Market Overview

| Study Period | 2020 - 2031 |

|---|---|

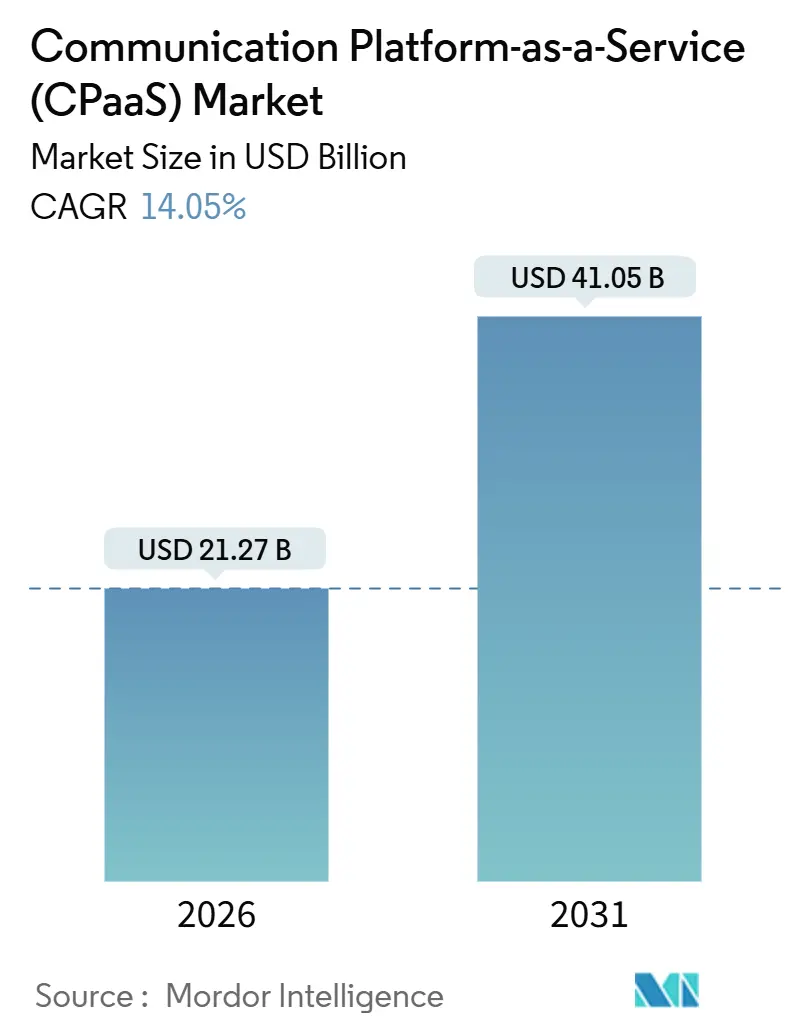

| Market Size (2026) | USD 21.27 Billion |

| Market Size (2031) | USD 41.05 Billion |

| Growth Rate (2026 - 2031) | 14.05% CAGR |

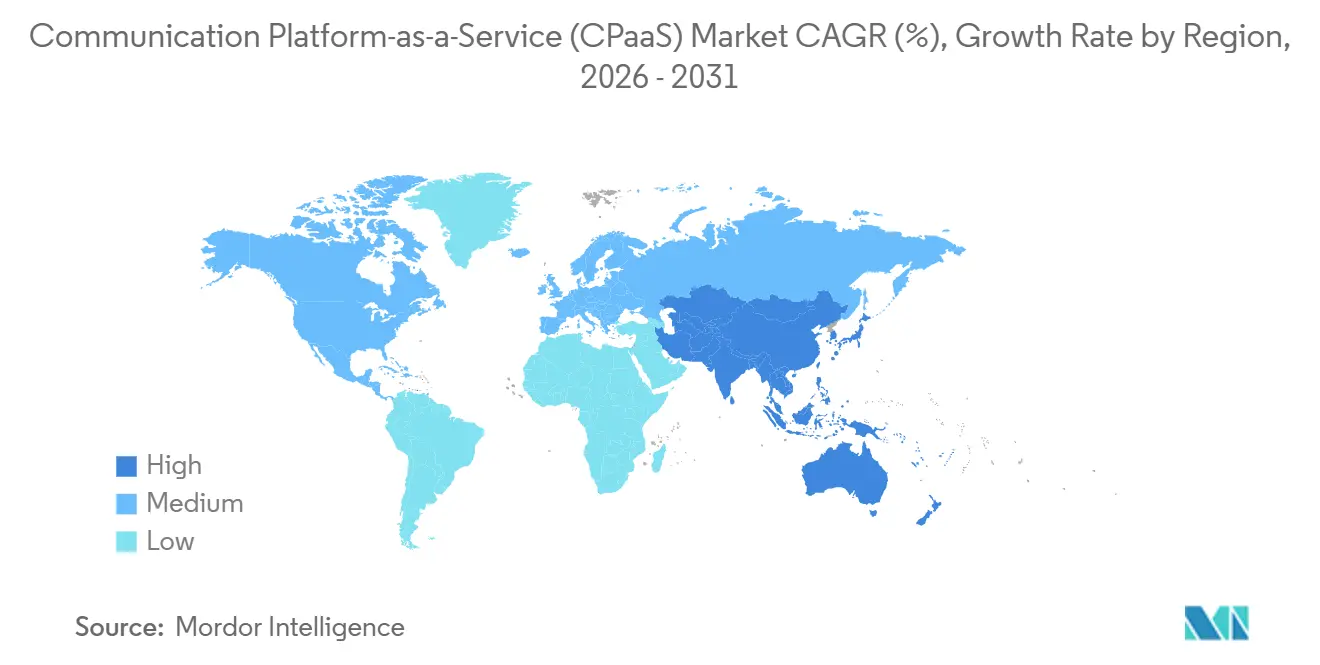

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

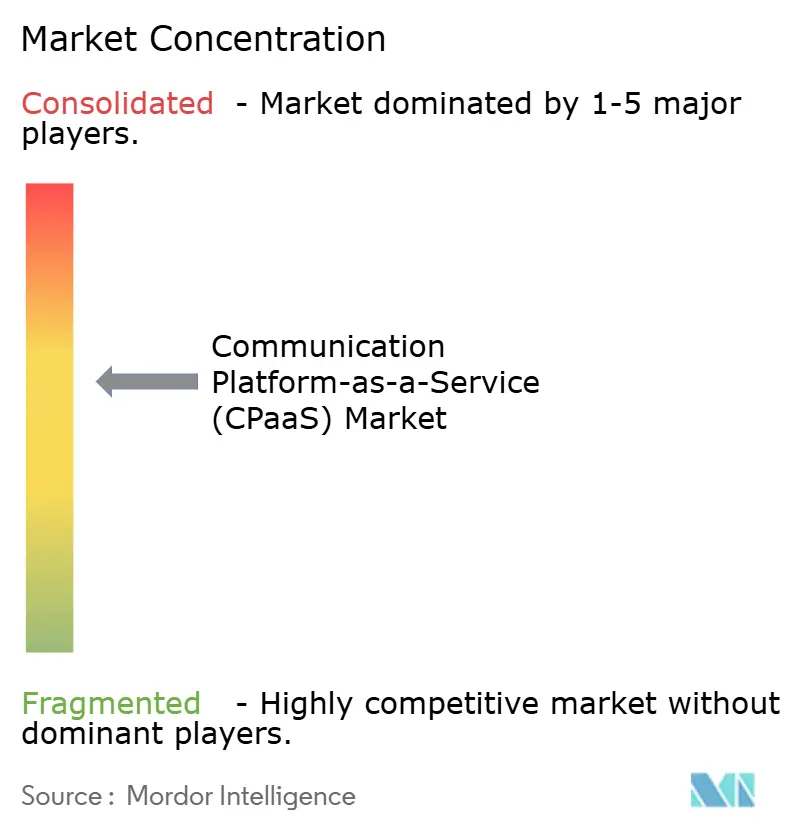

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Communication Platform-as-a-Service (CPaaS) Market Analysis by Mordor Intelligence

The Communication Platform-as-a-Service market size is USD 21.27 billion in 2026, and it is projected to reach USD 41.05 billion by 2031, advancing at a 14.05% CAGR. Heightened demand for embedded voice, messaging, and video is reshaping customer-experience architectures, encouraging firms to swap monolithic contact-center suites for API-first, composable layers that plug directly into digital workflows. Three catalysts drive this shift: stronger authentication rules such as PSD2 in Europe, which require programmable one-time-password flows; the migration of consumers to over-the-top chat channels that enterprises must now unify under a single vendor relationship; and the arrival of 5G network slicing that lets operators carve low-latency lanes for mission-critical workloads. Competitive intensity is rising, yet no vendor controls more than 15%, so the Communication Platform-as-a-Service market still offers white-space opportunities for specialists addressing vertical gaps or regional data-sovereignty requirements.

Key Report Takeaways

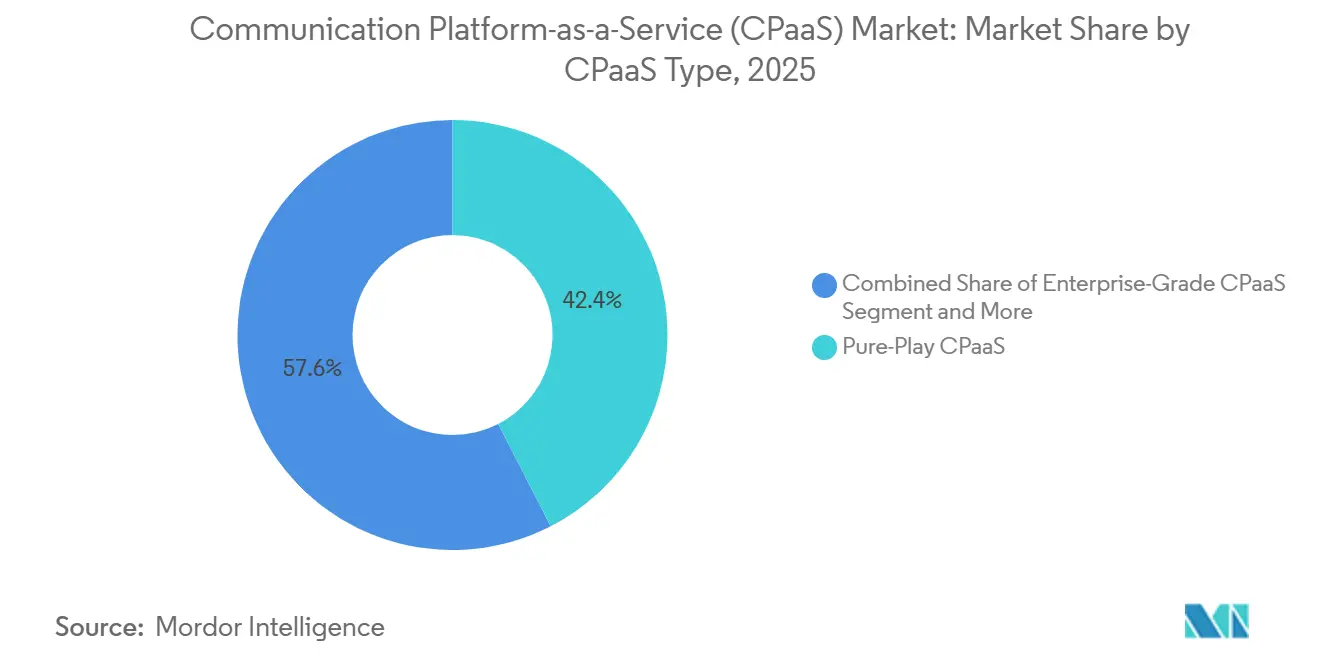

- Pure-play providers captured 42.44% of the Communication Platform-as-a-Service market share in 2025, while telco-driven offerings are projected to grow at a 14.67% CAGR through 2031.

- SMS and A2P messaging led the communication-channel category with 39.21% revenue share in 2025; Rich Communication Services is forecast to expand at a 14.98% CAGR to 2031.

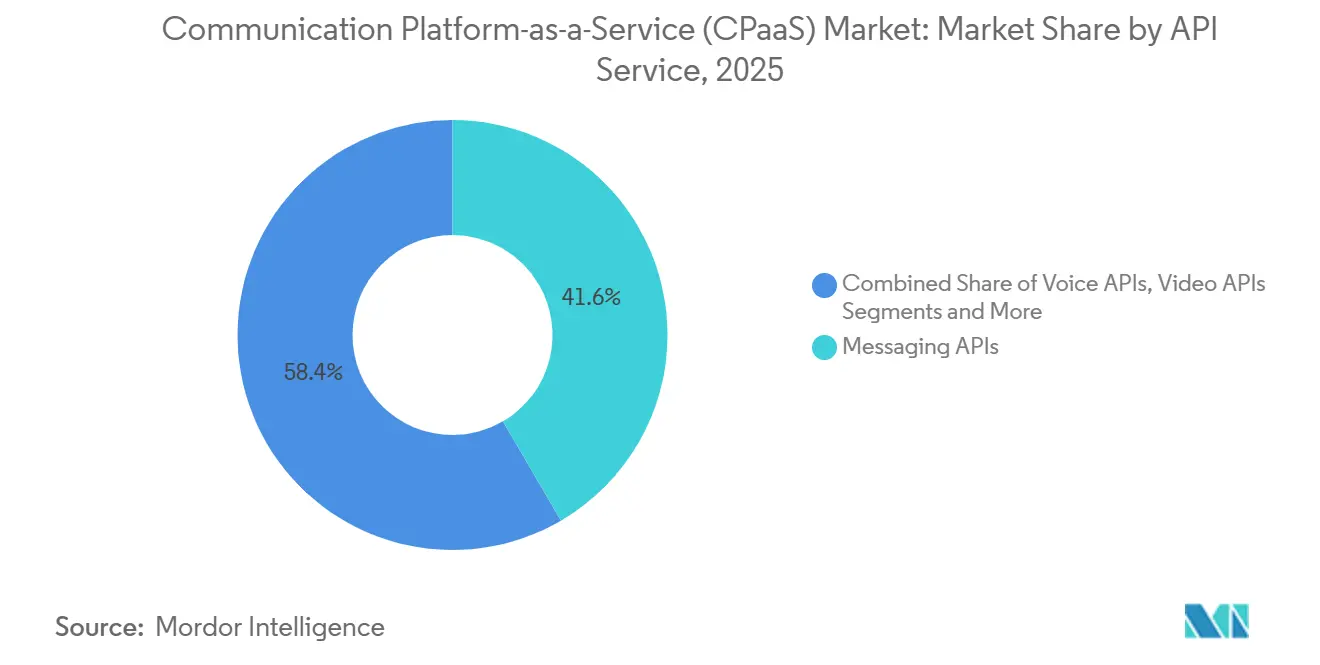

- Messaging APIs accounted for 41.59% of the Communication Platform-as-a-Service market size in 2025, whereas authentication and security APIs are advancing at a 14.67% CAGR through 2031.

- Public-cloud deployments held 57.6% share of the Communication Platform-as-a-Service market size in 2025; hybrid-cloud configurations exhibit the fastest growth at a 15.01% CAGR.

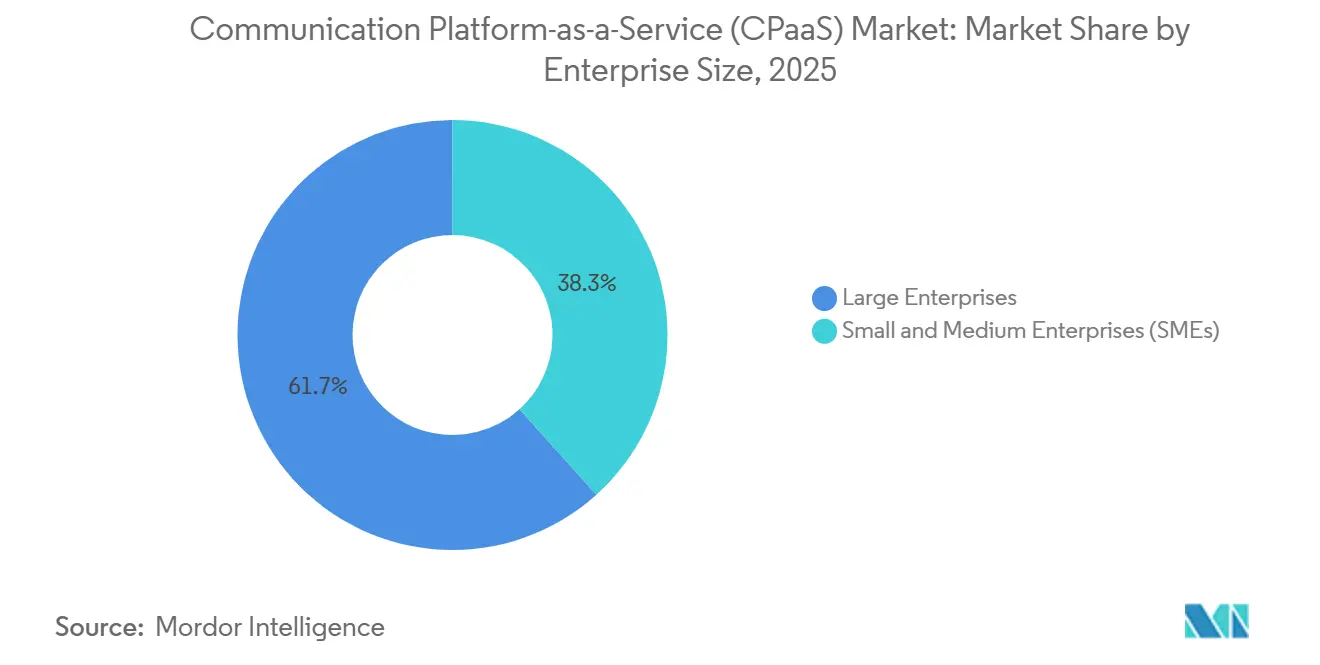

- Large enterprises commanded 61.68% of 2025 revenue, but the SME segment is predicted to expand at a 15.78% CAGR over the forecast horizon.

- IT and telecom led with 27.51% revenue share in 2025; healthcare is the fastest-growing vertical, progressing at a 15.22% CAGR through 2031.

- North America captured 36.01% of 2025 revenue, whereas Asia Pacific is projected to accelerate at a 15.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Communication Platform-as-a-Service (CPaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OTT Chat-Centric Engagement | +2.8% | Global, strong in Asia Pacific and Europe | Medium term (2-4 years) |

| Low-Code / No-Code CPaaS Build-Outs | +2.3% | North America and Europe, expanding in Asia Pacific | Short term (≤ 2 years) |

| PSD2-Driven Programmable Messaging | +1.6% | Europe, spillover to Middle East and Africa | Short term (≤ 2 years) |

| Telco 5G-Anchored CPaaS Innovation | +2.1% | North America, Europe, Asia Pacific | Long term (≥ 4 years) |

| AI-Powered Automation and Analytics | +2.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| IoT and Edge-Integrated Workloads | +1.4% | Asia Pacific and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OTT Chat-Centric Engagement

WhatsApp Business API alone now handles more than 100 billion messages per month, a scale that forced Meta to adopt conversation-based pricing in July 2025.[1]Meta Platforms, “Q2 2025 Earnings,” investor.fb.com Enterprises flock to platforms that maintain turnkey integrations with WhatsApp, Telegram, LINE, WeChat, and Viber because each channel carries unique approval workflows and content rules. Retailers and e-commerce players use these integrations to automate order confirmations, shipping updates, and returns entirely within chat threads, trimming web-portal dependencies. CPaaS vendors incapable of sustaining multi-OTT support risk falling back to commoditized SMS delivery. Even so, data-localization rules in India and Brazil compel providers to keep regional hosting nodes, adding complexity and cost.

Low-Code / No-Code CPaaS Build-Outs

Visual flow builders such as Twilio Studio let non-technical staff design appointment-reminder calls or abandoned-cart campaigns in minutes, removing the need for dedicated developers. Rapid prototyping shortens sales cycles for SMEs and lets large enterprises pilot engagement ideas before allocating engineering budgets. Healthcare clerical workers, for instance, can set up post-consultation SMS follow-ups without IT involvement. The democratization of orchestration tools is broadening the Communication Platform-as-a-Service market by lowering entry barriers, particularly in emerging Asia Pacific where small businesses face acute developer shortages. Compliance with spam-consent rules such as the TCPA in the United States still requires guardrails, so leading vendors embed opt-in management inside their builders.[2]Federal Communications Commission, “TCPA Rules,” fcc.gov

AI-Powered CPaaS Automation and Analytics

Artificial-intelligence modules now underpin routing, sentiment analysis, and predictive outreach. Twilio’s Conversational Intelligence, launched in early 2025, offers pre-trained models that highlight churn risk and upsell opportunities directly within chat transcripts, translating to conversion gains enterprises can quantify. AI engines also forecast the best send time for a given customer, pushing CPaaS from reactive service plumbing to proactive revenue catalysts. Regulatory frameworks such as the European Union’s AI Act mandate explainability and opt-out mechanisms, so providers that document training datasets and expose model governance dashboards hold a compliance edge.

Telco 5G-Anchored CPaaS Innovation

Operators leverage network slicing to deliver ultra-low-latency paths for video consults or augmented-reality troubleshooting, capabilities that over-the-top vendors struggle to replicate without local carrier deals. Verizon’s 5G Edge and Deutsche Telekom’s MagentaBusiness CPaaS suite bundle programmable channels with enterprise contracts, appealing to regulated sectors such as banking and healthcare that demand carrier-grade SLAs. As slicing matures, physical-infrastructure ownership becomes a moat, tilting share toward telco-aligned offers inside the Communication Platform-as-a-Service market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Country-Level A2P SMS Surcharges | -1.8% | India, United States, Europe, rising in Latin America | Short term (≤ 2 years) |

| Enterprise Data-Residency Mandates | -1.3% | Europe, China, India, Indonesia, Middle East | Medium term (2-4 years) |

| Stricter Anti-Spam and Consent Regulations | -0.9% | United States, Europe, India | Short term (≤ 2 years) |

| Growing Messaging and API Security Risk | -1.1% | Global, concentrated in high-volume markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Country-Level A2P SMS Surcharges

Operators in India, the United States, and much of Europe have imposed fees of USD 0.005–0.02 per message on enterprise SMS, eroding margins by up to 25 percentage points for high-volume traffic.[3]Telecommunications Regulatory Authority of India, “DLT Framework,” trai.gov.in Registration systems such as India’s blockchain-based DLT platform and the U.S. 10DLC framework require every template to be pre-approved, lengthening onboarding cycles for time-sensitive alerts. Vendors are nudging customers toward RCS or OTT channels where surcharges do not apply, but fragmented handset support outside developed markets slows migration.

Enterprise Data-Residency Mandates

Regulations in the European Union, China, India, and Indonesia oblige providers to keep messaging metadata and recordings inside national borders, adding 20–40% infrastructure cost versus centralized clouds. Smaller vendors that cannot afford multi-region footprints are being acquired or exiting regulated jurisdictions, tightening vendor selection and potentially tempering innovation in the Communication Platform-as-a-Service industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By CPaaS Type: Pure-Play Dominance Faces Telco Encroachment

Pure-play specialists captured a 42.44% revenue slice of the Communication Platform-as-a-Service market in 2025. Their growth stems from rapid release cadences, unified APIs, and carrier-agnostic routing that speed global expansion. However, telco-driven offerings exhibit the segment’s quickest advance at a 14.67% CAGR to 2031, riding bundled enterprise mobility contracts and direct network access that eliminates a hop in the signaling path.

In practice, multinational banks often dual-source, using a pure-play vendor for omnichannel innovation and a carrier subsidiary for latency-critical authentication inside domestic borders. Hyperscale clouds are now embedding native messaging and voice, narrowing switching costs further. Consequently, the Communication Platform-as-a-Service market is tilting toward hybrid consumption, where enterprises mix API-rich innovation from independents with regulated-workload delivery from mobile-network operators.

By Communication Channel: RCS Poised to Disrupt SMS Hegemony

SMS and traditional A2P traffic retained 39.21% share in 2025, in part because every handset can receive a text even when data connectivity is unreliable.[4]GSMA, “Mobile Economy Asia Pacific 2025,” gsma.com Yet Apple’s iOS 18 added native RCS support in 2024, clearing a major adoption hurdle and driving a 14.98% CAGR for RCS through 2031.

Retailers now embed product carousels and quick-reply buttons inside RCS messages, achieving tap-through rates triple that of plain-text SMS. Enterprises that move early gain richer engagement metrics without forcing customers to install standalone apps. Still, security-sensitive organizations retain voice and interactive-voice-response flows where verbal consent remains mandatory, confirming that a channel portfolio rather than a single medium underpins the Communication Platform-as-a-Service market.

By API Service: Authentication Surges Amid Fraud Epidemic

Messaging APIs enjoyed 41.59% revenue share in 2025, reflecting their versatility and low cost. Rising account-takeover fraud, however, propels authentication APIs at a 14.67% CAGR, the fastest inside this segmentation. Banks now layer voice biometrics and SMS one-time-password flows in parallel, doubling token traffic during high-risk events.

Video, voice, and RCS APIs compete on latency, jitter management, and fraud protection enhancements such as real-time risk scoring. Providers that pre-integrate fraud analytics into the authentication stack justify higher average-revenue-per-user, reinforcing their stake in the Communication Platform-as-a-Service market.

By Deployment Model: Hybrid Architectures Reconcile Cloud Economics with Sovereignty Constraints

Public-cloud nodes generated 57.6% of 2025 revenue thanks to elastic scale and pay-as-you-go pricing. Multinationals are shifting toward hybrid topologies that split non-sensitive marketing traffic into global clouds while keeping regulated workloads in-country, pushing hybrid deployments to a 15.01% CAGR through 2031.

Vendors sustain this pattern by operating data centers in more than 20 jurisdictions, yet that capital intensity raises barriers for newcomers. For customers, hybrid routing lets them fine-tune total cost while staying inside compliance guardrails, an architecture likely to dominate the Communication Platform-as-a-Service market through the decade.

By Enterprise Size: Low-Code Platforms Democratize SME Access

Large enterprises produced 61.68% of 2025 revenue, reflecting sizable messaging volumes and multi-year contracts. SMEs, however, clock the fastest rise at a 15.78% CAGR as visual builders eliminate API fluency hurdles. An e-commerce seller can launch WhatsApp order updates spending under USD 50 per month, growing usage as sales climb.

Template libraries tuned to vertical niches further shrink time-to-value. Consequently, the Communication Platform-as-a-Service market is bifurcating: product-led growth funnels thousands of small customers into pay-go tiers while account teams court Fortune 500 implementations that need bespoke integration and 99.99% SLAs.

By End-User Vertical: Healthcare Telemedicine Drives Fastest Expansion

IT and telecom firms held 27.51% of 2025 spending, but healthcare grows at the vertical peak of 15.22% CAGR through 2031 as telehealth reimbursement moves toward permanence. Clinics embed video consults and prescription reminders, reducing no-shows and driving patient-satisfaction gains.

Retail, BFSI, logistics, and public sector lines also scale CPaaS adoption, yet none match healthcare’s pace. That spread shows how the Communication Platform-as-a-Service market diversifies beyond its software roots into every consumer-facing domain.

Geography Analysis

North America commanded 36.01% of 2025 revenue due to deep cloud penetration, a dense start-up ecosystem, and proximity to hyperscalers. Regional buyers prioritize AI-driven analytics and omnichannel orchestration, translating into premium ARPU that props up vendor profitability.

Asia Pacific is the growth engine, forecast to surge at a 15.90% CAGR to 2031 as smartphone-first economies in India, China, and Southeast Asia leapfrog desktop web to mobile engagement. India’s Unified Payments Interface processed 11.4 billion monthly transactions by late 2025, each triggering real-time alerts that inflate baseline traffic on domestic CPaaS platforms.

Europe retains a solid base order flow anchored in PSD2 authentication, but growth moderates after the initial compliance wave. South America, the Middle East and Africa trail in absolute revenue, though Saudi Arabia and the United Arab Emirates are accelerating due to public-sector digitization. In Africa, coverage gaps mean SMS dominates for now, sustaining a revenue floor for legacy channels inside the Communication Platform-as-a-Service market.

Regulatory Landscape

CPaaS providers operate under telecom and digital communications rules that increasingly treat programmable messaging and voice as regulated pathways for fraud, privacy, and consumer consent. In the United States, the Federal Communications Commission (FCC) has tightened enforcement around robocall mitigation and caller-ID authentication. In July 2026, it published a Know-Your-Upstream-Provider (KYUP) Further Notice of Proposed Rulemaking in the Federal Register, which raises due diligence expectations across upstream voice traffic and STIR/SHAKEN attestation. Consent and opt-out obligations under frameworks such as the Telephone Consumer Protection Act (TCPA) further reinforce the need for auditable opt-in, revocation handling, and template governance inside CPaaS workflows.

Across Europe, compliance is shaped by layered telecom and data requirements, with PSD2-driven authentication flows supporting continued reliance on programmable messaging for financial verification. The EU regulatory agenda is moving into another reform cycle in 2026 through work on a proposed Digital Networks Act. These developments sit alongside international guidance from bodies such as the ITU-T, which approved Recommendations D.265 and D.1141 in April 2025 and D.1142 in November 2025. Together, these recommendations provide policy frameworks that touch tariff principles, personal data protection in big data contexts, and interoperability for IoT and platforms, influencing how CPaaS vendors set pricing transparency, data-handling controls, and integration patterns.

Value Chain Analysis

The CPaaS value chain starts with telecom operators and interconnect partners that provide numbering, termination, SMS/A2P routes, and voice infrastructure. It then moves to CPaaS platform providers that aggregate carrier access and expose messaging, voice, video/WebRTC, email, and authentication capabilities via APIs and SDKs. Above the core APIs, an assembly and orchestration layer packages compliance guardrails (consent capture, template approvals, identity checks) into reusable journey components, increasingly using low-code builders, workflow engines, and AI-assisted routing. The last layer is the enterprise application surface, where CPaaS is embedded into CRM, ITSM, contact center, and vertical systems to power notifications, customer service, verification, and conversational commerce.

Value capture is shifting toward orchestration, assurance, and identity as operators impose tighter controls on A2P messaging routes and regulators elevate verification and anti-fraud expectations for voice traffic. Data-residency mandates and local registration regimes increase the weight of regional hosting, carrier relationships, and documented audit trails, favoring vendors that can combine multi-country delivery, policy-driven routing, and workflow integrations. At the same time, telecom operators are trying to reclaim margin by exposing network capabilities and fraud signals more directly, making the ecosystem more complex as CPaaS providers, telcos, and enterprise-software platforms compete and partner across overlapping layers.

Competitive Landscape

The top five vendors held roughly 45% collective revenue in 2025, signaling moderate fragmentation. Pure-play names Twilio, Vonage, Sinch, Infobip, MessageBird compete on channel breadth and developer experience, releasing weekly API upgrades. Telco affiliates such as Verizon and AT&T bundle CPaaS with connectivity, undercutting standalone vendors on per-message cost and leveraging existing billing relationships.

Consolidation continues: Sinch acquired Pathwire for USD 1.9 billion in 2025, adding email APIs; Bandwidth bought Voxbone’s numbering inventory to widen coverage. Smaller challengers like Plivo and Telnyx differentiate via transparent per-segment pricing and high-touch support.

Hyperscalers loom large: AWS Chime SDK and Azure Communication Services let corporate developers add messaging without leaving familiar cloud consoles. Vendors that layer compliance certifications (ISO 27001, SOC 2, HIPAA BAAs) sustain premium pricing in heavily regulated verticals, thereby defending share in the Communication Platform-as-a-Service market despite the giants’ entry.

Communication Platform-as-a-Service (CPaaS) Industry Leaders

Twilio Inc.

Vonage Holdings Corp

MessageBird BV

Plivo Inc.

Snich AB

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-led productization is creating whitespace for CPaaS vendors that can operationalize anti-fraud and consent requirements as turnkey services, rather than leaving enterprises to stitch controls together. The FCCs June 2026 FNPRM on KYUP obligations and tighter STIR/SHAKEN attestation increases the premium on vendors with strong verification, monitoring, and documentation capabilities for voice. Messaging programs are also moving toward more formal security expectations, including industry bodies updating best practices around SIM-enabled abuse. Providers that package consent capture, revocation handling, template governance, and traffic scoring into low-code journeys can reduce onboarding friction for regulated and high-volume use cases.

Infrastructure and regional partnerships also remain a priority as A2P surcharges, route controls, and data-sovereignty requirements push buyers toward predictable delivery and in-region governance. Twilios disclosed 2026 focus on strengthening direct carrier connections highlights the competitive value of deeper network integration in high-volume markets. Carrier-linked moves such as the Liberty Latin America and Messangi CPaaS partnership to integrate with SMSC infrastructure reflect demand for multi-tenant governance and localized delivery across fragmented geographies. Separately, CPaaS is continuing to converge with CCaaS and enterprise workflow platforms. CPaaS offerings that embed into enterprise systems such as ServiceNow and Salesforce, and deliver verticalized AI-assisted engagement flows, align with budget that is being reallocated from monolithic customer experience suites to composable, API-first architectures.

Recent Industry Developments

- June 2026: Vonage launched industry-specific AI agents for healthcare, financial services, and retail contact centers through partnerships with Avaamo and Syndeo. The release extends CPaaS from channel access into verticalized automation, aligning programmable communications with domain workflows and compliance needs. It also raises competitive pressure on CPaaS vendors to deliver packaged outcomes rather than standalone APIs.

- March 2026: Vonage expanded its partnership with ServiceNow to embed real-time voice and AI capabilities into ServiceNow Voice across customer service and IT service management workflows. This strengthens CPaaS attachment to enterprise operational systems where engagement events originate, supporting usage beyond messaging notifications. The development reinforces the role of native integrations as a distribution channel for programmable communications.

- September 2024: Vonage joined forces with SAP to integrate communications and network APIs with SAP environments, targeting customer engagement and fraud-related use cases. By positioning CPaaS capabilities closer to core business applications, the partnership supports faster adoption for enterprises standardizing on SAP. It also signals broader momentum toward network API consumption and workflow-embedded communications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the CPaaS market covers cloud platforms that let businesses embed communications (such as SMS, voice, video, RCS, email, push, and verification) into their apps and workflows using APIs or SDKs.

Scope exclusions: We exclude pure contact center suites, on-premise PBX hardware, and standalone UCaaS bundles from the market value.

Segmentation Overview

- By CPaaS Type

- Pure-Play CPaaS

- Enterprise-Grade CPaaS

- Telco-Driven CPaaS

- Service-Provider-Based CPaaS

- Hybrid CPaaS

- By Communication Channel

- SMS and A2P Messaging

- Voice and IVR

- Video and WebRTC

- Push and In-App Notifications

- Rich Communication Services (RCS) Messaging

- By API Service

- Messaging APIs

- Voice APIs

- Video APIs

- Authentication and Security APIs

- Rich Communication Services (RCS) APIs

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Vertical

- IT and Telecom

- BFSI

- Retail and E-commerce

- Healthcare

- Travel and Hospitality

- Logistics and Transportation

- Government and Public Sector

- Education

- Other End-User Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public signals that help map the demand pool and the supply side before any modeling begins. We typically review sources such as the FCC and ITU for telecom indicators, the World Bank for macro and digital adoption context, and the OECD for cross-country technology indicators.

To anchor CPaaS specific usage patterns, we also use openly available materials from organizations such as GSMA, plus standards and messaging ecosystem updates from bodies like 3GPP. These are complemented with company filings, earnings call transcripts, investor presentations, and reliable press coverage to track pricing moves, channel shifts, and product focus. When needed, a paid subscription source is used for company financials and intelligence and for patent databases to validate product direction and timelines. The sources listed here are illustrative, and many other references were used for data collection, validation, and clarification during research.

Primary Interviews and Surveys

Primary work is used to pressure test what we see in public sources, especially around monetization (API pricing and platform fees), regional mix, and adoption pace by end users. We speak with a mix of platform-side leaders, channel partners, and enterprise users across key regions, so assumptions around traffic growth, verification demand, and customer churn can be checked and refined.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 37% |

| Mid tier: 52% | Functional/Unit leaders: 27% | EMEA: 36% |

| Smaller Players: 19% | Managers: 59% | Americas: 27% |

Market-Sizing & Forecasting

The core build uses a top-down approach where enterprise communication demand is reconstructed through CPaaS adoption and usage intensity, then translated into revenue using typical pricing and take-rate patterns observed across channels. To keep the model practical, inputs include CPaaS channel mix (SMS, voice, video, RCS, email, push), verification and authentication volumes, price per message or minute trends, platform fee prevalence, and regional enterprise digitization indicators that shape usage frequency.

After forming the top-down totals, we corroborate the result with selective bottom-up approximations, such as sampled vendor revenue disclosures, channel checks on average pricing, and sanity checks using implied traffic volumes times blended ASPs. When bottom-up data is missing for smaller countries or newer channels, gaps are handled through regional proxies and adoption curves discussed in expert sessions, then adjusted during analyst review.

For forecasting, we mainly use scenario analysis supported by a light multivariate regression on a few stable drivers, such as enterprise software adoption, messaging volume growth, and authentication needs. The scenarios are aligned to what interviewees expect for pricing pressure, new channel uptake (like RCS), and regulatory impacts on messaging and verification.

Data Validation & Update Cycle

Model outputs are checked against independent market signals, including reported growth rates, regional demand patterns, and implied usage economics, so outliers can be flagged early. Where variances are large, assumptions are revisited, and if needed, follow-up calls are done to confirm whether the issue is scope, timing, or pricing.

Before sign-off, the work goes through multi-step analyst reviews that look for arithmetic errors, inconsistent drivers, and sudden jumps that do not match industry behavior. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major pricing resets, regulation changes affecting messaging routes, or sharp demand shifts. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Communication Platform As A Service Cpaas Market Size Compared With Other Published Estimates

Published CPaaS market values often differ because each publisher makes different choices on what revenue streams count, which years are treated as the base, and how fast pricing is assumed to change over time. Differences also show up when some sources rely on a single channel proxy, while others attempt to capture a broader set of programmable communications.

The benchmark table shows a spread that is largely explained by scope and monetization treatment, and in Mordor Intelligence's model, CPaaS includes API-driven voice, video, messaging (including RCS), email, push, and verification revenues, while excluding pure contact center suites and standalone UCaaS bundles. Some published figures also lean on aggressive or conservative scenarios for traffic growth and pricing, and they may not re-check assumptions with fresh interviews when routes, termination costs, or authentication demand shift.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.27 B (2026) | |

| Industry Analytics Firm A | USD 14.30 B (2024) | Uses reported platform spending for a single year and may undercount non-messaging channels and platform fees, which can pull the total down versus a broader CPaaS revenue capture. |

| Industry Association B | USD 32.00 B (2025) | Provides a point estimate with limited clarity on inclusions, and the total can rise if adjacent items like wider engagement services or scenario-led upside cases are folded into CPaaS. |

Taken together, the comparison suggests that the biggest driver is not math, it is what is counted and how pricing and channel mix are treated across years. Our approach stays traceable to clear usage and pricing inputs, and it is repeatedly checked with industry feedback so the final number can be explained and replicated in simple steps.

Key Questions Answered in the Report

How big will the Communication Platform-as-a-Service market be by 2031?

It is projected to reach USD 41.05 billion by 2031, expanding at a 14.05% CAGR.

Which channel is growing fastest inside CPaaS portfolios?

Rich Communication Services is forecast to climb at a 14.98% CAGR after Apple enabled native support in iOS 18.

Why are SMEs adopting CPaaS faster than large enterprises?

Low-code builders let non-technical staff deploy messaging flows in minutes, lowering upfront cost and accelerating ROI.

What role does 5G play in CPaaS evolution?

Network slicing lets operators deliver guaranteed-quality lanes for real-time video and AR support, bolstering telco-led CPaaS growth.

Which vertical shows the highest future adoption?

Healthcare leads with a 15.22% CAGR as telemedicine embeds video consults and prescription reminders into patient journeys.

Page last updated on: