Power Management System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

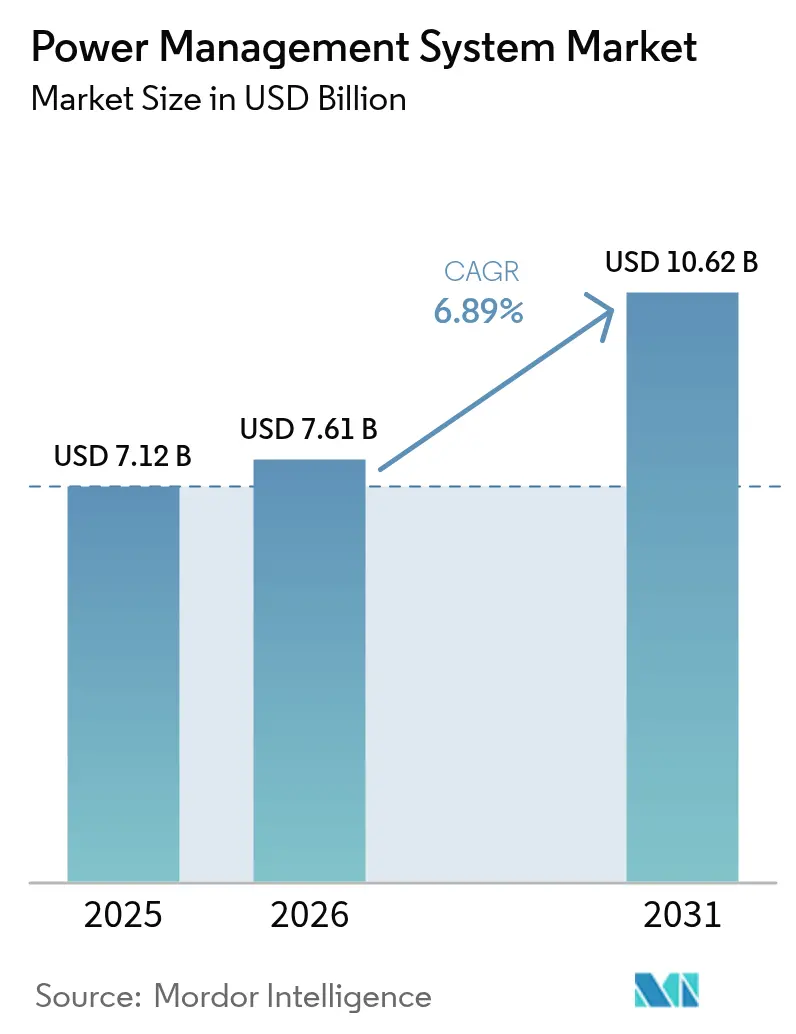

| Market Size (2026) | USD 7.61 Billion |

| Market Size (2031) | USD 10.62 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Management System Market Analysis by Mordor Intelligence

The Power Management System market size is expected to grow from USD 7.12 billion in 2025 to USD 7.61 billion in 2026 and is forecast to reach USD 10.62 billion by 2031 at 6.89% CAGR over 2026-2031.

Rising AI workloads, expanding renewable penetration, and the need for intelligent load orchestration underpin this momentum. North American hyperscale data center expansion, coupled with Asia-Pacific industrial automation mandates, accelerates demand for real-time optimization platforms. Simultaneously, supply-chain constraints in medium-voltage equipment elevate the strategic importance of software-defined energy management. Vendors respond through acquisitions that deepen analytics portfolios and fortify cybersecurity, positioning the power management system market for resilient growth.

Key Report Takeaways

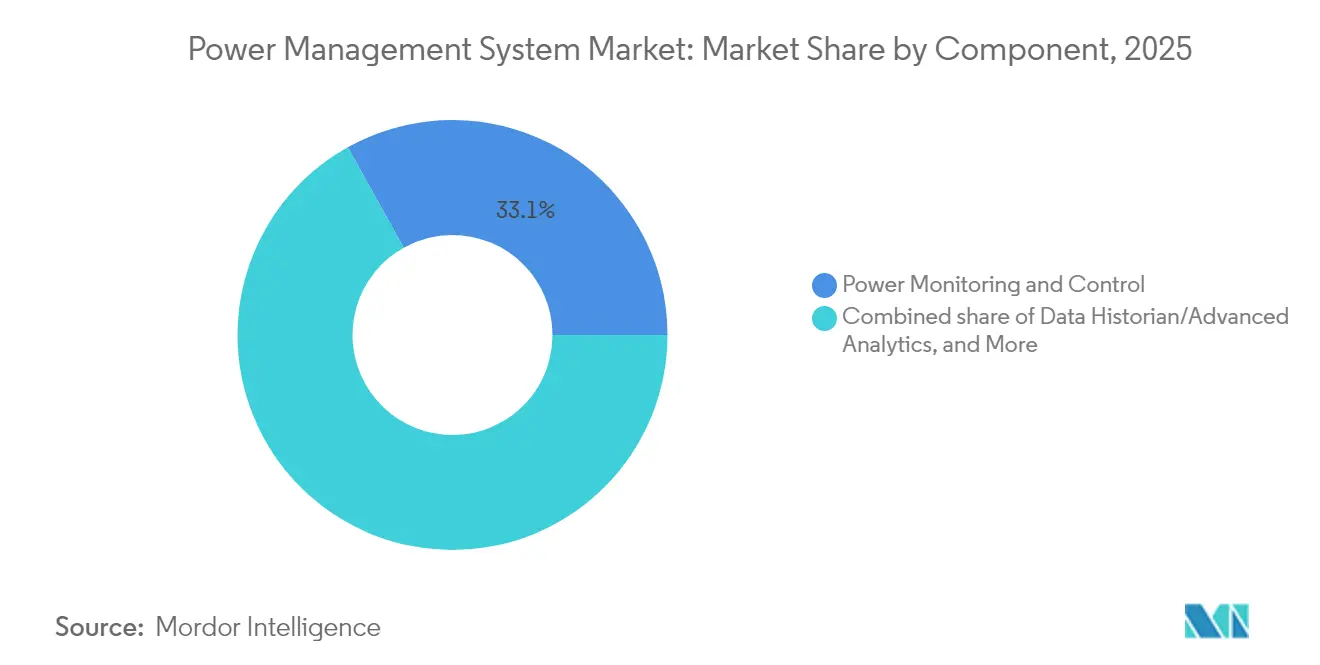

- By component, Power Monitoring & Control held 33.10% of the power management system market share in 2025, while Data Historian/Analytics is projected to post a 10.62% CAGR through 2031.

- By power architecture, centralized PMS captured 47.70% of the power management system market size in 2025; modular/hybrid PMS is anticipated to expand at a 9.37% CAGR through 2031.

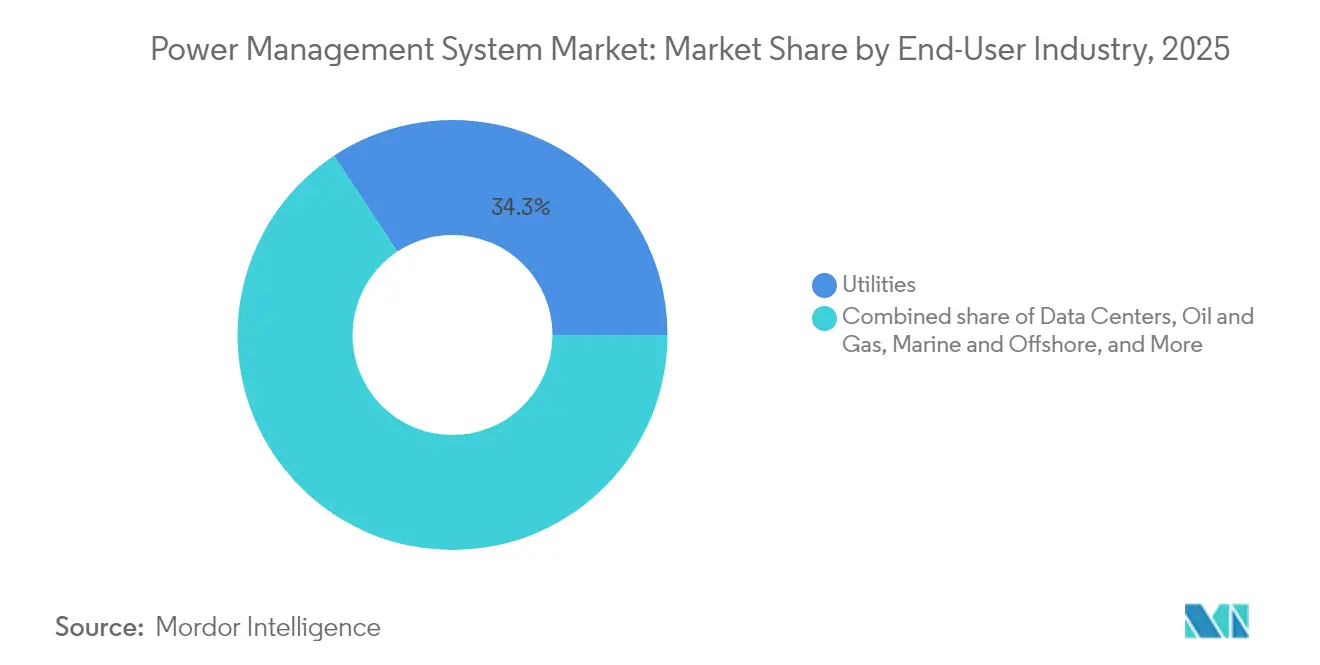

- By end-user, utilities commanded 34.30% revenue share of the power management system market in 2025, whereas data centres are forecast to register a 10.05% CAGR over 2026-2031.

- By geography, North America led with 32.40% of 2025 revenue, but the Asia-Pacific region is poised for 8.98% CAGR growth through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Power Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory pressure for industrial-scale energy efficiency programs | +1.20% | Global (early gains in EU, Japan, California) | Medium term (2-4 years) |

| Rapid renewable-grid integration driving grid-stability solutions | +1.80% | Global, concentrated in APAC, North America, EU | Long term (≥ 4 years) |

| Exponential rise of hyperscale & AI data-center power demand | +2.10% | North America & EU, spill-over to APAC core | Short term (≤ 2 years) |

| Digitalisation/IIoT enabling real-time optimisation & analytics | +1.40% | Global, early adoption in North America, Germany | Medium term (2-4 years) |

| Wide-bandgap (SiC/GaN) semiconductors slash switching losses | +0.90% | Global, led by automotive and renewable sectors | Long term (≥ 4 years) |

| Corporate PPAs create micro-grid complexity needing PMS orchestration | +0.60% | North America, EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure for Industrial-Scale Energy Efficiency Programs

Minimum performance standards now apply to commercial furnaces in the United States, requiring 80% thermal efficiency for gas-fired units and 81% for oil-fired systems. Japan’s Energy Efficiency Act obliges designated factories to appoint certified energy managers and submit annual performance reports, fostering systematic energy savings that have reached 26% in early deployments.(1)International Energy Agency, “Japan Energy Efficiency Act Analysis,” iea.orgSimilar mandates across the EU accelerate digital retrofits and strengthen the power management system market as plants race to document real-time energy performance.

Rapid Renewable-Grid Integration Driving Grid-Stability Solutions

Intermittent solar and wind are forecast to supply 57% of global service-load electricity by 2050, challenging conventional frequency-control paradigms. Flexible AC transmission systems paired with hybrid storage deliver 30% stability improvements and cut total harmonic distortion below 2% compared with legacy designs. These technical gains stimulate procurement of advanced orchestration software that balances variable supply and demand across microgrids, bolstering the power management system market.

Exponential Rise of Hyperscale & AI Data-Center Power Demand

AI training clusters push rack densities to 80-100 kW, versus 5-10 kW for legacy workloads. U.S. data center electricity demand is set to reach 35 GW within five years, with AI responsible for half of the incremental load.(2)Schneider Electric, “U.S. Data Center Demand Forecast,” se.comOperators adopt grid-independent microgrids and asset-level analytics, propelling immediate uptake of predictive energy management solutions across the power management system market.

Wide-Bandgap (SiC/GaN) Semiconductors Slash Switching Losses

SiC devices excel above 800 V, while GaN devices perform better below 400 V, offering superior high-frequency performance.(3)IEEE Spectrum, “SiC vs. GaN: The Future of Power Electronics,” ieee.orgEfficiency gains across inverters, chargers, and solid-state transformers make WBG devices central to renewable and EV ecosystems, indirectly fuelling demand for adaptive control layers within the power management system market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront system & retrofit costs | -1.30% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Escalating cyber-security & data-sovereignty risks | -0.80% | Global, heightened in critical infrastructure sectors | Medium term (2-4 years) |

| Transformer & switchgear supply-chain bottlenecks | -1.10% | Global, most severe in North America and EU | Short term (≤ 2 years) |

| Legacy OT / IT interoperability barriers | -0.70% | Global, concentrated in heavy industry and utilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront System & Retrofit Costs

Budget constraints slow adoption in price-sensitive economies where capital recovery timelines exceed typical board expectations. Equipment plus integration outlays can exceed USD 1 million for a mid-sized plant, pressuring CFOs to delay digital retrofits. Government incentives mitigate some burden, yet financing gaps persist, temporarily tempering the expansion of the power management system market.

Escalating Cyber-Security & Data-Sovereignty Risks

Expanded connectivity broadens attack surfaces. Air-gap strategies, once common in operational technology, are giving way to secure gateways that require IEC 62443-certified devices, such as ABB’s SL2-rated air circuit breaker. Compliance costs and concerns about breaches restrain full-scale cloud adoption among critical infrastructure owners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Data Analytics Drives Digital Transformation

Power Monitoring & Control booked USD 2.36 billion in 2025, equivalent to 33.10% of the power management system market size. Legacy SCADA platforms remain indispensable for breaker status and feeder metering; however, operators are increasingly overlaying historian databases that unlock cross-site benchmarking. Data Historian/Advanced Analytics is projected to have the quickest trajectory, with a 10.62% CAGR, reaching USD 2.66 billion by 2031, as AI-driven predictive models reduce unplanned downtime and cut energy waste. Load Shedding and Management tools leverage optimisation algorithms that trim load overcut by 30% compared to rule-based logic, sharpening industrial resiliency. Generator Controls gain relevance in microgrid deployments, with GE’s PowerNode initiating protective load-sheds within 15 milliseconds while safeguarding cyber-perimeters through IEC 61850 GOOSE messaging.

Integrated suites now converge monitoring, historian, and optimisation modules into cloud-ready dashboards, steering the power management system market toward platform economics. Vendors embed secure APIs, allowing third-party developers to build applications on top of core data services. ABB’s SACE Emax 3 breaker showcases this shift by exposing energy-quality metrics directly into historian pipelines. As decarbonisation mandates tighten, analytics modules quantify avoided emissions and monetise demand-response credits, elevating their share of new-build specifications.

By Power-Architecture: Hybrid Solutions Address Flexibility Demands

Centralised architectures accounted for 47.70% of 2025 revenue, favoured by utilities and oil & gas owners that value proven redundancy. However, modular/hybrid configurations are projected to achieve a 9.37% CAGR, as AI workloads and renewable intermittency necessitate edge-level autonomy. Distributed PMS nodes placed at the turbine level or rack level circumvent latency, maintaining critical control during WAN outages. Emerson’s Ovation 4.0 incorporates software-defined modules and generative AI guidance, illustrating the pivot to micro-services that reconfigure without site downtime.

Hybrid topologies combine central oversight with local agents, striking a balance between reliability and agility across complex estates. Multi-agent frameworks deployed in wind-solar-battery farms achieve significant peak shaving and frequency stabilisation. As a result, the power management system market gravitates toward libraries of containerized functions deployable in either data center pods or embedded gateway hardware. System integrators differentiate through reference-architecture blueprints that accelerate commissioning while maintaining cyber-hardening.

By End-User Industry: Data Centers Surge Amid Infrastructure Modernization

Utilities generated USD 2.44 billion in 2025, translating to 34.30% of the power management system market. Grid operators rely on fast-acting voltage-var supports and adaptive islanding logic to absorb 57% renewable penetration forecasts. Data centres, though on a smaller scale, will climb at a 10.05% CAGR as hyperscalers race to manage 500 MW-scale campuses with grid-independent power blocks. Oil & gas facilities are maintaining steady investments to electrify offshore platforms and reduce flare-gas emissions. Marine & offshore fleets install DC distribution and hybrid propulsion that trim fuel burn and cut maintenance costs.

Metals & mining initiatives realise up to a 10% energy-efficiency uplift through digital energy management; ArcelorMittal recovers 22% of blast-furnace gas, slashing CO₂ emissions by 340,000 tonnes annually. Chemical and pharmaceutical operations embed resource-efficiency indicators that shave more than 1% of total energy costs each year. Hospitals and telecom exchanges in the “Others” category benefit from common reference architectures that simplify ISO 50001 compliance, broadening the end-user base of the power management system market.

Geography Analysis

North America contributed 32.40% of 2025 revenue, underpinned by the Inflation Reduction Act and a pipeline of more than 30 GW in new data-center power agreements. Federal incentives have encouraged Schneider Electric to commit USD 700 million toward U.S. manufacturing expansion, enhancing domestic supply resilience. Canada’s Industry Partnership for Energy Conservation sponsors ISO 50001 adoption grants, while Mexican transformer investments mitigate regional bottlenecks.

Europe maintains a stringent regulatory environment that mandates corporate sustainability reporting and tightens eco-design rules, sustaining steady demand across Germany, France, and the United Kingdom. Industrial automation upgrades in Germany deploy historian-driven OEE dashboards, whereas the U.K. pushes smart-grid pilots funded by Ofgem innovation programs. The Corporate Sustainability Reporting Directive drives enterprises to integrate granular energy data into ESG workflows, thereby strengthening the uptake of analytics throughout the power management system market.

Asia-Pacific region is poised for a 8.98% CAGR. China’s national power market saw green-electricity trading exceed 220 TWh in early 2025, spurring utilities to adopt AI-enabled dispatch planning. India advances industrial energy efficiency under the Perform, Achieve, and Trade scheme and commits to achieving 11.4% transformer efficiency gains by 2027 through Japan’s Top Runner collaboration. Japan’s chemical clusters embrace factory-wide IIoT overlays, while Australia pilots integrated microgrids to support remote mining operations.

Competitive Landscape

Moderate consolidation defines the ecosystem, with top suppliers expanding through targeted acquisitions. ABB’s acquisition of Siemens Gamesa’s power electronics division added 40 GW of installed renewable converter capacity, reinforcing its wind, solar, and storage offerings. In Q2 2025, ABB reported record USD 9.8 billion in orders, reflecting robust grid modernization spend. Schneider Electric’s USD 700 million U.S. program boosts switchgear and UPS capacity, directly addressing the AI-driven demand for data centers.

Technology differentiation now centres on AI-native platforms and cyber-resilience. Emerson’s Ovation 4.0 embeds Microsoft Azure OpenAI services, enabling conversational support for operators and accelerating mean time to remediation. Eaton is scaling high-power DC infrastructure through the acquisition of Resilient Power Systems, anticipating rapid electrification of mobility and edge-computing hubs.

White-space opportunities remain in microgrid orchestration for campuses with corporate PPAs. Start-ups are developing solid-state transformers and SiC-based converters that promise significant improvements in conversion efficiency. Incumbents counter by integrating open-API marketplaces, ensuring third-party innovators can plug analytics into base PMS installations, sustaining competitive dynamism across the power management system market.

Power Management System Industry Leaders

ComAp AS

Brush Group

ABB LIMITED

etap (Operation Technology Inc.)

Wartsila oyj abp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ABB recorded USD 9.8 billion in orders for Q2 2025 and launched the SL2-certified SACE Emax 3 breaker for critical infrastructure.

- March 2025: Schneider Electric is investing USD 700 million in its U.S. operations through 2027, with a focus on expanding manufacturing and creating 1,000 new jobs.

- August 2024: Wärtsilä unveiled the GEMS 7 Digital Energy Platform for multi-GWh storage optimisation.

- July 2024: Emerson recently released Ovation 4.0, an automation platform for the power and water industries, featuring a software-defined architecture and integration with generative AI.

Global Power Management System Market Report Scope

A Power Managemnt System (PMS) is a control system or electrical generators which are often provided as a part of the IAS. They ensure the safety, reliability and efficiency of all the electrical distribution systems in a given area. Hence ensuring the power capacity is in line with vessel power at any time. The study is focuses only on various harware porvided by diffrent competitive vendors

| Power Monitoring and Control |

| Load Shedding and Management |

| Energy Cost Accounting and Optimisation |

| Switching and Safety Management |

| Generator Controls |

| Data Historian/Advanced Analytics |

| Centralised PMS |

| Distributed PMS |

| Modular / Hybrid PMS |

| Utilities |

| Data Centres |

| Oil and Gas |

| Marine and Offshore |

| Metals and Mining |

| Chemicals and Pharmaceuticals |

| Others (Manufacturing, Healthcare, Telecom) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Power Monitoring and Control | |

| Load Shedding and Management | ||

| Energy Cost Accounting and Optimisation | ||

| Switching and Safety Management | ||

| Generator Controls | ||

| Data Historian/Advanced Analytics | ||

| By Power-Architecture | Centralised PMS | |

| Distributed PMS | ||

| Modular / Hybrid PMS | ||

| By End-User Industry | Utilities | |

| Data Centres | ||

| Oil and Gas | ||

| Marine and Offshore | ||

| Metals and Mining | ||

| Chemicals and Pharmaceuticals | ||

| Others (Manufacturing, Healthcare, Telecom) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the power management system market?

The power management system market size measured USD 7.61 billion in 2026 and is forecast to reach USD 10.62 billion by 2031.

Which segment is growing the fastest?

Data Historian/Advanced Analytics is projected to register a 10.62% CAGR through 2031, the highest among all component categories.

Why are data centres driving demand?

Rising AI workloads push rack densities to 80-100 kW, creating complex energy-management requirements that only advanced PMS platforms can satisfy.

Which region will add the most incremental revenue by 2031?

Asia-Pacific is expected to post the highest CAGR at 8.98%, propelled by industrial automation and renewable mandates across China, India, and Japan.

How are supply-chain constraints affecting the market?

Transformer lead times of up to 130 weeks and price hikes of 60-80% delay hardware installations, prompting greater investment in software-centric optimisation.

What role do wide-bandgap semiconductors play in PMS adoption?

SiC and GaN devices enhance conversion efficiency, enabling compact, high-temperature power electronics that integrate seamlessly into next-generation PMS architectures.

Page last updated on: