Enterprise VSAT System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

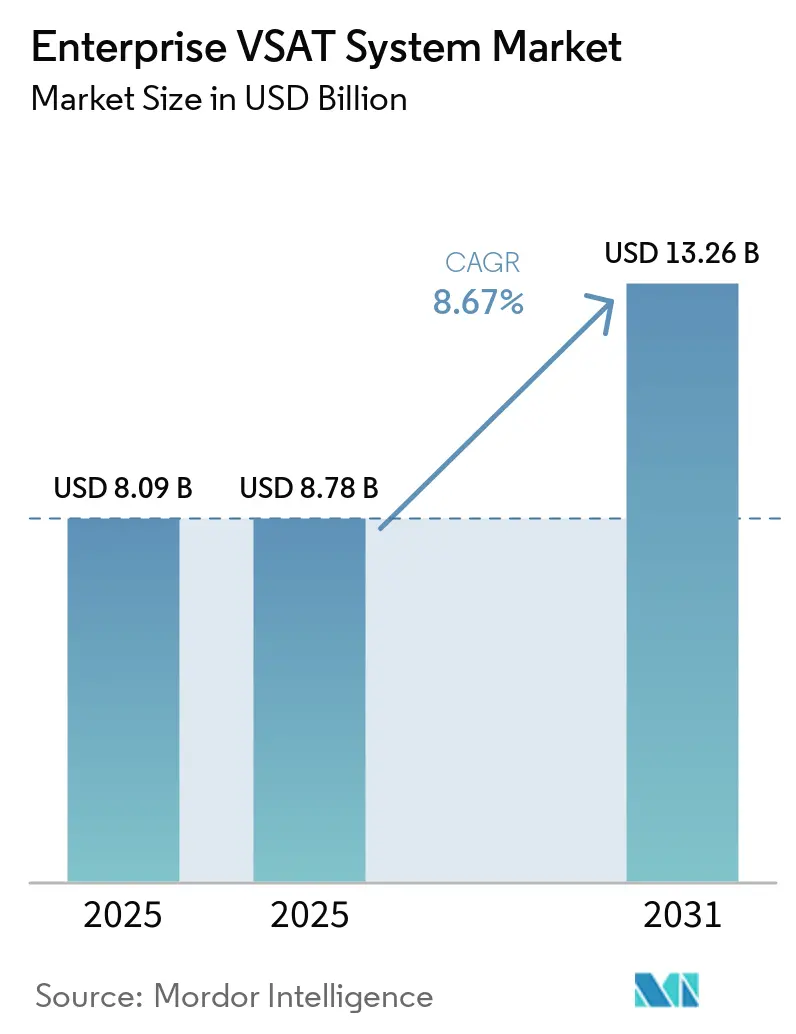

| Market Size (2025) | USD 8.78 Billion |

| Market Size (2031) | USD 13.26 Billion |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

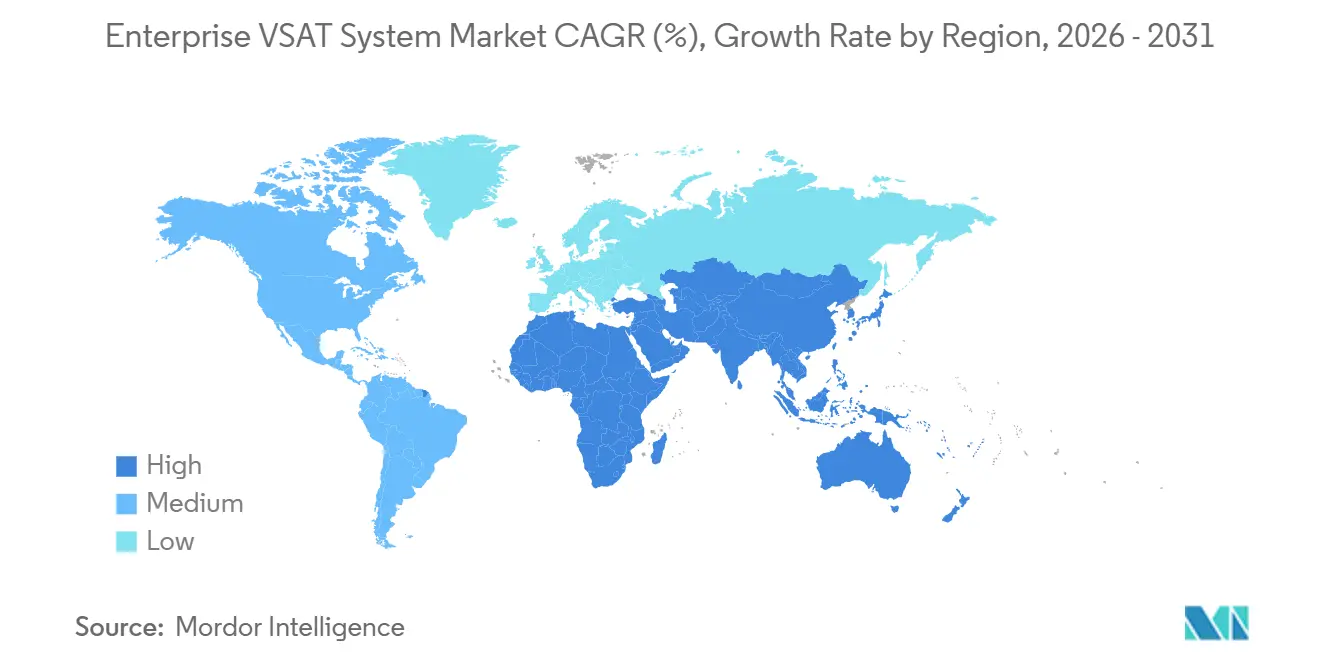

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise VSAT System Market Analysis by Mordor Intelligence

The enterprise VSAT system market size is expected to increase from USD 8.09 billion in 2025 to USD 8.78 billion in 2026 and reach USD 13.26 billion by 2031, growing at a CAGR of 8.67% over 2026-2031. Escalating adoption of high-throughput satellites, maturing flat-panel antenna technology, and 5G non-terrestrial standards are each reducing total cost of ownership, so satellite links are now viable for use cases that previously relied on terrestrial transport. Hardware continued to dominate revenue in 2025, yet managed services are gaining momentum as enterprises outsource network monitoring, cybersecurity, and regulatory filings. Demand is particularly strong for compact electronically steered terminals that simplify vessel and vehicle retrofits. On the supply side, operators are prioritizing Ka-band payloads that can be reconfigured in orbit, enabling them to shift capacity toward sudden spikes in traffic without ground-segment upgrades. Moderate fragmentation of the vendor landscape encourages regional integrators to package terminals, bandwidth, and 24/7 support into single operating-expenditure contracts, positioning the enterprise VSAT system market for sustained expansion.

Key Report Takeaways

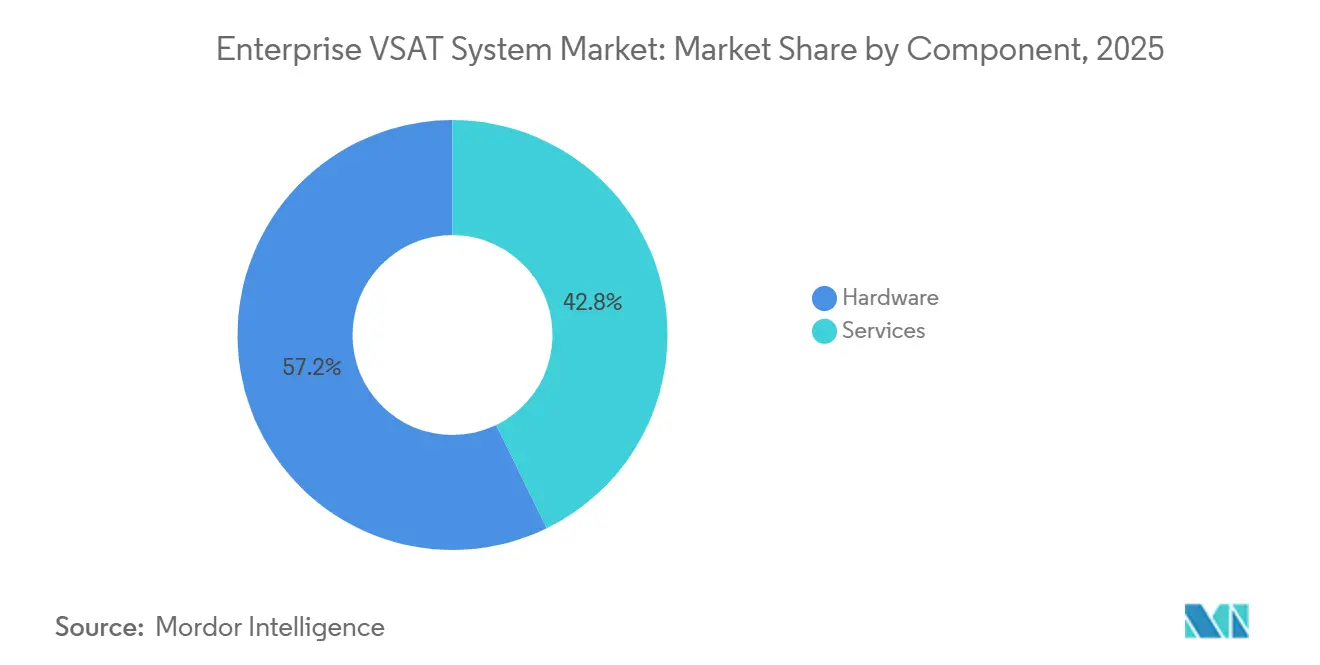

- By component, hardware led with 57.22% revenue share of the enterprise VSAT system market in 2025, while managed services are projected to advance at a 9.98% CAGR through 2031.

- By platform size, Medium Earth Station (1.2-2.4 m) captured 45.67% of the enterprise VSAT system market share in 2025, whereas Small Earth Station (less than 1.2 m) is forecast to grow at a 9.63% CAGR.

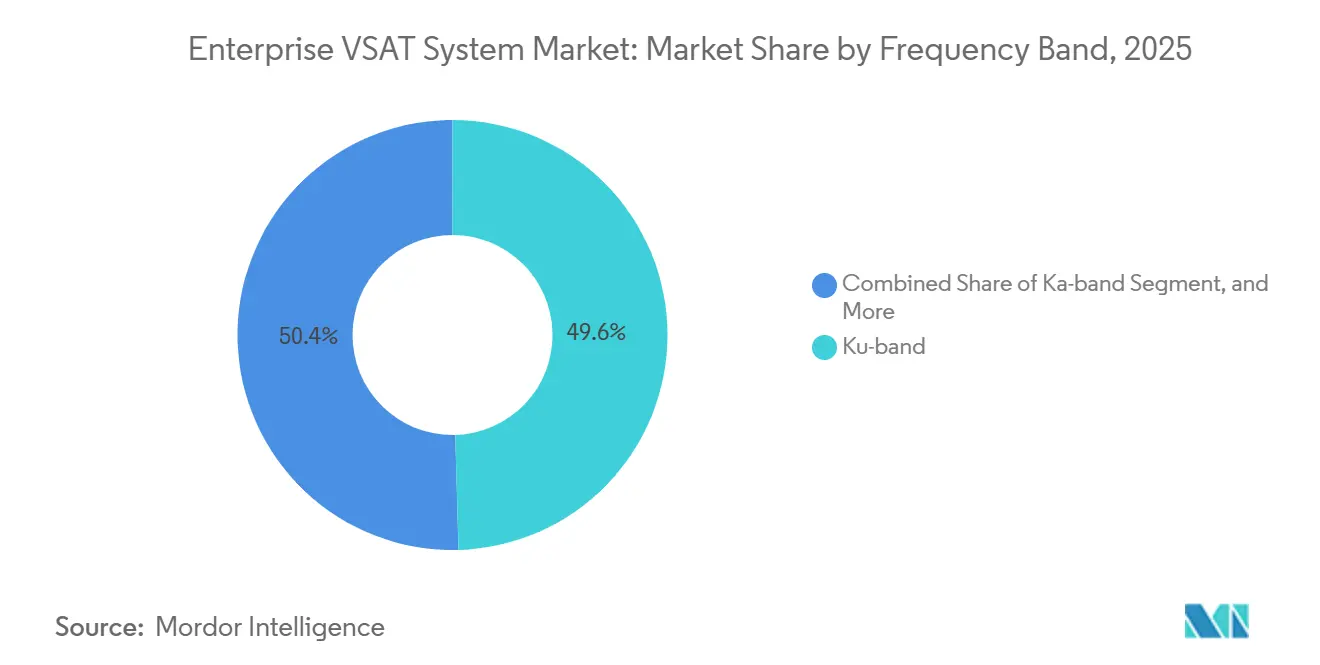

- By frequency band, Ku-band retained 49.56% share in 2025, and Ka-band is poised for 9.19% CAGR growth to 2031.

- By end-user industry, oil and gas accounted for 27.54% of revenue in 2025, but maritime is the fastest-growing segment with an 8.79% CAGR.

- By geography, North America held 34.56% revenue share in 2025, yet Asia-Pacific is on track for the highest regional CAGR of 8.78%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enterprise VSAT System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Broadband Connectivity in Remote and Offshore Sites | +2.1% | North America shale and offshore fields; Middle East Gulf; Asia-Pacific maritime corridors | Medium term (2-4 years) |

| Digital-Oilfield and Smart-Shipping Initiatives Accelerating VSAT Uptake | +1.8% | North America, Middle East, Brazil, Indonesia, Malaysia, Australia | Medium term (2-4 years) |

| Expansion of HTS Constellations Lowering Bandwidth Cost | +1.6% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Growth of Cloud-Based Enterprise Applications Requiring Always-On Links | +1.3% | North America, Europe; spillover to Asia-Pacific | Short term (≤ 2 years) |

| Emergence of Flat-Panel Electronically Steered Antennas Reducing Installation Footprint | +1.0% | Early maritime and defense adopters in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Proliferation of 5G Non-Terrestrial Network Standards Unlocking Enterprise-Grade Service Classes | +0.9% | Pilot deployments in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Broadband Connectivity in Remote and Offshore Sites

Operations in offshore drilling, remote mining, and blue-water shipping now demand symmetric, low-latency links that fiber and cellular often cannot deliver. Petrobras subsidiary Transpetro completed hybrid VSAT and Starlink upgrades across 26 vessels in early 2025, achieving 3-5% fuel savings through optimized routing.[1]Inmarsat Maritime, “Transpetro Completes VSAT and Starlink Installations Across Fleet,” inmarsat.com Movistar Argentina noted 40% year-over-year growth in satellite subscriptions among contractors in the Vaca Muerta shale as of February 2026. Intellian equipped a Petronas floating LNG unit with triple-redundant terminals, underscoring the sector’s willingness to over-provision to avoid costly downtime. ITU radio-regulation frameworks have streamlined licensing, so new enterprise VSAT system market deployments can scale without protracted approvals.

Digital-Oilfield and Smart-Shipping Initiatives Accelerating VSAT Uptake

Sensor-rich drilling programs and data-driven fleet operations convert connectivity into a production enabler. ST Engineering iDirect works with Solutions by stc to monitor wells and refineries under Saudi Arabia’s USD 90 billion digital economy initiative.[2]ST Engineering, “ST Engineering iDirect Partners with Solutions by stc,” stengg.com SES and Viasat Energy introduced sub-150 ms services to offshore platforms in Asia-Pacific, enabling real-time robot control. Shipping lines such as Pacific Basin and Mitsui O.S.K. Lines finalized NexusWave retrofits in 2025 to comply with IMO cyber guidelines and cut unplanned dry-dock visits by up to 30%. The enterprise VSAT system market is benefiting as stakeholders treat bandwidth as a performance lever rather than a utility overhead.

Expansion of HTS Constellations Lowering Bandwidth Cost

Spot Ka-band capacity prices declined below USD 200 per Mbps per month by 2019 and continued falling as new geostationary, MEO, and LEO assets entered service. OmanSat’s November 2025 contract for a software-defined payload that reallocates beams across three regions exemplifies this shift. Viasat merged ViaSat-3 coverage zones in December 2025, enabling multi-region contracts under a single SLA and accelerating procurement cycles. Cheaper megabits expand the addressable base for the enterprise VSAT system market, especially in mid-tier enterprises that previously viewed satellite as cost-prohibitive.

Growth of Cloud-Based Enterprise Applications Requiring Always-On Links

Cloud migration elevates the business impact of even brief outages. RCBC equipped 25% of its Philippine ATM Go estate with Starlink in February 2026 to maintain operations during typhoons. Bank of Guam extended satellite backup across Micronesia to protect against submarine-cable cuts. Speedcast’s integration of Comtech terminals into 3,000 Mexican stores keeps point-of-sale links live and inventory data current. As uptime becomes a board-level metric, satellite fills resiliency gaps, boosting the enterprise VSAT system market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Opex Relative to Terrestrial Alternatives | −1.4% | North America and Europe urban corridors with dense fiber and 5G | Short term (≤ 2 years) |

| Spectrum Congestion and Licensing Hurdles in Key Bands | −0.9% | Europe, North America, Asia-Pacific city belts where 5G overlaps satellite use | Medium term (2-4 years) |

| Escalating Cyber-Attacks on Satellite Ground Segment | −0.7% | Europe, Middle East, Asia-Pacific hotspots | Short term (≤ 2 years) |

| RF Component Supply-Chain Risk Amid Geopolitical Frictions | −0.6% | Global dependence on Chinese gallium arsenide supply | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex and Opex Relative to Terrestrial Alternatives

VSAT hardware, installation labor, and teleport overhead still exceed terrestrial equivalents where fiber or 5G are present. Component shortages in 2024 pushed gallium arsenide LNA prices from USD 28.50 to USD 175. Public filings show Comtech and KVH carried quarterly operating expenses of USD 136.24 million and USD 30.96 million, respectively, highlighting the fixed-cost burden of 24/7 network operations.[3]U.S. SEC, “Comtech Telecommunications Q3 FY2024 10-Q,” sec.gov While remote users accept the premium, urban enterprises weigh the economics carefully, curbing wider uptake within the enterprise VSAT system market.

Spectrum Congestion and Licensing Hurdles in Key Bands

Ku- and Ka-bands face growing interference from expanding 5G allocations, proliferating LEO satellites, and documented spoofing incidents. The ITU condemned Russian interference with European satellites in July 2024. GPS jamming disrupted 46,000 flights across three regions the same year, demonstrating collateral risk. Added coordination requirements extend deployment timelines and inflate engineering budgets, acting as a structural drag on enterprise VSAT system market momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Amid Demand for Turnkey Connectivity

Hardware-dominated revenue in 2025 thanks to up-front terminal purchases, yet managed offerings are outpacing boxes at 9.98% CAGR. The enterprise VSAT system market size for service contracts is rising as organizations fold bandwidth, cybersecurity, and regulatory compliance into OPEX. L3Harris and Comtech’s 5650C2/MP modem simplifies multi-orbit roaming, lowering in-house skill demands. Vendors now bundle orchestration, installation, and ticketing portals, shifting competition toward total cost of ownership rather than sticker price. Integrators leverage bulk capacity deals to shield customers from bandwidth volatility, deepening recurring revenue streams. Hardware innovation continues, Hughes’ HM400 airborne modem targets ISR aircraft, but product releases increasingly act as on-ramps to long-term service agreements.

The enterprise VSAT system market, therefore, reflects broader IT outsourcing trends. Enterprises consolidate suppliers, preferring a single throat to choke for uptime SLAs. Vendors respond by acquiring regional installers and investing in network operations centers, shrinking time-to-deploy and standardizing support across geographies. As service portfolios mature, differentiation leans on cybersecurity overlays and API access that integrate satellite links into DevOps toolchains.

By Platform Size: Flat-Panel Terminals Unlock New Mobility Use Cases

Medium earth stations (1.2-2.4 m) balanced gain and cost to win 45.67% share in 2025. Small terminals under 1.2 m, advancing at 9.63% CAGR, benefit from electronically steered arrays that mount flush on decks and vehicles without mechanical gimbals. The enterprise VSAT system market size for compact antennas grows as maritime and defense customers prioritize reduced wind drag, faster installation, and lower maintenance. Orbit’s OrBeam MIL and Egatel’s retrofit panels exemplify offerings that slide into existing modem ecosystems, minimizing swap-out friction.

Large teleport dishes remain essential for gateways and bandwidth hubs, but enterprise appetite skews toward mobility-ready form factors. Hughes and QEST’s phased array proved multi-satellite tracking in 2024, signaling a future where a single panel can roam across GEO, MEO, and LEO networks. This architecture enhances link resiliency while containing topside real estate on cramped vessel masts.

By Frequency Band: Ka-Band Climbs on Reconfigurable Payloads

Ku-band retains nearly half of 2025 revenue because of its entrenched ground infrastructure. However, Ka-band beams, backed by 9.19% CAGR, unlock higher spectral efficiency and steerable spot-beams. OmanSat’s software-defined satellite typifies capacity that can be redirected within minutes, a critical requirement when offshore demand spikes mid-hurricane season. Kymeta’s KuKa antenna contract with the U.S. Office of Naval Research demonstrates interest in radios that toggle bands instantly, mitigating jamming and rain fade. The enterprise VSAT system market share advantage of Ku-band narrows as Ka-band modem costs fall and regulatory familiarity rises. C-band persists where monsoon rain fade challenges higher frequencies, notably in the Gulf of Mexico and Indian Ocean routes, and L-band retains niches needing global coverage at kilobit data rates.

Operators diversify spectrum holdings to hedge congestion risk. Dual-band terminals give enterprises flexibility to chase the best link margin or avoid contested channels. Licensing, however, remains band-specific, so integrators must package regulatory filings alongside terminals, strengthening the service value proposition.

By End-User Industry: Maritime Surges on Crew Welfare and Cargo Visibility

Oil and gas maintained 27.54% of 2025 revenue, driven by always-on safety systems on offshore rigs and desert pads. Maritime, however, leads growth at 8.79% CAGR as shipping firms install connectivity that meets new crew-welfare bandwidth mandates and supports real-time cargo telemetry. Government and defense sustain steady demand via modernization budgets that replace aging X-band kits with multi-orbit Ka-band systems. The enterprise VSAT system market size attached to banking rises as branch and ATM networks in frontier markets seek uptime during storms and civil outages, illustrated by RCBC’s Starlink rollout.

Telecom operators extend 4G and 5G footprints via satellite backhaul in archipelago nations, while miners deploy links for autonomous haulage vehicles deep in the outback. Retail chains use VSAT as primary or failover networks to keep payments flowing even when terrestrial circuits falter. As terminal prices fall and managed services simplify onboarding, a long-tail of construction, forestry, and emergency response users is expected to join the installed base.

Geography Analysis

North America contributed 34.56% of 2025 revenue, underpinned by defense procurement and shale activity, yet urban saturation of fiber and 5G caps incremental growth. Viasat’s unified Ka-band service eliminates cross-border contract friction across Canada, the United States, and Mexico, accelerating regional deployments. Multiple U.S. Department of Defense contracts awarded to Gilat and L3Harris during 2025-2026 reinforce the strategic value of satellite redundancy.

Asia-Pacific is the fastest-growing territory with an 8.78% CAGR outlook. National oil companies in India, Indonesia, and Malaysia are digitizing assets that sit beyond terrestrial reach. SES’s O3b mPOWER low-latency links empower subsea robot operations and live data collaboration, while Pacific Basin and Mitsui O.S.K. Lines have already outfitted full fleets to meet IMO cyber-resilience rules. Indonesia’s BRIsat illustrates how banking networks exploit domestic satellites to blanket rural archipelagos.

Europe’s fiber richness restrains broad adoption, yet specialty use cases, North Sea rigs, Baltic shipping, defense mobility, sustain niche growth. The ITU’s public censure of cross-border jamming spotlights the geopolitical sensitivity of continental satellite assets. In the Middle East, Saudi Arabia’s digital economy vision drives nationwide deployments through partnerships between local telcos and global modem vendors. OmanSat’s software-defined satellite, Es’hailSat’s North Africa extension, and Eutelsat’s KONNECT deal in Côte d’Ivoire confirm that emerging economies view satellite as the quickest route to universal broadband.

South America benefits from Brazil’s pre-salt assets and Argentina’s shale revolution. Anatel’s March 2026 license approvals permit Viasat to blanket Brazil, while Transpetro’s early success with hybrid terminals illustrates tangible fuel savings. Africa remains an under-penetrated frontier; capacity deals such as MTN Côte d’Ivoire’s with Eutelsat show promise, but fragmented regulation and limited purchasing power moderate the near-term curve of the enterprise VSAT system market.

Competitive Landscape

The top five vendors command roughly 40-45% of global revenue, earning the enterprise VSAT system market a moderate concentration profile. Viasat’s December 2025 network unification signals a pivot from transponder leasing toward vertically integrated service orchestration. ST Engineering iDirect extends reach by partnering with national carriers that package VSAT with terrestrial MPLS, while integrators leverage volume discounts to wrap equipment, installation, and 24/7 monitoring into predictable OPEX.

Antenna innovators such as Kymeta and Isotropic Systems reduce switching costs by enabling terminals to roam multiple constellations. L3Harris and Comtech’s multi-orbit modem lowers vendor lock-in by allowing enterprises to swap satellites on the fly. Release 17 and 18 of 3GPP cement roaming between 5G terrestrial and satellite networks, which could shift value capture from hardware manufacturers toward software orchestration layers and managed-service providers.

White-space opportunities persist in branch banking, frontier retail, and autonomous mining, where reliability trumps raw throughput. Vendors that integrate cybersecurity, zero-touch provisioning, and spectrum analytics into turnkey offerings stand to win share as enterprises pursue fewer suppliers with broader shoulders. Given the pace of flat-panel R&D and Ka-band launch manifests, competitive dynamics will hinge on bagging anchor-tenant contracts that guarantee long-haul capacity utilization.

Enterprise VSAT System Industry Leaders

Hughes Network Systems LLC

ViaSat Inc.

ST Engineering iDirect

Gilat Satellite Networks Ltd.

Comtech Telecommunications Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Kymeta won a U.S. Office of Naval Research contract to deliver a KuKa flat-panel antenna that switches bands within milliseconds for maritime trials.

- April 2026: Eutelsat and MTN Côte d’Ivoire signed a multi-year KONNECT deal to extend broadband across West Africa.

- March 2026: L3Harris and Comtech debuted the 5650C2/MP multi-orbit modem, enabling hands-off GEO-MEO-LEO transitions.

- March 2026: Hughes introduced the HM400 airborne modem under the AFRL RAPID STAR-FISH program.

Global Enterprise VSAT System Market Report Scope

The Enterprise VSAT System Market pertains to the global industry focused on Very Small Aperture Terminal (VSAT) satellite communication systems. These systems enable enterprises to provide reliable broadband connectivity in remote, underserved, and mobile locations, particularly where terrestrial networks are insufficient.

The Enterprise VSAT System Market Report is Segmented by Component (Hardware, Services), Platform Size (Small Earth Station, Medium Earth Station, Large Earth Station), Frequency Band (Ku-Band, C-Band, Ka-Band, Other Frequency Band), End-User Industry (Oil and Gas, Maritime, Government and Defense, Banking and Financial Services, Telecom and IT, Mining, Energy and Utilities, Retail, Other End-User Industry), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Services |

| Small Earth Station (Less Than 1.2 m) |

| Medium Earth Station (1.2-2.4 m) |

| Large Earth Station (Greater Than 2.4 m) |

| Ku-Band |

| C-Band |

| Ka-Band |

| Other Frequency Band |

| Oil and Gas |

| Maritime |

| Government and Defense |

| Banking and Financial Services |

| Telecom and IT |

| Mining |

| Energy and Utilities |

| Retail |

| Other End-User Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Hardware | ||

| Services | |||

| By Platform Size | Small Earth Station (Less Than 1.2 m) | ||

| Medium Earth Station (1.2-2.4 m) | |||

| Large Earth Station (Greater Than 2.4 m) | |||

| By Frequency Band | Ku-Band | ||

| C-Band | |||

| Ka-Band | |||

| Other Frequency Band | |||

| By End-User Industry | Oil and Gas | ||

| Maritime | |||

| Government and Defense | |||

| Banking and Financial Services | |||

| Telecom and IT | |||

| Mining | |||

| Energy and Utilities | |||

| Retail | |||

| Other End-User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current enterprise VSAT system market size and its expected value by 2031?

The enterprise VSAT system market is valued at USD 8.78 billion in 2026 and is projected to reach USD 13.26 billion by 2031, reflecting an 8.67% CAGR.

Which component segment is growing fastest within enterprise VSAT deployments?

Managed services are the fastest-growing segment, expanding at a 9.98% CAGR through 2031 as enterprises shift from capex-heavy hardware models to turnkey OPEX-based service contracts.

Why is Ka-band gaining momentum over Ku-band?

Ka-band offers steerable spot beams and declining capacity costs, enabling dynamic bandwidth allocation, higher throughput, and more competitive pricing compared with Ku-band.

Which industry vertical is expected to drive the next wave of VSAT adoption?

Maritime is the fastest-growing vertical, advancing at an 8.79% CAGR, driven by investments in crew welfare connectivity and real-time cargo and vessel monitoring.

How are multi-orbit modems changing enterprise procurement decisions?

Multi-orbit modems that operate across GEO, MEO, and LEO networks reduce vendor lock-in, enable real-time cost optimization, and improve network resiliency against congestion or jamming.

What regional market offers the strongest growth outlook?

Asia-Pacific leads in growth at an 8.78% CAGR, supported by offshore energy developments, maritime fleet upgrades, and satellite backhaul for remote cellular infrastructure.

Page last updated on: