Market Overview

| Study Period | 2021 - 2031 |

|---|---|

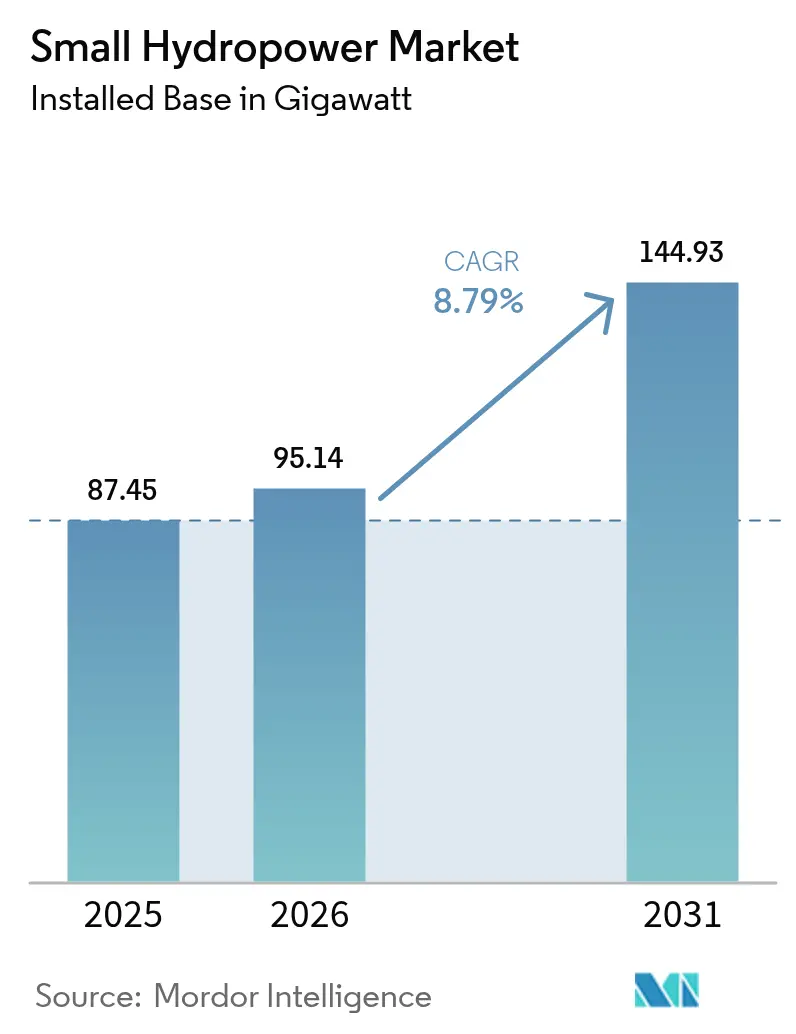

| Market Volume (2026) | 95.14 gigawatt |

| Market Volume (2031) | 144.93 gigawatt |

| Growth Rate (2026 - 2031) | 8.79% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Hydropower Market Analysis by Mordor Intelligence

The Small Hydropower Market size was valued at 87.45 gigawatt in 2025 and estimated to grow from 95.14 gigawatt in 2026 to reach 144.93 gigawatt by 2031, at a CAGR of 8.79% during the forecast period (2026-2031).

This expansion stems from the technology’s ability to supply steady baseload power without grid-scale storage, a feature that increasingly appeals to corporate renewable-energy buyers seeking 24/7 clean electricity. Rural electrification programs in emerging economies, especially in Asia-Pacific and Africa, are turning to distributed small hydropower assets to anchor mini-grids where transmission extension is uneconomical. Continuous innovations in fish-friendly turbines have opened previously restricted rivers, accelerating project pipelines in Europe and North America. Meanwhile, digitalization, through IoT sensors and predictive maintenance, lowers operating costs and extends asset life, strengthening the small hydropower market’s competitiveness against falling solar-plus-storage prices.

Key Report Takeaways

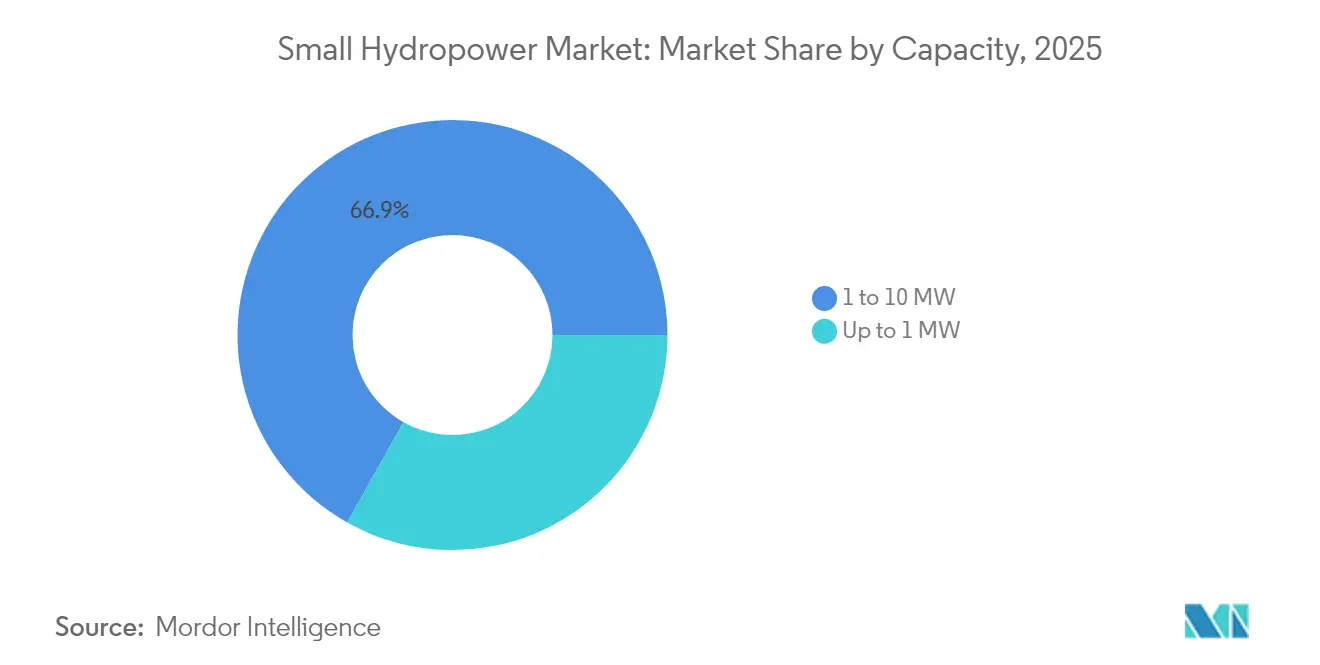

- By capacity, the 1–10 MW segment held 66.85% of the small hydropower market share in 2025, while micro systems up to 1 MW are expanding at a 10.26% CAGR through 2031.

- By technology, run-of-river installations retained 60.35% revenue share in 2025; in-stream and micro-conduit projects record the fastest growth at 10.72% CAGR to 2031.

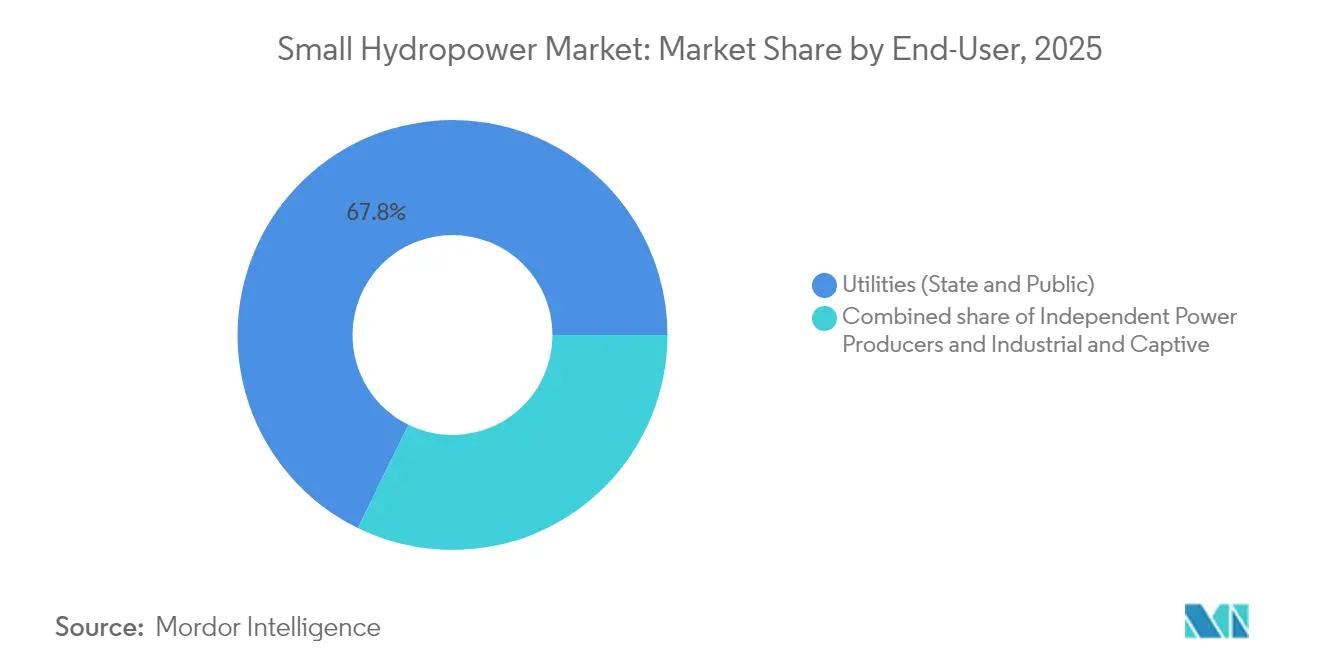

- By end-user, utilities captured 67.75% revenue in 2025; independent power producers show the highest growth momentum at 11.03% CAGR through 2031.

- By geography, Asia-Pacific commanded 63.55% revenue in 2025; the Middle East & Africa leads growth with a 14.31% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Small Hydropower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for clean & sustainable power | 1.20% | Global, with concentration in Europe & North America | Medium term (2-4 years) |

| Rural electrification programmes for off-grid communities | 2.10% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Modernisation & repowering of ageing small-hydro assets | 1.80% | Europe & North America, selective APAC markets | Medium term (2-4 years) |

| Fish-friendly micro-turbine innovations unlocking new sites | 1.50% | North America & EU regulatory zones | Short term (≤ 2 years) |

| Water-energy-food nexus projects attracting blended finance | 0.90% | MEA & South America, selective APAC regions | Long term (≥ 4 years) |

| Corporate renewable PPAs seeking baseload renewables | 0.70% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Clean & Sustainable Power

Corporate sustainability mandates now prize around-the-clock renewable procurement, and small hydropower’s baseload profile matches that goal better than wind or solar paired with costly batteries. The International Renewable Energy Agency anticipates corporate-led clean-power contracting to exceed 100 GW annually by 2030, with baseload sources commanding premium contract prices. Utility-scale buyers, including data-center operators, increasingly bundle small hydropower with intermittent renewables to meet internal carbon accounting frameworks. These trends channel investment toward new projects in Europe and North America, where certificate markets allow differentiated pricing. The result reinforces long-term offtake certainty that de-risks financing and accelerates construction starts.

Rural Electrification Programmes for Off-Grid Communities

Government-backed rural-energy programs allocate sizable funding to distributed hydropower mini-grids because steep terrain makes long transmission lines cost-prohibitive. India’s Deen Dayal Upadhyaya Gram Jyoti Yojana earmarked USD 2.5 billion for electrification in 2024, with 15% of new megawatts sourced from small hydropower. Community ownership models ensure tariffs remain affordable and profits stay local, strengthening social acceptance. World Bank initiatives now blend concessional finance with technical assistance to replicate similar approaches across sub-Saharan Africa. As local industry grows around agro-processing and cold storage, demand curves align with steady river-based generation, reinforcing revenue stability for operators.

Modernisation & Repowering of Ageing Small-Hydro Assets

Much of Europe and North America’s installed base dates to the 1980s and now benefits from sensor-driven upgrades that raise output while lowering operations costs.[1]European Commission, “REPowerEU Plan – Hydropower Modernisation Grants,” ec.europa.eu The EU’s REPowerEU fund committed EUR 1.2 billion in 2024 to modernize turbines and automate controls, driving 15-25% capacity uplifts. Norwegian utility Statkraft retrofitted 12 plants by embedding machine-learning algorithms that adjust wicket gates in real time, extending useful life by up to 30 years. By integrating predictive maintenance, owners can curb unscheduled outages and stagger refurbishment capital more efficiently. The repowering wave also supports stricter fish passage standards without sacrificing energy yield.

Fish-Friendly Micro-Turbine Innovations Unlocking New Sites

Certification of three new turbine designs under the U.S. Department of Energy’s HydroWIRES program lowered fish mortality to below 2%, unlocking rivers long barred from hydropower. Manufacturers such as Natel Energy and Siemens Energy now deploy compact runners that deflect aquatic species rather than fragment them, simplifying regulatory approval. Early pilots in Pacific Northwest salmon habitats demonstrate economic feasibility and environmental compliance in tandem. As permitting hurdles shrink, up to 40% more U.S. sites could qualify for low-impact development, expanding the small hydropower market without large civil works. Similar policy shifts in the EU encourage rapid replication across biodiversity-sensitive regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-driven flow variability & unstable output | -1.40% | Global, acute in drought-prone regions | Long term (≥ 4 years) |

| Lengthy, uncertain environmental-permitting cycles | -0.90% | North America & EU regulatory zones | Medium term (2-4 years) |

| Falling solar-plus-storage LCOE compressing hydro IRRs | -0.70% | Global, concentrated in high-solar regions | Short term (≤ 2 years) |

| Siltation & sedimentation raising O&M costs | -0.50% | APAC & South America, selective global sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Driven Flow Variability & Unstable Output

Intensifying droughts reduce river discharge and erode capacity factors, undercutting the dependable-power narrative that originally justified many projects. The IPCC expects flow variability to rise 20-30% by 2030. In 2024, average capacity factors in southern Europe fell 8%, forcing generators to buy balancing power on spot markets. Hybridization with solar offers a partial hedge but inflates capital budgets by 10-15%. Without dedicated climate-resilience finance, smaller developers could struggle to absorb higher insurance premiums and debt-service cushions required by lenders.

Lengthy, Uncertain Environmental-Permitting Cycles

Multi-agency oversight extends licensing to an average of 4.2 years in the United States, with environmental studies accounting for 60% of that period.[2]Federal Energy Regulatory Commission, “2024 Hydropower Licensing Timeframes,” ferc.gov Europe’s patchwork of fish-passage standards compounds complexity: developers must tailor designs across borders, driving engineering costs higher. Financing charges accumulate during these delays, raising all-in project costs by up to one-third. Only a handful of jurisdictions fast-track truly low-impact installations; elsewhere, lengthy reviews remain standard practice, limiting deployment speed even where economics are favorable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Mid-Scale Dominates, Micro Momentum Accelerates

The 1–10 MW tier continues to anchor the small hydropower market, holding 66.85% revenue in 2025 thanks to proven utility business models and bankable levelized costs of USD 0.05–0.08 per kWh. Asset developers favor this bracket because equipment vendors offer standardized packages and lenders perceive lower execution risk. With many rivers already assessed for such projects, brownfield upgrades further solidify the segment’s revenue base through repowering.

Micro units under 1 MW, however, expand at a brisk 10.26% CAGR through 2031, reflecting streamlined permitting pathways and innovative funding such as community cooperatives. Certification of sub-2% fish-mortality turbines mitigates biodiversity objections that once sidelined small creeks. For remote villages in India or mountainous areas in Peru, ownership stakes keep cash flows local, improving tariff recovery and social license. These attributes ensure the micro tier remains the principal growth engine within the small hydropower market.

By Technology: Run-of-River Reigns, In-Stream and Conduit Gain Share

Run-of-river schemes account for 60.35% of 2025 revenue owing to favorable environmental profiles and the absence of large reservoirs. Financiers value predictable output matched to natural hydrology without major civil works. Automation upgrades, such as real-time gate control, optimize spill and maximize dispatched energy, reinforcing the technology’s leadership.

In-stream and micro-conduit devices register 10.72% CAGR, leveraging existing canals and water-supply networks to circumvent land-acquisition battles. Modern designs slide into irrigation channels or city pipelines, using excess head to produce distributed power without altering flow regimes. Municipal utilities in France and Morocco adopt these solutions to monetize water infrastructure, confirming rapid commercial acceptance. Collectively, such systems erode run-of-river dominance while diversifying the small hydropower market’s technology mix.

By End-User: Utility Hegemony Tested by Independent Power Producers

Utilities retained 67.75% revenue in 2025 as regulators often mandate them to extend service to rural areas that private players deem uneconomic. Access to concessional capital and integrated grid control further cements their position, ensuring priority dispatch and simplified interconnection approvals.

Independent power producers, however, compound capacity at 11.03% CAGR, spurred by deregulated markets and corporate power-purchase agreements that reward firm renewable output. Community-backed IPPs in Kenya and Chile combine equity crowdfunding with multilateral guarantees, closing finance faster than many utilities. As carbon-accounting rules tighten, corporate offtakers lock in multidecade contracts, reinforcing IPP project pipelines and challenging utility hegemony in the small hydropower market.

Geography Analysis

Asia-Pacific dominated with 63.55% revenue in 2025, led by China’s USD 8.5 billion commitment to add 15 GW by 2030 and India’s expedited permitting for sub-5 MW projects. Upgrades in Japan, 15 sites retrofitted by Tokyo Electric Power, demonstrate a mature yet evolving landscape, where digitalization raises output without fresh ecological footprints. Indonesia and the Philippines rely on small hydropower anchor plants to energize island mini-grids, translating resource endowment into inclusive growth.

The Middle East & Africa is the fastest-growing region at 14.31% CAGR toward 2031, buoyed by Morocco’s eight-plant rollout totaling 45 MW and Kenya’s rural-electrification partnerships that served 50,000 residents in 2024. Uganda streamlines approvals for under-5 MW projects, slashing regulatory timelines 40%. In the Democratic Republic of Congo, Chinese finance underwrites schemes that power mineral processing while expanding access for off-grid villages. These initiatives validate the water-energy-food nexus model that integrates irrigation, electricity, and local value addition.

Europe and North America concentrate on repowering and environmental compliance. The EU’s EUR 1.2 billion REPowerEU fund targets efficiency gains and fish-passage retrofits, while Norway’s Statkraft achieves 20% capacity boosts on 12 plants through machine-learning optimization. In the United States, FERC certified three fish-friendly turbines in 2024, enabling projects once barred by salmon-protection rules. South America centers on Brazil and Chile, leveraging robust hydrology to extend grids into remote agrarian zones, proving that modernization and greenfield builds can coexist.

Competitive Landscape

Competition remains moderate, with legacy turbine makers, Voith, Andritz, GE Renewable Energy, Siemens Energy, sharing space with disruptors such as Natel Energy and Turbulent NV. Market leaders deploy IoT-enabled condition monitoring to cut downtime and use predictive analytics to defer major overhauls by fine-tuning operating parameters. Fish-friendly design expertise is now a key differentiator because regulatory acceptance increasingly hinges on aquatic-biodiversity performance. This pivot has led to Andritz’s 2024 purchase of Canyon Hydro for USD 85 million, adding low-head specialization and a North American foothold.

Larger firms pursue bolt-on acquisitions to enter the micro-conduit niche, reflecting the segment’s double-digit growth rate. Partnerships are likewise gaining traction: GE’s venture with Bharat Heavy Electricals aligns foreign technology with local fabrication, reducing cost and shortening lead time for South Asian developers. Price pressure from solar-plus-storage, whose LCOE continues to fall, forces turbine vendors to emphasize life-cycle value rather than headline capex. Consequently, service-based contracts that guarantee output and share performance risk are proliferating, tightening the bond between OEMs and asset owners within the small hydropower industry.

Small Hydropower Industry Leaders

Andritz AG

Voith GmbH & Co. KGaA

Siemens Energy AG

Toshiba Energy Systems & Solutions Corp.

GE Vernova, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The World Bank has approved a $150 million concessional credit to help Uzbekistan develop its small hydropower (SHP) sector and strengthen the national electricity supply. The project will involve private sector participation, engaging local SHP developers and banks.

- December 2024: Bhutan’s DHyE awarded civil works contracts for the second phase of four small hydropower projects (195 MW), Jomori, Gamri-I, Druk Bindu I & II, and Begana, with a total budget of Nu 20 billion. Construction is set to start, and the projects are expected to be completed within 2.5-4 years, supporting Bhutan’s plan to expand hydropower and solar capacity by 20,000 MW over the next 15 years.

- November 2024: The Kuwarsi 9.9 MW hydroelectric project in Himachal Pradesh, India, has started operations ahead of schedule. Developed by V.B. Hydro Projects with engineering support from Geppert Hydro India, the facility uses two Francis turbines to generate and evacuate power at 33 kV and 66 kV, harnessing the Ravi River tributary efficiently.

- April 2023: Shizen Energy Inc. (Shizen Energy) has partnered with GUGLER Water Turbines GmbH (GUGLER), an Austrian firm specializing in the development, design, and manufacturing of water turbines for small to medium-sized hydroelectric power plants. Together, they've installed a 2.2 MW Pelton turbine, accompanied by a synchronous generator, at the Kuroda Hydroelectric Power Plant in Toyota City, Aichi Prefecture. This facility is owned by Chubu Electric Power Co., Inc. (Chubu Electric Power). The newly installed turbine commenced full-scale operations in April 2023, marking it as GUGLER's inaugural megawatt-class turbine to be operational in Japan.

Global Small Hydropower Market Report Scope

Small hydropower refers to hydroelectric power plants with an installed capacity of less than 10MW. These plants generate electrical energy by harnessing the gravitational force of falling or flowing water to drive turbines and generators. Water, primarily through the natural processes of evaporation, wind, and rain, returns to its original height, underscoring its renewable nature. Small-scale hydropower can effectively electrify isolated sites and bolster national electricity production during peak demand.

The small hydropower market is segmented by capacity, technology, end-user, and geography. For each segment, the market sizing and forecasts have been done based on installed capacity. The small hydropower market report includes:

By Capacity

| Up to 1 MW |

| 1 to 10 MW |

By Technology

| Reservoir-Based |

| Run-of-River |

| Pumped-Storage |

| In-Stream and Micro-conduit |

By Component (Qualitative Analysis only)

| Turbines |

| Generators |

| Control and Automation |

| Balance-of-Plant |

By End-User

| Utilities (State & Public) |

| Independent Power Producers |

| Industrial and Captive |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | France |

| Italy | |

| Spain | |

| Norway | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Philippines | |

| Tajikistan | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Chile | |

| Colombia | |

| Honduras | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Uganda | |

| Morocco | |

| Kenya | |

| Democratic Republic of the Congo | |

| Rest of Middle East and Africa |

| By Capacity | Up to 1 MW | |

| 1 to 10 MW | ||

| By Technology | Reservoir-Based | |

| Run-of-River | ||

| Pumped-Storage | ||

| In-Stream and Micro-conduit | ||

| By Component (Qualitative Analysis only) | Turbines | |

| Generators | ||

| Control and Automation | ||

| Balance-of-Plant | ||

| By End-User | Utilities (State & Public) | |

| Independent Power Producers | ||

| Industrial and Captive | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | France | |

| Italy | ||

| Spain | ||

| Norway | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Philippines | ||

| Tajikistan | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Chile | ||

| Colombia | ||

| Honduras | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Uganda | ||

| Morocco | ||

| Kenya | ||

| Democratic Republic of the Congo | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected installed capacity for small hydropower by 2031?

Global capacity is forecast to reach 144.93 GW, up from 95.14 GW in 2026.

How fast is small hydropower capacity expected to grow annually?

The sector is advancing at an 8.79% CAGR through 2031, reflecting sustained policy and corporate demand for 24/7 clean power.

Which region leads in small hydropower deployment currently?

Asia-Pacific holds 63.55% of worldwide installed capacity, driven by programs in China and India that prioritize rural electrification.

Why are fish-friendly turbines important for small hydropower projects?

Turbines that cut fish mortality to below 2% unlock previously restricted river sites and help projects clear stringent environmental reviews faster.

What role does small hydropower play in corporate renewable-energy procurement?

Its steady baseload output lets companies pair it with intermittent solar and wind to meet 24/7 carbon-free power targets without large battery systems.

Who are some leading companies modernizing small hydropower plants?

Voith, Andritz, GE Vernova, Siemens Energy, and Statkraft are investing in IoT monitoring, predictive maintenance, and fish-friendly upgrades to boost efficiency and extend asset life.

Page last updated on: