Oral Transmucosal Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

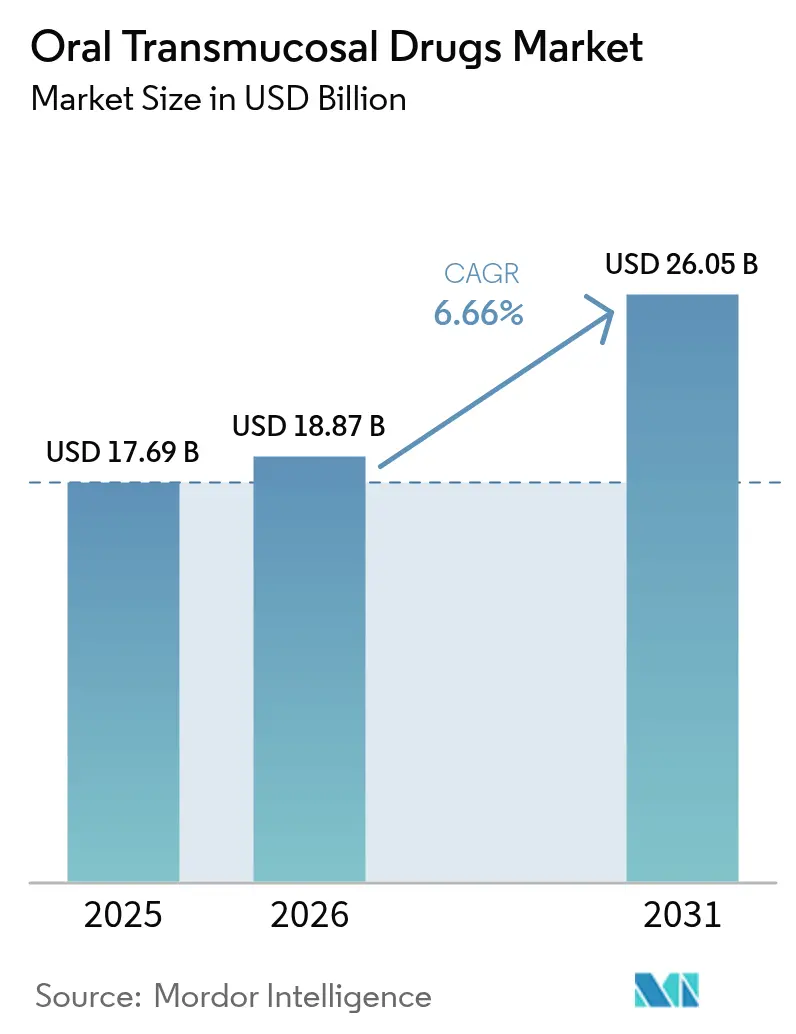

| Market Size (2026) | USD 18.87 Billion |

| Market Size (2031) | USD 26.05 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oral Transmucosal Drugs Market Analysis by Mordor Intelligence

The oral transmucosal drugs market size was valued at USD 17.69 billion in 2025 and estimated to grow from USD 18.87 billion in 2026 to reach USD 26.05 billion by 2031, at a CAGR of 6.66% during the forecast period (2026-2031). Sustained growth comes from established use in opioid dependence treatment, rapid adoption in seizure rescue, and expanding applications in pain and psychedelic therapies. Continuous advances in sublingual and buccal film technologies shorten onset times and improve bioavailability, while the preference for needle-free, swallow-free dosing boosts uptake among pediatric and geriatric patients. Regulatory agencies in the United States, Europe, and China have accelerated reviews for innovative formulations, encouraging pipelines that target high-value CNS indications. Competitive intensity has risen as large pharmaceutical companies license specialty film platforms and as intellectual-property cliffs for first-generation buprenorphine products open the door to generics and next-generation designs.

Key Report Takeaways

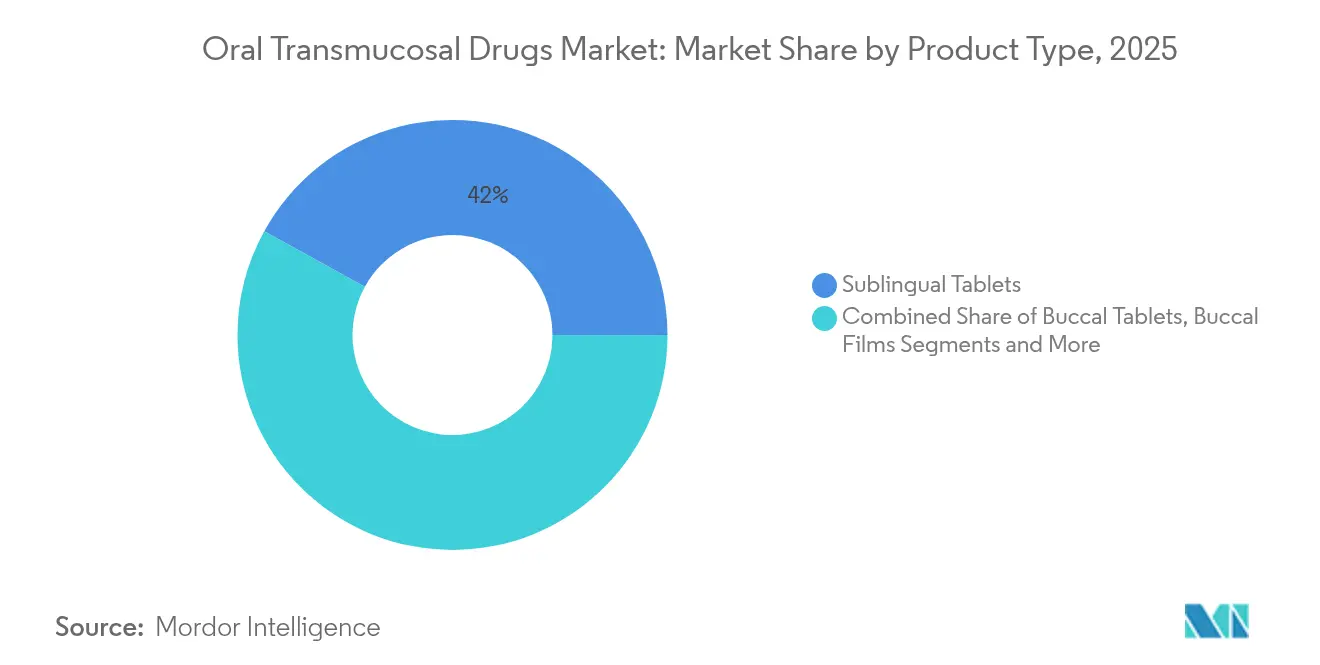

- By product type: Sublingual tablets led with 41.98% revenue share in 2025, while buccal tablets are projected to expand at a 7.12% CAGR to 2031.

- By route of administration: The sublingual mucosa route held 35.22% of oral transmucosal drugs market share in 2025, whereas buccal mucosa delivery is advancing at a 7.70% CAGR through 2031.

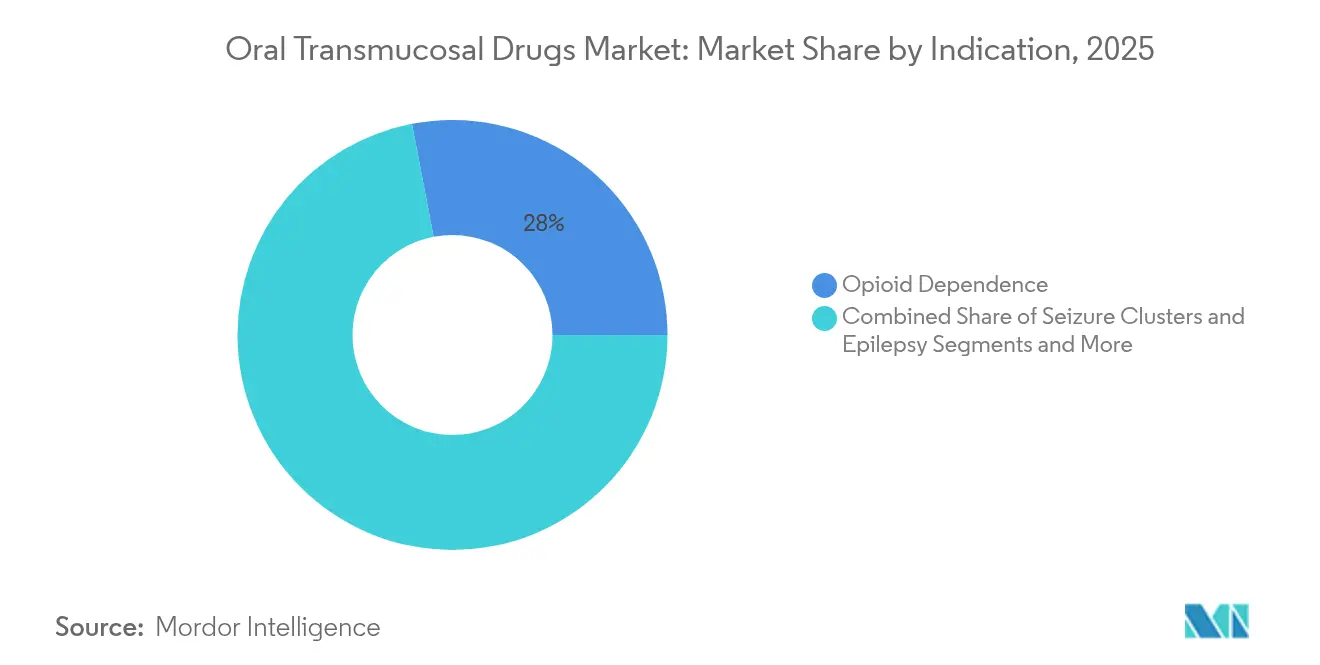

- By indication: Opioid dependence accounted for 28.02% share of the oral transmucosal drugs market size in 2025, with seizure-cluster therapies forecast to grow at 7.47% CAGR between 2026-2031.

- By distribution channel: Hospital pharmacies maintained 46.05% share in 2025; online and specialty pharmacies record the highest projected CAGR at 8.11% through 2031.

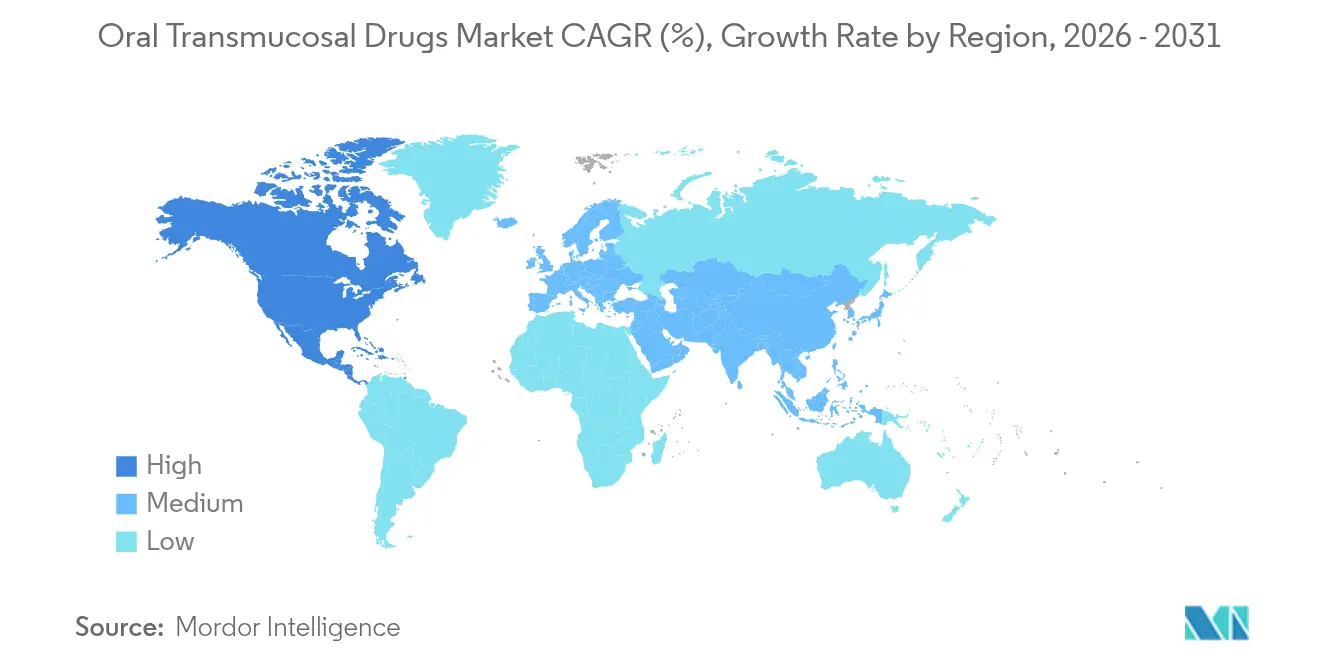

- By geography: North America captured 42.10% share in 2025, while Asia-Pacific is poised for the fastest growth at an 8.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oral Transmucosal Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of target CNS and pain disorders | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Surge in R&D pipelines & regulatory approvals post-2023 | +0.9% | North America & EU regulatory jurisdictions | Medium term (2-4 years) |

| Preference for needle-free, swallow-free dosage forms among geriatrics & pediatrics | +0.8% | Global, particularly aging populations in developed markets | Medium term (2-4 years) |

| Rapid take-up of transmucosal rescue therapies in community EMS protocols | +0.6% | North America & EU emergency medical systems | Short term (≤ 2 years) |

| Micro-dose psychedelic & cannabinoid films entering Phase-II pipelines | +0.4% | North America & select EU markets with regulatory pathways | Long term (≥ 4 years) |

| Temperature-stable film formulations supporting low-cold-chain markets | +0.3% | APAC, MEA, and Latin America emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing burden of CNS and pain disorders

Rising prevalence of opioid use disorder, epilepsy, and breakthrough cancer pain sustains demand for fast-acting transmucosal options. The FDA approval of buccal non-opioid pain drug suzetrigine in 2025 signals regulator support for safer pain alternatives [1]U.S. Food and Drug Administration, “Buprenorphine Transmucosal Dosing Guidance Update,” fda.gov. Pediatric seizure-cluster needs were addressed when Libervant received pediatric approval, broadening age coverage for rapid benzodiazepine rescue. Aging populations with dysphagia further tilt prescribing toward films and sprays that dissolve without water. Together, epidemiology and usability reinforce the long-run trajectory of the oral transmucosal drugs market.

Post-2023 surge in R&D pipelines and approvals

Expanded breakthrough and orphan-drug designations after 2023 shortened review cycles. Examples include RizaFilm for migraine and the re-scoped buprenorphine dosing guidance that cleared higher-strength products. Psychedelic candidates such as atai Life Sciences’ DMT buccal film advanced to Phase 2, pointing to novel CNS indications entering late-stage development. Faster approvals encourage investment, lifting the market growth curve.

Patient preference for needle-free, swallow-free dosing

Geriatric and pediatric adherence improves with dissolving films that avoid swallowing difficulties. Taste-masking advances using cyclodextrins and sweetening agents raise acceptance among children [2]Royal Society of Chemistry, “Advances in Taste-Masking Technologies,” rsc.org. Rescue therapies under development—for example, anaphylaxis epinephrine OTFs—illustrate how convenience can outweigh legacy injection routes in emergency care. Consistent consumer preference adds steady volume to the oral transmucosal drugs market.

Rapid adoption of transmucosal rescue in EMS protocols

Emergency medical systems now stock buccal diazepam rather than rectal gels, delivering faster seizure-cluster relief. Clinical data show median time to next seizure expands from 0.8 days when untreated to 4.9 days when buccal solutions are used. Training modules that emphasize ease of film application shorten response times, bolstering usage in ambulances and at-home care settings.

Restraints Impact Analysis*

| Restraint | I~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited drug-load & taste-masking challenges | -0.7% | Global, particularly affecting pediatric formulations | Medium term (2-4 years) |

| Patent cliffs for first-generation opioid dependence films | -0.5% | North America & EU markets with established generic pathways | Short term (≤ 2 years) |

| Emerging competition from intranasal powder auto-injectors | -0.4% | Global, with concentration in emergency medicine applications | Medium term (2-4 years) |

| Persistent FDA concerns on pediatric dosing uniformity for high-potency APIs | -0.3% | North America, with spillover effects to other regulatory jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited drug-load and taste-masking challenges

Films rarely exceed a few milligrams of active ingredient without compromising dissolution, restricting the modality to potent molecules. Bitter APIs such as buprenorphine demand sophisticated flavor-blocking that lengthens development and raises cost [3]Frontiers in Drug Delivery, “Challenges in High-Load Mucoadhesive Films,” frontiersin.org. Formulators are evaluating permeation enhancers, yet every new excipient faces toxicology hurdles that may delay approvals and weigh on near-term market growth.

Patent cliffs for first-generation opioid-dependence films

Key buprenorphine film patents begin expiring in 2027, inviting generic entrants that could erode branded revenue. Innovators are mitigating risk by launching long-acting injections and higher-dose films under fresh intellectual-property umbrellas. The transition phase may compress margins, moderating CAGR in mature indications of the oral transmucosal drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Leadership of Sublingual Tablets and Rising Buccal Tablets

Sublingual tablets held 41.98% share of oral transmucosal drugs market size in 2025 on the strength of established prescribing habits and broad reimbursement. Continuous film innovation, however, allows buccal tablets to register a 7.12% CAGR to 2031, propelled by pediatric formulations that dissolve slowly and reduce dosing frequency. Oro-dispersible films benefit from PharmFilm technology, giving poorly soluble molecules higher bioavailability in migraine and psychiatric pipelines. Liquids and sprays carve out rescue niches for anaphylaxis and neonatal seizures, while medicated confectionaries improve compliance in chronic settings. Temperature-stable tablet formats targeting 40°C ambient storage broaden access in tropical regions.

Although tablets dominate, manufacturers integrate mucoadhesive polymers to extend retention time and enhance permeation. Films deliver rapid relief—often within two minutes—making them strategic for breakthrough pain episodes. Elevated demand in emerging markets encourages investment in ambient-stable blister packs that reduce cold-chain burden. Collectively, product diversity maintains growth momentum across the oral transmucosal drugs market.

By Route of Administration: Sustained Growth of Buccal Pathway

The sublingual pathway commanded 35.22% oral transmucosal drugs market share in 2025 thanks to rich vascularization that speeds systemic uptake. Buccal delivery grows 7.70% annually through 2031 by catering to therapies that require longer contact time, such as mood stabilizers and analgesics. Lingual and gingival routes remain specialized, addressing localized periodontal pain or targeted hormone therapy.

Permeation enhancers such as bile-salt derivatives improve buccal absorption of peptides that previously required injection. Mucoadhesive patches anchored to the cheek maintain plasma levels over eight hours, reducing rescue-dose frequency. As bioavailability data build, formularies are widening coverage, reinforcing the upward path for buccal applications in the oral transmucosal drugs market.

By Indication: Seizure Management Sets the Pace

Opioid-dependence therapy constituted 28.02% of oral transmucosal drugs market share in 2025, underpinned by mandated medication-assisted-treatment programs. Seizure-cluster interventions expand fastest at 7.47% CAGR, aided by pediatric approval of Libervant and broader age labeling for Valtoco. Breakthrough cancer pain demands ultra-rapid fentanyl films, while non-opioid options such as suzetrigine reshape pain protocols.

Psychedelic micro-dose films move through Phase 2 trials in treatment-resistant depression, hinting at additional growth layers beyond conventional CNS segments.Commercial focus is now shifting toward high-value indications where transmucosal delivery provides clear clinical advantage, fostering diversified pipelines. This breadth supports a resilient outlook for the oral transmucosal drugs market.

By Distribution Channel: Shift Toward Specialty and Online Dispensing

Hospital pharmacies represented 46.05% sales in 2025 because many rescue therapies initiate in acute settings. Online and specialty channels post an 8.11% CAGR, driven by direct-to-patient shipments of chronic therapies and expanded telehealth. Retail chains remain relevant for maintenance buprenorphine scripts, but specialty outlets lead on adherence programs and pharmacovigilance.

Specialty pharmacists provide education on film placement and manage insurance authorizations, improving persistence rates. Digital tracking tools alert clinicians to missed doses, integrating outcome metrics favored under value-based reimbursement. As these services proliferate, specialty channels will capture a larger slice of the oral transmucosal drugs market.

Geography Analysis

North America contributed 42.10% revenue in 2025, benefiting from breakthrough-therapy pathways and wide insurance coverage. The FDA’s 2024 update removing buprenorphine dose ceilings has encouraged higher-strength films that enhance retention in opioid-use-disorder programs. Academic-industry collaborations at leading U.S. epilepsy centers speed recruitment for pediatric trials, consolidating the region’s leadership.Asia-Pacific registers the fastest 8.52% CAGR through 2031. China’s National Medical Products Administration implemented accelerated reviews that cleared more than 60 innovative drugs in 2024, including transmucosal formulations for pain and oncology. Investment in peptide and high-potency-film production by contract manufacturer WuXi STA underscores the region’s scale advantage. Regulatory harmonization initiatives in ASEAN facilitate cross-border market entry, expanding total addressable patients.Europe maintains steady growth on the back of the European Medicines Agency Pediatric-Use Marketing Authorization, which encourages child-friendly formulations. Recent approval of Buprenorphine Neuraxpharm illustrates ongoing innovation within mature indications . National health systems increasingly reimburse films that demonstrate superior adherence over oral tablets.Middle East & Africa and South America deliver incremental volume where temperature-stable films bypass cold-chain gaps. Humanitarian programs that stock oral transmucosal naloxone films for opioid toxicity build early market presence, offering future upside once economic conditions improve. Combined, geographic diversification supports sustained expansion of the oral transmucosal drugs market.

Competitive Landscape

The market shows moderate concentration. Aquestive Therapeutics leverages its PharmFilm platform both for partnered products such as Suboxone and for proprietary candidates including Libervant and Anaphylm. Indivior expanded into long-acting injections but continues to develop higher-dose films with rapid induction profiles to prolong exclusivity. Large pharmaceutical groups pursue licensing deals: a 2025 Merck agreement valued at USD 493 million secured oral peptide rights, illustrating big-pharma interest in transmucosal technologies (Merck press release).

Generic entrants prepare to capitalize on buprenorphine patent expiries after 2027, which may compress branded margins yet broaden patient access. Meanwhile, disruptors target psychedelic and cannabinoid indications with proprietary buccal films, forging a frontier largely untouched by incumbents. Manufacturing alliances with contract development organizations enable smaller firms to launch without owning capital-intensive facilities.

Strategically, leaders emphasize heat-stable formulations to penetrate emerging markets and invest in taste-masking science to secure pediatric labels. Competitive differentiation increasingly rests on formulation science and regulatory execution rather than molecule ownership alone, shaping the evolution of the oral transmucosal drugs market.

Oral Transmucosal Drugs Industry Leaders

ZIM Laboratories Limited

Aquestive Therapeutics, Inc.

IntelGenx Corp.

Novartis AG

Sunovion Pharmaceuticals, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Aspire Biopharma dosed the last patient in a Phase 1 study of a fast-acting high-dose aspirin oral transmucosal film; topline data expected in Q3 2025.

- October 2023: atai Life Sciences completed a Phase 1 trial of VLS-01 DMT oral transmucosal film, reporting favorable safety in healthy volunteers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study characterizes the oral transmucosal drugs market as all prescription or over-the-counter pharmaceutical products intentionally formulated for systemic absorption through the sublingual, buccal, gingival, or palatal mucosa. Tablets, films, sprays, lozenges, and drops that bypass the gastrointestinal tract and first-pass metabolism are included.

OTC mouth-fresheners, oral care pastes, and nutritional supplements, where systemic delivery is neither primary nor regulated as a drug, fall outside this scope.

Segmentation Overview

- By Product Type

- Sublingual Tablets

- Buccal Tablets

- Oro-dispersible Films

- Buccal Films

- Liquids & Sprays

- Medicated Confectionaries (Lozenges, Lollipops, Gums)

- Others (Patches, Gels)

- By Route of Administration

- Sublingual Mucosa

- Buccal Mucosa

- Lingual

- Gingival

- By Indication

- Opioid Dependence

- Seizure Clusters & Epilepsy

- Pain / Oncology Pain

- Nausea & Vomiting

- Erectile Dysfunction

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online & Specialty Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

To validate secondary signals, Mordor analysts interviewed formulators, hospital pharmacists, addiction-medicine clinicians, and procurement leads across North America, Europe, India, Japan, and Brazil. These conversations clarified patient volumes, off-label usage, typical film versus tablet price gaps, and regional reimbursement hurdles, which were pivotal in fine-tuning incidence-to-therapy ratios and average selling prices.

Desk Research

We began with structured desk work that pulled recent regulatory filings from the US FDA, EMA, and PMDA, morbidity datasets from the Global Burden of Disease study, and drug-utilization dashboards hosted by entities such as the CDC and Eurostat. Further, trade association white papers from IFPMA and PhRMA, clinical-trial registries, and select academic journals (Journal of Controlled Release, Drug Development & Industrial Pharmacy) offered molecule pipelines, adoption curves, and pricing clues. Subscriber resources, including D&B Hoovers for company revenues and Dow Jones Factiva for deal tracking, added context. This list is illustrative, not exhaustive; many other public and proprietary sources informed our work.

Market-Sizing & Forecasting

We constructed a top-down patient-pool model that starts with country-level prevalence of opioid dependence, migraine, and seizure clusters, then applies treatment penetration, formulation mix, and annual dosage assumptions. Results are tested against selective bottom-up rollups, sampled manufacturer shipments, and channel checks to balance understatement or double counting.

Yearly buprenorphine waiver patient count, Average sublingual film ASP trends in hospital formularies, Neurological disorder incidence growth among 45-64 age group, Controlled-substance scheduling changes influencing prescription volumes, and Adoption rate of fast-dissolving film technology patents granted per year.

Forecasts to 2030 rely on a multivariate regression where incidence growth, pricing elasticity, and technology penetration serve as predictors; scenarios were stress-tested with our primary panel.

Data gaps in manufacturer rollups were bridged using regional import values and validated substitution ratios.

Data Validation & Update Cycle

Outputs pass a two-level analyst review: variance checks against historic IMS sales, cross-region outlier scans, and reconciliation with expert call notes. Models refresh annually, with interim updates triggered by material events (e.g. FDA approvals, scheduling reclassifications). Before release, an analyst reruns the latest variables so clients receive the freshest view.

Why Mordor's Oral Transmucosal Drugs Baseline Is Highly Credible

Published estimates often differ because firms vary scope, input granularity, and refresh cadence. We acknowledge these gaps upfront.

Key gap drivers include: some publishers bundle topical oral gels or transdermal patches, others apply aggressive ASP escalation without channel-mix validation, and many freeze epidemiology inputs for three-year cycles while Mordor revisits them yearly. Currency conversion year and undisclosed discounting further widen spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.69 B (2025) | Mordor Intelligence | - |

| USD 38.43 B (2025) | Regional Consultancy A | Includes oral care pastes and nutraceutical films; assumes uniform 8% annual price uplift |

| USD 43.53 B (2025) | Global Publisher B | Uses static 2022 patient prevalence and aggregates intranasal transmucosal forms |

These comparisons show that when scope alignment, live epidemiology, and real-world pricing are enforced, Mordor delivers a balanced, transparent baseline that decision-makers can trace to clear variables and repeat with confidence.

Key Questions Answered in the Report

How big is the Oral Transmucosal Drugs Market?

The Oral Transmucosal Drugs Market size is expected to reach USD 18.87 billion in 2026 and grow at a CAGR of 6.66% to reach USD 26.05 billion by 2031.

Which product segment holds the largest share today?

Sublingual tablets dominate with 41.98% revenue share as of 2025.

Who are the key players in Oral Transmucosal Drugs Market?

ZIM Laboratories Limited, Aquestive Therapeutics, Inc., IntelGenx Corp., Novartis AG and Sunovion Pharmaceuticals, Inc. are the major companies operating in the Oral Transmucosal Drugs Market.

Which is the fastest growing region in Oral Transmucosal Drugs Market?

Asia-Pacific, supported by regulatory reforms and manufacturing expansion, is forecast to grow at 8.52% CAGR to 2031.

Which region has the biggest share in Oral Transmucosal Drugs Market?

In 2026, the North America accounts for the largest market share in Oral Transmucosal Drugs Market.

Page last updated on: