Ketoanalogues For Kidney Diseases Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

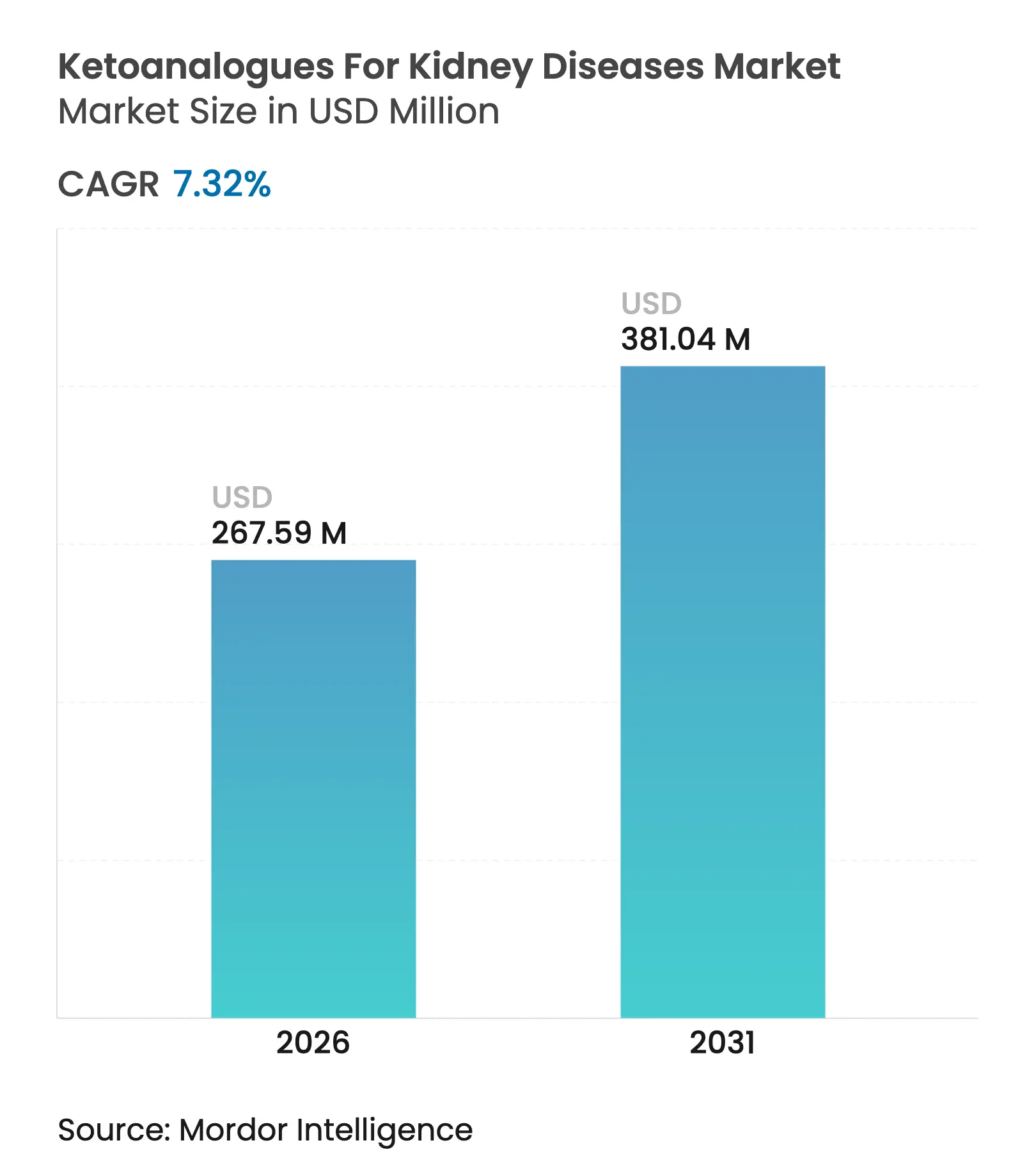

| Market Size (2026) | USD 267.59 Million |

| Market Size (2031) | USD 381.04 Million |

| Growth Rate (2026 - 2031) | 7.32 % CAGR |

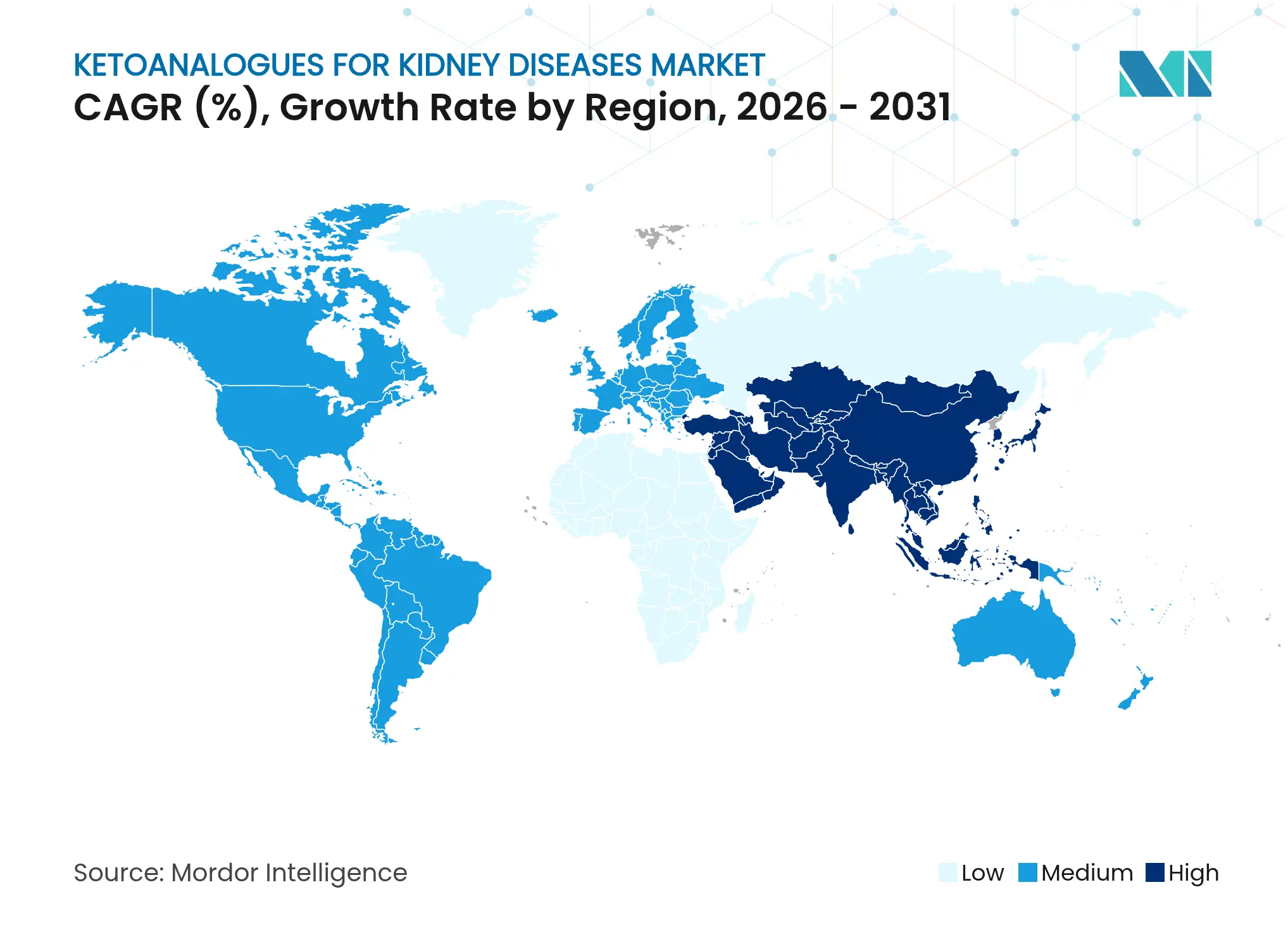

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ketoanalogues For Kidney Diseases Market Analysis by Mordor Intelligence

The ketoanalogues for kidney diseases market size was valued at USD 249.34 million in 2025 and estimated to grow from USD 267.59 million in 2026 to reach USD 381.04 million by 2031, at a CAGR of 7.32% during the forecast period (2026-2031). Strong growth links to rising chronic kidney disease (CKD) prevalence, updated KDOQI and ERBP guidelines that endorse very low-protein diets with ketoanalogue supplementation, and payer moves to cover nutrition-first approaches that postpone costly dialysis. As dialysis supply chains become less predictable, physicians lean on dietary therapeutics that protect residual kidney function while easing hospital resource pressure. Concurrently, plant-dominant low-protein diet programs gain traction, positioning ketoanalogues as the biochemical linchpin that keeps protein restriction safe and sustainable. Competitive activity remains moderate but intensifying: global leaders Fresenius Kabi and B. Braun pair formulation upgrades with provider-education campaigns, whereas regional Asian manufacturers use cost-efficient production to capture price-sensitive demand. Looming raw-material shortages following Evonik’s planned 2025 exit from keto acid production introduce supply concentration risk that could lift average selling prices and favor vertically integrated firms.

Key Report Takeaways

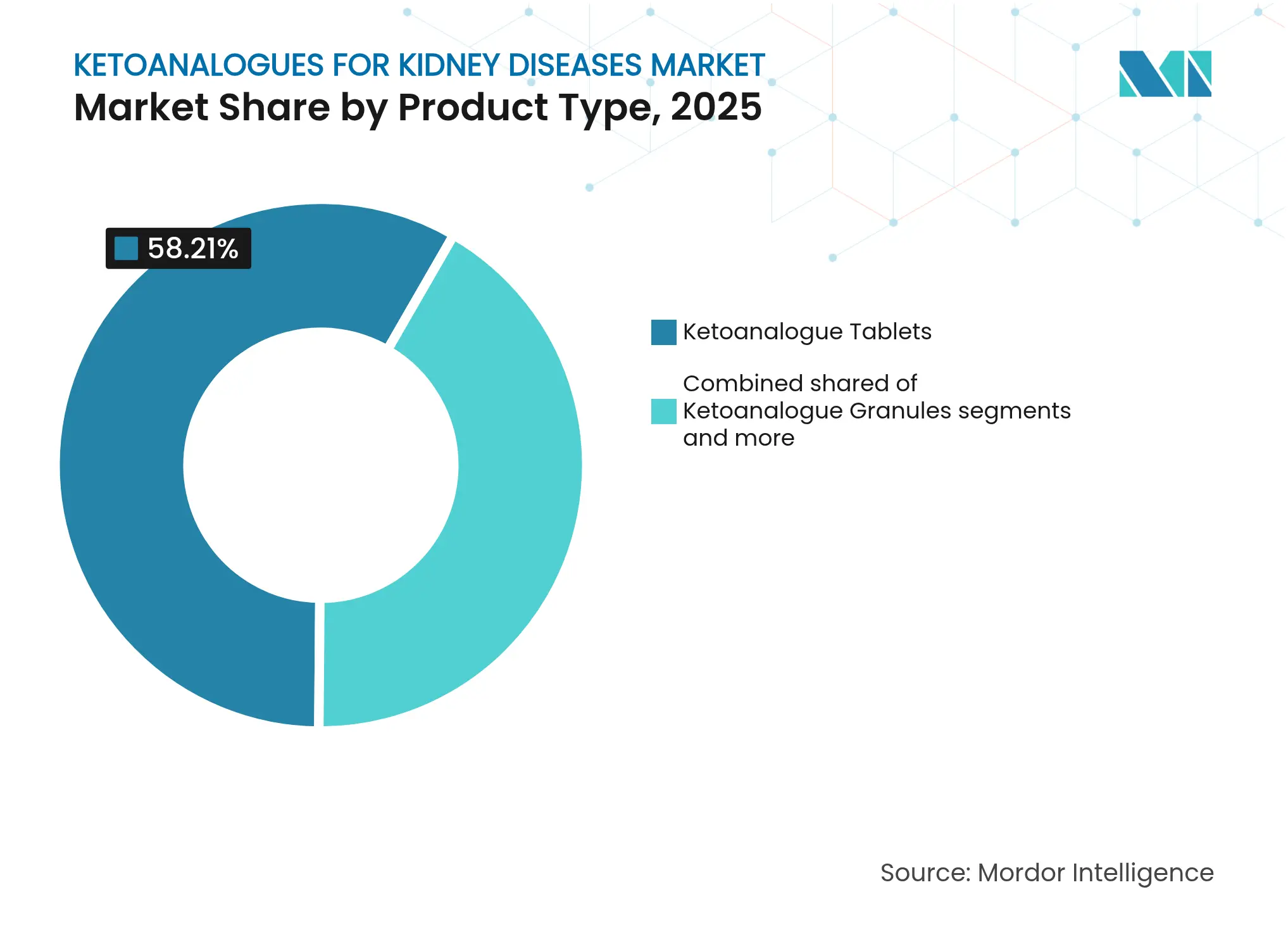

- By product type, tablets held 58.21% revenue share in 2025 and granules are set to expand at an 8.12% CAGR through 2031.

- By formulation, stand-alone presentations accounted for 66.74% of the ketoanalogues for kidney diseases market size in 2025 while vitamin-mineral combinations record the fastest 8.37% CAGR to 2031.

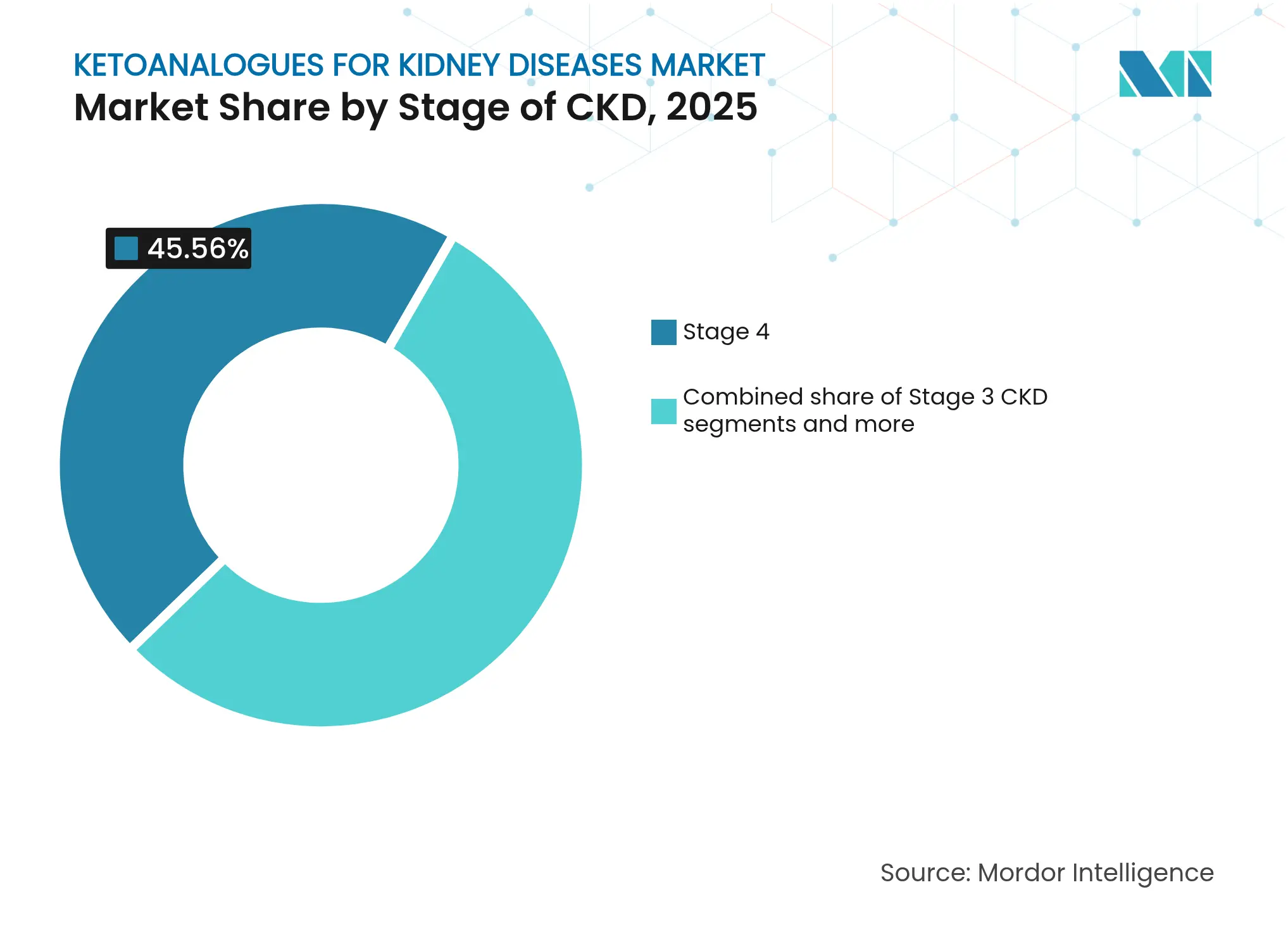

- By CKD stage, Stage 4 patients generated 45.56% of 2025 demand; the Stage 5 pre-dialysis cohort shows a 8.78% CAGR forecast.

- By distribution channel, hospital pharmacies captured 53.27% of the ketoanalogues for kidney diseases market share in 2025 and online pharmacies advance at a 9.08% CAGR to 2031.

- By geography, North America commanded 37.88% revenue in 2025; Asia-Pacific posts the strongest 9.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ketoanalogues For Kidney Diseases Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of chronic kidney disease (CKD) Rising prevalence of chronic kidney disease (CKD) | +1.8% | Global, with highest impact in North America and Asia-Pacific | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, with highest impact in North America and Asia-Pacific | Impact Timeline:Long term (≥ 4 years) |

Broader reimbursement of Ketosteril & class analogues Broader reimbursement of Ketosteril & class analogues | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Inclusion of ketoanalogues in 2023-24 KDOQI & ERBP dietary guidelines Inclusion of ketoanalogues in 2023-24 KDOQI & ERBP dietary guidelines | +0.9% | Global, with immediate impact in developed markets | Short term (≤ 2 years) | |||

Growing evidence from RCTs/meta-analyses supporting delayed dialysis Growing evidence from RCTs/meta-analyses supporting delayed dialysis | +0.7% | Global, with faster adoption in academic medical centers | Medium term (2-4 years) | |||

Surge in plant-dominant low-protein diet (PLADO) programmes Surge in plant-dominant low-protein diet (PLADO) programmes | +0.6% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) | |||

Dialysis-supply shocks driving physicians toward diet therapeutics Dialysis-supply shocks driving physicians toward diet therapeutics | +0.5% | Global, with acute impact in resource-constrained regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising prevalence of chronic kidney disease (CKD)

More than 800 million people live with CKD, and incidence skews toward late-stage disease in diabetics and hypertensive patients. An ageing demographic in industrialised economies sustains demand, while lifestyle change and better diagnostics lift Asian caseloads. Health systems now calculate that delaying dialysis by even six months saves over USD 45,000 per patient, prompting earlier dietary intervention. Payers therefore revisit benefit designs to include ketoanalogues as a preventive line item, amplifying the ketoanalogues for kidney diseases market growth trajectory. This epidemiological reality also pushes primary care physicians to collaborate with dietitians so that nutrition therapy begins well before referral to nephrology.

Broader reimbursement of Ketosteril & class analogues

Medicare and several European insurers classified ketoanalogues as reimbursable in 2024, erasing a historic cost barrier. Cost-utility studies show incremental cost-effectiveness ratios below USD 50,000 per QALY relative to early dialysis start, satisfying common payer thresholds. Once coverage codes went live, prescription volume jumped because physicians no longer feared sticker shock for patients. Harmonised billing codes also shorten administrative cycles, turning formerly niche prescriptions into standard electronic medical record prompts. This cascade strengthens evidence loops, as higher usage feeds registries that document longer dialysis-free survival.

Inclusion of ketoanalogues in 2023-24 KDOQI & ERBP dietary guidelines

Guideline endorsement shifted ketoanalogues from an optional add-on to protocolised therapy. Hospitals responded by adding products to formularies and embedding dietitian consults into CKD care pathways. The recommendations highlight safe protein targets and caution against malnutrition, easing clinician hesitation. Guideline momentum quickly travelled to Latin American and Southeast Asian societies, which adapt the same algorithms, thereby globalising demand and reinforcing the ketoanalogues for kidney diseases market relevance.

Growing evidence from RCTs/meta-analyses supporting delayed dialysis

Recent meta-analysis covering 1,500 patients reported a 51% reduction in dialysis initiation risk when ketoanalogues augment a very low-protein diet. Trials further link therapy to improved serum albumin, refuting malnutrition fears. Such data underpin regulatory approvals and payer dossiers, giving manufacturers solid clinical narratives. Academic centres leverage the evidence to win grants for nutrition-first CKD programs, reinforcing institutional buy-in.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High out-of-pocket cost for patients in many countries High out-of-pocket cost for patients in many countries | -0.8% | Global, with highest impact in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Global, with highest impact in emerging markets | Impact Timeline:Medium term (2-4 years) |

Limited prescriber & dietitian familiarity with ketoanalogues Limited prescriber & dietitian familiarity with ketoanalogues | -0.6% | Global, particularly in primary care settings | Short term (≤ 2 years) | |||

Regulatory classification ambiguity (drug vs. food for special use) Regulatory classification ambiguity (drug vs. food for special use) | -0.4% | Emerging markets and regions with evolving regulatory frameworks | Long term (≥ 4 years) | |||

Shortage of keto-acid raw materials affecting production scale-up Shortage of keto-acid raw materials affecting production scale-up | -0.3% | Global, with supply chain concentration in Europe and Asia | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High out-of-pocket cost for patients in many countries

Monthly retail prices ranging from USD 200-400 remain prohibitive where insurance does not cover medical foods. Patients in Thailand and Taiwan spend more than 10% of household income on ketoanalogues, often discontinuing therapy when wages dip. Such affordability gaps depress unit sales despite clear clinical value. Governments that subsidise dialysis yet not nutrition face budget paradoxes; pilot bundled-payment models now test whether early reimbursement actually lowers total renal spend.

Limited prescriber & dietitian familiarity with ketoanalogues

Many nephrologists finish training without hands-on experience titrating ketoanalogue doses, and community dietitians rarely counsel on very low-protein diets. This know-how deficit slows adoption outside tertiary centres. Manufacturers responded with e-learning modules and dosing calculators embedded in electronic health records. Continuing-education credits linked to these tools already lift prescription volumes in pilot markets, hinting at a scalable remedy.

Segment Analysis

By Product Type: Tablets Dominate Despite Granule Innovation

Tablet formulations held 58.21% of the ketoanalogues for kidney diseases market share in 2025, underscoring clinician preference for fixed dosing and patient familiarity with solid forms. Granules deliver the strongest 8.12% CAGR to 2031 by addressing paediatric dosing and dysphagic elderly patients, positioning manufacturers to capture underserved subgroups. Tablets benefit from lower cost-per-dose and robust stability data, cementing their role in hospital formularies where procurement teams prioritise proven shelf life. Granules, however, dissolve easily into liquids, supporting home-care regimens that rely on caregivers rather than clinical staff, helping the ketoanalogues for kidney diseases market reach community settings. Active R&D focuses on taste-masking and faster dispersion for granules to match tablet convenience without sacrificing palatability, signalling future convergence in user experience.

A third format, ketoacid sachets, maintains a niche profile for customised compounding or liquid preparations but lacks scale economies. Paediatric nephrologists nevertheless value sachets when weight-based dosing is pivotal. Manufacturers weigh whether to broaden sachet availability or migrate those volumes to improved granule technology. Successful migration would simplify manufacturing lines and enhance capacity utilisation, indirectly improving tablet output resilience during raw-material shocks.

Note: Segment shares of all individual segments available upon report purchase

By Formulation: Stand-Alone Products Lead Amid Combination Growth

Stand-alone amino-acid analogues controlled 66.74% of 2025 revenue, reflecting prescriber desire to individualise vitamin and mineral supplementation based on frequent lab monitoring. Combination products achieve an 8.37% CAGR due to simplified pill burden; one capsule covers both ketoanalogues and common micronutrient deficits. Hospitals increasingly adopt combination SKUs for outpatient starters because fewer units streamline dispensing and adherence tracking. Still, some nephrologists worry that fixed-ratio vitamins complicate hyperphosphataemia management, so they reserve combinations for stable patients. Manufacturers employ micro-encapsulation to prevent nutrient interaction, and stability studies now support two-year shelf life even in humid tropics, expanding geographic reach.

Regulatory pathways differ: drugs with combined active ingredients usually demand more rigorous trials than medical-food equivalents. Firms seeking global registrations often launch stand-alone first, then add combinations once regional data satisfy risk/benefit assessments. This sequencing protects early revenue while building physician familiarity that later boosts combination uptake, reinforcing the ketoanalogues for kidney diseases market expansion curve.

By Stage of CKD: Stage 4 Dominance with Pre-Dialysis Acceleration

Stage 4 CKD patients generated 45.56% of 2025 demand and remain the clinical sweet spot where estimated glomerular filtration rate (eGFR) between 15-29 mL/min still allows meaningful delay before dialysis. Stage 5 pre-dialysis patients log the highest 8.78% CAGR as nephrologists push aggressive diet therapy to preserve residual function. Evidence suggests ketoanalogues paired with <0.3 g/kg/day protein delay vascular access placement by nine months on average, a timeline that carries emotional and cost benefits for patients. Stage 3 adoption remains exploratory; guideline committees call for more trials before universal endorsement. Nonetheless, early-stage pilot studies in Italy and Japan intimate that earlier protein moderation may slow trajectory toward end-stage disease, hinting at a future expansion band for the ketoanalogues for kidney diseases market.

Transplant recipients emerge as an ancillary segment after a 2024 study demonstrated improved graft nitrogen balance when ketoanalogues supplemented reduced protein intake. If ongoing trials confirm this finding, post-transplant protocols could unlock a new revenue column, diversifying the risk profile otherwise concentrated in late-stage CKD.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Hospital Pharmacies Lead Digital Transformation

Hospital pharmacies accounted for 53.27% of 2025 sales because initiation often coincides with nephrology clinic visits where laboratory monitoring infrastructure exists. Online channels climb at a 9.08% CAGR, accelerated by e-prescription laws and direct-to-patient logistics that cut co-pay friction. Home-delivery models integrate tele-dietitian consults, giving payers confidence that remote dispensing does not erode adherence. Retail pharmacies occupy a bridging role for refills but wrestle with stock-turn challenges given lower volume per store. Some chains pilot automatic replenishment tied to electronic lab results, foreshadowing an omnichannel future where data flows dictate replenishment timing, bolstering the ketoanalogues for kidney diseases market resilience against supply hiccups.

Manufacturers experiment with subscription bundles that combine product, diet-tracking apps and quarterly lab kits, essentially framing ketoanalogues as a service. Early evidence shows 15% higher refill persistence among subscription users, translating into more stable revenue forecasting and reduced payer spend on preventable hospitalisations.

Geography Analysis

North America held 37.88% of global revenue in 2025, anchored by Medicare reimbursement, high nephrologist density and strong dietitian networks. United States academic centres publish continual real-world evidence, further entrenching ketoanalogues in care pathways. Canada's single-payer model reimburses ketoanalogues through provincial formularies, though regional coverage disparities prompt patient travel to obtain subsidised supply. Telehealth adoption accelerates cross-border e-commerce, enlarging reach of US-based online pharmacies into rural Canadian locales.

Europe offers a heterogenous landscape: Germany and France post robust hospital uptake owing to long-standing nutrition research programmes, while Italy leads outpatient penetration through PLADO clinics embedded in public hospitals. Southern economies face tighter drug budgets, slowing combination-product rollout and thereby moderating ketoanalogues for kidney diseases market growth. The UK adheres to post-Brexit MHRA rules but remains largely aligned with EMA dossiers, averting duplication for manufacturers. Home-delivery models flourish under National Health Service digital initiatives, potentially narrowing regional access gaps.

Asia-Pacific is the fastest-growing theatre at 9.42% CAGR to 2031. China and India feature massive CKD bases and improving insurance penetration; provincial Chinese tenders already include ketoanalogues as cost-effective alternatives to dialysis in under-resourced counties. Japan's ageing society sustains volume, and its food-for-special-medical-use (FFSMU) framework eases regulatory burden. South Korea, with robust online grocery infrastructures, showcases rapid consumer adoption through pharmacy-linked marketplaces. Meanwhile, Australian nephrologists pilot indigenous-community nutrition outreach that integrates locally sourced plant proteins with ketoanalogue supplementation, demonstrating cultural adaptation possibilities.

Latin America and the Middle East register moderate uptake due to fragmented reimbursement but benefit from ongoing humanitarian initiatives that supply ketoanalogues in disaster-prone regions. Regional producers in Brazil and Turkey plan to localise synthesis to cut import duties and lead times; success could turn these geographies from net importers into emerging export hubs by 2030, further broadening the ketoanalogues for kidney diseases market footprint.

Competitive Landscape

Market Concentration

The ketoanalogues for kidney diseases market remains moderately consolidated. Fresenius Kabi and B. Braun leverage full-line renal portfolios plus global distribution to secure long-term tenders with hospital groups. These companies invest in clinical-education grants that embed their brands in residency curricula, locking in early prescriber loyalty. Fresenius Kabi’s 2024 launch of a micro-encapsulated combination tablet extended product shelf life in humid climates and targeted Asia-Pacific expansion.

Second-tier players such as Julphar and Changan Pharma exploit price niches in Middle East and China respectively, relying on local GMP facilities that dodge import tariffs. However, limited R&D spend restricts their ability to produce innovative formats, posing long-term competitiveness questions. Japanese amino-acid specialist Ajinomoto supplies intermediates to multiple formulators, cushioning revenue via B2B channels while exploring a consumer-facing granule slated for 2026.

Supply-side risk intensifies after Evonik’s exit, prompting strategic stockpiles and multi-year framework deals among the top five manufacturers. Fresenius Kabi reportedly negotiated a three-supplier arrangement spanning Europe and India to hedge. Smaller entrants lacking such leverage confront higher spot prices, widening cost differentials that may spark consolidation. Meanwhile, digital health partnerships emerge: B. Braun collaborates with a US tele-nutrition start-up to integrate dosing calculators into at-home blood-urea-nitrogen monitors, differentiating service layers rather than molecule composition.

White-space innovation targets paediatric chewables and sachets fortified with fibre to counter constipation common in low-protein diets. Early prototypes show stable dissolution and acceptable taste scores. Success would grant first-mover advantage in a segment currently addressed through off-label dose splitting. Overall, the competitive theatre balances scale economies against niche agility, setting the stage for selective mergers as raw-material volatility persists.

Ketoanalogues For Kidney Diseases Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vitafoods Insights highlighted supplement firms entering GLP-1 modulation, signalling broader metabolic-health convergence that could influence ketoanalogue positioning.

- October 2024: Evonik confirmed 2025 closure of its Hanau keto acid plant, stoking supply-security planning

Table of Contents for Ketoanalogues For Kidney Diseases Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising prevalence of chronic kidney disease (CKD)

- 4.2.2Broader reimbursement of Ketosteril & class analogues

- 4.2.3Inclusion of ketoanalogues in 2023-24 KDOQI & ERBP dietary guidelines

- 4.2.4Growing evidence from RCTs/meta-analyses supporting delayed dialysis

- 4.2.5Surge in plant-dominant low-protein diet (PLADO) programmes

- 4.2.6Dialysis-supply shocks driving physicians toward diet therapeutics

- 4.3Market Restraints

- 4.3.1High out-of-pocket cost for patients in many countries

- 4.3.2Limited prescriber & dietitian familiarity with ketoanalogues

- 4.3.3Regulatory classification ambiguity (drug vs. food for special use)

- 4.3.4Shortage of keto-acid raw materials affecting production scale-up

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitute Products

- 4.7.5Competitive Rivalry

- 4.8Pricing Analysis

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Ketoanalogue Tablets

- 5.1.2Ketoanalogue Granules

- 5.1.3Ketoacid Sachets

- 5.2By Formulation

- 5.2.1Stand-alone Ketoanalogues

- 5.2.2Ketoanalogues + Vitamins / Minerals

- 5.3By Stage of CKD

- 5.3.1Stage 3 CKD

- 5.3.2Stage 4 CKD

- 5.3.3Stage 5 (Pre-dialysis)

- 5.4By Distribution Channel

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies

- 5.4.3Online Pharmacies

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4South America

- 5.5.4.1Brazil

- 5.5.4.2Argentina

- 5.5.4.3Rest of South America

- 5.5.5Middle East and Africa

- 5.5.5.1GCC

- 5.5.5.2South Africa

- 5.5.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Fresenius Kabi AG

- 6.3.2B. Braun SE

- 6.3.3Julphar (Gulf Pharmaceutical Industries)

- 6.3.4Fagron NV

- 6.3.5Ajinomoto Co., Inc.

- 6.3.6Tonghua Dongbao Pharmaceutical Co., Ltd.

- 6.3.7Sichuan Kelun Pharmaceutical Co., Ltd.

- 6.3.8Zhejiang Tianrui Pharmaceutical Co., Ltd.

- 6.3.9Hunan Wuzhi Pharmaceuticals

- 6.3.10Chiral Pharma Corporation

- 6.3.11Renal Tech International

- 6.3.12Avanscure Lifesciences

- 6.3.13Synergen Healthcare

- 6.3.14Beijing Fresenius Kabi Pharmaceutical

- 6.3.15Navita Pharma

- 6.3.16Kibion AB

- 6.3.17Hebei Langfang Pharmaceutical

- 6.3.18Omecal Nutraceuticals

- 6.3.19PharmaVitae

- 6.3.20Jubilant Life Sciences

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Ketoanalogues For Kidney Diseases Market Report Scope

As per the scope of the report, ketoanalogues are used for the treatment of various kidney diseases, and they work by preventing the unnecessary increase in urea levels in the blood due to the intake of non-essential amino acids.

The ketoanalogues for kidney diseases market is segmented by application (chronic kidney disease, renal failure, and other applications), distribution channel (hospital pharmacy, retail pharmacy, and other distribution channels), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers market sizes and forecasts in terms of value (USD) for the above segments.