Pretzel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.95 Billion |

| Market Size (2031) | USD 9.49 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

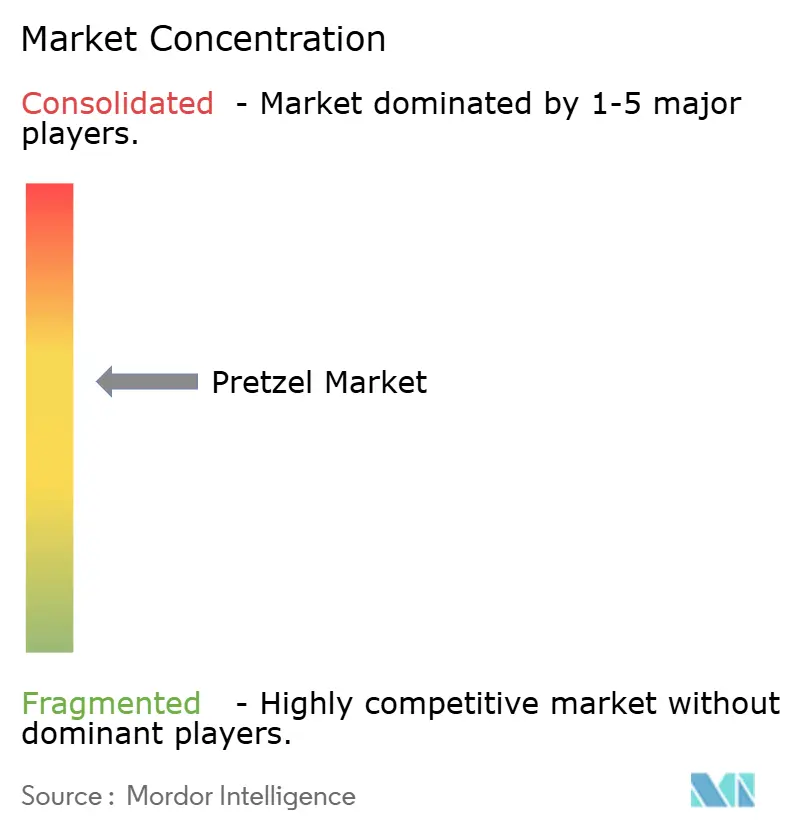

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pretzel Market Analysis by Mordor Intelligence

pretzel market size in 2026 is estimated at USD 7.95 billion, growing from 2025 value of USD 7.67 billion with 2031 projections showing USD 9.49 billion, growing at 3.62% CAGR over 2026-2031. Sustained demand for convenient salty snacks, premium recipe experimentation, and rising e-commerce penetration underpin the upward trajectory despite supply chain volatility and stricter sodium guidelines. Hard pretzels continue to anchor revenue because of their long shelf life and robust retail distribution, while soft and artisanal formats record faster growth as craft bakeries step up menu innovation. Manufacturers are also capitalizing on healthier-snacking behavior, expanding protein-enriched or grain-free lines and reformulating seasonings to comply with voluntary sodium targets. Premiumization and flavor experimentation, from Bavarian sourdough twists to Cheetos-flavored sticks, support elevated price points, which, together with modest input-cost relief from lower wheat futures, provide margin stability even as logistics expenses remain a watch item.

Key Report Takeaways

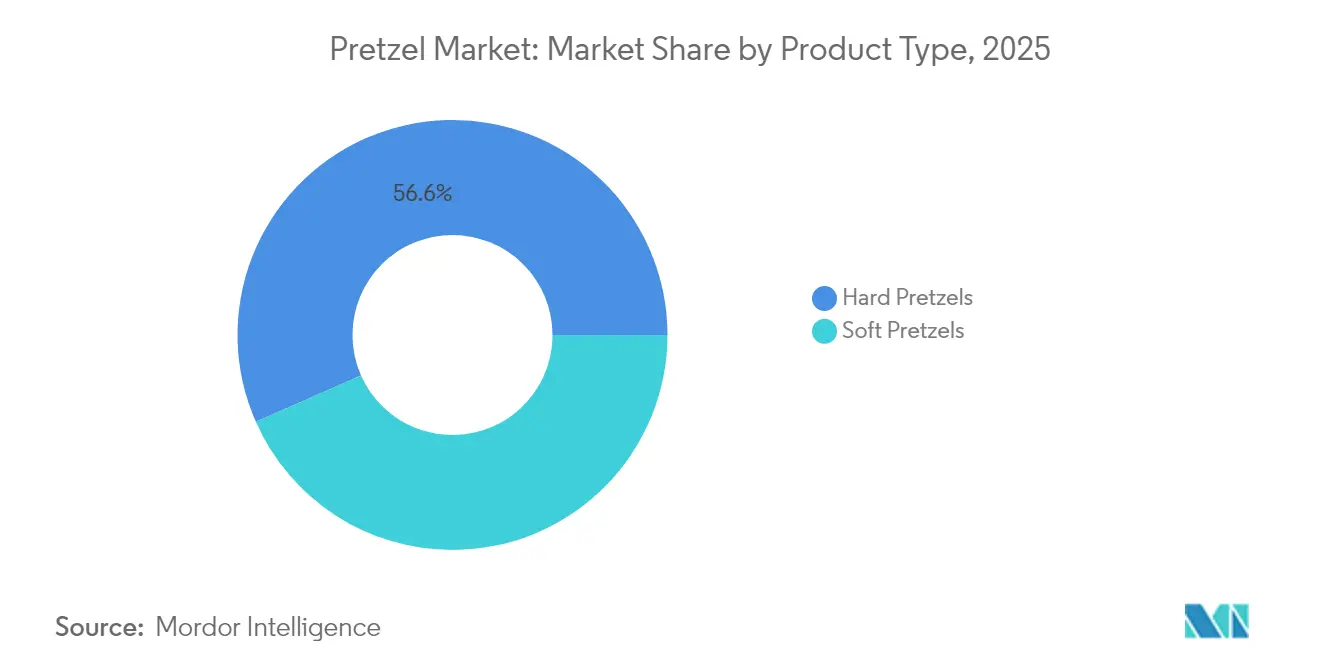

- By product type, hard pretzels led with 56.62% revenue share in 2025; soft pretzels are forecast to expand at a 5.02% CAGR to 2031.

- By content, salted variants accounted for 80.74% of pretzel market share in 2025, while unsalted lines recorded the highest projected CAGR at 5.41% through 2031.

- By ingredient claim, conventional formulations retained 73.86% share of the pretzel market size in 2025, whereas free-from/organic products are advancing at a 5.24% CAGR.

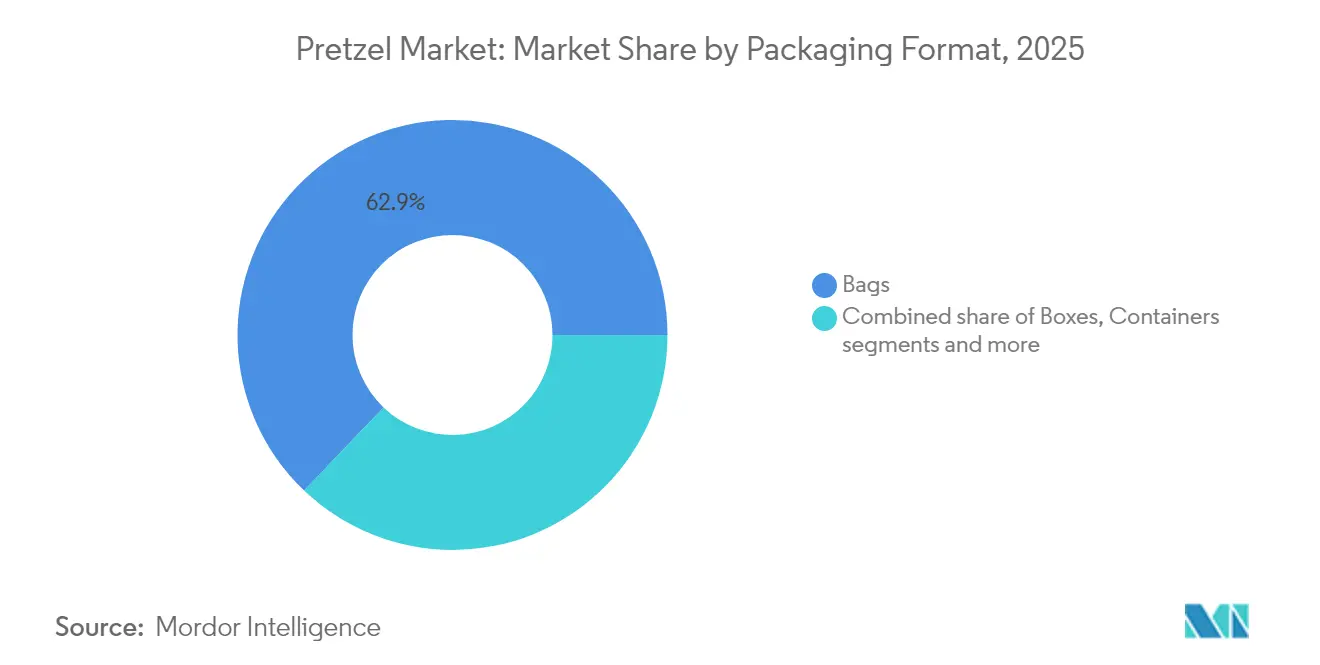

- By packaging format, bags dominated with a 62.88% share in 2025, but containers posted the strongest growth at a 5.08% CAGR between 2026 and 2031.

- By distribution channel, supermarkets/hypermarkets captured 51.35% share of the pretzel market size in 2025; online retail stores registered the quickest expansion at a 4.87% CAGR to 2031.

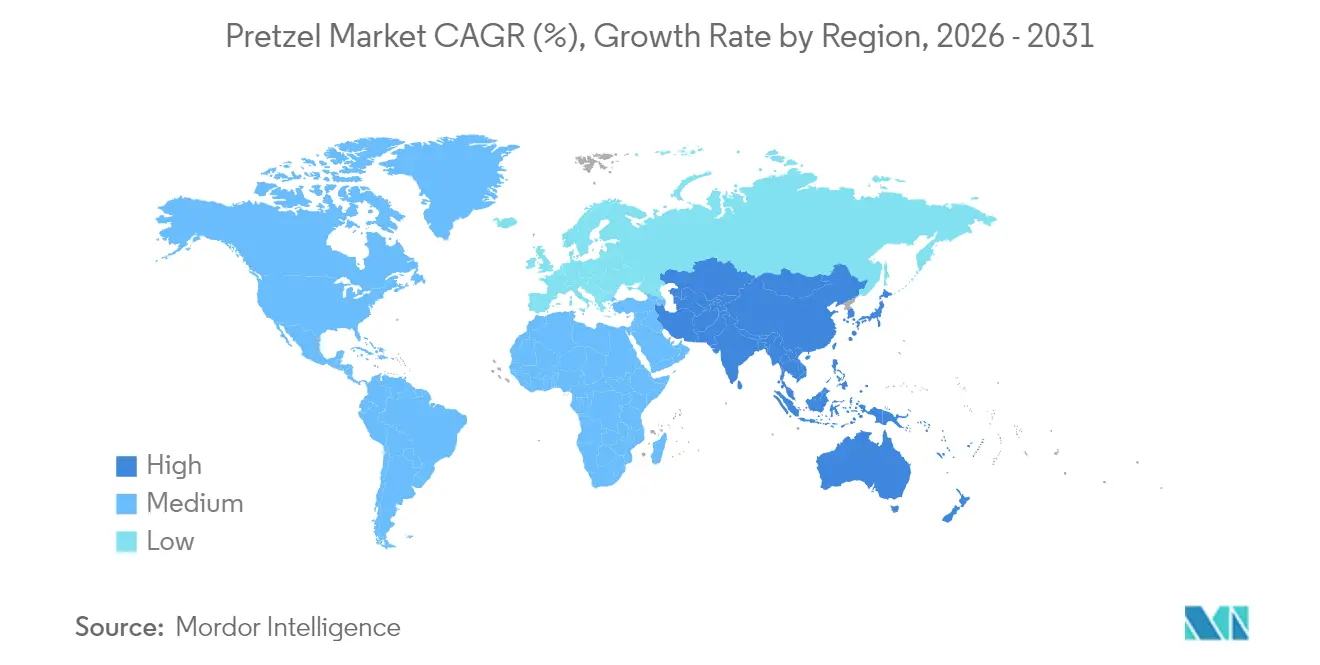

- By geography, North America captured 37.89% revenue share in 2025; however, Asia-Pacific records the highest projected CAGR at 4.58% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pretzel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in healthier snacking trends | +0.8% | Global, with early gains in North America, European Union | Medium term (2-4 years) |

| Innovation in pretzel flavors | +0.6% | North America core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of premium/gourmet product ranges | +0.5% | North America and European Union, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Convenience snack demand surge in urban megacities | +0.7% | Asia-Pacific core, North America urban, Middle East and Africa select cities | Long term (≥ 4 years) |

| Rising interest in traditional/craft bakery formats | +0.4% | European Union and North America, selective Asia-Pacific markets | Long term (≥ 4 years) |

| Clean-label and ingredient transparency concerns | +0.5% | Global, with regulatory influence from the FDA, European Union standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in healthier snacking trends

The healthier snacking trend is driving significant changes in product development within the pretzel market, influenced by regulatory updates and shifting consumer preferences. Starting February 2025, the FDA's revised "healthy" nutrient content claim imposes stricter limits on added sugars, saturated fats, and sodium, while allowing certain foods with higher healthy fats to qualify. This regulatory shift is prompting manufacturers to reformulate pretzels to align with modern nutritional science. Supporting this transition, market insights from the Specialty Food Association (SFA) reveal that in 2023, 83% of millennials and 77% of Gen Z purchased specialty foods, with a strong preference for high-protein snacks [1]Source: Institute of Food Technologists (IFT), "The Mainstream Appeal of Specialty Foods", ift.org. For example, Kindling Snacks launched protein-packed pretzels in March 2025, featuring wheat protein and chickpea flour. Additionally, the American Heart Association's Heart-Check certification is influencing product development, encouraging the use of superfood ingredients. Stellar Snacks exemplified this trend by introducing grain-free pretzel thins in August 2024, made with cassava, chickpea flour, and hemp protein. These developments highlight the alignment between stricter regulatory definitions of "healthy" and consumer demand for nutrient-rich, functional pretzel snacks. In response, pretzel brands are refining their strategies to emphasize protein enrichment, clean-label transparency, and certification endorsements. This evolving dynamic is fostering innovation in pretzel formats and ingredients while reinforcing their position in the growing better-for-you snacking category.

Innovation in pretzel flavors

Flavor innovation is becoming a critical driver of competitive advantage in the pretzel industry. Flavored and seasoned pretzels now account for over half of total sales, highlighting a strong consumer preference for diverse taste experiences. For instance, Utz attributes a 5% growth in the overall category in 2024 to its flavored pretzel innovations, demonstrating the significant market impact of bold flavors [2]Source: Utz Brands, Inc., "UTZ 2024 Annual Report", investors.utzsnacks.com. Additionally, PepsiCo's October 2023 introduction of Cheetos Flamin’ Hot Pretzels, which combines the iconic Cheetos flavor with pretzel textures, further illustrates this trend, appealing to adventurous consumers. Moreover, regional preferences are also fueling localized innovations, with unique spice profiles such as Korean gochujang, Middle Eastern za’atar, and Latin American tajín showcasing a global shift toward culturally inspired tastes. These flavor choices not only evoke nostalgia but also deliver novel, sensory-rich experiences, particularly resonating with younger generations seeking intense, multi-dimensional flavors. In a fragmented market where craveability is paramount, this trend not only helps brands stand out on shelves but also aligns with evolving consumer demand for spirited snacks, driving category growth and expanding global appeal.

Convenience snack demand surge in urban megacities

The increasing demand for convenient snacks in urban megacities is driving significant changes in the pretzel market. This shift is fueled by evolving consumption patterns and rapid urbanization. Notably, three-quarters of consumers report snacking as a meal replacement at least once a week in 2023, as per the Specialty Food Association (SFA). In response, companies are developing more substantial pretzel formats, aligning with findings from the Institute of Food Technologists in 2023. E-commerce is playing a pivotal role in enhancing urban convenience. For example, in Japan, 53.5% of households shop online, with food accounting for 21.3% of their internet spending, according to the Statistics Bureau, Ministry of Internal Affairs and Communications [3]Source: Statistics Bureau, Ministry of Internal Affairs and Communications Japan, "Statistical Handbook of Japan 2024", stat.go.jp. This trend is boosting accessibility to packaged pretzel snacks. Urban consumers, often pressed for time, are increasingly opting for packaging innovations like multipacks and boxes. These formats, the fastest-growing in the salty snacks category, offer portion control and are ideal for on-the-go consumption. Recognizing this, pretzel manufacturers are refining their product development and packaging strategies to meet the needs of urban snackers. They are focusing on combining convenience with appealing textures and flavors. Brands that successfully integrate convenient formats with consumer-preferred flavors and healthier ingredients are well-positioned to capitalize on this trend. This highlights the critical role of e-commerce and innovative packaging in driving market growth across dense metropolitan regions worldwide.

Rising interest in traditional/craft bakery formats

Consumer demand for authentic, artisanal snack experiences rooted in heritage and quality is driving significant changes in the pretzel market. This shift aligns with the increasing preference for organic, natural, and locally sourced ingredients, which are integral to traditional baking. In key regions such as Germany, Austria, and Switzerland, where pretzels hold deep cultural significance, sales of both soft and crunchy varieties are on the rise. Leading companies like PepsiCo are expanding their product portfolios to include artisanal and specialty pretzel lines, catering to evolving consumer preferences. Simultaneously, smaller brands such as Martin’s Handmade Pretzels are gaining traction by offering premium, differentiated products. The emphasis on traditional baking methods and ingredient transparency complements broader health-conscious trends, including gluten-free and whole-grain options. Retail expansion and the growth of e-commerce platforms are further enhancing the availability of these specialty products, driving global market penetration. This combination of authenticity, quality, and convenience is fostering innovation in packaging and flavor development, enabling brands to balance tradition with modern consumer expectations. The craft bakery movement is thus emerging as a key cultural and commercial driver, delivering authenticity-driven differentiation that resonates across markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sodium-content regulations tightening in EU and Canada | -0.4% | European Union, Canada, with spillover to export markets | Short term (≤ 2 years) |

| Volatile wheat prices squeezing mid-size bakers' margins | -0.6% | Global, particularly affecting smaller manufacturers | Medium term (2-4 years) |

| Competitive pressures from alternative salty snacks | -0.5% | Global, with intensity highest in North America and Europe | Medium term (2-4 years) |

| Complexity in logistics for fresh product distribution | -0.3% | Global, with acute challenges in rural and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sodium-content regulations tightening in European Union and Canada

Pretzel manufacturers in the European Union and Canada are facing significant challenges due to tightening sodium-content regulations, leading to costly reformulations and compliance efforts. Starting January 1, 2026, Canada’s front-of-package nutrition symbol requirements will mandate warning labels on prepackaged foods, including pretzels, that exceed 15% of the Daily Value for sodium. This move, highlighted by the Canadian Food Inspection Agency, could shift consumer perceptions. Meanwhile, the WHO European Salt Action Network, representing 23 countries, is pushing for unified salt-reduction initiatives, noting that 70-75% of Europe's salt intake comes from processed foods, snacks like pretzels included. Adding to the complexity, EU Regulation 2023/915 sets maximum contaminant limits for bakery products, addressing mycotoxins and heavy metals. This regulation directly influences pretzel raw material sourcing and product compliance. As a result of these regulatory pressures, manufacturers face heightened reformulation costs, stringent testing protocols, and potential market access challenges if sodium limits are breached. Smaller manufacturers, with limited research and development resources, feel this burden more acutely. In response, pretzel companies are innovating sodium-reduction strategies, striving to uphold taste and texture while meeting regulatory demands and consumer flavor expectations. This shifting regulatory landscape marks a significant turn in the industry, emphasizing health-driven compliance in product development and competitive strategy. Brands adeptly navigating this terrain, perhaps through salt substitutes or ingredient innovations, stand to benefit in European and Canadian markets, which are becoming increasingly cautious of high-sodium foods.

Volatile wheat prices squeezing mid-size bakers’ margins

Mid-sized pretzel manufacturers, lacking the purchasing power and hedging capabilities of industry giants, are struggling with volatile wheat prices that continue to compress their margins. While the USDA forecasts wheat prices to decline to USD 5.30 per bushel for 2025/26, below the 16-year average of USD 5.99, supply chain disruptions are intensifying cost pressures. Manufacturers are dealing with logistics challenges, including inadequate distribution resilience, fluctuating monthly shipment volumes, and complex picking processes. In response, the USDA is engaging third-party logistics firms to address these issues. Mid-sized bakers, such as regional players like Uncle Jerry’s Pretzels, are facing rising input costs and logistics uncertainties, which are affecting their pricing strategies and profitability. These businesses are contending with input cost variability and stringent regulatory requirements, but lack the scale to absorb these expenses effectively. This creates a challenging operational environment, making it increasingly difficult to balance quality, compliance, and cost control. As wheat price volatility and distribution inefficiencies persist, mid-sized players are seeing their growth prospects constrained. This highlights the critical need for strategic sourcing and operational agility to remain competitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Soft Pretzel Innovation Accelerates Growth

Hard pretzels maintain a leading 56.62% share in 2025, driven by their extended shelf life, convenience, and strong distribution networks across retail channels. Their durability supports efficient storage and transportation, making them particularly appealing in regions with limited access to fresh products. In comparison, soft pretzels are poised for faster growth, with a projected 5.02% CAGR from 2026 to 2031. This growth is fueled by the expansion of premium positioning strategies. J&J Snack Foods exemplifies this trend with its April 2025 reformulation of SUPERPRETZEL, featuring a bolder Bavarian-style flavor and softer texture while maintaining a vegan formulation and national freezer distribution. Additionally, the company’s Brauhaus Pretzel launch targets the artisanal segment with premium positioning, involving a labor-intensive production process exceeding eight hours and a higher price point of USD 6.99 for 4-count packs in 2024.

The soft pretzel segment benefits from versatile flavor applications and pairing opportunities with mustards, cheeses, and beverages, which gain particular traction during seasonal promotions like Oktoberfest. This versatility enhances premiumization and consumer engagement across retail and foodservice settings globally. Moreover, compliance with FDA sodium reduction guidelines may favor soft pretzels due to their typically lower sodium content compared to heavily seasoned hard pretzel varieties, aligning with healthier snack positioning. These factors collectively strengthen the appeal and growth potential of soft pretzels, balancing traditional snack enjoyment with evolving consumer preferences for premium, flavorful, and healthier options in the market.

By Content: Unsalted Variants Gain Health-Conscious Consumers

Salted pretzels hold a commanding 80.74% share of the market in 2025, reflecting strong consumer loyalty to traditional flavor profiles and well-established brand offerings. The segment's dominance is further reinforced by the success of seasoned pretzel launches. For instance, Utz has reported that flavored pretzels now contribute to over 50% of their sales, driving a 5% growth in the category during 2024. In comparison, unsalted pretzels are witnessing significant momentum, with a 5.41% CAGR projected through 2031. This growth is fueled by increasing health-conscious consumer behavior and regulatory initiatives targeting sodium reduction. For instance, Whole Foods Market's 365 brand exemplifies this trend with its organic unsalted mini pretzel twists, made from simple ingredients such as organic wheat flour and organic expeller-pressed soybean oil.

The FDA's Phase II voluntary sodium reduction targets, which aim to lower average U.S. sodium intake to approximately 2,750 mg per day, are driving manufacturers to innovate with lower-sodium alternatives. Additionally, Canada's front-of-package nutrition symbol requirements, effective January 2026, will mandate warning labels on products exceeding 15% of the Daily Value for sodium, potentially accelerating the adoption of unsalted variants. The unsalted segment also benefits from its pairing versatility, enabling consumers to manage sodium intake through dip selection and portion control.

By Ingredient Claim: Free-From/Organic Segment Captures Premium Positioning

Conventional pretzels hold a dominant 73.86% share of the market in 2025, leveraging established supply chains, competitive pricing, and widespread consumer acceptance. Their affordability and accessibility solidify their status as the go-to choice for daily snacking. In contrast, the free-from/organic segment is on a rapid ascent, boasting a 5.24% CAGR, driven by a surge in consumer appetite for clean-label products that align with specific dietary needs. This segment's momentum mirrors a broader health consciousness trend, with consumers gravitating towards pretzels devoid of artificial additives, gluten, or those boasting organic credentials. Brands such as Real Food From The Ground Up and Quinn Foods are seizing this opportunity, rolling out certified organic and allergen-friendly pretzel options, thereby carving a niche in the premium market.

Moreover, the free-from/organic segment resonates with consumers prioritizing sustainability and ethical sourcing, amplifying its allure among eco-conscious shoppers in both developed and emerging markets. This evolving landscape is spurring product innovations, introducing claims like vegan, non-GMO, and whole grain, further distinguishing the segment. Enhanced accessibility of these premium pretzels is bolstered by e-commerce platforms and specialty food retailers. As the free-from/organic segment outpaces conventional pretzels in growth, it reshapes market dynamics, urging mainstream brands to roll out healthier, cleaner options while still leading in cost within the traditional segment. This dual growth trajectory not only boosts volume but also enhances value, paving the way for sustainable expansion in the global pretzel arena.

By Packaging Format: Containers Drive Convenience Innovation

Bags hold a dominant 62.88% market share in 2025, driven by cost efficiency, consumer familiarity, and optimal shelf space utilization across retail channels. Traditional bag formats remain a preferred choice for family-size purchases and bulk consumption occasions. However, containers are witnessing the fastest growth at a 5.08% CAGR through 2031, fueled by convenience and premium positioning strategies. The container format meets consumer demand for resealability, portion control, and product protection, which are particularly significant for premium and artisanal pretzel varieties. Industry data indicates that multipacks and boxes represent the fastest-growing packaging format in salty snacks, reinforcing the container trend.

In 2025, Campbell's Snack Factory Pop'ums introduced resealable 9-ounce bags, highlighting hybrid packaging approaches that merge convenience with traditional formats. Box formats are gaining popularity for gift and premium positioning, with companies leveraging seasonal promotions and variety pack configurations. The container segment also benefits from the growth of e-commerce, where protective packaging reduces shipping damage and enhances the unboxing experience for direct-to-consumer sales. Sustainability considerations are shaping packaging innovation, with companies exploring recyclable and reduced-plastic container options to align with environmentally conscious consumer preferences.

By Distribution Channel: Online Retail Transforms Market Access

Supermarkets/hypermarkets dominate the market in 2025, holding a 51.35% share by leveraging extensive shelf space, strong promotional capabilities, and established consumer shopping patterns for grocery purchases. These channels capitalize on impulse buying opportunities and cross-merchandising strategies, pairing complementary products like dips and beverages. However, online retail stores are witnessing the fastest growth, with a 4.87% CAGR projected through 2031, fundamentally transforming market access and consumer purchasing behavior. E-commerce penetration is particularly strong in developed markets, with 53.5% of Japanese households ordering goods online and food representing 21.3% of internet spending in 2024, according to the Statistics Bureau, Ministry of Internal Affairs and Communications. The online channel facilitates direct-to-consumer strategies, subscription models, and access to niche products that may not achieve retail distribution. Companies like Stellar Snacks are utilizing online platforms for national expansion, offering products through stellarsnacks.com and forming airline partnerships with Southwest, Alaska, and Emirates.

Convenience stores continue to perform steadily, particularly in urban areas where grab-and-go consumption patterns drive demand for single-serve pretzel formats. Specialty stores cater to the premium and artisanal segment, offering curated selections and expert recommendations for gourmet pretzel varieties. The growth of the online channel is supported by advancements in logistics, with companies addressing last-mile delivery challenges and ensuring cold-chain requirements for fresh pretzel products.

Geography Analysis

In 2025, North America captures a significant 37.89% share of the market, driven by established consumption patterns, an extensive distribution network, and continuous product innovation from leading players such as PepsiCo, Campbell Soup, and Utz Brands. Recent product launches, including J&J Snack Foods' Brauhaus Pretzel artisanal line and PepsiCo's Cheetos Flamin' Hot Pretzels, highlight the market's vitality, leveraging established brand equity to drive category growth. Regulatory developments, such as the FDA's Phase II voluntary sodium reduction targets in 2024, are influencing market dynamics by encouraging reformulations that reduce sodium content while preserving taste. The mature nature of the market enables companies to implement premium positioning strategies, with higher-priced artisanal and organic variants appealing to value-conscious consumers.

Asia-Pacific is positioned as the fastest-growing region, with a projected 4.58% CAGR through 2031, supported by increasing disposable incomes, urbanization, and the adoption of Western snacking habits among younger demographics. Japan offers a notable growth opportunity despite its dependency on wheat imports and global commodity markets. The country's demographic trends, including 38.1% one-person households and 29.1% of the population aged 65+, favor single-serve and convenience formats in 2024 that align with pretzel offerings, as reported by the Statistics Bureau of Japan. Meiji's launch of Hello Panda Pretzel in October 2024, backed by a USD 28 million investment in U.S. production capacity, underscores Japanese companies' commitment to expanding their presence in the pretzel market. E-commerce penetration further supports market development, with online grocery platforms serving as a key channel for packaged snacks and providing access to premium imported varieties.

Europe continues to experience steady growth despite regulatory challenges. The European Salt Action Network, comprising 23 member countries, is driving harmonized sodium reduction initiatives across the region. The focus on artisanal and traditional bakery formats aligns with the cultural heritage of pretzels, particularly in Germany, where they hold significant local authenticity. Compliance with EU Regulation 2023/915, which establishes maximum contaminant levels for bakery products, promotes quality standardization across member states while presenting compliance challenges. Additionally, the withdrawal of eight smoke flavorings from EU markets may require reformulations for certain seasoned pretzel varieties to maintain flavor profiles while adhering to regulatory requirements.

Competitive Landscape

Established players like Campbell Soup Co., PepsiCo, and Utz Brands leverage their vast distribution networks, strong brand recognition, and manufacturing scale to maintain dominance in the moderately consolidated pretzel market. These industry leaders bolster their market share through investments in product innovation, strategic partnerships, and operational efficiencies. On the other hand, emerging brands carve out niche segments, emphasizing artisanal quality, clean-label formulations, and direct-to-consumer sales. They tap into the growing consumer demand for authenticity and transparency. Flavor innovation and premium positioning stand out as key strategies, with companies broadening their offerings from traditional salted pretzels to a range of sophisticated flavors, catering to the appetite for indulgence and variety.

Companies are increasingly turning to technology as a competitive advantage, investing in proprietary manufacturing processes and automation to ensure consistent quality and lower production costs. A prime example is Pretzelized, which employs custom-built machinery to craft hybrid snacks like pretzel-crackers and pretzel-pita chips, boasting a first-mover advantage in these new categories. The confidence in the pretzel market's long-term growth is evident in manufacturing capacity expansions. Stellar Snacks, for instance, inaugurated a USD 137 million facility in Kentucky in November 2024, benefiting from state-supported enhancements like rail spurs and flour piping systems, which elevate both operational efficiency and sustainability.

Health-focused formulations present a wealth of opportunities, with protein-enhanced and grain-free pretzels gaining momentum among health-conscious consumers. The American Heart Association's Heart-Check certification program is influencing product development, urging companies to uphold nutritional standards without sacrificing flavor. While regulatory pressures on sodium reduction pose challenges, they also present opportunities, often benefiting firms with advanced research capabilities. In contrast, smaller players may struggle with the complexities of compliance. These dynamics underscore a vibrant, innovation-driven landscape in the pretzel market, setting the stage for continued growth and diversification.

Pretzel Industry Leaders

-

PepsiCo, Inc.

-

Campbell Soup Company

-

Utz Brands Holdings, LLC

-

Intersnack Group GmbH & Co. KG

-

Roark Capital Group (Auntie Anne's)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Snyder's of Hanover introduced its Pretzel Pieces to the United Kingdom market, offering four flavors: Cheddar Cheese, Honey Mustard and Onion, Hot Buffalo Wing, and Jalapeño. Each 110g bag retailed for GBP 2.50.

- April 2025: Reese’s Filled Pretzels, a product introduced by The Hershey Company, entered the United States market. This product combined the brand's signature peanut butter with a crispy pretzel exterior. Reese’s Filled Pretzels were made available in three convenient pack sizes: 5-ounce bags suited for on-the-go consumption, 9-ounce pouches for personal indulgence, and 18-ounce jars designed for sharing.

- February 2025: Guinness partnered with Farmer Companies to introduce a new line of pretzel pieces. These pretzels were launched in four flavors: original pub style, pub style cheese, caramelized onion, and dry stout barbecue. Consumers could purchase these pretzels at Publix, Price Chopper, and Shaw's.

Global Pretzel Market Report Scope

Pretzel is a dough-based, baked bread food product, which is usually twisted knot shaped, crisp, and brittle in nature. The global pretzel market is segmented based on type and distribution channel. On the basis of product type, the market is segmented into salted and unsalted, and the distribution channel is segmented into hypermarkets/supermarkets, convenience stores, food specialty stores, online channels, and other distribution channels. The report also covered a detailed geographical analysis, which includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Hard Pretzels |

| Soft Pretzels |

| Salted Pretzels |

| Unsalted Pretzels |

| Conventional |

| Free-From/Organic |

| Bags |

| Boxes |

| Containers |

| Others |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hard Pretzels | |

| Soft Pretzels | ||

| By Content | Salted Pretzels | |

| Unsalted Pretzels | ||

| By Ingredient Claim | Conventional | |

| Free-From/Organic | ||

| By Packaging Format | Bags | |

| Boxes | ||

| Containers | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the pretzel market in 2026?

The pretzel market size is USD 7.95 billion in 2026 and should climb to USD 9.49 billion by 2031.

Why are unsalted pretzels gaining momentum?

Regulatory sodium targets and consumer wellness goals push demand, giving unsalted variants a 5.41% CAGR outlook.

Which sales channel is expanding quickest?

Online retail delivers a 4.87% CAGR as e-grocery platforms, direct-to-consumer sites, and subscription boxes widen product reach.

What regions present the strongest future growth?

Asia-Pacific posts the highest regional CAGR at 4.58%, supported by urbanization, rising incomes, and flavor exploration.

Page last updated on: