Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 27.21 Billion |

| Market Size (2026) | USD 28.43 Billion |

| Market Size (2031) | USD 35.39 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Ice Cream Market Analysis by Mordor Intelligence

The Europe ice cream market size was valued at USD 27.21 billion in 2025 and estimated to grow from USD 28.43 billion in 2026 to reach USD 35.39 billion by 2031, at a CAGR of 4.48% during the forecast period (2026-2031). Despite facing inflationary challenges, the market is buoyed by several key trends. Premiumization is driving demand as consumers increasingly seek high-quality, indulgent products. The shift towards plant-based options is gaining momentum, catering to the growing vegan and health-conscious population. Adventurous flavor experimentation is also attracting consumers looking for unique and innovative taste experiences. Additionally, a strong emphasis on sustainability is shaping purchasing decisions, with eco-friendly packaging and transparent labeling becoming critical factors. Consumers are willing to pay a premium for products that align with these values. In response, established brands are actively renovating their portfolios to include such offerings while leveraging cost-efficient scales to maintain competitiveness and defend their market share.

Key Report Takeaways

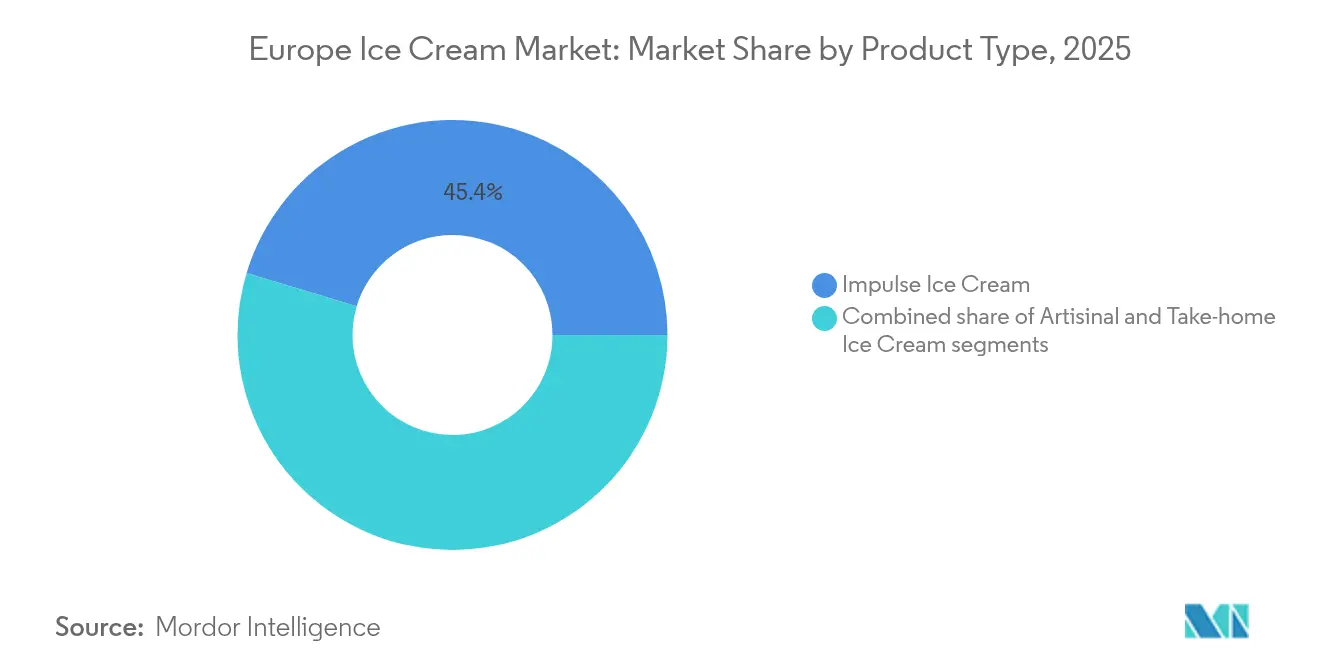

- By product type, impulse ice cream led with 45.35% of the Europe ice cream market share in 2025 while artisanal offerings are projected to advance at a 6.55% CAGR through 2031.

- By category, dairy accounted for 71.58% of the Europe ice cream market size in 2025, whereas non-dairy alternatives are expected to expand at a 7.09% CAGR between 2026-2031.

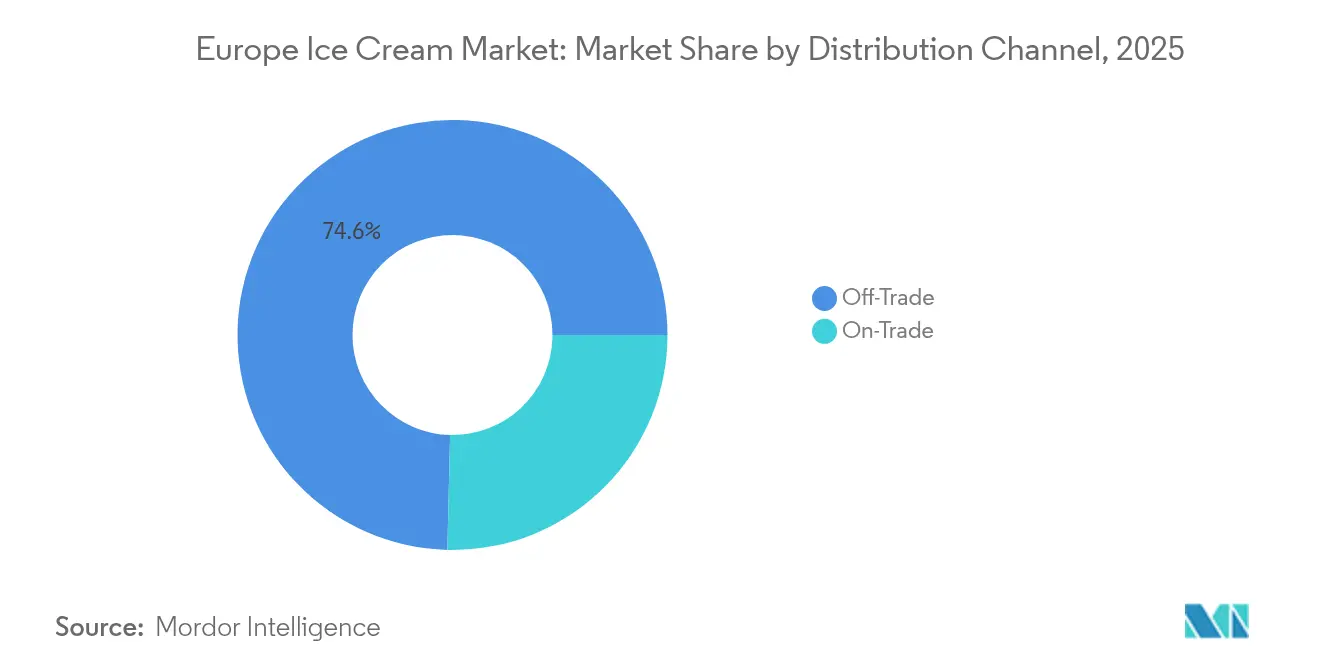

- By distribution channel, off-trade captured 74.62% value share of the Europe ice cream market size in 2025, yet on-trade is set to rebound at a 6.16% CAGR during the same horizon.

- By geography, Germany held 18.94% of the Europe ice cream market share in 2025, while Belgium is forecast to grow at a 7.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ice Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium, high-end, and artisan ice cream products | +1.8% | Italy, Germany, France, Belgium | Medium term (2-4 years) |

| Increasing consumer preference for low-calorie, low-sugar, and vegan options | +1.2% | Northern Europe, Germany, Netherlands | Long term (≥ 4 years) |

| Continuous flavor innovation and introduction of novel textures and formats | +0.9% | EU-wide | Short term (≤ 2 years) |

| Seasonal demand peaks in warmer months enhancing sales | +0.6% | Southern Europe, Mediterranean regions | Short term (≤ 2 years) |

| Indulgence-led snacking culture and premiumization | +0.7% | Western Europe, Urban centers | Medium term (2-4 years) |

| Growing emphasis on eco-friendly and sustainable packaging | +0.4% | EU-wide, Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for premium, high-end, and artisan ice cream products

Consumers increasingly seek premium, high-end, and artisan ice cream products, driving growth in the market. For instance, the rising popularity of gelato and sorbet, known for their rich flavors and natural ingredients, reflects this trend. Additionally, brands are introducing innovative offerings, such as organic, dairy-free, and low-calorie options, to cater to health-conscious consumers while maintaining a premium appeal. This shift is further supported by the growing preference for unique and indulgent flavors, such as salted caramel, pistachio, and exotic fruit blends, which resonate with the evolving tastes of European consumers. Furthermore, the increasing focus on sustainability and ethical sourcing has led to the introduction of ice creams made with locally sourced ingredients and eco-friendly packaging. Premium brands, such as Häagen-Dazs and Magnum, continue to dominate the market by offering limited-edition flavors and collaborating with renowned chefs to create exclusive products. The rise of artisanal ice cream parlors across Europe, emphasizing small-batch production and handcrafted quality, also contributes to this growing demand.

Increasing consumer preference for low-calorie, low-sugar, and vegan options

The increasing consumer preference for low-calorie, low-sugar, and vegan ice cream options is a significant market driver fueling growth and innovation within the market. Consumers today are more health-conscious and environmentally aware, seeking treats that align with lifestyle choices centered on wellness, sustainability, and ethical consumption. Low-calorie and low-sugar ice creams appeal to those managing diets and conditions like diabetes or those simply wishing to indulge guilt-free, while vegan ice creams attract a broader demographic concerned with animal welfare, lactose intolerance, and reducing carbon footprints. Vegan ice cream innovation is thriving with brands introducing diverse flavor profiles and improved textures to satisfy consumers without compromising on indulgence. Popular bases like almond milk are favored for their creamy texture and lower calorie content compared to dairy, while flavors such as caramel and chocolate are reformulated to deliver richness that parallels traditional ice creams. Notable examples include companies like Over The Moo in the UK, which introduced new dairy-free chocolate, vanilla, and caramel flavors in 2024, further expanding the market’s appeal. This trend is supported by increased availability in supermarkets, specialty stores, and e-commerce platforms, making these healthier and ethical choices increasingly accessible.

Continuous flavor innovation and introduction of novel textures and formats

Manufacturers in Europe are driving the ice cream market by innovating with flavors and textures. They are creating unique combinations like lavender honey, matcha green tea, and salted caramel to meet evolving consumer preferences. Additionally, the market has seen the emergence of innovative textures like mochi ice cream and rolled ice cream, which offer consumers a distinctive sensory experience. Furthermore, the introduction of plant-based and dairy-free ice cream options, such as almond milk or oat milk-based products, has gained traction among health-conscious and vegan consumers. Seasonal and limited-edition flavors, such as pumpkin spice in autumn or berry-infused varieties in summer, also play a crucial role in attracting consumer interest. These advancements not only attract new customers but also encourage repeat purchases, contributing significantly to market growth. The incorporation of functional ingredients, such as probiotics or added protein, further enhances the appeal of ice cream products, aligning with the growing demand for healthier indulgence options.

Seasonal demand peaks in warmer months enhancing sales

The European ice cream market experiences a pronounced seasonal demand pattern, with sales peaking significantly during the warmer months. This seasonal surge is driven largely by consumer behavior favoring cold treats as a refreshing option to beat the summer heat. As temperatures rise, consumers increase their ice cream consumption, turning to a variety of formats such as cones, tubs, and bars, which are more appealing in warm weather. Retailers and manufacturers capitalize on this pattern through targeted marketing campaigns, innovative limited-edition summer flavors, and expanded product availability in convenience stores, supermarkets, and foodservice outlets. This peak season not only boosts volume sales but also allows premium and artisanal brands to introduce exclusive offerings that cater to heightened consumer indulgence during these months. The seasonal demand cycle enhances the overall market growth and revenue generation capacity. This seasonal spike is crucial for businesses to optimize production planning, supply chain logistics, and inventory management to avoid stockouts and meet surge demands efficiently. Moreover, the seasonality influences product innovation, with brands often launching lighter, fruit-based, and plant-based options tailored for summer consumption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing awareness and concerns about sugar and fat content impacting sales | -0.8% | Northern Europe, Health-conscious markets | Medium term (2-4 years) |

| Competition from alternative frozen desserts and snacks | -0.6% | EU-wide, Urban centers | Short term (≤ 2 years) |

| Supply chain disruptions affecting raw material availability and costs | -0.4% | EU-wide | Short term (≤ 2 years) |

| Volatile dairy commodity prices and supply shocks | -0.5% | Western Europe, Urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing awareness and concerns about sugar and fat content impacting sales

Rising awareness of sugar and fat content is affecting sales in the European ice cream market. Consumers are increasingly prioritizing healthier dietary choices, leading to a decline in the demand for traditional ice cream products that are high in sugar and fat. In 2024, the International Diabetes Federation reports that approximately 66 million individuals in Europe are grappling with diabetes [1]Source: International Diabetes Federation, "The Diabetes Atlas- Data by Region", diabetesatlas.org. This alarming statistic highlights the growing health concerns among the population, further influencing purchasing decisions. Additionally, the increasing prevalence of obesity and related health conditions has amplified the demand for low-sugar, low-fat, or alternative dessert options. As a result, manufacturers are under pressure to reformulate their products and introduce healthier alternatives to cater to this shifting consumer preference. However, the reformulation process often involves higher production costs and challenges in maintaining the taste and texture of traditional ice cream, which can hinder market growth.

Competition from alternative frozen desserts and snacks

The market faces notable competition from alternative frozen desserts and snacks, which acts as a significant restraint on its growth. Consumers today are increasingly drawn to a wide range of frozen treats beyond traditional ice cream, such as frozen yogurt, dairy-free puddings, sorbets, gelatos, and plant-based alternatives, which offer different textures, flavors, and perceived health benefits. These substitutes appeal particularly to health-conscious consumers seeking lower-calorie, lower-fat, or lactose-free options, thereby eroding the conventional ice cream customer base. The availability and growing popularity of these alternatives reflect broader shifts in consumer preferences toward wellness, dietary restrictions, and ethical consumption practices. Frozen yogurt, for example, has gained traction as a perceived healthier substitute due to its probiotic content and lower fat profile compared to typical ice creams. Similarly, non-dairy frozen desserts made from almond, coconut, oat, or soy milk cater to vegan consumers and those with lactose intolerance. The rising adoption of plant-based diets in Europe has driven innovation and expanded the range of these products, making them increasingly competitive with traditional ice cream.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Artisanal Momentum Challenges Impulse Dominance

Impulse ice cream dominated the European ice cream market in 2025, capturing a substantial 45.35% share. This leadership is largely fueled by the widespread presence of convenience stores, which provide easy access and encourage spontaneous purchases. The format’s strength lies in its ability to cater to quick, on-the-go consumption, appealing to a broad demographic that values accessibility and immediate gratification. Impulse ice cream products typically include single-serve options such as cones, bars, and sandwiches, making them highly suitable for busy lifestyles. Retailers leverage prominent shelf placement and frequent promotions to drive volume sales within this segment across Europe’s diverse retail environments. Despite increasing competition from premium and artisanal offerings, impulse ice cream remains a cornerstone of market volume due to its convenience and affordability.

Conversely, artisanal ice cream represents the fastest-growing segment in the European market, expanding at an impressive CAGR of 6.55% through 2031. This growth mirrors consumer trends toward premiumization, where shoppers increasingly prioritize authentic, high-quality experiences over basic convenience. Artisanal ice cream appeals especially to discerning consumers who seek craftsmanship, unique and sophisticated flavor profiles, and often locally sourced or organic ingredients. This segment benefits from growing consumer interest in natural, less processed products as well as elevated packaging and storytelling that enhance perceived value. Premium artisanal brands typically focus on small-batch production and innovative recipes, differentiating themselves from mass-market offerings.

By Category: Plant-Based Acceleration Amid Dairy Dominance

Dairy ice cream maintained its dominant position commanding a substantial 71.58% share in 2025. This segment’s longevity stems from deep-rooted consumer preferences for the traditional creamy texture, rich taste, and familiarity associated with dairy-based products. Many established brands continue to rely on their heritage dairy lines, supported by widespread availability across supermarkets, convenience stores, and foodservice outlets. The segment benefits from strong brand loyalty, extensive production capacity, and distribution efficiencies that help sustain its leading market presence. Moreover, continuous innovation within dairy ice cream—including new flavors, premium ingredients, and enhanced quality—helps maintain consumer interest. Despite rising health and ethical concerns, dairy ice cream remains the foundational choice for a wide demographic across Europe.

In contrast, non-dairy ice cream alternatives represent the fastest-growing segment, expanding at a notable CAGR of 7.09% through 2031. This surge is driven by increasing consumer demand for plant-based and vegan options, reflecting wider lifestyle shifts toward health consciousness, environmental sustainability, and ethical consumption. Non-dairy alternatives utilize a variety of bases such as almond, oat, coconut, and soy, appealing to lactose-intolerant consumers and those seeking cleaner, more natural ingredient profiles. The segment’s growth is further fueled by innovative formulations that closely mimic the texture and creaminess of traditional dairy ice cream, improving consumer acceptance. Additionally, heightened marketing efforts around sustainability and transparency, along with expanding retail and foodservice offerings, have boosted accessibility and consumer trial.

By Distribution Channel: Off-Trade Strength Meets On-Trade Recovery

Off-trade channels dominated the European ice cream market in 2025, commanding a significant 74.62% share of total revenue. This leading position is largely supported by the widespread availability and extensive reach of supermarkets, hypermarkets, and grocery stores, which remain the primary purchasing destinations for most consumers. Off-trade benefits from strong distribution networks, competitive pricing, and frequent promotional activities that enhance product visibility and accessibility. The convenience of in-home consumption also sustains steady demand, especially for traditional and premium ice cream varieties. Additionally, the growth of e-commerce within off-trade offers consumers easy access to a broad selection of products, including niche and emerging brands, further reinforcing this channel’s dominance.

In contrast, on-trade channels are the fastest-growing segment, recovering at a CAGR of 6.16% through 2031 as hospitality venues rebound from pandemic disruptions. Establishments such as cafés, restaurants, hotels, and experiential dining venues are innovating their ice cream offerings, introducing creative serving formats that blur the lines between dessert and immersive culinary experiences. This growth reflects consumers’ renewed enthusiasm for social dining, premiumization, and unique indulgences that go beyond conventional ice cream consumption. On-trade operators increasingly emphasize artisanal products, novel presentations, and limited-edition flavors to attract discerning clientele seeking both quality and novelty. Moreover, sustainability considerations and ethical sourcing are becoming key differentiators in this segment, aligning with evolving consumer values.

Geography Analysis

In 2025, Germany commanded a notable 18.94% share of the market. This leadership is anchored in Germany's strong retail infrastructure and a pronounced consumer inclination towards premium and artisanal ice cream. Moreover, the nation champions sustainable agriculture and responsible ingredient sourcing. Urban hubs in Germany, where the urbanization rate reached 78% in 2024 (World Bank) , play a crucial role in fueling demand, particularly for plant-based and premium ice creams, reflecting a shift towards quality and health-conscious choices. Additionally, Germany's deep-rooted collaborations with local farmers and producers not only fortify its market stance but also drive innovation, ensuring both freshness and traceability. Furthermore, Germany's ice cream imports surged to approximately EUR 461.2 million in 2023, up from EUR 372.15 million in 2020, as reported by Statistisches Bundesamt , highlighting the growing demand for diverse ice cream offerings.

Belgium emerges as the fastest-growing geography in the Europe ice cream market, with a projected CAGR of 7.33% through 2031. This growth is fueled by Belgium’s rich confectionery heritage and its strategic focus on premium positioning. Belgian producers capitalize on quality ingredient sourcing and artisanal innovation, attracting discerning consumers who value authentic, high-quality frozen treats. The country’s emphasis on craftsmanship and luxury in its confectionery and ice cream segments helps differentiate its offerings, supporting robust growth in both domestic and export markets.

Other key European markets also contribute prominently to the ice cream sector's landscape. The United Kingdom is poised for substantial growth, driven by urban hubs like London and Manchester that benefit from strong investments in e-commerce and grocery retail. The UK market notably embraces plant-based ice creams, reflecting broader shifts toward vegan and health-oriented diets. France maintains steady growth through premium and artisanal ice cream demand, supported by innovation hubs in Paris and a surge in online grocery sales. Italy is notable for its artisanal gelato tradition, with Milan and Rome leading in growth due to a focus on locally sourced ingredients and government incentives that support sustainable agricultural practices.

Competitive Landscape

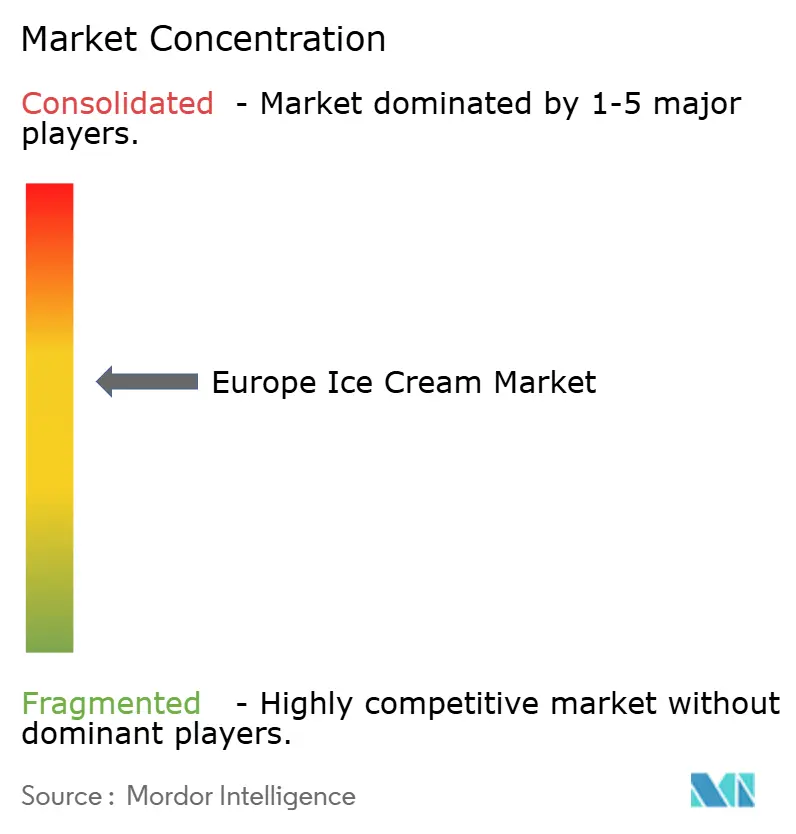

The European ice cream market exhibits a moderate concentration with a score of approximately 6, indicating a competitive landscape where several large multinational corporations coexist with a vibrant array of regional artisanal producers. This structure reflects a balance that allows dominant companies to leverage their scale, extensive distribution networks, and brand recognition while creating space for smaller, craft-focused brands to thrive by catering to niche consumer preferences for authenticity and unique flavors. The coexistence of these two segments fuels innovation and variety in the market, ensuring a broad spectrum of products from mainstream to premium artisan offerings.

Established multinational players such as Unilever, Nestlé, General Mills, and Mars dominate significant market share by capitalizing on economies of scale, extensive Research and Development, and strategic marketing. These companies continuously renovate their portfolios to include premium, plant-based, and health-oriented products aligned with evolving consumer demands. Their widespread distribution across supermarkets, convenience stores, and online channels provides strong market penetration. Simultaneously, they also navigate inflationary pressures through cost efficiencies and supply chain optimization, solidifying their market leadership while responding to sustainability mandates with eco-friendly packaging and responsible sourcing.

On the other hand, the artisanal and regional producers form a critical segment, representing the growing consumer demand for high-quality, authentic, and locally sourced products. These smaller producers thrive on craftsmanship, innovative flavors, and traditional production methods, often emphasizing natural and organic ingredients. The artisanal segment's growth is propelled by consumers willing to pay a premium for personalized experiences and specialty formats such as gelato and organic varieties. This interplay between large multinationals and specialty brands defines the moderate concentration score and highlights the dynamic nature of the European ice cream market, where scale and specialization coexist to meet diverse consumer tastes and drive overall market growth.

Europe Ice Cream Industry Leaders

-

Unilever PLC

-

Mars, Incorporated

-

General Mills, Inc.

-

Nestlé S.A

-

Froneri International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lotus Bakeries expanded its partnership with Mondelēz International to include the ice cream category through collaboration with Froneri, starting production and marketing of Biscoff ice cream in several European countries beginning 2026, leveraging Froneri's manufacturing expertise for enhanced distribution and product development.

- February 2025: Magnum, the UK ice cream brand under Unilever, has unveiled its latest offering: a marbled ice cream stick range named Utopia. Magnum touts these as its ‘most indulgent and premium flavours yet. Utilizing a novel ingredient marbling technology, the Utopia range promises a ‘truly multisensorial’ experience, blending rich flavours with a multi-layered architecture and sauce. The debut features two enticing variants: Double Cherry and Double Hazelnut.

- February 2025: Häagen-Dazs, with robust marketing backing, has introduced Stickbars in the United Kingdom. These premium ice cream bars, wrapped in rich Belgian chocolate, feature popular flavors such as Salted Caramel and Cookies & Cream. The launch aims to reshape the brand's indulgence image by appealing to consumers seeking a luxurious dessert experience.

- November 2024: Ferrero UK has unveiled its latest offering: Kinder Bueno ice cream cones, tapping into the surging appetite for novel frozen treats. These cones, designed to cater to diverse consumer preferences, are available in both single servings and multipacks. They feature two delectable flavors: the classic Kinder Bueno, known for its rich hazelnut and chocolate taste, and the lighter Kinder Bueno White, offering a creamy and refreshing alternative.

Europe Ice Cream Market Report Scope

Ice cream is a sweetened frozen food typically eaten as a snack or dessert. The European ice cream market is segmented by product type, category, distribution channel, and geography. By product type, the market is segmented into artisanal ice cream, impulse ice cream, and take-home ice cream. By category, the market is segmented into dairy and non-dairy. By distribution channel, the market is segmented into on-trade and off-trade. Off-trade is further sub-segmented into specialist retailers, hypermarkets/supermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into Germany, the United Kingdom, France, Russia, Spain, Italy, and Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Artisanal Ice Cream |

| Impulse Ice Cream |

| Take-home Ice Cream |

By Category

| Dairy |

| Non-Dairy (Plant-based) |

Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Specialist Retailers | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Belgium |

| Poland |

| Sweden |

| Rest of Europe |

| By Product Type | Artisanal Ice Cream | |

| Impulse Ice Cream | ||

| Take-home Ice Cream | ||

| By Category | Dairy | |

| Non-Dairy (Plant-based) | ||

| Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Specialist Retailers | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Poland | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe ice cream market?

The market is valued at USD 28.43 billion in 2026.

How fast is plant-based ice cream growing across Europe?

Non-dairy alternatives are forecast to expand at a 7.09% CAGR between 2026-2031.

Which country leads regional sales?

Germany accounts for 18.94% of 2025 value thanks to large-scale production and strong exports.

Which product segment is expanding quickest?

Artisanal ice cream shows the fastest momentum with a 6.55% CAGR through 2031.

Page last updated on: