Liquid Dietary Supplements Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

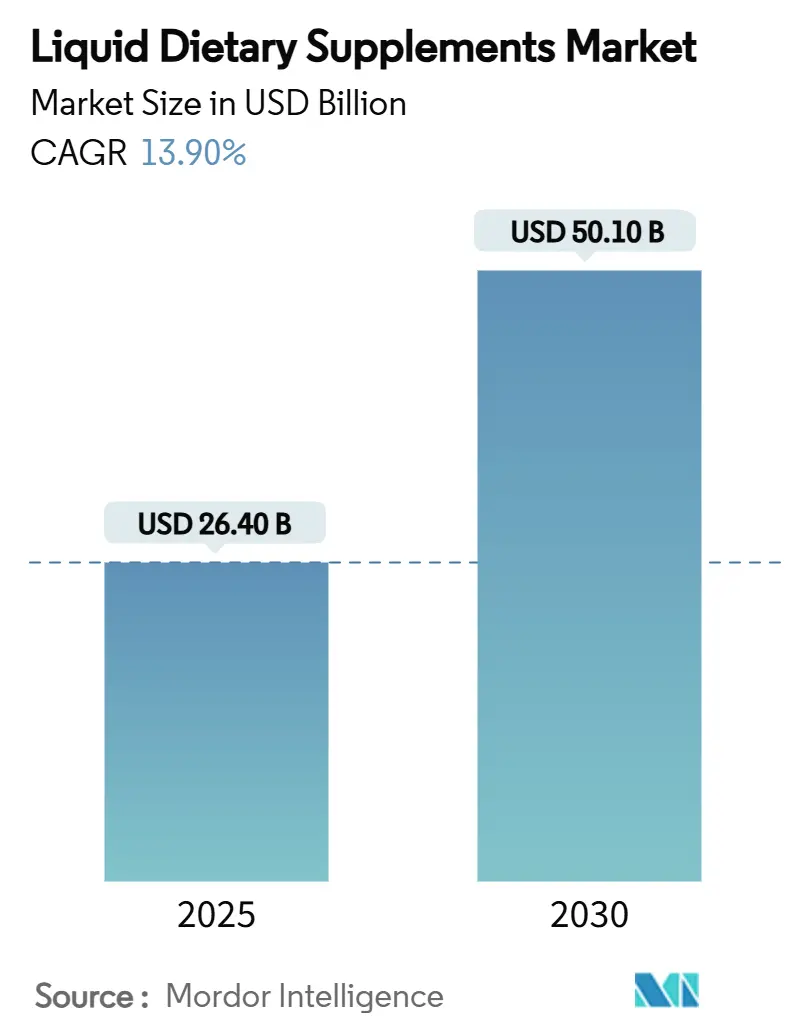

| Market Size (2025) | USD 26.40 Billion |

| Market Size (2030) | USD 50.10 Billion |

| Growth Rate (2025 - 2030) | 13.90% CAGR |

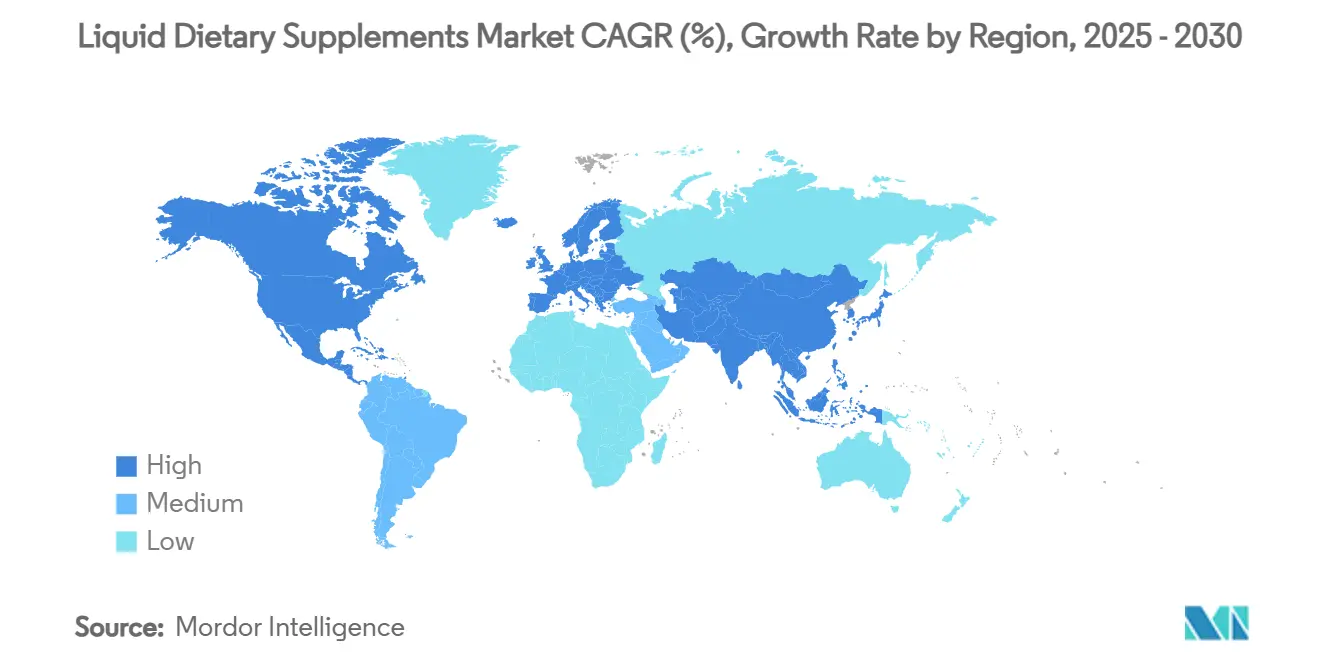

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Dietary Supplements Market Analysis by Mordor Intelligence

The liquid dietary supplements market reached a market size of USD 26.4 billion in 2025 and is forecast to expand to USD 50.1 billion by 2030 at a 13.9% CAGR, underscoring the sector’s rapid scale-up trajectory. Liposomal vitamin C demonstrates 30% higher bioavailability than non-liposomal formats. Adults increasingly favour liquid delivery systems that promise faster absorption, fueled by growing scientific validation and the convenience of ready-to-drink (RTD) formats. Omega-3 free-fatty-acid formulations now deliver measurably improved uptake even on low-fat diets, widening therapeutic potential. Direct-to-consumer (DTC) subscription models, temperature-controlled fulfilment innovations, and premium claims around cognitive, immune, and gut health collectively accelerate revenue gains within the liquid dietary supplements market. Competitive intensity rises as consumer-packaged-goods (CPG) majors acquire agile brands to enter high-growth liquid niches. At the same time, sustainability commitments on post-consumer-recycled (PCR) packaging begin to influence buyer choice.

Key Report Takeaways

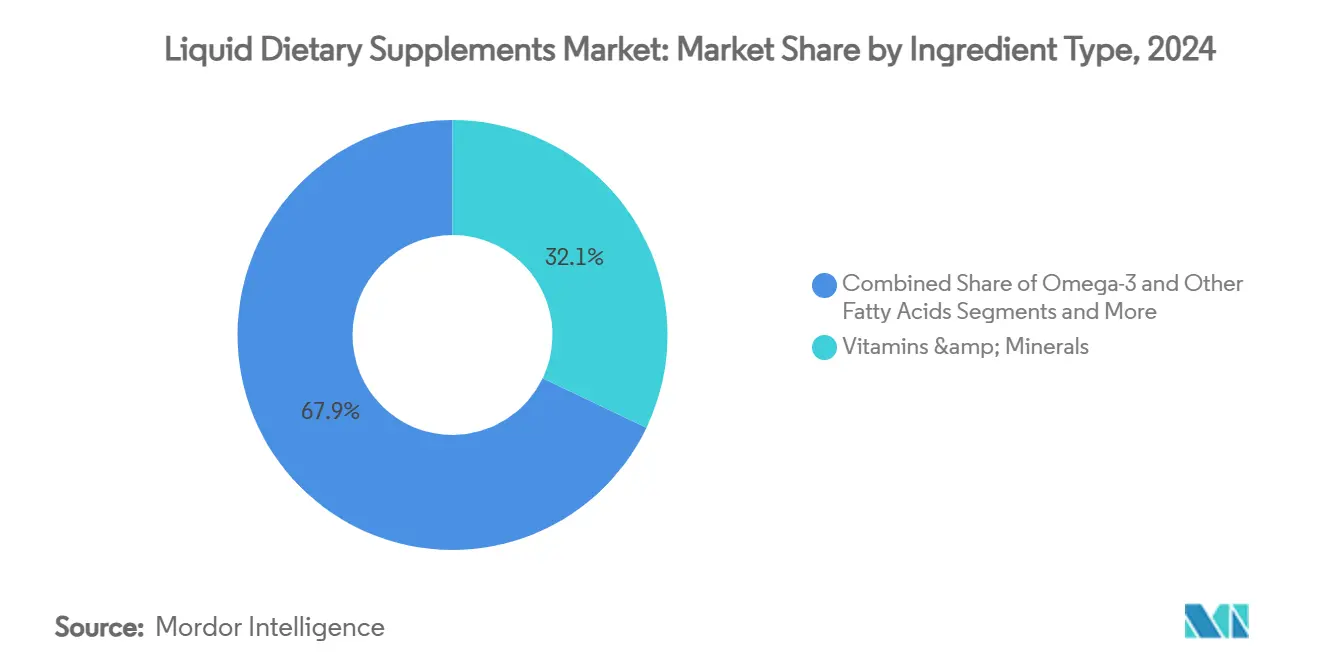

- By ingredient type, sports nutrition captured a 28.4% revenue share of the liquid dietary supplements market in 2024, and omega-3 and fatty-acids ingredients are forecast to grow at 12.6% CAGR, while vitamins and minerals maintained 32.1% liquid dietary supplements market share in 2024.

- By application, cognitive and stress-support applications are projected to expand at 11.8% CAGR, outpacing all other functional categories within the liquid dietary supplements market.

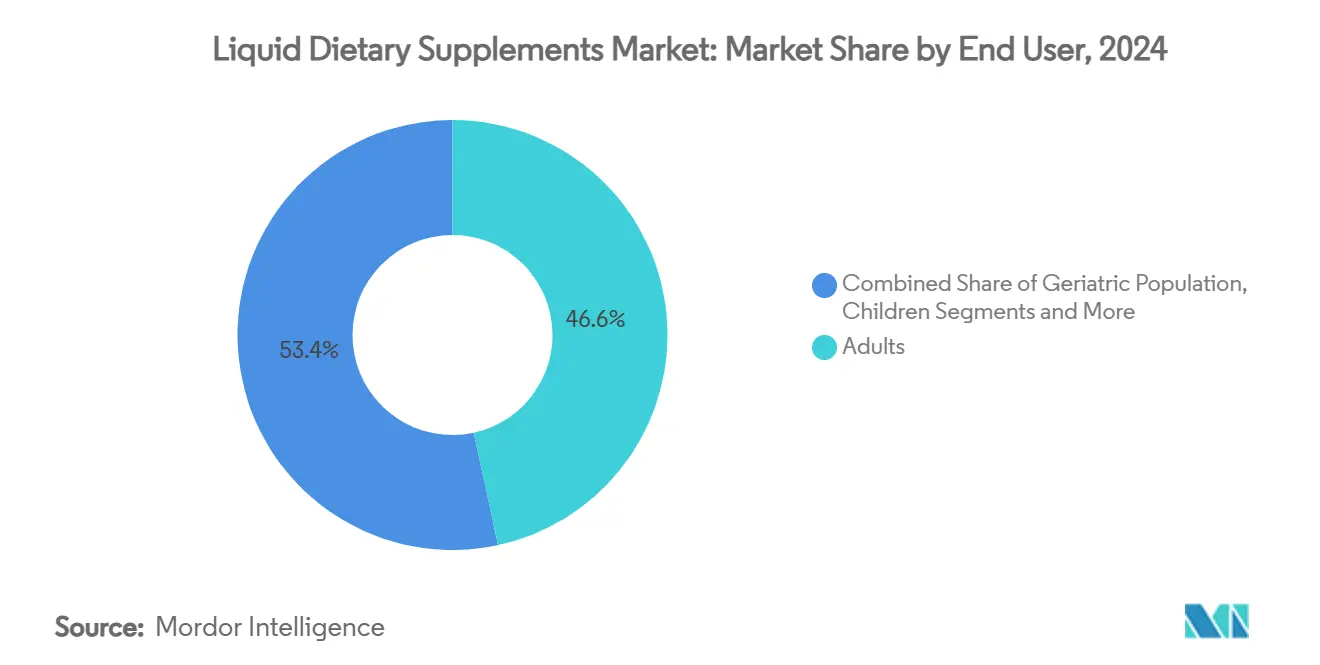

- By end user, pregnant and lactating women represent the fastest-rising end-user cohort, with a 9.9% CAGR, overtaking the broader adult segment’s 46.6% base share by 2030.

- By distribution channel, online retail channels are recording 14.5% CAGR, narrowing the gap with super/hypermarkets that held 41.8% channel share in 2024.

- Geographically, Asia Pacific is set to post the quickest regional expansion at 7.5% CAGR, contrasting North America’s 34.5% lead in 2024 liquid dietary supplements market share.

Global Liquid Dietary Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-Population Driven Preventive Health Focus | +3.20% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Surge In E-Commerce & DTC Liquid Formats | +2.80% | Global, led by North America & APAC | Medium term (2-4 years) |

| Superior Bio-Availability Versus Pills | +2.10% | Global | Medium term (2-4 years) |

| Sports-Nutrition Demand For RTD Shots | +1.90% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Smart Single-Dose Pouch Innovation | +1.50% | Global, early adoption in North America | Medium term (2-4 years) |

| AI-Powered Personalised On-Site Blending Kiosks | +1.20% | North America & Europe pilot markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing-Population Driven Preventive Health Focus

Rapid growth in the global 65+ population transforms product demand as older adults look to nutrition to preserve mobility and immune resilience. Abbott’s Ensure surpassed USD 3 billion in global liquid sales in 2024, showing strong uptake among seniors who find swallowing large tablets difficult. Liquid formulations enable higher nutrient density per dose, assist dysphagia management, and lower gastrointestinal irritation compared with compressed pills. Consumers also perceive liquid formats as more “medical-grade,” encouraging routine usage alongside healthcare-provider recommendations. Sustained purchasing power among baby boomers and a cultural shift toward proactive, rather than reactive, care create multi-year tailwinds for the liquid dietary supplements market. Industry players therefore prioritise portfolio extensions that address sarcopenia, bone density, and immune function, positioning liquid products as essential daily tools rather than optional accessories.

Surge In E-Commerce & DTC Liquid Formats

Digital channels reshape route-to-market economics by compressing traditional retail mark-ups and enabling data-driven personalization. Online sales within the liquid dietary supplements market are trending at 14.5% CAGR, buoyed by subscription models that align perfectly with daily dosing habits. Fulfilment specialist Stord’s 2024 acquisition of temperature-controlled operator ProPack exemplifies investment into cold-chain infrastructures critical for shelf-stable delivery. Direct communication about bioavailability and ingredient provenance strengthens brand loyalty, while AI-powered recommender tools raise cross-sell conversions. DTC brands further capture premium positioning by bundling lab-testing kits, personalized dashboards, and auto-refill services that elevate perceived value and lock in recurring revenue streams.

Superior Bio-Availability Versus Pills

Peer-reviewed studies confirm that liposomal vitamin C provides 30% higher plasma concentrations than standard tablets, and free-fatty-acid omega-3 formats significantly outperform ethyl-ester versions in low-fat conditions.[1]Cong L., “Functional Beverages in Asia Pacific,” Beverages, mdpi.com Liquid delivery circumvents disintegration delays, allowing immediate absorption and less nutrient degradation through first-pass metabolism. Clinicians now recommend liquid B12 for patients on proton-pump inhibitors that impede intrinsic-factor activity, reinforcing therapeutic credibility within the liquid dietary supplements market. Bioavailability proof points support higher pricing, help products migrate from general-wellness positioning into quasi-clinical use cases, and set new product-development benchmarks for encapsulation, micellization, and nano-emulsion technologies.

Sports-Nutrition Demand for RTD Shots

RTD functional shots fit modern, on-the-go lifestyles for both elite athletes and time-pressed consumers. Segment revenues are climbing 16.1% annually, eclipsing powder-based sports formulas. Compact 60-millilitre formats deliver concentrated amino acids, electrolytes, or adaptogens without shaker bottles, eliminating texture objections that deter mainstream users. Manufacturers capitalize on premium per-unit pricing and lower shipping weights relative to large PET bottles. Convenience-centric packaging in aluminium or PCR PET lines up with consumers’ interest in sustainability, while smart QR-coded labels extend engagement through training tips and loyalty programmes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Cross-Border Labelling Regulations | -1.80% | Global, particularly EU-US-APAC trade | Medium term (2-4 years) |

| Shorter Shelf-Life & Cold-Chain Needs | -1.40% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Counterfeit Risk On Crypto-Enabled Grey Channels | -1.10% | Global, concentrated in online marketplaces | Medium term (2-4 years) |

| Sustainability Backlash On PET Bottles | -0.90% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Cross-Border Labelling Regulations

Varying definitions and permitted claims force companies to maintain separate stock-keeping units for each market. FDA guidance distinguishes liquid dietary supplements from beverages and triggers distinct nutrient-content and structure-function claim requirements.[2]Food and Drug Administration, “Guidance on Distinguishing Liquid Dietary Supplements from Beverages,” fda.govThe European Union’s 2022 plastics regulation adds fresh documentation for recycled-content containers, complicating sustainable packaging rollouts. Non-alignment slows speed-to-market, raises compliance costs, and intensifies reliance on expert regulatory affairs teams. Smaller DTC entrants thus face disproportionate hurdles, reinforcing the importance of strategic partnerships and region-specific labelling automation tools.

Shorter Shelf-Life & Cold-Chain Needs

Many liquid blends demand refrigeration or controlled ambient storage to protect labile nutrients such as probiotics and emulsified omega-3 oils. Any temperature excursion risks potency loss and mandatory recalls, with NSF warning that improper warehousing can breach product-label claims.[3]NSF, “Dietary Supplement Storage Issues: Temperature Control,” nsf.org Emerging markets often lack robust cold-chain networks, inflating logistics costs and limiting penetration. Shelf-life stability-testing protocols further extend research timelines and add capital expenditure for pilot-scale runs. Brands therefore invest in aseptic processing, high-pressure pasteurization, and oxygen-scavenging closures to extend ambient viability while preserving sensory qualities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Omega-3 Innovation Drives Premium Growth

Omega-3 and fatty-acid formulations are forecast to compound at 12.6% annually, outpacing vitamins and minerals, which retain 32.1% of the liquid dietary supplements market share in 2024. The liquid dietary supplements market size for omega-3 products is projected to reach USD 8.9 billion by 2030, assisted by innovations in micro-emulsion and algal-sourced oils. Free-fatty-acid structures achieve superior absorption on low-fat diets and provide science-based marketing claims around cardiovascular, cognitive, and prenatal health. Botanical extracts, including curcumin and ashwagandha, gain shelf presence via advanced solubilization aids that mitigate sediment and flavor challenges. Meanwhile, probiotics gain traction as encapsulation technologies keep colony-forming units viable without refrigeration, expanding functional synergy opportunities.

The premiumization trend allows producers to command gross margins above 55%, especially when layering clean-label positioning and third-party testing seals. Regulatory scrutiny on omega-3 claims remains strict, yet well-conducted clinical trials and pharmaceutical-grade manufacturing open reimbursement pathways in select geographies. Ingredient diversification ultimately supports risk mitigation for brands previously over-indexed on core vitamins, ensuring top-line stability while feeding consumer appetite for targeted, science-backed benefits in the liquid dietary supplements market.

By Application: Cognitive Health Emerges as Premium Category

Sports nutrition delivered 28.4% of total 2024 revenues, aided by RTD formats that appeal to both endurance athletes and casual gym-goers. However, cognitive and stress-support liquids are advancing 11.8% annually, the fastest clip among all functional areas. The liquid dietary supplements market size for cognition is forecast to top USD 6.4 billion by 2030 as nootropic beverages post 16% CAGR. Gaming communities, corporate wellness programmes, and ageing consumers worried about memory decline all amplify demand.

Immune-health tonics containing zinc, vitamin D, and elderberry maintain baseline volume, particularly during winter seasons. Digestive-health shots featuring synbiotics address bloating and microbiome wellbeing, with on-pack QR codes linking to personalized gut-health dashboards. Application diversification lowers seasonality risk while enabling brands to spin off focused sub-lines supported by condition-specific advertising, influencer partnerships, and healthcare-professional endorsements.

By End User: Pregnant Women Drive Specialized Growth

Adults contributed 46.6% of liquid dietary supplements market revenue in 2024, yet pregnant and lactating women are growing 9.9% annually amid heightened awareness of prenatal micronutrient adequacy. Research reveals that many tablet-based prenatal formulations under-deliver on key vitamins, driving interest in liquid alternatives that simplify dosing compliance. Liquid prenatal lines employ methylated folate, chelated iron, and gentle flavors to mitigate nausea, supporting premium price points and repeat purchases through trimester-based bundles.

Pediatric formats benefit from taste-masking capabilities and pipette-style droppers that allow precise milligram dosing. Geriatric consumers appreciate easy-to-swallow textures and joint-support blends combining collagen and vitamin K2. End-user segmentation thus informs packaging ergonomics, flavour palette development, and channel strategy—pharmacies for prenatal, e-commerce for adult everyday wellness, and institutional care networks for older-adult medical nutrition.

By Distribution Channel: Digital Transformation Accelerates

Super/hypermarkets held 41.8% distribution share in 2024, yet online retail volumes are compounding 14.5% per year. The liquid dietary supplements market size flowing through DTC portals is set to exceed USD 15 billion by 2030. Subscription programmes leverage AI to adjust replenishment cycles and recommend add-on products, boosting customer lifetime value while reducing churn. Pharmacies sustain relevance for therapeutic lines such as liquid iron or high-dose vitamin D, given pharmacist trust and reimbursement pathways.

Specialty vitamin shops cultivate experiential merchandising with on-site sampling of single-dose pouches and dispenser bars. Convenience stores test ambient-stable energy shots near checkout zones, capturing impulse demand. Multi-level-marketing networks fallback on social-commerce integrations that allow live-video product demonstrations and peer-recommendation loops. Channel blend complexity compels brands to optimize pack sizes, temperature-control protocols and messaging to fit each retail environment seamlessly.

Geography Analysis

North America generated 34.5% of global turnover in 2024, led by established supplement adoption and fertile venture funding for DTC disruptors. Asia Pacific, posting a 7.5% CAGR, is gaining ground thanks to a USD 36 billion functional-beverage ecosystem that primes consumer familiarity with drinkable nutrition.

China, Japan, and South Korea push boundaries in beauty-from-within collagen waters and ginseng tonics, while India’s Ayurveda-infused shots marry tradition with modern convenience. The liquid dietary supplements market size in Asia Pacific is expected to reach USD 12.7 billion by 2030 as urban middle classes prioritise preventive wellness.

Europe emphasizes traceability and recyclability, accelerating adoption of PCR PET and tinted-glass bottles. Middle East & Africa open pharmacy-centric routes for diabetic and bone-health liquids, though cold-chain gaps persist. South America’s economic recovery encourages functional juice blends fortified with regional botanicals such as acerola and guarana. Local palate preferences oblige global brands to tailor sweetness profiles, flavor carriers, and pack dimensions, ensuring mouthfeel and shelf-life meet regional norms without eroding global brand equity.

Competitive Landscape

Market fragmentation persists despite a handful of multinationals holding double-digit positions. Abbott controls the single-largest slice through Ensure, Glucerna, and Protality, while Herbalife’s 2025 acquisitions of Pro2col Health and Pruvit Ventures signal strategic intent to bring personalized liquid ketone and amino-acid lines under one roof. MaryRuth’s Organics scaled from USD 165 million in 2022 to a projected USD 300 million in 2023 on an organic, family-friendly platform that resonates on Amazon and its own webstore.

Innovation increasingly revolves around delivery technology and sustainability. Unilever injected capital into Liquid IV manufacturing to secure supply capacity for electrolyte hydration blends. Amcor’s 100% PCR PET bottle for Ritual multivitamins demonstrates packaging leadership, catering to consumer eco-pressure while maintaining clarity for vibrant liquid hues. Berry Global follows ClariPPil moisture-barrier bottles validated by RecyClass A certification, signaling collective industry movement toward circular-economy targets.

Digital authenticity tools emerge as competitive differentiators; blockchain tracing and tamper-evident NFC seals help combat USD 600 billion in counterfeit losses across nutrition and cosmetics. Patent filings around vending kiosks capable of on-demand micronutrient blending underscore future possibilities for hyper-personalized sales points in malls, airports, and gyms. As consolidation continues, the liquid dietary supplements industry witnesses more cross-border deals that fuse R&D pipelines, regional distribution licenses, and digital-commerce assets into vertically integrated ecosystems.

Liquid Dietary Supplements Industry Leaders

Abbott Laboratories

Herbalife Nutrition

Amway (Nutrilite)

Bayer AG

Nestlé Health Science

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Herbalife completed strategic acquisitions of Pro2col Health LLC and Pruvit Ventures to enhance personalized nutrition capabilities.

- March 2025: Unilever invested in Liquid IV beverage-brand production facilities, signalling large-scale functional hydration ambitions.

- March 2025: New Chapter launched a Liquid Multivitamin with 22 essentials, packaged in 100% PCR plastic and priced at USD 48 for 30 oz

- October 2024: dōTERRA rolled out VMG+ Whole-Food Nutrient Complex, uniting amla and moringa in a foundational drink.

Global Liquid Dietary Supplements Market Report Scope

| Vitamins & Minerals |

| Botanicals/Herbals |

| Proteins & Amino Acids |

| Omega-3 & Other Fatty Acids |

| Others |

| Sports Nutrition |

| Immune Health |

| Weight Management |

| Digestive & Gut Health |

| Others |

| Adults |

| Geriatric Population |

| Children |

| Pregnant & Lactating Women |

| Others |

| Supermarkets / Hypermarkets |

| Pharmacies & Drugstores |

| Online Retail & DTC |

| Specialty Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Ingredient Type | Vitamins & Minerals | |

| Botanicals/Herbals | ||

| Proteins & Amino Acids | ||

| Omega-3 & Other Fatty Acids | ||

| Others | ||

| By Application | Sports Nutrition | |

| Immune Health | ||

| Weight Management | ||

| Digestive & Gut Health | ||

| Others | ||

| By End User | Adults | |

| Geriatric Population | ||

| Children | ||

| Pregnant & Lactating Women | ||

| Others | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Pharmacies & Drugstores | ||

| Online Retail & DTC | ||

| Specialty Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current liquid dietary supplements market size and its expected growth rate?

The liquid dietary supplements market size stands at USD 26 billion in 2025 and is projected to hit USD 50.1 billion by 2030, reflecting a 13.9% CAGR.

Which application area is expanding fastest within the liquid dietary supplements market?

Cognitive and stress-support liquids are forecast to grow at 11.8% CAGR through 2030, outpacing sports nutrition and immune health.

Why are liquid supplements perceived as more effective than pills?

Clinical studies show liposomal or emulsified nutrients deliver superior plasma concentrations—up to 30% higher for vitamin C—because liquids bypass disintegration delays and enhance absorption.

Which region is leading growth momentum?

Asia Pacific is the fastest-growing region, expected to post 7.5% CAGR, fuelled by rising preventive-health awareness and a USD 36 billion functional-beverage ecosystem.

How significant is e-commerce to market expansion?

Online sales are advancing at 14.5% CAGR as DTC brands leverage temperature-controlled fulfilment and subscription models that fit daily dosing habits.

What packaging innovations are addressing sustainability concerns?

Players such as Amcor and Berry Global introduced 100% PCR PET and fully recyclable high-barrier bottles that maintain product integrity while meeting environmental goals.

Page last updated on: