Spirulina Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

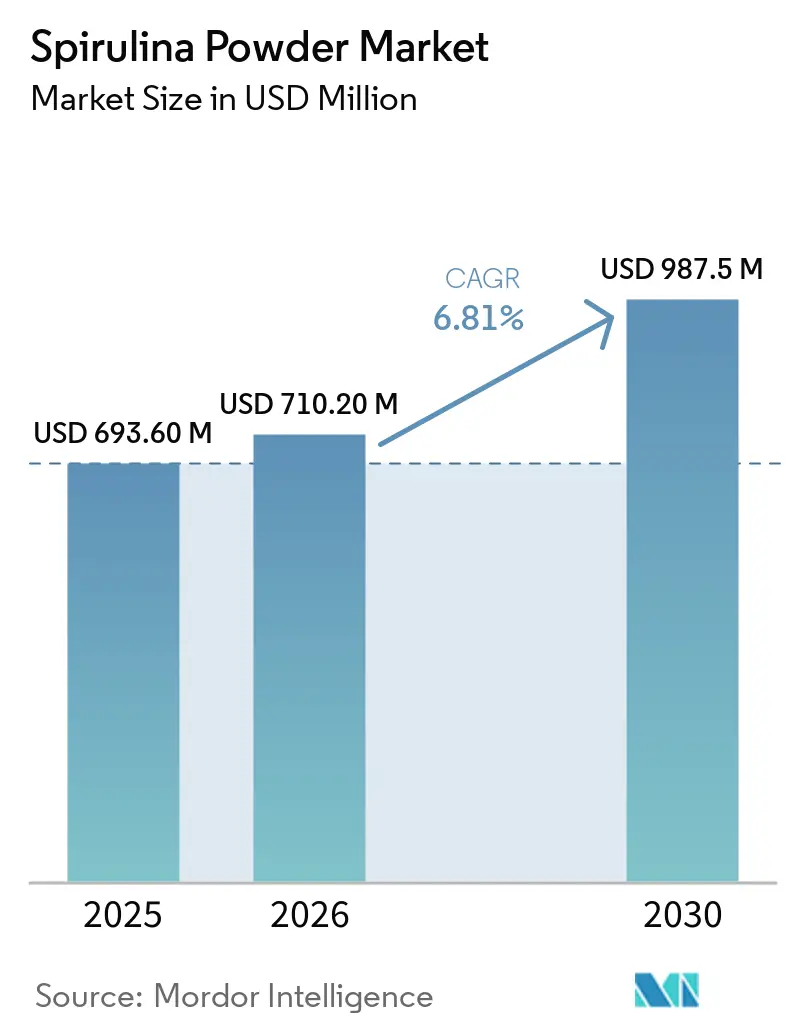

| Market Size (2026) | USD 710.20 Million |

| Market Size (2030) | USD 987.5 Million |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

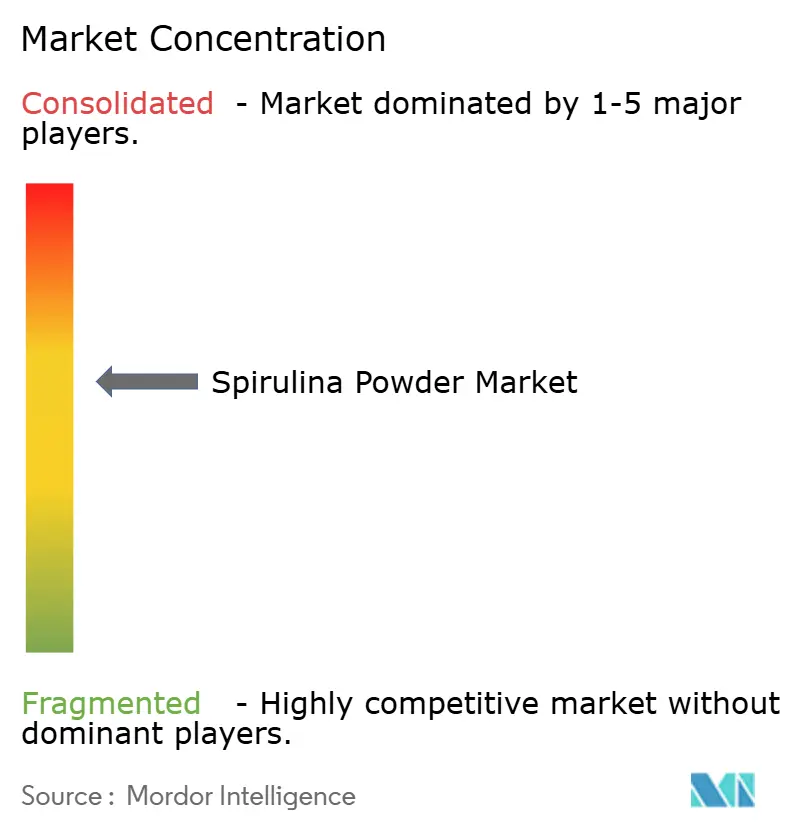

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spirulina Powder Market Analysis by Mordor Intelligence

The spirulina powder market size is valued at USD 693.6 million in 2025, is projected to reach USD 710.2 million by 2025, and is expected to reach USD 987.5 million by 2031, reflecting a CAGR of 6.18%. Demand is rising as food, supplement, and feed manufacturers use spirulina for protein enrichment, natural coloring, and broader clean-label positioning. In contrast, the 2026 United States regulatory expansion for spirulina extract has widened the commercial path for phycocyanin in food use. The spirulina market is also benefiting from stronger interest in plant-based nutrition, especially in premium supplements and sports nutrition, where protein density and antioxidant content support higher value positioning. At the same time, quality standards are becoming more demanding, which is pushing producers to invest in contamination control, better extraction systems, and more consistent cultivation models across the spirulina market. The competitive structure remains split between high-volume Asia-Pacific suppliers that compete on price and a smaller group of integrated producers that compete through certification, traceability, and application-focused product development, a gap reinforced by DIC Corporation’s USD 8 million smart-farming investment in California. This mix of regulatory expansion, premiumization, and rising process discipline is keeping the spirulina market on a steady growth path while shifting more value toward certified and specification-led supply chains.

Key Report Takeaways

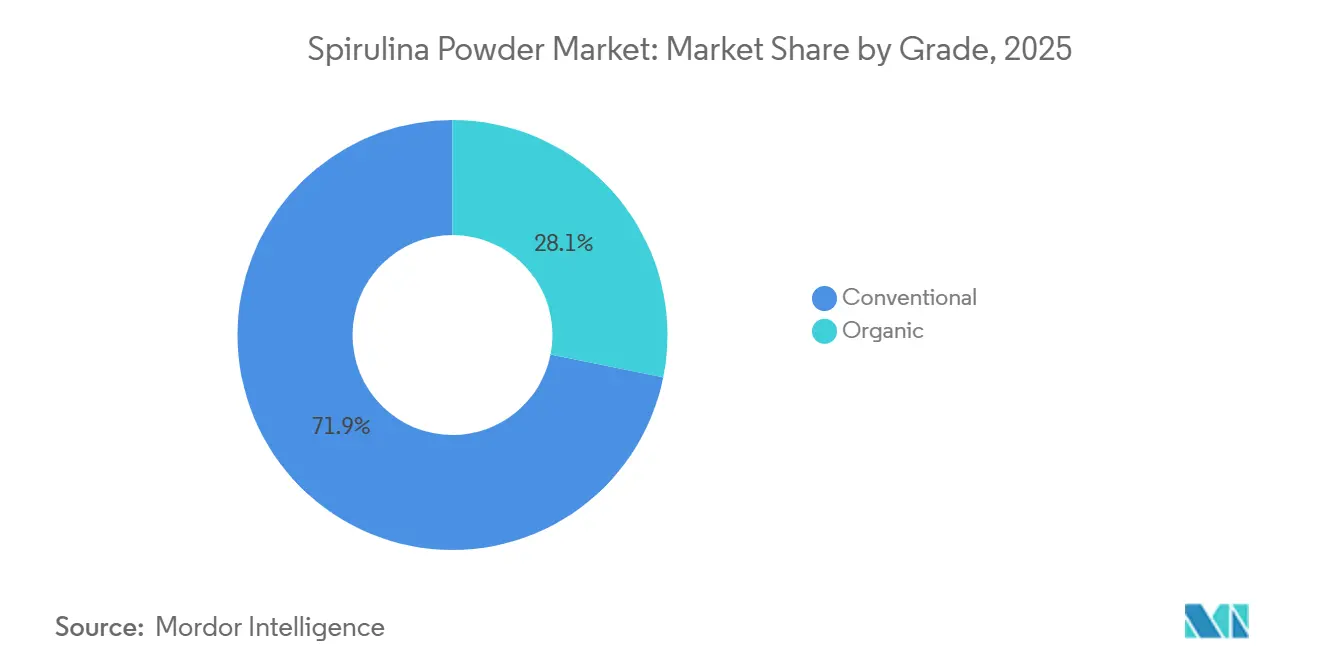

- By grade, conventional spirulina led with a 71.9% share in 2025, while organic spirulina is projected to grow at an 8.1% CAGR through 2031.

- By color, green spirulina held an 82.5% share in 2025, while blue spirulina is forecast to advance at a 7.4% CAGR through 2031.

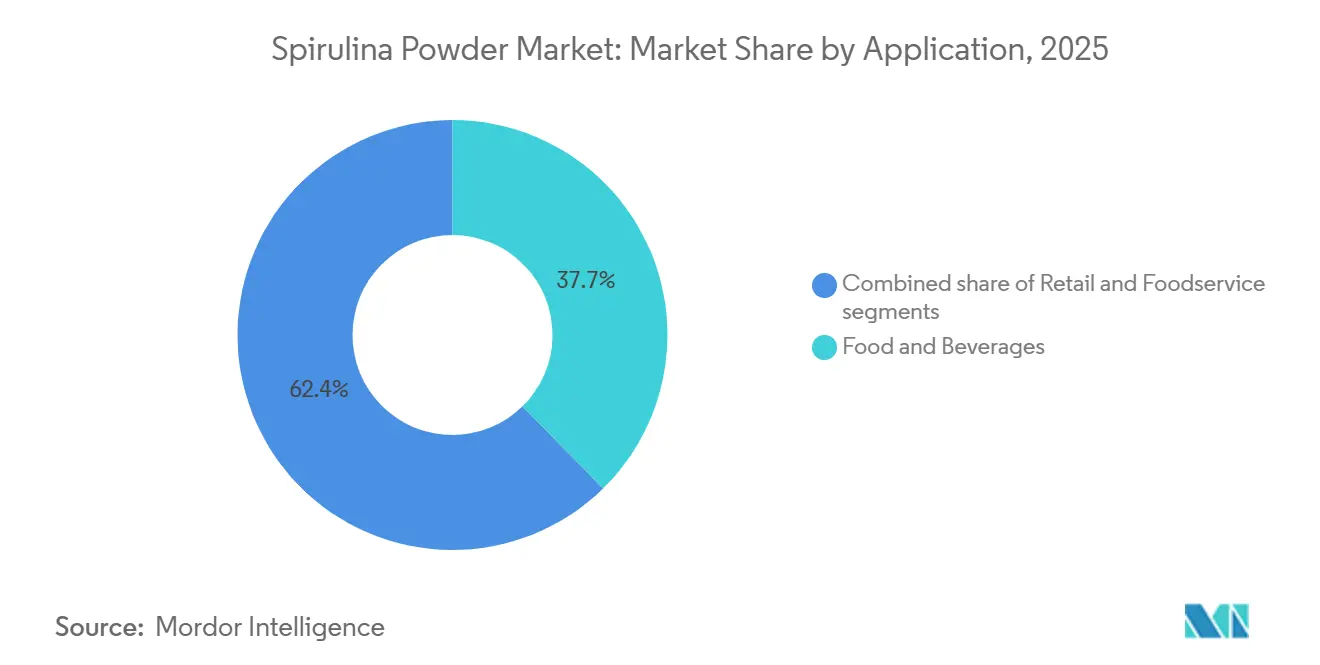

- By application, food and beverages accounted for 37.7% share of the spirulina market size in 2025, while dietary supplements are set to grow at a 7.5% CAGR through 2031.

- By production technology, open-pond cultivation held an 86.0% share in 2025, while closed-pond/photobioreactor systems are projected to expand at a 9.5% CAGR through 2031.

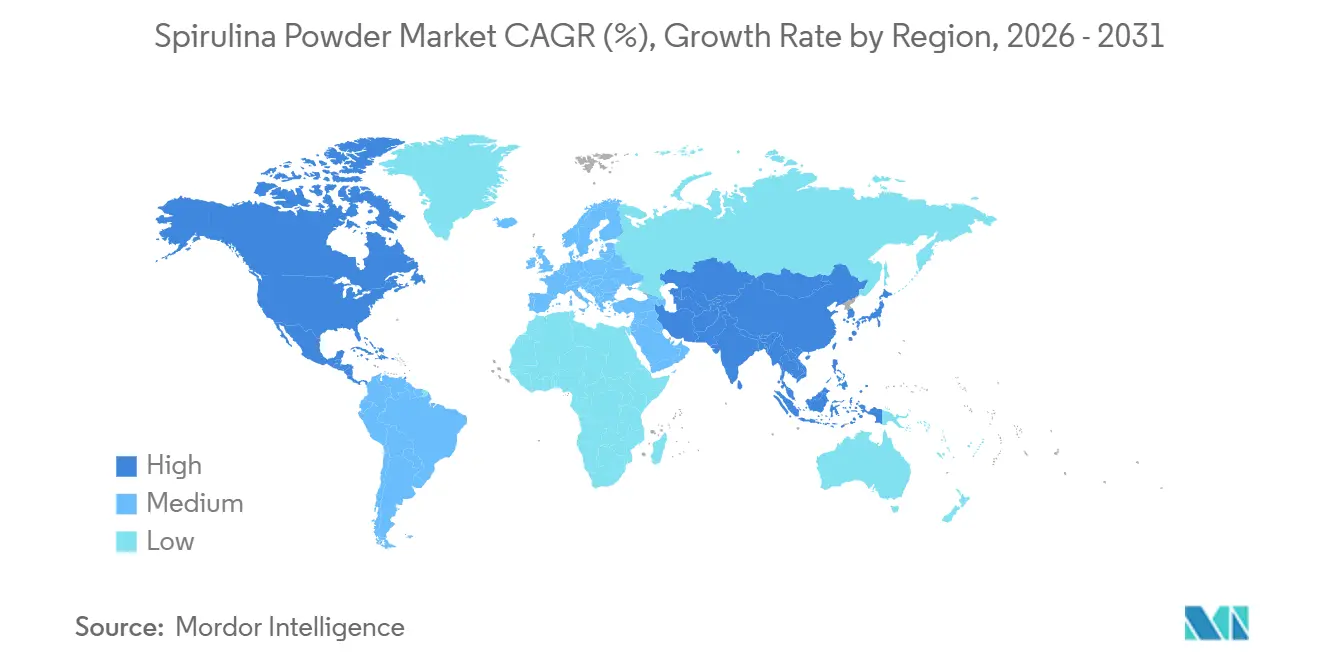

- By geography, North America held 38.6% of the spirulina market share in 2025, while Asia-Pacific is expected to record the highest regional CAGR at 9.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Spirulina Powder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label natural blue colorants | +1.3% | North America and Europe, Asia-Pacific emerging | Short term (≤ 2 years) |

| Functional beverage reformulation to replace synthetic pigments | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Premiumization of nutraceuticals and sports nutrition | +1.1% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Strain optimization and downstream yield gains in phycocyanin extraction | +0.7% | Asia-Pacific, especially China, and North America | Long term (≥ 4 years) |

| Expanding use in aquaculture feed and pet nutrition | +0.8% | Asia-Pacific, especially China and India, and Europe | Medium term (2-4 years) |

| Increasing consumption of Spirulina-based dietary supplements | +1.2% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label natural blue colorants

The spirulina market is benefiting from the growing demand for natural blue colorants in packaged food and beverage formulations. In February 2026, the United States Food and Drug Administration issued its final order expanding permitted use of spirulina extract to all human foods generally, which widened the ingredient’s commercial role beyond earlier, narrower applications[1]Source: U.S. Food and Drug Administration, “Listing of Color Additives Exempt From Certification, Spirulina Extract,” Federal Register, fda.gov. The same order also tightened heavy-metal specifications by lowering limits for lead, arsenic, and mercury and by adding a cadmium standard, which raised the quality threshold at the same time that the commercial scope increased. Blue remains one of the hardest shades to replace with natural ingredients, and spirulina-derived phycocyanin is among the few scalable options available to food formulators. The procedural delay announced in March 2026 did not change the Food and Drug Administration’s underlying safety determination, so the spirulina market continues to plan around a broader long-term role for spirulina extract in food reformulation. This is supporting a stronger demand for processors that can deliver stable color performance and tighter.

Functional beverage reformulation to replace synthetic pigments

The spirulina market is also gaining from reformulation activity in functional beverages, where synthetic pigment replacement has become more urgent. Food and Drug Administration approvals moved in steps from tablet and capsule coatings to beverage use and then to food use more broadly, which gave beverage makers a clearer regulatory path for gradual adoption. Beverage use remains technically demanding because phycocyanin can degrade under low pH and higher processing temperatures, so stable formulations require more advanced downstream know-how. That technical hurdle favors suppliers that can offer stabilized ingredients instead of only commodity powder, which is shifting value capture inside the spirulina market. The result is a more attractive growth path for high-purity liquid and formulation-ready extracts than for crude powder alone. This is likely to keep specification-led producers in a stronger position as the spirulina market expands across drink applications.

Premiumization of nutraceuticals and sports nutrition

The spirulina market is benefiting from a premium shift in nutraceuticals and sports nutrition, where consumers are looking for cleaner and more functional plant-based ingredients. The 2025 International Food Information Council (IFIC) Food and Health Survey found that 23% of Americans followed a high-protein diet, making it the most common dietary choice among surveyed adults[2]Source: International Food Information Council, “2025 IFIC Food & Health Survey,” IFIC, ific.org. Spirulina fits this demand because it combines high protein content with phycocyanin and other bioactive compounds that help it stand apart from more basic plant protein options. In the spirulina market, this makes certified and branded products more attractive to supplement companies that want a stronger quality signal at the shelf level. Organic certification also supports higher pricing, with certified products in the user-supplied draft carrying margins that are materially above conventional grades. That pricing gap is helping the spirulina market move value toward suppliers with better documentation, cleaner sourcing, and broader compliance credentials.

Strain optimization and downstream yield gains in phycocyanin extraction

The spirulina market is also being shaped by better strain selection and more efficient extraction methods for phycocyanin. Research published in 2025 described a phycocyanin biorefinery framework that combines direct air CO2 capture, passive dark-incubation extraction, and nutrient recovery, reducing dependence on more energy-intensive steps. Separate 2025 research showed that variable-frequency mixing in thin-layer fountain photobioreactors improved productivity without proportionate energy growth. Other 2025 work showed hydrodynamic cavitation as a viable extraction route, offering a lower-intensity path than freeze-thaw cycling or high-pressure homogenization. These process improvements matter because energy and yield remain key cost points in the spirulina market, especially for phycocyanin-rich products. Producers that commercialize these gains first are likely to strengthen margins and batch consistency across the spirulina market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Contamination control costs in open-pond cultivation | Contamination control costs in open-pond cultivation | Contamination control costs in open-pond cultivation | Contamination control costs in open-pond cultivation |

| Flavor, color, and solubility limitations in mainstream foods | Flavor, color, and solubility limitations in mainstream foods | Flavor, color, and solubility limitations in mainstream foods | Flavor, color, and solubility limitations in mainstream foods |

| Supply concentration in a few production hubs | Supply concentration in a few production hubs | Supply concentration in a few production hubs | Supply concentration in a few production hubs |

| Labeling and health-claim friction across markets | Labeling and health-claim friction across markets | Labeling and health-claim friction across markets | Labeling and health-claim friction across markets |

| Source: Mordor Intelligence | |||

Contamination control costs in open-pond cultivation

The spirulina market still faces a clear quality challenge in open-pond cultivation, where cost advantages can be weakened by contamination risk. The user-supplied draft pointed to a 2026 cross-market review by Cyanotech that found many retail spirulina products initially exceeded California Proposition 65 lead limits, signaling a broader supply-chain issue rather than an isolated event. Scientific literature also shows that open systems can concentrate heavy metals through water evaporation and can face cyanotoxin risk from co-cultivation with unwanted species. The Food and Drug Administration updated spirulina extract specifications and broader regulatory attention to contaminant limits, raising testing and remediation costs for suppliers that want access to premium channels. In the spirulina market, this narrows part of the historical cost gap between low-capex open ponds and higher-control production systems. It also shifts buyer preference toward suppliers that can prove contaminant control at both cultivation and finished-product stages.

Flavor, color, and solubility limitations in mainstream foods

The spirulina market also remains constrained by taste, color, and solubility issues in mainstream food applications. Recent academic work noted that spirulina’s grassy and marine sensory profile can restrict inclusion rates in many food formats, which limits its use as a major protein enrichment ingredient in volume categories. Phycocyanin also remains sensitive to heat and acidity, which narrows its application fit in pasteurized beverages and other harsher processing environments. Research on microencapsulation showed partial progress in odor masking and color management, but it also adds processing cost that can weigh on scalability for mid-sized buyers. This keeps more of the spirulina market centered in tablets, capsules, powders, and other formats where taste matters less. That product mix limits how quickly the spirulina market can move into larger-volume packaged food use cases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Organic Premiumization Drives Value Migration

Conventional spirulina retained 71.86% of the spirulina market share in 2025, which shows how strongly the segment still anchors industry volume. The spirulina market continues to rely on conventional output because open-pond infrastructure in major producing countries supports large batches and cost-sensitive supply. Bulk food enrichment, aquaculture feed, and private-label supplement channels all benefit from this price and scale position. Broad regulatory familiarity also keeps conventional spirulina as the default choice for many industrial buyers. This means the spirulina market still builds its base economics on conventional material even while premium subsegments expand.

Organic spirulina is forecast to grow at an 8.05% CAGR through 2031, which makes it the fastest-growing grade segment in the user-supplied draft. The spirulina market is seeing stronger demand for organic products because premium supplement brands and natural retailers increasingly treat certification as a shelf-access requirement rather than an optional label. In the United States, organic production is governed under the United States Department of Agriculture National Organic Program, while the European Union sets parallel rules through Regulation (EU) 2018/848 AMS. Those frameworks raise entry requirements, but they also help suppliers justify better pricing and stronger customer retention within the spirulina market. This makes organic spirulina less important for volume than conventional product, but more important for value growth.

By Color: Green Dominates Volume; Blue Commands Value Growth

Green Spirulina held an 82.5% share in 2025, which confirms that it remains the core color format by volume. The spirulina market depends on green spirulina because it fits the broadest application range across supplements, food fortification, cosmetics, and aquafeed. Its nutritional density, including protein, chlorophyll, carotenoids, and vitamins, keeps it useful even when precise color control is not the main purchase criterion. Large conventional cultivation systems in China and India also support a reliable supply of green powder for price-sensitive buyers. This leaves green spirulina as the base product that carries much of the spirulina market by tonnage.

Blue Spirulina is forecast to grow at a 7.39% CAGR through 2031, making it the fastest-growing color segment. The spirulina market is giving more attention to blue formats because food makers still have few scalable natural alternatives to synthetic blue pigments. The 2026 Food and Drug Administration order expanding spirulina extract use supports long-term formulation planning for phycocyanin-based color systems. This matters because the spirulina market can capture more value where customers need stable, application-ready color solutions instead of raw biomass. As a result, blue spirulina is becoming more important to margin growth than to absolute volume.

By Application: Food and Beverages Leads; Dietary Supplements Accelerates

Food and Beverages accounted for 37.65% share of the spirulina market size in 2025, which makes it the largest application segment. The spirulina market benefits here from two roles at once, protein enrichment and natural color provision, especially in drinks, dairy alternatives, confectionery, and functional food products. Food and Drug Administration approvals expanded step by step from narrower uses to beverages and then to broader food use, which gave the application a clearer route for commercial development. This regulatory sequence has helped the spirulina market move from niche use toward wider food reformulation planning. It also supports demand for suppliers that can deliver both nutrition and color performance in one ingredient family.

Dietary supplements are projected to expand at a 7.54% CAGR through 2031, making it the fastest-growing application segment. The spirulina market is seeing sustained supplement demand because consumers increasingly connect preventive health, plant-based diets, and daily protein intake with multifunctional ingredients. This demand pattern fits spirulina well because the ingredient can be positioned around protein density, micronutrient content, and antioxidant support at the same time. It also favors branded and certified products, where trust matters more than in lower-touch bulk channels.

By Production Technology: Open-Pond Dominates Volume; Photobioreactors Capture Specification Premium

Open-Pond Cultivation held an 85.98% share in 2025, confirming that it remains the dominant production method by volume. The spirulina market still relies on open ponds because they offer lower capital intensity, larger cultivation footprints, and practical use of non-arable saline land. This production logic suits bulk ingredient demand across food, feed, and entry-level supplement channels. It also explains why open ponds remain the foundation of high-volume Asia-Pacific supply in the spirulina market. The method is efficient for scale, but it becomes less attractive when buyers need very tight contaminant and batch controls.

Closed-Pond/Photobioreactor systems are forecast to grow at a 9.47% CAGR through 2031, the fastest rate among production technologies. The spirulina market is giving these systems more space because premium buyers in colorants, pharmaceuticals, and cosmetics value cleaner cultivation and stronger batch consistency. A 2025 study on nested-bottled photobioreactor systems reported better CO2 dissolution, improved light distribution, and lower energy use than conventional approaches, improving the economic case for closed systems[3]. This matters because the spirulina market is moving toward applications where contamination control can justify higher prices. As more premium demand shifts to specification-led ingredients, closed systems become more commercially relevant.

Geography Analysis

North America held 38.59% of the spirulina market share in 2025, making it the largest regional segment. The spirulina market in North America is supported by strong supplement demand, active food reformulation around natural colorants, and the presence of established producers such as Cyanotech and DIC’s Earthrise Nutritionals. The Food and Drug Administration’s February 2026 order expanding spirulina extract use has strengthened the region’s long-term commercial case for bakery, dairy, confectionery, and snack applications, even though the effective date remains under procedural review. Organic and premium-grade demand is also stronger here because the United States Department of Agriculture organic rules and retail expectations make certification an important gatekeeper for natural product channels. Cyanotech’s FY2025 results showed nearly 20% revenue growth and a direct-to-consumer mix of 30% of revenue, which signals the willingness of buyers in this region to pay for branded and higher-margin spirulina products.

Asia-Pacific spirulina market size is projected to expand at a 9.33% CAGR through 2031, making it the fastest-growing region. The spirulina market in Asia-Pacific benefits from China’s cost-efficient production infrastructure, India’s export-oriented nutraceutical base, and expanding domestic supplement demand across major Asian economies. DIC LifeTech’s long commercial history in Japan and its broad certification base show how the region supports both mature premium demand and supply capability Japan’s Functional Food Claims environment and its median age of 49 years in 2024 also support routine supplement use, which keeps the regional demand mix favorable for spirulina. EID Parry’s annual report also shows that Parry Nutraceuticals serves more than 40 export markets, reinforcing India’s role as a certified production node within the spirulina market.

Europe remains another quality-led destination within the spirulina market, especially across Germany, France, the United Kingdom, and Benelux. The region’s health-claim framework under Regulation (EC) No 1924/2006 and its organic rules under Regulation (EU) 2018/848 create a structured, but demanding, route for compliant commercialization. South America remains smaller in the spirulina market, but it offers diversification potential on the supply side and early room for branded product expansion. The user-supplied draft highlighted Chile as an emerging point of alternative production, which matters because buyers increasingly want more than one supply geography. The Middle East and Africa also remain smaller today, but the spirulina market is gaining relevance there through aquafeed demand and interest in nutrition-linked use cases. These regions do not yet match the scale of North America, Europe, or Asia-Pacific, but they add strategic optionality to the global footprint.

Competitive Landscape

The spirulina market is moderately fragmented, with a visible split between Asia-Pacific volume producers and a smaller set of integrated suppliers competing on quality, certification, and application know-how. DIC Corporation, Cyanotech Corporation, and EID Parry’s Parry Nutraceuticals form the most visible premium-oriented group in the user-supplied draft, supported by cultivation scale, compliance depth, and downstream commercial reach. The spirulina market remains open enough for many regional suppliers to compete, but the premium tier is harder to access because certifications and process controls require sustained investment. This leaves price-led competition concentrated in bulk powder, while value-led competition is stronger in supplements, refined colorants, and tighter specification ingredients. The result is a spirulina market where scale still matters, but where compliance and application fit increasingly shape profit.

DIC Corporation’s March-April 2025 start of operations at its smart-farming facility in California is one of the clearest strategic moves in the spirulina market. The USD 8 million project added AI-based algae assessment, Supervisory Control and Data Acquisition (SCADA) controls, drone monitoring, a zero-discharge water system, and a purified CO2 supply arrangement, which lifted both efficiency and quality credibility. Cyanotech’s FY2025 results showed nearly 20% revenue growth and a larger direct-to-consumer mix, which indicates a deliberate strategy toward better-margin channels inside the spirulina market. Zhejiang Binmei Biotechnology’s 9 national patents in phycocyanin purification show another strategic path, where intellectual property and processing depth create stronger protection in blue spirulina applications. These moves show that leading companies in the spirulina market are no longer competing only on cultivation volume.

A second pattern in the spirulina market is the growing commercial value of certification breadth and export readiness. EID Parry’s annual report shows that Parry Nutraceuticals serves more than 40 export markets, which reflects the importance of regulatory and customer documentation in winning international business. DIC LifeTech’s use of Food and Drug Adminstartion Generally Recoghnized as Safe (FDA GRAS), Non-GMO (Genetically Modified Organism), HALAL, and KOSHER credentials across more than 30 countries points to the same strategic priority.This means the spirulina market is still accessible to many growers, but a smaller group holds the advantage where customers require premium, traceable, and application-ready supply. That gap is likely to remain a central feature of the spirulina market during the forecast period.

Spirulina Powder Industry Leaders

DIC Corporation

Cyanotech Corporation

E.I.D. Parry India Ltd

Sensient Technologies Corporation

Far East Bio-Tec Co., Ltd. (FEBICO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AlgaeCore Technologies commercialized spirulina-based seafood alternatives under its Simplii Texture line, strengthening its portfolio in alternative seafood products. The company also secured USD 19 million in funding, along with an additional USD 4 million from the Israel Innovation Authority, to support its commercial and innovation activities.

- April 2025: DIC Corporation's United States subsidiary Earthrise Nutritionals commenced operations at a new smart-farming spirulina cultivation facility in California, with an approximately USD 8 million investment, 420,000 m² total area, annual production capacity of 550 tonnes, integrating AI-driven algae growth assessment, SCADA controls, drone-based monitoring, a zero-discharge water system, and a purified CO2 supply agreement with LINDE for sustainable cultivation of spirulina and LINABLUE phycocyanin.

- December 2024: Far East Bio-Tec Co., Ltd. FEBICO approved a private placement plan and entered a strategic partnership with Shiny Brands Group Co., Ltd. to advance commercial application of microalgae exosomes, representing a new R&D-driven growth vector beyond FEBICO's established organic spirulina and chlorella product lines.

Global Spirulina Powder Market Report Scope

The spirulina powder market is segmented by grade, color, application, production technology, and geography. By grade, the market includes conventional and organic. By color, the market includes green spirulina and blue spirulina. By application, the market includes food and beverages, pharmaceuticals, personal care and cosmetics, animal and aquaculture feed, and others. By production technology, the market includes open-pond cultivation and closed-pond/photobioreactor. By geography, the market includes North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Conventional |

| Organic |

| Green Spirulina |

| Blue Spirulina |

| Food and Beverages |

| Dietary Supplements |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Animal and Aquaculture Feed |

| Others |

| Open-Pond Cultivation |

| Closed-Pond/Photobioreactor |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| Grade | Conventional | |

| Organic | ||

| Color | Green Spirulina | |

| Blue Spirulina | ||

| By Application | Food and Beverages | |

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Animal and Aquaculture Feed | ||

| Others | ||

| Production Technology | Open-Pond Cultivation | |

| Closed-Pond/Photobioreactor | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the spirulina market in 2026 and what is its expected value by 2031?

The spirulina market size is USD 710.2 million in 2025 and is projected to hit USD 987.5 million by 2031 on a 6.81% CAGR.

Which region leads global demand for spirulina products?

North America led with a 38.59% share in 2025, helped by supplement demand, natural colorant reformulation, and a strong base of premium producers.

Why is Blue Spirulina expanding faster than Green Spirulina?

Blue Spirulina is growing faster because phycocyanin remains one of the few scalable natural blue color options, and the 2026 FDA expansion widened long-term food application potential.

What is the main risk for suppliers and buyers?

Contamination control in open-pond cultivation remains the main risk because heavy metals, cyanotoxins, and tighter specifications can raise testing costs and affect sourcing confidence.

Page last updated on: