Immunosuppressant Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

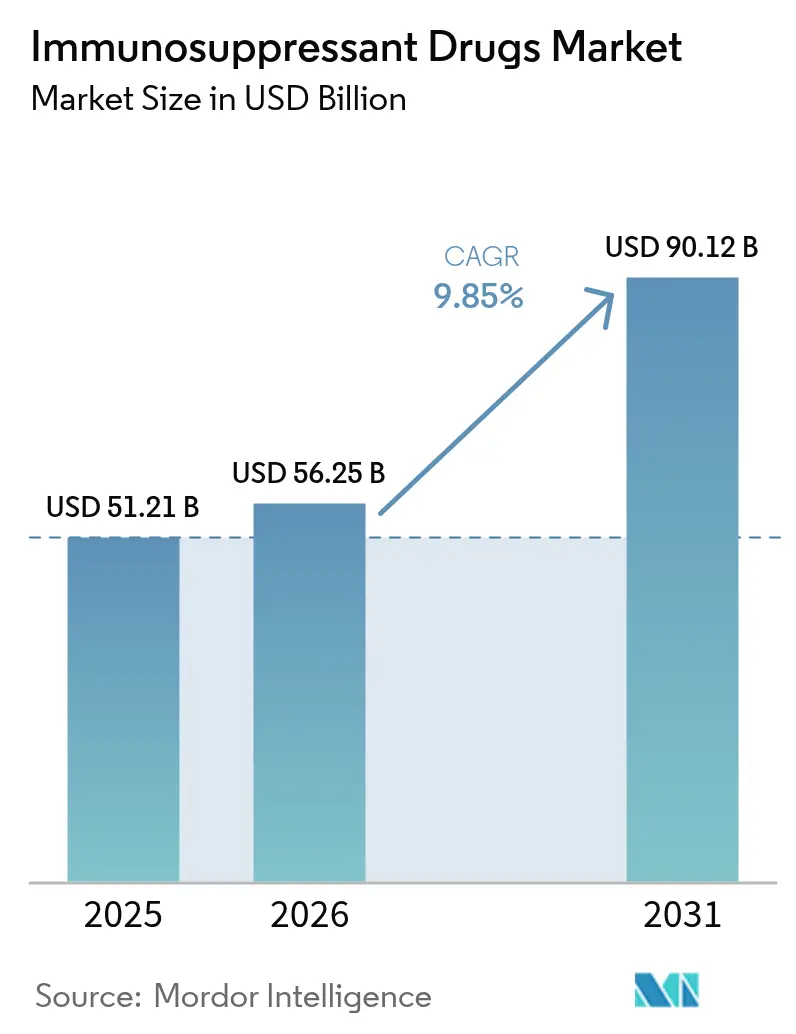

| Market Size (2026) | USD 56.25 Billion |

| Market Size (2031) | USD 90.12 Billion |

| Growth Rate (2026 - 2031) | 9.85% CAGR |

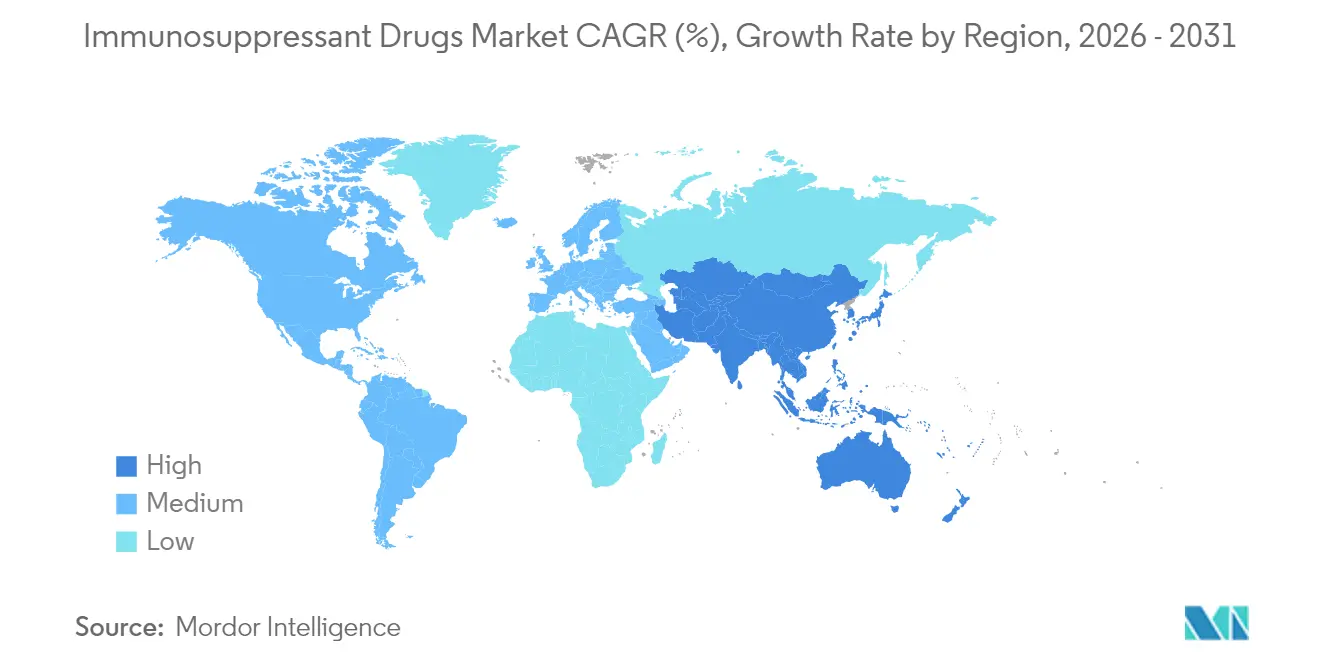

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Immunosuppressant Drugs Market Analysis by Mordor Intelligence

The Immunosuppressant Drugs Market size was valued at USD 51.21 billion in 2025 and estimated to grow from USD 56.25 billion in 2026 to reach USD 90.12 billion by 2031, at a CAGR of 9.85% during the forecast period (2026-2031).

Rising autoimmune-disease incidence, record organ-transplant volumes, rapid uptake of next-generation biologics, and Medicare inflation-rebate reforms combine to pull demand upward [1]U.S. Centers for Medicare & Medicaid Services, “Medicare Drug Inflation Rebate Program Fact Sheet,” cms.gov . Additional momentum comes from wider off-label dermatology use of JAK inhibitors and biologics, biosimilar penetration that broadens patient access, and artificial-intelligence platforms that individualize dosing patterns. Commercial strategies now extend far beyond traditional transplant centers, with direct-to-patient digital distribution driving a structural shift in pharmacy channels. Against this backdrop, the immunosuppressant drugs market faces simultaneous threats from cell- and gene-therapy substitutes and from stringent multi-regional regulatory surveillance, keeping competitive stakes high.

Key Report Takeaways

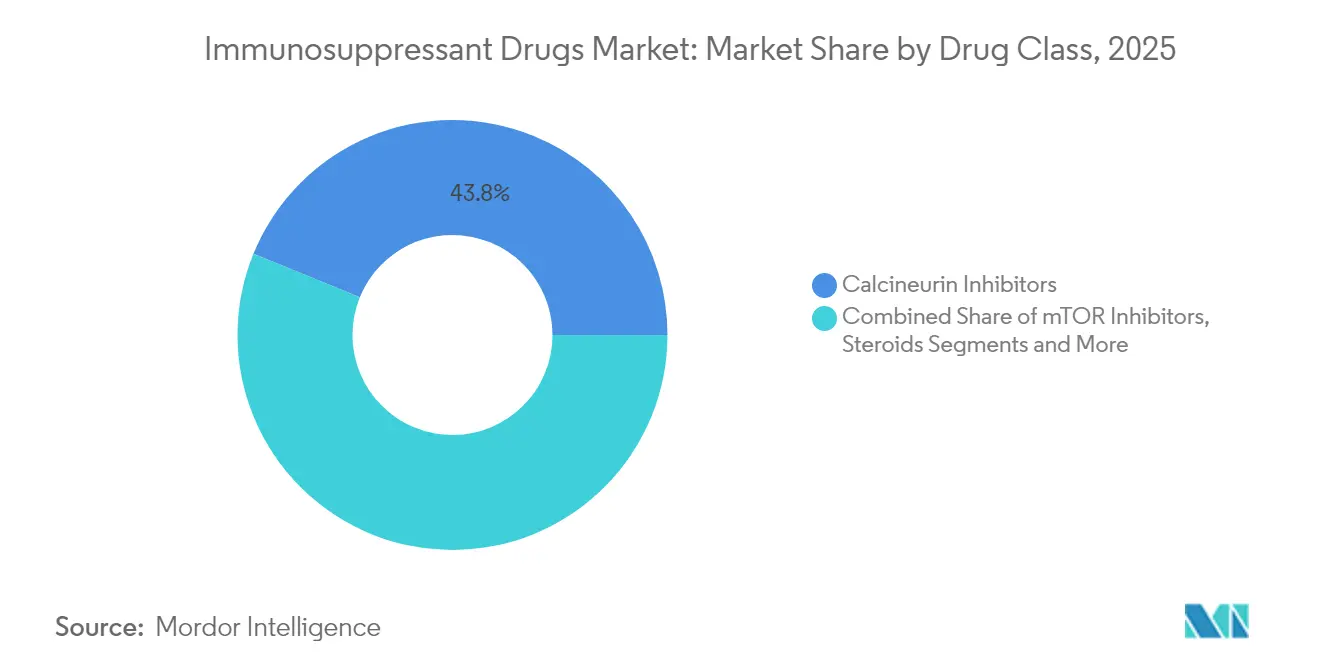

- By drug class, Calcineurin inhibitors held 43.83% immunosuppressant drugs market share in 2025; mTOR inhibitors post the fastest 10.52% CAGR to 2031.

- By application, Autoimmune diseases captured 55.35% of the immunosuppressant drugs market size in 2025, while organ-transplant therapy expands at a 10.55% CAGR through 2031.

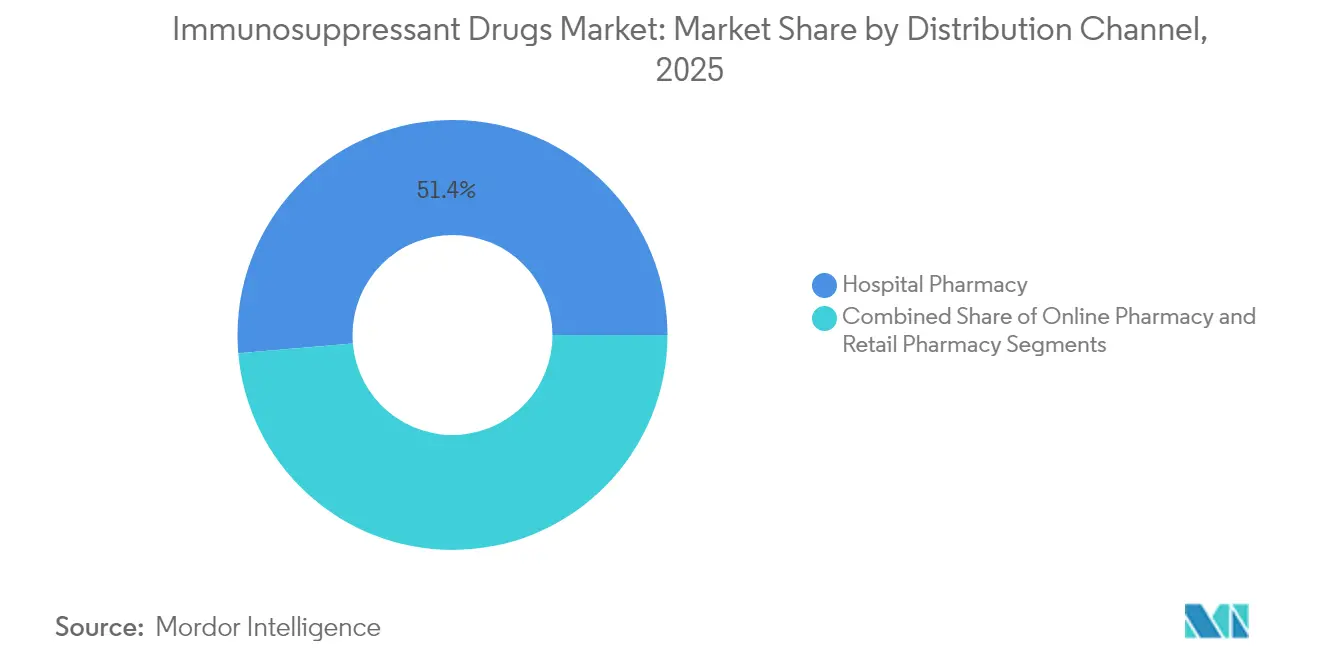

- By distribution channel, Hospital pharmacies accounted for 51.35% revenue share in 2025; online pharmacies advance at a 10.6% CAGR to 2031.

- By geography, North America commanded 40.42% of the immunosuppressant drugs market in 2025, whereas Asia-Pacific accelerates at a 10.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Immunosuppressant Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Autoimmune Diseases & Organ-Transplant Procedures | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Technological Advances in Tissue Engineering & Transplant Techniques | +2.1% | North America & EU leading, APAC adoption accelerating | Long term (≥ 4 years) |

| Launch Of Next-Gen Biologics & Small-Molecule Formulations | +1.9% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Wider Adoption Of TDM-Driven Personalised Combination Regimens | +1.6% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Gene-Edited Xenotransplantation Breakthroughs | +1.2% | United States leading, regulatory approval pending globally | Long term (≥ 4 years) |

| Off-Label Dermatology Use Surges in EMS | +0.9% | Global, with highest penetration in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Autoimmune Diseases & Organ-Transplant Procedures

Autoimmune-disease recognition intensifies as advanced diagnostics uncover previously undetected patient pools requiring long-term pharmacologic suppression. The United States performed more than 48,000 organ transplants in 2024, a 3.3% rise over 2023, setting a new demand baseline for lifelong maintenance therapy [2] Health Resources and Services Administration, "Organ transplants exceeded 48,000 in 2024; a 3.3 percent increase from the transplants performed in 2023," optn.transplant.hrsa.gov. Enhanced organ-preservation technologies and expanded donor criteria raise procedure volumes further, while the OPTN target of 60,000 annual transplants by 2026 underscores sustained need for immunosuppressants. Aging demographics in developed economies add complexity to care plans, enlarging per-patient dosing and boosting aggregate spending. Collectively, these forces anchor the upward trajectory of the immunosuppressant drugs market.

Technological Advances in Tissue Engineering & Transplant Techniques

Gene-edited pig organs progress from proof-of-concept to early clinical evaluation, signaling a paradigm shift that could alleviate donor-organ scarcity and redefine immunologic protocols. FDA frameworks now detail expectations for xenograft submissions, positioning the United States at the forefront of next-generation transplant medicine. Concurrently, tissue-engineering innovations—such as biocompatible scaffolds and 3-D bioprinted constructs—lower immunogenicity, prompting novel immunosuppression regimens that blend biologics with nanoparticle-based delivery. Pharmaceutical companies that align R&D pipelines with these changes strengthen defensibility in an expanding immunosuppressant drugs market.

Launch of Next-Generation Biologics & Small-Molecule Formulations

Regulators continue to approve targeted agents that deliver superior efficacy-safety profiles. The 2024 authorization of axatilimab-csfr for chronic graft-versus-host disease exemplifies the trend toward mechanism-based innovation. JAK inhibitors—abrocitinib and upadacitinib—solidify positions beyond rheumatology, gaining dermatologist favor for atopic dermatitis and psoriasis. Small-molecule programs focus on improving bioavailability and mitigating metabolic liabilities, providing alternatives to calcineurin-cum-corticosteroid staples [3]U.S. Food and Drug Administration, “Workshop on In-Utero Exposure to Immunosuppressive Drugs,” fda.gov . M&A activity, including Sanofi’s USD 1.9 billion acquisition of Dren Bio’s DR-0201 asset, highlights industry commitment to replenishing portfolios that can compete effectively in the immunosuppressant drugs market.

Wider Adoption of TDM-Driven Personalized Combination Regimens

Integration of therapeutic drug monitoring (TDM) with artificial-intelligence eng ines moves dosing decisions from empirical averages to precision algorithms. Model-informed precision dosing frameworks already refine tacrolimus management, accounting for CYP3A5 polymorphisms that alter metabolism. FDA’s 2024 M15 guidance on model-informed development accelerates incorporation of AI-enhanced tools into regulatory submissions, reinforcing commercial viability. Home-based self-monitoring kits and cloud-linked apps reduce clinic visits, boosting adherence and freeing capacity in transplant centers. Vendors that embed digital health platforms into core products deepen switching costs and extend reach in the immunosuppressant drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Regional Regulatory & PV Hurdles | -1.4% | Global, with highest impact in EU & Japan | Medium term (2-4 years) |

| High Therapy Cost & Patchy Reimbursement | -1.1% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Curative Cell- & Gene-Therapy Substitutes | -0.8% | North America & EU leading, limited APAC penetration | Long term (≥ 4 years) |

| Rising AMR Burden Complicating Immunosuppression | -0.6% | Global, with highest burden in hospital settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Regional Regulatory & Pharmacovigilance Hurdles

Regulatory divergence forces companies to navigate disparate approval timelines, safety requirements, and real-world-evidence obligations. FDA scrutiny now extends to in-utero exposure studies, lengthening clinical programs and escalating costs. Although trans-Atlantic harmonization efforts improve alignment, region-specific pharmacovigilance still mandates custom infrastructures, tilting competitive advantage toward incumbents with robust compliance resources. In aggregate, these complexities compress margins and temper expansion across the immunosuppressant drugs market.

High Therapy Cost & Patchy Reimbursement

Global payers intensify cost containment, introducing stricter prior-authorization triggers and inflation-rebate claw-backs. Medicare’s Drug Inflation Rebate Program reduced coinsurance on 64 products effective January 2025, offering relief to more than 853,000 enrollees but squeezing manufacturer pricing latitude. Emerging economies apply sharper formulary discounts, boosting generic uptake yet limiting penetration of cutting-edge biologics. Differential reimbursement landscapes therefore shape go-to-market tactics across the immunosuppressant drugs industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Calcineurin Inhibitors Remain the Anchor While mTOR Catalyzes Future Upside

Calcineurin inhibitors retained 43.83% immunosuppressant drugs market share in 2025 owing to long-standing clinical familiarity and broad guideline endorsement. Yet nephrotoxicity worries open white space for mTOR inhibitors, whose 10.52% CAGR marks the fastest segment growth to 2031. The immunosuppressant drugs market size for mTOR-based protocols is projected to expand at a notably brisk clip, helped by favorable renal-function outcomes among liver and kidney recipients. Tacrolimus and cyclosporine will continue to dominate early-post-transplant dosing, but belatacept and everolimus drive steroid-sparing approaches that appeal to multidisciplinary transplant teams.

Momentum toward precision combinations accelerates as therapeutic-drug-monitoring platforms pair calcineurin inhibitors with low-dose mTOR inhibitors to balance rejection risk and adverse-event profiles. Antiproliferative agents such as mycophenolate mofetil and emerging costimulation blockers round out cocktail regimens, creating high-moat portfolios for innovators that own multiple mechanisms of action. As biosimilar tacrolimus diffusion lowers unit prices, innovators lean on differentiated delivery technologies—nanoparticle encapsulation, once-weekly patches—to protect franchise economics inside the immunosuppressant drugs market.

By Application: Autoimmune Diseases Drive Volume, Transplant Settings Propel Growth

Autoimmune pathologies supplied 55.35% of 2025 volume, yet organ-transplant therapy posts the quickest 10.55% CAGR, revealing divergent demand drivers inside the immunosuppressant drugs market size. Surgeons performed a record 48,000+ U.S. transplants in 2024, and the federal target of 60,000 annual procedures by 2026 extends visibility for drug-consumption expansion. Meanwhile, rheumatology and gastroenterology clinics keep autoimmune scripts on a steady ascent as diagnostics mature.

Off-label dermatology uptake adds an incremental leg to growth, especially across North America and Western Europe where regulatory flexibility and insurance alignment accelerate biologic adoption. Ophthalmology (uveitis) and nephrology (lupus nephritis) deliver steady tailwinds. As curative cell therapies inch closer to commercialization, pharmaceutical companies reposition chronic regimens toward maintenance niches or rare-disease subsets, safeguarding longer-term prospects in the immunosuppressant drugs market.

By Distribution Channel: Digital Pathways Chip Away at Hospital Supremacy

Hospital pharmacies owned 51.35% revenue in 2025, but online channels now rise 10.6% annually, reflecting broader direct-to-patient logistics. Remote prescription verification and cold-chain automation let specialty pharmacies ship biologics nationwide, eroding physical-hospital exclusivity. The immunosuppressant drugs market size tied to e-commerce models is set for sustained growth as Medicare’s 90-day-supply rule raises mail-order appeal.

Retail chains partner with specialty distributors to manage prior-authorization complexities, while integrated physician-pharmacy platforms close adherence gaps via real-time refill nudges. These innovations lower administrative costs and enhance quality-of-life metrics for patients juggling lifelong regimens. Consequently, manufacturers craft channel-agnostic support programs—virtual nurse educators, telehealth titration consults—to stay embedded across the immunosuppressant drugs market.

Geography Analysis

North America maintained 40.42% market share in 2025 grounded in robust transplant ecosystems, comprehensive Medicare coverage, and rapid guideline adoption for novel dosing algorithms. Clinical research networks speed time-to-practice for late-stage products, raising revenue certainty for developers. Canada’s provincial formularies and Mexico’s Seguro Popular upgrades extend reach, yet pricing differentials complicate cross-border procurement strategies, a factor requiring vigilant trade-compliance oversight across the immunosuppressant drugs market.

Asia-Pacific exhibits the most rapid 10.58% CAGR to 2031 as China and India scale transplant capacity and as Japan’s aging demographics swell autoimmune caseloads. Regional agencies craft accelerated review pathways for breakthrough biologics, which improves launch windows relative to historic precedents. Local biosimilar manufacturing cuts acquisition costs, spurring broader usage even in secondary-tier cities. Australia and South Korea lead uptake of AI-enabled TDM platforms, further enriching patient-management frameworks within the immunosuppressant drugs market.

Europe posts steady gains aided by universal coverage and strong pharmacovigilance structures, but health-technology-assessment price caps curb top-line growth for high-ticket entrants. Germany, United Kingdom, and France represent transplant volume leaders, while Southern European nations outpace on autoimmune prescriptions. Regulatory convergence with FDA eases multi-regional filing burdens; however, post-Brexit dual submissions add friction for manufacturers operating pan-European supply chains. Middle East & Africa and South America remain nascent but invest heavily in transplant-center accreditation and generic manufacturing respectively, signaling future relevance to the worldwide immunosuppressant drugs market.

Competitive Landscape

Market concentration is moderate: top multinationals defend share by layering AI-dosing software atop legacy molecules and by progressing differentiated mechanisms through late-stage trials. Novartis banked USD 6.1 billion from Cosentyx and USD 1.6 billion from Xolair in 2024, leveraging these anchors to cross-fund Phase III xenotransplant programs. Astellas reported CNY 203.1 billion in PROGRAF sales, buttressing cash flow for mTOR combination research. Bristol Myers Squibb’s growth collections delivered USD 6.4 billion (+21%), indicating success in pivoting toward biologic niches.

Biosimilar penetration hit 23% volume across the immunosuppressant drugs market; nevertheless, adalimumab copycats stalled at 2% penetration due to incumbent rebate structures that favor originators. White-space competition intensifies in pediatric dosing, AI-guided micro-titration platforms, and xenotransplant-specific regimens. Disruptors include CAR-T developers whose potential curative outcomes challenge chronic immunosuppression economics.

Manufacturers track patent sunsets—most notably for Stelara in 2025—and restructure portfolios to withstand generic erosion while leaning on life-cycle-management tactics such as subcutaneous reformulations and fixed-dose co-formulations, strategies pivotal to retaining relevance in the immunosuppressant drugs market.

Immunosuppressant Drugs Industry Leaders

-

Astellas Pharma, Inc

-

Sanofi (Genzyme)

-

Bristol-Myers Squibb Company

-

Novartis AG

-

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: UNOS confirmed the United States completed 48,000+ organ transplants in 2024, eclipsing prior records and expanding downstream immunosuppressive drug demand.

- December 2024: FDA issued final M15 guidance on model-informed drug development, clarifying expectations for AI-enhanced dosing strategy submissions.

- December 2024: CMS announced coinsurance savings for 64 drugs via the Medicare Prescription Drug Inflation Rebate Program, effective January 2025.

- July 2024: FDA convened a workshop on evaluating immunosuppressive effects of in-utero drug exposure, underscoring heightened reproductive-safety oversight.

Global Immunosuppressant Drugs Market Report Scope

Immunosuppressant drugs inhibit or prevent the activity of the immune system, and they are used to prevent the rejection of a transplanted organ and to treat autoimmune diseases.

The Immunosuppressant Drugs Market is segmented By Drug Class (Calcineurin Inhibitors, Antiproliferative Agents, mTOR Inhibitor, Steroids, and Other Drug Classes), Application (Autoimmune diseases (Systemic Autoimmune Disease, and Localized Autoimmune Disease), Organ transplant, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Calcineurin Inhibitors |

| Antiproliferative Agents |

| mTOR Inhibitors |

| Steroids |

| Other Classes |

| Autoimmune Diseases |

| Organ Transplant |

| Other Applications |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Calcineurin Inhibitors | |

| Antiproliferative Agents | ||

| mTOR Inhibitors | ||

| Steroids | ||

| Other Classes | ||

| By Application | Autoimmune Diseases | |

| Organ Transplant | ||

| Other Applications | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the immunosuppressant drugs market today?

The market generated USD 56.25 billion in 2026 and is projected to climb to USD 90.12 billion by 2031.

Which drug class holds the biggest share?

Calcineurin inhibitors lead with 43.83% market share in 2025, reflecting long-standing clinical reliance.

What is the fastest-growing segment of the immunosuppressant drugs market?

MTOR inhibitors are forecast to advance at a 10.52% CAGR through 2031, outpacing all other drug classes.

Why is Asia-Pacific growing so quickly?

Expanding transplant infrastructure, rising autoimmune prevalence, and expedited biologic approvals support a 10.58% regional CAGR.

How are biosimilars affecting market dynamics?

Biosimilars account for 23% overall volume, pressuring prices but still facing low uptake in certain molecules due to contracting practices favoring originators.

Could cell or gene therapies disrupt the market?

Yes. Curative approaches such as CAR-T therapies for autoimmune disorders could limit long-term need for chronic immunosuppression, posing a strategic threat to incumbent portfolios.

Page last updated on: