Packed Pickles Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 11.66 Billion |

| Market Size (2031) | USD 14.01 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

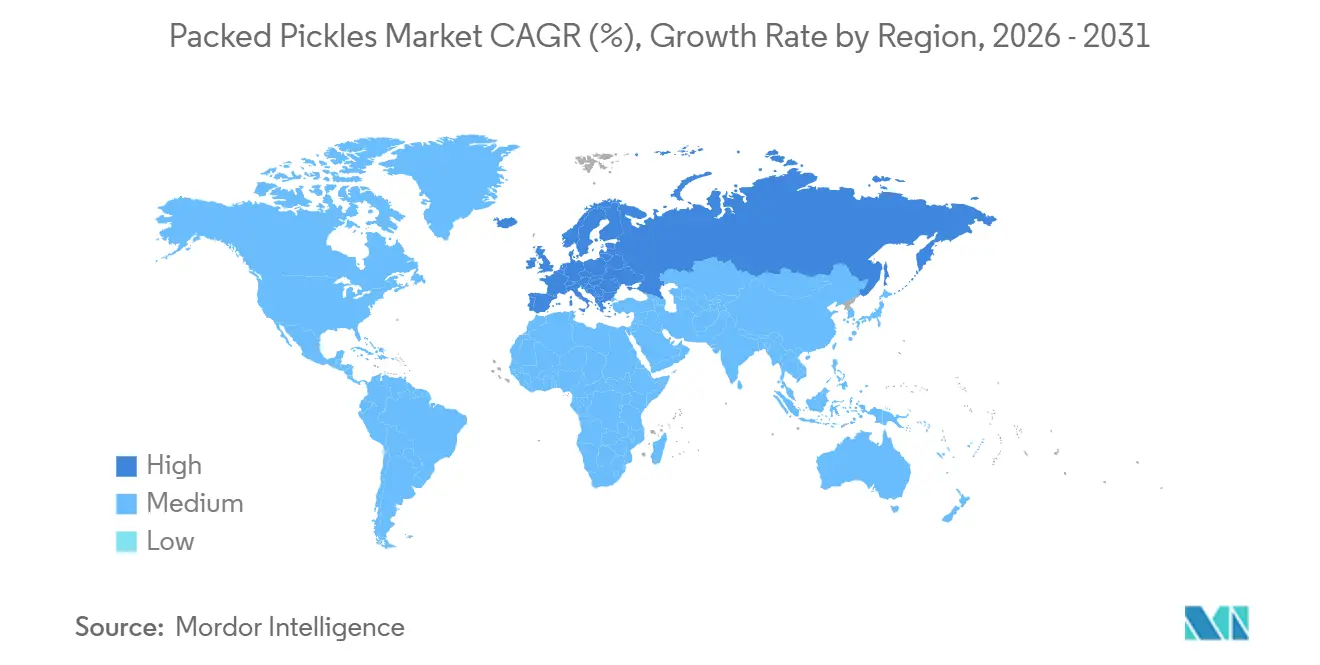

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

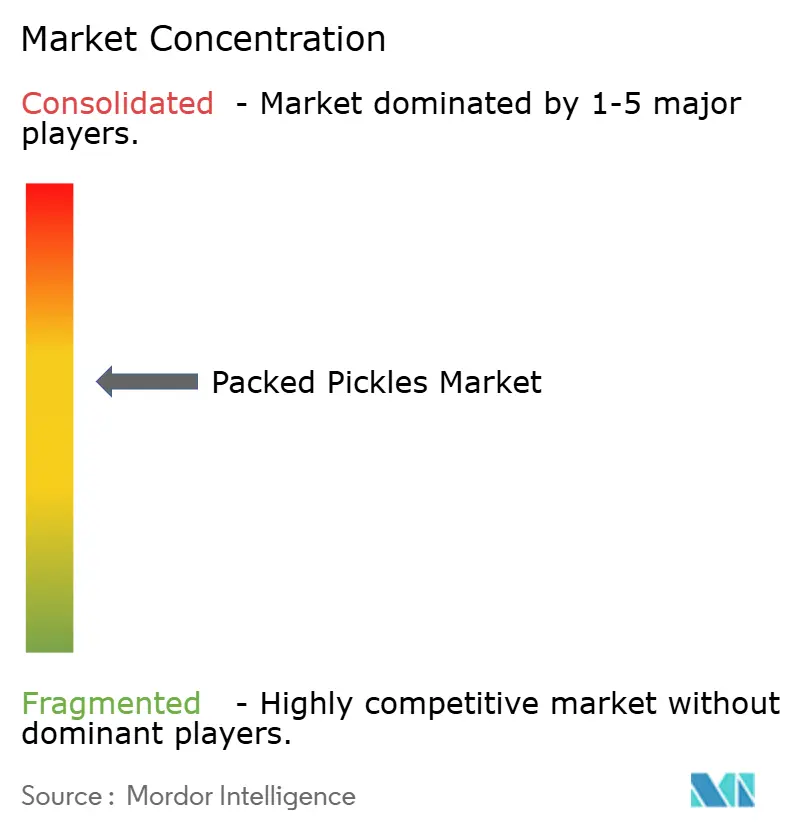

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Packed Pickles Market Analysis by Mordor Intelligence

The packed pickles market size is projected to expand from USD 11.24 billion in 2025 and USD 11.66 billion in 2026 to USD 14.01 billion by 2031, registering a 3.74% CAGR between 2026 and 2031. Probiotic positioning is driving incremental volume gains for fermented variants, as consumers increasingly seek functional foods that support gut health. Meanwhile, flexible pouches are replacing glass containers, a shift prompted by rising costs, improved convenience, and mandates on recyclability. In North America and Europe, retailers are reducing ambient shelf space as kombucha and kefir gain prominence in refrigerated displays due to their perceived health benefits and growing consumer demand. This shift is nudging pickle brands to forge partnerships within the cold chain to maintain competitiveness. In India and Türkiye, contract-farming hubs continue to bolster the supply of private-label gherkins, ensuring consistent production for export markets. However, extreme weather events, such as unseasonal rains and heatwaves, are causing volatility in raw material prices, impacting cost structures. Stricter regulations on traceability and packaging recyclability are reshaping the competitive landscape, favoring players with strong investments in digital technologies and supply-chain capabilities, which enable better compliance and operational efficiency.

Key Report Takeaways

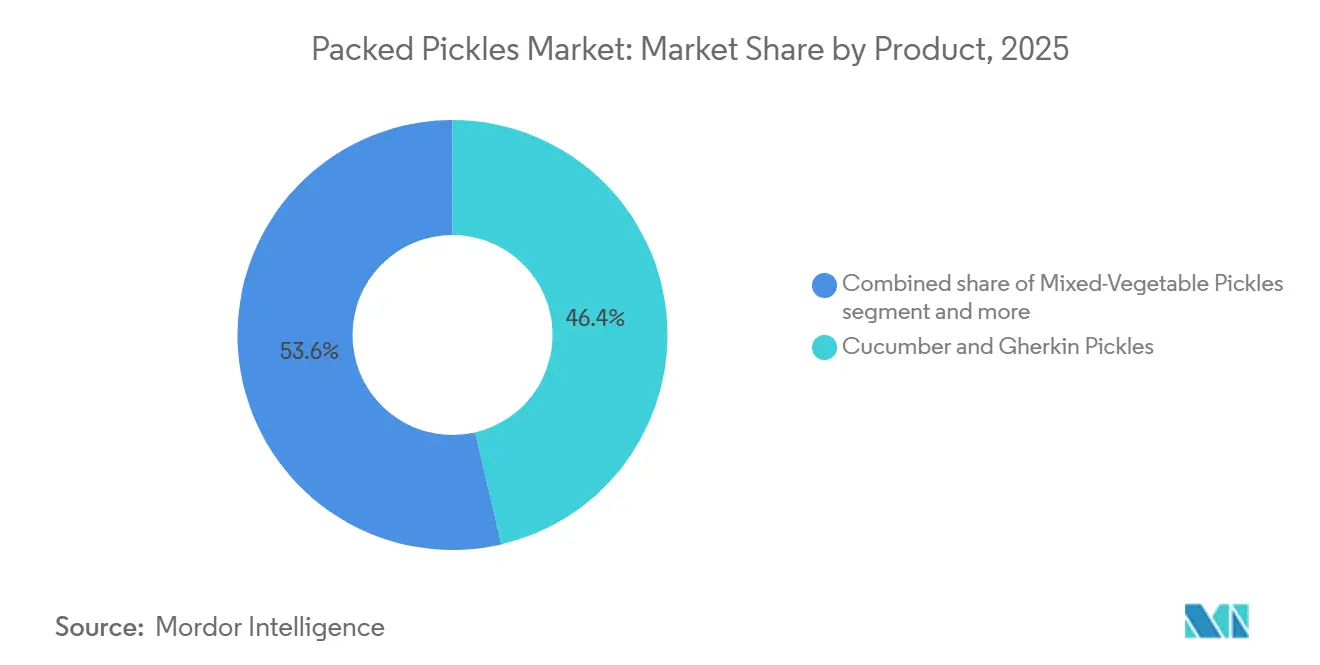

- By product type, cucumber and gherkin pickles held 46.36% of the packed pickles market share in 2025. Mixed-vegetable blends are projected to record a 4.05% CAGR between 2026 and 2031.

- By packaging type, glass jars dominated with 58.68% of 2025 sales. Pouches and stand-up bags are forecast to advance at a 5.35% CAGR over 2026-2031.

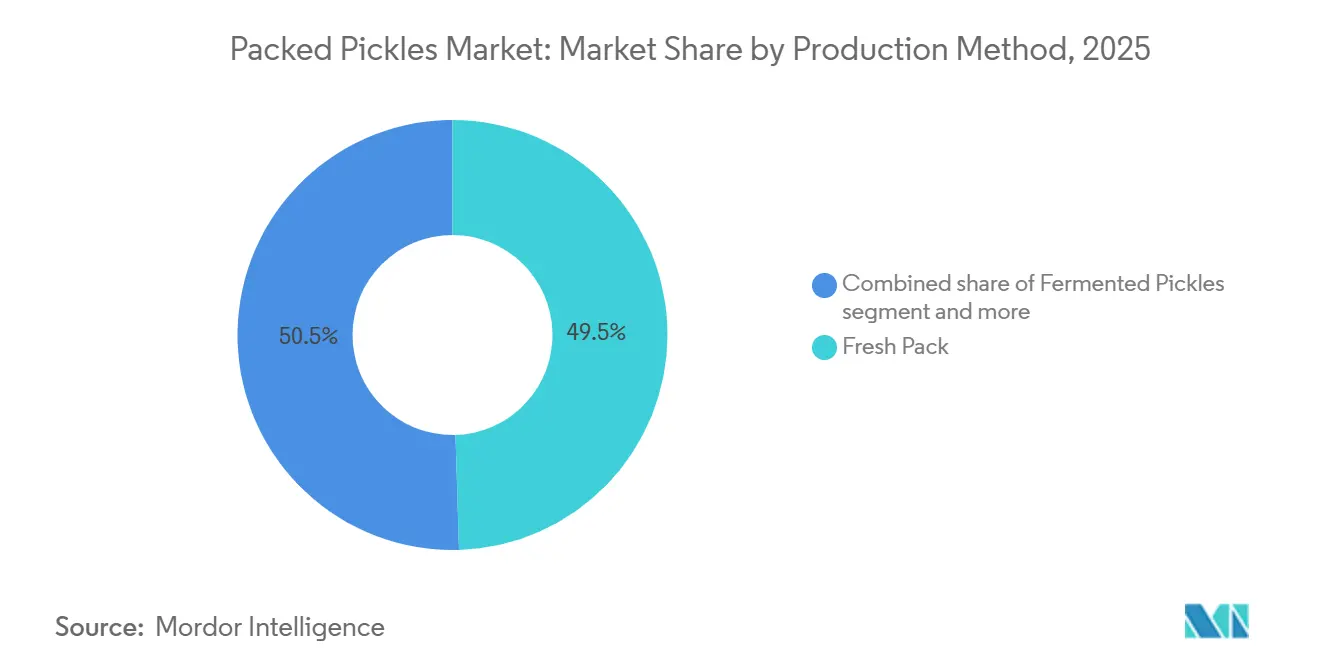

- By production method, fresh-pack formats accounted for 49.52% of 2025 revenue. Fermented variants are expected to increase at a 4.83% CAGR through 2031.

- By distribution channel, off-trade commanded 67.51% of the packed pickles market size in 2025. On-trade is anticipated to expand at a 4.21% CAGR during 2026-2031.

- By geography, Asia-Pacific led with 31.54% of global sales in 2025. Europe is poised to be the fastest region, growing at a 4.17% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Packed Pickles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Fermented Foods | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Innovative Packaging Formats | +0.8% | Global, led by North America and Europe | Short to Medium term (≤ 3 years) |

| E-commerce Access to Regional Flavors | +0.6% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Stricter Clean-Label Regulations | +0.7% | North America and Europe | Long term (≥ 4 years) |

| Gen-Z Preference for Fresh-Crunch Textures | +0.5% | Urban centers worldwide | Medium term (2-4 years) |

| Contract-Farming Securing Gherkin Supply | +0.4% | India and Türkiye exporting to EU and North America | Medium to Long term (3-5 years) |

| Source: Mordor Intelligence | |||

Increasing demand for fermented foods due to gut-health benefits

Fermented pickles are gaining traction as lacto-fermentation imparts live cultures, bioactive peptides, and short-chain fatty acids, all of which play a role in modulating gut microbiota. These benefits lead to tangible health outcomes, justifying premium pricing. In light of this, brands are spotlighting small-batch fermentation and advocating for transparent, clean labels[1]Source: Multidisciplinary Digital Publishing Institute, "The Role of Fermented Vegetables as a Sustainable and Health-Promoting Nutritional Resource", mdpi.com. This has led to increased consumer awareness about the health benefits of fermented foods, driving demand in both developed and emerging markets. Additionally, the growing trend of clean-label and minimally processed foods further supports the popularity of fermented pickles. In North America and Europe, brands emphasize the presence of “live cultures” and intentionally bypass pasteurization. This strategy is particularly effective in regions where the premium on functional foods justifies the expenses of refrigerated logistics.

Innovative packaging formats expanding snacking opportunities

Pouches are gaining popularity due to their ability to offer single-serve convenience while reducing shipping weight by 60-70%. This reduction in weight not only lowers transportation costs but also contributes to sustainability by minimizing carbon emissions. Additionally, the lightweight nature of pouches makes them easier to handle and store for both retailers and consumers. SIG's newly patented aseptic pouch for 2024 allows for ambient storage, broadening its distribution reach into convenience stores. The ambient storage capability eliminates the need for refrigeration, making it a cost-effective solution for retailers. Furthermore, this innovation aligns with the growing demand for packaging solutions that support extended shelf life without compromising product quality. Meanwhile, Conagra's innovative resealable oxygen-barrier films ensure a 12-month crunch, catering to consumer preferences for texture preservation. This development highlights the growing focus on packaging technologies that enhance product shelf life and meet evolving consumer demands.

E-commerce enhancing accessibility to niche regional pickle flavors

Small-batch Andhra avakaya and Korean oi-sobagi can now reach diaspora customers directly, thanks to direct-to-consumer platforms, bypassing the need for national retail listings. These online storefronts have also sped up flavor iteration cycles, shrinking them from 18 months to just 6 weeks, which has heightened competitive churn. This shift has enabled niche producers to test and refine their products more rapidly, catering to evolving consumer preferences. Additionally, it has lowered entry barriers for smaller players, fostering innovation in the market. As a result, the direct-to-consumer model is reshaping traditional supply chains and creating new opportunities for growth. The model also allows producers to gather direct feedback from consumers, enabling data-driven decision-making. Furthermore, it enhances customer engagement by offering personalized experiences and fostering brand loyalty. This transformation is driving a significant change in how specialty food products are marketed and consumed globally.

Stricter traceability and clean-label regulations driving premium products

FSMA 204 and EU 1169/2011 mandate lot-level tracking and clear ingredient listings. While larger firms leverage compliance as a marketing tool, branding it as "farm-to-jar transparency," smaller packers grapple with expensive system upgrades or risk exiting the channel. These regulations aim to enhance consumer trust by ensuring traceability and accurate product information. Larger companies often invest in advanced technologies to streamline compliance processes, gaining a competitive edge. However, smaller players face challenges in securing the necessary resources, which could lead to market consolidation over time. Additionally, the growing consumer demand for transparency is driving firms to adopt innovative solutions. Non-compliance with these regulations could result in penalties, further pressuring smaller businesses. As a result, partnerships and collaborations are emerging as potential strategies to share compliance costs and expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-Induced Volatility in Harvests | -0.3% | India, Mexico, Mediterranean | Short to Medium term (≤ 3 years) |

| Sodium-Reduction Mandates | -0.2% | North America and Europe | Medium to Long term (3-5 years) |

| Global Glass-Jar Shortages | -0.2% | Global, acute in India and North America | Short term (≤ 2 years) |

| Probiotic Beverage Shelf Competition | -0.1% | North America and Europe | Short to Medium term (≤ 3 years) |

| Source: Mordor Intelligence | |||

Climate-induced volatility in cucumber and chilli harvests

In 2024-2025, cucumber yields plummet by as much as 40% due to heat and drought, leading to surging spot prices that strain processors. While genomic advancements, such as qHT1.1, offer hope, commercial seeds are still 3-5 years away. This significant yield reduction disrupts the supply chain, impacting both producers and end-users. In 2024, cucumbers worth USD 1.45 billion made their way into the United States, according to the Observatory of Economic Complexity (OEC). Mexico led the charge, supplying cucumbers valued at USD 876 million. Canada followed suit with imports worth USD 562 million. Other notable sources included Honduras (USD 7.12 million), the Dominican Republic (USD 4.49 million), and Spain (USD 3.61 million)[2]Source: The Observatory of Economic Complexity (OEC), " Cucumbers in the United States", oec.world.com.Processors face increased costs, which may translate to higher prices for consumers. The delay in the availability of commercial seeds underscores the urgent need for interim solutions to mitigate the effects of climate change on agriculture. Additionally, the reduced yields are expected to intensify competition among processors for limited raw materials. This situation could also prompt increased investment in research and development to accelerate the availability of resilient seed varieties. Furthermore, policymakers may need to intervene with subsidies or support programs to stabilize the market and protect stakeholders across the value chain.

Sodium-reduction mandates limiting formulation flexibility

Under the FDA's phased sodium targets, brands are being pushed to reduce salt, a key player in preservation and flavor. While potassium chloride offers a substitute, it comes with a metallic aftertaste, leading brands to invest in expensive sensory trials.Meanwhile, Europe's Regulation 2023/915 sets strict ceilings on contaminant levels and demands rigorous traceability, adding to the compliance challenges for manufacturers[3]Source: European Union, "COMMISSION REGULATION (EU) 2023/915", eur-lex.europa.eu. This regulatory shift is driving innovation in salt reduction technologies, as companies seek alternatives that maintain product quality. Additionally, the pressure to meet these targets is influencing supply chain dynamics, with ingredient suppliers exploring new formulations. The long-term impact of these changes could reshape consumer preferences and market trends in the food industry. Furthermore, brands are increasingly collaborating with research institutions to develop advanced solutions for sodium reduction. Consumer education campaigns are also gaining traction, aiming to raise awareness about the health benefits of reduced sodium intake. These efforts collectively highlight the growing importance of regulatory compliance and consumer health in shaping the competitive landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mixed-Vegetable Blends Outpace Cucumber Dominance

Cucumber and gherkin formats lead the global packed pickles market, commanding the largest share of revenue. In 2025, making up roughly 46.36% of the total market. Their dominance is bolstered by strong consumer recognition, widespread availability, and ingrained consumption habits in both developed and emerging markets. Furthermore, consistent supply chains and standardized processing methods have solidified their scale advantage. While there's a growing interest in alternative variants, cucumber and gherkin products remain central to the category's growth, thanks to their mainstream allure.

Mixed-vegetable pickles are the market's fastest-growing segment, with projections of a 4.05% CAGR over the forecast period. This surge is largely attributed to shifting consumer tastes, especially among Gen-Z, who are drawn to diverse and experimental flavors. The segment's growth is further enhanced by its reduced dependence on a single crop, enabling manufacturers to navigate agricultural risks and supply changes more adeptly. Innovations in product formulations, including blends of cauliflower, carrot, and radish, are driving heightened demand. Moreover, brands like Mother’s Recipe have rolled out regionally inspired Indian variants between 2024 and 2026, underscoring the potential of localized flavors on a global stage.

By Packaging Type: Flexible Formats Disrupt Glass-Jar Hegemony

In 2025, glass jars are set to maintain their dominance in the packed pickles market, representing 58.68% of the total tonnage. This stronghold is attributed to consumer perceptions of premium quality, product safety, and flavor preservation associated with glass packaging. Furthermore, glass not only resonates with traditional consumption habits but also boosts shelf appeal in retail settings. Yet, the industry grapples with challenges: surging input and energy costs have led to a notable 40% price hike for jars in markets like India. Such cost pressures are starting to squeeze profit margins, casting a shadow on the segment's long-term outlook.

Pouches are rapidly gaining traction as the packaging format of choice, with projections indicating a robust CAGR of 5.35% during the forecast period. While they currently represent about 18% of shipments, their growth is fueled by cost efficiency and logistical benefits. Moreover, breakthroughs in aseptic packaging technology have done away with refrigeration needs, paving the way for broader distribution channels like vending machines and convenience stores. These advantages position pouches as a favored choice in both price-sensitive and rapidly expanding markets. Consequently, by 2031, glass packaging is anticipated to cede 6–8 percentage points of its market share, signaling a notable shift in packaging trends.

By Production Method: Fermented Variants Claim Health Halo

In 2025, fresh-pack vinegar brines dominated the packed pickles market, capturing 49.52% of total sales. Their leading position stems from widespread consumer familiarity and the benefits of shelf-stable storage, which streamlines distribution and lessens logistical challenges. These brines consistently deliver taste profiles that resonate with mainstream regional preferences. Furthermore, their extended shelf life renders them ideal for both large-scale retail and export markets. Consequently, while there's a growing interest in alternative preservation methods, fresh-pack formats remain the cornerstone of the category.

Fermented pickles are the segment to watch, with projections indicating a robust CAGR of 4.83% during the forecast period. This surge is largely attributed to heightened consumer awareness surrounding gut health and the advantages of live cultures found in fermented foods. Europe stands out as a pivotal market, bolstered by its rich heritage of fermented delicacies like sauerkraut and cornichons. On the other hand, North America's momentum is driven by a surge in chilled deli offerings and a focus on premium, health-centric products.

By Distribution Channel: On-Trade Gains as QSRs Add Pickle Menus

In 2025, off-trade channels will dominate the packed pickles market, accounting for 67.51% of total turnover. Supermarkets, hypermarkets, and grocery stores, as primary purchase points, bolster this segment's dominance. With a robust retail infrastructure and strong household consumption patterns, off-trade channels have solidified their position. Yet, as consumption increasingly leans towards foodservice channels, off-trade's share is witnessing a gradual decline. Restaurants are now experimenting with pickles on their menus, subtly shifting demand away from conventional retail. This trend highlights the evolving consumer preferences and the growing influence of dining-out experiences on the packed pickles market.

On-trade channels are set to be the fastest-growing segment, with a projected CAGR of 4.21% during the forecast period. Quick-service and casual dining restaurants are transforming pickles from mere side garnishes to main menu attractions. Innovations like fried pickle chips and brined chicken sandwiches are driving this trend. Concurrently, the online grocery segment within off-trade is booming in 2025, as per USDA e-commerce metrics. This online surge is empowering niche and regional brands to tap into national markets, lessening their reliance on traditional retail spaces. The rapid growth of online grocery platforms underscores the increasing importance of digital channels in reshaping distribution strategies for the packed pickles market.

Geography Analysis

In 2025, the Asia-Pacific region, fueled by India's robust achaar consumption and China's affinity for fermented mustard greens, commanded 31.54% of global revenue. In fiscal 2024, Indian gherkin exports, valued at USD 256 million, fortified the European private-label supply chain, even in the face of looming U.S. tariff hurdles. The region's supremacy is bolstered by a burgeoning middle class with shifting dietary inclinations. Additionally, the increasing urbanization in countries like India and China has led to higher demand for processed and ready-to-eat foods. The region's strategic focus on enhancing export infrastructure and fostering innovation in food processing technologies further strengthens its competitive edge.

Europe, with a spirited 4.17% CAGR, thrives on the clean-label edicts of EU 1169/2011 and a longstanding cultural penchant for fermented vegetables. Leading the pack, German households boast a per capita consumption of 3.2 kg. The region's commitment to sustainability and health-centric consumption fuels continuous product innovation. Furthermore, the growing popularity of organic and non-GMO fermented products is reshaping consumer preferences. The adoption of advanced manufacturing techniques to meet clean-label and sustainability standards is also driving growth in the European market.

North America, while a seasoned market, pulses with innovation. The FSMA 204 traceability mandate, with a compliance deadline set for July 2028, favors tech-savvy processors. Prioritizing food safety and transparency, the region has seen a surge in investments towards cutting-edge traceability solutions. The increasing consumer demand for locally sourced and ethically produced fermented foods is further shaping market dynamics. Additionally, the region's focus on mitigating risks from climate-related disruptions has led to the exploration of alternative sourcing regions and diversification strategies.

Competitive Landscape

The packed pickles market shows moderate consolidation. In January 2024, TreeHouse Foods strengthened its operations in Canada by acquiring J.M. Smucker’s pickle assets for USD 20 million. This acquisition is expected to enhance TreeHouse Foods' market presence and product offerings in the region. Additionally, Kraft Heinz has announced plans to restructure by splitting into two publicly traded companies in H2 2026. This strategic move aims to separate its high-growth global condiment business from its slower-growing U.S. grocery categories, allowing each entity to focus on its core strengths and market opportunities.

Key strategic priorities in the packed pickles market include the development of premium probiotic SKUs, the adoption of flexible packaging solutions, and the implementation of e-commerce models that bypass traditional distribution channels. SIG’s 2024 patent for aseptic pouches is a significant innovation, enabling the production of ambient probiotic pickles. This breakthrough has the potential to transform cold-chain logistics by reducing dependency on refrigeration. Meanwhile, smaller, disruptive players are leveraging social media platforms to highlight and monetize unique regional flavors. This trend is compelling established brands to accelerate their product development cycles to remain competitive.

Compliance capabilities are increasingly becoming a critical differentiator in the market. Companies equipped with ERP-enabled traceability systems and recyclable packaging portfolios are gaining favor with major retailers. These retailers are proactively preparing to meet the 2030 EU waste regulations, making compliance a key factor in supplier selection. On the other hand, companies that lack the financial resources to transition to sustainable formats face significant risks, including market rationalization or acquisition by larger, more adaptable competitors.

Packed Pickles Industry Leaders

-

The Kraft Heinz Company

-

Conagra Brands, Inc.

-

Mt. Olive Pickle Company, Inc.

-

Fenwick Food Group, LLC

-

Nilon’s Enterprises Pvt. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hearty Roots, a new brand launched by Mother’s Recipe, presents a range of Ayurveda-inspired pickles designed for today's health-conscious consumers. The Hearty Roots collection includes Oil-Free Lime Pickle, Mango Pickle infused with Ashwagandha, Mango Pickle enhanced with Flax Seed, Garlic Pickle with Moringa Leaf, and Sweet Lime Pickle sweetened exclusively with 100% Jaggery, among others.

- July 2025: Cleveland Kitchen launched its "lightly fermented™" fresh pickles, Classic Dill and Kimchi, now enhanced with live cultures. These pickles made their national debut in the refrigerated sections of major grocery chains, supported by the marketing campaign “Hot Pickled Summer.”

- June 2025: Nissin has rolled out a limited-time offering: Cup Noodles Dill Pickle. This new flavor infuses the zesty essence of dill-pickle seasoning into Nissin's signature ramen. The launch took place on various online platforms and at U.S. retailers, prominently featuring Walmart and Albertsons.

- March 2025: The viral brand "Pickle-In-A-Pouch" partnered with Chamoy Mega to bring the spicy, salty, and tangy flavors of Mexican chamoy to its pouches. This collaboration premiered at the Sweets and Snacks 2025 event and was later launched online via Amazon and select retailers in the spring of 2025.

Global Packed Pickles Market Report Scope

Packed pickles are vegetables or fruits that are preserved in brine, vinegar, or oil with spices and then sealed in retail packaging for storage, distribution, and sale. Based on the product type, cucumber and gherkin pickles, mixed-vegetable pickles, and others. Based on the packaging type, the market is segmented into glass jars, pouches, stand-up bags, and others. By production method, the market is segmented into fermented, fresh-pack, and refrigerated fresh-pack. By distribution channel, the market is segmented into off-trade and on-trade. Also, the report offers a detailed analysis of major economies across North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Cucumber and Gherkin Pickles |

| Mixed-Vegetable Pickles |

| Fruit Pickles |

| Meat/Seafood Pickles |

| Glass Jars |

| Pouches and Stand-Up Bags |

| Others |

| Fermented |

| Fresh-Pack |

| Refrigerated Fresh-Pack |

| Off Trade | Convenience Stores |

| Online Retail Stores | |

| Supermarkets/Hypermarkets | |

| Others | |

| On Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Cucumber and Gherkin Pickles | |

| Mixed-Vegetable Pickles | ||

| Fruit Pickles | ||

| Meat/Seafood Pickles | ||

| By Packaging Type | Glass Jars | |

| Pouches and Stand-Up Bags | ||

| Others | ||

| By Production Method | Fermented | |

| Fresh-Pack | ||

| Refrigerated Fresh-Pack | ||

| By Distribution Channel | Off Trade | Convenience Stores |

| Online Retail Stores | ||

| Supermarkets/Hypermarkets | ||

| Others | ||

| On Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast CAGR for the packed pickles market to 2031?

The packed pickles market is forecast to grow at 3.74% between 2026 and 2031

Which product type holds the largest revenue share?

Cucumber and gherkin pickles led with 46.36% of the packed pickles market share in 2025

Which packaging format is growing the fastest?

Stand-up pouches and flexible bags are projected to advance at a 5.35% CAGR through 2031

Which region is expected to record the highest growth?

Europe is projected to post the fastest regional growth at a 4.17% CAGR to 2031

Page last updated on: