Pickles And Pickle Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.18 Billion |

| Market Size (2031) | USD 18.91 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

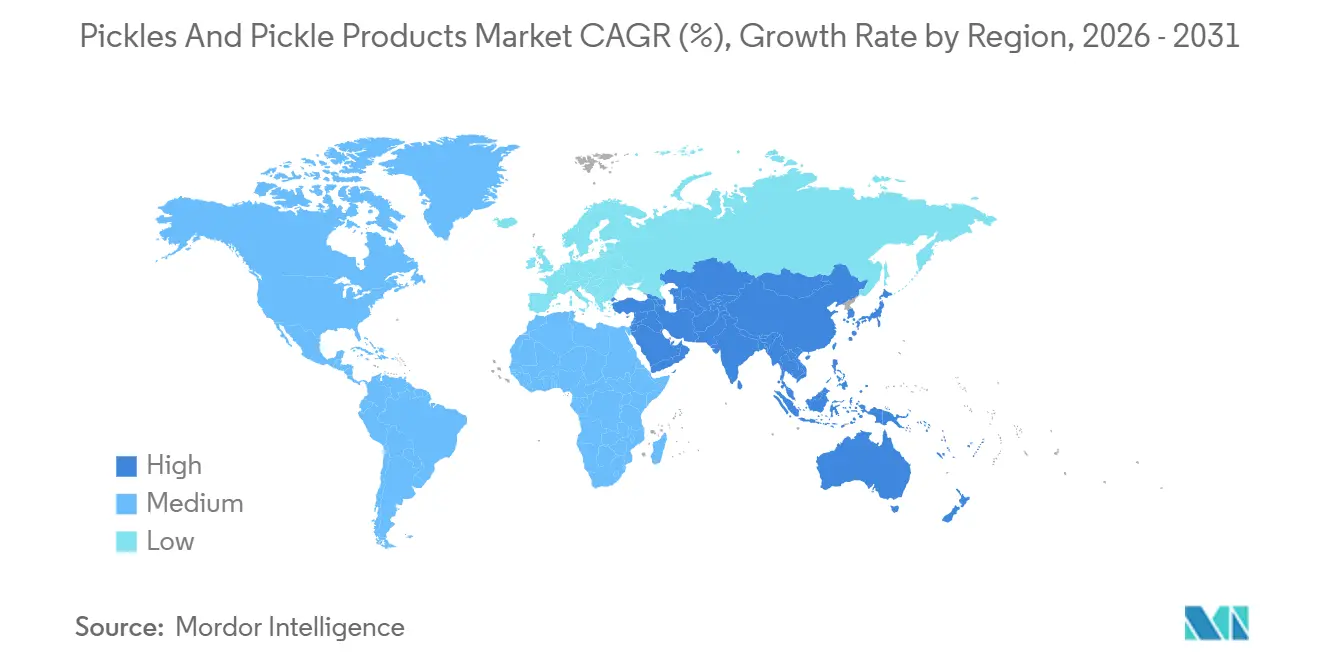

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

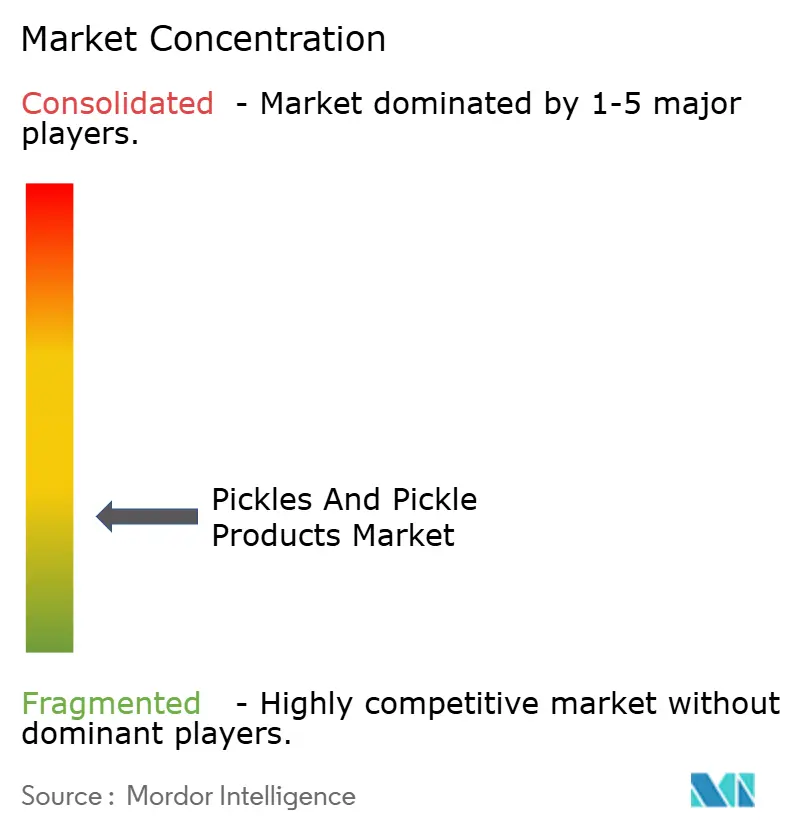

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pickles And Pickle Products Market Analysis by Mordor Intelligence

The global pickles and pickle products market size was valued at USD 14.61 billion in 2025 and is projected to grow from USD 15.18 billion in 2026 to USD 18.91 billion by 2031, registering a CAGR of 4.49% during the forecast period (2026–2031). This growth is driven by increasing consumer interest in fermented food products, rising demand for clean-label formulations, and ongoing flavor innovations, which collectively enhance inventory turnover in retail channels. Government export programs are also bolstering manufacturing capabilities, particularly among emerging producers. Leading market players are focusing on recyclable packaging solutions and expanding their digital retail presence to reduce distribution timelines and improve market accessibility. While regional taste preferences vary, social media platforms are significantly influencing global flavor trends and amplifying promotional efforts. Furthermore, companies are targeting higher-value segments by emphasizing organic certifications, functional benefits, and exclusive limited-edition product launches to meet premium consumer demand.

Key Report Takeaways

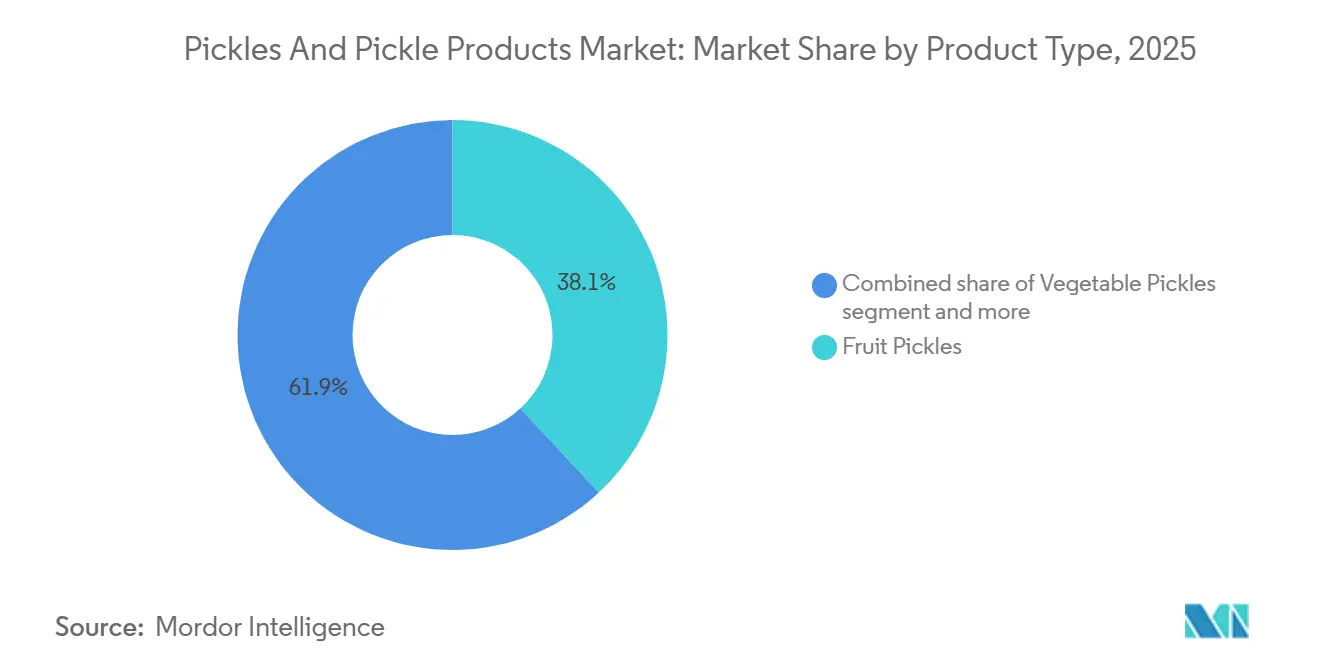

- By product type, fruit pickles held 38.09% of the pickle and pickle products market share in 2025, whereas vegetable pickles are set to expand at a 4.59% CAGR through 2031.

- By packaging type, glass jars accounted for 45.10% of the pickle and pickle products market size in 2025, while stand-up pouches are projected to advance at a 4.81% CAGR through 2031.

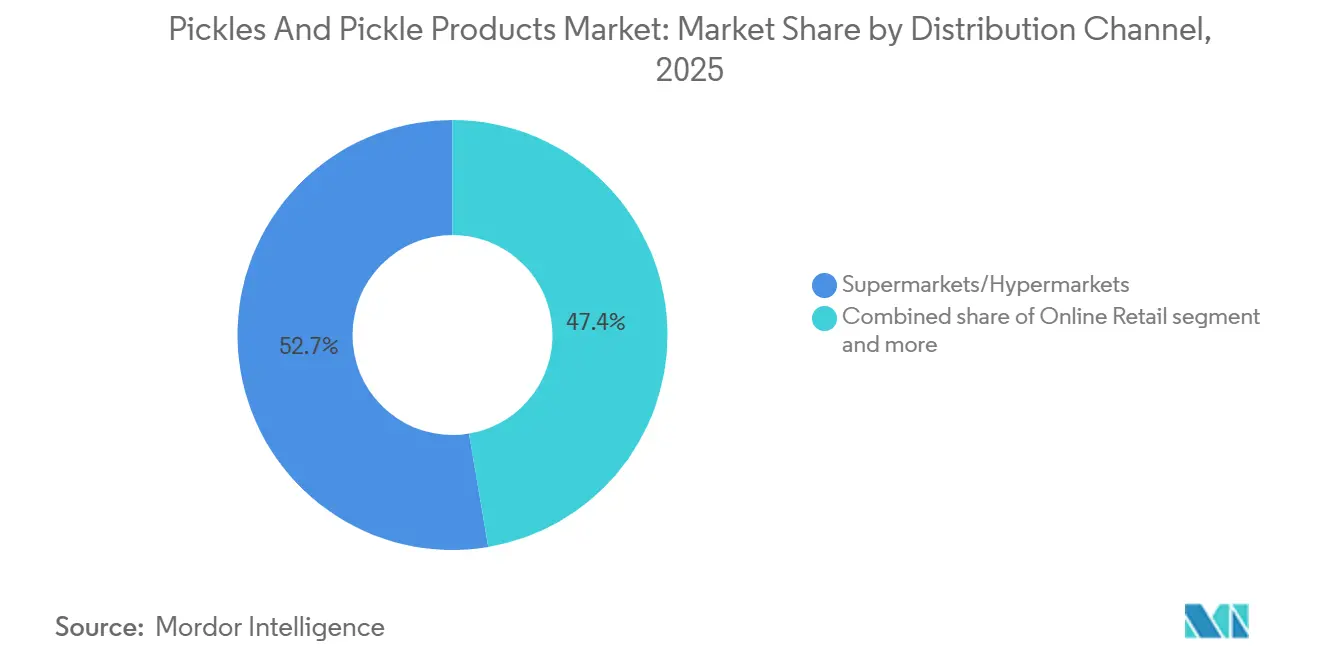

- By distribution channel, supermarkets/hypermarkets captured 52.65% of 2025 revenue, yet online retail is projected to post a 5.97% CAGR during the forecast period.

- By geography, Asia-Pacific accounted for 43.92% of 2025 sales and is predicted to grow at a 5.01% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pickles And Pickle Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing preference for fermented and probiotic foods | +0.8% | Global, with strongest uptake in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Clean label, organic, Non-GMO, and minimal ingredient focus | +0.7% | North America and European Union (EU) core, expanding to Australia and Japan | Long term (≥4 years) |

| Export incentives for Indian pickle SMEs | +0.4% | National (India), with spillover gains in Middle East, North America, and United Kingdom | Short term (≤2 years) |

| Rising demand for bold, diverse, and ethnic flavors | +0.6% | North America and Western Europe, with emerging interest in Latin America | Medium term (2-4 years) |

| Product innovation and premiumization | +0.5% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Cultural and traditional consumption patterns | +0.3% | Asia-Pacific core (India, Japan, Korea, China), with diaspora influence in North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing preference for fermented and probiotic foods

The increasing consumer preference for fermented and probiotic-rich foods is a key driver of the global pickles and pickle products market. As awareness of digestive health and the gut microbiome grows, consumers are seeking food products that provide functional health benefits in addition to basic nutrition. Fermented pickles, especially those made through natural lactic acid fermentation, are increasingly viewed as beneficial for gut health, digestion, and overall immunity. This shift toward functional eating habits is elevating pickles from a traditional condiment to a health-oriented food category. Health-conscious consumers are focusing on products that support digestive wellness, driving demand for probiotic-containing foods. By 2024, approximately 36% of consumers in the United States preferred food products linked to digestive or gut health, highlighting a significant market segment seeking such benefits [1]Source: International Food Information Council, "2024 IFIC Food & Health SURVEY", ific.org. This trend aligns with the growing popularity of naturally fermented pickles, which are valued for their beneficial bacteria when minimally processed and free from artificial preservatives. As digestive health remains a central focus of global wellness trends, the demand for fermented and probiotic foods is expected to support sustained growth in the pickles and pickle products market.

Clean label, organic, non-GMO, and minimal ingredient focus

Consumer preference for clean-label, organic, Non-GMO, and minimally processed foods is a key driver of growth in the global pickles and pickle products market. Modern consumers are increasingly scrutinizing ingredient lists, avoiding artificial preservatives, synthetic additives, excessive sodium, and chemical stabilizers. Since pickles are traditionally made with simple ingredients such as vegetables, salt, spices, oil, or vinegar, the category aligns well with clean-label expectations when manufacturers prioritize transparency and authenticity. This trend is particularly prominent among younger demographics. By 2025, Gen Z and Millennial shoppers were willing to pay 20–30% more for products labeled as organic, natural, high protein, or free from artificial ingredients [2]Source: Ingredion, "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com . This willingness to pay a premium creates significant revenue opportunities for pickle manufacturers that reformulate products using organic-certified vegetables, Non-GMO ingredients, and reduced additives. Consequently, brands are increasingly introducing small-batch, preservative-free, and minimally processed variants to target higher-margin market segments.

Export incentives for Indian pickle SMEs

Export incentives and government-supported export enablement programs are becoming key growth drivers for the global pickle and pickle products market, particularly aiding Indian small and medium-sized enterprises (SMEs). India ranks among the largest producers and exporters of pickles, driven by robust agricultural output, diverse regional recipes, and consistent demand from diaspora and international markets. Government initiatives to boost agri-food exports are enhancing production capacity, improving compliance with international standards, and facilitating global market access for pickle manufacturers. One such initiative is Bharati (Bharat’s Hub for Agritech, Resilience, Advancement, and Incubation for Export Enablement), which aims to support 100 agri-food and agri-tech startups by fostering growth, promoting innovation, and creating export opportunities for young entrepreneurs. Developed under APEDA’s vision to achieve USD 50 billion in agri-food exports for its Scheduled Products by 2030, Bharati represents a strategic effort to strengthen India’s agricultural and processed food export ecosystem [3]Source: APEDA, "APEDA launches Bharati initiative to boost agri-food exports", apeda.gov.in. As pickles are categorized under processed food products with high export potential and long shelf life, SMEs in this segment are well-positioned to leverage these export-focused programs.

Rising demand for bold, diverse, and ethnic flavors

The growing consumer preference for bold, diverse, and ethnically inspired flavors is a key factor driving the global pickle and pickle products market. As consumers increasingly seek adventurous taste experiences, there is a rising demand for flavors that are spicy, tangy, smoky, fermented, and region-specific. Pickles cater to this demand with their strong flavor profiles, regional authenticity, and versatility in complementing various cuisines. Globalization, exposure to international travel, cross-cultural dining experiences, and the influence of digital food content have accelerated the adoption of ethnic flavors beyond their traditional origins. Social media platforms and food influencers are introducing consumers to products such as Korean kimchi, Indian mango and lime pickles, Middle Eastern preserved vegetables, Southeast Asian spicy relishes, and Latin American escabeche-style pickles. This cultural exchange is driving the demand for regional pickle varieties in mainstream retail markets. Younger demographics, particularly Millennials and Gen Z, are leading this trend, showing a greater willingness to experiment and incorporate global flavors into their daily meals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sodium-reduction regulations tighten | -0.5% | North America and European Union, with emerging pressure in Australia and Japan | Short term (≤2 years) |

| Volatility in raw materials (vinegar, spices) prices | -0.4% | Global, with acute impact in India, China, and Southeast Asia | Short term (≤2 years) |

| Limited shelf life and spoilage issues | -0.3% | Global, particularly in regions with underdeveloped cold-chain infrastructure | Medium term (2-4 years) |

| Competition from alternative condiments and spreads | -0.4% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sodium-reduction regulations tighten

Public health agencies are increasing efforts to reduce sodium levels in processed foods, posing a challenge to traditional pickle formulations that depend on high-salt brines for preservation and flavor. The U.S. Food and Drug Administration's voluntary sodium-reduction targets for 2024 recommend reducing sodium in pickles to 300 milligrams per serving, compared to the current average of 450-600 milligrams. These guidelines require manufacturers to invest in reformulation research and development, often involving the substitution of sodium chloride with alternatives like potassium chloride or calcium chloride. However, these substitutes can introduce bitter or metallic flavors, potentially deterring consumers. Small and medium enterprises face additional challenges, as they often lack the resources for sensory testing and shelf-life validation, leaving them vulnerable to losing market share to larger competitors with dedicated food science capabilities.

Volatility in raw-material (vinegar, spices) prices

Fluctuations in commodity prices for key inputs pose a risk to margin stability, particularly for producers lacking vertical integration or effective hedging strategies. In March 2025, turmeric prices in India rose to INR 18,500 per quintal (USD 220), reflecting a 22% increase compared to the previous year. This surge was primarily attributed to below-average monsoon rainfall in Andhra Pradesh and Telangana, the main turmeric cultivation regions. These rising costs have a significant impact on small pickle manufacturers in India and Southeast Asia, which operate with narrow margins and lack the financial capacity to secure long-term contracts. In contrast, larger companies such as The Kraft Heinz Company and Conagra Brands manage price volatility through forward contracts and diversified sourcing strategies. However, passing these costs on to consumers could lead to reduced sales volumes in price-sensitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetable Pickles Outpace Fruit Despite Smaller Base

Fruit pickles accounted for a 38.09% market share in 2025, driven by popular varieties such as mango, lime, and mixed-fruit, which are staples in South Asian and Middle Eastern cuisines. In contrast, vegetable pickles are expected to grow at a faster rate, with a projected CAGR of 4.59% through 2031. This growth is supported by innovations in low-sodium cucumber formulations and the increasing popularity of fermented vegetable medleys among health-conscious Western consumers. Within the vegetable category, cucumber pickles, the largest subcategory, are benefiting from collaborations between growers and processors to develop brine-tolerant, high-yield cultivars that reduce input costs and enhance product consistency.

Meat pickles, a niche segment primarily found in Central Europe and parts of Asia-Pacific, are experiencing modest growth as charcuterie boards and grazing platters gain traction in North American restaurants and home settings. Seafood pickles, including products like pickled herring and octopus, remain regionally concentrated in Scandinavia and Japan. However, they are beginning to attract interest from adventurous consumers in urban U.S. markets, with specialty retailers such as Whole Foods dedicating endcap space to imported Swedish and Japanese seafood pickles. Relishes, which bridge the pickle and condiment categories, are undergoing premiumization as brands introduce organic, small-batch options featuring heirloom tomatoes and artisanal spices.

By Packaging Type: Stand-Up Pouches Gain Ground on Convenience

Glass jars accounted for 45.10% of packaging volume in 2025, driven by consumer perceptions of glass as a premium, inert, and recyclable material, along with retailers' preference for transparent packaging that highlights product quality. However, stand-up pouches are growing at a CAGR of 4.81%, supported by their lighter weight, reduced breakage risk, and suitability for e-commerce fulfillment, where shipping costs and damage rates are critical factors. Brands targeting younger, on-the-go consumers are increasingly adopting single-serve pouches with resealable zippers, which command a 20-25% price premium over jar equivalents and help reduce food waste through portion control.

Plastic jars, while cost-effective, are losing market share due to sustainability concerns and retailer commitments to minimize single-use plastics. Major European grocers, such as Tesco and Carrefour, are phasing out non-recyclable PET containers by 2027. The "Others" category, which includes cans and tubs, primarily serves institutional and foodservice channels, where bulk formats and extended ambient shelf life are prioritized over consumer appeal. Cans are particularly common in military and emergency-preparedness applications, where multi-year shelf stability is essential.

By Distribution Channels: Online Retail Surges as Supermarkets Consolidate

Supermarkets/hypermarkets accounted for 52.65% of the distribution share in 2025, supported by high foot traffic, promotional pricing strategies, and the ability to cross-merchandise pickles with deli meats, cheeses, and sandwich ingredients. Online retail stores are growing at a CAGR of 5.97%, driven by subscription models, direct-to-consumer brands, and the convenience of home delivery. Convenience and grocery stores, while holding a smaller market share, play a significant role in impulse purchases and fill-in trips, particularly for single-serve pickle snacks and pickle-flavored chips that blur traditional category boundaries.

Dollar stores and discount chains are expanding their pickle assortments to appeal to price-sensitive consumers, often offering private-label or secondary brands at discounts of 30-40% compared to national brands. The "Other Distribution Channels" segment, which includes farmers' markets, food trucks, and direct farm sales, is experiencing the fastest growth in percentage terms, fueled by consumer interest in locally sourced, small-batch pickles that support regional agriculture and reduce food miles.

Geography Analysis

Asia-Pacific dominates the global pickle market with a 43.92% share in 2025 and demonstrates the highest regional growth at 5.01% CAGR through 2031. India leads the region's expansion, with pickle exports surpassing USD 200 million in 2023, a 15% increase supported by government programs including the PMFME scheme (Rs. 10,000 crore allocation) and PLISFPI (Rs. 10,900 crore funding). China exhibits robust domestic consumption growth driven by urbanization and rising disposable incomes, while Japan and South Korea enhance the premium segment through traditional fermentation methods. The region leverages advantageous raw material costs, agricultural supply chains, and government export initiatives. APEDA's support has led to a 47.3% increase in India's fruit and vegetable exports from 2019-20 to 2023-24, strengthening infrastructure and quality capabilities for pickle exporters.

North America maintains a mature market position, with the United States pickle segment influenced by social media trends and product innovation. The region shows strong premiumization, as consumers opt for higher-priced artisanal, organic, and innovative flavors. Canada benefits from US distribution networks while maintaining distinct regulatory standards. North American manufacturers excel in packaging innovation, exemplified by Berry Global's recyclable solutions. FDA sodium reduction guidelines influence product development, requiring reformulation while creating opportunities for health-focused products. The region's developed retail infrastructure and high e-commerce adoption support new product launches and direct-to-consumer distribution.

Europe's pickle and pickle products market continues to grow annually, with Germany leading as the largest importer and consumer. The region emphasizes organic and sustainable products, with Germany serving as Europe's primary organic food market. Key consumption markets include the UK, France, Netherlands, Belgium, and Poland, each exhibiting unique preferences for products, packaging, and flavors. Compliance with European Union organic standards and environmental packaging regulations presents challenges but also offers competitive advantages. The region's well-established retail and distribution networks support quality-focused brands with reliable supply chains. Turkey's role as a major supplier to European markets highlights the acceptance of international producers meeting quality and regulatory standards.

Regulatory Landscape

Regulation for pickles and pickle products is shaped by food safety, compositional standards, and chemical limits that vary by region, but tend to converge around acidification control, additive permissions, and residue compliance. In the United States, FDA rules for acidified foods under 21 CFR Part 114 define acidified foods as those with water activity (aw) greater than 0.85 and an equilibrium pH of 4.6 or below. Processors are expected to apply scheduled processes and maintain records to control hazards associated with low-acid ingredients that are acidified for shelf stability.

Internationally, Codex Alimentarius standards provide baseline product specifications for trade, including the Standard for Pickled Cucumbers (CXS 115-1981), which was amended in November 2024 and again in November 2025 with updates related to food additives. In the European Union, chemical compliance remains an active area, with Commission Regulation (EU) 2026/752 of 31 March 2026 updating maximum residue levels (MRLs) for specific substances under the EU framework, reinforcing the need for exporters and EU-based manufacturers to align agricultural sourcing and testing programs with evolving MRL schedules.

Competitive Landscape

The pickles market is highly fragmented, comprising multinational food conglomerates, regional specialists, and artisanal producers competing across various price points, quality levels, and distribution channels. Companies such as The Kraft Heinz Company, Conagra Brands, and Del Monte Foods utilize their scale advantages in procurement, manufacturing, and retail partnerships to maintain their positions in mainstream markets. In contrast, smaller players like Mt. Olive, Bubbies, and Pacific Pickle Works focus on differentiation through features such as probiotic functionality, organic certification, and direct-to-consumer sales models.

Market dynamics indicate a division between volume-driven incumbents prioritizing cost efficiency and shelf stability, and premium-focused disruptors emphasizing live cultures, minimal processing, and transparent sourcing. Growth opportunities are particularly evident in functional pickles offering measurable health benefits, such as those containing clinically validated probiotic strains or fortified with vitamins and minerals. Additionally, sustainable packaging solutions that align with retailer ESG commitments and consumer preferences present significant potential.

Technological advancements are influencing competitive dynamics. High-pressure processing (HPP) enables the production of shelf-stable, unpasteurized pickles that retain live cultures without requiring refrigeration. Blockchain-based traceability systems are also gaining traction, offering farm-to-fork transparency that appeals to quality-conscious consumers. Compliance with food safety standards, including HACCP and BRC Global Standards, remains essential for entry into major retail chains. These requirements create barriers to entry, favoring established players with robust quality assurance teams and audit-ready documentation systems.

Pickles And Pickle Products Industry Leaders

-

Mt. Olive Pickle Company

-

Conagra Brands Inc

-

The Kraft Heinz Company

-

ADF Foods Limited

-

Del Monte Foods Private Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product formats that bridge condiments and snacks are widening the addressable market beyond traditional jars, supported by clean-label positioning and e-commerce-friendly packaging. In February 2026, Bubbies launched clean-label, low-brine, shelf-stable pouched pickles, reflecting movement toward portable, resealable formats that fit convenience-led consumption while reducing leakage and breakage risks in online fulfillment.

Operational and packaging upgrades are also creating room for scale players and premium entrants to improve cost-to-serve while meeting retailer sustainability requirements. In February 2025, The Kraft Heinz Company implemented AI and machine learning across the Claussen pickle supply chain and reported a 12% increase in production efficiency, indicating how digital tools can support raw-material planning and throughput. Packaging circularity is becoming a differentiator as well: in July 2026, PureCycle Technologies, IPL Schoeller, and Cleveland Kitchen partnered to produce polypropylene tubs and lids for fermented foods containing 25% post-consumer recycled content, while Berry Globals work with Grillo’s Pickles on nestable, recyclable PP jars highlights how pack design can improve storage density and logistics efficiency in retail and distribution.

Recent Industry Developments

- July 2026: PureCycle Technologies partnered with IPL Schoeller and Cleveland Kitchen to produce polypropylene tubs and lids for fermented foods containing 25% post-consumer recycled content. The move increases access to food-grade recycled PP packaging for refrigerated and fermented formats, supporting brand sustainability claims while protecting product performance. It also raises competitive pressure on packaging suppliers and brands that rely on virgin plastics in tubs and lidded containers.

- September 2025: The Kraft Heinz Company announced plans to split into two independent public companies, separating a condiments and sauces-focused business from a general grocery products business, with the transaction targeted for the second half of 2026. The restructuring signals sharper category-level focus and capital allocation for condiments and adjacent segments where pickles and pickle-flavored offerings compete for shelf and promotional space. Supplier negotiations and portfolio prioritization can shift as each entity optimizes its own growth and margin playbook.

- July 2024: Berry Global partnered with Grillo’s Pickles to develop nestable, easy-open, recyclable polypropylene jars and closures designed to improve convenience and supply chain efficiency. Nestable geometry supports higher storage density in warehousing and transport, while recyclable PP aligns with retailer packaging criteria and reduces breakage versus glass in e-commerce shipments. The collaboration reinforced packaging innovation as a lever for sustainability positioning and lower distribution costs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the retail and foodservice value of pickles and related pickle products sold for consumption, counted as finished packaged goods across major regions and channels, and tracked in USD value terms.

Scope exclusions: It excludes fresh cucumbers and other fresh vegetables sold without a pickling or relish processing step, and it also excludes at-home prepared pickles that are not sold commercially.

Segmentation Overview

-

By Product Type

- Fruit Pickles

- Vegetable Pickles

- Meat Pickles

- Seafood Pickles

- Relishes

- Others (pickled nuts, and more)

-

By Pakaging Type

- Glass Jars

- Plastic Jars

- Stand-up Pouches

- Others (Cans and Tubs)

-

By Distribution Channels

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Netherlands

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the supply and demand context for packaged pickles by country and then aligning it with how products are labeled and sold. We mainly use public sources such as USDA and ERS food outlook data, FAOSTAT food balance and crop series, UN Comtrade trade flows, and national statistics offices for CPI and food category consumption.

To avoid relying on one lens, we also cross-check with company annual reports, investor presentations, and reputable press coverage on pricing, packaging shifts, and distribution expansion. Patent databases are referenced at a high level to understand preservation and packaging activity that may affect product mix over time. For places where company splits are not directly visible, we use a paid company financials and intelligence subscription to map ownership, brand footprints, and estimated category exposure. The sources listed here are illustrative, and many other public documents and databases were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test pricing, channel mix, and what is actually counted as a pickle product in different countries. We spoke with manufacturers, ingredient and packaging participants, distributors, and retail-facing category contacts across APAC, EMEA, and the Americas so assumptions could be corrected where secondary data was silent or published with a lag.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 46% |

| Mid tier: 47% | Functional/Unit leaders: 35% | EMEA: 30% |

| Smaller Players: 14% | Managers: 51% | Americas: 24% |

Market-Sizing & Forecasting

The sizing logic starts from a top-down reconstruction where packaged pickles demand is rebuilt using country-level food category consumption signals, trade directionality, and observed retail price movements. These are then mapped to the defined product boundary. We also check the results with selective bottom-up approximations such as sampled brand-level shelf pricing and volume proxies, channel checks with distributors, and manufacturer revenue context when it can be reasonably tied back to pickles and pickle products.

Key inputs used in the model include average unit price trends by market (linked to CPI and packaging cost direction), import and export balances for pickled vegetables and related preparations, penetration of modern grocery and e-commerce in food sales, household usage versus foodservice share shifts, and mix movement across jars, tubs, and flexible packs. When bottom-up visibility is weak in fragmented markets, we fill gaps with ratio-based assumptions anchored to trade intensity and per-capita packaged food spend, then re-test the outputs through interview feedback.

For forecasting, scenario analysis is applied on top of a short trend model so the base case reflects expected price normalization, channel growth, and mix shifts. We also run conservative and upside paths when input costs or demand trends move faster than expected. Assumptions are kept transparent so each country roll-up can be repeated and reviewed without relying on hard-to-access data.

Data Validation & Update Cycle

Validation is done in layers so outliers get caught before totals are finalized. We compare outputs against independent signals like trade movements, price inflation direction, and category growth commentary from filings and retail-facing sources. Any large variance triggers a deeper review of the scope boundary or the price-volume split.

Before sign-off, the model goes through step-by-step analyst checks, including arithmetic controls, currency consistency tests, and reasonableness checks at the regional roll-up level. Reports are refreshed annually, and interim updates are made when material events occur such as major price shocks or notable regulation and labeling changes. Right before delivery, a final pass is completed so clients receive the latest updated view rather than an older draft.

Mordor Intelligence's Pickles and Pickle Products Market Estimate Compared With Other Published Estimates

Published market sizes for pickles and pickle products often do not match because the product boundary is not identical, and because price and channel assumptions are handled differently across studies. The year used as the starting point also matters since food inflation and packaging costs can swing value-based totals quickly.

By tracking scope at the product-type level and refreshing price and channel-mix assumptions through primary checks, Mordor Intelligence keeps the count focused on packaged pickles and defined pickle products rather than folding in broad fermented foods or fresh produce adjacencies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.18 B (2026) | |

| Global Consultancy A | USD 15.60 B (2024) | Uses an earlier base year and a wider category language around pickles that can include adjacent fermented items and broader ingredient bases, which can lift totals even before adjusting for inflation timing. |

| Regional Consultancy B | USD 14.94 B (2025) | Anchors the base year one year earlier than the 2026 current size and may apply different price progression choices during a high volatility period, which can compress the current-year value estimate. |

Across the three estimates, the spread is mainly explained by base-year timing and what gets counted inside the pickle-products boundary, followed by how price is carried forward year to year. Our approach makes each driver visible so the final number can be traced back to clear scope rules, price inputs, and channel weighting that can be rechecked.

Key Questions Answered in the Report

What is the current value of the pickles and pickle products market worldwide?

The pickles and pickle products market size reached USD 15.18 billion in 2026 and should advance to USD 18.91 billion by 2031.

Which region contributes the most revenue to global pickles and pickle products sales?

Asia-Pacific led with 43.92% of worldwide revenue in 2025, buoyed by strong demand in India, China, and Japan.

Which product category is growing fastest within pickle and pickle products?

Vegetable pickles are forecast to post the highest 4.59% CAGR to 2031, spurred by low-sodium, probiotic-rich launches.

How are packaging trends shifting in the pickles segment?

Stand-up pouches are gaining share at a 4.81% CAGR as brands seek lighter, shatter-proof, e-commerce-friendly solutions.

Page last updated on: