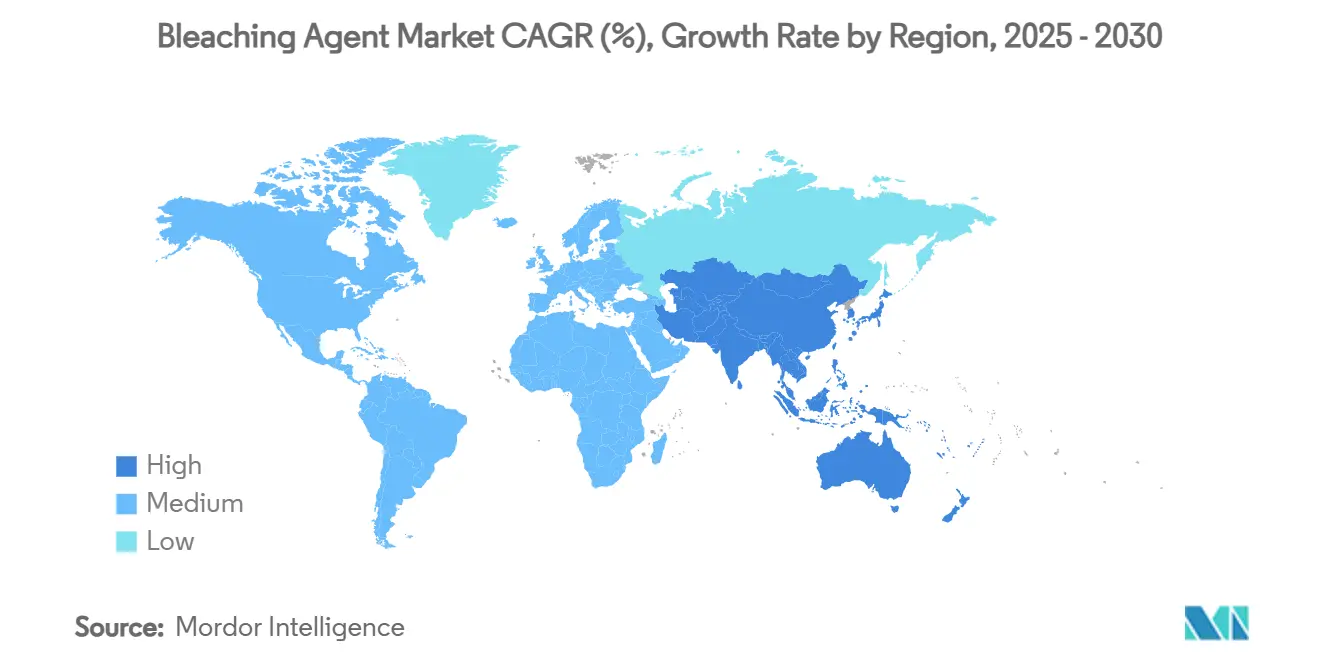

- By geography, Asia Pacific led with 45.22% revenue share in 2024 and is forecast to enlarge at a 6.21% CAGR through 2030.

Global Bleaching Agent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for municipal & industrial water treatment | +1.8% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Surging pulp & paper output in APAC | +1.4% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Expanding textile processing capacity | +1.2% | APAC core, emerging in MEA and Latin America | Medium term (2-4 years) |

| Tightening potable-water residual-chlorine regulations | +0.9% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Rapid uptake of chlorine-dioxide generators in decentralized disinfection | +0.7% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Municipal & Industrial Water Treatment

Utilities worldwide are replacing legacy chlorination systems with chlorine-dioxide solutions because these deliver stronger pathogen control while curbing trihalomethane formation[1]United States Environmental Protection Agency, “Chemical Safety Facts: Chlorine Dioxide,” epa.gov . Installations of on-site generators are growing more than 20% each year as operators aim to bypass hazardous chemical transport and enhance dosage precision. Parallel growth stems from industrial users in food, beverage, and pharmaceutical plants that must meet tighter microbial standards. Heightened hygiene awareness that emerged during the COVID-19 pandemic sustains elevated consumption in health-care and institutional settings. In regions experiencing water scarcity, utilities favor bleaching agents that can treat increasingly contaminated sources without escalating byproducts.

Surging Pulp & Paper Output in APAC

Rapid urbanization and e-commerce have boosted packaging demand, lifting pulp and paper output and, consequently, bleaching agent consumption across China, India, Japan, and South Korea. Mill operators are transitioning from elemental chlorine to chlorine-dioxide and enzyme-aided sequences, which cut chemical oxygen-demand while maintaining brightness targets. Hydrogen peroxide remains pivotal in elemental-chlorine-free processes as producers raise brightness from 88 to more than 92 ISO. Regional producers also continue to invest in safety retrofits to curb incidents in high-pressure oxidation units.

Expanding Textile Processing Capacity

Competitive labor costs and trade-zone incentives have drawn textile finishing plants to South and Southeast Asia. Brands pursuing eco-labels demand fabric whiteness with lower water and energy footprints, spurring mills to deploy chlorine-dioxide or stabilized peroxide baths that reduce re-bleach cycles and minimize fiber damage. Fast-fashion’s compressed timelines make batch-to-batch shade consistency critical, favoring bleaching agents with narrow process tolerances. Research into enzyme-peroxide hybrids shows promise for cotton and viscose substrates, yet high enzyme costs still limit widespread commercial adoption.

Tightening Potable-Water Residual-Chlorine Regulations

The United States limits chlorine-dioxide to 0.8 mg/L and chlorite to 1.0 mg/L in finished water[2]Centers for Disease Control and Prevention, “Disinfection with Chlorine and Chlorine Compounds,” cdc.gov. European directives impose similar or stricter thresholds, pushing utilities toward equipment with real-time monitoring and automatic shutoff. Compliance investments have prompted suppliers to introduce digital controllers and vacuum-feed systems that improve dosing accuracy and mitigate gas leak risks. For manufacturers, REACH dossier requirements raise formulation costs and lengthen product-approval cycles, reinforcing the advantage of established players that can navigate regulatory obligations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute & chronic toxicity concerns of chlorinated bleaches | -1.1% | Global, most pronounced in Europe and North America | Short term (≤ 2 years) |

| Stringent environmental regulations | -0.8% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Volatility in raw material costs | -0.6% | Global, with regional variations in energy costs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute & Chronic Toxicity Concerns of Chlorinated Bleaches

Occupational-exposure limits for chlorine-dioxide vapors are set at 0.1 ppm (8-hour TWA) in several jurisdictions, prompting industrial users to install advanced ventilation and leak-detection systems. Publicized poisoning events during the pandemic reinforced consumer skepticism and spurred retailers to offer alternatives with lower hazard symbols. Healthcare and food sectors increasingly favor peroxide or peracetic-acid blends, even at higher unit costs, to reduce staff training and storage controls.

Stringent Environmental Regulations

REACH and analogous rules elsewhere oblige bleaching-agent producers to supply extensive toxicological and environmental-fate data for substances above 1 t/y, inflating compliance costs. For pulp mills, conversion to totally chlorine-free sequences would necessitate capital outlays surpassing USD 1.7 billion and push up annual operating costs by USD 320 million, according to the American Chemistry Council. The economic burden may accelerate consolidation as smaller regional suppliers exit or sell to integrated groups with deeper regulatory resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chlorine Maintains Dominance Despite Environmental Pressures

The chlorine segment retained 35.11% of bleaching agent market share in 2024—largely due to entrenched infrastructure, low raw-material cost, and diversified supply controlled by vertically integrated chlor-alkali producers. Chlor-alkali cogeneration ensures continuous chlorine gas availability, allowing large players to honor long-term supply contracts, especially for municipal disinfection plants. Despite scrutiny over chlorinated byproducts, replacement remains gradual because many facilities lack immediate capital for new reactors or safety retrofits. Hydrogen peroxide and sodium percarbonate together posted the fastest 5.76% CAGR, buoyed by pulp and paper mills striving for elemental-chlorine-free status and laundry formulators marketing eco-labels. Catalyzed peroxide, which decomposes into water and oxygen, appeals to food, beverage, and pharmaceutical processors seeking residue-free sanitation. Specialty oxidants such as potassium permanganate and activated bleaching earth fill high-value but lower-volume niches in semiconductor, oil-refining, and edible-oil purification.

By Form: Powder Formulations Lead Through Operational Advantages

Powdered products accounted for 61.18% of bleaching agent market size in 2024. Their low water content concentrates active ingredient, cutting freight cost per activity unit and easing compliance with transport-hazard regulations. Powders also grant processors tight dosage control, an attribute prized in color-critical applications such as paper and textile finishing. Encapsulation techniques that embed active chlorinated granules in inert carriers suppress dust and extend shelf life, enabling distributors to stock larger inventories without performance loss. Liquids, though less dominant, maintain relevance where immediate solubilization is critical—namely in on-site chlorine-dioxide generation, membrane-bio-reactors, and certain healthcare decontamination systems.

By End-User Industry: Pulp and Paper Industry Leads the Way in Consumption Growth

In 2024, the pulp and paper industry held a significant 36.66% share of the market and is expected to grow steadily at a 6.13% CAGR through 2030. This growth is driven by increasing production capacities in the Asia Pacific region and the adoption of advanced bleaching technologies that not only enhance brightness but also reduce environmental impact. Kemira, a key player with an 18% share in pulp and paper bleaching chemicals, highlights the industry's move toward specialized suppliers who offer comprehensive solutions and technical expertise. Manufacturers are increasingly turning to chlorine dioxide systems to achieve better brightness levels while cutting down on harmful byproducts. Leading the way in innovation, Japanese and Korean mills are utilizing enzyme-assisted processes that improve pulp brightness by 3.7% ISO compared to traditional methods. Sodium chlorate plays a crucial role in this segment, accounting for over 85% of global demand.

Water treatment applications are expanding rapidly as municipalities work to modernize outdated infrastructure and comply with stricter disinfection standards. Chlorine dioxide generators are becoming the go-to choice over traditional chlorination systems due to their better pathogen control and fewer byproducts. Regulatory requirements further support this growth, with EPA standards limiting chlorine dioxide to 0.8 mg/L and chlorite to 1.0 mg/L in drinking water systems. In the textile processing sector, growing capacities in emerging markets are driving demand for chlorine dioxide, which delivers superior fabric whiteness and strength while being more environmentally friendly than traditional hydrogen peroxide treatments.

Geography Analysis

Asia Pacific’s 45.22% revenue share in 2024 underscores its combined manufacturing scale and rising local consumption. Government incentives for paper recycling, coupled with export-oriented textile clusters, underpin a 6.21% CAGR outlook. Mills across coastal China have upgraded to multi-stage chlorine-dioxide sequences that raise brightness while cutting adsorbable-organic-halide discharge. India’s downstream paper and garment sectors, supported by new sodium-chlorate and hydrogen-peroxide plants, contribute to steady regional demand growth.

North America benefits from advanced process control, high regulatory awareness, and recent capital projects that reduce reliance on transported chlorine gas. A USD 70 million plant in Arizona converting salt brine to sodium hypochlorite typifies the on-shoring trend, which enhances supply security for western utilities. Healthcare facilities favor chlorine-dioxide for hot-water-line disinfection; Johns Hopkins Hospital’s multi-decade performance record demonstrates sustained Legionella suppression without pipe corrosion.

Europe confronts the costliest compliance burden. REACH dossier fees and upcoming emissions ceilings push producers toward lower-hazard formulations and raise interest in bio-based or enzyme-aided bleaching. Pilot installations in Scandinavian pulp mills demonstrate 25% chemical-consumption cuts when replacing the first alkaline extraction with laccase-mediated steps. Latin American and Middle-Eastern markets remain comparatively small but present upside through infrastructure projects that expand potable-water networks and cellulose fiber capacity.

Competitive Landscape

The bleaching agent market is moderately concentrated. BASF, Dow, and Olin integrate upstream chlor-alkali electrolysis with downstream formulation, shielding margins from sodium-chloride and electricity volatility. BASF’s focus on specialty oxidants for semiconductor wet processes exemplifies diversification beyond commodity chlorine, while Dow’s peroxygens unit expands capacity to serve eco-label detergents.

Strategic acquisitions target geographic reach and feedstock security. Technology partnerships also play a role: Occidental Chemical’s licensing of proprietary vacuum-feed chlorine-dioxide generators to equipment OEMs accelerates adoption in mid-sized municipal plants. For smaller firms, niche performance additives—such as chelating agents that boost peroxide stability—offer defensible segments but require continuous research investment to keep pace with evolving regulatory standards.

Bleaching Agent Industry Leaders

Evonik Industries AG

BASF

Solvay

Nouryon

Kemira

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Chlorum Solutions announced plans to invest over USD 70 million in an Arizona facility to convert salt into sodium hypochlorite (bleach) and other chemicals, eliminating the need to store chlorine gas and reducing transportation risks for municipal water treatment applications.

- November 2024: ANSA McAL completed its USD 327 million acquisition of BLEACHTECH, a Cleveland-based chlor-alkali producer specializing in high-purity bleach, hydrochloric acid, and caustic soda for municipal and industrial water treatment applications. The acquisition strengthens ANSA McAL's position in the Caribbean chlor-alkali market.

Global Bleaching Agent Market Report Scope

The Global Bleaching Agent market report includes:

| Chlorine |

| Peroxides |

| Sodium |

| Calcium |

| Others (Permanganate, Activated Bleaching Earth, etc.) |

| Powder |

| Liquid |

| Pulp and Paper |

| Textile |

| Construction |

| Electrical and Electronics |

| Healthcare |

| Water Treatment |

| Others (Food, Oil and Gas, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Chlorine | |

| Peroxides | ||

| Sodium | ||

| Calcium | ||

| Others (Permanganate, Activated Bleaching Earth, etc.) | ||

| By Form | Powder | |

| Liquid | ||

| By End-user Industry | Pulp and Paper | |

| Textile | ||

| Construction | ||

| Electrical and Electronics | ||

| Healthcare | ||

| Water Treatment | ||

| Others (Food, Oil and Gas, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Bleaching Agent Market size?

The bleaching agent market is valued at USD 0.86 billion in 2025.

Which region leads the bleaching agent market?

Asia Pacific holds the top position with 45.22% revenue share and is projected to expand at a 6.21% CAGR through 2030.

Which end-user sector consumes the most bleaching agents?

The pulp and paper sector leads with 36.66% market share and is forecast for a 6.13% CAGR.

Why are powder bleaching agents preferred?

Powder formulations offer higher active-ingredient concentration, lower shipping costs, improved storage stability, and more precise dosing in automated systems.

Page last updated on: