Outdoor Power Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

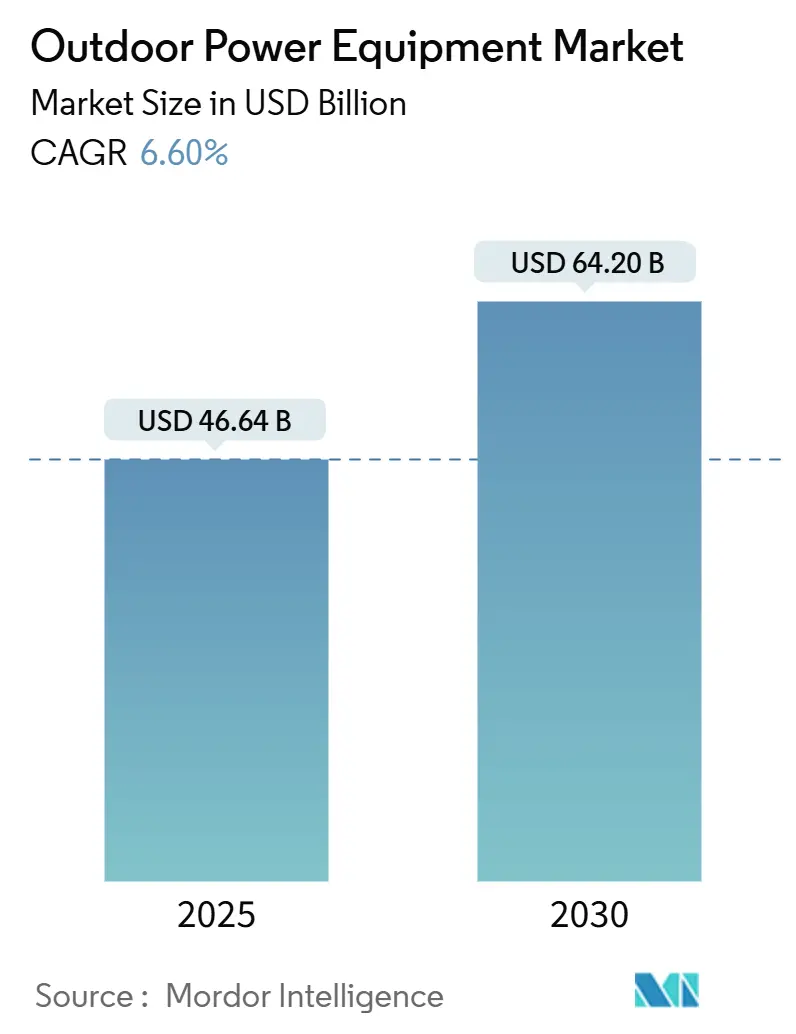

| Market Size (2025) | USD 46.64 Billion |

| Market Size (2030) | USD 64.20 Billion |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

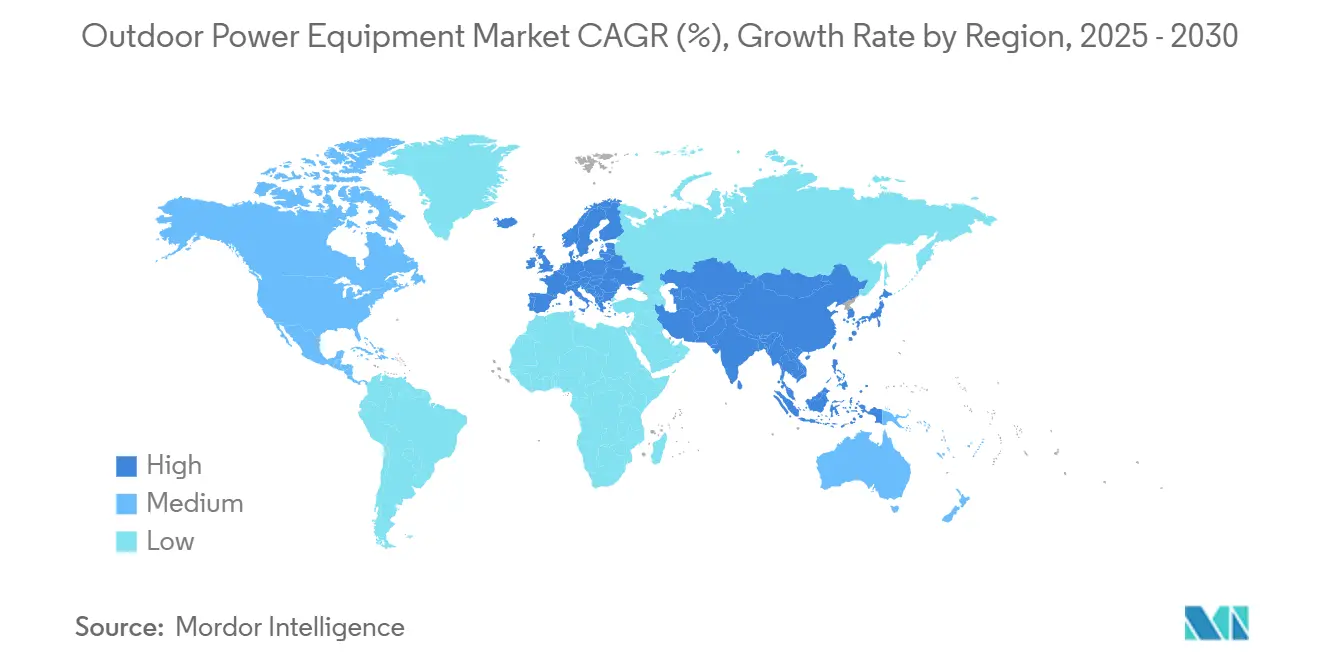

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

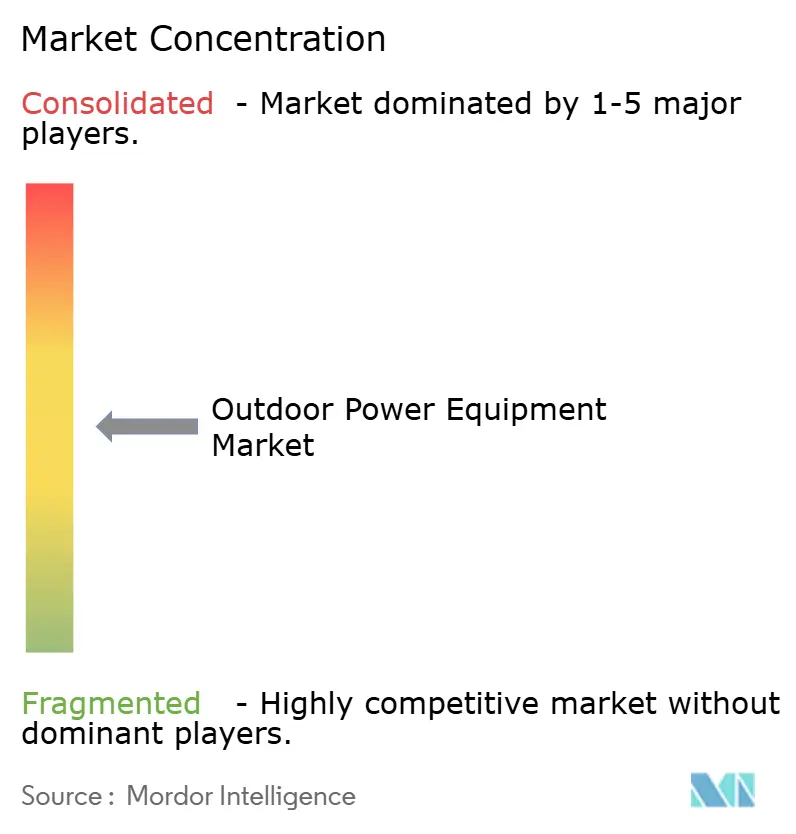

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outdoor Power Equipment Market Analysis by Mordor Intelligence

The Outdoor Power Equipment Market size is estimated at USD 46.64 billion in 2025, and is expected to reach USD 64.20 billion by 2030, at a CAGR of 6.60% during the forecast period (2025-2030).

The robust trajectory confirms solid demand fundamentals while underlining the sector’s shift from gasoline engines to battery-electric systems. Stricter emission and noise regulations, growing professional landscaping fleets, and lifestyle-driven yard care spending collectively drive revenue growth. Competitive pressure intensifies as battery platform specialists and autonomous-equipment start-ups target high-value niches, prompting incumbent manufacturers to accelerate electrification roadmaps. Meanwhile, rental penetration rises on both the contractor and homeowner fronts, enabling users to access upgraded cordless products without locking up capital.

Key Report Takeaways

- By product type, lawn mowers led with 46.0% revenue share in 2024; the segment is projected to grow at a 7.1% CAGR through 2030.

- By power source, gasoline/diesel equipment held 58.7% of the outdoor power equipment market share in 2024, while battery-electric offerings are projected to advance at an 8.9% CAGR through 2030.

- By end user, residential/homeowners accounted for 45.5% of the outdoor power equipment market size in 2024 and are expected to expand at a 7.0% CAGR through 2030.

- By geography, North America commanded 38.2% of the 2024 revenue, whereas the Asia-Pacific is projected to post the fastest 8.3% CAGR between 2025 and 2030.

Global Outdoor Power Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of cordless battery-powered OPE | 2.1% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Growing consumer spend on lawn & garden care | 1.8% | North America, Europe, emerging APAC markets | Long term (≥ 4 years) |

| Stricter global emissions & noise regulations | 1.5% | Global, led by California, EU, select APAC cities | Short term (≤ 2 years) |

| Expansion of professional landscaping services & rental fleets | 1.2% | North America, Europe, urban APAC centers | Medium term (2-4 years) |

| Municipal zero-emission fleet procurement mandates | 0.9% | North America, Europe, select APAC metropolitan areas | Short term (≤ 2 years) |

| Venture funding for autonomous robotic OPE platforms | 0.7% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cordless Battery-Powered OPE

Battery platforms built on lithium-iron-phosphate chemistry deliver runtime comparable to gasoline models while eliminating tune-ups and fuel costs that once deterred heavy users. Einhell reported its Power X-Change family generated 51% of Q1 2025 revenue, and the line will surpass 350 compatible products by year-end.(1)Einhell Germany AG, “High Demand for Power X-Change Takes Einhell’s Revenue to a Record High,” EQS-NEWS.COM Landscaping contractors have grown battery purchases from 3% in 2016 to 35% in 2022, aided by fleet standardization benefits. Municipal zero-emission mandates guarantee baseline demand, encouraging suppliers to prioritize cordless R&D. Improved energy density and falling cell costs, coupled with the promise of solid-state batteries, support acceleration beyond current forecasts.

Growing Consumer Spend on Lawn & Garden Care

Remote work and lifestyle changes reshaped discretionary budgets toward home improvement. SiteOne noted that resilient homeowner investment helped its net sales climb in 2024 despite commodity price deflation.(2)SiteOne Landscape Supply, “FY 2024 Earnings,” SITEONE.COM Rental outlets captured a share of the surge as consumers sought commercial-grade tools without ownership hassles; United Rentals projects USD 15.6-16.1 billion revenue in 2025. Millennials and Gen Z place convenience and sustainability above engine familiarity, fueling the adoption of cordless walk-behind mowers and robotic units that keep lawns trim with minimal intervention.

Stricter Global Emissions & Noise Regulations

California’s Small Off-Road Engine rules bar most new gasoline models after 2024, offering a template for peers worldwide. EU Euro 7 standards widen the scope to cover handheld tools, while urban sound ordinances compress allowable operating hours. New York, Toronto, and other cities converted their municipal fleets to battery-powered equipment, creating immediate demand for suppliers. Because regulatory timelines are shorter than typical replacement cycles, manufacturers must rapidly convert product lines to retain public-sector contracts.

Expansion of Professional Landscaping Services & Rental Fleets

Private-equity-backed rollups in landscaping services build scaled platforms that demand unified, data-rich equipment. The American Rental Association expects 8.9% rental revenue growth in 2024 and 5.3% in 2025. Contractors prefer asset-light approaches that free cash for labor and marketing, making rental houses key gateways for advanced cordless models. Construction starts are expected to rise to USD 1.277 trillion, bolstered by demand from site preparation and groundskeeping activities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront price of electric & robotic equipment | -1.3% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) |

| Runtime / power-density anxiety among heavy users | -0.8% | North America, Europe, commercial user segments | Medium term (2-4 years) |

| Intense price competition from low-cost imports | -0.6% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Lithium-ion supply constraints & trade tariffs | -0.5% | Global, with concentration in import-dependent regions | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

High Upfront Price of Electric & Robotic Equipment

Cordless handhelds can cost 40-60% more than gasoline equivalents, and autonomous mowers priced above USD 15,000 stretch smaller budgets. The premium reflects pack costs, complex electronics, and lower production scale. While raw-material swings in lithium and nickel inject cost risk, lifetime economics still tilt in favor of battery units once fuel, maintenance, and engine overhauls are factored in. The differential should narrow as cell factories reach volume and as leasing or battery-as-a-service schemes become more widespread.

Runtime / Power-Density Anxiety Among Heavy Users

Commercial crews often run equipment for multiple hours without access to charging. Lithium-ion packs currently deliver 1-3 hours of charge; output falls in cold weather, and fast chargers are not yet standard at every jobsite. Manufacturers mitigate worries through modular packs, range-extending hybrids, and telematics that pre-schedule charging windows. The wider deployment of 120-160 kWh mobile charging trailers could alleviate concerns, but until then, some high-duty buyers will likely delay full electrification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lawn-Mower Electrification Gains Share

Lawn mowers accounted for 46.0% of 2024 revenue, the largest slice of the outdoor power equipment market, and the group is projected to log a 7.1% CAGR, the fastest among all products. The lawn mower outdoor power equipment market size is set to climb swiftly as cordless walk-behind and zero-turn riders satisfy homeowners craving low-maintenance care and contractors looking to meet municipal zero-emission bids. Robotic mowers, leveraging RTK-GPS and vision systems, penetrate premium residential plots, trimming labor hours while ensuring a uniform turf appearance. Within commercial fleets, hybrid zero-turns pair battery packs with small generators, extending runtime for sports-field and campus work without breaching noise limits.

Chainsaws and pruners trail as the second-largest category, but professional arborists now use lightweight battery saws in confined spaces where fumes are a hazard. Leaf blowers are attracting sharp regulatory scrutiny; several U.S. cities plan to implement outright bans on gasoline models, accelerating the shift to high-voltage cordless turbines that meet decibel caps. Trimmers and edgers have already reached near-parity in performance, making them early adopters of battery technology. Generators and portable power stations expand beyond landscaping into emergency backup, diversifying revenue pools.

By Power Source: Battery Momentum Challenges Gasoline

Gasoline/diesel engines generated 58.7% of 2024 revenue. However, battery systems will carve away dominance as their 8.9% CAGR leads the growth league. Fleet buyers report that battery purchases have risen from 3% in 2016 to 35% in 2022. The outdoor power equipment market size for battery units benefits from LFP chemistry, which offers over 2,500 cycles, reducing the total cost of ownership below that of comparable spark-ignition engines in less than three seasons of professional duty. Corded models thrive in a niche where properties are small and outlets are plentiful. Hybrid systems combining compact engines and battery modules emerge in longer-duty municipal applications, providing stepping stones toward full electrification.

By End-User Segment: Residential Investment Stays Resilient

Homeowners booked 45.5% of 2024 revenue, and the segment is forecasted to grow at a 7.0% CAGR to 2030, maintaining the largest share of the outdoor power equipment market. The outdoor power equipment market share for residential buyers is driven by continued suburban expansion, remote work that keeps owners at home, and the influence of social media on lawn-care aesthetics. Cordless platforms simplify DIY maintenance; robotic mowers add convenience for time-starved households. Meanwhile, equipment rental services widen access to commercial-grade pieces for weekend projects.

Commercial landscaping outpaces overall growth as institutional customers outsource grounds care for malls, schools, and multi-family housing. The construction and rental industry's demand depends on infrastructure spending pipelines, and current projections show sizable capital flows that should keep order books firm. Agricultural and forestry applications require high torque and longer runtime, making gasoline and hybrid systems relevant in the medium term. Public-sector entities pivot fastest to zero-emission fleets, guaranteeing baseline battery volumes for suppliers.

Geography Analysis

North America accounted for 38.2% of 2024 sales, driven by established suburban yards, affluent homeowners, and a deeply entrenched professional contracting base. California’s phase-out of internal combustion engines accelerates battery adoption, and major metropolitan areas obligate municipal departments to procure zero-emission fleets. Retail giants, notably Home Depot and Lowe’s, are expanding their cordless assortments, while online channels are introducing price transparency. Rental houses are expanding their footprints as contractors and consumers prefer usage over ownership.

Asia-Pacific logs the fastest 8.3% CAGR through 2030. Rapid urbanization in China, India, and Southeast Asia lifts equipment penetration from low baselines. Domestic OEMs leverage cost advantages in battery cells and electronics to drive competitive pricing, yet trade frictions introduce volatility in component supply chains. Urban air quality drives local governments toward the adoption of electric equipment, although enforcement timelines vary across jurisdictions. The Japanese and South Korean markets, already mature, are pivoting toward robotic mowing solutions to counter labor shortages.

Europe combines strict environmental regulation with high disposable incomes. Euro 7 standards widen the scope across product classes, and urban sound caps compress gasoline operating windows. Professional landscaping services consolidate under private-equity umbrellas, creating scaled purchasing power that favors suppliers offering battery-fleet management software. South America and the Middle East & Africa occupy nascent positions but show upside as infrastructure investment and tourism development push demand for resort and public-space maintenance gear.

Competitive Landscape

Incumbents such as Husqvarna, STIHL, and Toro continue to command channel presence, yet the competitive field is in flux. Start-ups specializing in autonomous navigation secure venture capital; Scythe Robotics raised USD 22.8 million, and Electric Sheep secured USD 21.5 million to accelerate the commercialization of robotic mowers.(3)Scythe Robotics, “Company Information,” SCYTHEROBOTICS.COM Battery platform compatibility becomes a key differentiator: Einhell’s modular 18 V & 36 V packs power hundreds of SKUs, while Techtronic Industries posted record USD 14.6 billion sales in 2024 on the strength of its cordless ecosystem.(4)Techtronic Industries, “Annual Report 2024,” TTI.COM.HK

Channel dynamics evolve as rental giants and big-box retailers shape portfolio decisions. Home Depot expanded exclusive Ryobi lines, whereas Lowe’s leans on Toro to fill assortment gaps. Amazon gains market share in seasonal categories, prompting brick-and-mortar players to accelerate e-commerce fulfillment. Intellectual property moats shift from engine performance to battery management, software integration, and cloud-connected diagnostics.

Manufacturers allocate capital to in-house cell production, firmware upgrades, and AI-powered autonomy. White-space opportunities emerge in battery-as-a-service, predictive maintenance analytics, and turnkey charging infrastructure for municipal depots. Competitive winners will marry robust supply chains, digital capabilities, and field-service networks to meet evolving buyer expectations.

Outdoor Power Equipment Industry Leaders

Husqvarna Group

ANDREAS STIHL AG

The Toro Company

Techtronic Industries (Ryobi/Milwaukee)

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Einhell Germany AG reported a record Q1 revenue of EUR 302.8 million, with its Power X-Change line accounting for 51% of sales, and plans to expand to 350 SKUs by year-end.

- April 2025: Generac Holdings scheduled its Q1 2025 earnings release, highlighting traction in residential energy-storage and portable generation segments.

- March 2025: Home Depot deepened exclusive Ryobi partnerships, while Lowe’s leaned on Toro, amid mounting e-commerce pressure from Amazon.

- February 2025: SiteOne Landscape Supply closed seven acquisitions in 2024 and projected low-single-digit organic growth for 2025.

Global Outdoor Power Equipment Market Report Scope

| Lawn Mowers |

| Chainsaws and Pruners |

| Leaf Blowers and Vacuums |

| Garden Trimmers and Edgers |

| Generators and Portable Power Stations |

| Others (Pressure Washers, Snow Blowers, Tillers) |

| Gasoline/Diesel |

| Battery-Electric (Li-ion, LFP, Solid-State) |

| Corded-Electric |

| Hybrid and Others |

| Residential/Homeowners |

| Commercial Landscaping and Groundskeeping |

| Construction and Rental Industry |

| Agricultural and Forestry Users |

| Municipal/Government |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Lawn Mowers | |

| Chainsaws and Pruners | ||

| Leaf Blowers and Vacuums | ||

| Garden Trimmers and Edgers | ||

| Generators and Portable Power Stations | ||

| Others (Pressure Washers, Snow Blowers, Tillers) | ||

| By Power Source | Gasoline/Diesel | |

| Battery-Electric (Li-ion, LFP, Solid-State) | ||

| Corded-Electric | ||

| Hybrid and Others | ||

| By End-User Segment | Residential/Homeowners | |

| Commercial Landscaping and Groundskeeping | ||

| Construction and Rental Industry | ||

| Agricultural and Forestry Users | ||

| Municipal/Government | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the outdoor power equipment market in 2025?

It stands at USD 46.64 billion, and it is on track for a 6.60% CAGR to reach USD 64.20 billion by 2030.

Which product category in the outdoor power equipment market is expanding fastest?

Lawn mowers are projected to grow at 7.1% CAGR, driven by cordless and robotic innovations.

What share of revenue comes from battery-electric units?

Gasoline still holds 58.7%, yet battery models grow at 8.9% CAGR, rapidly narrowing the gap.

Which region will post the highest growth through 2030?

Asia-Pacific will advance at an 8.3% CAGR on the back of urbanization and expanding middle-class demand.

What is the biggest hurdle to cordless adoption?

Higher upfront purchase prices remain the main barrier, especially in cost-sensitive markets, although lifecycle savings soften the impact.

Which companies lead in autonomous mowing?

Venture-backed entrants such as Scythe Robotics and Electric Sheep spearhead the commercial robotic segment, challenging incumbents with proprietary AI navigation.

Page last updated on: