Liver Diseases Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

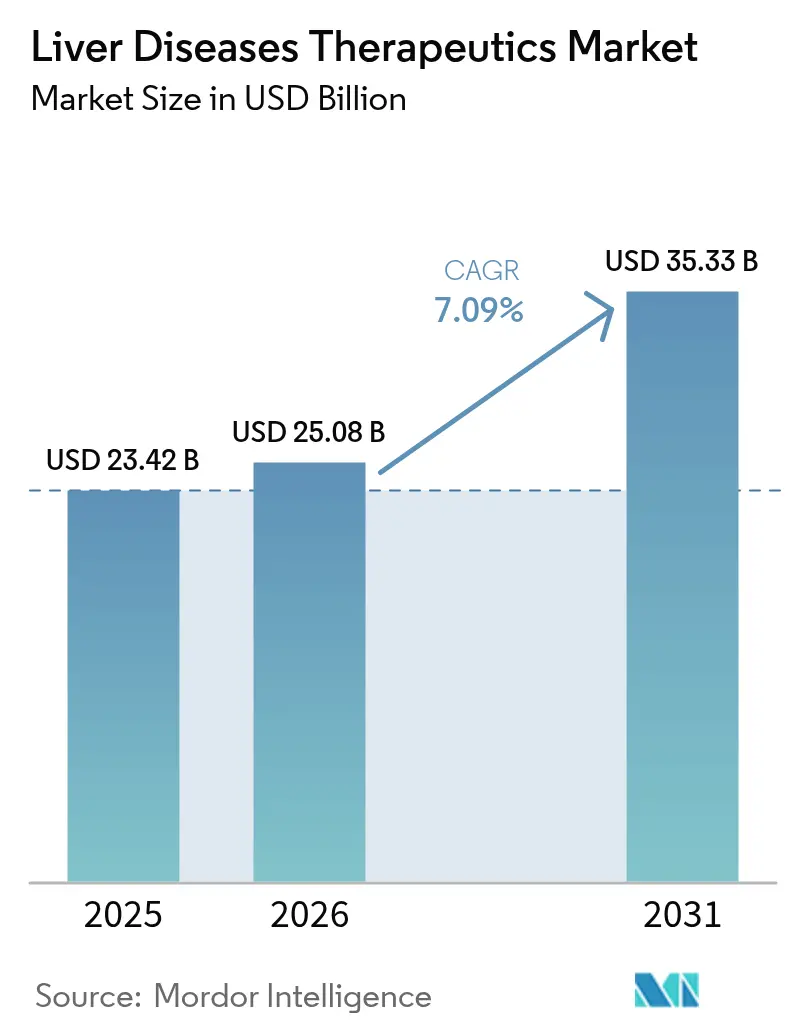

| Market Size (2026) | USD 25.08 Billion |

| Market Size (2031) | USD 35.33 Billion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

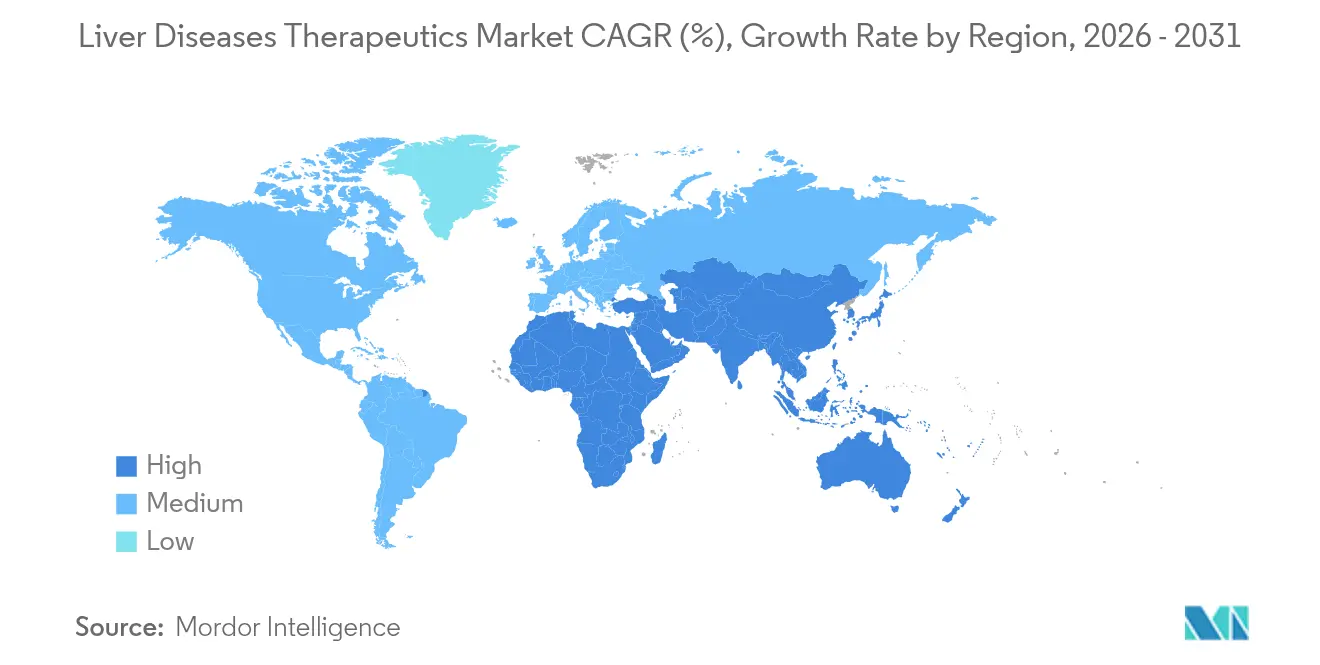

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liver Diseases Therapeutics Market Analysis by Mordor Intelligence

The Liver Diseases Therapeutics Market size is expected to grow from USD 23.42 billion in 2025 to USD 25.08 billion in 2026 and is forecast to reach USD 35.33 billion by 2031 at 7.09% CAGR over 2026-2031.

Robust demand is underpinned by breakthrough regulatory approvals, the rising global prevalence of viral hepatitis and metabolic dysfunction-associated steatotic liver disease (MASLD), and technological leaps in RNA-based delivery platforms. Manufacturers prioritise precision medicine, integrating companion diagnostics that stratify patients by viral genotype, fibrosis stage, or metabolic profile to maximise treatment benefit. Meanwhile, hospital formulary committees face escalating budget pressures as multi-drug regimens reach five-digit annual costs, prompting negotiations around risk-sharing contracts linked to sustained virologic response or histology-confirmed fibrosis reversal.

Key Report Takeaways

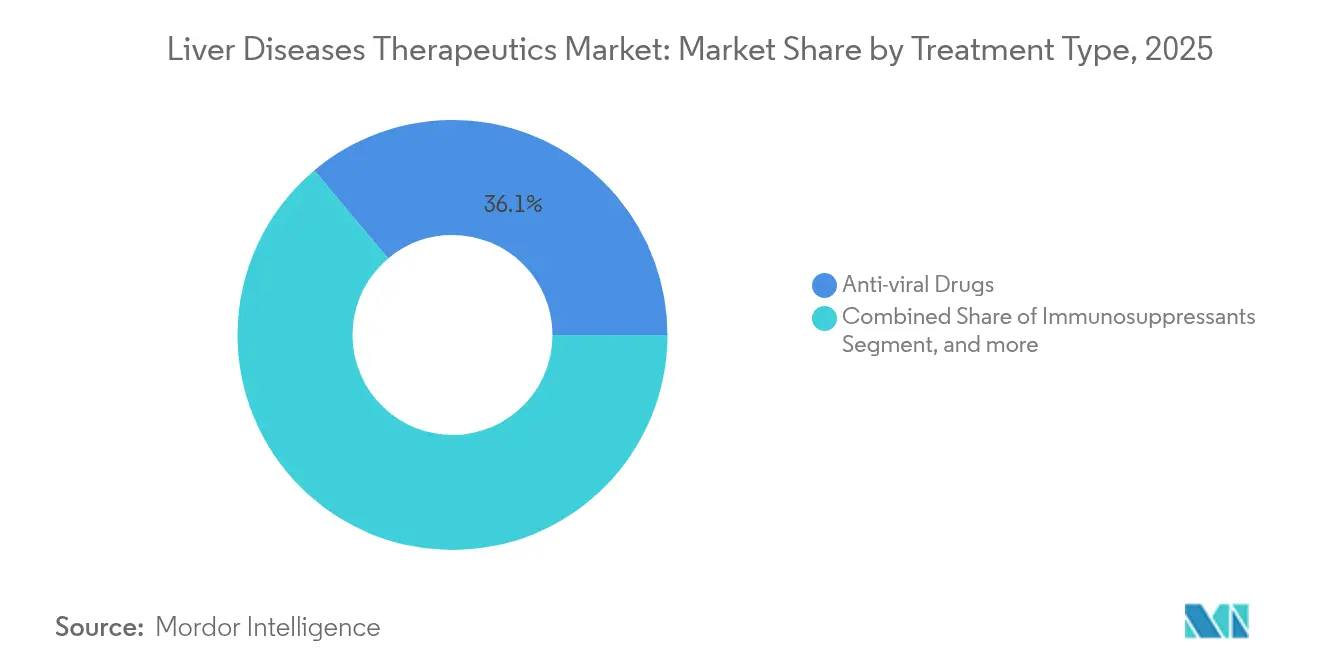

- By treatment type, anti-viral drugs commanded 36.12% of liver disease therapeutics market share in 2025, whereas antifibrotic/antisteatotic agents are projected to accelerate at a 10.22% CAGR through 2031.

- By disease type, viral hepatitis accounted for a 42.35% share of the liver disease therapeutics market size in 2025; MASLD is expanding at an 11.28% CAGR to 2031.

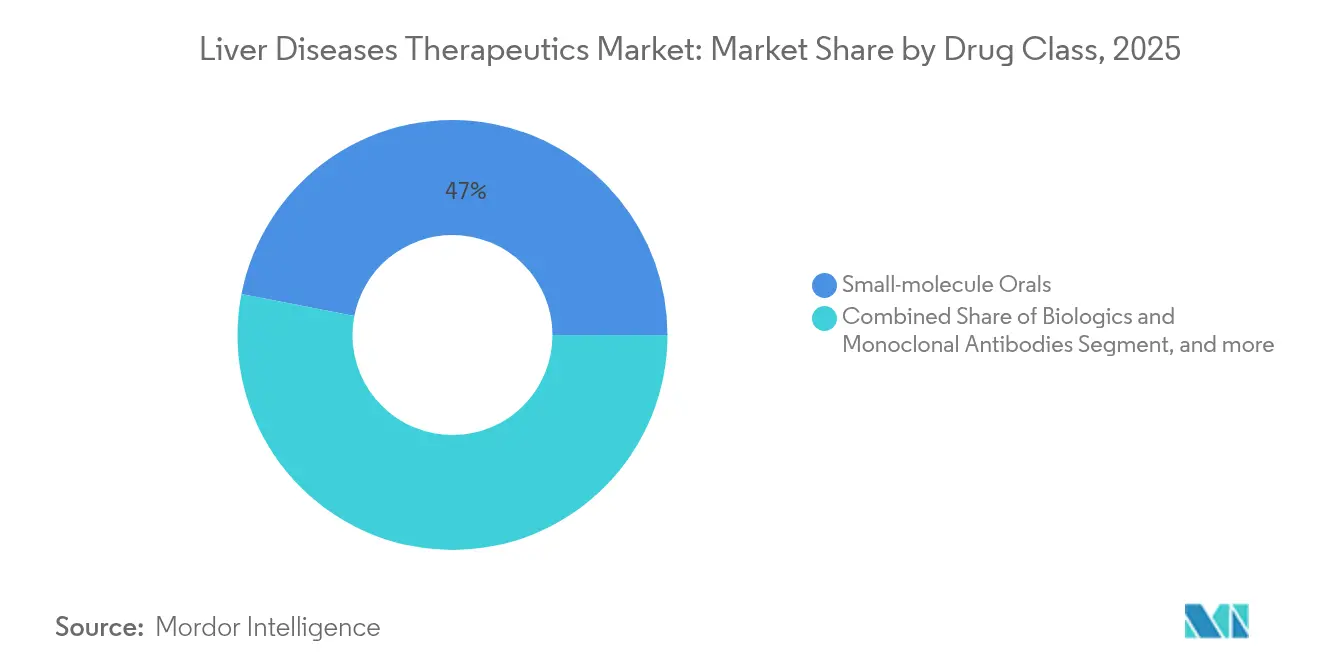

- By drug class, small-molecule orals captured 46.95% share of the liver disease therapeutics market size in 2025, while RNA-based therapeutics exhibit the fastest 11.92% CAGR through 2031.

- By route of administration, injectable formulations are advancing at a 13.10% CAGR to 2031, outpacing oral alternatives; orals captured 62.84% share of the liver disease therapeutics market size in 2025,

- By end user, hospitals held 53.05% of liver disease therapeutics market share in 2025, but specialty clinics are growing at an 10.74% CAGR through 2031.

- By geography, North America held 42.10% of the liver disease therapeutics market share in 2025, whereas Asia Pacific exhibits the fastest regional CAGR at 12.45% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Liver Diseases Therapeutics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in the incidence of liver diseases | +1.2% | Global | Long term (≥ 4 years) |

| Alcohol consumption & obesity-driven MASLD | +0.8% | North America & Europe | Medium term (2-4 years) |

| Government vaccination & screening programs | +0.6% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Breakthrough NASH-specific approvals | +0.4% | Global | Short term (≤ 2 years) |

| AI-powered non-invasive diagnostics | +0.3% | North America & EU | Medium term (2-4 years) |

| Combination RNAi-immunotherapy pipelines | +0.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in the Incidence of Liver Diseases

Hepatocellular carcinoma ranks as the third-leading cause of cancer mortality worldwide, while chronic liver disease affects more than 4.5 million Americans each year.[1]World Health Organization, “Global Hepatitis Report Update,” who.int This epidemiological surge stimulates sustained uptake of antivirals, immunotherapies, and disease-modifying antifibrotics. Asia-Pacific carries a heavier viral hepatitis burden, whereas Western economies confront rising MASLD linked to obesity and diabetes. Aging populations compound disease prevalence because hepatic regenerative capacity declines with age. National payer systems respond by broadening screening programmes that detect disease earlier, expanding the addressable pool for curative therapies and boosting the liver disease therapeutics market.

Increase in Alcohol Consumption & Obesity-Driven MASLD

MASLD touches roughly 25% of the global population, making it the fastest-growing indication for liver transplantation. Clinical evidence from 2024 shows metabolic-syndrome patients possess triple the risk of advancing to stage 3-4 fibrosis, and concurrent alcohol use accelerates disease by seven years. Dual-pathway drugs, including FGF21 agonists and PPAR modulators, are now in late-phase trials. Regulators embrace adaptive designs that test combination regimens, acknowledging MASLD’s multifactorial nature. In the United States alone, MASLD-related spending exceeds USD 103 billion annually, prompting insurers to accept premium pricing for therapies that avert progression to end-stage disease.

Rising Government Vaccination & Screening Initiatives

WHO’s hepatitis elimination roadmap galvanises policy-makers to fund mass vaccination, point-of-care diagnostics, and procurement of pan-genotypic antivirals. China’s March 2025 approval of Encofosbuvir, its first locally manufactured hepatitis C cure, underscores how national mandates can catalyse domestic innovation and widen access.[2]Synapse, “China Approves Encofosbuvir,” synapse.org.cn The European Commission backed the TherVacB therapeutic vaccine programme, with Phase Ia data slated for 2025, illustrating public commitment to functional cures. Expanded screening uncovers asymptomatic cases, fuelling near-term growth in the liver disease therapeutics market.

Breakthrough Approvals for NASH-Specific Drugs

FDA clearance of the thyroid hormone receptor-β agonist Resmetirom in 2024 set a precedent for therapies that reverse steatohepatitis on histology. More than 50 late-stage NASH candidates are now competing, ranging from FGF21 analogues to dual PPAR agonists. EMA clearance of Elafibranor for primary biliary cholangitis the same year signals global regulatory alignment.[3]European Medicines Agency, “Elafibranor Assessment Report,” europa.eu Shorter trial durations, because biopsy endpoints suffice, enable small biotech entrants to rival Big Pharma and quicken therapeutic variety within the liver disease therapeutics market.

Restraints Impact Analysis of Liver Diseases Therapeutics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse events & long-term safety issues | -0.5% | Global | Medium term (2-4 years) |

| Multi-regional regulatory timelines | -0.3% | Global | Short term (≤ 2 years) |

| Escalating therapy costs & reimbursement | -0.2% | North America & Europe | Long term (≥ 4 years) |

| Limited validated biomarkers | -0.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Events & Long-Term Safety Concerns of Therapies

Immunosuppressive regimens elevate infection risk by 40%; new antifibrotic agents mandate cardiac and renal monitoring. FDA now demands five-year post-marketing safety studies for NASH drugs. Complex dosing schedules undermine adherence, and physicians adopt conservative prescribing until long-term real-world data mature. To curb attrition, sponsors are investing in predictive toxicology and microphysiological liver models that flag safety liabilities earlier in drug development.

Stringent, Multi-Regional Regulatory Approval Timelines

Distinct endpoint requirements across FDA, EMA, and Asian agencies add 12-24 months to global launches. The scarcity of expert liver pathologists delays biopsy read-outs, and local ethnic-specific pharmacokinetic studies are compulsory in several Asian markets, inflating trial budgets. While adaptive designs win acceptance, they require extended protocol negotiations, pushing first-patient-in dates later and capping short-term growth of the liver disease therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Liver Diseases Therapeutics Market Segment Analysis

By Treatment Type:

Antivirals Dominate; Antifibrotics AccelerateAnti-viral therapies retained 36.12% share of the liver disease therapeutics market in 2025, propelled by pan-genotypic direct-acting antivirals that sustain 95% cure rates. Chronic hepatitis B suppression for 296 million carriers assures durable revenue. Meanwhile, antifibrotic/antisteatotic agents are projected to log a 10.22% CAGR to 2031, benefitting from Resmetirom’s first-in-class approval and a ballooning MASLD population. Immunosuppressants maintain a niche for autoimmune hepatitis, whereas oncology-focused immunotherapies increasingly supplant cytotoxic chemotherapies. Combination regimens blending metabolic correctors with anti-inflammatory agents are expanding prescribing patterns, lifting the liver disease therapeutics market size.

The competitive narrative is evolving as pipeline dispersion intensifies; more than a dozen dual-pathway candidates have entered Phase II within 18 months. Pay-for-performance contracts tied to non-invasive fibrosis regression scores bolster market uptake, especially among integrated health systems. As late-line antiviral resistance remains rare, lifecycle management pivots to fixed-dose combinations that lessen pill burden and shield franchises from generic erosion.

By Disease Type:

Viral Hepatitis Leads; MASLD Rising FastViral hepatitis contributed 42.35% of liver disease therapeutics market share in 2025 due to sheer patient volume and life-saving curative regimens. WHO elimination targets sustain procurement funding, and domestic production efforts in China and India lower per-course costs by 65%, broadening access and reinforcing the liver disease therapeutics market. MASLD, however, will post an 11.28% CAGR as obesity climbs worldwide. Steatotic liver disease’s multifactorial pathogenesis encourages combination therapy architectures that elevate average selling prices.

Alcohol-related liver disease receives fresh attention following FDA Breakthrough Therapy status for larsucosterol, which demonstrated 25% reduction in 90-day mortality in severe alcoholic hepatitis. Autoimmune liver diseases, although representing a smaller segment, achieve premium reimbursement for biologic agents that delay transplant need. Rare genetic and paediatric disorders benefit from orphan incentives that speed approvals and permit higher pricing benchmarks, cushioning research risk.

By Drug Class:

Small Molecules Prevail; RNA Therapeutics SurgeSmall molecules captured 46.95% of liver disease therapeutics market size in 2025 on the strength of oral antivirals and metabolic regulators requiring once-daily dosing. Their pharmacokinetic flexibility underpins broad utility across disease stages. RNA therapeutics, while accounting for a smaller base, will rise at a 11.92% CAGR, supported by GalNAc conjugates that direct siRNA to hepatocytes with 40-fold higher specificity. Regulatory confidence grows as accumulating real-world data corroborate sustained antigen knockdown without immunogenicity.

Biologic checkpoint inhibitors, including durvalumab plus tremelimumab, now anchor first-line therapy for unresectable hepatocellular carcinoma, unseating sorafenib. Cell and gene therapies remain early-stage but attract record venture funding; ex vivo CRISPR-edited hepatocyte implants entered Phase I in 2025, aiming to offer single-procedure cures. Portfolio managers increasingly co-develop oral back-ups to injectables in case payer resistance to high-cost parenteral regimens rises.

By Route of Administration:

Injectables Gain MomentumOral formulations still represent 62.84% market share, reflecting patient preference and decentralised care models. Yet injectables will clock a 13.10% CAGR to 2031 as biologics and RNA therapeutics demand parenteral delivery for systemic bioavailability. Monthly or quarterly subcutaneous versions improve adherence, and pen-injector devices enable at-home administration, reducing clinic visits. Hospitals expand infusion suites, while specialty pharmacies manage cold-chain logistics, widening distribution capacity for the liver disease therapeutics market.

Stakeholders anticipate a further shift toward ultra-long-acting depot injections that sustain drug exposure for six months, a move that could lower total cost of care by reducing monitoring frequency. Formulation scientists are also pursuing oral-to-injectable switches for legacy antivirals to extend patent life and bolster differentiation in crowded categories.

By End User:

Hospital Dominance Faces Rising Clinic PresenceHospitals controlled 53.05% of liver disease therapeutics market share in 2025, given their transplant infrastructure and multidisciplinary expertise. Complex inpatients with decompensated cirrhosis rely on intensive care resources available only in tertiary centres, ensuring hospitals’ central role. However, specialty clinics deliver an 10.74% CAGR through 2031, driven by value-based reimbursement that rewards outpatient management. Telehepatology follow-up visits surged 170% post-pandemic, enabling stable patients to remain in community settings.

Ambulatory surgery centres exploit minimally invasive ablation and endoscopic bariatric procedures that intercept disease progression, intersecting therapeutics with procedural care. Payers incentivise early discharge by reimbursing home-health nursing that administers injectable biologics, gradually shifting utilisation patterns and diversifying the liver disease therapeutics market.

Geography Analysis

North America Liver Diseases Therapeutics Market

North America captured 42.10% of revenue in 2025, underpinned by rapid adoption of newly approved NASH drugs and broad insurance coverage for pan-genotypic HCV antivirals. The presence of academic centres accelerates enrolment in late-phase trials, and tax credits support R&D. Yet ballooning therapy prices heighten scrutiny from pharmacy benefit managers that negotiate indication-based rebates.

APAC Liver Diseases Therapeutics Market

Asia-Pacific is the fastest-growing territory at a 12.45% CAGR to 2031. China alone houses 80 million chronic hepatitis B patients, and national reimbursement now covers first-line tenofovir generics, expanding the treated population. Japan’s fast-track review system shortens approval timelines for breakthrough biologics, while South Korea’s biotech tax incentives spur domestic RNAi pipelines.

EMEA and South America Liver Diseases Therapeutics Market

Europe witnesses steady, slower growth as health technology assessment agencies seek cost-effectiveness before authorising new entries. EMA alignment with FDA scientific advice has smoothed parallel submissions, but price-volume agreements can delay country-level launches by more than a year. Middle East & Africa and South America together account for minor share of global revenue; however, multilateral donor programmes and tiered pricing models improve access to WHO-preferred therapies, gradually enlarging the liver disease therapeutics market.

Competitive Landscape

Moderate consolidation defines the sector. The top five manufacturers account significant share of global revenue, with Gilead Sciences and AbbVie leading the antiviral category, while Novo Nordisk, Eli Lilly, and Madrigal Pharmaceuticals spearhead the emerging metabolic arena. Recent strategic moves include GSK’s USD 1.2 billion acquisition of efimosfermin, expanding its FGF21 pipeline, and Boehringer Ingelheim’s USD 2 billion RNAi alliance with Ribo Life Science. These deals illustrate premium valuations for assets that differentiate on fibrosis reversal or once-monthly dosing convenience.

Firms deploy artificial intelligence to cut lead-optimisation time by 30%, and digital twins model disease progression to inform pivotal trial design. Intellectual-property battles intensify around lipid nanoparticle compositions and GalNAc linker chemistry, as delivery technology becomes a key competitive lever. Co-marketing partnerships emerge in Europe, where niche biotech innovators lack the field force scale to penetrate multiple national formularies.

As combination therapy paradigms mature, collaboration replaces rivalry; co-development contracts align profit-sharing to simultaneous launch of dual mechanisms, smoothing regulatory review and payer negotiations. Suppliers of companion diagnostics gain bargaining power, securing long-term kit-placement deals that lock laboratories into specific therapeutic brands and deepen ecosystem moats in the liver disease therapeutics market.

Liver Diseases Therapeutics Industry Leaders

Abbott Laboratories

Novartis AG

Gilead Sciences Inc.

Sanofi S.A.

Astellas Pharma Inc.

- *Disclaimer: Major Players sorted in no particular order

Liver Diseases Therapeutics Market Companies Covered in this Report

- Abbott Laboratories

- Abbvie

- Astellas Pharma

- Alnylam Pharmaceuticals

- Bristol-Myers Squibb

- Roche

- Gilead Sciences

- GlaxoSmithKline

- Merck

- Novartis

- Pfizer

- Sanofi

- Takeda Pharmaceutical Co.

- Endo International

- Provectus Biopharmaceuticals

- Intercept Pharmaceuticals

- Madrigal Pharmaceuticals Inc.

- Eiger BioPharmaceuticals Inc.

- Ionis Pharmaceuticals

- Aligos Therapeutics Inc.

Recent Industry Developments in Liver Diseases Therapeutics Market

- May 2025: GSK announced a USD 1.2 billion acquisition of efimosfermin from Boston Pharmaceuticals, strengthening its liver disease portfolio with a novel FGF21 analog for metabolic liver conditions.

- May 2024: Bausch Health completed its USD 63 million acquisition of DURECT Corporation, gaining access to larsucosterol for alcoholic hepatitis treatment, which holds FDA Breakthrough Therapy Designation and represents a potential USD 413 million opportunity including milestone payments.

- April 2024: Boehringer Ingelheim established a partnership with Ochre Bio worth over USD 1 billion to develop regenerative treatments for advanced liver disease, focusing on RNA therapies and deep phenotyping approaches to enhance liver self-repair capabilities.

- January 2024: Boehringer Ingelheim partnered with Suzhou Ribo Life Science in a deal potentially exceeding USD 2 billion to develop RNA interference therapeutics for NASH, targeting disease-causing genes in hepatocytes.

Global Liver Diseases Therapeutics Market Report Scope

As per the scope of the report, liver disease is either inherited or caused by factors that damage the liver, such as viruses and the use of alcohol. Liver disease, if not treated, damages the liver and further leads to liver failure. Therefore, some of the major drugs used in treating various types of liver diseases include vaccines, immunosuppressants, chemotherapy drugs, and anti-viral drugs. The liver disease therapeutics market is segmented by treatment type (anti-viral drugs, targeted therapy, immunosuppressant drugs, chemotherapy drugs, immunoglobulin, vaccines, and other treatment types), end user (hospitals, ambulatory surgery centers, and other end users), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

Segmentation Overview

| Anti-viral Drugs |

| Immunosuppressants |

| Targeted Therapy & Small Molecules |

| Chemotherapy Drugs |

| Antifibrotic/Antisteatotic Agents |

| Vaccines |

| Immunoglobulins |

| Viral Hepatitis (A-E) |

| Alcohol-Related Liver Disease (ARLD) |

| Metabolic Dysfunction-Associated Steatotic Liver Disease (MASLD) / MASH |

| Autoimmune Liver Diseases |

| Genetic & Pediatric Disorders |

| Other Disease Types |

| Small-molecule Orals |

| Biologics & Monoclonal Antibodies |

| RNA-based Therapeutics |

| Cell & Gene Therapy |

| Oral |

| Injectable |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Anti-viral Drugs | |

| Immunosuppressants | ||

| Targeted Therapy & Small Molecules | ||

| Chemotherapy Drugs | ||

| Antifibrotic/Antisteatotic Agents | ||

| Vaccines | ||

| Immunoglobulins | ||

| By Disease Type | Viral Hepatitis (A-E) | |

| Alcohol-Related Liver Disease (ARLD) | ||

| Metabolic Dysfunction-Associated Steatotic Liver Disease (MASLD) / MASH | ||

| Autoimmune Liver Diseases | ||

| Genetic & Pediatric Disorders | ||

| Other Disease Types | ||

| By Drug Class | Small-molecule Orals | |

| Biologics & Monoclonal Antibodies | ||

| RNA-based Therapeutics | ||

| Cell & Gene Therapy | ||

| By Route of Administration | Oral | |

| Injectable | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the liver disease therapeutics market by 2031?

The market is forecast to reach USD 35.33 billion by 2031, growing at a 7.09% CAGR.

Which treatment type currently leads in revenue?

Anti-viral drugs hold 36.12% of revenue, driven by chronic hepatitis B and C therapies.

Why is MASLD attracting rapid investment?

Rising global obesity and metabolic syndrome rates push MASLD to an 11.28% CAGR, incentivising multi-mechanism drug development.

How fast are RNA-based therapeutics expanding?

RNA agents are advancing at a 11.92% CAGR, enabled by GalNAc and lipid nanoparticle delivery innovations.

Which region will grow the quickest to 2031?

Asia-Pacific is set to expand at a 12.45% CAGR due to high viral hepatitis prevalence and policy-driven access improvements.

What recent deal illustrates rising asset valuations?

GSK’s USD 1.2 billion acquisition of efimosfermin underscores the premium commanded by breakthrough metabolic candidates.

Page last updated on: