Residential Generators Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

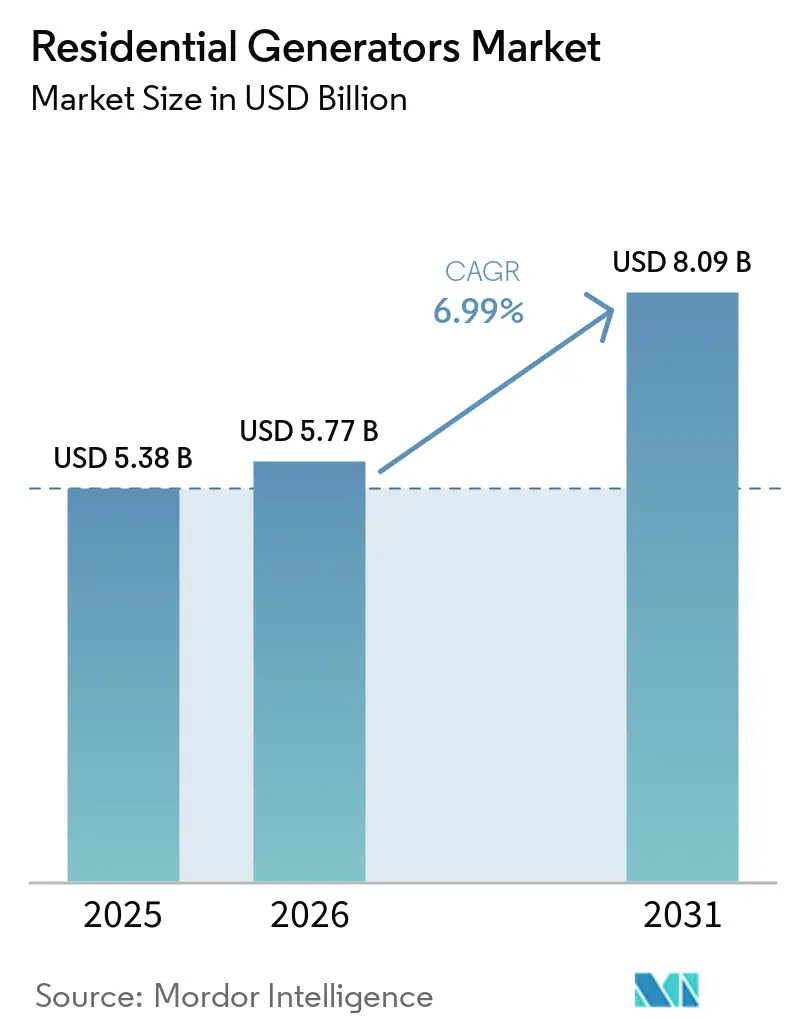

| Market Size (2026) | USD 5.77 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

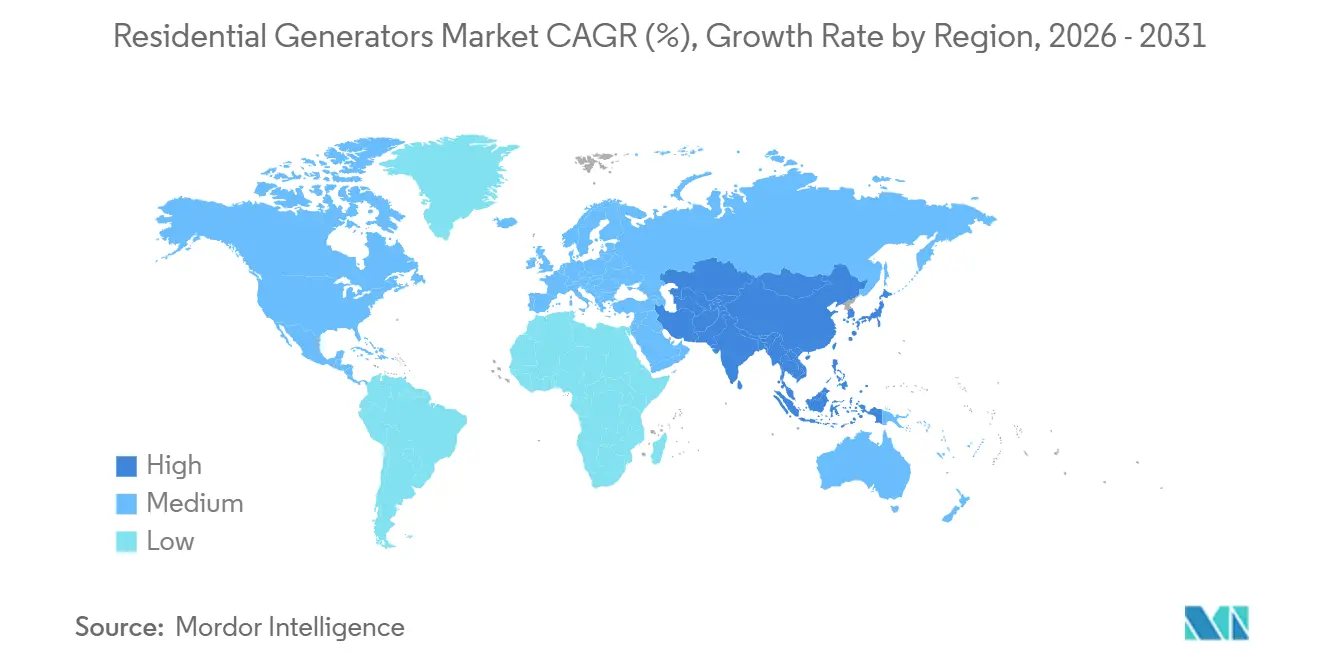

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

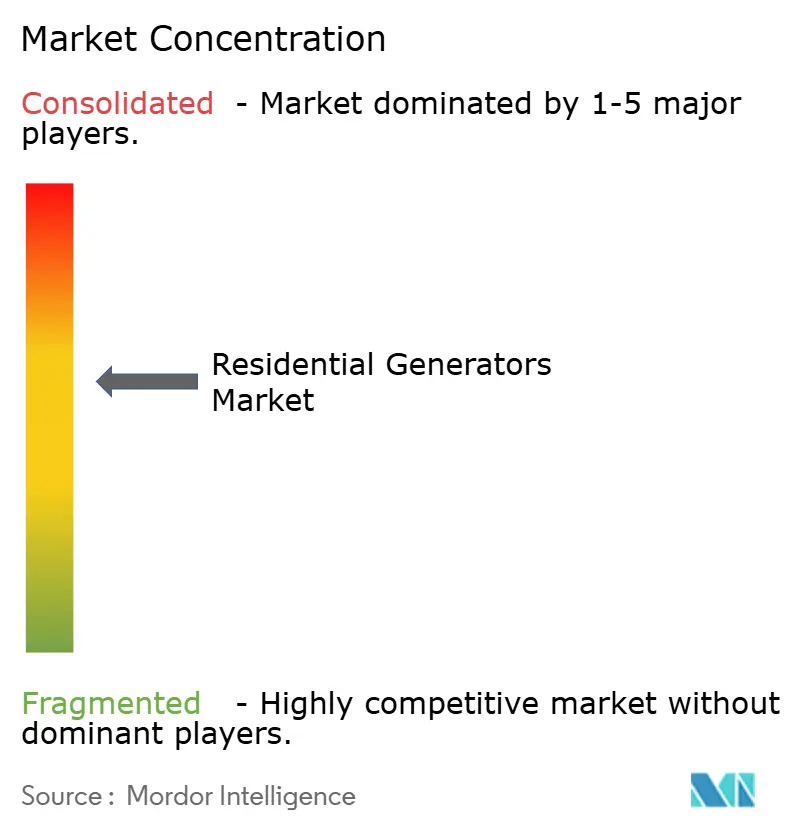

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Residential Generators Market Analysis by Mordor Intelligence

The Residential Generators Market size was valued at USD 5.38 billion in 2025 and is estimated to grow from USD 5.77 billion in 2026 to reach USD 8.09 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031). Persistent grid-reliability shortfalls, a sharp rise in extreme-weather events, and the electrification of home heating and mobility are converting backup power from a convenience item into an essential household asset. North American homeowners receive insurance premium reductions of 3-7% when a certified standby unit is installed, encouraging higher-value purchases. In parallel, 70% of U.S. large power transformers now exceed 25 years of service life, stretching restoration timelines after faults and giving the Residential generators market a structural rather than cyclical tailwind. Hybrid solar-storage-generator packages are scaling quickly because state incentives narrow the payback period on battery capacity, while automatic-start natural-gas sets remain the default for whole-home coverage in pipeline-served suburbs. Competitive dynamics are shifting as battery specialists and inverter innovators enter the space, fragmenting high-growth niches even though conventional engine technology still dominates unit volume.

Key Report Takeaways

- By fuel type, natural gas led with 34.8% of Residential generators market share in 2025; solar-battery hybrids are advancing at an 11.0% CAGR through 2031.

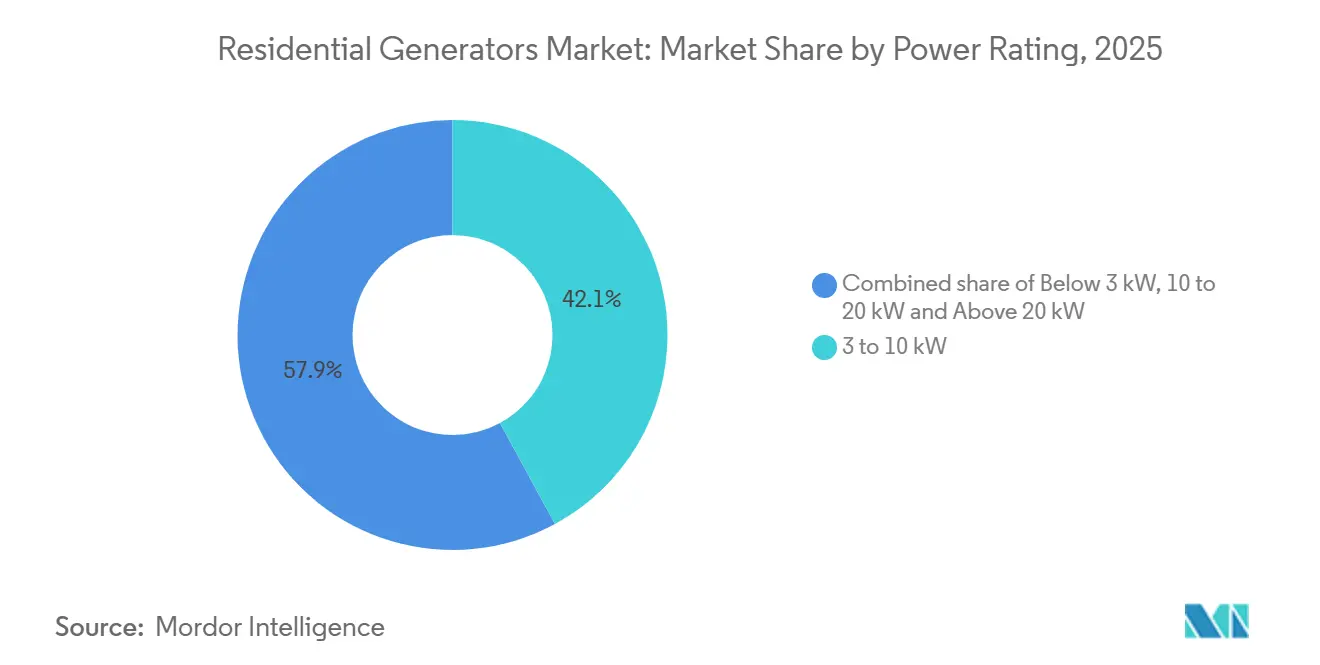

- By power rating, the 3-10 kW band accounted for 42.1% share of the Residential generators market size in 2025, and the 10-20 kW segment is projected to expand at a 7.7% CAGR between 2026 and 2031.

- By phase, single phase led with 88.2% of Residential generators market share in 2025 and is expected to advance at an 7.1% CAGR through 2031.

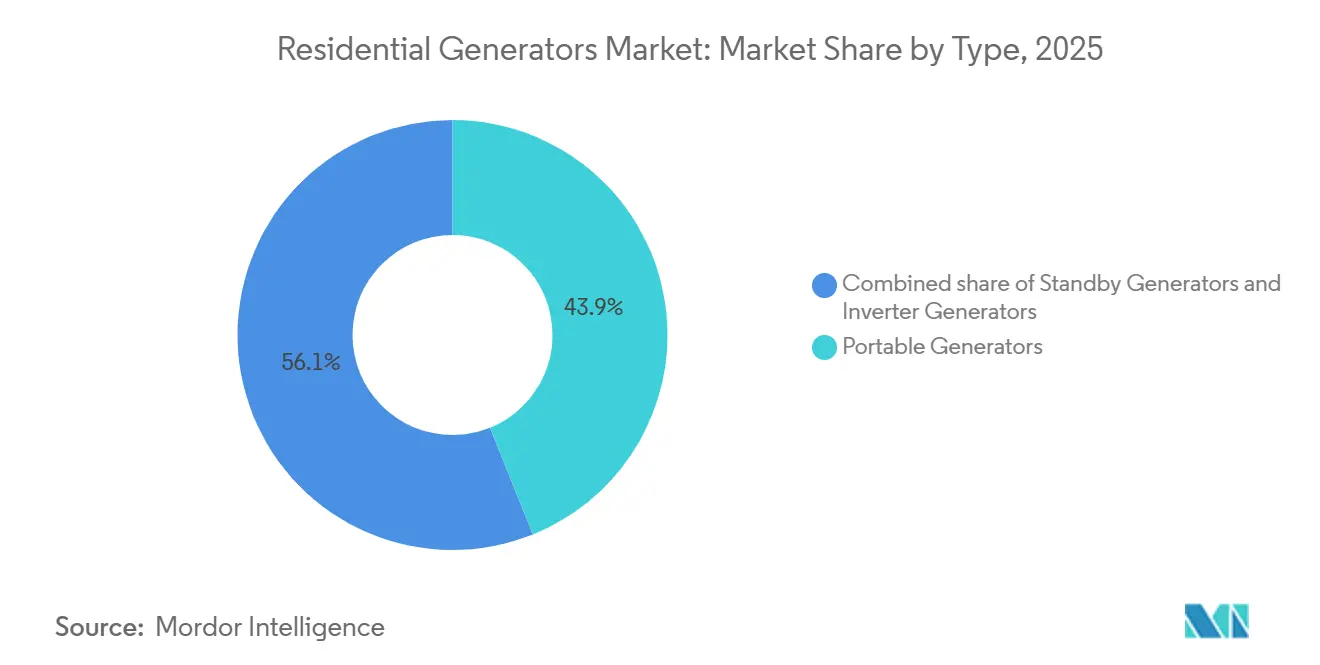

- By type, portable units captured 43.9% revenue in 2025, whereas standby systems are forecast to grow at an 8.2% CAGR through 2031.

- By technology, conventional engines held 64.3% Residential generators market share in 2025, and hybrid architectures are forecast to rise at a 10.8% CAGR over 2026-2031.

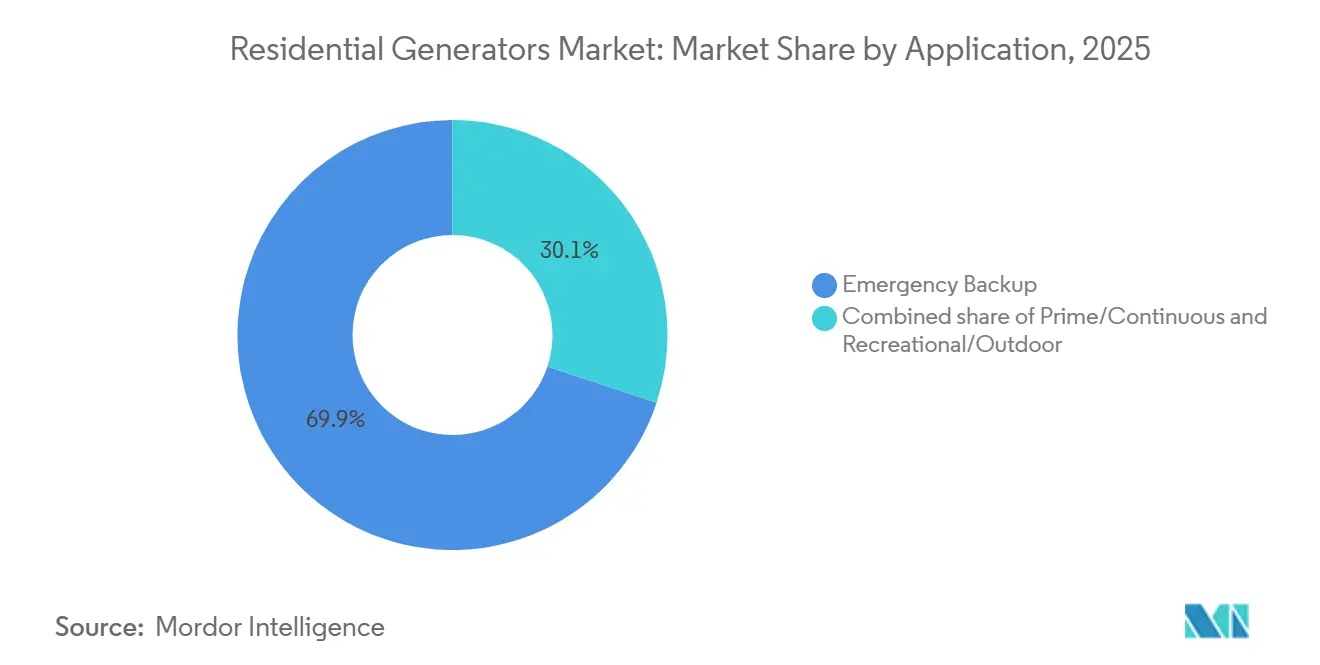

- By application, emergency-backup installations represented 69.9% of the Residential generators market size in 2025 and are set to advance at a 7.2% CAGR to 2031.

- By geography, North America commanded 37.0% revenue in 2025, while Asia-Pacific is the fastest-growing at an 8.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Residential Generators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing frequency of extreme-weather-related outages | + 1.8% | Global, with concentration in North America, Europe, and Asia-Pacific coastal zones | Short term (≤ 2 years) |

| Aging transmission & distribution infrastructure | + 1.5% | North America, Europe (especially Germany, UK, France), parts of Asia-Pacific | Medium term (2-4 years) |

| Expansion of residential natural-gas grids | + 0.9% | North America (U.S., Canada), select European markets (Germany, Italy), emerging Asia-Pacific urban centers | Medium term (2-4 years) |

| Work-from-anywhere surge in home load-critical electronics | + 0.7% | Global, with highest intensity in North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Hybrid solar-storage-generator resilience packages | + 1.3% | North America (California, Texas), Europe (Germany, Italy, Spain), Australia, Japan | Medium term (2-4 years) |

| Grid-cybersecurity breach concerns among homeowners | + 0.4% | North America, Europe, developed Asia-Pacific markets (Japan, South Korea, Australia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing frequency of extreme-weather-related outages

Severe storms generated 80.1% of U.S. power interruptions between 2000 and 2023, and the average major event lasted 229 minutes in 2022, double the restoration windows common a decade earlier [1] International Energy Agency, “Electricity Market Report 2026,” iea.org. Similar patterns emerged worldwide in 2025 when Chile’s nationwide outage and Iraq’s heat-wave blackout underscored how compound climate stressors topple grids already operating near capacity. County-level studies confirm that days above 32.2 °C combined with wind or precipitation sharply elevate outage counts, pushing households in California, Texas, and the Southeast toward automatic-start solutions that can cover multi-day disruptions. As refrigerators, HVAC systems, and connectivity equipment all become mission-critical, buyers increasingly select standby or hybrid units featuring long runtime and remote monitoring. The outcome is a sustained uplift in the Residential generators market as backup power becomes a core element of household resilience planning.

Aging transmission & distribution infrastructure

Roughly 70% of U.S. transmission lines and large transformers now exceed 25 years of service, a lifespan bracket correlated with higher failure rates during extreme temperatures [2]North American Electric Reliability Corporation, “2025 Long-Term Reliability Assessment,” nerc.com. Planned grid-hardening investments of USD 480 billion in 2025 and USD 5.8 trillion through 2035 will ease the strain eventually, but permitting delays and labor shortages stretch completion timelines, leaving homeowners exposed for the next decade. North American reliability assessments already flag 13 of 23 regions at elevated risk, so demand for backup generation persists even as utilities invest. Similar replacement lags characterize Western Europe, where legacy infrastructure meets rising electrification loads. Consequently, the Residential generators market benefits from a long, visible demand horizon that encourages manufacturers to expand dealer networks, financing options, and hybrid product lines.

Hybrid Solar-Storage-Generator Resilience Packages

Battery costs are falling fast enough that California’s Self-Generation Incentive Program, which rebates USD 1,100-5,000 per kWh, cuts hybrid system payback to under five years for outage-prone zip codes [3]California Public Utilities Commission, “Self-Generation Incentive Program Handbook,” cpuc.ca.gov. Generac’s 28 kW battery-ready standby generator, launched in 2025, signals incumbent recognition that seamless solar-storage integration is becoming a mainstream expectation. Homeowners appreciate silent, zero-emission operation for routine load coverage while retaining fuel-based generation for multi-day events, a combination that inverter-battery hybrids deliver. Jurisdictions with strict noise ordinances likewise favor hybrids that can run on batteries overnight. These factors propel a 10.8% CAGR for hybrid architectures, outpacing overall Residential generators market growth and forcing conventional engine suppliers to accelerate inverter and storage compatibility roadmaps.

Work-from-Anywhere Surge in Home Critical Electronics

Remote work embeds 100-260 W of continuous IT load in residences, translating into 500-1,500 Wh per day that must remain online during business hours. Even short outages now impose measurable income losses on knowledge workers. Consequently, demand skews toward units with automatic transfer switches and zero-downtime capability, explaining why the 3-10 kW power-rating band dominated 2025 shipments. As electric-vehicle adoption rises, homes add Level 2 chargers that push aggregate critical load into the 10-20 kW tier, which is growing at 7.7% CAGR. Participation in utility demand-response programs further sweetens the value proposition, letting owners monetize their standby asset during peak events. The effect is a premiumization trend within the Residential generators market as convenience and reliability trump entry-level pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening small-engine emission limits (EU Stage V, CARB) | -0.8% | Europe (EU Stage V), North America (California CARB, EPA Tier 2), select Asia-Pacific markets adopting similar standards | Medium term (2-4 years) |

| Municipal noise / zoning restrictions | -0.5% | North America (suburban U.S., Canada), Europe (Germany, UK, France), urban Asia-Pacific | Short term (≤ 2 years) |

| Falling Li-ion home-battery costs | -1.1% | Global, with highest impact in North America, Europe, Australia, Japan | Medium term (2-4 years) |

| Insurance rebates favouring zero-emission backup | -0.3% | North America (U.S., Canada), Europe (Germany, UK), Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening small-engine emission limits

EPA Tier 2, California’s small off-road engine rules, and EU Stage V standards demand particulate filters, catalytic reduction, and advanced injection systems that add 15-20% to the bill of materials for sub-20 kW sets [4]Caterpillar, “Cat D1500 Diesel Generator Set Launch,” cat.com. Vendors such as Kohler hedge with hydrogen-compatible and HVO-ready products to preserve market access as thresholds tighten. Compliance costs hit portable and entry-level standby models hardest, compressing margins and nudging buyers toward quieter inverter or battery solutions that sidestep combustion limits. The regulatory drag is moderate yet persistent, shaving 0.8 percentage points off forecast CAGR in the Residential generators market.

Falling Lithium-Ion Home-Battery Costs

Installed prices for 10 kWh residential storage systems now drop below USD 8,000, and incentive-adjusted costs in California, Australia, and Germany undercut mid-range standby generators. Solar-equipped households find battery-only backups sufficient for sub-four-hour interruptions, eroding generator demand in that duration bracket. Companies respond by emphasizing multi-day runtime, cold-weather performance, and high-start current capacity, attributes where fuel-based units still excel. Generac’s battery-ready architecture and Cummins’ inverter advances illustrate adaptation, yet the restraint trims 1.1 percentage points from overall Residential generators market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Natural Gas Strength Faces Zero-Emission Disruption

Natural-gas units accounted for 34.8% Residential generators market share in 2025 on the back of pipeline availability, automatic-start ease, and lower fuel cost per kWh. Ongoing grid expansions in Ontario and the U.S. Sun Belt widen the addressable base, supporting steady volume. The Residential generators market size for natural-gas sets is projected to reach USD 3.2 billion by 2031 as installations migrate from manual transfer switches to fully automated whole-home coverage. Meanwhile, solar-battery hybrids log an 11.0% CAGR, luring urban, noise-sensitive buyers with rebate-driven economics and silent operation. Diesel remains relevant for rural, off-grid properties requiring multi-day autonomy, but emission compliance raises system cost. Gasoline portables cling to entry-level niches yet lose share to dual-fuel LPG models that store safer and run cleaner. Manufacturers hedging across dual- and tri-fuel capabilities best capture mixed-infrastructure markets flagged by reliability agencies where winter pipeline pressure can drop.

Renewables adoption steers future preferences. Regions crossing 20% rooftop solar penetration lean heavily toward hybrids that self-charge daily and ride through evening peaks on batteries. In contrast, suburban tracts with mature natural-gas grids prefer fuel-based standby sets sized for HVAC and EV-charger loads. Strategic positioning, therefore, revolves around offering both zero-emission and dual-fuel pathways inside branded ecosystems so customers can add or swap modules as policy or price signals evolve.

By Power Rating: The Critical-Load Sweet Spot Expands Upward

With 42.1% share, 3-10 kW generators represent the mainstream choice for refrigerators, HVAC blowers, lighting, and home-office electronics. Their installed cost per kW and footprint suit single-family dwellings, keeping shipment volume high even as hybrids gain ground. The Residential generators market size tied to this band is forecast to climb to USD 3.5 billion by 2031, though share inches down as larger homes and EV charging drive upgrades. The 10-20 kW bracket grows fastest at 7.7% CAGR, reflecting Level 2 charger prevalence and rising adoption of electric heat pumps. Portable power stations under 3 kW eat into small gasoline generator demand thanks to silent, indoor-safe batteries that meet camping and tailgating needs. Units above 20 kW remain niche—luxury estates, farms, and small businesses—but could scale if vehicle-to-grid rules allow export revenues that offset higher capex.

Capacity planning increasingly accounts for peak-start loads of heat pumps and EV chargers rather than average draw, nudging households to size up. Manufacturers emphasize load-management modules that orchestrate appliances dynamically, letting a 10 kW generator run a 15 kW connected load sequentially, stretching the sweet spot while containing costs.

By Phase: Single-Phase Dominance, Three-Phase Niche

Single-phase models comprised 88.2% of 2025 shipments and will maintain supremacy at a 7.1% CAGR through 2031 because most homes worldwide receive 120/240 V service. The Residential generators industry sees three-phase demand confined to estates with workshops or agricultural equipment. Limited panel wiring, higher unit price, and sparse product catalogs restrict penetration. Vendors instead invest in power-conditioning electronics that deliver utility-grade sine waves from single-phase machines, satisfying sensitive loads without the complexity of three-phase supply.

By Type: Portable Volume Meets Standby Value

Portable generators secured 43.9% revenue in 2025 thanks to mass-market price points and zero installation requirements. However, standby systems, already leading in dollar contribution, are posting an 8.2% CAGR as automatic-start convenience aligns with remote-work needs. The Residential generators market size associated with standby sets is projected to exceed USD 5 billion by 2031. Inverter portables bridge categories, offering clean power at 50-58 dBA that complies with growing municipal noise rules such as Princeton, New Jersey’s Ordinance #2024-05. Manufacturers split channel strategy accordingly: big-box retail for portables, dealer-installer networks plus financing for standby.

By Technology: Conventional Maturity Versus Hybrid Innovation

Conventional engines held 64.3% Residential generators market share in 2025 due to cost advantages and entrenched service networks. Yet hybrid systems, combining inverter gensets and lithium-ion batteries, register a 10.8% CAGR, marking the top technology growth track. Incentives, silent overnight operation, and the ability to island from both grid and fuel supply underpin adoption. Cummins’ inverter-based Centum platform and Kohler’s hydrogen-ready models illustrate an industry refocusing R&D on alternative architectures that boost fuel efficiency 20-30% and drop noise by 10-15 dBA.

By Application: Emergency-Backup Primacy and Niche Diversification

Emergency-backup use represented 69.9% Residential generators market size in 2025 and expands at 7.2% CAGR as outages lengthen, and electrification raises critical-load stakes. Prime/continuous duty retains importance in weak-grid pockets of South Asia, Africa, and the Middle East, while recreational demand leans toward battery-based power stations rather than combustion generators. Marketing, therefore, stresses automatic start, multi-day fuel autonomy, and smart-home connectivity for backup buyers, whereas durability and mobility headline recreational models.

Geography Analysis

North America anchored 37.0% of 2025 revenue, a leadership position sustained by mature natural-gas grids, streamlined permitting for standby installations, and insurance discounts tied to certified backup systems. Chronic hurricane, wildfire, and ice-storm activity keeps consumer awareness high. Canada’s Enbridge expansions in Ontario broaden pipeline coverage and enlarge the Residential generators market as gas standbys become feasible for another 2,200 rural homes by 2027. Mexico shows faster unit growth than revenue growth because portable sets dominate in lower-income regions. Outage-risk assessments through 2035 flag resource adequacy shortfalls in MISO, PJM, ERCOT, and WECC, pointing to a long demand runway.

Asia-Pacific, the quickest riser at an 8.5% CAGR, features highly varied national profiles. India’s tier-2 cities endure frequent blackouts, boosting portable uptake; Honda’s 2026 UPS leasing rollout captures this affordability-focused niche. Japan’s typhoon seasons and aging grid elevate standby demand, while Australia’s cyclone belt fuels dual-fuel portable sales. Mainland China’s rural electrification gaps still prompt weekly outages, sustaining low-price gasoline generator volume. Permitting hurdles and fuel-logistics issues slow standby penetration in Indonesia and the Philippines, but inverter portables gain share where noise limits apply in dense urban areas.

Europe blends strict emission policies with growing outage risk as renewable intermittency rises. EU Stage V compliance costs push buyers toward inverter and hybrid sets, and municipal sound ordinances drive less than 60 dBA equipment preference. Storm Éowyn’s 2025 damage to Ireland’s network showed that even advanced grids remain vulnerable. Germany, Italy, and Spain use generous feed-in tariffs to promote solar-battery hybrids, eating into short-duration generator demand. South America clusters demand in Brazil and Argentina, though economic volatility caps high-end sales. The Middle East relies on diesel prime power where grids falter, evidenced by Lebanon’s 80% diesel share, yet income levels support sizeable unit shipments. Sub-Saharan Africa’s 2.5 million annual portable sales reflect urbanization outpacing grid build-out, with South Africa recording 200 load-shedding days in 2023.

Competitive Landscape

The Residential generators market is moderately concentrated. Generac leverages a dense North American dealer network plus telematics to defend share, while its battery-ready product family pre-empts hybrid challengers. Kohler diversifies into hydrogen-compatible and HVO-capable engines to navigate emission tightening. Cummins translates large-scale inverter expertise into premium residential offerings and hit its 10,000-unit milestone at Daventry in 2026. The portable and inverter segments remain fragmented among Honda, Yamaha, Briggs & Stratton, Champion, and emerging battery-station brands such as EcoFlow and Jackery. Dual-fuel innovation represents white space, especially in winter-peaking gas regions flagged by reliability agencies. Strategic moves include Caterpillar’s USD 840 million natural-gas generator agreement with Atlas Energy Solutions that may cascade into high-end residential bundles as distributed generation gains mainstream credibility.

Smart-home integration, predictive maintenance, and demand-response monetization are the new competitive battlegrounds. Battery entrants differentiate with app-centric ecosystems, while engine incumbents add remote diagnostics to close the gap. M&A or strategic partnerships between generator makers and storage vendors are likely as technology roadmaps converge.

Residential Generators Industry Leaders

Generac Holdings Inc.

Kohler Co.

Briggs & Stratton Corporation

Cummins Inc.

Honda Motor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Generac has unveiled its newest line of Diesel Generators tailored for the Indian market. These generators promise reliable, efficient, and consistent power for residential, commercial, and industrial uses. This launch comes hand-in-hand with the expansion of Generac's cutting-edge manufacturing facility in India.

- July 2025: Generac and Highland Homes agreed to pre-install backup systems in new Texas residences.

- April 2025: Generac completed the MOTORTECH purchase, expanding European gaseous-engine controls.

- April 2025: Generac introduced a 26 kW Guardian air-cooled standby model with virtual-power-plant readiness.

Global Residential Generators Market Report Scope

Residential generators supply homes with electrical power during grid outages. These devices vary from portable, manually operated units to permanently installed standby systems. The latter automatically delivers seamless backup power, utilizing natural gas, propane, or diesel. Their primary functions include preventing food spoilage, maintaining heat, and powering essential appliances.

The global residential generators market is segmented by fuel type, power rating, phase, type, technology, application, and geography. By fuel type, the market is segmented into diesel, natural gas, gasoline, solar-battery hybrid, and others. By power rating, the market is segmented into below 3 kW, 3-10 kW, 10-20 kW, and above 20 kW. By phase, the market is segmented into single-phase and three-phase. By type, the market is segmented into portable, standby, and inverter. By technology, the market is segmented into conventional, inverter, and hybrid. By application, the market is segmented into emergency backup, prime/continuous, and recreational/outdoor. The report also covers the market size and forecasts for 18 countries across major regions. Market forecasts are provided in terms of value (USD).

| Diesel |

| Natural Gas |

| Gasoline |

| Solar-Battery Hybrid |

| Others |

| Below 3 kW |

| 3 to 10 kW |

| 10 to 20 kW |

| Above 20 kW |

| Single-Phase |

| Three-Phase |

| Portable Generators |

| Standby Generators |

| Inverter Generators |

| Conventional |

| Inverter |

| Hybrid |

| Emergency Backup |

| Prime/Continuous |

| Recreational / Outdoor |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Fuel Type | Diesel | |

| Natural Gas | ||

| Gasoline | ||

| Solar-Battery Hybrid | ||

| Others | ||

| By Power Rating | Below 3 kW | |

| 3 to 10 kW | ||

| 10 to 20 kW | ||

| Above 20 kW | ||

| By Phase | Single-Phase | |

| Three-Phase | ||

| By Type | Portable Generators | |

| Standby Generators | ||

| Inverter Generators | ||

| By Technology | Conventional | |

| Inverter | ||

| Hybrid | ||

| By Application | Emergency Backup | |

| Prime/Continuous | ||

| Recreational / Outdoor | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Residential generators market by 2031?

It is forecast to reach USD 8.09 billion, expanding at a 6.99% CAGR from 2026-2031.

Which fuel segment is growing fastest in residential backup power?

Solar-battery hybrid systems are advancing at an 11.0% CAGR through 2031 thanks to rebates and falling battery costs.

Why are standby generators gaining share over portable units?

Automatic-start convenience, insurance incentives, and the criticality of zero-downtime remote work drive an 8.2% CAGR for standby systems.

How do emission regulations affect generator choices?

Stricter EPA Tier 2 and EU Stage V limits increase costs for small engines, encouraging buyers to consider inverter or hybrid models that run cleaner.

Which region leads sales of residential generators?

North America holds the largest revenue share at 37.0% due to mature natural-gas infrastructure and frequent weather-related outages.

What technological trend will shape future residential backup solutions?

Integration of lithium-ion storage with inverter gensets will dominate new installations, delivering silent operation and demand-response capability.

Page last updated on: