Organic Yogurt Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

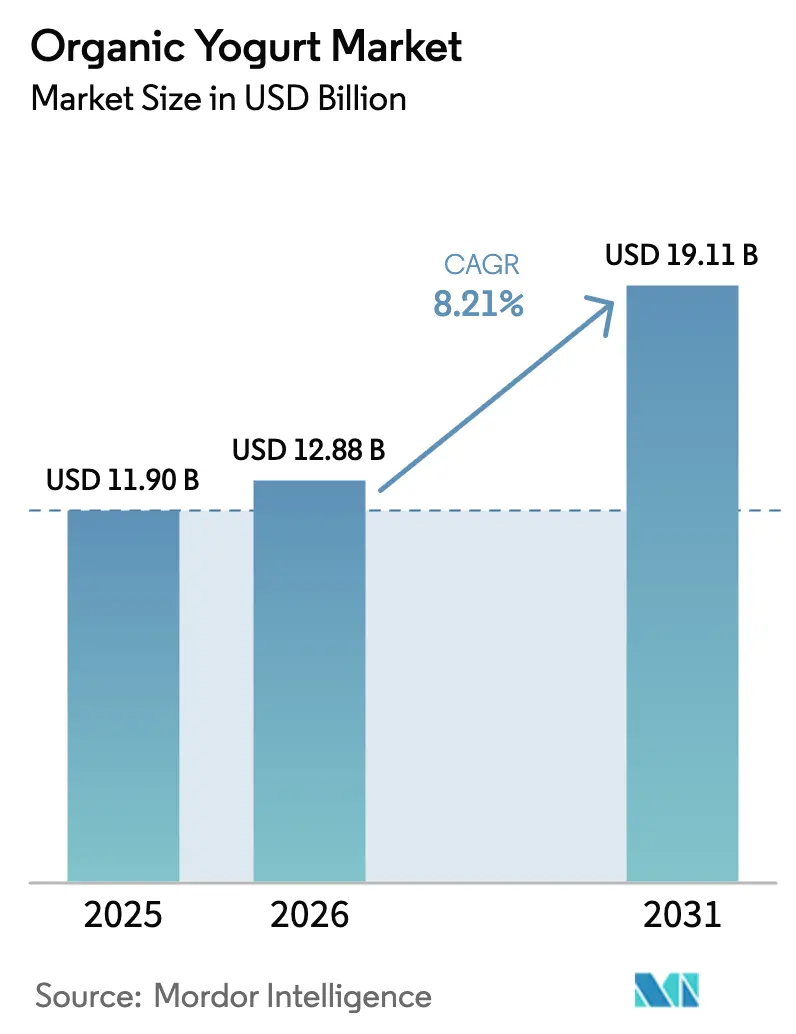

| Market Size (2026) | USD 12.88 Billion |

| Market Size (2031) | USD 19.11 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

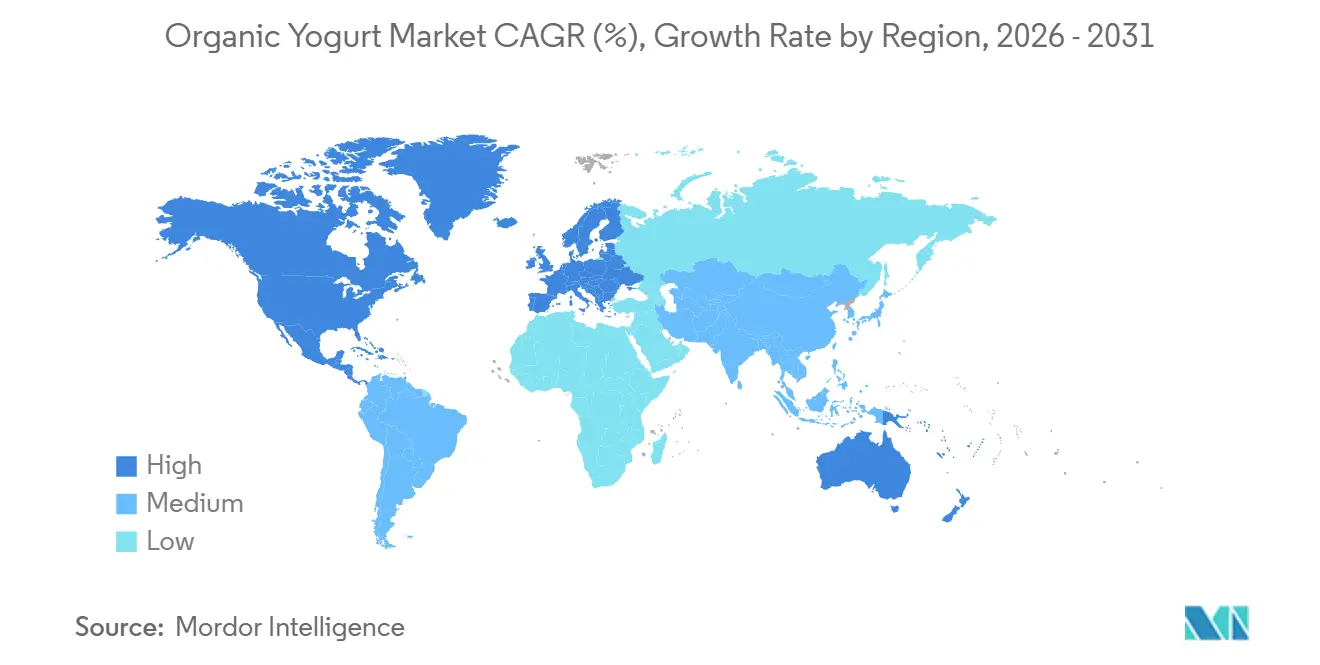

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Yogurt Market Analysis by Mordor Intelligence

The global organic yogurt market is witnessing steady growth, driven by increasing consumer preference for health-focused, clean-label, and functional food products. The market was valued at USD 11.90 billion in 2025, is estimated to reach USD 12.88 billion in 2026, and is projected to grow to USD 19.11 billion by 2031, registering a CAGR of 8.21% during 2026–2031. This growth is attributed to the rising incorporation of organic yogurt into daily diets as consumers prioritize nutrient-rich foods offering benefits such as digestive health support, high protein content, and natural ingredients. Growing awareness of gut health and the role of probiotics is further driving demand, establishing organic yogurt as both a staple and a functional dietary choice. Additionally, changing lifestyle patterns, including busy schedules and the need for convenient, ready-to-eat options, are boosting the popularity of organic yogurt for various consumption occasions such as breakfast, snacking, and post-workout nutrition.

Key Report Takeaways

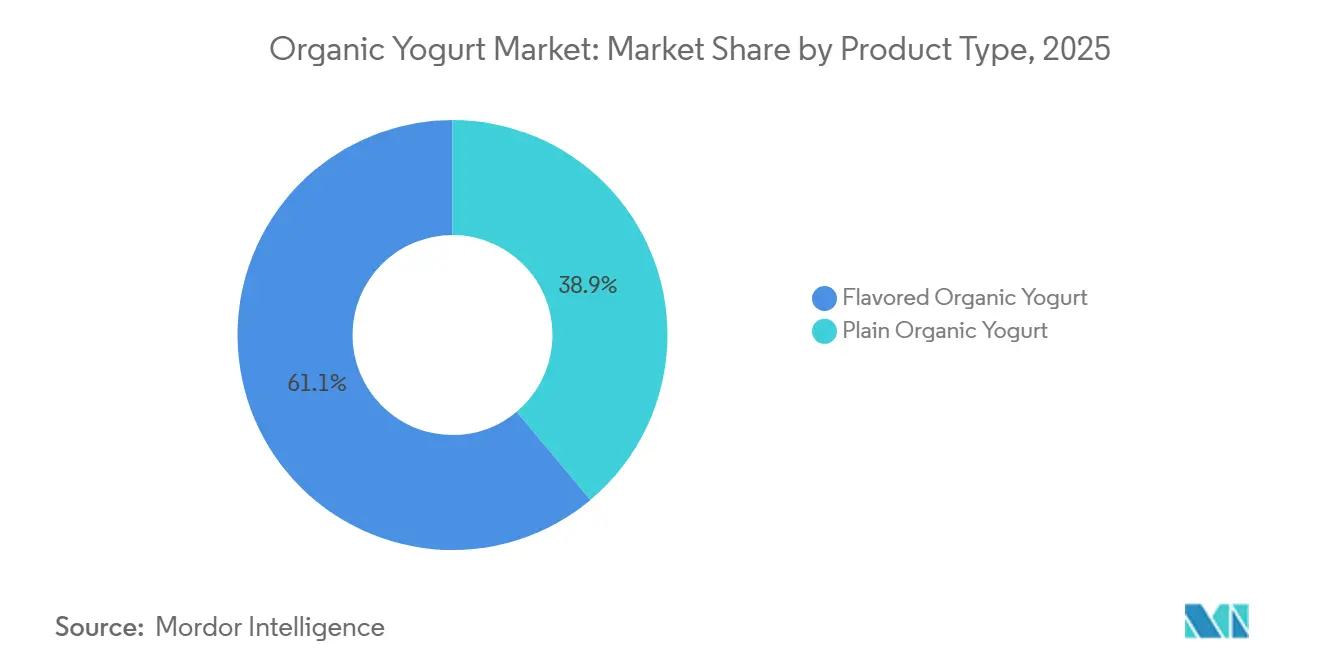

- By product type, flavored organic yogurt led with a 61.09% revenue share in 2025, while plain organic yogurt is forecast to advance at an 8.26% CAGR through 2031.

- By form, spoonable yogurt held 68.73% of the organic yogurt market share in 2025; drinkable yogurt is projected to record the highest CAGR at 9.87% over 2026-2031.

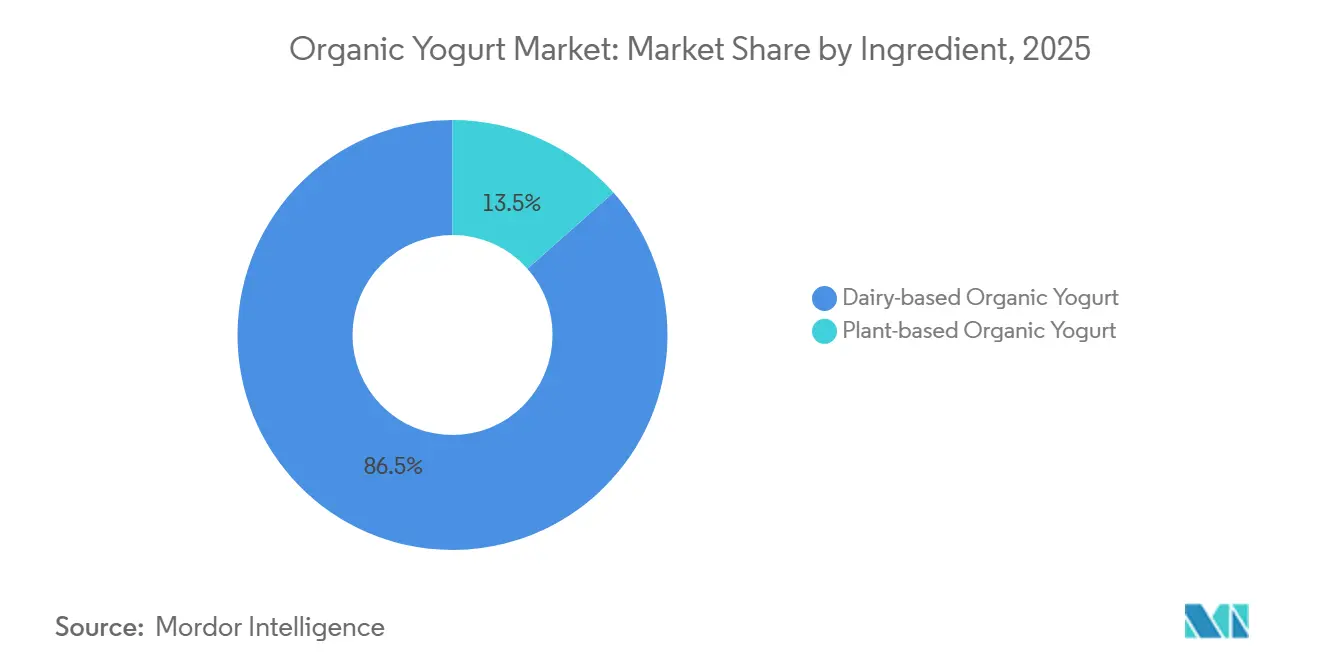

- By source, dairy-based offerings accounted for 86.53% of the organic yogurt market size in 2025, yet plant-based organic yogurt is expected to expand at a 10.09% CAGR to 2031.

- By distribution channel, off-trade controlled 69.82% of 2025 sales, whereas on-trade is recovering fastest at a 9.45% CAGR as foodservice reintroduces organic options.

- By geography, North America commanded 38.78% of global value in 2025; Asia-Pacific is poised for the swiftest growth at a 9.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Yogurt Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness awareness | +1.8% | Global, with strongest uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Convenience and on-the-go consumption trends | +1.5% | North America and Europe lead; Asia-Pacific urban centers accelerating | Short term (≤ 2 years) |

| Clean-label and natural ingredient preference | +1.3% | North America and Europe core; spillover to premium segments in Asia-Pacific | Medium term (2-4 years) |

| Preference for sustainable, eco-friendly farming practices | +1.0% | Europe (especially Nordics, Germany, United Kingdom); emerging in North America millennials | Long term (≥ 4 years) |

| Product innovation and flavor diversification | +1.2% | Global, with North America and Asia-Pacific leading exotic/functional flavors | Short term (≤ 2 years) |

| Increasing demand for probiotic-rich foods | +1.4% | Global, with Asia-Pacific and North America showing highest growth in gut-health awareness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health and wellness awareness

Consumers increasingly view organic yogurt as a functional food that provides essential nutrients, including protein, probiotics, and calcium, without artificial additives or synthetic ingredients. This perception is strongly supported by scientific research, which highlights the benefits of probiotic yogurt in improving glycemic control, enhancing gut health, and supporting microbiome recovery, particularly after antibiotic use. Consequently, organic yogurt is becoming popular not only as a daily dietary choice but also as a targeted health-focused product. Additionally, the growing emphasis on protein consumption is significantly driving demand, particularly for high-protein options like Greek organic yogurt. According to the International Food Information Council's 2025 Food & Health Survey, nearly 70% of Americans are actively seeking to increase their protein intake, which directly supports the expansion of protein-rich organic yogurt products [1]Source: International Food Information Council, "Americans’ Perceptions of Protein ", ific.org.

Convenience and on-the-go consumption trends

Convenience and on-the-go consumption trends are major factors driving the global organic yogurt market. As busy lifestyles become more prevalent, consumers are increasingly seeking quick, portable, and ready-to-eat nutritional options. Organic yogurt, especially in single-serve and drinkable formats, integrates well into modern routines such as commuting, office snacking, and post-workout consumption, offering strong nutritional value without requiring preparation. This emphasis on convenience is also broadening consumption occasions beyond traditional meals, positioning organic yogurt as a versatile snack or mini-meal option. For example, in January 2025, Little Spoon introduced YoGos, an on-the-go yogurt product made with organic whole milk Greek yogurt. YoGos provide 4 grams of protein, real fruit, hidden vegetables, and probiotics, addressing both convenience and nutrition needs.

Clean-label and natural ingredient Preference

Consumer preference for clean-label and natural ingredients is a key driver of the global organic yogurt market. Shoppers are increasingly prioritizing transparency, simplicity, and authenticity in their food choices. They actively examine product labels, favoring options with recognizable, minimally processed ingredients free from artificial preservatives, synthetic additives, or genetically modified components. Organic yogurt meets these expectations by using certified organic milk and natural ingredients, reinforcing its image of purity and safety. Additionally, concerns about the long-term health effects of artificial ingredients are encouraging a shift toward foods perceived as more natural. Clean-label positioning also strengthens brand trust and credibility, fostering repeat purchases and long-term consumer loyalty. The simplicity of organic yogurt's ingredient list, often limited to organic milk and live cultures, further supports its appeal as a wholesome, everyday food choice.

Preference for sustainable, eco-friendly farming practices

The preference for sustainable and eco-friendly farming practices is a significant driver of the global organic yogurt market, as consumers increasingly base their purchasing decisions on environmental and ethical considerations. Organic dairy farming prioritizes practices such as minimizing chemical usage, preserving soil health, ensuring animal welfare, and protecting biodiversity. These practices strongly appeal to environmentally conscious consumers. This growing awareness is driving a shift toward products perceived to have a lower environmental impact compared to conventional alternatives. Organic yogurt, closely associated with these sustainable farming methods, is often selected as a more responsible dairy option. Furthermore, concerns about climate change, resource depletion, and sustainable agriculture are motivating consumers to support brands that emphasize responsible sourcing and environmentally friendly production processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher price premium compared to conventional yogurt | -1.6% | Global, most acute in price-sensitive emerging markets and lower-income segments | Short term (≤ 2 years) |

| Supply constraints of organic milk | -1.4% | North America and Europe core; limited organic dairy infrastructure in Asia-Pacific and MEA | Medium term (2-4 years) |

| Stringent certification and regulatory requirements | -0.8% | Global, with highest compliance costs in North America and Europe due to USDA NOP and EU Organic Regulation | Long term (≥ 4 years) |

| Taste perception and preference barriers | -0.7% | Primarily plant-based organic yogurt in North America and Europe; dairy-based less affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher price premium compared to conventional yogurt

The higher price premium of organic yogurt compared to conventional yogurt serves as a significant restraint on the global organic yogurt market. The elevated cost of organic production directly leads to higher retail prices, which limits broader consumer adoption. Organic yogurt production requires certified organic milk, necessitating stricter farming practices, higher feed costs, and lower yield efficiencies compared to conventional dairy farming. Additionally, costs associated with certification, compliance, and supply chain segregation further contribute to increased production expenses. Consequently, organic yogurt is often priced significantly higher than conventional alternatives, making it less accessible to price-sensitive consumers and discouraging frequent purchases. This pricing disparity is particularly pronounced in emerging markets, where affordability often takes precedence over perceived health and environmental benefits. Even among health-conscious consumers, the premium pricing can restrict consumption to occasional purchases rather than regular use.

Supply constraints of organic milk

Supply constraints of organic milk pose a significant challenge to the global organic yogurt market, as the availability of certified organic dairy inputs remains limited compared to conventional milk production. Organic dairy farming requires strict compliance with regulations, including the use of organic feed, the prohibition of synthetic chemicals and hormones, and adherence to animal welfare standards. These requirements collectively reduce yield efficiency and extend production timelines. Transitioning from conventional to organic farming is also a lengthy process, often taking several years for land and livestock to achieve certification, which slows the expansion of supply. Furthermore, organic dairy farms generally operate on a smaller scale, further limiting output and creating imbalances between growing demand and available raw materials. These supply constraints can result in production inconsistencies, higher input costs, and potential disruptions in the value chain for organic yogurt manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plain Gains as Customization Trend Rises

The flavored organic yogurt segment, which accounted for 61.09% of the market share in 2025, is a significant driver of growth in the global organic yogurt market. This segment enhances product appeal, increases consumption frequency, and broadens consumer reach beyond traditional health-focused buyers. The inclusion of natural fruit blends, botanical extracts, and dessert-inspired flavors improves palatability, making organic yogurt more appealing to a wider audience, including children and first-time organic consumers who may find plain variants less attractive. These sensory improvements contribute to higher repeat purchases and habitual consumption, thereby supporting volume growth. Additionally, the use of organic-certified flavoring ingredients aligns with clean-label expectations, fostering trust and reinforcing product authenticity without compromising taste.

The plain organic yogurt segment, projected to grow at a CAGR of 8.26% through 2031, is emerging as a key growth contributor in the global organic yogurt market. This growth is driven by the segment's alignment with clean-label, minimal ingredient, and functional nutrition trends. Plain organic yogurt is perceived as a more authentic and unprocessed option, typically containing only essential ingredients such as organic milk and live cultures. This simplicity appeals to consumers seeking transparency and purity in their food choices. Furthermore, its versatility as a base product allows customization with fruits, cereals, or natural sweeteners, enabling consumers to control sugar intake and flavor profiles. The segment also benefits from increasing adoption among health-conscious individuals who prioritize high-protein, probiotic-rich foods without added sugars or artificial flavoring, particularly in diets focused on weight management, gut health, and overall wellness.

By Form: Drinkable Yogurt Captures On-the-Go Premium

The spoonable or cup organic yogurt segment, projected to hold a 68.73% market share in 2025, is a key driver of the global organic yogurt market. This dominance is attributed to its alignment with everyday consumption habits, convenience, and product familiarity. The format is widely favored as it integrates seamlessly into daily routines such as breakfast, mid-day snacks, and light meals, offering a ready-to-eat option that requires no preparation. Its thick, creamy texture enhances satiety and provides an indulgent eating experience, appealing to both health-conscious consumers and those seeking comfort-oriented foods. Additionally, the cup format supports portion control and portability, making it ideal for on-the-go consumption in urban lifestyles. The segment's versatility further adds to its appeal, as it can be easily paired with toppings like fruits, granola, and seeds, enabling consumers to personalize their meals while maintaining a healthy profile.

The drinkable organic yogurt segment, anticipated to grow at a CAGR of 9.87% through 2031, is emerging as the fastest-growing format in the global organic yogurt market. This growth is primarily driven by its superior convenience, portability, and compatibility with fast-paced consumer lifestyles. Unlike spoonable formats, drinkable yogurt offers a highly accessible, on-the-go solution that fits seamlessly into busy routines, including commuting, work breaks, and post-workout consumption. Its easy-to-consume format eliminates the need for utensils, making it particularly appealing to time-constrained consumers seeking quick yet nutritious options. Additionally, the segment benefits from its strong positioning as a functional beverage, often associated with hydration, digestion support, and energy replenishment, thereby broadening its appeal beyond traditional yogurt consumption occasions.

By Source: Plant-Based Organic Yogurt Disrupts Dairy Dominance

The dairy-based organic yogurt segment, accounted for 86.53% of the market share in 2025, is a key driver of the global organic yogurt market. This dominance is attributed to its strong foundation in traditional consumption patterns, superior nutritional profile, and high consumer trust. Dairy-based yogurt is widely valued for its rich content of protein, calcium, and naturally occurring probiotics, making it a staple in daily diets and a preferred choice for health-conscious consumers seeking functional and nutrient-dense foods. Its long-standing familiarity across cultures fosters acceptance and repeat consumption, solidifying its position as the core category within the organic yogurt market. Additionally, dairy-based variants offer a creamy texture and balanced taste that align with consumer expectations, further supporting their widespread adoption.

The plant-based organic yogurt segment, projected to grow at a CAGR of 10.09% through 2031, is emerging as the fastest-growing category within the global organic yogurt market. This growth is driven by shifting dietary preferences, sustainability concerns, and increasing demand for allergen-free alternatives. The segment is gaining traction among consumers adopting vegan, flexitarian, and lactose-free lifestyles, as it provides a suitable substitute without compromising on organic and clean-label standards. Made from sources such as almond, coconut, soy, and oats, plant-based organic yogurt appeals to a broader consumer base, including those with lactose intolerance or dairy sensitivities, thereby expanding overall market penetration. Furthermore, the segment aligns with evolving perceptions of environmental sustainability, as plant-based production is often associated with a lower environmental impact compared to traditional dairy farming.

By Distribution Channel: On-Trade Recovery Lags Off-Trade Dominance

The off-trade distribution channel, projected to account for 69.82% of the market share in 2025, plays a significant role in driving the global organic yogurt market. This channel, encompassing supermarkets, hypermarkets, convenience stores, and online retail platforms, ensures widespread product accessibility, consistent availability, and high-volume retail sales. It serves as the primary purchase point for consumers seeking organic yogurt for at-home consumption. The channel's dominance is attributed to its ability to offer a wide range of product variants, including flavored, plain, dairy-based, and plant-based options, enabling consumers to compare, select, and purchase products in one location. Furthermore, off-trade channels support bulk purchasing and repeat buying behaviors, which are critical for sustained volume growth.

The on-trade distribution channel, expected to recover at a CAGR of 9.45% through 2031, is becoming an increasingly important contributor to the global organic yogurt market. This growth is supported by the resurgence of foodservice consumption and out-of-home dining trends. According to the United States Department of Agriculture, foodservice sales reached USD 1.52 trillion in 2024, underscoring the scale and renewed momentum of this channel [2]Source: United States Department of Agriculture (USDA), "Food Service Industry", usda.gov. As consumers return to cafés, restaurants, hotels, and quick-service outlets, organic yogurt is gaining popularity as a versatile, health-focused menu ingredient. It is featured in breakfast bowls, smoothies, parfaits, desserts, and functional beverages. The on-trade environment also plays a pivotal role in introducing consumers to premium and organic offerings, often serving as a trial platform that influences subsequent retail purchases.

Geography Analysis

North America is set to dominate the global organic yogurt market, holding a 38.78% market share in 2025. This leadership is attributed to strong consumer awareness of organic foods, well-established certification systems, and a mature retail ecosystem that ensures wide product availability. The region benefits from a deeply ingrained culture of health and wellness, where consumers actively seek clean-label, probiotic-rich, and minimally processed dairy products. According to the Organic Trade Association, organic food sales in the United States reached USD 71.6 billion in 2024, highlighting robust demand for organic products, including yogurt [3]Source: Organic Trade Association, "Organic Market Overview", ota.com. This solid market foundation is further strengthened by continuous product innovation, high penetration of organic certifications, and the integration of organic yogurt into daily consumption habits such as breakfast and snacking, making North America a key revenue-generating region.

The Asia-Pacific region is projected to be the fastest-growing market, with a CAGR of 9.46% through 2031. This growth is driven by rapid urbanization, evolving dietary patterns, and increasing exposure to health-focused food choices. Countries such as China, India, Indonesia, and Vietnam are experiencing a shift toward convenient and functional dairy products, including organic yogurt, as consumers increasingly prioritize gut health and nutritional quality. The expansion of organized retail and e-commerce platforms is significantly enhancing product accessibility, while growing awareness of organic certifications is fostering consumer trust. Additionally, the rising popularity of Western-style diets and on-the-go consumption patterns is accelerating the adoption of yogurt-based products, positioning Asia-Pacific as a major growth driver for the market.

Europe, South America, and the Middle East & Africa are collectively experiencing steady growth in the organic yogurt market. In Europe, the market is gaining momentum due to strong sustainability initiatives, stringent organic standards, and a well-informed consumer base that values ethical sourcing and environmental impact. South America is witnessing increased interest in organic dairy products as health awareness improves and retail infrastructure develops, particularly in urban areas. Meanwhile, the Middle East and Africa region is gradually emerging, supported by growing exposure to international food trends, a rising focus on premium and health-oriented products, and the expansion of modern retail formats.

Competitive Landscape

The global organic yogurt market is moderately consolidated, featuring a mix of multinational dairy leaders and emerging niche players. Companies such as Danone S.A., General Mills Inc., Lactalis Group, Chobani LLC, and Arla Foods amba dominate the competitive landscape. These key players leverage strong brand equity, established supply chains, and extensive product portfolios. Their vertically integrated operations and long-standing relationships with certified organic dairy farmers ensure consistent raw material sourcing and quality assurance. Meanwhile, smaller and regional brands continue to enter the market, offering differentiated products that emphasize purity, local sourcing, and artisanal appeal, contributing to a dynamic competitive environment.

Competition in the organic yogurt market increasingly revolves around product differentiation and value-added innovation. Key areas of focus include clean-label formulations, high-protein variants, probiotic enrichment, and plant-based alternatives. Leading companies are expanding their portfolios to include flavored, functional, and fortified organic yogurts that address evolving consumer preferences for health, taste, and convenience. Additionally, innovation in packaging formats, such as single-serve cups, drinkable bottles, and multi-layered products, plays a significant role in attracting diverse consumer segments and promoting on-the-go consumption. Sustainability initiatives, including environmentally friendly packaging and responsible sourcing practices, are also being prioritized to enhance brand perception and meet consumer expectations for ethical consumption.

Brands that invest in supply chain transparency, sustainable packaging, and direct-to-consumer (DTC) channels are well-positioned to capture market share from incumbents relying on traditional retail distribution and commodity-driven strategies. The increasing importance of traceability and authenticity in organic products is driving companies to adopt more transparent sourcing and labeling practices, which significantly influence consumer purchasing decisions. Furthermore, the growth of digital commerce and subscription-based models enables newer entrants to establish direct relationships with consumers, bypassing conventional retail barriers. While established players maintain dominance through scale and distribution, the competitive landscape is gradually shifting toward agile, purpose-driven brands that effectively combine innovation, transparency, and consumer engagement.

Organic Yogurt Industry Leaders

-

Danone S.A.

-

General Mills Inc.

-

Lactalis Group

-

Chobani LLC

-

Arla Foods amba

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Forager Project launched its Greek Style Yogurt lineup, featuring four new flavored 5oz cups and a Vanilla 24oz multi-serve tub. It contains 10g of plant-based protein derived from organic cashews, coconut milk, and rice protein.

- October 2025: Yeo Valley Organic introduced its Little Yeos range with the addition of Little Yeos Organic Yogurt & Oats Pots. This product features smooth organic yogurt combined with British-grown oats and real fruit purée, available in strawberry and peach flavors.

- April 2025: Norr Organic introduced its Non-fat Skyr line at Sprouts Farmers Market. The Norr Organic Skyr is made with high-quality organic milk from grass-fed cows, offering a nutrient-rich yogurt that is low in sugar and contains live BB-12 probiotics.

- September 2024: Kaneka Corporation launched an organic JAS-certified yogurt, Pur Natur Organic Yogurt Strawberry-Mix. This product is an individual-serving type and features a two-layered yogurt with strawberry and raspberry confiture.

Global Organic Yogurt Market Report Scope

Organic yogurt is made from milk that comes from cows raised without prohibited pesticides, herbicides, antibiotics, or growth hormones. The Organic yogurt market is segmented by product type, form, source, distribution channel, and geography. Based on product type, the market is segmented into plain organic yogurt and flavored organic yogurt. Based on form, the market is segmented into spoonable/cup yogurt and drinkable yogurt. Based on source, the market is segmented into dairy-based organic yogurt and plant-based organic yogurt. Based on distribution channel, the market is segmented into on-trade and off-trade. Off-trade segment is further segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Plain Organic Yogurt |

| Flavored Organic Yogurt |

| Spoonable / Cup Yogurt |

| Drinkable Yogurt |

| Dairy-based Organic Yogurt |

| Plant-based Organic Yogurt |

| On-trade | |

| Off-trade | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Plain Organic Yogurt | |

| Flavored Organic Yogurt | ||

| By Form | Spoonable / Cup Yogurt | |

| Drinkable Yogurt | ||

| By Source | Dairy-based Organic Yogurt | |

| Plant-based Organic Yogurt | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the organic yogurt market by 2031?

It is expected to reach USD 19.11 billion by 2031, growing at an 8.21% CAGR over 2026-2031.

Which product type is forecast to grow the fastest?

Plain organic yogurt is projected to advance at an 8.26% CAGR through 2031 as consumers favor customizable, lower-sugar bases.

Why are drinkable organic yogurts gaining popularity?

Urban lifestyles favor portable nutrition, and drinkables offer resealable, high-protein options suited to breakfast commutes and desk-side snacks.

Which region will witness the fastest market growth?

Asia-Pacific is projected to expand at a 9.46% CAGR through 2031, led by China’s middle-class expansion and India’s organized retail growth.

Page last updated on: