Compounding Pharmacy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.78 Billion |

| Market Size (2031) | USD 22.08 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

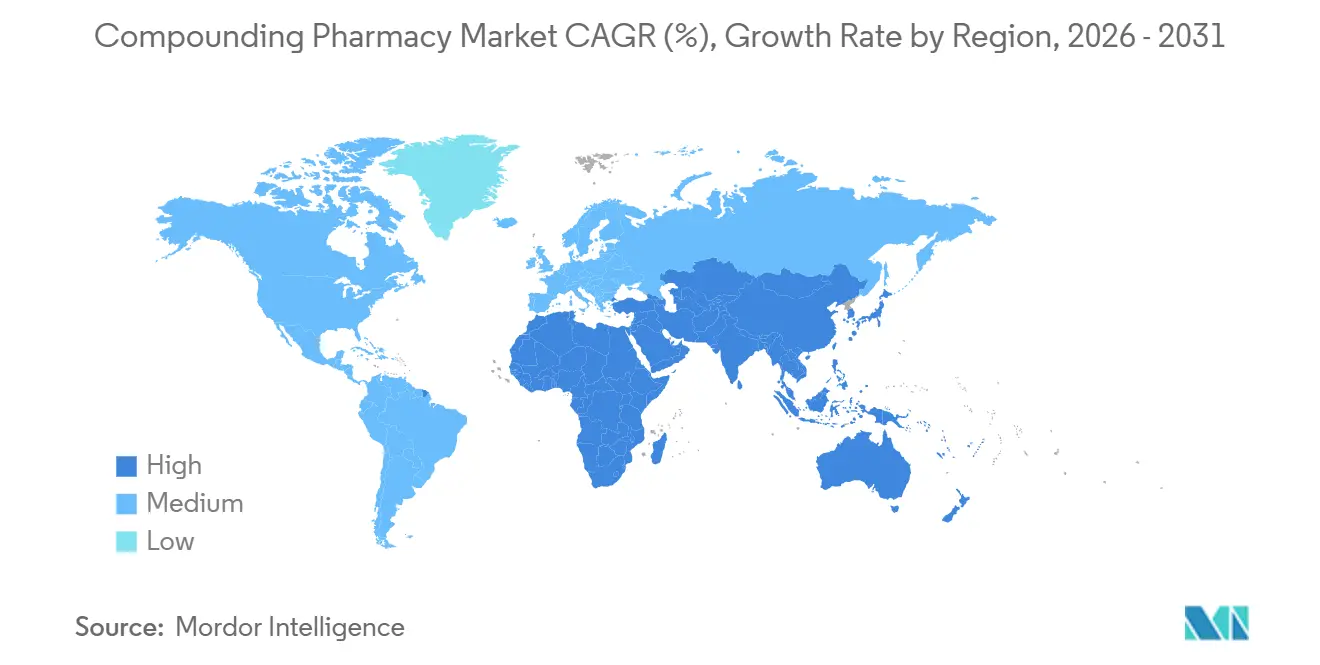

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

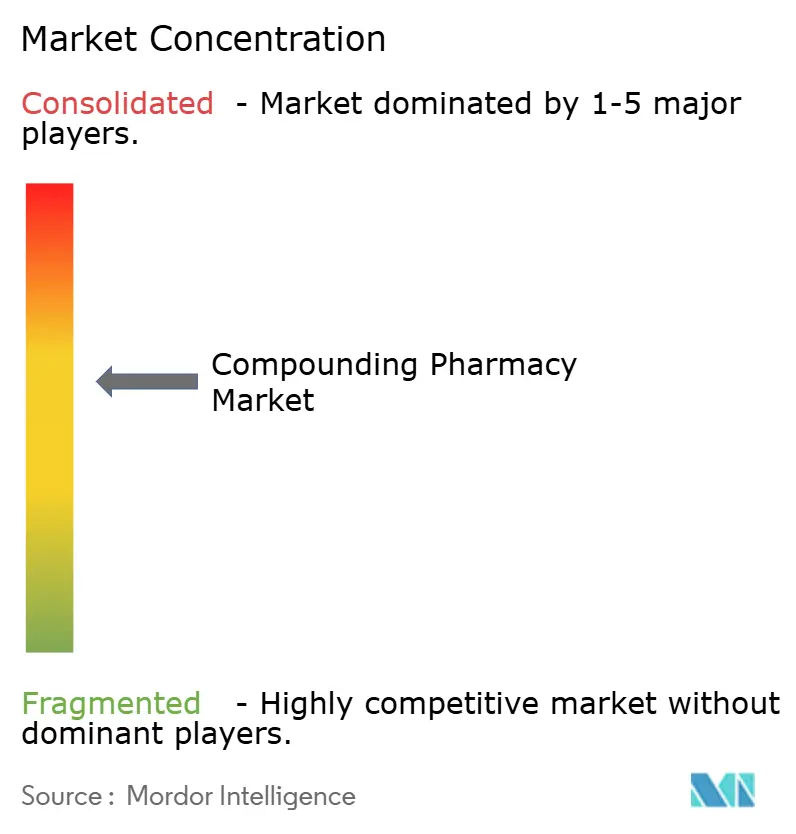

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compounding Pharmacy Market Analysis by Mordor Intelligence

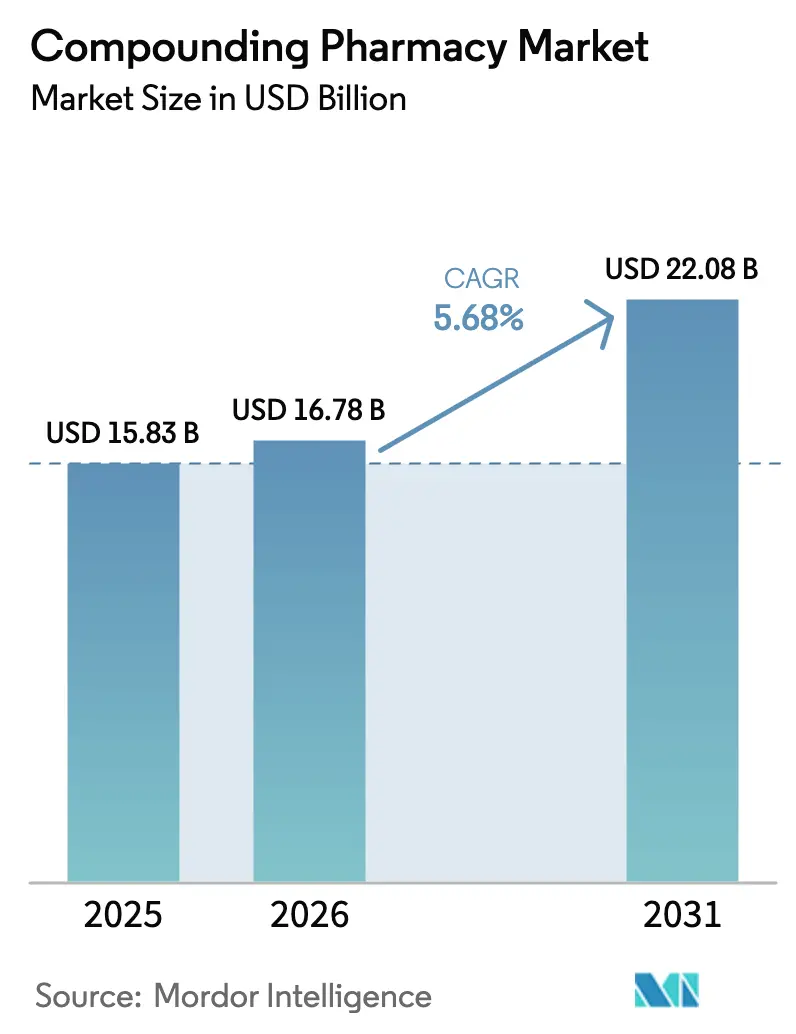

The Compounding Pharmacy Market size is expected to grow from USD 15.83 billion in 2025 to USD 16.78 billion in 2026 and is forecast to reach USD 22.08 billion by 2031 at 5.68% CAGR over 2026-2031.

Persistent drug shortages, wider acceptance of personalized medicine, and regulatory support for outsourcing have elevated compounded preparations from fringe solutions to essential components of hospital formularies. Health systems now formalize long-term supply contracts with 503B facilities to mitigate supply chain shocks, while capital-rich manufacturers view compounding as a strategic insurance against production lapses. Demand is strongest for sterile admixtures, bioidentical hormone therapy, and pediatric‐friendly formats that commercial producers overlook. The adult chronic-disease base remains dominant; yet, rapid growth in pediatric and veterinary markets underscores how customization imperatives broaden the addressable population for the compounding pharmacy market. Competition is intensifying as extensive outsourcing facilities consolidate capacity and integrate robotic technologies that cut contamination risk by more than 95%.

Key Report Takeaways

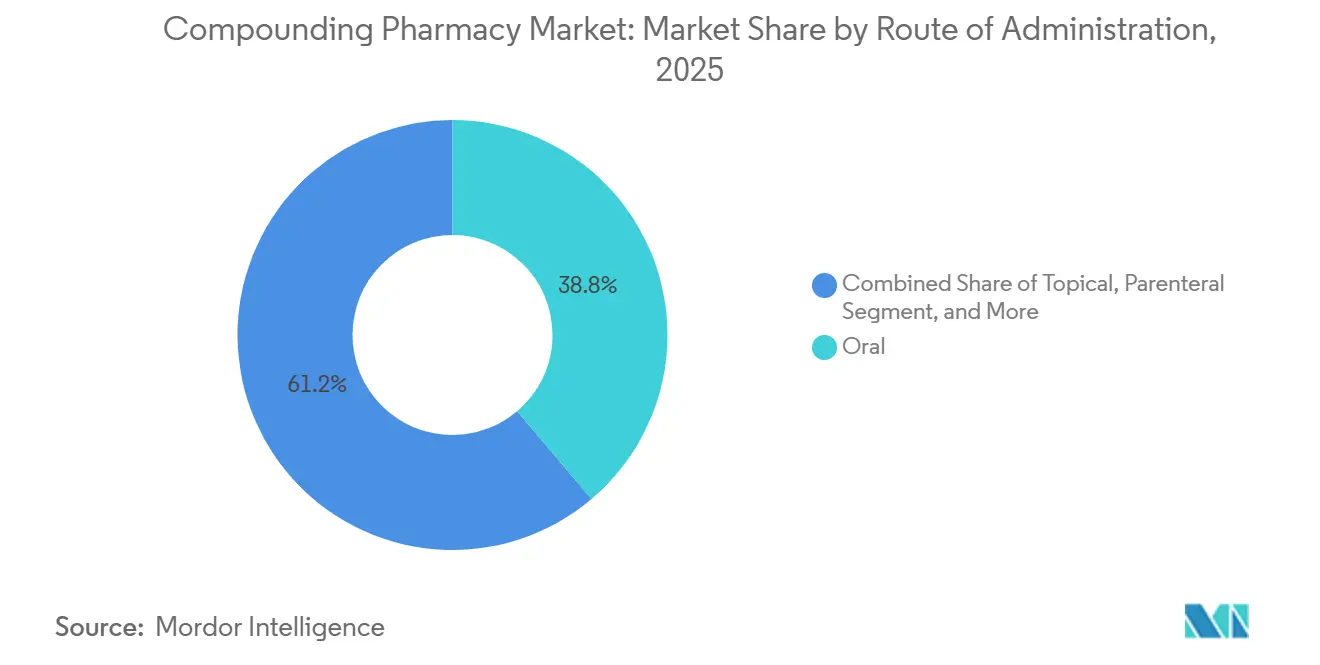

- By route of administration, oral formulations led with 38.81% revenue share in 2025; parenteral preparations are forecast to expand at a 7.38% CAGR through 2031.

- By therapeutic area, pain management accounted for 31.23% of the compounding pharmacy market share in 2025, while hormone replacement therapy is projected to grow at the fastest rate, with a 7.86% CAGR, from 2026 to 2031.

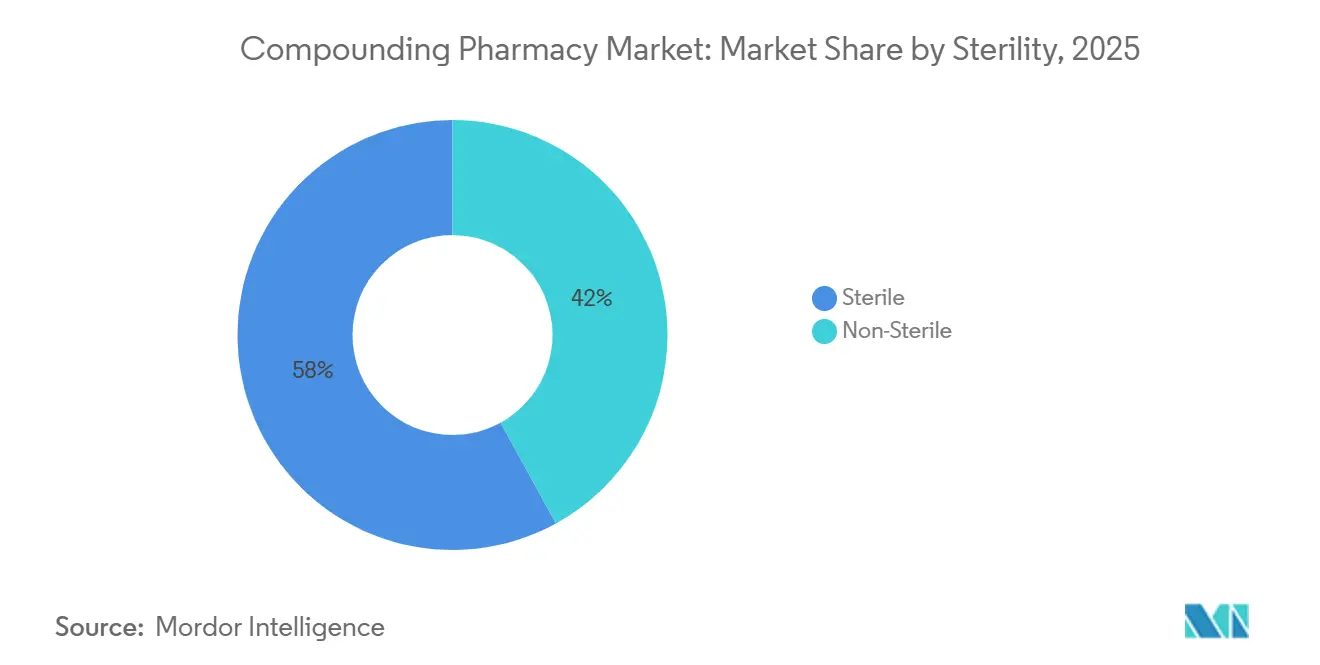

- By sterility, sterile products accounted for 57.98% of the compounding pharmacy market size in 2025; non-sterile formulations are set to grow at a 6.45% CAGR through 2031.

- By age group, adults dominated with a 48.26% share in 2025; pediatric preparations are expected to advance at a 7.66% CAGR to 2031.

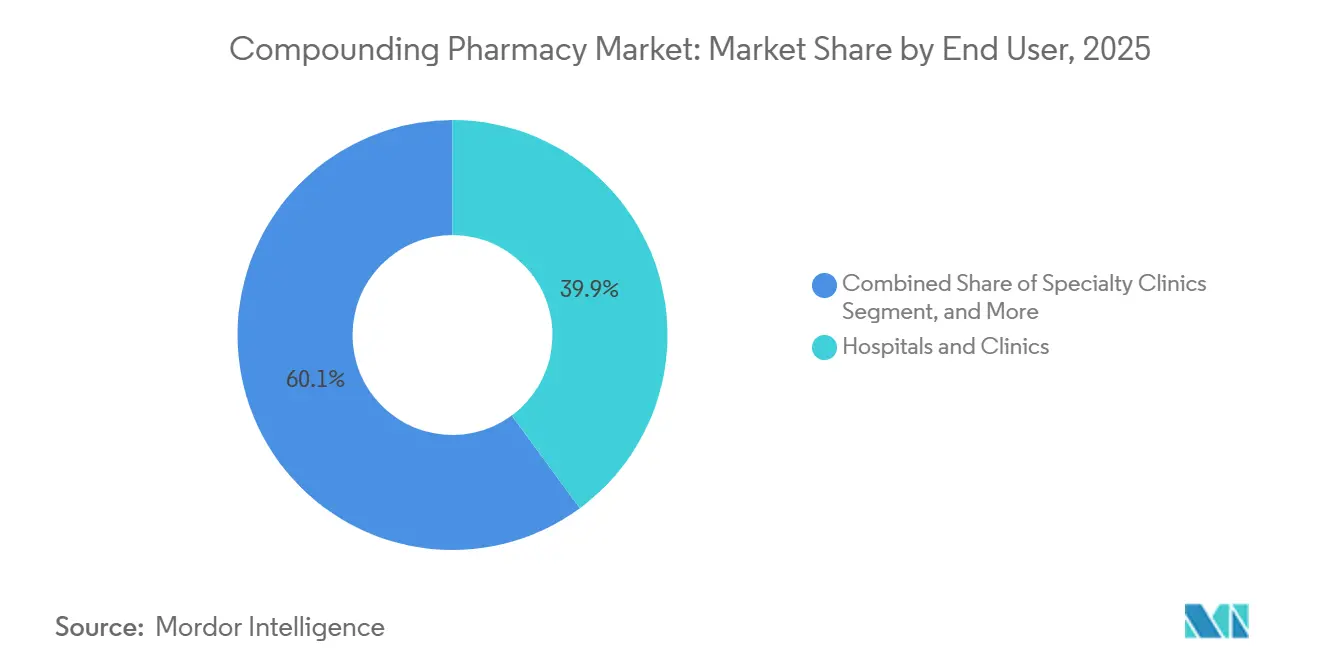

- By end user, hospitals and clinics captured a 39.94% share in 2025, whereas specialty clinics are registering the strongest 8.42% CAGR through 2031.

- By geography, North America dominated the compounding pharmacy market with a 37.44% share in 2025; the Asia-Pacific region recorded the fastest growth at a 9.26% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Compounding Pharmacy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising drug-shortage frequency | +1.0% | United States, Canada, Western Europe | Medium term (2-4 years) |

| Growing demand for personalized doses | +1.2% | North America, Europe, urban Asia-Pacific | Long term (≥4 years) |

| Expansion of 503B outsourcing facilities | +1.1% | North America, Australia, Japan | Medium term (2-4 years) |

| Uptake of sterile automated compounding technologies | +0.7% | North America, Western Europe, China, India | Medium term (2-4 years) |

| Consumer-led bioidentical hormone therapy boom | +0.8% | North America, UK, Germany, Australia | Short term (≤2 years) |

| Large-scale compounding of GLP-1 agonists | +0.6% | United States, Canada, select EU | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Drug-Shortage Frequency

The FDA reported 113 active shortages in 2024, with 15 new listings despite 283 averts, underscoring the structural fragility of the supply chain.[1]U.S. Food & Drug Administration, “Guidance for Industry #256,” FDA.GOV Hospitals responded by pre-stocking compounded substitutes for oncology analgesics, anesthetics, and parenteral nutrition, transforming 503B partners into critical infrastructure. Longer shortage durations often stretching 18–24 months have spurred multi-hundred-million-dollar investments by manufacturers that now seek end-to-end control of both commercial and compounded output. These dynamics anchor a positive feedback loop for the compounding pharmacy market, where rising baseline demand sustains factory-scale sterile capacity and continuous quality upgrades.

Large-Scale Compounding of GLP-1 Agonists Amid Obesity-Drug Gaps

When commercial supplies of semaglutide and tirzepatide tightened in 2024, compounders filled the vacuum under drug-shortage exemptions, scaling robotic filling lines that later repurposed to other injectables once enforcement resumed. Although revenue from GLP-1 copies is receding, the episode validated the sector’s agility, prompting payers and integrated delivery networks to view compounders as rapid-response buffers for future blockbuster gaps. The equipment and quality-system upgrades implemented during the GLP-1 surge now enhance throughput for oncology biologics and critical-care infusions, reinforcing long-term growth prospects for the compounding pharmacy market.

Growing Demand for Personalized Doses & Dosage Forms

Children with epilepsy, seniors with dysphagia, and pets needing palatable drugs all benefit from dosage forms that commercial lines ignore. The American Society for Parenteral and Enteral Nutrition notes that home TPN costs can reach USD 200 per day, magnifying the clinical and economic value of precise, individualized admixtures.[2]American Society for Parenteral and Enteral Nutrition, “Clinical Guidelines: Nutrition Support Therapy,” NUTRITIONCARE.ORG Pediatric demand alone is rising at a 7.66% CAGR as caregivers seek allergen-free, dye-free suspensions that improve adherence. Veterinary prescriptions are also increasing, as FDA Guidance #256 limits office stock, redirecting veterinarians to patient-specific scripts. This long-tail spectrum of low-volume, high-margin needs secures a durable niche for the compounding pharmacy market.

Expansion of 503B Outsourcing Facilities for Hospital Supply

Fagron’s EUR 70 million investment in Wichita and Nephron’s USD 350 million build-out in South Carolina exemplify the shift from regional to national sterile compounding footprints. Because 503B sites may batch without individual prescriptions, hospitals treat them like conventional drug manufacturing facilities, thereby reducing in-house liability while meeting USP 797 mandates. Consolidation follows naturally, as larger operators spread compliance costs across a higher volume of output. For the compounding pharmacy market, this fuels scale efficiencies, accelerates technology adoption, and increases purchaser confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating FDA & USP compliance costs | −0.8% | United States, Canada, EU | Medium term (2-4 years) |

| PBM steering limiting independent pharmacy access | −0.5% | United States | Short term (≤2 years) |

| API supply bottlenecks for specialty actives | −0.4% | Global | Medium term (2-4 years) |

| Rising insurer refusal to reimburse compounded scripts | −0.6% | United States, UK, Germany | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Escalating FDA & USP Compliance Costs

Revised USP 797 and 800 rules, effective 2024, forced upgrades to ISO-classified cleanrooms, environmental monitoring, and staff training, raising capital thresholds well beyond the reach of many independents. Fresenius Kabi invested USD 90 million in Wilson, North Carolina, and B. Braun allotted USD 70 million to its Pennsylvania plant to stay compliant. Heightened FDA inspection cadence, quarterly for 503B sites, adds further operating expense. While patient safety improves, a shrinking number of suppliers risks deepening shortages and dampening growth momentum for the compounding pharmacy market.

Rising Insurer Refusal to Reimburse Compounded Prescriptions

Pharmacy benefit managers such as Express Scripts and OptumRx apply stricter prior authorization, citing limited clinical data for compounded alternatives. The American College of Obstetricians and Gynecologists has questioned the consistency of compounded bioidentical hormone dosing, reinforcing payer skepticism.[3]American College of Obstetricians and Gynecologists, “Compounded Bioidentical Menopausal Hormone Therapy,” ACOG.ORG Patients must shoulder out-of-pocket costs, skewing demand toward wealthier demographics. Retail-focused 503A pharmacies feel the squeeze most acutely, tempering what would otherwise be a robust expansion of the compounding pharmacy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Parenteral Growth Outpaces Oral Dominance

The oral formulation segment accounted for 38.81% of the compounding pharmacy market size in 2025, reflecting its primacy in inpatient oncology, ICU, and surgical support. Hospital outsourcing to 503B partners, coupled with the widespread adoption of automated compounding devices, drives a 7.38% forecast CAGR for parenteral preparations. Oral formats retain leadership in chronic outpatient therapy but face slower 4% growth trajectories as commercial producers broaden their dose-strength lines. Demand for nasal sprays and sublingual troches is increasing in applications related to allergies and hormonal disorders. Yet, parenteral gains illustrate how sterility and precision tilt revenue toward high-complexity service providers within the compounding pharmacy market.

The American Society for Parenteral and Enteral Nutrition attributes lower sepsis rates to the use of closed-system parenteral nutrition, reinforcing the clinical preference for outsourced admixtures. Pediatric hospitals use flavored oral suspensions to enhance adherence, while veterinary prescribers choose transdermal gels to improve feline compliance. Nonetheless, capital-intensive parenteral workflows concentrate volume among fewer players, raising barriers for new entrants and cementing the segment’s influence over overall compounding pharmacy market share.

By Therapeutic Area: Hormone Therapy Accelerates After Regulatory Shift

Pain management generated 31.23% of 2025 revenue, banking on compounded topical analgesics that blend NSAIDs with anesthetics for opioid-averse patients. However, hormone replacement therapy is poised to deliver the fastest 7.86% CAGR, buoyed by the FDA’s label revision that removed boxed warnings and normalized customized estrogen-progesterone regimens. Canadian data cite 92 recorded hormone shortages since 2017, underscoring a chronic supply imbalance that funnels patients to compounders.

Dermatology follows close behind, driven by compounding’s ability to formulate patient-specific corticosteroid strengths and hydroquinone combinations. Oncology admixtures represent a lower-volume but higher-margin niche abetted by robotic aseptic lines. Pediatric and veterinary care is tailored via weight-based dosing and flavor customization, while nutritional supplements for metabolic disorders carve out a small but defensible niche within the compounding pharmacy industry.

By Sterility: Non-Sterile Uptick Parallels Topical and Veterinary Demand

Sterile products dominated with 57.98% of 2025 revenue, yet non-sterile lines are slated for a 6.45% CAGR through 2031 as dermal and veterinary scripts proliferate. Hazardous non-sterile items, such as hormone creams governed by USP 800, require exhaust hoods and PPE but fall short of cleanroom investments, making them an appealing option for community pharmacies. Lower regulatory barriers, quicker turnaround, and insurer leniency on topical coverage elevate the growth curve of non-sterile products, steering segment opportunities toward smaller operators still active in the compounding pharmacy market.

Health systems are increasingly outsourcing high-risk, sterile production to 503B sites to avoid infrastructure expenditures, while retaining low-risk sterile and non-sterile preparations in-house. This split assignment reallocates revenue and underpins stable demand for both sterile experts and nimble local pharmacies. Regulatory harmonization in Europe, as outlined in EMA Annex 1, aligns with U.S. sterility standards, directing capital toward larger facilities that can amortize compliance costs.

By Age Group: Pediatric Customization Spurs Outsized Growth

Adults still command 48.26% of 2025 value, spanning chronic pain, HRT, and oncology maintenance. Pediatric prescriptions, although smaller in absolute dollars, expand at a robust 7.66% CAGR as parents seek dye-free, allergen-free options and precise dosing increments that are not achievable with mass-manufactured drugs. Many insurers authorize compounded pediatric formulations when commercial equivalents lack approved weight-based strengths, easing reimbursement barriers.

Specialty compounders compile stability data libraries for pediatric suspensions, positioning themselves as indispensable partners to children’s hospitals. Geriatric scripts, hampered by stricter PBM oversight, grow more modestly but still benefit from liquid re-formulations aiding dysphagia management. These demographic contrasts diversify revenue streams and buffer the compounding pharmacy market against payer or regulatory shocks targeting any single patient group.

By End User: Specialty Clinics Gain the Fast Lane

Hospitals and integrated delivery networks represented 39.94% of the 2025 demand; however, perpetual USP audits and staffing constraints are expected to encourage further outsourcing. Specialty clinics, dermatology, endocrinology, and veterinary, post the highest 8.42% CAGR by leveraging customized products as patient-retention tools. Dermatologists compound hydroquinone-tretinoin blends tailored to individual Fitzpatrick scores, while hormone clinics deliver titratable troches following laboratory monitoring.

Veterinary practices utilize flavored liquids and transdermal gels to address dosing challenges in cats and dogs, thereby gaining client loyalty despite higher per-dose costs. Retail community pharmacies confront PBM steering toward branded generics, motivating some to pivot into wellness and nutraceutical compounding. The widening specialty-care footprint ultimately widens the transaction base for the compounding pharmacy market.

Geography Analysis

North America maintained 37.44% of 2025 revenue, fortified by the United States’ extensive 503B network, Canada’s hormone shortages, and Mexico’s maturing API hubs. Baxter’s acquisition of PharMEDium, Fagron’s investment in Wichita, and Nephron’s 1 billion-unit South Carolina megasite exemplify the capital consolidation redefining regional competitive dynamics. Canada’s shortage database logged two-digit annual deficits in hormone products, prolonging reliance on compounders for menopausal care. Mexico’s lower-cost API exports support North American finished-dose plants, though U.S. import scrutiny keeps value capture stateside.

Asia-Pacific presents the fastest 9.26% CAGR, propelled by China’s regulatory modernization, India’s API dominance, and Japan’s super-aged demographics craving dose customization. Australia’s private insurers fund compounded bioidentical hormones under strict quality frameworks, while China’s National Medical Products Administration tightens GMP parity, raising entry barriers yet boosting trust in domestic compounders. India’s export restrictions on certain oncology agents temporarily squeeze global supply, revealing interdependence between regional API flows and worldwide compounding capacity.

Europe’s mosaic of country-specific rules complicates scaling but rewards knowledgeable incumbents. Germany’s historic Apotheke culture supports independent compounding, whereas the UK’s National Health Service bundles demand through centralized tenders. EMA’s Annex 1 revision elevates sterility protocols, nudging smaller hospital units toward outsourcing. The Middle East and Africa remain exploratory but attractive as Gulf Cooperation Council states embed pharmaceutical self-sufficiency goals in national plans. South American growth is steady, led by Brazil’s chronic-disease burden and Argentina’s favorable currency dynamics, although reimbursement inconsistencies still cap uptake compared to the compounding pharmacy market leaders.

Competitive Landscape

The compounding pharmacy market balances moderate fragmentation and accelerating consolidation. Top outsourcing facilities leverage scale to amortize nine-figure compliance investments and deploy robotics that exceed 95% contamination reduction benchmarks. Baxter’s purchase of PharMEDium grants vertically integrated control from bulk sterile bags to patient-ready syringes, allowing bundling alongside IV solutions. Fagron pursues a dual-sourcing model, combining API supply with finished formats, and has strengthened its U.S. presence by acquiring QuVa Pharma for an undisclosed sum.

Fresenius Kabi and B. Braun extend longstanding IV portfolios into 503B territories, leveraging distribution assets to secure long-term hospital contracts. Nephron’s state-of-the-art complex in South Carolina epitomizes automated sterility at an industrial scale, targeting 1 billion units annually, thereby positioning the firm as a volume outlier capable of sprint production when shortages strike. Digital health entrants pair telemedicine diagnostics with centralized compounding, shortening prescription-to-door timelines to under 48 hours in select pilots.

White-space prospects arise in pediatric, dermatology, and veterinary care, where customization depth discourages commoditization. Yet reimbursement friction pressures retail-centric 503A pharmacies, inciting niche diversification into wellness creams and supplement blends. Over the medium term, scale-driven 503B leaders and data-rich specialty compounds are likely to expand their share, leaving midsize independents as the most vulnerable cohort as the compounding pharmacy market progresses toward more concentrated oligopoly structures.

Compounding Pharmacy Industry Leaders

Wedgewood Pharmacy

Fagron NV

B. Braun SE

Baxter International Inc.

Fresenius Kabi AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Novo Nordisk warned of legal action against pharmacies compounding Wegovy, spotlighting intellectual-property tensions between originators and compounders.

- March 2025: Sycamore Partners unveiled a USD 10 billion bid for Walgreens, signaling potential private-equity capitalization of in-store compounding capabilities.

- December 2024: Novo Holdings secured EU approval to acquire Catalent for USD 16.5 billion, expanding biologics fill-finish capacity that could ease future shortages.

- October 2024: Strive Compounding Pharmacy purchased a 50,000 sq ft St. Louis facility aimed at sterile-volume growth.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the compounding pharmacy market as the global value generated by licensed 503A pharmacies and 503B outsourcing facilities that formulate patient-specific or bulk compounded medicines across all therapeutic classes and routes of administration. Products made through simple reconstitution or standard blister packaging are out of scope.

Scope Exclusion: Veterinary-only feed additives and in-hospital IV admixture services handled entirely by nursing staff are excluded.

Segmentation Overview

- By Route of Administration

- Oral

- Capsules

- Tablets

- Granules / Powder

- Syrups & Suspensions

- Topical

- Creams & Ointments

- Gels

- Lotions

- Pastes

- Parenteral

- Small-Volume Parenteral

- Large-Volume Parenteral

- Prefilled Syringes

- Ophthalmic Injectables

- Nasal

- Sprays

- Drops

- Other Route of Administration

- Oral

- By Therapeutic Area

- Pain Management

- Hormone Replacement Therapy (HRT)

- Dermal Disorders / Dermatology

- Nutritional Supplements

- Oncology / Specialty Drugs

- Pediatrics

- Veterinary

- Others

- By Sterility

- Sterile

- High-Risk Sterile

- Medium-Risk Sterile

- Low-Risk Sterile

- Non-Sterile

- Hazardous Non-Sterile

- Non-Hazardous Non-Sterile

- Sterile

- By Age Group

- Adult

- Geriatric

- Pediatric

- By End User

- Hospitals & Clinics

- Specialty Clinics

- Retail / Community Dispensing

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured calls with pharmacists running 503A counters, managers at sterile 503B plants, purchasing heads in hospital chains, and regulators across North America, Europe, and Asia-Pacific. These conversations refined utilization rates, average sterile batch sizes, and realistic active pharmaceutical ingredient mark-ups, closing gaps spotted in desk research.

Desk Research

We collated facility counts, script volumes, and price references from tier-1 public sources such as the US FDA drug-shortage bulletins, the European Medicines Agency's EudraGMDP listings, the International Pharmaceutical Federation, and trade association papers from APC and PCCA. Macroeconomic inputs, population aging, chronic pain prevalence, and health spend per capita were obtained from World Bank, WHO, and OECD datasets. Company filings, selected 10-Ks, and reputable press releases supplemented supply-side insights, while D&B Hoovers and Dow Jones Factiva fed us historical financial indicators. This list is illustrative; many other open datasets informed validation.

Market-Sizing & Forecasting

We applied a top-down demand pool rebuild that starts with national prescription volumes for customizable therapies, then layers penetration rates of compounded scripts and average selling prices. Supplier roll-ups of flagship facilities and channel checks offered bottom-up cross-tests to tune totals. Key variables inside the model include 503A versus 503B facility growth, FDA shortage frequency, weighted ASP differentials between sterile and non-sterile doses, geriatric share of population, and chronic pain incidence. A multivariate regression, stress tested through three scenario bands, projects each driver to 2030; irregular series were smoothed with exponential techniques before final aggregation.

Data Validation & Update Cycle

Outputs pass variance checks against independent prescription audits, with anomalies routed to a senior reviewer. We refresh the file annually, and we trigger interim updates when FDA shortage alerts, major regulatory shifts, or blockbuster drug discontinuations materially move any driver.

Why Our Compounding Pharmacy Baseline Earns Trust

Published estimates often diverge because firms select different facility scopes, price assumptions, and refresh cadences.

Key gap drivers are scope, some add pharmacy automation hardware, currency conversion timing, and whether veterinary scripts are rolled into human totals. Mordor's model aligns strictly to licensed compounding output in human healthcare and uses live ASPs gathered each quarter, whereas others may lean on older tariff data or inflate totals with related automation sales.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.12 bn (2025) | Mordor Intelligence | - |

| USD 13.10 bn (2023) | Global Consultancy A | Excludes 503B facilities; older price deck |

| USD 16.92 bn (2024) | Industry Publisher B | Includes veterinary revenue; single-country inflation factor applied globally |

| USD 13.10 bn (2023) | Analytics Firm C | Uses list prices, not transaction ASPs |

Taken together, the comparison shows that when scope precision, timely ASP capture, and dual-track validation are applied, Mordor Intelligence provides a balanced, reproducible baseline clients can rely on.

Key Questions Answered in the Report

How large is the compounding pharmacy market in 2026?

The compounding pharmacy market size stood at USD 16.78 billion in 2026 and is projected to reach USD 22.08 billion by 2031.

Which segment is growing fastest through 2031?

Hormone replacement therapy leads with a 7.86% CAGR, driven by the FDA’s 2025 boxed-warning removal.

Why are 503B outsourcing facilities important?

They batch-produce sterile drugs without individual scripts, enabling hospitals to stock ready-to-use injectables while meeting stringent USP <797> standards.

What is driving pediatric demand for compounded medicines?

Guardians seek dye-free, allergen-free, weight-based formulations that commercial manufacturers do not offer, pushing pediatric prescriptions at a 7.66% CAGR.

Which region is expected to record the highest CAGR to 2031?

Asia-Pacific is forecast to grow at 9.26% CAGR, propelled by regulatory modernization and expanding chronic-disease treatment needs.

Page last updated on: