Digital Isolator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

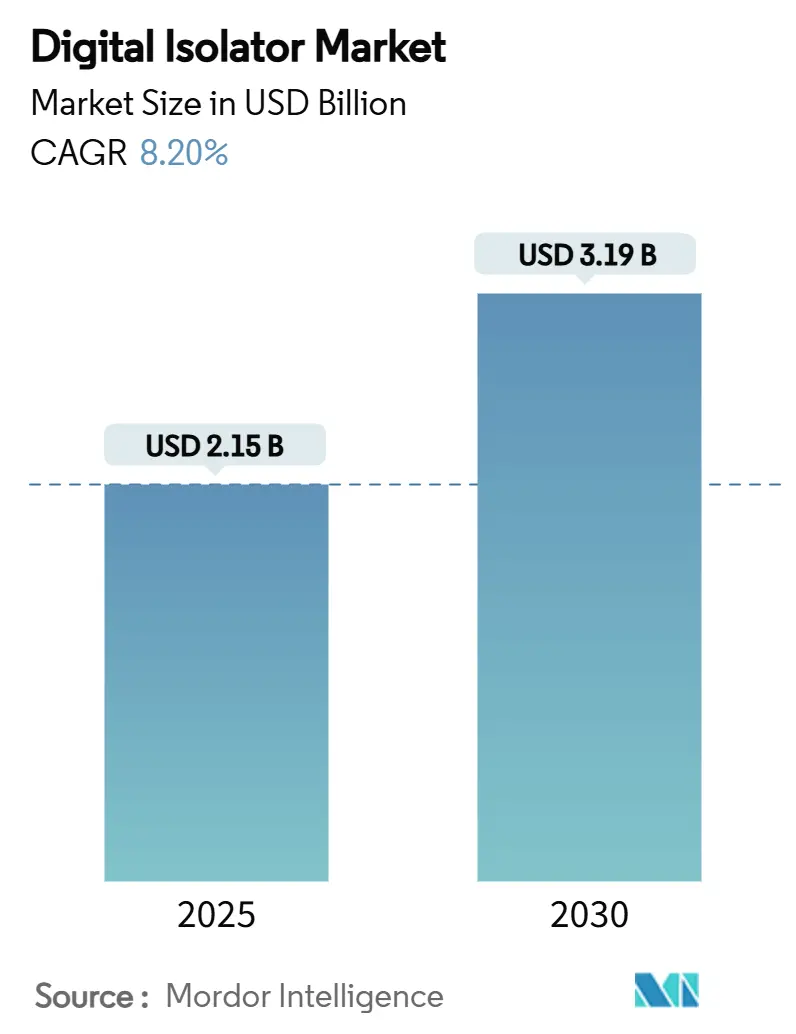

| Market Size (2025) | USD 2.15 Billion |

| Market Size (2030) | USD 3.19 Billion |

| Growth Rate (2025 - 2030) | 8.20% CAGR |

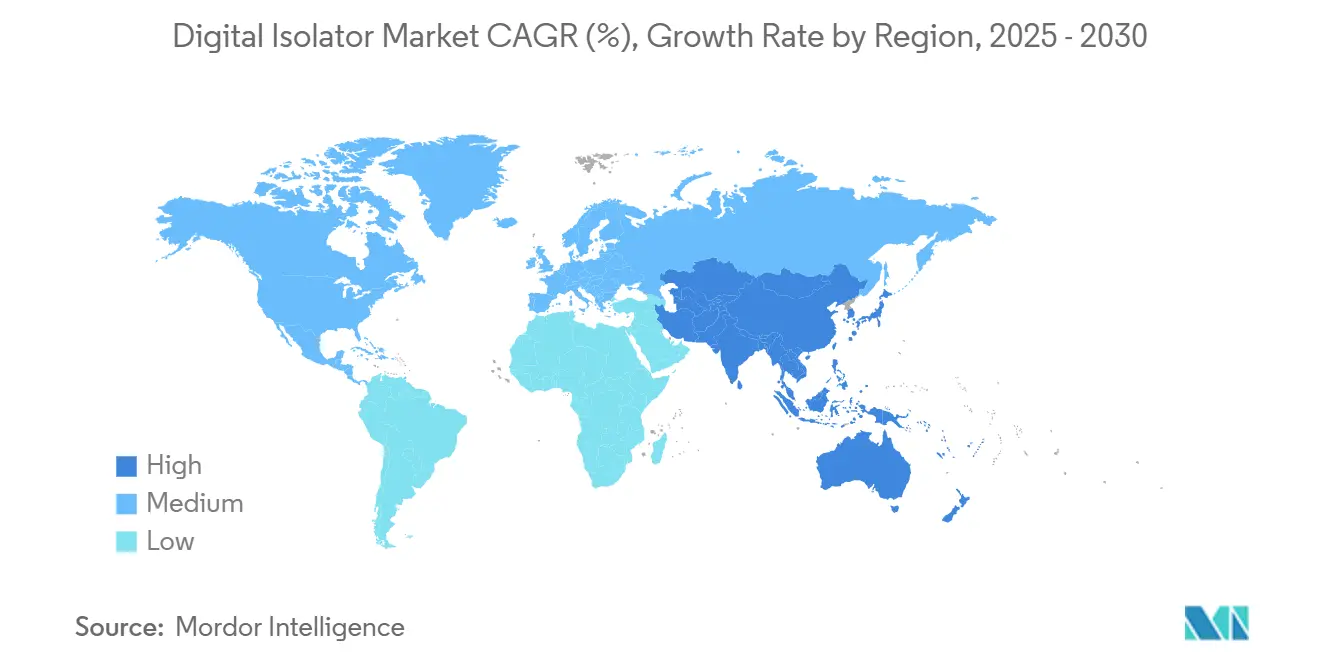

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

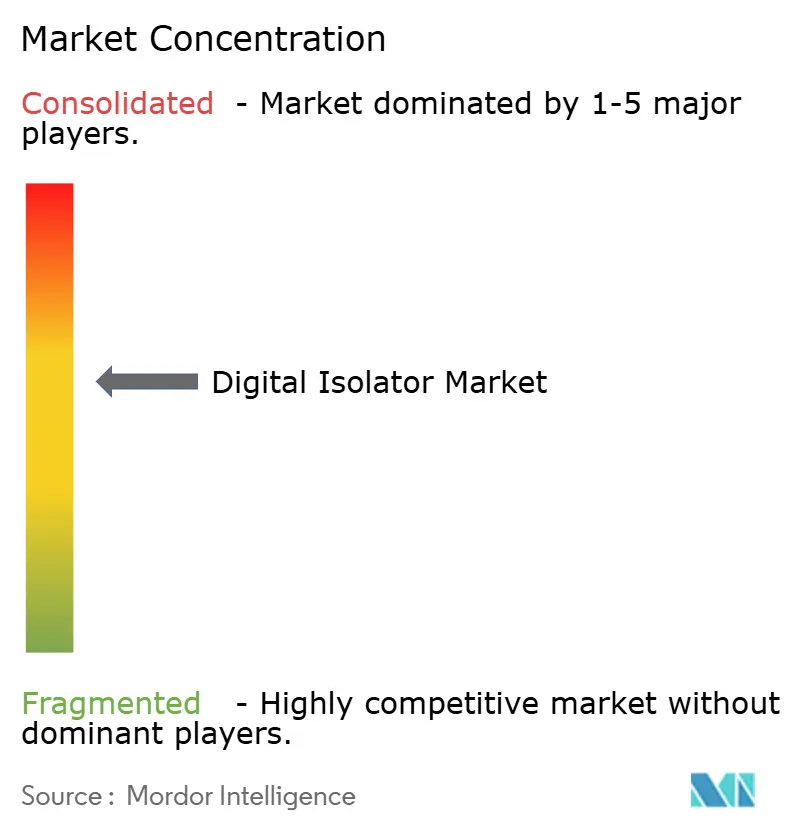

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Isolator Market Analysis by Mordor Intelligence

The digital isolator market size stands at USD 2.15 billion in 2025 and is on track to reach USD 3.19 billion by 2030, reflecting an 8.2% CAGR during the forecast period. Growth comes from rapid Industry 4.0 investments, accelerating electric vehicle platforms, and stringent medical-device safety mandates that are prompting a shift away from optocouplers toward advanced capacitive and magnetic isolation. Industrial automation projects increasingly demand isolation that supports data rates above 150 Mbps while maintaining kilovolt-level surge capability, which directly boosts the digital isolator market. Automotive OEMs adopting 800 V battery systems need gate-driver isolation that withstands dv/dt values beyond 50 kV/µs, widening revenue opportunities for suppliers offering reinforced barriers. Medical device makers seek reinforced leakage protection under IEC 60601-1, creating steady demand for polyimide-based isolation rated to 5 kVrms. Finally, the transition from optical to digital coupling cuts power draw by up to 90%, which aligns with the energy-efficiency priorities of edge devices and battery-powered sensors.

Key Report Takeaways

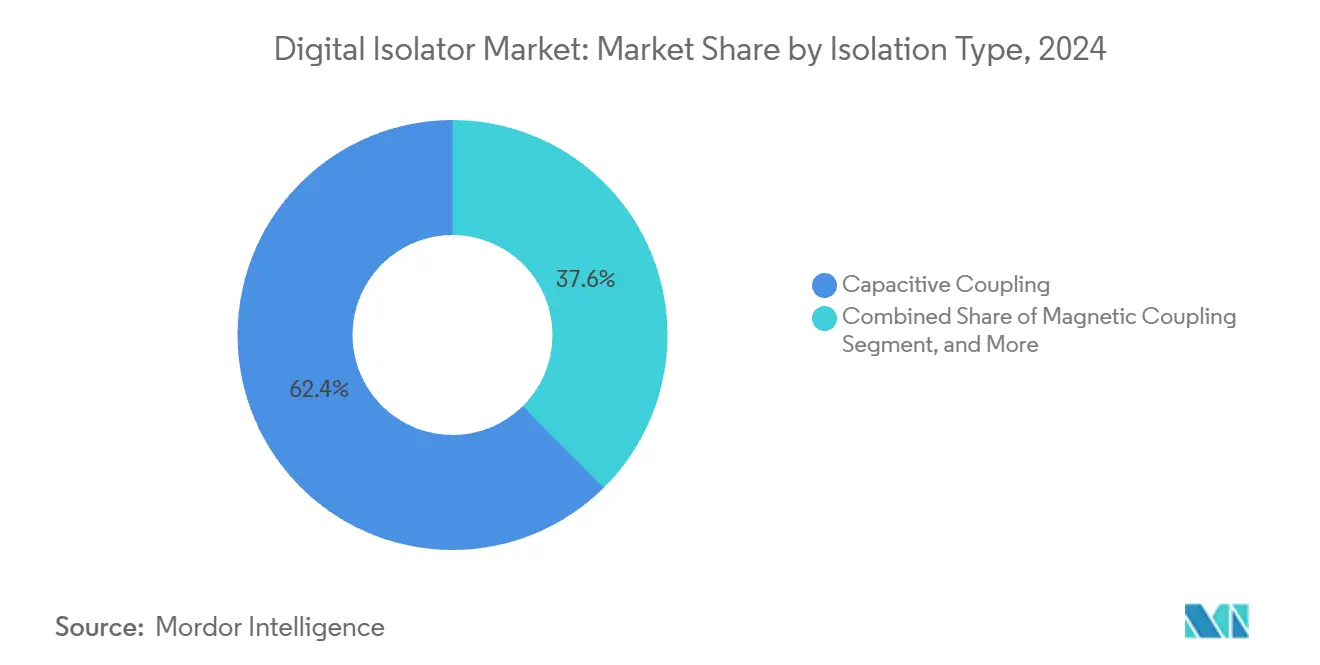

- By isolation type, capacitive coupling led with 62.4% revenue share in 2024; giant magnetoresistive solutions are projected to expand at an 11.4% CAGR through 2030.

- By channel count, 4 channels led the market with a 31.6% market share in 2024, while 8 channels recorded the highest projected CAGR of 9.8% through 2030.

- By data rate, the 25–75 Mbps data rate segment accounted for 52.7% of the digital isolator market size in 2024. The segment with a data rate greater than 75 Mbps showed the fastest growth, at a CAGR of 11.7%, through 2030.

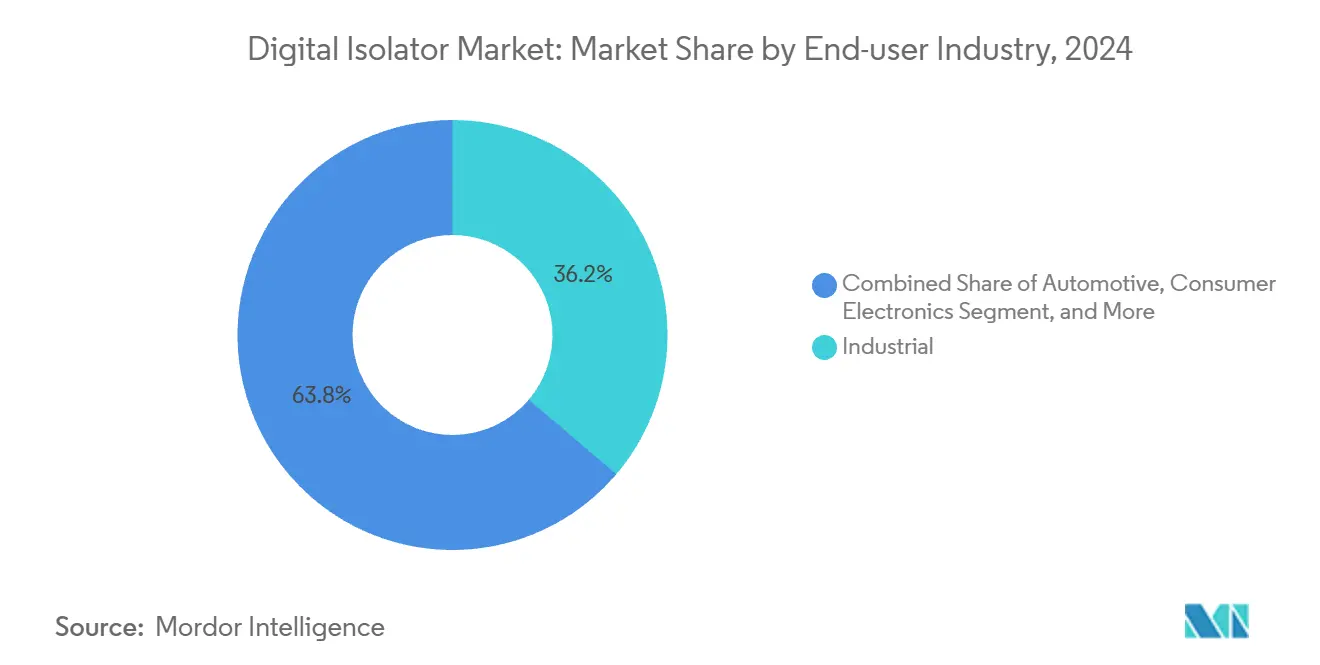

- By end-use industry, industrial automation accounted for 36.2% of the digital isolator market share in 2024, while automotive applications were projected to have the highest CAGR of 12.1% through 2030.

- By application, gate-driver applications accounted for 30.3% of the digital isolator market size in 2024; USB and other interface categories are expected to show the fastest growth, at a 10.3% CAGR, through 2030.

- By geography, the Asia-Pacific region commanded 47.8% of the digital isolator market size in 2024 and is projected to advance at a 10.6% CAGR through 2030.

Global Digital Isolator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption in industrial automation and Industry 4.0 | +1.8% | Global, with APAC leading adoption | Medium term (2-4 years) |

| EV and hybrid vehicle demand for isolated gate drivers | +2.1% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) |

| Rising need for signal isolation in medical devices | +1.2% | North America and EU regulatory markets | Short term (≤ 2 years) |

| Transition from optical to digital isolators | +1.5% | Global, accelerated in industrial segments | Medium term (2-4 years) |

| Wide-bandgap (SiC/GaN) designs creating high dv/dt environments | +0.9% | APAC manufacturing, global deployment | Long term (≥ 4 years) |

| Cyber-security-driven galvanic isolation for EMI resilience | +0.7% | North America and EU critical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adoption in Industrial Automation and Industry 4.0

Smart factories connect thousands of sensors, drives, and controllers that must exchange data at sub-microsecond latency while surviving kilovolt transients. Designers therefore specify capacitive or magnetic isolators that provide robust electromagnetic immunity in packages up to 40% smaller than legacy optocouplers. Ethernet-APL rollouts in chemicals and oil-and-gas plants further raise channel density requirements, encouraging multi-channel isolators that integrate eight barriers in one SOIC footprint.

Rising Need for Signal Isolation in Medical Devices

IEC 60601-1 tightening in 2024 pushed device makers to leakage limits below 10 µA for patient-connected circuits, leading to reinforced digital isolators built on polyimide film rated 5 kVrms.[1]U.S. Food and Drug Administration, “Electromagnetic Compatibility of Medical Devices,” fda.gov USB-based telehealth equipment now needs 480 Mbps throughput with galvanic isolation, a specification matched by ADuM3160-class components that also cut power by 80% compared with optocouplers.

Transition from Optical to Digital Isolators

Optocouplers lose 50% CTR over a decade of use, whereas silicon-dioxide or polyimide barriers keep timing within spec for 40 years. Capacitive isolators deliver four-fold data-rate gains and 90% lower standby power, enabling battery-powered industrial sensors and handheld diagnostic tools.

Wide-bandgap (SiC/GaN) designs creating high dv/dt environments

Wide-bandgap semiconductors, such as silicon carbide (SiC) and gallium nitride (GaN), are driving advancements in power electronics by enabling dv/dt rates exceeding 100 kV/µs, thereby challenging traditional isolation components. Digital isolators with CMTI above 150 kV/µs ensure signal integrity in high-speed systems. As the adoption of SiC and GaN in EV powertrains, solar inverters, and industrial drives grows, vendors are enhancing dielectric materials and isolation packages with surge withstand ratings of up to 6 kV. These isolators, with low propagation delay and minimal skew, are critical for precise timing in PWM control loops, making them essential for safety and performance in power conversion systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity in consumer electronics | -1.40% | Global, particularly APAC manufacturing | Short term (≤ 2 years) |

| Automotive functional-safety qualification cycles | -0.80% | Global automotive supply chains | Long term (≥ 4 years) |

| Fragmented consumer device categories limit scale economies | -0.60% | APAC manufacturing | Short term (≤ 2 years) |

| Conservative approval timelines favor legacy technology | -0.70% | Global safety-critical sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity in Consumer Electronics

Smartphone and wearable OEMs are pursuing aggressive bill-of-materials cuts, making optocouplers suitable for non-critical isolation even if they draw higher power. Local suppliers in China and Southeast Asia offer low-cost variants, which intensify price wars and slow the adoption of premium digital isolators. [2]Semiconductor Industry Association, “State of the U.S. Semiconductor Industry,” semiconductors.org

Automotive Functional-Safety Qualification Cycles

ISO 26262 programs require multi-year validation with extensive FMEA documentation and 15-year supply continuity commitments, which increase costs and lengthen the time-to-market for new isolation technologies.[3]Microchip Technology, “ISO 26262 Automotive Functional Safety,” microchip.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Isolation Type: Capacitive Coupling Maintains the Lead

Capacitive isolators captured 62.4% of the digital isolator market share in 2024, thanks to CMOS-compatible silicon-dioxide barriers rated up to 5.7 kVrms. This category is expected to post steady single-digit growth as industrial automation and healthcare remain loyal to its low-power profile. Giant magnetoresistive devices post the fastest 11.4% CAGR, propelled by EV traction systems that require robust noise immunity in wide-bandgap switching environments.[4]Allegro MicroSystems, “Tunneling Magnetoresistance Technology,” allegromicro.com Magnetic-transformer options gain a moderate share by offering common-mode transient immunity exceeding 100 kV/µs, which suits motor-drive inverters. Optocouplers continue to decline due to LED aging and limited data-rate capability.

Second-generation GMR sensors now achieve nano-tesla sensitivity across automotive temperature ranges, opening new revenue streams in battery management units that need microsecond-class propagation.[5]NVE Corporation, “GMR and TMR Digital Sensors,” nve.com Capacitive suppliers respond with reinforced polyimide stacks that raise insulation life at 125 °C. Overall, technology transitions keep the digital isolator market dynamic while giving OEMs multiple paths to balance cost, speed, and durability.

By Channel Count: Integration Spurs Efficiency

Four-channel products represented 31.6% of the digital isolator market in 2024, balancing PCB area and flexibility for programmable-logic and sensor-gateway designs. Eight-channel devices enjoy a 9.8% CAGR to 2030 because PLC and battery-string monitors demand high channel density inside tight enclosures. Two-channel parts remain popular in entry-level servo drives and medical probes, while six-channel variants target motor-control boards. Multi-channel integration enables matched delay skew, which is critical for half-bridge gate timing.

Advances in stacked-die bonding let manufacturers embed eight reinforced barriers in one wide-SOIC, trimming board space by 20% compared with discrete pairs. This packaging advantage enhances production yield and reduces test time, underpinning further unit-cost reductions that strengthen the digital isolator market through 2030.

By Data Rate: High-Speed Interfaces Accelerate

Mid-tier 25-75 Mbps isolators held 52.7% of 2024 revenue because most industrial sensors and automotive CAN-FD lines operate within this band. However, digital isolator market demand above 75 Mbps is climbing at an 11.7% CAGR as USB 3.0 and Ethernet-APL push channel bandwidths. Vendors now qualify 480 Mbps USB isolators with 2.5 kVrms reinforcement for medical imaging carts and factory test stations. Data-center network cards moving to 400 GbE need isolation for monitoring and hot-swap control circuits, which further boosts high-speed sales.

Low-speed devices under 25 Mbps still serve level-translation and housekeeping functions where quiescent current under 100 µA is critical. Thus, the digital isolator market caters to a spectrum of speed-power trade-offs rather than forcing a single high-speed roadmap.

By End-Use Industry: Industrial Stays on Top, Automotive Surges

Industrial automation kept a 36.2% revenue share in 2024, helped by edge-computing nodes that require kV-level protection from drive-cabinet transients. Automotive electronics are projected to post the highest 12.1% CAGR, thanks to EV inverters, onboard chargers, and wireless BMS modules that mandate reinforced galvanic barriers. Telecom and data-center operators also adopt digital isolators to shield high-speed transceivers from ground loops, and these segments become secondary growth engines.

Consumer electronics adoption remains sporadic due to price concerns, though emerging AR/VR headsets with high-speed USB-C connections may shift the equation. Medical device buying patterns stay resilient because new IEC 60601-1 editions tighten leakage limits every review cycle. Aerospace and defense sustain low-volume, high-margin demand for radiation-tolerant isolator die.

By Application: Gate Drivers Dominate but Interfaces Emerge

Gate-driver circuits collected 30.3% of 2024 revenue, reflecting the centrality of isolation in power electronics from solar inverters to robot servo drives. Interface isolators for USB, HDMI, and proprietary links show a 10.3% CAGR because industrial PCs and hospital imaging systems need high-throughput mains-safety separation. DC-DC converter feedback and isolated ADCs and DACs remain mid-tier applications.

Power stages based on SiC or GaN now ship with integrated drivers and digital isolators that coordinate protection, fault reporting, and charge delivery within one package. This trend lifts content per module and underpins long-term growth for the digital isolator industry.

Geography Analysis

Asia-Pacific generated 47.8% of the digital isolator market size in 2024 owing to China’s NEV subsidies and Japan’s precision IC packaging capabilities. Regional fabs supply reinforced capacitive and GMR parts that meet AEC-Q100, giving local OEMs cost and logistics advantages. Government incentives for domestic semiconductor production further help suppliers gain share in industrial automation rollouts across Southeast Asia.

North America remains the second-largest region as factories retrofit Industry 4.0 controls and healthcare providers upgrade patient-connected equipment to reinforced isolation. The 2024 CHIPS Act accelerates local wafer capacity, which secures supply for mission-critical applications and supports the digital isolator market through 2030. Demand also comes from data centers that need isolated control in 48 V to 54 V power distribution racks.

Europe shows steady uptake because EU electrification directives push automotive OEMs toward 800 V architectures and home-energy storage systems that rely on safe isolation. German and French industrial conglomerates continue to migrate from optocouplers to capacitive solutions for predictive-maintenance sensor arrays. Eastern Europe’s emerging EMS hubs add price-competitive assembly options, broadening regional consumption.

Competitive Landscape

The digital isolator market exhibits moderate concentration. Analog Devices capitalizes on its iCoupler platform and holds a broad automotive-qualified portfolio that spans capacitive and transformer products. Texas Instruments competes with opto-emulator devices that allow drop-in replacement for legacy optocouplers, simplifying design migrations. Silicon Labs differentiates with ultra-low-power options suited for battery devices, whereas Infineon focuses on high-current gate drivers bundled with SiC power MOSFETs.

Asian challengers such as NOVOSENSE and BrightKing exploit proximity to EV supply chains and deliver cost-effective AEC-Q products, pressuring incumbents on price. Patent disputes around GaN and reinforced insulation reflect intensifying competition, as illustrated by Infineon’s ongoing litigation with Innoscience. Suppliers able to provide isolation, power conversion, and monitoring in one chipset gain a route to design-win lock-in, influencing procurement decisions across industrial and automotive tiers.

Strategic moves include Infineon’s 2025 launch of 20 A EiceDRIVER units for traction inverters, Texas Instruments’ USD 60 billion investment in U.S. fabs that secures local capacity for isolators, and Silicon Labs’ expansion of wireless BMS reference designs. Overall, portfolio breadth, automotive quality processes, and vertical integration drive competitive advantage in the digital isolator market.

Digital Isolator Industry Leaders

Texas Instruments Incorporated

Analog Devices, Inc.

Silicon Laboratories Inc.

Infineon Technologies AG

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vishay unveiled isolation amplifiers with industry-leading common-mode transient immunity for precision applications.

- June 2025: Saelig released Intona 7055 USB 2.0/3.0 isolators rated to 5 kVrms for automation and medical use.

- April 2025: Infineon introduced gallium-nitride power transistors with integrated Schottky diodes targeting telecom power systems.

- May 2025: NOVOSENSE launched an automotive-grade digital isolator family designed for new energy vehicles.

Global Digital Isolator Market Report Scope

| Capacitive Coupling |

| Magnetic Coupling |

| Giant Magnetoresistive (GMR) |

| Optical Isolation (LED-based) |

| Other Isolation Types |

| 2 Channels |

| 4 Channels |

| 6 Channels |

| 8 Channels |

| Other Channel Counts |

| Less than 25 Mbps |

| 25 - 75 Mbps |

| Greater than 75 Mbps |

| Industrial |

| Automotive |

| Telecommunications and Data Centers |

| Consumer Electronics |

| Medical |

| Aerospace and Defense |

| Other End-use Industries |

| DC/DC Converters |

| Gate Drivers |

| ADCs and DACs |

| USB and Other Interfaces |

| Power Supply and Battery Management |

| Isolated Serial Communications |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Isolation Type | Capacitive Coupling | ||

| Magnetic Coupling | |||

| Giant Magnetoresistive (GMR) | |||

| Optical Isolation (LED-based) | |||

| Other Isolation Types | |||

| By Channel Count | 2 Channels | ||

| 4 Channels | |||

| 6 Channels | |||

| 8 Channels | |||

| Other Channel Counts | |||

| By Data Rate | Less than 25 Mbps | ||

| 25 - 75 Mbps | |||

| Greater than 75 Mbps | |||

| By End-use Industry | Industrial | ||

| Automotive | |||

| Telecommunications and Data Centers | |||

| Consumer Electronics | |||

| Medical | |||

| Aerospace and Defense | |||

| Other End-use Industries | |||

| By Application | DC/DC Converters | ||

| Gate Drivers | |||

| ADCs and DACs | |||

| USB and Other Interfaces | |||

| Power Supply and Battery Management | |||

| Isolated Serial Communications | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the global digital isolator market?

The digital isolator market size is USD 2.15 billion in 2025.

What CAGR is expected for the digital isolator market between 2025 and 2030?

The market is forecast to grow at an 8.2% CAGR through 2030.

Which region leads the digital isolator market?

Asia-Pacific leads with 47.8% revenue share in 2024 and the highest 10.6% CAGR outlook.

What isolation technology holds the largest share?

Capacitive coupling dominates with 62.4% market share in 2024.

Which end-use industry is growing fastest for digital isolators?

Automotive electronics show the highest 12.1% CAGR through 2030 due to EV adoption.

Why are digital isolators replacing optocouplers?

Digital isolators offer higher data rates, lower power draw, and longer life without LED degradation.

Page last updated on: