Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 34.09 Billion |

| Market Size (2026) | USD 36.07 Billion |

| Market Size (2031) | USD 44.86 Billion |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Ice Cream Market Analysis by Mordor Intelligence

The Asia-Pacific ice cream market size is expected to grow from USD 34.09 billion in 2025 to USD 36.07 billion in 2026 and is forecast to reach USD 44.86 billion by 2031 at 4.46% CAGR over 2026-2031. Urban migration, the expansion of convenience-store networks, and rising disposable incomes are driving significant volume growth. At the same time, premiumization, particularly in markets like China, Japan, and Australia, is contributing to substantial value expansion. Structural cold-chain gaps in rural India and Southeast Asia are causing spoilage rates to reach up to 20%, which continues to compress margins outside of top-tier cities. Multinational companies are addressing these challenges by establishing in-market production facilities and introducing super-premium sub-brands to cater to evolving consumer preferences. Meanwhile, local players are leveraging niche flavors and affordable impulse formats to safeguard their market share and remain competitive. Although input-cost volatility in milk and cocoa presents a near-term risk, companies are actively adopting digital cold-chain monitoring systems and innovating with sustainable packaging solutions. These efforts are not only reducing costs but also creating measurable brand differentiation in the market.

Key Report Takeaways

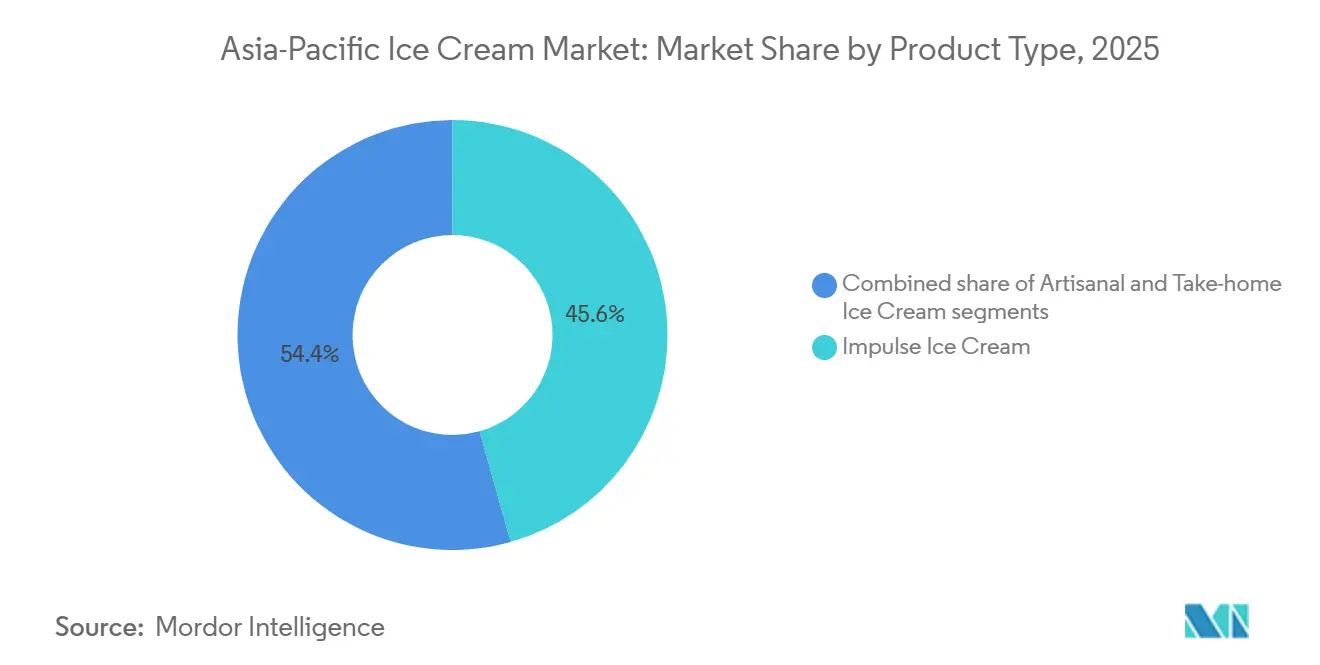

- By product type, impulse ice cream led with 45.63% revenue share in 2025, while artisanal formats are advancing at a 5.04% CAGR through 2031.

- By category, dairy-based offerings captured 86.26% of the Asia-Pacific ice cream market share in 2025; non-dairy alternatives are expanding at a 6.31% CAGR.

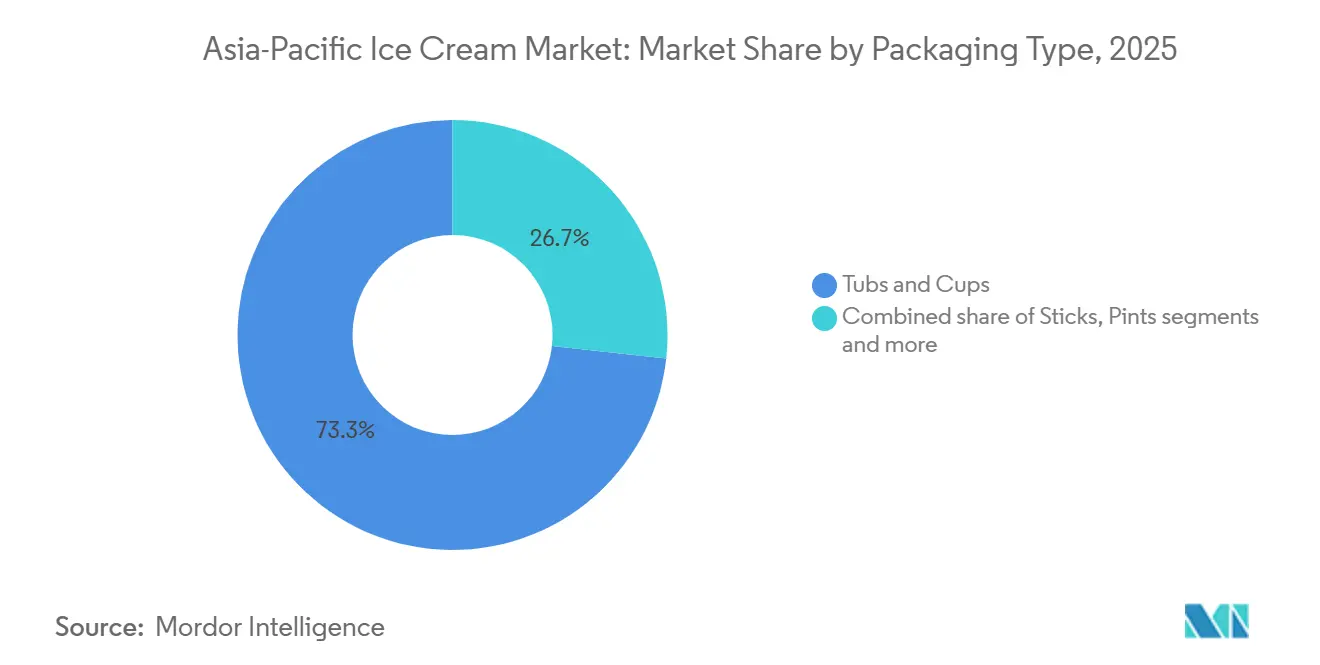

- By packaging, tubs and cups held 73.18% share in 2025; pints are projected to grow at a 5.52% CAGR to 2031.

- By distribution channel, off-trade commanded 77.21% share in 2025, whereas on-trade venues are set to record a 5.54% CAGR.

- By geography, China accounted for 41.69% revenue in 2025, while India is forecast to post the fastest 6.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Ice Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urbanization and changing lifestyles | +1.2% | China, India, Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Growing demand for premium and artisanal ice cream with innovative flavors | +0.9% | China, Japan, South Korea, Australia, Singapore | Long term (≥ 4 years) |

| Surging demand for functional, low-sugar, and plant-based ice cream options | +0.8% | Australia, Japan, China, India | Medium term (2-4 years) |

| Expansion of foodservice outlets, dessert cafés, and experiential dining concepts | +0.7% | China, India, Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Rising adoption of Western-style desserts fueling the demand | +0.6% | India, Vietnam, Indonesia, Philippines | Medium term (2-4 years) |

| Strong influence of social media and digital marketing increasing product visibility | +0.5% | Regional, with concentration in China, India, Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising urbanization and changing lifetsyles

Urbanization is reshaping ice cream consumption patterns, with city dwellers preferring convenience-oriented products and consuming more per capita. A UN-Habitat report states that Asia hosts 54% of the world's urban population, or over 2.2 billion people. By 2050, this figure is expected to grow by 1.2 billion, a 50% increase[1]Source: UN-Habitat, "Asia and the Pacific Region", unhabitat.org. Rapid metropolitan growth in India and China has concentrated consumers with rising disposable incomes, boosting demand for premium ice cream products and increasing purchase frequency. Urban lifestyles have driven demand for quick-consumption formats. In cities like Jakarta, Manila, and Mumbai, working professionals are replacing sit-down desserts with grab-and-go options, favoring stick and cone formats over tubs. Yili's 2024 acquisition of Thailand's Chomthana reflects a strategy to capitalize on this trend, leveraging Chomthana's 60-year distribution network to make single-serve SKUs easily accessible to commuters. Urbanization also accelerates cold-chain investments, as cities attract logistics infrastructure faster than rural areas. This reduces spoilage risks and enables multinationals to introduce premium lines requiring strict temperature control.

Growing demand for premium and artisanal ice cream with innovative flavors

Consumers in China, Japan, and Australia are driving the premiumization trend by willingly paying 30-50% more for artisanal brands that emphasize provenance, unique ingredients, and limited-edition offerings. According to the Japan Ice Cream Association, the average household spending on ice cream for households with two or more people rose to approximately JPY 12,295 in 2024, up from JPY 11,580 in 2023, marking a new record high and highlighting growing consumer demand[2]Source: Japan Ice Cream Association, "Domestic and Overseas Sales of Japanese Ice Cream Hit Record Highs", icecream.or.jp. Nestlé's Mövenpick responded to this trend in 2024 by launching in China with Swiss-origin positioning and flavors like caramelized almond and Madagascar vanilla, securing distribution in over 5,000 premium retail outlets within six months. Barry Callebaut's 2024 trend report revealed that 80% of Asian consumers prefer multi-texture experiences such as crunchy inclusions, swirls, and layered cores—over single-note flavors. This preference is pushing brands to adopt advanced co-extrusion and variegation technologies, which were previously cost-prohibitive for mid-tier players. Artisanal brands like Singapore's Inside Scoop and Malaysia's Udders are leveraging local ingredients, including pandan, black sesame, and yuzu, to differentiate themselves from multinational portfolios.

Surging demand for functional, low-sugar, and plant-based ice cream options

Surging demand for functional, low-sugar, and plant-based ice cream options is emerging as a key growth driver in the Asia-Pacific ice cream market, reflecting shifting consumer preferences toward healthier indulgence. Health-conscious reformulation is accelerating as governments tighten sugar regulations and consumers increasingly seek added functional benefits such as probiotics, protein fortification, and reduced-calorie formulations. Manufacturers are responding by introducing plant-based alternatives made from oat, almond, coconut, and soy bases, catering to lactose-intolerant and flexitarian consumers across markets like Australia, Japan, and South Korea. Regulatory initiatives are further influencing product innovation; for instance, Australia’s front-of-pack Health Star Rating system, updated in 2024, penalizes frozen desserts containing more than 15 grams of sugar per 100 milliliters. This has prompted companies such as Bulla and Peters to reformulate flagship products using stevia and allulose blends that maintain sweetness while avoiding labeling penalties.

Expansion of foodservice outlets, dessert cafés, and experiential dining concepts

Expansion of foodservice outlets, dessert cafés, and experiential dining concepts is significantly driving growth in the Asia-Pacific ice cream market, particularly in urban centers with strong youth and middle-class populations. The rapid proliferation of specialty dessert cafés, premium gelato chains, and quick-service restaurant formats has increased the visibility and accessibility of ice cream as an impulse and social consumption product. Experiential dining trends, including live ice cream preparation, customizable toppings, and visually appealing presentations, are encouraging higher consumer engagement and repeat purchases. Tourism recovery across key markets such as Japan, Thailand, and South Korea is further supporting demand through hotel, café, and entertainment venue channels. Foodservice operators are also collaborating with ice cream brands to introduce limited-edition flavors and seasonal offerings that enhance menu innovation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health concerns regarding sugar, fat content, and calorie intake | -0.7% | Australia, Japan, South Korea, urban China and India | Medium term (2-4 years) |

| Fluctuating raw material prices including milk, sugar, and cocoa | -0.5% | Regional, with acute impact in China, India, Indonesia | Short term (≤ 2 years) |

| Limited cold chain infrastructure and refrigeration challenges in rural and emerging markets | -0.6% | India, Indonesia, Vietnam, Philippines, rural China | Long term (≥ 4 years) |

| High energy costs impacting frozen storage and distribution efficiency | -0.4% | Southeast Asia, Australia, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health concerns regarding sugar, fat content, and calorie intake

Health consciousness increasingly constrains traditional ice cream consumption as consumers become more aware of nutritional content and its health implications, particularly in developed Asia-Pacific markets where obesity rates and diabetes prevalence drive dietary behavior changes. In 2024, the International Diabetes Federation highlighted that around 107 million individuals in Southeast Asia are contending with diabetes, further influencing dietary choices[3]Source: International Diabetes Federation, "The Diabetes Atlas- Data by Region", diabetesatlas.org. For example, Singapore's Nutri-Grade initiative, which imposes stricter regulations on sodium and fat content, emphasizes the pivotal role of government interventions in altering product formulations and marketing tactics. In response to this divide, manufacturers are increasingly investing in Research and Development, particularly in sugar reduction technologies and alternative sweetening systems. As consumer education campaigns highlight nutritional content, consumers are scrutinizing ingredient lists more than ever. This heightened scrutiny has prompted brands to adopt transparent labeling strategies and healthier formulations, all to maintain their market access. Significantly, this trend is influencing impulse purchase decisions.

Limited cold chain infrastructure and refrigeration challenges in rural and emerging markets

In the Asia-Pacific ice cream market, limited cold storage facilities and inadequate accessibility in rural areas pose significant challenges. Many rural regions lack the infrastructure essential for storing and distributing ice cream, which needs a controlled temperature to ensure quality. Without reliable cold chain systems, ice cream products frequently spoil in these areas, leading to financial losses for both manufacturers and distributors. Logistical hurdles, including poor road connectivity, weak transportation networks, and minimal investment in rural infrastructure, further complicate supply chain operations. Moreover, high energy costs and an unreliable electricity supply in these regions make it even harder to maintain the necessary temperatures for ice cream storage and transport. These challenges not only limit market penetration but also reduce the availability of ice cream in rural areas, stunting the overall growth of the Asia-Pacific ice cream market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Artisanal Gains as Impulse Dominates

Impulse ice cream accounted for the largest revenue share in the Asia-Pacific ice cream market, capturing 45.63% of total market revenue in 2025. The dominance of this segment is primarily driven by strong consumer demand for convenient, single-serve formats that cater to on-the-go consumption and impulse purchasing behavior. Wide product availability across supermarkets, convenience stores, and vending channels further strengthens its market position. Manufacturers continue to invest in innovative flavors, attractive packaging, and affordable pricing strategies to maintain high purchase frequency among younger consumers and urban populations. Seasonal demand spikes, particularly during warmer months, also contribute significantly to the segment’s consistent sales performance.

Artisanal ice cream is emerging as the fastest-growing segment in the Asia-Pacific ice cream market, projected to expand at a CAGR of 5.04% through 2031. Growth in this segment is largely driven by increasing consumer preference for premium, authentic, and locally sourced products that emphasize quality and uniqueness. Rising disposable incomes and evolving taste preferences are encouraging consumers to explore small-batch and craft ice cream offerings with natural ingredients and innovative flavor profiles. The expansion of specialty ice cream parlors and boutique dessert outlets across urban centers is further accelerating demand. Consumers are also showing greater interest in products perceived as less processed and more indulgent, supporting the shift toward artisanal formats.

By Category: Non-Dairy Accelerates Amid Dairy Dominance

In 2025, dairy ice cream commanded a dominant 86.26% share of the Asia-Pacific ice cream market. This stronghold is bolstered by well-established supply chains that guarantee consistent quality, availability, and affordability. Consumers across diverse markets associate traditional dairy formulations with superior taste and creaminess. Furthermore, a long-standing cultural affinity for dairy-based desserts solidifies this preference, making dairy the go-to choice for indulgence. With broad distribution channels spanning supermarkets, convenience stores, and foodservice outlets, dairy ice cream's accessibility is unparalleled. These combined advantages not only position dairy ice cream as the bedrock of the regional industry but also underscore its continued influence in mainstream market dynamics, even amidst a rising interest in alternatives.

While dairy ice cream maintains its dominance, non-dairy ice cream is swiftly carving out a niche as the fastest-growing segment, projected to grow at a CAGR of 6.31% through 2031. This surge is a testament to evolving consumer preferences, driven by heightened health consciousness and a growing awareness of lactose intolerance in the Asia-Pacific. Plant-based alternatives are winning over consumers who desire lighter, allergen-free options that don't skimp on taste. Moreover, as consumers become increasingly concerned about environmental sustainability, the perception of plant-based options as more eco-friendly than traditional dairy is driving their adoption. Additionally, global trends in veganism and flexitarianism are encouraging experimentation, especially among younger, urban consumers with greater purchasing power.

By Packaging Type: Pints Rise as Tubs Hold Share

Tubs and cups represented the largest packaging segment in the Asia-Pacific ice cream market, accounting for 73.18% of total revenue share in 2025. The strong performance of this segment is largely attributed to its suitability for family consumption and multi-serving occasions, making it a preferred choice for household purchases. Consumers increasingly favor larger pack sizes that offer better value for money, particularly in price-sensitive markets across the region. The format also supports a wide range of product varieties, including premium, indulgent, and family-oriented offerings, enabling manufacturers to target diverse consumer groups. Retail expansion through supermarkets and hypermarkets has further strengthened the visibility and accessibility of tubs and cups, contributing to consistent sales volumes.

Pints are expected to emerge as the fastest-growing packaging segment in the Asia-Pacific ice cream market, projected to expand at a CAGR of 5.52% through 2031. Growth in this segment is closely linked to the rising demand for premium and personalized consumption experiences, as pints are often associated with indulgence and higher-quality formulations. Increasing urbanization and smaller household sizes are encouraging consumers to opt for single-portion or limited-quantity packaging that reduces wastage while maintaining freshness. Premium brands and artisanal producers are increasingly using pint packaging to introduce innovative flavors and niche offerings, attracting younger and higher-income consumers. The growing popularity of at-home indulgence and dessert consumption has also supported the expansion of this format.

By Distribution Channel: On-Trade Gains Ground

Off-trade channels dominated the Asia-Pacific ice cream market in 2025, accounting for 77.21% of total distribution. This segment’s leadership is primarily driven by the presence of hypermarkets, supermarkets, and e-commerce platforms that offer extensive product assortments and competitive promotional pricing. Consumers increasingly prefer these channels for their convenience, availability of bulk packs, and frequent discount offers. Retailers in these channels also benefit from high footfall and established supply chains, which ensure consistent product availability. Marketing initiatives, such as in-store displays and seasonal campaigns, further reinforce consumer engagement in off-trade outlets. The combination of affordability, accessibility, and variety has solidified off-trade channels as the largest contributor to regional ice cream sales.

On-trade channels are projected to be the fastest-growing distribution segment in the Asia-Pacific ice cream market, expanding at a CAGR of 5.54% through 2031. This growth is fueled by rising consumer interest in experiential consumption, as dessert cafés, parlors, and quick-service restaurants offer unique flavors and immersive tasting experiences. Social-media-driven trends and influencer marketing are encouraging younger consumers to visit on-trade venues for both indulgence and sharing experiences online. The expansion of specialty outlets and themed dessert cafés across urban centers is further boosting the segment’s visibility and attractiveness. Consumers increasingly view on-trade purchases as a lifestyle choice rather than just a product purchase, enhancing foot traffic and repeat visits.

Geography Analysis

China held the largest share in the Asia-Pacific ice cream market, accounting for 41.69% of total revenue in 2025. The segment’s dominance is driven by the country’s large population, rapid urbanization, and growing disposable incomes, which support high consumption of both mainstream and premium ice cream products. Expanding retail networks, including hypermarkets, supermarkets, and online platforms, have further increased product accessibility across urban and semi-urban areas. Strong marketing campaigns by leading international and domestic brands have helped create widespread brand awareness and loyalty. Additionally, evolving consumer preferences for indulgent flavors, innovative formats, and convenience products continue to fuel demand. Seasonal spikes during summer months also contribute significantly to sales, reinforcing China’s position as the largest market in the region.

India is projected to be the fastest-growing market in the Asia-Pacific ice cream segment, expected to expand at a CAGR of 6.39% through 2031. Growth is driven by rising disposable incomes, a young population, and increasing exposure to international brands and premium offerings. Rapid urbanization and the proliferation of modern retail outlets and e-commerce platforms are enhancing product availability and convenience. Changing lifestyles, coupled with growing interest in indulgent desserts and innovative flavors, are encouraging frequent consumption. Marketing initiatives targeting younger consumers and social-media-driven trends are also boosting brand engagement. As awareness of artisanal and premium ice cream increases, India is set to become a key growth engine for the regional market.

Other countries in the Asia-Pacific region, including Japan, Australia, Indonesia, and South Korea, contribute significantly to the ice cream market, each exhibiting distinct consumption patterns. Japan and South Korea show strong demand for premium, innovative, and health-conscious ice cream offerings, driven by urban consumers with high disposable incomes. Australia’s market is characterized by high per capita consumption and growing interest in natural, organic, and plant-based formats. Southeast Asian countries like Indonesia and Thailand are experiencing steady growth due to expanding modern retail infrastructure, rising middle-class populations, and increasing exposure to global brands. Across these markets, factors such as flavor innovation, convenient packaging, and retail promotions continue to shape consumer choices.

Competitive Landscape

The Asia-Pacific ice cream market exhibits a moderately fragmented competitive landscape, reflecting a mix of multinational corporations and regional players striving to capture market share. While global giants such as Unilever PLC and Nestlé S.A. dominate through their extensive brand portfolios, established distribution networks, and economies of scale, smaller regional and local companies focus on niche positioning and consumer-specific preferences. This fragmentation encourages continuous innovation, with companies competing not just on price, but on flavor development, packaging, and product formats that resonate with diverse consumer tastes across the region. Seasonal promotions, festive launches, and co-branding initiatives further intensify the competitive dynamics, creating an environment where differentiation is key to sustaining growth.

Multinational corporations bring significant advantages in terms of research and development, marketing capabilities, and brand recognition. Unilever, for instance, leverages its expertise in creating globally appealing products while adapting to local palates, introducing flavors and formats tailored to specific regional demands. Nestlé employs a similar strategy, combining global innovation pipelines with targeted campaigns for premium, artisanal, and health-conscious segments. These companies also benefit from advanced supply chain management and widespread retail presence, enabling rapid distribution and timely responses to changing market trends.

Regional and local players, on the other hand, often compete by offering unique flavors, culturally relevant products, and competitive pricing suited to domestic consumer preferences. They tend to be more agile in responding to emerging trends such as artisanal ice cream, plant-based alternatives, or functional ingredients. This localized focus allows smaller brands to carve out loyal customer bases and differentiate themselves from the larger, more standardized offerings of multinational firms. Additionally, collaborations with local suppliers, innovative marketing campaigns on social media, and presence in niche retail formats enable these players to capture growth in urban centers and emerging towns alike.

Asia-Pacific Ice Cream Industry Leaders

-

General Mills Inc.

-

Unilever PLC

-

Nestlé S.A.

-

Gujarat Cooperative Milk Marketing Federation Ltd (Amul)

-

Inner Mongolia Yili Industrial Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Meiji unveiled "Meiji Dear Milk Tokuno," a winter-exclusive addition to its Dear Milk ice cream lineup, with a nationwide debut in Japan on December 1, 2025. This new variant boasted a milk fat content of 19.5% and featured fresh cream sourced from Hokkaido's Tokachi region, ensuring a richer flavor tailored for the colder months.

- August 2025: Godiva Japan introduced a new premium ice cream product, the Godiva Cup Ice Cream Pistachio Chocolate, initially launched in late August 2025 at convenience stores nationwide, with a subsequent rollout to supermarkets from mid‑September. The offering combines a rich pistachio ice cream layer with decadent milk chocolate ice cream, encased in a crisp Belgian chocolate shell, delivering a multi‑sensory indulgence.

- August 2025: HOCCO Ice Creams expanded its product line with a limited‑edition Modak‑shaped ice cream created for the Ganesh Chaturthi festival. Available in two variants: White Chocolate Modak (coconut ice cream in a white chocolate shell) and Milk Chocolate Modak (coconut‑cream base with milk chocolate coating) the product blends cultural relevance with indulgent flavor.

- July 2025: Britannia Industries has unveiled its latest creation, NIC Bourbon Ice Cream. This new offering melds luxurious chocolate ice cream with the beloved crumbs of Britannia's Bourbon biscuits, catering to the cravings of chocolate lovers. With this launch, Britannia further redefines the Bourbon experience, presenting its signature flavor in a decadent ice cream format.

Asia-Pacific Ice Cream Market Report Scope

Ice cream is a sweetened frozen food typically eaten as a snack or dessert. The Asia-Pacific ice cream market has been segmented based on product type, category, packaging type, distribution channel, and geography. By product type, the market is segmented into impulse ice cream, artisanal ice cream, and take-home ice cream. Based on category, the market is segmented into dairy and non-dairy. By packaging type, the market is segmented by pints, tubs/cups, sticks and others. By distribution channel, the market is segmented into on-trade and off-trade. By geography, the market covers the major countries in the Asia-Pacific region like China, Japan, Australia, India, and the Rest of Asia-Pacific. For each segment, the market sizing and forecasts have been done on the basis of the value (in USD million) and Volume (liters).

By Product Type

| Artisanal Ice Cream |

| Impulse Ice Cream |

| Take-home Ice Cream |

By Category

| Dairy |

| Non-Dairy |

By Packaging Type

| Pints |

| Tubs/Cups |

| Sticks |

| Others |

Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Specialist Retailers | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Australia |

| New Zealand |

| Indonesia |

| Thailand |

| Vietnam |

| Malaysia |

| Philippines |

| Rest of Asia-Pacific |

| By Product Type | Artisanal Ice Cream | |

| Impulse Ice Cream | ||

| Take-home Ice Cream | ||

| By Category | Dairy | |

| Non-Dairy | ||

| By Packaging Type | Pints | |

| Tubs/Cups | ||

| Sticks | ||

| Others | ||

| Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Specialist Retailers | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large will the Asia-Pacific ice cream market be by 2031?

It is forecast to reach USD 44.86 billion by 2031, expanding at a 4.46% CAGR from 2026-2031.

Which product type leads regional revenue today?

Impulse formats, including sticks and cones, held 45.63% of 2025 sales.

What is driving non-dairy ice cream growth?

Rising lactose intolerance awareness and supportive labeling rules in Australia and India are pushing non-dairy alternatives at a 6.31% CAGR.

Which packaging format is growing fastest?

Pints, favored for portion control and premium positioning, are set to grow at 5.52% CAGR through 2031.

Why is India considered the fastest-growing national market?

Improving cold-chain infrastructure and rising urban incomes support a forecast 6.39% CAGR, outpacing mature Northeast Asian markets.

Page last updated on: