Automotive Ethernet Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

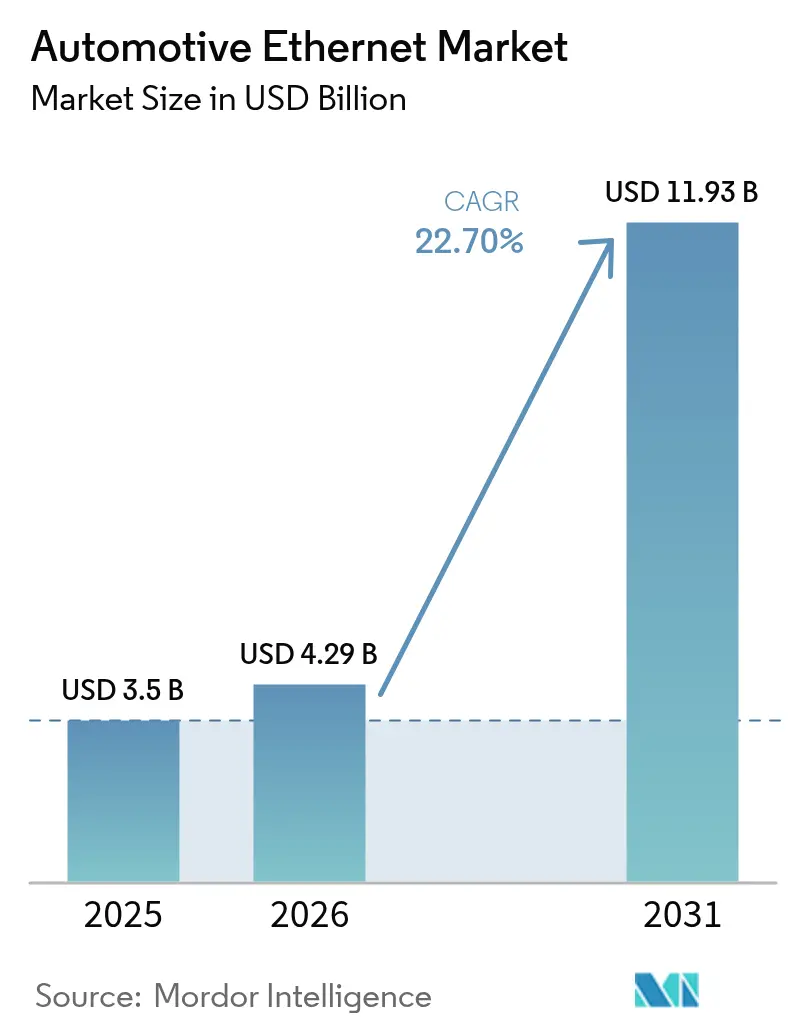

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 11.93 Billion |

| Growth Rate (2026 - 2031) | 22.70% CAGR |

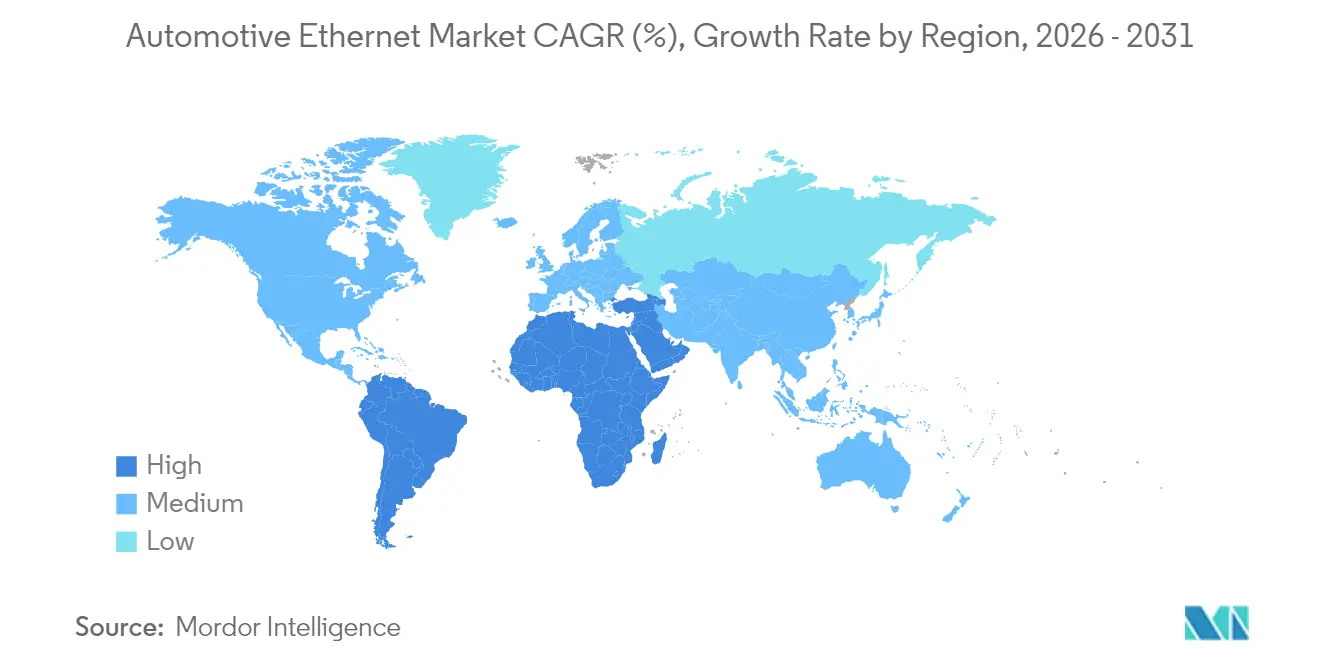

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

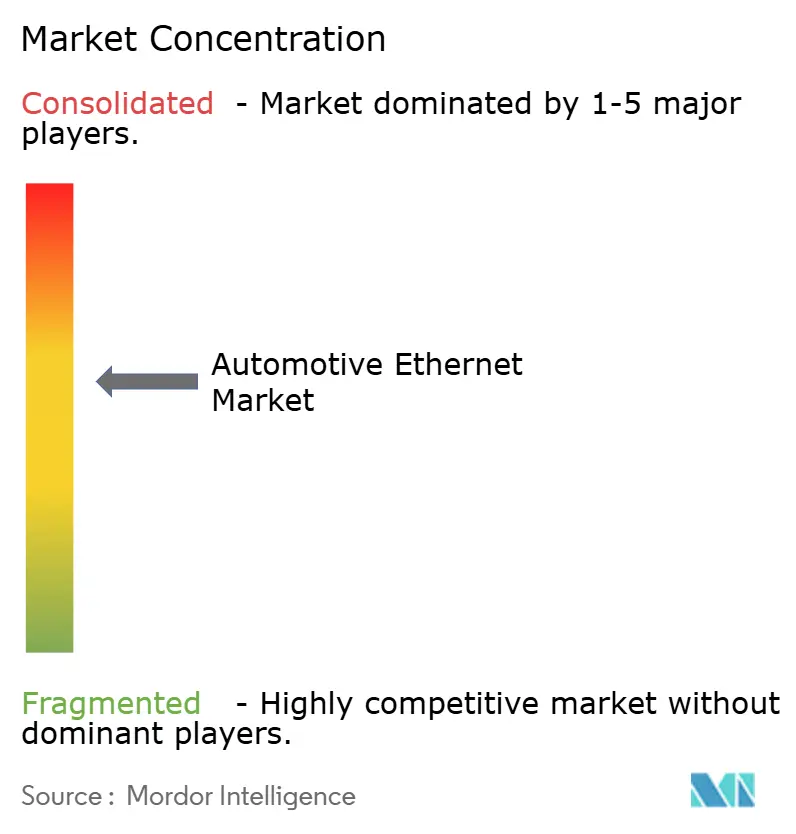

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Ethernet Market Analysis by Mordor Intelligence

The Automotive Ethernet Market size was valued at USD 3.5 billion in 2025 and estimated to grow from USD 4.29 billion in 2026 to reach USD 11.93 billion by 2031, at a CAGR of 22.70% during the forecast period (2026-2031).

The expansion is driven by the move from domain-based electronics to zonal architecture, the rise of software-defined vehicles, and the need for deterministic, high-bandwidth backbones that replace legacy CAN, LIN, and FlexRay buses. Growth momentum is reinforced by strong sensor proliferation in advanced driver assistance systems (ADAS), over-the-air (OTA) software pipelines, and single-pair Ethernet (SPE) deployments that reduce wiring cost and weight. Semiconductor consolidation is reshaping supplier strategies, while ISO 26262 functional-safety and ISO/SAE 21434 cybersecurity obligations create new layers of integration and testing complexity. Interoperability with legacy electronic control units (ECUs) remains a short-term hurdle, yet migration roadmaps are maturing as gateway designs and IEEE time-sensitive networking (TSN) profiles converge. Collectively, these trends keep the Automotive Ethernet market on a strong double-digit growth trajectory with ample white-space opportunities in testing, security, and multi-gig PHY solutions.

Key Report Takeaways

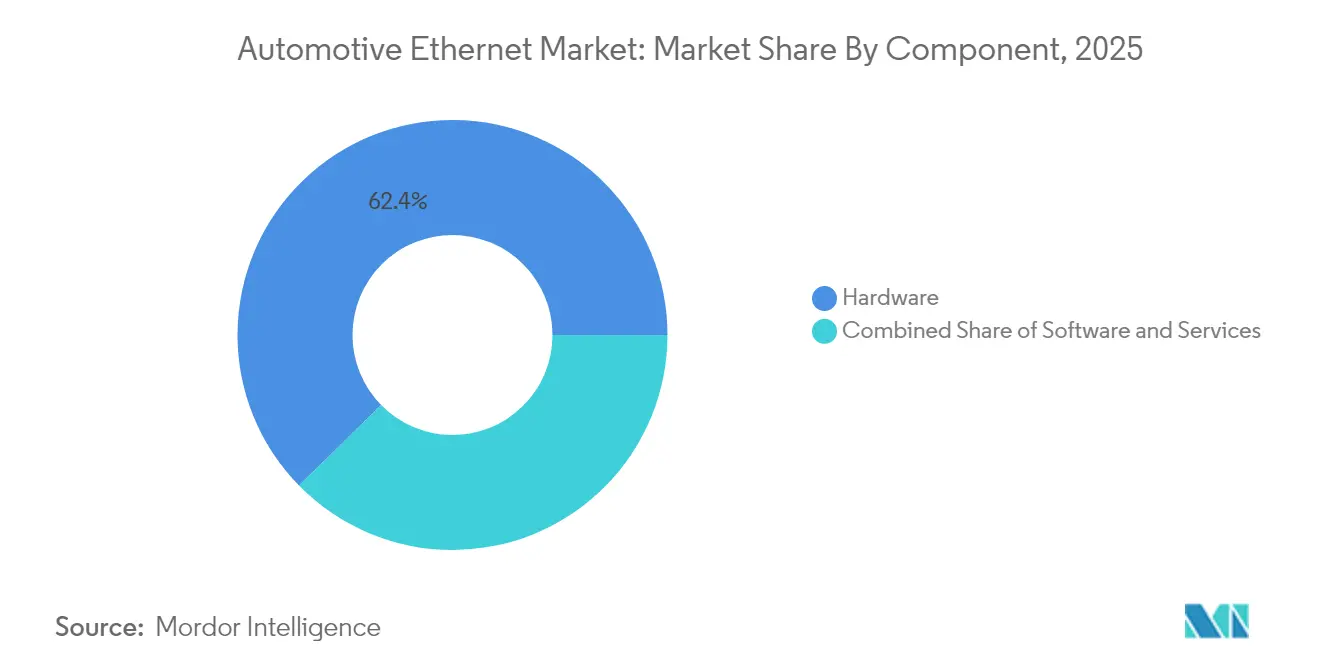

- By component, hardware captured 62.35% of 2025 revenue, while services are projected to expand at a 26.95% CAGR through 2031, reflecting escalating demand for validation and integration expertise.

- By bandwidth, 100BASE-T1 held a 41.10% share in 2025; multi-gig (2.5/5/10 Gbps) speeds are set to grow at a 36.60% CAGR over 2026-2031, propelled by sensor data loads.

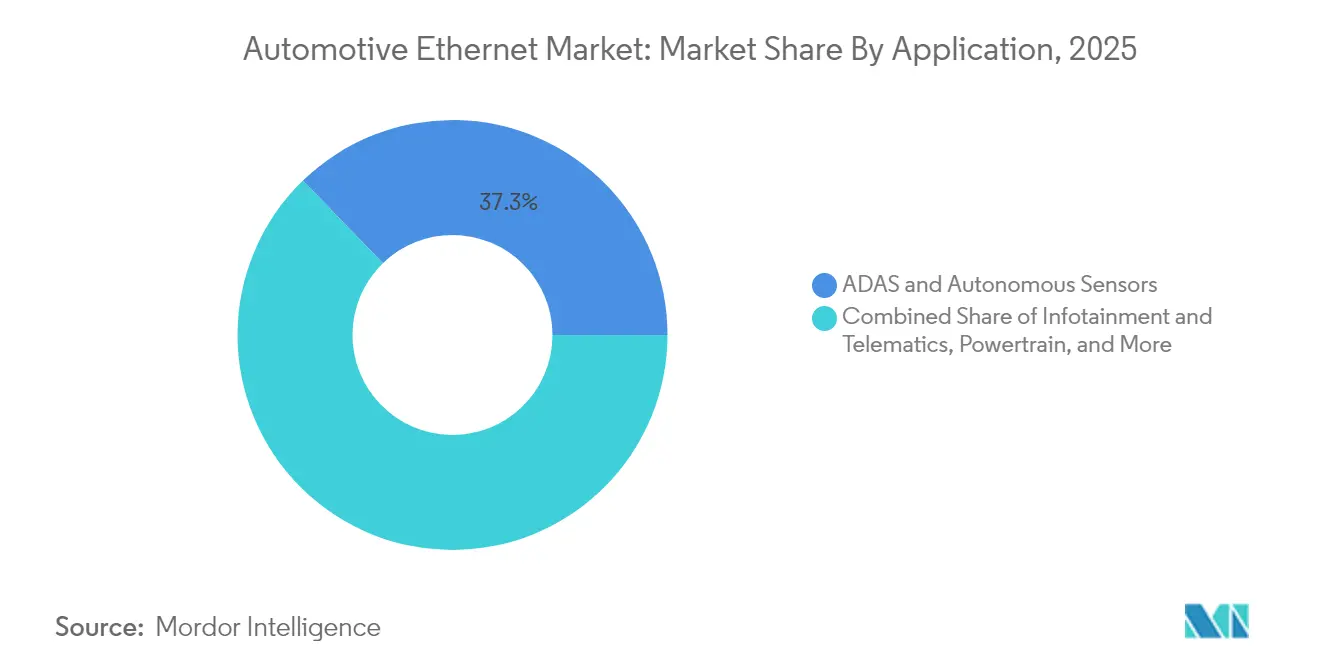

- By application, ADAS & autonomous sensors led with 37.25% revenue share in 2025; diagnostics & OTA updates are advancing at a 25.85% CAGR to 2031, lowering recall costs and speeding feature rollouts.

- By vehicle type, passenger cars accounted for 71.20% of the 2025 volume, but commercial platforms are integrating Ethernet to satisfy fleet management and zero-emission mandates.

- By geography, Asia-Pacific commanded 47.60% of global 2025 demand; the Middle East & Africa is the fastest-growing region with a 24.75% CAGR through 2031, supported by new assembly plants and premium-vehicle uptake.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Automotive Ethernet Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging infotainment & ADAS bandwidth demand | +6.2% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Rapid adoption of low-cost single-pair Ethernet (SPE) | +4.8% | Global, with early adoption in Asia-Pacific | Short term (≤ 2 years) |

| EV & autonomous platforms shifting to zonal E/E architectures | +5.5% | Global, led by Europe & North America | Medium term (2-4 years) |

| OEM standardization via OPEN Alliance & IEEE TSN profiles | +3.7% | Global | Medium term (2-4 years) |

| OEM push for end-to-end OTA software pipelines needing GbE backbones | +4.2% | North America, Europe, China | Medium term (2-4 years) |

| Weight-reduction incentives in EU/China favouring Ethernet over CAN-FD | +3.1% | Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Infotainment & ADAS Bandwidth Demand

Advanced camera, radar, and LiDAR arrays can stream up to 40 Gbps of raw data that must reach centralized processors with minimal latency. Ethernet backbones scaling from 100 Mbps to 10 Gbps are therefore replacing legacy buses capped at 10 Mbps, enabling high-resolution mapping and immersive cabin experiences. Luxury brands already equip roughly 60% of premium models with Ethernet infotainment links, a pattern expected to cascade to volume segments over the forecast window. Real-time multi-sensor fusion is also accelerating the shift to gigabit-class links because safety algorithms require deterministic latency budgets. Together, these forces keep network throughput on an upward trajectory and underpin continuous chipset innovation.

Rapid Adoption of Low-Cost Single-Pair Ethernet

Single-pair Ethernet eliminates two differential pairs, cutting harness weight by up to 40% and wiring cost by nearly 20%, benefits that directly extend the range of electric vehicles. 10BASE-T1S supports multidrop topologies, allowing multiple edge sensors to share a single twisted pair without complex gateways. Leading OEM programs in China are already releasing pre-production vehicles with SPE to connect door, seat, and lighting modules, while suppliers such as Analog Devices offer PHYs with integrated MACsec to simplify security compliance. Early deployments confirm that simplified cabling accelerates zonal architecture rollouts and scales cost-sensitive platforms.

EV & Autonomous Platforms Shift to Zonal E/E Architectures

Zonal designs consolidate ECUs by physical location rather than function, trimming harness length, and removing redundant microcontrollers. Weight falls up to 30 %, an outcome critical for battery-electric vehicles that must offset cell mass and meet efficiency targets. Marvell’s 90 Gbps Brightlane switch family exemplifies the silicon response, carrying local zone traffic while connecting to a central compute node through multi-gig links. In parallel, the market for zonal ECUs is forecast to touch USD 12 billion by 2030, giving component suppliers a sizeable served available market and reinforcing Ethernet as the default zonal backbone.

OEM Standardization via OPEN Alliance & IEEE TSN Profiles

With 340+ members, the OPEN Alliance publishes physical-layer specifications such as 100BASE-T1 that harmonize requirements for shielding, crosstalk, and EMC, removing integration ambiguity[1]OPEN Alliance, “100BASE-T1 System Implementation Specification,” openalliance.org. IEEE TSN profiles build deterministic scheduling on top of Ethernet, guaranteeing microsecond-level delivery for safety-critical traffic. NXP’s S32G family pairs payload processing with hardware TSN engines, demonstrating that standardization is not merely theoretical but baked into production-grade silicon. Unified specs reduce supplier fragmentation, ease interoperability checks, and compress validation timelines, accelerating the Automotive Ethernet market rollout.

Restraints Impact Analysis of Automotive Ethernet Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability & legacy ECU compatibility issues | -3.2% | Global, with higher impact in regions with established automotive manufacturing | Short term (≤ 2 years) |

| Vehicle-level cyber-security & functional-safety certification hurdles | -2.7% | Global, with stricter impact in Europe due to regulatory requirements | Medium term (2-4 years) |

| Multi-gig EMC/EMI compliance costs above 5 Gbps | -1.8% | Global | Medium term (2-4 years) |

| US-China tariff volatility on PHY chip supply chains | -1.5% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Interoperability & Legacy ECU Compatibility Issues

Many mass-production platforms still rely on CAN or LIN domains that do not disappear overnight. Bridging gateways must translate protocols while safeguarding timing constraints, adding bill-of-materials cost and software complexity. The Automotive Central Gateway Module market, valued at USD 2.1 billion in 2025, highlights the scale of this interim architecture. Chinese OEMs such as Chery have thus designed Ethernet gateways tailored to coexist with instrument-cluster CAN buses, proving that transition strategies can mitigate but not fully erase integration pain. Over the next two years, these gateways will remain essential as fleets slowly migrate toward full Ethernet zones.

Vehicle-Level Cybersecurity & Functional-Safety Certification Hurdles

UNECE WP.29 mandates cybersecurity management systems for all new vehicles sold in the European Union after July 2024, forcing OEMs to embed risk-based methodologies and acquire certificates before mass rollout. ISO/SAE 21434 complements this regulation with granular engineering requirements, while ISO 26262 continues to govern functional safety. Meeting both security and safety audits lengthens test cycles, and Ethernet’s broad attack surface amplifies verification scope. Although global suppliers offer pre-qualified IP, final responsibility remains with the vehicle manufacturer, elevating program risk and tempering immediate growth prospects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Ethernet Market Segment Analysis

By Component:

Services Scale Faster than HardwareThe hardware segment held 62.35% of 2025 revenue, led by PHY transceivers, switches, and controllers that anchor every in-vehicle network. Multi-generation roadmaps from vendors such as Microchip add 100 Mbps to 1 Gbps capabilities on a single die, underscoring performance-per-dollar improvements. The services sub-segment, though smaller in absolute revenue, is the fastest riser at a 26.95% CAGR because OEMs increasingly outsource compliance, TSN tuning, and deep packet inspection. Keysight’s automated compliance suits accelerate IEEE conformance, reflecting how test expertise commands premium fees. Collectively, this dynamic positions services as a strategic growth lever even as silicon volumes remain the revenue anchor.

In parallel, software stacks that support secure boot, network orchestration, and over-the-air configuration gain relevance as zonal architectures mature. Real-time operating systems suppliers bundle ISO 26262 certification artifacts to simplify adoption, proving that the Automotive Ethernet market rewards turnkey solutions over discrete components. As data volumes rise, cloud-linked analytics platforms will likely emerge as an adjacent services layer, further diversifying revenue pools in the Automotive Ethernet industry.

By Bandwidth:

Multi-Gig Standards Redefine Network Capacity100BASE-T1 retains a 41.10% share in 2025, serving body control and infotainment needs that top out below 100 Mbps. Its mature cost curve and OPEN Alliance interoperability profile sustain its appeal, balancing throughput against price. The 2.5/5/10 Gbps class exhibits the strongest upside with a 36.60% CAGR through 2031, moving the Automotive Ethernet market size for high-speed links into the multi-billion-dollar range by the end of the forecast window. Supply-chain readiness is improving as switch silicon integrates 10GBASE-T1 PHYs, allowing single-package zonal backbones.

10BASE-T1S addresses edge sensor connectivity by providing 10 Mbps multidrop capability, removing gateway cost where deterministic latency is less critical. Meanwhile, 1000BASE-T1 plays an intermediate role, bridging today’s needs and tomorrow’s zonal ambitions. Overall, the shift toward gigabit and multi-gigabit tiers unlocks new software-defined features, including real-time object classification and high-definition cabin streaming, reinforcing the Automotive Ethernet market expansion.

By Application:

ADAS Dominates, OTA Updates SurgeADAS & autonomous sensors generated 37.25% of 2025 revenue, validating the view that perception workloads drive bandwidth decisions. Radar modules alone are forecast to approach 500 million units annually by 2041, funneling uncompressed waveforms over Ethernet to a centralized drive policy engine. High-capacity TSN switches ensure deterministic delivery, while MACsec encrypts payloads to guard against spoofing.

Diagnostics & OTA updates are the fastest riser at 25.85% CAGR, positioning the segment to capture a larger Automotive Ethernet market share in the second half of the decade. Software recall avoidance is a primary economic driver, with OTA-enabled manufacturers able to patch vulnerabilities remotely instead of issuing costly workshop campaigns. Additional segments such as infotainment, powertrain, and body-control join the Ethernet roadmap at a steadier pace, still benefiting from the broader network overhaul.

By Vehicle Type:

Passenger Cars Lead, Commercial Fleets Catch UpPassenger cars delivered 71.20% of the 2025 volume as consumers demand smartphone-like experiences in the cabin. Tesla’s architecture already routes autopilot video and infotainment data over Ethernet, illustrating the value proposition in a mainstream context. High-trim models from German marquees likewise integrate multi-gig backbones to support 4K streaming rear-seat displays and surround-view cameras.

Commercial platforms, light trucks, heavy trucks, buses, and off-highway machinery are beginning to align with zero-emission mandates, which intensify electronic complexity and connectivity needs. California’s mandate for electric trucks kicks in from 2024, pushing OEMs to incorporate Ethernet-based battery-management and telematics modules. Ruggedized connectors and PHYs rated for 40 °C to 105 °C enable harsh-duty adoption, closing the feature gap with passenger platforms and enlarging the addressable Automotive Ethernet industry.

Geography Analysis

APAC Automotive Ethernet Market

Asia-Pacific commands 47.60% of global 2025 demand, anchored by China’s rapid transition to connected and automated vehicles. The Chinese Automotive Ethernet market size is projected to surpass RMB 12 billion (USD 1.7 billion) in 2025 as national standards such as GB/T 45503-2025 define ECU compliance test methods. Local silicon champions shorten design cycles, benefiting domestic OEMs that iterate quickly on zonal prototypes. Japan and South Korea extend regional dominance through vertically integrated electronics and automotive supply chains, deploying SPE production lines by 2025.

North America Automotive Ethernet Market

North America leverages its software ecosystem and venture-capital pipeline to pilot advanced software-defined vehicles. Regulatory bodies emphasize cybersecurity, as the U.S. Department of Commerce weighs restrictions on suspect semiconductor inputs in connected vehicles. OEMs in Detroit and Silicon Valley accelerate OTA frameworks, fostering demand for gigabit backbones. Trade frictions with China inject supply-chain risk around PHY chip logistics, prompting near-shoring strategies and dual-sourcing agreements to sustain program schedules.

MEA Automotive Ethernet Market

The Middle East & Africa holds a smaller base but exhibits the fastest regional growth at 24.75% CAGR through 2031. Governments in Saudi Arabia and the UAE incentivize local assembly and electric-vehicle uptake, encouraging global OEMs to import Ethernet-enabled premium models. Smart-city deployments complement high-speed vehicle networks, allowing traffic-signal priority and V2X safety features to flourish. Premium European brands leverage free-trade zones to position their latest models, further accelerating Ethernet penetration across the region.

Competitive Landscape

The Automotive Ethernet market shows moderate concentration as incumbent semiconductor leaders deepen portfolios and niche entrants capture specialized domains. Broadcom, NXP, and Marvell long dominated PHY and switch footprints. However, Infineon’s USD 2.5 billion purchase of Marvell’s automotive Ethernet unit in April 2025 tilts the share, projecting USD 225–250 million incremental revenues for Infineon in 2025. The deal evidences a land-grab for zonal computing relevance amid the software-defined vehicle transition.

Opportunities emerge in TSN switch cores, packet-inspection accelerators, and network-security IP. China’s Yutai Microelectronics and MotorComm move aggressively with cost-optimized TSN chips, targeting domestic automakers that prefer local sourcing. Testing and compliance firms such as Rohde & Schwarz and Keysight diversify offerings to include 10BASE-T1S analysis and PoDL diagnostics, monetizing the growing validation workload.

Ecosystem partnerships accelerate technology maturation. OPEN Alliance memberships expanded past 340 in 2025, while the Automotive SerDes Alliance (ASA) aligns camera links with Ethernet routes, broadening total addressable connectivity. Cloud providers collaborate with Tier-1 suppliers on fleet data analytics, hinting at future competition in over-the-air orchestration services once standards stabilize.

Automotive Ethernet Industry Leaders

Broadcom Inc.

NXP Semiconductors NV

Marvell Technology Group Ltd.

Microchip Technology Inc.

Texas Instruments Inc.

- *Disclaimer: Major Players sorted in no particular order

Automotive Ethernet Market Companies Covered in this Report

- Broadcom Inc.

- NXP Semiconductors N.V.

- Marvell Technology Group Ltd.

- Microchip Technology Inc.

- Texas Instruments Inc.

- Molex Incorporated

- TE Connectivity Ltd.

- Cadence Design Systems Inc.

- Keysight Technologies Inc.

- TTTech Auto AG

- AMD Xilinx

- Analog Devices Inc.

- Renesas Electronics Corp.

- Realtek Semiconductor Corp.

- Rohde and Schwarz GmbH

- Vector Informatik GmbH

- Aptiv PLC

- Infineon Technologies AG

- Continental AG

- HMS Networks AB

- Aeonsemi Corp.

- Aukua Systems Inc.

- Spirent Communications PLC

Recent Industry Developments in Automotive Ethernet Market

- April 2025: Infineon Technologies AG acquired Marvell Technology’s Automotive Ethernet business for USD 2.5 billion, enhancing its zonal compute portfolio.

- April 2025: Broadcom expanded its Ethernet switch line to support mass-market software-defined vehicles, adding multi-gig interfaces with TSN scheduling.

- March 2025: Aeonsemi launched the Nemo multi-Gig Ethernet chipset with the first integrated 10GBASE-T1 PHY, reducing PCB footprint and power.

- December 2024: NXP Semiconductors bought Aviva Links for USD 242.5 million to reinforce SerDes capabilities for high-bandwidth video links.

Automotive Ethernet Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the automotive ethernet market as the total value generated from the sale of new, in-vehicle single-pair and multi-pair ethernet transceivers, switches, controllers, cabling, and related software or services that are factory-fitted by light-duty and heavy-duty vehicle manufacturers across all power-train types.

Scope exclusion: after internal scoping, we do not count plant-floor ethernet, aftermarket retrofit harnesses, or stand-alone test equipment that never leaves the lab.

Segments Covered in This Report

- By Component

- Hardware

- Software

- Services

- By Bandwidth/Operating Speed

- 10 Mbps (10BASE-T1S)

- 100 Mbps (100BASE-T1)

- 1 Gbps (1000BASE-T1)

- 2.5/5/10 Gbps Multi-Gig (2.5G/5G/10GBASE-T1)

- By Application

- ADAS and Autonomous Sensors

- Infotainment and Telematics

- Powertrain

- Chassis and Safety

- Body and Comfort

- Diagnostics and OTA Updates

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial/Truck and Bus

- Off-Highway and Agriculture

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed tier-1 network module engineers, OEM E/E architects in Asia, Europe, and North America, and procurement managers at cable harness makers. These conversations validated node counts per vehicle, confirmed penetration timelines for 2.5/5/10 Gbps links, and reconciled regional price dispersion that secondary sources only hinted at.

Desk Research

We began with production statistics from OICA, ACEA registration updates, and NHTSA recall filings, which helped us size the rolling vehicle parc and new-build volume. Standards documents from IEEE 802.3 and the OPEN Alliance clarified the bandwidth breakpoints that define our component universe, while UNECE WP.29 cybersecurity regulations framed the regulatory driver set. Annual reports aggregated through D&B Hoovers and patent families pulled via Questel revealed supplier revenue splits and design-win trajectories. These and many other open datasets created the factual spine for our model; the list above is illustrative rather than exhaustive.

A second pass tapped Volza customs bills to gauge export flows of automotive ethernet PHYs, and Dow Jones Factiva tracked multi-gig design announcements that shape average selling prices. Cross-checking with IMTMA and Asia Metal price benchmarks ensured bill-of-materials assumptions stayed grounded in prevailing cost curves.

Market-Sizing & Forecasting

A top-down build started with global light-vehicle output, which was then filtered through ethernet adoption rates by application cluster (ADAS sensor backbone, infotainment domain, diagnostics gateway). Select bottom-up checks sampled OEM bill-of-materials, channel audits, and average port pricing tempered the totals. Key variables include sensor attach rate, ethernet ports per vehicle, multi-gig share, component ASP drift, and regional EV mix.

For forecasting, a multivariate regression couples vehicle output, ADAS content growth, and regulatory triggers to predict port shipments. ARIMA smoothing captures cyclical production swings before revenue is derived through dynamic ASP curves. Where supplier roll-ups fell short, missing values were bridged using three-year moving averages agreed upon during expert calls.

Data Validation & Update Cycle

Model outputs are stress-tested against shipment data, customs records, and quarterly earnings. Variances beyond preset thresholds trigger re-checks by a second analyst and follow-up calls with earlier respondents. Reports refresh annually, and mid-cycle updates are issued when material events, such as new UNECE mandates, arise.

How Mordor Intelligence's Automotive Ethernet Market Size Compares to Other Published Estimates

Published numbers often differ, and the gaps usually stem from varying component baskets, currency bases, and refresh cadences. Our team flags these levers upfront so clients can trace every dollar back to a clear assumption.

Key gap drivers include whether higher-cost multi-gig ports are counted, if services revenue is blended with hardware, and whether 2024 or 2025 is treated as the base year. Some external publishers also extrapolate ASPs from consumer ethernet rather than automotive-grade parts, inflating totals, while their update cycle lags emerging regulations that Mordor analysts track quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.5 B (2025) | Mordor Intelligence | - |

| USD 2.9 B (2024) | Global Consultancy A | excludes multi-gig ports and uses 2023 ASP roll-over |

| USD 2.2 B (2023) | Regional Consultancy B | shorter component list and five-year-old production base |

| USD 3.19 B (2024) | Trade Journal C | mixes aftermarket retrofits with OEM factory fitment |

In short, Mordor Intelligence grounds every figure in up-to-date production data, application-level penetration checks, and transparent price tracking, giving decision-makers a balanced and reproducible baseline they can actually defend.

Key Questions Answered in the Report

What is the projected size of the Automotive Ethernet market by 2031?

The Automotive Ethernet market is forecast to reach USD 11.93 billion by 2031, expanding at a 22.70% CAGR.

Which component category is growing the fastest?

Services, including testing, validation, and integration, are advancing at a 26.95% CAGR as OEMs outsource complex compliance work.

Why are multi-gigabit Ethernet speeds important in vehicles?

Higher bandwidth links (2.5/5/10 Gbps) carry data from high-resolution sensors and support real-time processing essential for ADAS and autonomous functions.

Which region is currently the largest adopter of Automotive Ethernet?

Asia-Pacific leads with 47.60% of 2025 demand, driven by China’s aggressive connected-vehicle programs and strong domestic semiconductor supply.

How do single-pair Ethernet solutions benefit electric vehicles?

SPE reduces wiring weight by up to 40% and cost by about 20%, directly improving EV range and simplifying zonal architecture designs.

What are the main regulatory hurdles for Automotive Ethernet deployments?

UNECE WP.29 cybersecurity rules and ISO 26262 functional-safety requirements extend validation timelines and raise development costs.

Page last updated on: