Methotrexate Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

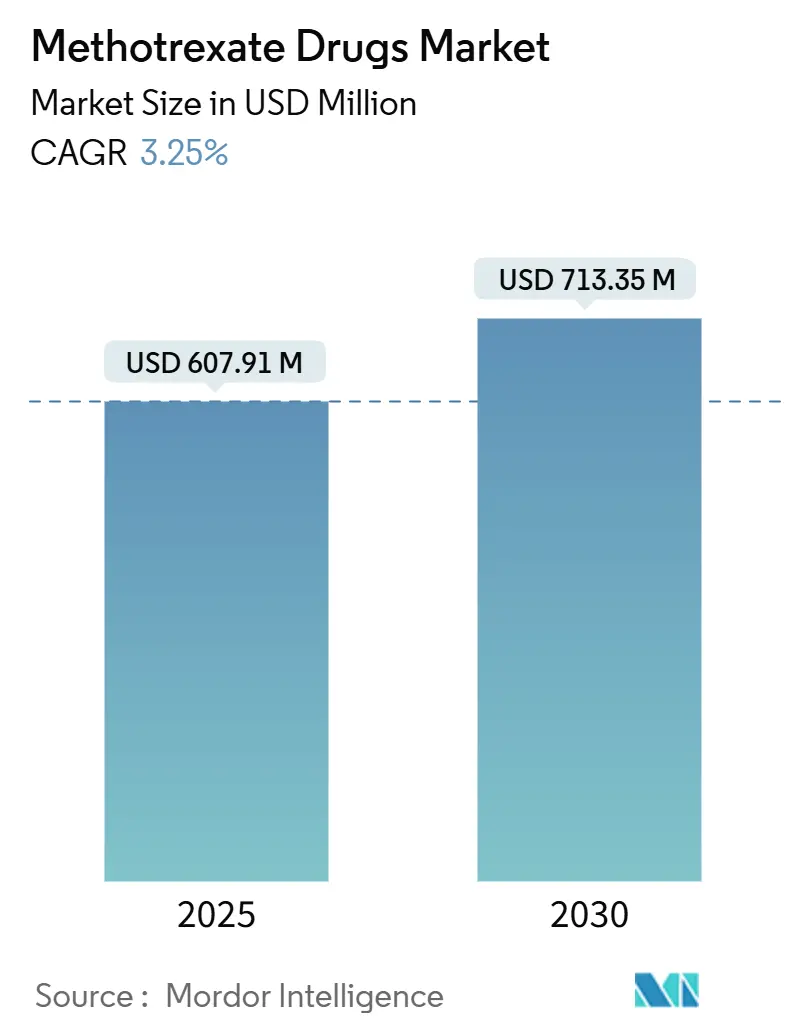

| Market Size (2025) | USD 607.91 Million |

| Market Size (2030) | USD 713.35 Million |

| Growth Rate (2025 - 2030) | 3.25% CAGR |

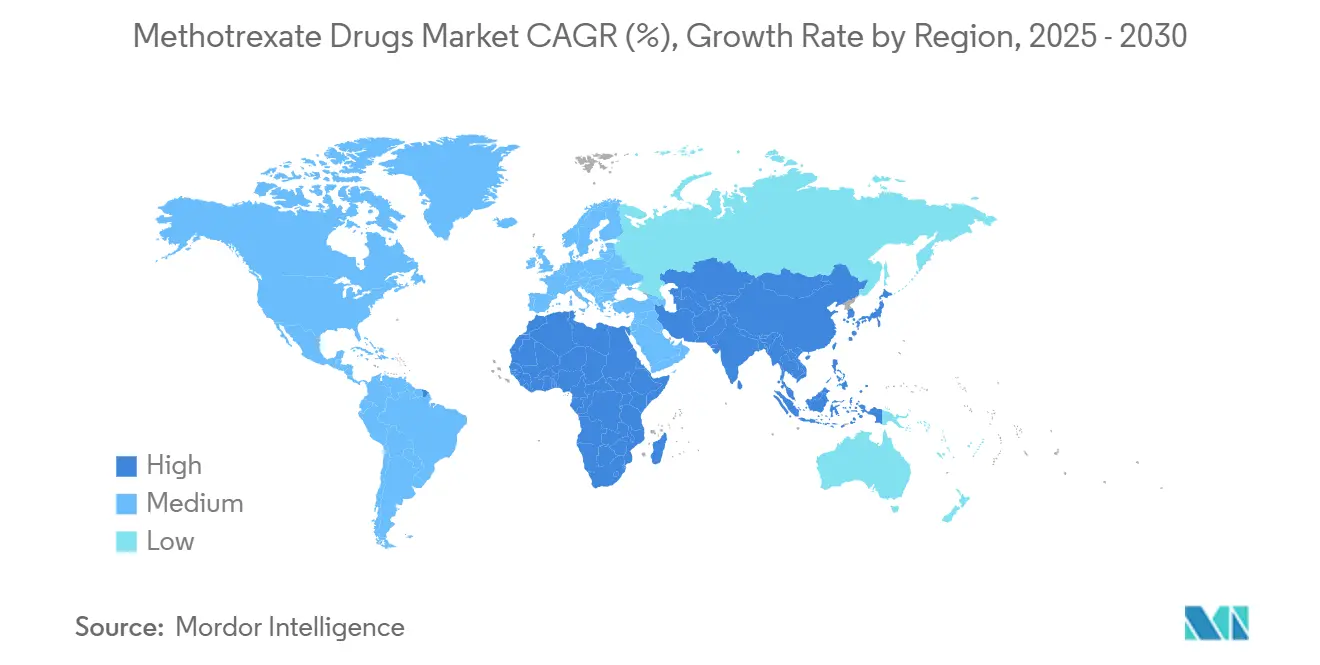

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Methotrexate Drugs Market Analysis by Mordor Intelligence

The methotrexate drugs market size is valued at USD 607.91 million in 2025 and is projected to reach USD 713.35 million by 2030, reflecting a 3.25% CAGR during the forecast period. Demand stability comes from the drug’s entrenched role as an anchor therapy in autoimmune conditions, even as targeted biologics intensify competitive pressure. Rheumatology guidelines across North America, Europe, and Japan continue to recommend methotrexate first-line, while technology-enabled delivery systems—particularly auto-injector pens—elevate patient adherence and bioavailability. Digital pharmacy growth and broader generic manufacturing in Asia-Pacific are reshaping global access, yet recurring active-pharmaceutical-ingredient (API) shortages expose supply-chain fragility. Manufacturers that combine dependable output with device innovation are best positioned to capture incremental share in the methotrexate drugs market over the next five years.

Key Report Takeaways

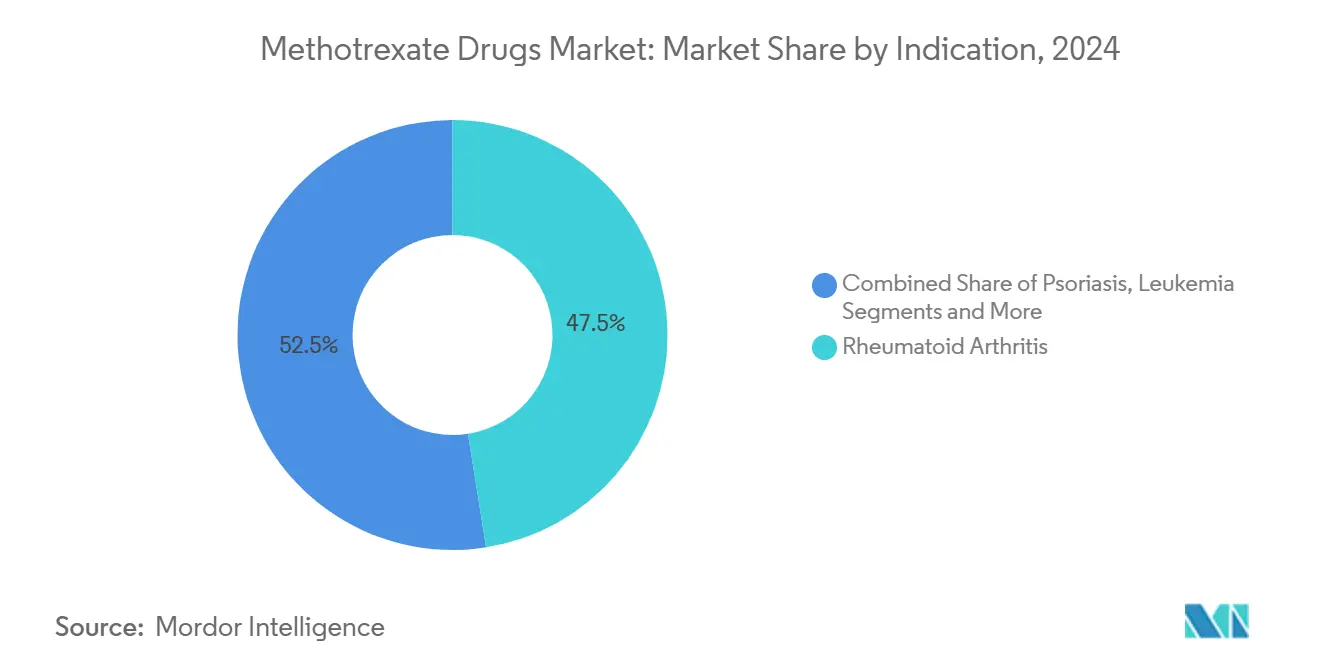

- By indication, rheumatoid arthritis led with 47.51% of methotrexate drugs market share in 2024, whereas psoriasis is set to expand at a 6.26% CAGR to 2030.

- By route of administration, oral formulations accounted for 63.25% of the methotrexate drugs market size in 2024, while subcutaneous delivery is progressing at a 5.83% CAGR through 2030.

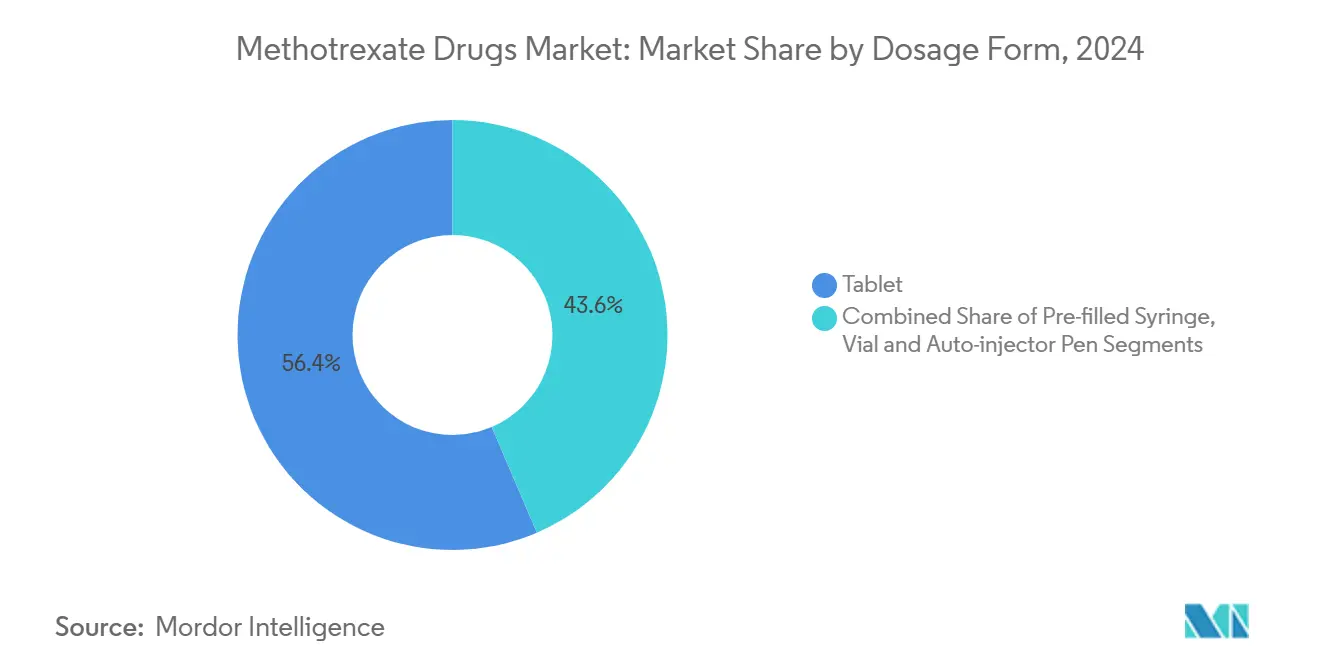

- By dosage form, tablets dominated with 56.42% revenue share in 2024; auto-injector pens represent the fastest-growing format at a 6.37% CAGR to 2030.

- By distribution channel, hospital pharmacies held 44.71% of the methotrexate drugs market share in 2024, whereas online pharmacies are forecast to climb at a 7.84% CAGR between 2025 and 2030.

- North America commanded 31.73% of global value in 2024; Asia-Pacific is projected to record the highest regional CAGR at 5.37% to 2030.

Global Methotrexate Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of rheumatoid arthritis | +0.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Increasing psoriasis incidence | +0.6% | Global, strongest in Asia-Pacific | Medium term (2-4 years) |

| Cost-effectiveness versus biologics | +0.5% | Emerging and developed markets | Medium term (2-4 years) |

| Combination-therapy anchor drug role | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Growth of subcutaneous auto-injectors | +0.3% | Developed markets, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Trials for COVID-19 hyper-inflammation | +0.2% | Research-centric regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Rheumatoid Arthritis

Aging populations in advanced economies are elevating autoimmune disease caseloads, and methotrexate remains the backbone disease-modifying option recommended by major rheumatology societies. Systematic reviews confirm durable symptom control without major hepatic or renal compromise in most patients.[1]Xiaofan Jiang et al., “Systematic Review on Methotrexate in Rheumatoid Arthritis,” Annals of Palliative Medicine, apm.amegroups.com Canadian real-world data show 30.4% of biologic-treated patients tapering or stopping methotrexate within two years without loss of disease control, indicating its continued relevance in combination regimens.[2]Louis Bessette et al., “Concomitant Methotrexate De-escalation Patterns,” Rheumatology and Therapy, springer.com Updated Japanese guidelines in 2024 reaffirm first-line status for roughly 750,000 local patients. These clinical endorsements sustain baseline demand within the methotrexate drugs market.

Increasing Psoriasis Incidence

Rising dermatologic caseloads, payer cost containment, and expanding topical technologies are steering more prescribers toward methotrexate. Transferosome-loaded microneedle patches have achieved 69% drug entrapment efficiency with sustained 24-hour release in preclinical work, pointing to lower systemic exposure and better patient comfort.[3]Snehal Shinde et al., “Transferosome-Loaded Microneedle Patch,” Pharmaceuticals, doi.org Early clinical evidence of methotrexate micro-infusion for scalp disorders signals broader dermatology potential. Together, these factors underpin the fastest-growing indication segment in the methotrexate drugs market.

Cost-Effectiveness versus Biologics

Payers worldwide are scrutinizing specialty-drug budgets, and methotrexate’s low price is gaining renewed strategic weight. Brazilian biosimilar stewardship generated 55.9% treatment-cost savings while sustaining outcomes, illustrating global applicability of value-focused protocols. Pharmacy benefit managers increasingly steer formularies toward economical generics and away from high-priced biologics, reinforcing methotrexate uptake when clinical outcomes are equivalent. Transparent pricing programs such as direct-to-consumer wholesale portals further support affordability positioning.

Combination-Therapy Anchor Drug Role

Methotrexate enhances biologic efficacy by reducing immunogenicity, as referenced in adalimumab biosimilar labeling. Mechanistic work shows low-dose methotrexate curbs T-cell migration through CXCR4 down-regulation, offering complementary pathway modulation. Network meta-analysis confirms similar ACR20/50 responses in psoriatic arthritis whether biologics are taken alone or with methotrexate, highlighting its tolerability benefits rather than efficacy redundancy. These synergistic qualities protect the methotrexate drugs market from complete displacement by targeted agents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from targeted biologics | −0.9% | North America, Europe, expanding globally | Long term (≥ 4 years) |

| Hepatotoxicity and adverse-event profile | −0.7% | Global, heightened focus in developed markets | Medium term (2-4 years) |

| API shortages and supply disruptions | −0.6% | North America, Europe, parts of Asia | Short term (≤ 2 years) |

| Heightened teratogenicity scrutiny | −0.3% | Global, stricter enforcement in high-income countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Targeted Biologics

Biosimilar rollouts and novel mechanisms such as anti-IL-23p19 elevate therapeutic benchmarks, eroding share from traditional disease-modifying agents. The U.S. has cleared 56 biosimilars with 41 launches, many directly overlapping autoimmune indications. Head-to-head data show limited methotrexate benefit in certain indications, and multiple ustekinumab biosimilars entered the market after 2024 patent expiries. These developments temper the long-term growth outlook of the methotrexate drugs market.

Hepatotoxicity and Adverse-Event Profile

Updated analyses reveal lower-than-assumed liver-fibrosis risk, yet severe multi-organ toxicities continue to surface. A 999-patient study found no link between cumulative dose and liver stiffness, challenging historic caution. Conversely, EudraVigilance data show kidney-related events carry a higher fatality than hepatic cases, warranting strict monitoring. Neurotoxicity prevalence of 5.22% in cancer patients further complicates long-term safety. This evolving risk narrative restrains broader uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Rheumatoid Arthritis Dominance Faces Psoriasis Acceleration

Rheumatoid arthritis retained 47.51% of the methotrexate drug market share in 2024 on the strength of long-term survival data showing 60% persistence at 24 months and 40% at 48 months. The segment is forecast to expand modestly as biologic cycling grows, yet anchor-therapy positioning safeguards baseline demand.

Psoriasis is projected to rise at a segment-leading 6.26% CAGR through 2030, propelled by payer focus on economical systemic options and device-enhanced delivery that minimizes systemic toxicity. Innovative microneedle patches and topical transferosome systems are broadening use cases, making psoriasis the primary growth lever in the methotrexate drugs market. Leukemia utilization remains clinically indispensable but increasingly vulnerable to supply shortages that disrupt pediatric regimens, while Crohn’s disease and other autoimmune disorders offer niche expansion based on cost-effectiveness versus biologic escalation.

By Route of Administration: Subcutaneous Innovation Disrupts Oral Dominance

The methotrexate drugs market size for oral formulations stood at USD 383.9 million in 2024, equal to 63.25% of global value. Despite this dominance, subcutaneous delivery is expected to post a 5.83% CAGR, lifted by superior bioavailability and auto-injector adoption.

Devices such as NORDIMET and Metoject accomplish predictable plasma exposure and reduce gastrointestinal intolerance, fostering switching among patients previously limited by oral side effects. Intramuscular and intravenous uses persist in oncology, especially for high-dose protocols that demand inpatient monitoring. Route diversification enhances physician flexibility, reinforcing overall resiliency of the methotrexate drugs market.

By Dosage Form: Auto-Injector Innovation Transforms Tablet Leadership

Tablet formats delivered 56.42% of 2024 revenues, yet variability in oral absorption and first-pass metabolism motivates clinicians to transition appropriate patients to parenteral options. Auto-injector pens are forecast to grow 6.37% annually, leveraging user-friendly mechanics and needle-safety shields that encourage self-administration without clinic visits.

Sustained-release and polymersome research points toward even longer dosing intervals, potentially widening therapeutic windows and further stimulating the methotrexate drugs market. Pre-filled syringes remain a transitional format, while vials hold importance for oncology pharmacies requiring dosing flexibility.

By Distribution Channel: Online Pharmacy Disruption Challenges Hospital Dominance

Hospital pharmacies generated 44.71% of global revenue in 2024 due to embedded oncology protocols and immediate rescue-therapy access. However, online platforms are slated for 7.84% CAGR growth as telehealth familiarity and direct-to-patient shipping improve chronic-care convenience.

Regulatory scrutiny of e-pharmacy operations is strengthening, yet compliant operators that integrate adherence monitoring and transparent pricing are poised to widen participation in the methotrexate drugs market.

Geography Analysis

North America contributed 31.73% of global value in 2024, underpinned by robust reimbursement and continuous device innovation. Domestic manufacturing initiatives, including Pfizer’s USD 465 million API expansion in Michigan, aim to reduce import exposure and stabilize supply.

Europe grapples with recurrent supply gaps; coordinated EMA-FDA engagement seeks rapid corrective action to secure cross-border flows. Auto-injector technology originating in Europe is diffusing globally, reinforcing the region’s device leadership.

Asia-Pacific represents the fastest-growing geography at a 5.37% CAGR through 2030, catalyzed by China’s shortage-monitoring policies, Japan’s early adoption of subcutaneous pens, and India’s dual role as producer and risk node. Improved insurance coverage and clinician training expand patient pools, amplifying the methotrexate drugs market in emerging economies.

Competitive Landscape

The methotrexate drugs market remains fragmented, yet supply reliability and device differentiation are driving moderate consolidation. Intellectual-property coverage on injector platforms extends competitive moats even within a mostly generic API context. Pharmascience’s USD 120 million Canadian fill-finish expansion underscores a strategic pivot toward localized capacity that hedges against overseas interruptions.

Patent protection on delivery hardware through 2040 further distinguishes innovators such as Antares Pharma. Digital health tie-ins—mobile apps that remind dosing and record adverse events—are emerging value-adds. Manufacturers integrating vertical supply with patient-centric services stand to capture incremental methotrexate drugs market share as purchasing decisions evolve from price-only to total-experience metrics.

Methotrexate Drugs Industry Leaders

Pfizer Inc.

Teva Pharmaceutical Industries Ltd.

Viatris Inc.

Sun Pharmaceutical Industries Ltd.

Hikma Pharmaceuticals PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Aldeyra Therapeutics secured FDA fast-track status for ADX-2191, an intravitreal methotrexate injection for retinitis pigmentosa, a disease affecting more than 1 million people worldwide.

- October 2024: FDA expanded Jylamvo oral solution labeling to include pediatric acute lymphoblastic leukemia and polyarticular juvenile idiopathic arthritis.

- May 2024: Eisai and Nippon Medac launched the Metoject subcutaneous injection pen in Japan. It is priced at 1,938–2,972 JPY per unit and serves approximately 750,000 rheumatoid arthritis patients.

Global Methotrexate Drugs Market Report Scope

| Rheumatoid Arthritis |

| Psoriasis |

| Leukemia |

| Breast Cancer |

| Crohn’s Disease |

| Other Autoimmune Disorders |

| Oral |

| Subcutaneous Injection |

| Intramuscular Injection |

| Intravenous Injection |

| Tablet |

| Pre-filled Syringe |

| Vial |

| Auto-injector Pen |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Indication | Rheumatoid Arthritis | |

| Psoriasis | ||

| Leukemia | ||

| Breast Cancer | ||

| Crohn’s Disease | ||

| Other Autoimmune Disorders | ||

| By Route of Administration | Oral | |

| Subcutaneous Injection | ||

| Intramuscular Injection | ||

| Intravenous Injection | ||

| By Dosage Form | Tablet | |

| Pre-filled Syringe | ||

| Vial | ||

| Auto-injector Pen | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2025 valuation of the methotrexate drugs market?

The methotrexate drugs market size stands at USD 607.91 million in 2025.

How fast is global demand expected to grow through 2030?

Market value is projected to reach USD 713.35 million by 2030, translating to a 3.25% CAGR.

Which indication will expand the quickest over the forecast period?

Psoriasis is forecast to grow at a 6.26% CAGR, the fastest within all tracked indications.

Why are subcutaneous auto-injectors gaining popularity?

Auto-injectors improve bioavailability, reduce gastrointestinal side effects, and support patient self-administration, fueling a 5.83% CAGR for the route.

Which region offers the highest growth potential?

Asia-Pacific is projected to post a 5.37% CAGR, driven by expanding generic manufacturing and improved healthcare access.

What is the primary competitive advantage for manufacturers today?

Supply-chain resilience combined with patented delivery-device innovation provides the key edge in winning hospital and outpatient contracts.

Page last updated on: