Immunotherapy Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

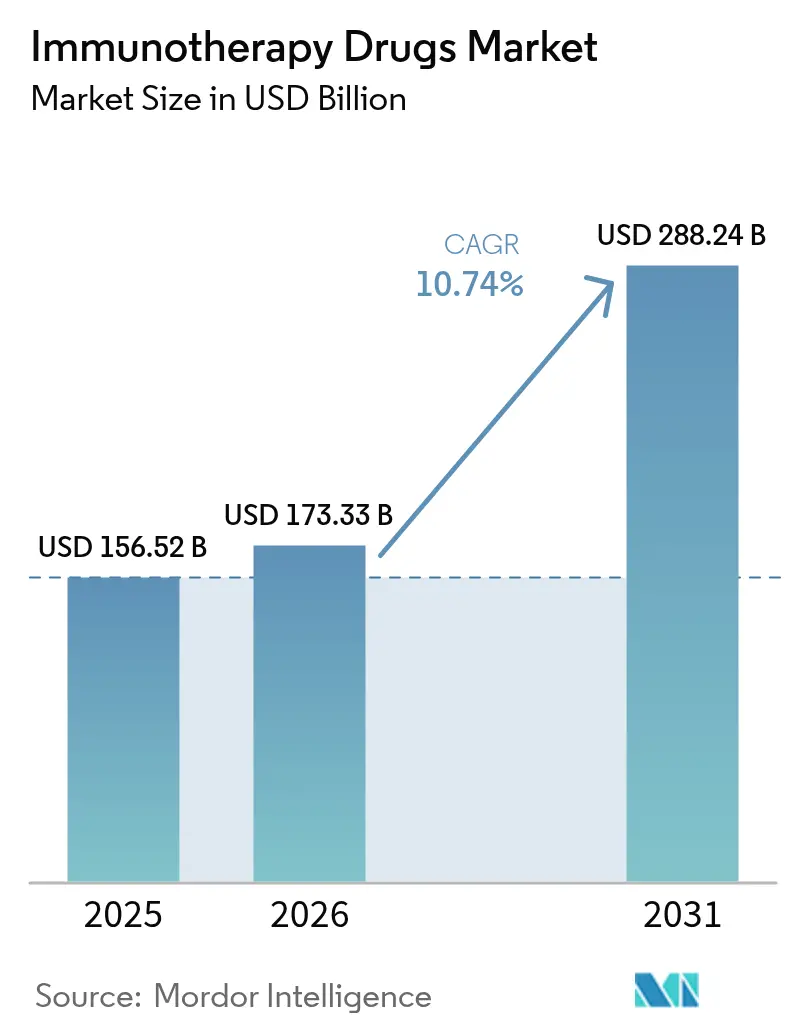

| Market Size (2026) | USD 173.33 Billion |

| Market Size (2031) | USD 288.24 Billion |

| Growth Rate (2026 - 2031) | 10.74% CAGR |

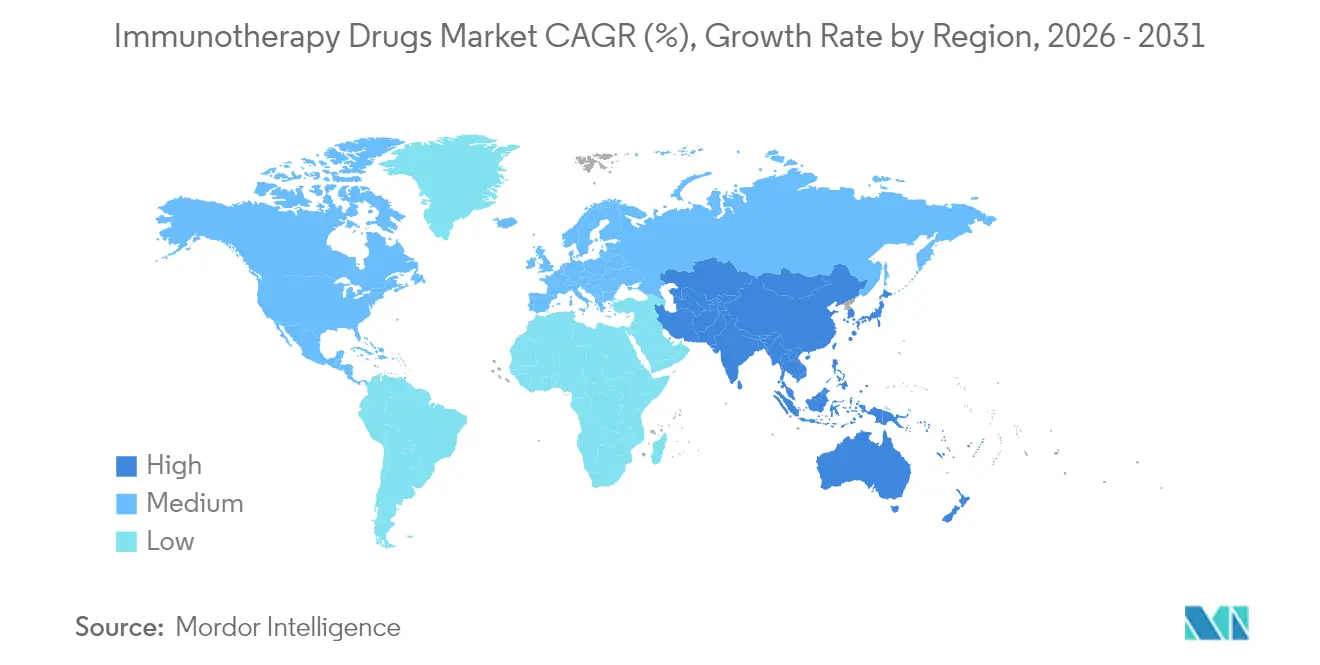

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immunotherapy Drugs Market Analysis by Mordor Intelligence

Global immunotherapy drugs market size in 2026 is estimated at USD 173.33 billion, growing from 2025 value of USD 156.52 billion with 2031 projections showing USD 288.24 billion, growing at 10.74% CAGR over 2026-2031. The surge originates from deeper checkpoint-inhibitor penetration, rapid maturation of T-cell engineering, and the routine use of artificial-intelligence platforms that shorten discovery cycles. Multi-modal regimens that merge monoclonal antibodies with precision biomarkers continue to dominate first-line protocols in solid tumors, while bespoke neoantigen vaccines graduate from early trials into pivotal studies in melanoma and lung cancer. Regulatory agencies simplify combination-therapy reviews, and outcomes-based payment pilots reduce upfront cost exposure for health systems. Manufacturing scale-ups in Asia–Pacific lower per-dose costs, and real-time pharmacovigilance networks improve adverse-event tracking, supporting broader geographic access for complex biologics.

Key Report Takeaways

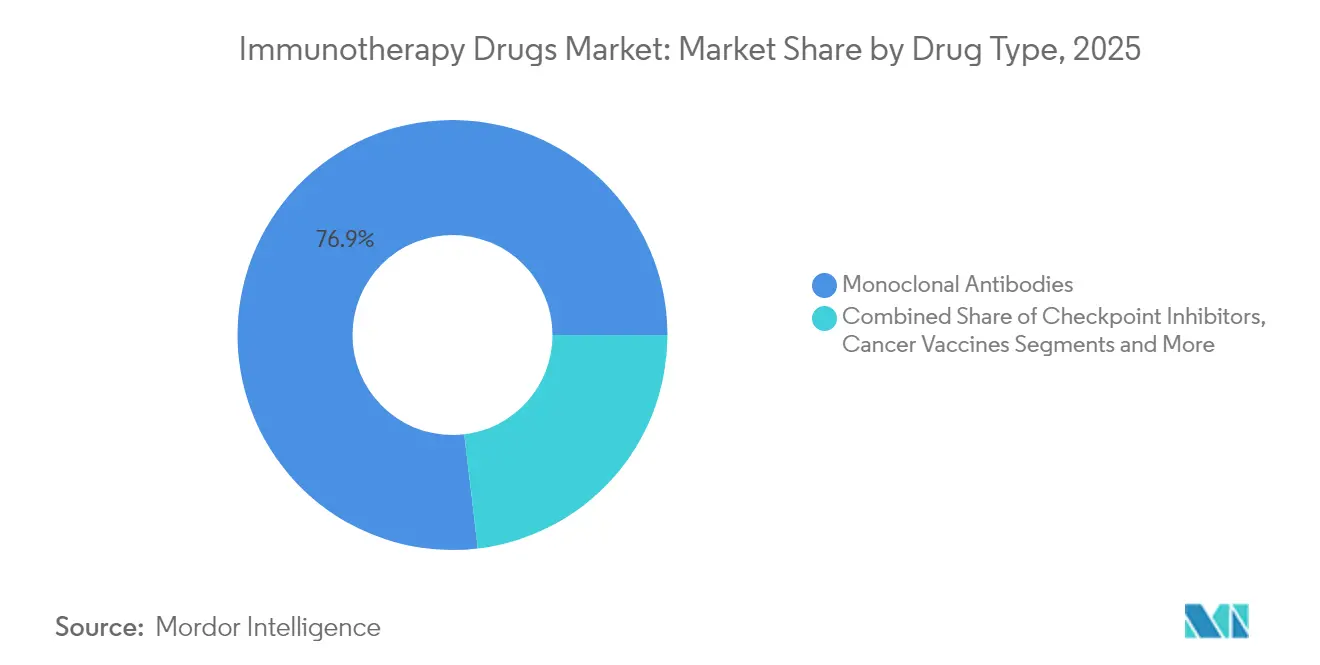

- By drug type, monoclonal antibodies led with 76.88% revenue share in 2025; T-cell therapies are on track to post the highest growth at an 17.62% CAGR through 2031.

- By therapy area, cancer accounted for 92.05% of the immunotherapy drugs market share in 2025, while autoimmune and inflammatory diseases exhibit a 13.74% CAGR to 2031.

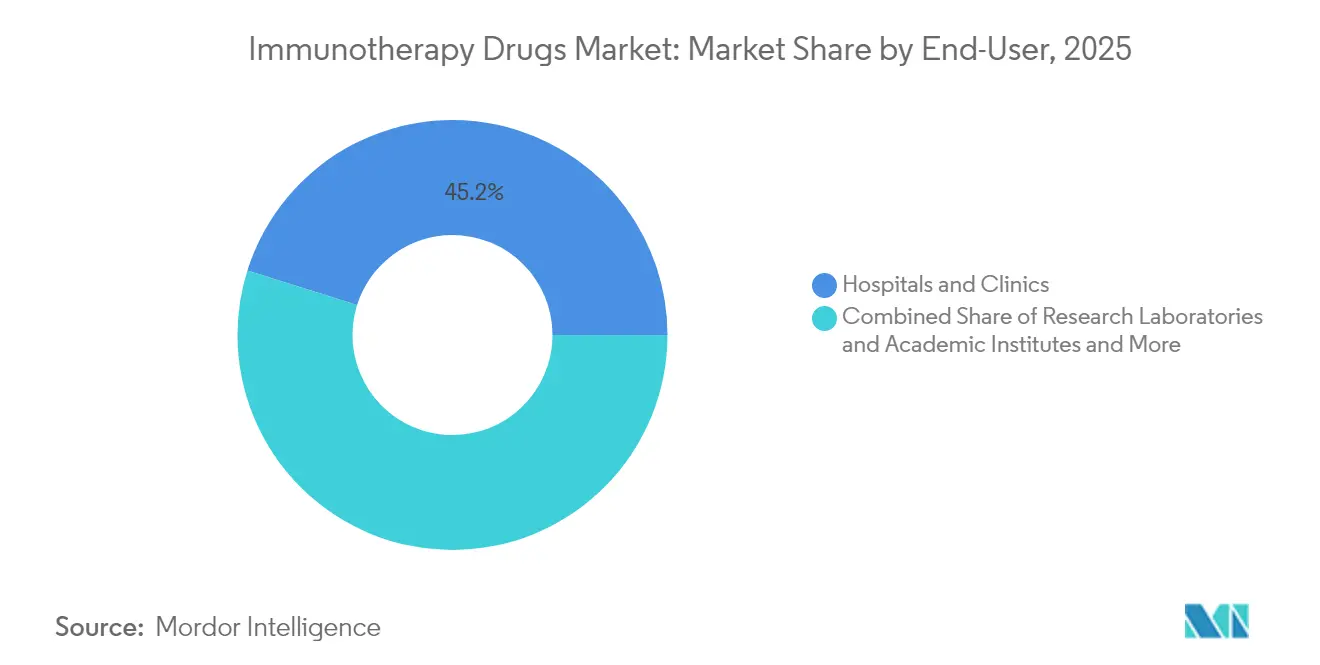

- By end-user, hospitals and clinics controlled 45.15% of 2025 spending, whereas research laboratories show the fastest expansion at a 13.08% CAGR.

- By geography, North America held 48.10% of global sales in 2025; Asia–Pacific is projected to rise at a 13.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Immunotherapy Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Pipeline Of Immune-Checkpoint Inhibitors | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Expanding Dominance Of Monoclonal Antibodies | +1.5% | Global, led by North America, expanding in APAC | Long term (≥ 4 years) |

| Rising Incidence Of Cancer & Chronic Diseases | +1.2% | Global, accelerated in aging populations of developed markets | Long term (≥ 4 years) |

| Biomarker-Driven Precision-Medicine Adoption | +1.0% | North America & EU leading, selective APAC markets | Medium term (2-4 years) |

| Bispecific Antibodies & Adcs Unlocking New Indications | +0.9% | Global, with regulatory leadership in US & EU | Short term (≤ 2 years) |

| AI-Enabled In-Silico Discovery Accelerating R&D | +0.8% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Pipeline of Immune-Checkpoint Inhibitors

Approvals of tislelizumab-jsgr and cosibelimab-ipdl in 2024 confirmed that PD-1, PD-L1, and CTLA-4 programs now pivot toward tumor-agnostic and rare-cancer settings, often as part of doublet or triplet regimens. Late-phase trials involving LAG-3, TIGIT, and TIM-3 candidates signal access to previously resistant populations, while adaptive trial designs shrink development timelines. Combination strategies such as nivolumab + ipilimumab secure higher complete-response rates in melanoma, underlining why regulators continue to grant breakthrough designations for synergistic protocols that deliver clear survival advantages over monotherapies[1]U.S. Food and Drug Administration, “FDA Approvals,” fda.gov.

Expanding Dominance of Monoclonal Antibodies

Iterative engineering upgrades—bispecific, trispecific, and antibody-drug conjugate (ADC) formats—preserve the 77.55% revenue grip held by antibodies. Tec¬listamab delivers a 63% overall response rate in late-line multiple myeloma, and Pfizer’s AI-guided ADC collaboration compresses lead-optimization windows from months to days. CD3-engaging bispecifics redirect T-cell cytotoxicity against solid-tumor antigens that remain out of reach for current CAR-T delivery mechanisms.

Rising Incidence of Cancer & Chronic Diseases

Global prevalence of malignancies rises as populations age, shifting immunotherapy from salvage status to first-line standard. Dostarlimab achieved a 100% complete-response rate in mismatch-repair-deficient rectal cancer, offering organ-preservation alternatives that reduce lifetime cost of care. Parallel breakthroughs in systemic lupus erythematosus and myasthenia gravis validate B-cell depletion via CD19 CAR-T cells, hinting at functional cures that replace decades of immunosuppressive maintenance[3]Jovana Vukovic et al., “CAR-engineered T cell therapy as an emerging strategy for treating autoimmune diseases,” Frontiers in Medicine, frontiersin.org.

Biomarker-Driven Precision-Medicine Adoption

Tumor mutational burden, microsatellite instability, and PD-L1 thresholds increasingly dictate regimen selection, preventing unnecessary toxicity and conserving payer budgets[2]John A. Thompson, “NCCN Guidelines® Insights: Management of Immunotherapy-Related Toxicities, Version 2.2024,” PubMed, pubmed.ncbi.nlm.nih.gov. The UK’s draft rule set for individualized mRNA cancer vaccines formalizes bespoke manufacturing pathways, and circulating-tumor-DNA assays supply near-real-time feedback on therapeutic efficacy, widening precision-medicine uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs & Reimbursement Hurdles | -1.4% | Global, most acute in emerging markets with limited healthcare budgets | Short term (≤ 2 years) |

| Manufacturing Complexity Of Biologics Supply Chains | -1.1% | Global, concentrated in regions with limited biomanufacturing capacity | Medium term (2-4 years) |

| Immune-Related Adverse-Event Management Burden | -0.8% | Global, requiring specialized healthcare infrastructure | Long term (≥ 4 years) |

| Price Erosion From Biosimilar Competition | -0.6% | Developed markets with established biosimilar pathways | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs & Reimbursement Hurdles

CAR-T price tags ranging from USD 373,000 to USD 4.25 million strain payer budgets; in response, CMS proposes a 17% base-payment increase and pilots outcomes-based contracts that refund non-responders. Medicaid’s CGT Access Model ties reimbursement to real-world durability metrics, yet emerging economies still struggle to afford premium biologics despite high unmet needs.

Manufacturing Complexity of Biologics Supply Chains

Contract development and manufacturing organizations average below-50% utilization because process variability in autologous cell lines resists standardization. Global capacity edges up to 17.4 million liters, but single-use bioreactors replace mega-plants to accommodate bespoke product runs. Workforce shortages and quality-assurance bottlenecks delay releases and push companies toward automation and AI-driven predictive maintenance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Living-Cell Platforms Gain Momentum

The immunotherapy drugs market continues to be dominated by monoclonal antibodies, yet T-cell therapies represent the fastest-rising pillar with an 17.62% CAGR through 2031. The immunotherapy drugs market size allocated to T-cell therapies is forecast to expand from USD 15.2 billion in 2025 to USD 40.18 billion by 2031, underscoring their transformative impact on relapsed multiple myeloma and aggressive lymphomas. FDA approvals of idecabtagene vicleucel and ciltacabtagene autoleucel produce minimal-residual-disease negativity rates above 70%, while dual-target CAR constructs broaden tumor-antigen coverage. Checkpoint inhibitors gather steady share via combination approvals, and the pipeline for mRNA cancer vaccines accelerates on the back of breakthrough-therapy designations. Oncolytic viruses such as LOAd703 post 44% response rates when paired with atezolizumab, while IL-15 super-agonists like Anktiva secure approvals for lymphopenic settings, signaling gains for cytokine-based products within the broader immunotherapy drugs market.

Progress in generative chemistry compresses ADC payload discovery, raising potency without parallel toxicity. The immunotherapy drugs market thus transitions from standalone biologics to integrated, multimodal regimens that pair cell therapies with oncolytic platforms and targeted cytokines. Manufacturing automation reduces vein-to-vein time for autologous constructs, suggesting that living products will secure larger slices of future immunotherapy drugs market share once cost curves decline.

By Therapy Area: Autoimmunity Shapes the Next Growth Horizon

Cancer retains 92.05% of 2025 revenues, but autoimmune diseases deliver a 13.74% CAGR, outpacing oncology’s high yet stabilizing growth. The immunotherapy drugs market size devoted to autoimmune indications is expected to rise from USD 5.8 billion in 2025 to USD 12.58 billion in 2031, reflecting durable remissions seen in systemic lupus erythematosus after CD19 CAR-T administration. Over 85 candidates target B-cell reset mechanisms, and programs for multiple sclerosis and rheumatoid arthritis implement both autologous and allogeneic platforms to counter cost and scalability concerns. Infectious-disease immunotherapy edges beyond HIV prophylaxis as bifunctional antibodies clear drug-resistant pathogens, opening ancillary revenue lines inside the wider immunotherapy drugs market.

Regulators now accept surrogate endpoints such as B-cell aplasia for accelerated autoimmune approvals, cutting development risk and inviting venture financing. European and Chinese authorities align on data-package requirements, enabling global launch sequences. With health systems quantifying the long-term savings from curative autoimmune interventions, payer resistance fades and access widens, further stimulating the immunotherapy drugs market.

By End-User: Academic-Industry Synergy Deepens

Hospitals and clinics capture 45.15% of spending given their role as treatment hubs, yet research laboratories grow fastest at 13.08% CAGR as complex discovery workflows merge wet-lab experimentation with cloud-based AI analytics. The immunotherapy drugs market benefits when academic centers like Memorial Sloan Kettering co-create AI-designed antibodies; such alliances turn early-stage ideas into de-risked clinical assets that rapidly move into large hospital systems for commercial rollout. Government grants—such as the USD 3.27 million National Cancer Institute award for a pancreatic vaccine—further underwrite translational infrastructure.

Community hospitals invest in specialized infusion suites, but autologous manufacturing still concentrates in academic medical centers capable of real-time cell-handling and gene-editing oversight. Meanwhile, decentralized cell-therapy suites linked by digital quality-control platforms promise to democratize access, opening fresh revenue channels and broadening geographic penetration for the immunotherapy drugs market.

Geography Analysis

North America keeps a 48.10% revenue stake through 2025, anchored by a mature reimbursement framework, dense innovation clusters, and early adoption of outcomes-based contracting. The region’s biopharma incumbents acquire AI start-ups and manufacturing specialists, consolidating platform control while reducing batch-failure rates. Strategic onshoring incentives lower supply-chain exposure to geopolitical shocks, strengthening long-term competitiveness for the regional immunotherapy drugs market.

Asia–Pacific records a 13.79% CAGR, the fastest worldwide, powered by regulatory harmonization, lower labor costs, and government-backed capacity expansions. China’s approval of Stapokibart, the first domestic IL-4Rα antagonist, reflects higher local regulatory sophistication and shortens launch lags versus Western benchmarks. Japan and South Korea refine conditional early-approval pathways, and India’s biomanufacturing corridors lure Western sponsors seeking cost-effective production slots, collectively lifting regional share in the global immunotherapy drugs market.

Europe demonstrates steady mid-single-digit growth under the Advanced Therapy Medicinal Products regulation that standardizes cell- and gene-therapy review. Biosimilar competition tempers monoclonal-antibody pricing but widens access, keeping overall market value intact. Targeted digital-health initiatives link registries with pharmacovigilance portals, streamlining post-approval monitoring and reinforcing public confidence in immunotherapy safety profiles.

The Middle East and Africa gain momentum from flagship projects such as Saudi Arabia’s Cancer BioShield platform, which delivers immune-restorative regimens tailored to local genetic backgrounds. Multinational partnerships with regional sovereign funds finance precision oncology centers that function as hubs for nearby emerging markets. Latin America focuses on licensing ready-to-fill formulations and implementing risk-sharing reimbursement, gradually lifting therapy uptake in high-burden cancers like gastric carcinoma. Together, these advancements broaden the global footprint of the immunotherapy drugs market and reduce dependency on a handful of mature territories.

Competitive Landscape

Moderate consolidation characterizes the immunotherapy drugs market as Big Pharma acquires niche platform specialists while venture-financed start-ups challenge incumbents with disruptive modalities. Pfizer’s ADC pact with PostEra exemplifies a vertical-integration push combining AI design, clinical execution, and in-house manufacturing to compress cycle times. Novartis’ USD 1 billion AI-protein alliance underscores the premiums paid for computational lead-generation engines that slash attrition.

Private-equity funds enter cell-therapy contract manufacturing, betting that capacity scarcity will drive premium margins until standardization takes root. Meanwhile, the Alliance for Regenerative Medicine highlights in-vivo CAR-T editing and non-double-strand-break gene cutters as nascent technologies likely to reshape competitive hierarchies. Intellectual-property bundles now couple biologics with digital companions—patient-monitoring apps and AI image-analysis tools—that together form value-based contracting ecosystems.

Regional champions arise in China and South Korea, often spinning out of state-backed research institutes with advantaged access to local trials and fast-track approvals. Western firms respond by co-locating R&D units in Asia–Pacific to gain proximity to high-growth pools, thereby reinforcing innovation clusters and feeding competitive intensity inside the worldwide immunotherapy drugs market.

Immunotherapy Drugs Industry Leaders

Amgen Inc.

Novartis AG

AbbVie Inc.

F. Hoffmann-La Roche AG

GSK PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Scripps Research Institute dosed the first patient in a phase 1 study of CLBR001 + ABBV-461, a switchable CAR-T for advanced breast cancer.

- April 2025: Lyell Immunopharma secured FDA RMAT status for LYL314, a dual-target CD19/CD20 CAR-T that posted a 94% overall response rate in relapsed large B-cell lymphoma.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the immunotherapy drugs market as the worldwide sales revenue generated by approved pharmaceutical products that modulate a patient's immune response, principally monoclonal antibodies, checkpoint inhibitors, cytokines, oncolytic viruses, cancer vaccines, and adoptive cell therapies, administered for oncology as well as select autoimmune, inflammatory, and infectious conditions.

Pipeline molecules not yet approved, generalized immunomodulators used only for organ-transplant rejection, and pure allergy desensitization shots are excluded to keep the focus on labeled, revenue-earning therapeutics.

Segmentation Overview

- By Drug Type

- Monoclonal Antibodies

- Checkpoint Inhibitors

- Cancer Vaccines

- Interferons Alpha/Beta

- Interleukins

- Oncolytic Viral Therapies

- T-Cell Therapies (CAR-T, TCR, TIL)

- Cytokines & Immunomodulators

- Other Drug Types

- By Therapy Area

- Cancer

- Autoimmune & Inflammatory Diseases

- Infectious Diseases

- Other Therapy Areas

- By End-User

- Hospitals & Clinics

- Research Laboratories & Academic Institutes

- Pharmaceutical & Biotechnology Companies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold structured interviews and short surveys with hospital pharmacists, medical oncologists, autoimmune specialists, and payor advisors across North America, Europe, Asia-Pacific, and Latin America.

These conversations clarify real-world usage patterns, typical course pricing, access hurdles, and upcoming label expansions, which we fold back into desk findings for stronger confidence.

Desk Research

We start by collating publicly available, high-credibility datasets such as WHO Global Health Observatory incidence files, GLOBOCAN cancer registry counts, FDA Drugs@FDA approval timelines, EMA Community Register safety notices, and national procurement lists. Company 10-Ks, investor decks, and quarterly sales transcripts add brand-level revenue color, which is then validated through Dow Jones Factiva feeds that track pricing and reimbursement shifts across regions. Trade bodies like PhRMA, the European Federation of Pharmaceutical Industries, and the International Agency for Research on Cancer supply supplementary statistics. This list is illustrative; many additional open and subscription resources inform our evidence base.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-patient build, anchored to disease incidence and therapy penetration ratios, establishes market revenue.

Select bottom-up checks, sampled average selling price times manufacturer-reported shipment volumes, help us fine-tune totals where reimbursement caps or parallel trade shift effective revenues.

Key model drivers include new drug approvals per year, median therapy duration, pricing revisions in major formularies, biologic biosimilar uptake, and regional healthcare budget growth.

Multivariate regression, run on a rolling window, projects each driver and feeds an exponential smoothing overlay to capture sudden guideline changes. Before results are aligned with expert consensus.

Gap handling uses nearest-neighbor interpolation for smaller geographies with sparse data.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review, variance checks against quarterly sales flashes, and an outlier alert that triggers re-contacts when deviations exceed five percent.

Reports refresh annually, and we push interim updates after material regulatory or safety events to ensure clients receive the latest calibrated view.

Why Mordor's Immunotherapy Drugs Baseline Stands Reliable

Published estimates often diverge because firms pick different therapy baskets, fold in pipeline valuations, or apply list prices without discounts.

Key gap drivers include varying inclusion of allergy immunotherapy, double counting combination regimens, divergent currency conversion cut-offs, and refresh cadences that lag recent biosimilar launches.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 156.52 B (2025) | Mordor Intelligence | |

| USD 257.6 B (2024) | Global Consultancy A | Includes broad immunology biologics and hospital mark-ups beyond drug revenue |

| USD 285.3 B (2024) | Industry Association B | Applies list prices, counts pipeline milestones, and blends oncology with chronic autoimmune therapies |

In summary, our disciplined scope, transparent variable selection, and timely refresh give decision-makers a dependable baseline that is traceable to real treatment volumes and defendable pricing assumptions, minimizing surprises when strategies move from slide decks to operating budgets.

Key Questions Answered in the Report

What is the current size and growth rate of the immunotherapy drugs market?

Global revenues reach USD 173.33 billion in 2026 and are projected to advance at a 10.74% CAGR to USD 288.24 billion by 2031.

Which drug class contributes the largest share of immunotherapy sales?

Monoclonal antibodies hold 76.88% of 2025 revenues, driven by bispecific, trispecific, and antibody-drug-conjugate upgrades.

Where is the fastest regional growth expected?

Asia–Pacific shows a 13.79% CAGR through 2031, supported by regulatory harmonization and expanding biomanufacturing capacity.

What therapy areas are gaining momentum beyond oncology?

Autoimmune and inflammatory diseases post a 13.74% CAGR, fueled by CD19 CAR-T successes in systemic lupus erythematosus and multiple sclerosis.

How are high treatment costs being addressed?

Outcomes-based payment models such as the CMS CGT Access Model link reimbursement to real-world durability metrics, easing payer burden on therapies priced between USD 373,000 and USD 4.25 million per patient.

Which end-user segment is expanding fastest?

Research laboratories grow at a 13.08% CAGR as academic-industry alliances deploy artificial-intelligence discovery platforms and accelerate translational studies.

Page last updated on: