Oral Solid Dosage Pharmaceutical Formulation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

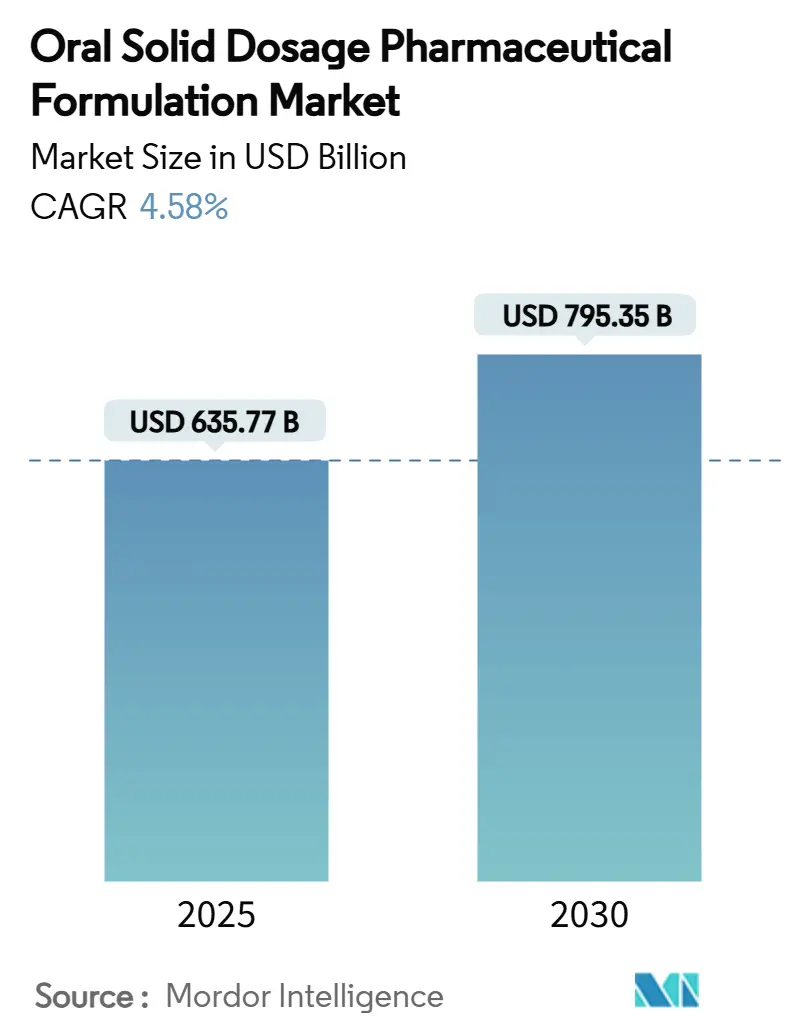

| Market Size (2025) | USD 635.77 Billion |

| Market Size (2030) | USD 795.35 Billion |

| Growth Rate (2025 - 2030) | 4.58% CAGR |

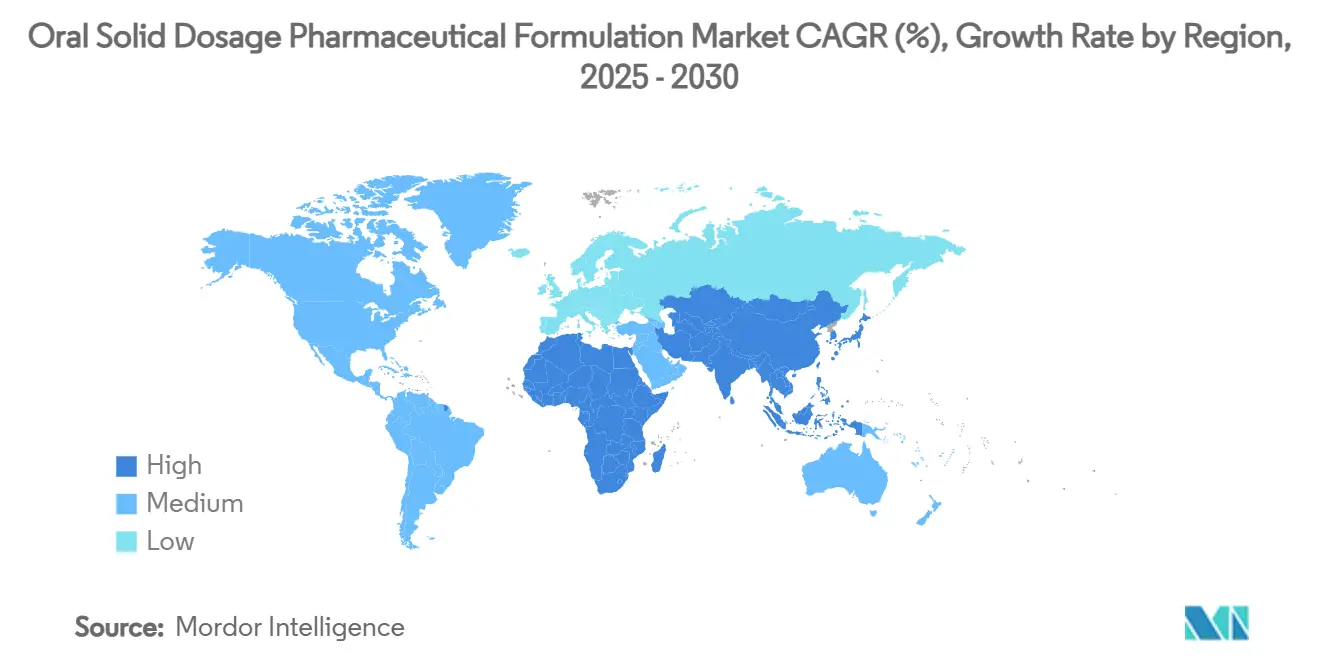

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

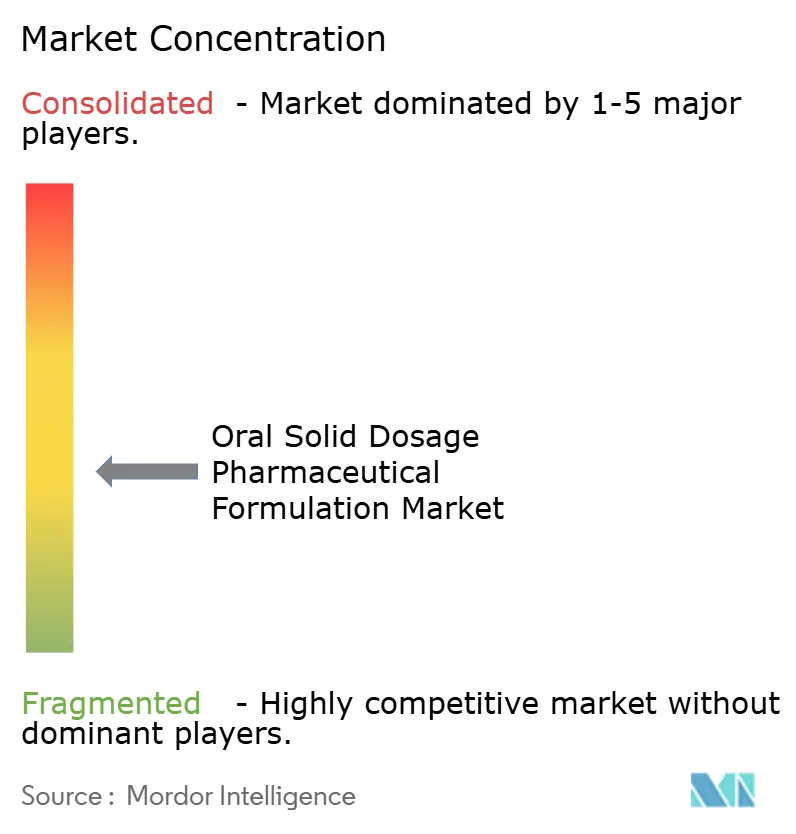

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oral Solid Dosage Pharmaceutical Formulation Market Analysis by Mordor Intelligence

The oral solid dosage pharmaceutical formulation market size reached USD 635.77 billion in 2025 and is forecast to reach USD 795.35 billion by 2030, advancing at a 4.58% CAGR. Robust demand for patient-friendly formats, accelerated adoption of continuous manufacturing, and patent-cliff-driven reformulations are sustaining expansion. Digital formulation platforms and artificial intelligence-guided screening are shortening development cycles and improving first-time-right success rates. At the same time, consolidation among contract development and manufacturing organizations is strengthening global capacity and widening access to advanced technologies. Regulatory scrutiny of nitrosamine and elemental impurities is prompting proactive quality-by-design strategies that further differentiate competitive offerings.

Key Report Takeaways

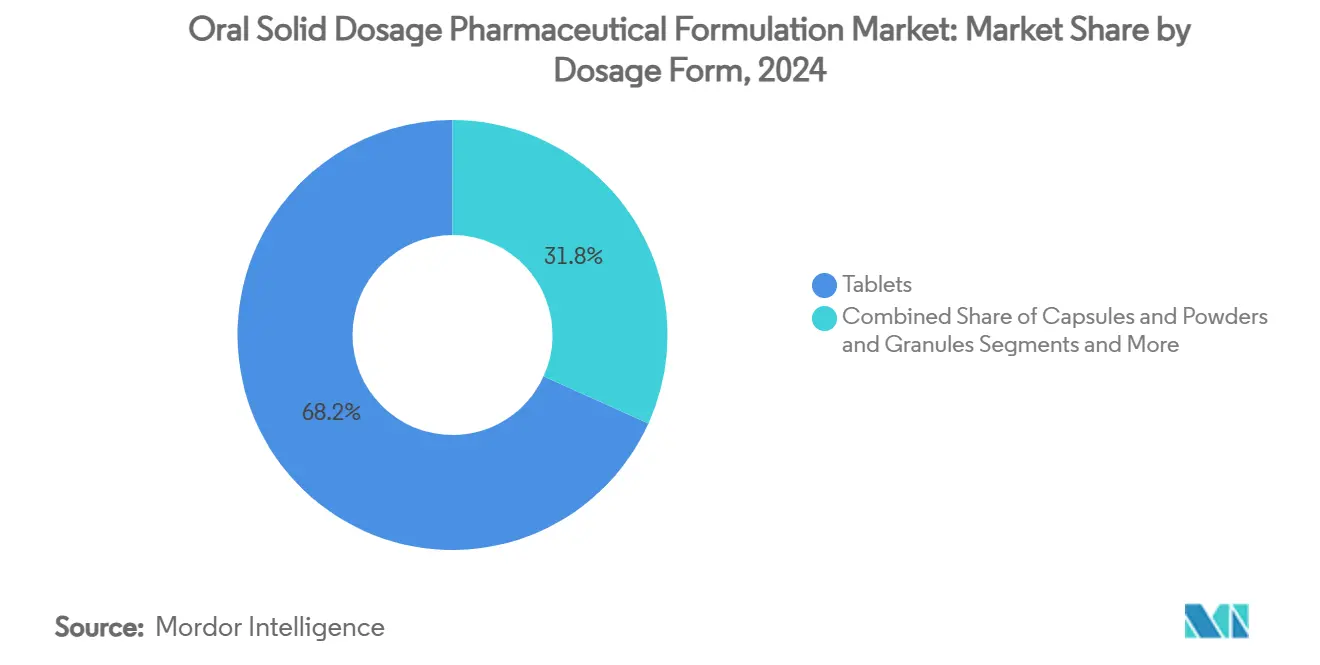

- By dosage form, tablets captured 68.24% of the oral solid dosage pharmaceutical formulation market share in 2024 while orally disintegrating films are projected to rise at a 7.36% CAGR through 2030.

- By release mechanism, immediate release products held 61.23% of the oral solid dosage pharmaceutical formulation market size in 2024; targeted and advanced delivery systems are growing at an 8.85% CAGR.

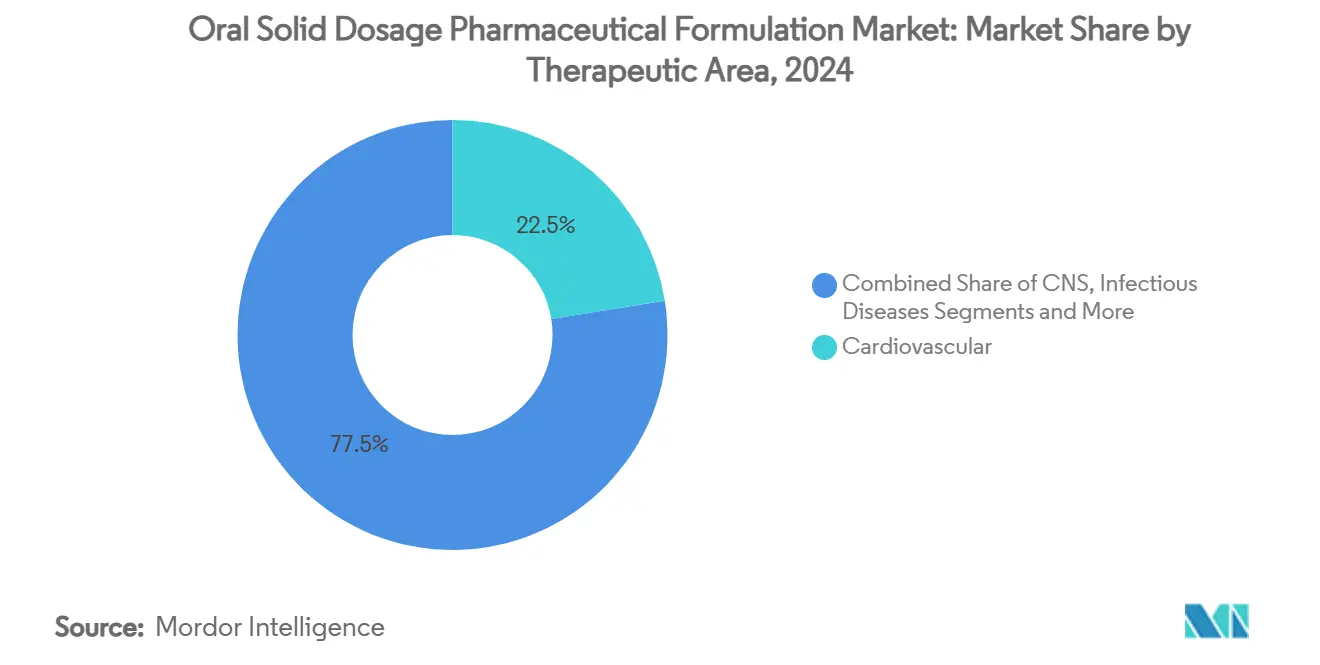

- By therapeutic area, cardiovascular products led with 22.46% revenue share in 2024, whereas oncology formulations are advancing at a 7.34% CAGR.

- By manufacturer type, large pharmaceutical companies retained 41.66% of the oral solid dosage pharmaceutical formulation market share in 2024, and CDMOs are forecast to post a 7.33% CAGR to 2030.

- By geography, North America commanded 34.74% revenue in 2024, while Asia-Pacific is on track for a 6.74% CAGR during the outlook period.

Global Oral Solid Dosage Pharmaceutical Formulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for patient-centric OSD formats | +1.2% | Global with early uptake in North America and Europe | Medium term (2-4 years) |

| Continuous manufacturing lowering COGS and time-to-market | +0.8% | North America and Europe, expanding in Asia-Pacific | Long term (≥ 4 years) |

| Patent-cliff reformulation into modified-release variants | +0.9% | Global, concentrated in mature markets | Short term (≤ 2 years) |

| Outsourcing surge among virtual and small pharma to CDMOs | +1.1% | Global with hubs in India, China, and Europe | Medium term (2-4 years) |

| AI-enabled formulation screening improving success rates | +0.7% | North America and Europe leading, Asia-Pacific following | Long term (≥ 4 years) |

| Low-solubility APIs requiring advanced excipients | +0.6% | Global, driven by oncology and CNS therapy areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Patient-Centric OSD Formats (ODTs, Mini-Tablets)

Oral formulations designed for easy administration are gaining broad acceptance across pediatric, geriatric, and dysphagia populations. The European Pharmacopoeia’s codification of orally disintegrating tablets validates the category and encourages standardized development. Functional excipients such as mannitol-based platforms improve wettability and mouthfeel without compromising stability. Mini-tablet technologies offer precise dose flexibility, which supports personalized medicine and fixed-dose combinations. Studies show that tablets larger than 13.3 mm pose handling challenges, a finding that is steering innovators toward smaller geometries to boost adherence.[1]Yuri Shimizu, “Analysis of Factors Affecting Difficulty in Handling Oral Medicine Using Electronic Medication Notebook-Based Personal Health Records,” Scientific Reports, nature.comCollectively, these preferences are steering the oral solid dosage pharmaceutical formulation market toward value-added designs that enhance the overall therapy experience.

Continuous Manufacturing Adoption Lowering COGS & Time-to-Market

Continuous manufacturing replaces discrete batch steps with streamlined, end-to-end processes. Integration with quality-by-design principles allows real-time release testing, which improves process control and reduces scrap.[2]M.A. VandenBerg, “Learning From the Future: Towards Continuous Manufacturing of Nanomaterials,” AAPS Open, springeropen.com Digital twins and Industrial Internet of Things sensors enable predictive maintenance that cuts unplanned downtime.[3]Peyman Z. Moghadam, “Bioprocessing 4.0: A Pragmatic Review and Future Perspectives,” Digital Discovery, pubs.rsc.org The United States Food and Drug Administration has accepted more than 100 AI-enabled filings since 2021, underscoring regulatory confidence in data-rich control strategies.[4]U.S. Food and Drug Administration, “Artificial Intelligence and Machine Learning in Drug Development,” fda.gov Companies that adopt continuous lines report development timelines shrinking from years to months, generating substantial cost of goods savings. As a result, competitive gaps are widening within the oral solid dosage pharmaceutical formulation market.

Patent-Cliff Reformulation into Modified-Release Variants

Twenty-five high-value drugs will lose protection in 2025, opening pathways for lifecycle-extending modified-release versions. Matrix and osmotic technologies allow tailored pharmacokinetic profiles that improve compliance and differentiate parity products. Cardiovascular and CNS therapies benefit most because steady plasma concentrations minimize breakthrough events and side effects. Global brand owners prioritize these approaches to defend revenue while generic challengers look to complex generics for share gains. The strategy elevates research spending on advanced coatings and barrier films that lengthen dissolution windows up to 24 hours.

Outsourcing Surge Among Virtual and Small Pharma to Specialised CDMOs

Virtual pharmaceutical companies increasingly prefer asset-light models, outsourcing development and manufacturing to partners with end-to-end capabilities. CDMOs respond with high-containment suites for oncology and hormonal compounds, single-use systems for rapid changeovers, and regulatory services that shorten the path to market authorization. India and China command an expanding share of global capacity owing to favorable cost structures and skilled labor pools. Strategic agreements now encompass joint process development, stability testing, and supply chain integration, positioning CDMOs as indispensable ecosystem players inside the oral solid dosage pharmaceutical formulation market. Ongoing consolidation, such as Novo Holdings’ purchase of Catalent, signals that scale will become even more critical.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in excipient supply chain and price spikes | -0.7% | Global with acute impact in supply-dependent regions | Short term (≤ 2 years) |

| Stringent nitrosamine and elemental-impurity regulations | -0.5% | Global, led by FDA and EMA enforcement | Medium term (2-4 years) |

| Rising competition from biologics and parenteral options | -0.6% | North America and Europe, expanding worldwide | Long term (≥ 4 years) |

| Limited harmonisation of global bioequivalence rules | -0.4% | Global with regional variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Excipient Supply Chain & Price Spikes

Raw-material shortages caused 27% of documented drug scarcities in 2024, exposing vulnerabilities in single-source supply models. Geopolitical events and pandemic disruptions have spurred price surges for critical excipients like microcrystalline cellulose and lactose. Manufacturers respond by dual-sourcing, expanding safety-stock levels, and qualifying alternative grades to secure continuity. Regulatory bodies are streamlining change-control pathways so producers can pivot suppliers without lengthy approvals. Nonetheless, near-term margin pressure is evident across the oral solid dosage pharmaceutical formulation market.

Stringent Nitrosamine & Elemental-Impurity Regulations

The FDA’s September 2024 guidance requires detailed risk assessments for both nitrosamines and drug-substance-related analogs. ICH Q3D sets daily limits for 24 toxic elements, compelling manufacturers to invest in inductively coupled plasma mass spectrometry and validated extraction methods. Compliance timelines vary by jurisdiction, creating complexity for globally distributed products. Several generic antihypertensives faced recalls after exceeding nitrosamine limits, reinforcing the financial stakes. Companies that embed impurity mitigation early in development are less likely to incur reformulation costs later in the product life cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Tablets Sustain Leadership Amid Diversification

Tablets accounted for 68.24% of the oral solid dosage pharmaceutical formulation market size in 2024. Long-established infrastructure and high-speed presses keep production costs low, while familiarity aids patient adherence. Capsules follow in popularity because they mask taste and can host multiparticulate fills. Powders and granules serve tailored dosing needs in pediatrics and geriatrics. Innovators now incorporate 3D printing to adjust geometry and porosity, which broadens therapeutic options and supports on-demand production.

Orally disintegrating films are the fastest-expanding format with a 7.36% CAGR outlook. They dissolve within two minutes, enabling buccal uptake that bypasses hepatic first-pass metabolism. Lozenges, pastilles, pellets, and mini-tablets round out the category by offering local or multi-unit delivery. Manufacturers are investing in multi-lane casting equipment to scale film capacity and meet surging demand. This diversification is likely to reshape volume mixes inside the oral solid dosage pharmaceutical formulation market during the forecast horizon.

By Release Mechanism: Immediate Release Dominates While Advanced Systems Accelerate

Immediate release products held 61.23% of the oral solid dosage pharmaceutical formulation market size in 2024 because they meet acute therapy needs and follow simple regulatory pathways. Modified release variants, including sustained and controlled release, secure chronic patient compliance by limiting dosing frequency to once daily. Enteric coatings protect acid-labile agents through the gastric environment.

Targeted and advanced delivery is growing at 8.85% CAGR on the back of 3D-printed, pH-responsive, and multi-material tablets that enable complex kinetics. Osmotic pump systems deliver zero-order release for up to 24 hours, and floating dosage forms prolong gastric residence time. Oncology developers employ microenvironment-sensitive coatings to release cytotoxics at specific intestinal loci, minimizing systemic exposure. These capabilities define premium segments within the oral solid dosage pharmaceutical formulation market.

By Therapeutic Area: Cardiovascular Dominance Faces Oncology Momentum

Cardiovascular products delivered 22.46% of 2024 revenue due to the global burden of hypertension and dyslipidemia. High generic penetration supports affordability, and reformulation strategies now center on polypills that bundle antihypertensives and statins into single tablets. Central nervous system disorders hold roughly 18% share, leveraging immediate onset demands and chronic dosing regimens.

Oncology is advancing at a 7.34% CAGR as protocols shift from infusion centers to home-based oral regimes. Multiple kinase inhibitors now launch first in capsules, emphasizing patient convenience. Gastrointestinal and metabolic segments see incremental growth through site-specific coatings and high-load metformin tablets. Collectively, shifting therapeutic priorities continue to influence the competitive balance within the oral solid dosage pharmaceutical formulation market.

By Manufacturer Type: Large Pharma Holds Scale Advantage as CDMOs Surge

Large pharmaceutical companies contributed 41.66% of the oral solid dosage pharmaceutical formulation market share in 2024. Integrated discovery-to-distribution models secure blockbuster pipelines and sustain economies of scale. Generic companies supply about 28% of global volumes, capitalizing on abbreviated approvals and cost leadership.

CDMOs, however, are tracking a 7.33% CAGR on the strength of flexible capacity, potent compound containment, and regulatory support services. Specialty and virtual firms leverage these platforms to commercialize niche therapies without fixed-asset risk. Recent megadeals, including Novo Holdings and Catalent, suggest further consolidation that could tighten capacity in high-demand categories and elevate service pricing across the oral solid dosage pharmaceutical formulation market.

Geography Analysis

North America generated 34.74% of global revenue in 2024, driven by strong research pipelines, supportive intellectual property laws, and rapid uptake of continuous manufacturing lines. The United States accounts for more than 80% of regional value owing to high per-capita medicine spending. Canada contributes specialized containment and packaging capabilities, while Mexico’s free-trade zones attract mid-scale production.

Europe remains a leading exporter of advanced formulations. Germany excels in high-speed compression machinery, and the United Kingdom anchors numerous digital health collaborations that integrate adherence monitoring. Stringent European Medicines Agency guidelines support consistent product quality and serve as reference for many emerging markets.

Asia-Pacific is the fastest-growing region at 6.74% CAGR. China and India expand active pharmaceutical ingredient and finished-dose capacity, aided by government incentives and skilled technicians. Japan and South Korea focus on high-value modified-release technologies and 3D printing. Regional harmonisation under PIC/S good manufacturing practice standards is lowering trade barriers and helping local firms capture contracts from multinational sponsors inside the oral solid dosage pharmaceutical formulation market.

Competitive Landscape

The oral solid dosage pharmaceutical formulation market exhibits moderate concentration with a dynamic mix of scale leaders and agile specialists. Top global players combine extensive portfolios with continuous manufacturing investments to safeguard margin and speed. CDMOs are expanding sterile and potent compound suites, creating capacity for oncology and hormonal pipelines.

Strategic acquisitions underscore a race for footprint. Novo Holdings paid USD 16.5 billion for Catalent, securing global tableting and capsuling lines, while Lonza purchased Roche’s Vacaville site for USD 1.2 billion to augment biologics and small molecule capabilities. Partnerships between AI formulation start-ups and heritage manufacturers further compress development timelines and spread risk.

Product differentiation now hinges on patient-centric design and data-rich process control. Firms that master rapid scale-up from lab to commercial suite gain a decisive edge. Continuous knowledge sharing between OEM equipment suppliers, excipient vendors, and formulation scientists accelerates innovation cycles across the oral solid dosage pharmaceutical formulation industry.

Oral Solid Dosage Pharmaceutical Formulation Industry Leaders

F. Hoffmann-La Roche Ltd

GSK plc.

Eli Lilly and Company

Sanofi

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Aptar CSP Technologies opened a cGMP site in New Jersey that supports clinical packaging for oral solid dose and capsule-based dry-powder inhaler products.

- February 2025: Ardena completed the acquisition of Catalent’s Somerset, New Jersey drug-product facility, expanding integrated CDMO services.

- February 2025: Jabil Inc. acquired Pharmaceutics International Inc., adding aseptic filling, lyophilization, and oral solid dose manufacturing capacity to its diversified network.

Global Oral Solid Dosage Pharmaceutical Formulation Market Report Scope

| Tablets |

| Capsules |

| Powders & Granules |

| Lozenges & Pastilles |

| Orally Disintegrating Films |

| Others (Pellets, Mini-tablets) |

| Immediate Release | |

| Modified Release | Sustained Release |

| Controlled Release | |

| Delayed / Enteric Release | |

| Targeted / Advanced Delivery (3-D printed, osmotic, etc.) |

| Oncology |

| Cardiovascular |

| CNS |

| Infectious Diseases |

| Gastrointestinal |

| Metabolic Disorders (Diabetes, Obesity) |

| Others |

| Large Pharmaceutical Companies |

| Generic Manufacturers |

| CDMOs |

| Specialty & Virtual Pharma |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Dosage Form | Tablets | |

| Capsules | ||

| Powders & Granules | ||

| Lozenges & Pastilles | ||

| Orally Disintegrating Films | ||

| Others (Pellets, Mini-tablets) | ||

| By Release Mechanism | Immediate Release | |

| Modified Release | Sustained Release | |

| Controlled Release | ||

| Delayed / Enteric Release | ||

| Targeted / Advanced Delivery (3-D printed, osmotic, etc.) | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular | ||

| CNS | ||

| Infectious Diseases | ||

| Gastrointestinal | ||

| Metabolic Disorders (Diabetes, Obesity) | ||

| Others | ||

| By Manufacturer Type | Large Pharmaceutical Companies | |

| Generic Manufacturers | ||

| CDMOs | ||

| Specialty & Virtual Pharma | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the global oral solid dosage pharmaceutical formulation market?

The market stood at USD 635.77 billion in 2025 and is projected to reach USD 795.35 billion by 2030.

Which dosage form leads global revenues?

Tablets generated 68.24% of 2024 sales, reflecting cost efficiency and patient familiarity.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 6.74% CAGR through 2030 thanks to capacity investments in China and India.

Why are CDMOs gaining share?

Virtual and small pharmaceutical firms outsource development and manufacturing to CDMOs, driving a projected 7.33% CAGR for the segment.

How is continuous manufacturing changing the sector?

Continuous lines lower cost of goods and cut development cycles from years to months while meeting stringent quality standards.

What regulatory issues are most pressing?

Nitrosamine and elemental impurity controls require advanced analytics and proactive risk assessment across supply chains.

Page last updated on: