Acetaminophen Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

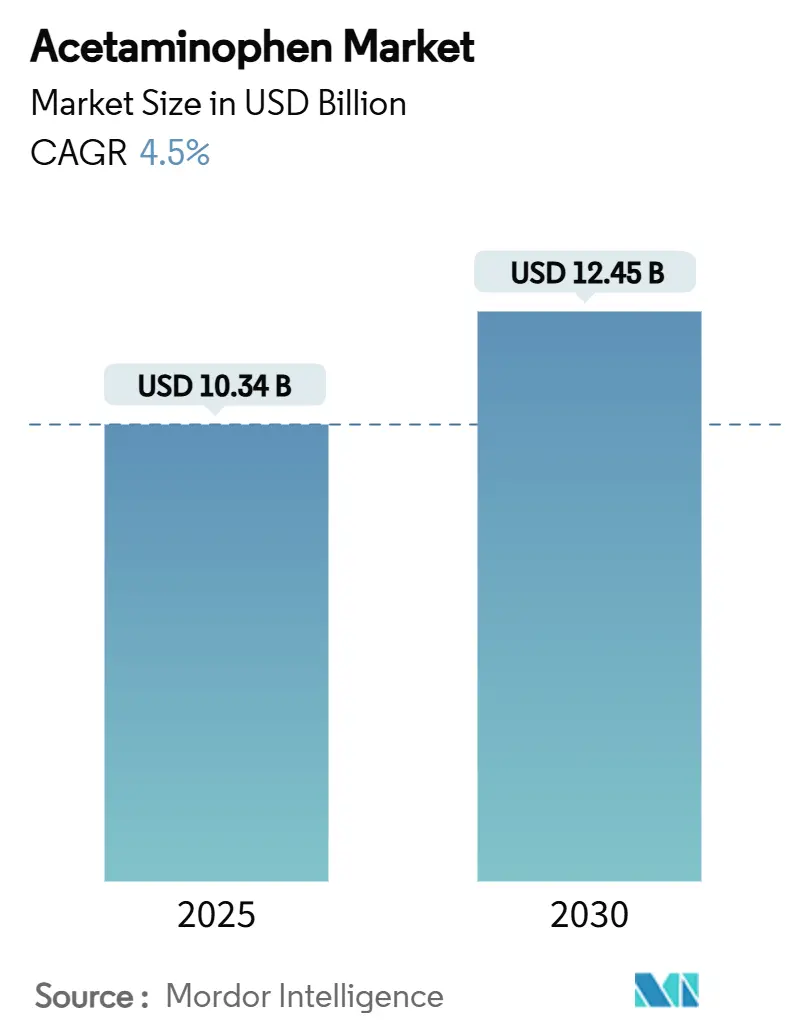

| Market Size (2025) | USD 10.34 Billion |

| Market Size (2030) | USD 12.45 Billion |

| Growth Rate (2025 - 2030) | 4.50% CAGR |

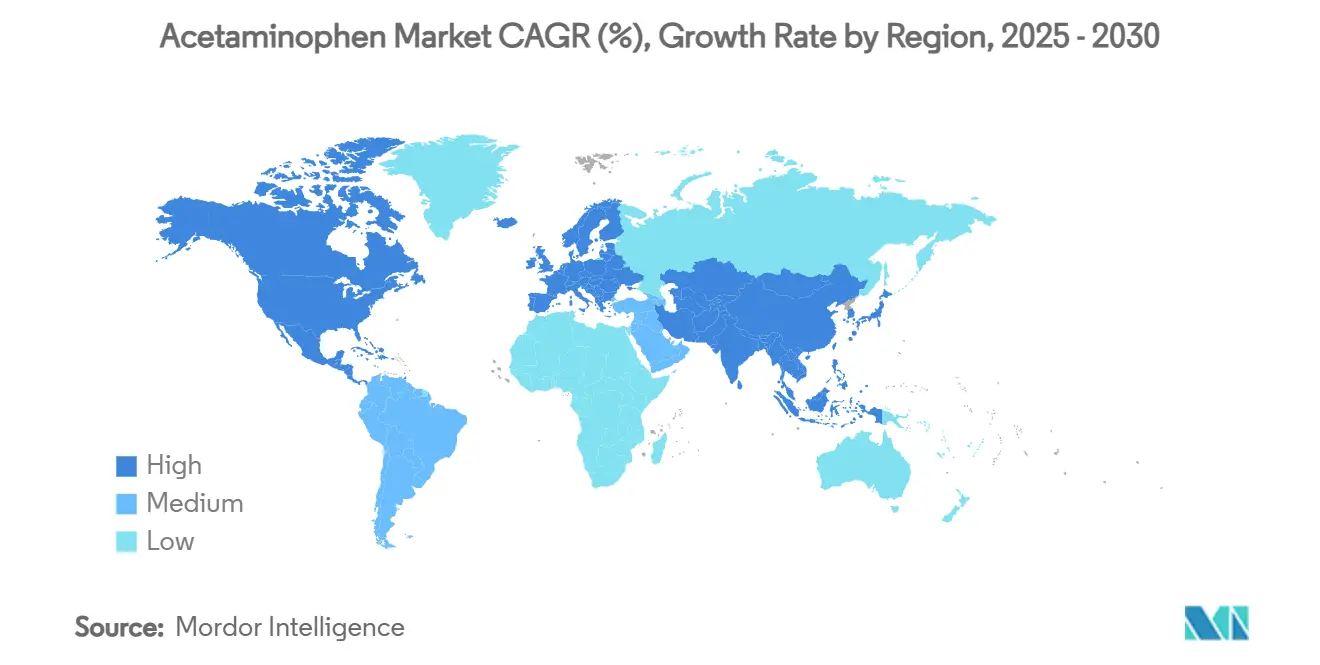

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acetaminophen Market Analysis by Mordor Intelligence

The acetaminophen market size reached USD 10.34 billion in 2025 and is forecast to climb to USD 12.45 billion by 2030, representing a 4.5% CAGR through the period. Demand expansion is steady rather than spectacular, yet the sector is undergoing deep structural realignment as regulators tighten dosage limits, manufacturers diversify supply chains, and innovators explore new delivery formats. Regulatory moves such as the U.S. Food and Drug Administration’s 325 mg ceiling on prescription combination products are shifting competitive boundaries by rewarding firms that can rapidly reformulate and certify lower-dose offerings. Parallel efforts to curb opioid prescriptions have amplified the clinical importance of non-opioid analgesics, positioning acetaminophen as a cornerstone in multimodal pain management protocols. Capacity additions for para-aminophenol in India and process-efficiency upgrades in China are gradually easing supply-security concerns but have not eliminated raw-material price volatility. Simultaneously, e-commerce penetration and hospital-based intravenous (IV) adoption are redefining channel dynamics and opening revenue pathways beyond traditional over-the-counter retail.

Key Report Takeaways

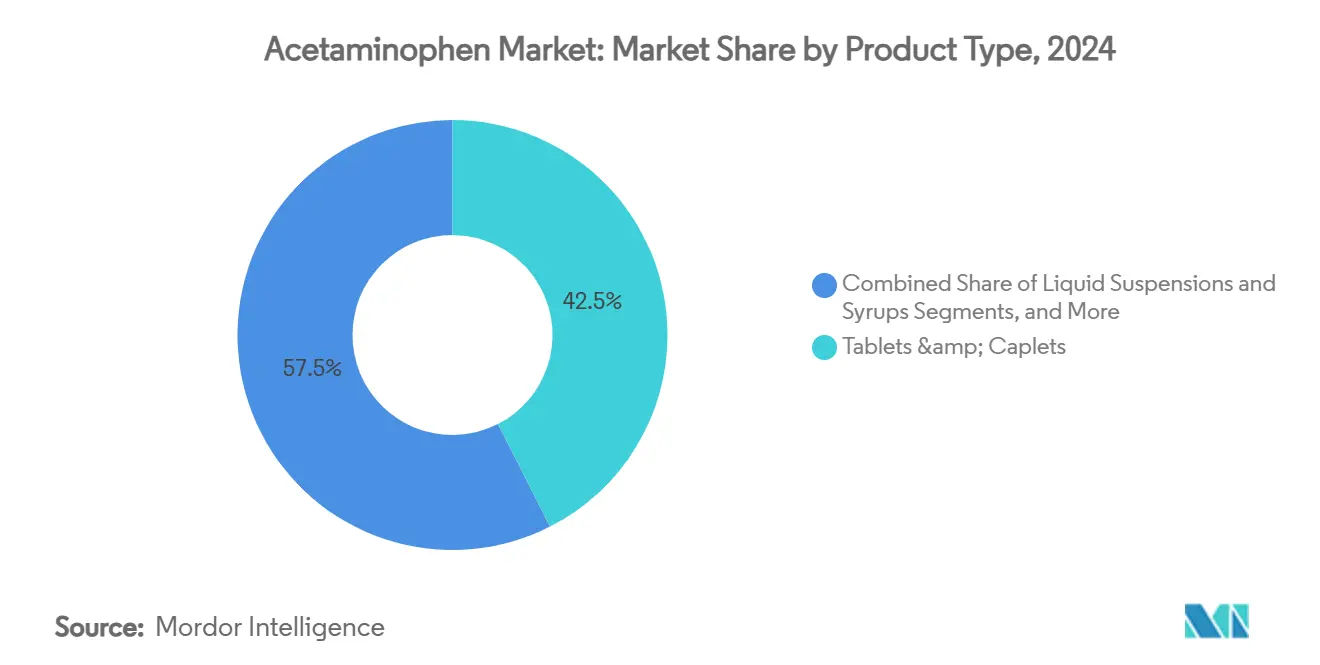

- By product type, tablets captured 42.5 of % acetaminophen market share in 2024, while IV formulations are forecast to grow at a 5.9% CAGR through 2030/

- By route of administration, oral products accounted for 88.7% of the acetaminophen market size in 2024; IV usage is projected to expand at a 5.8% CAGR.

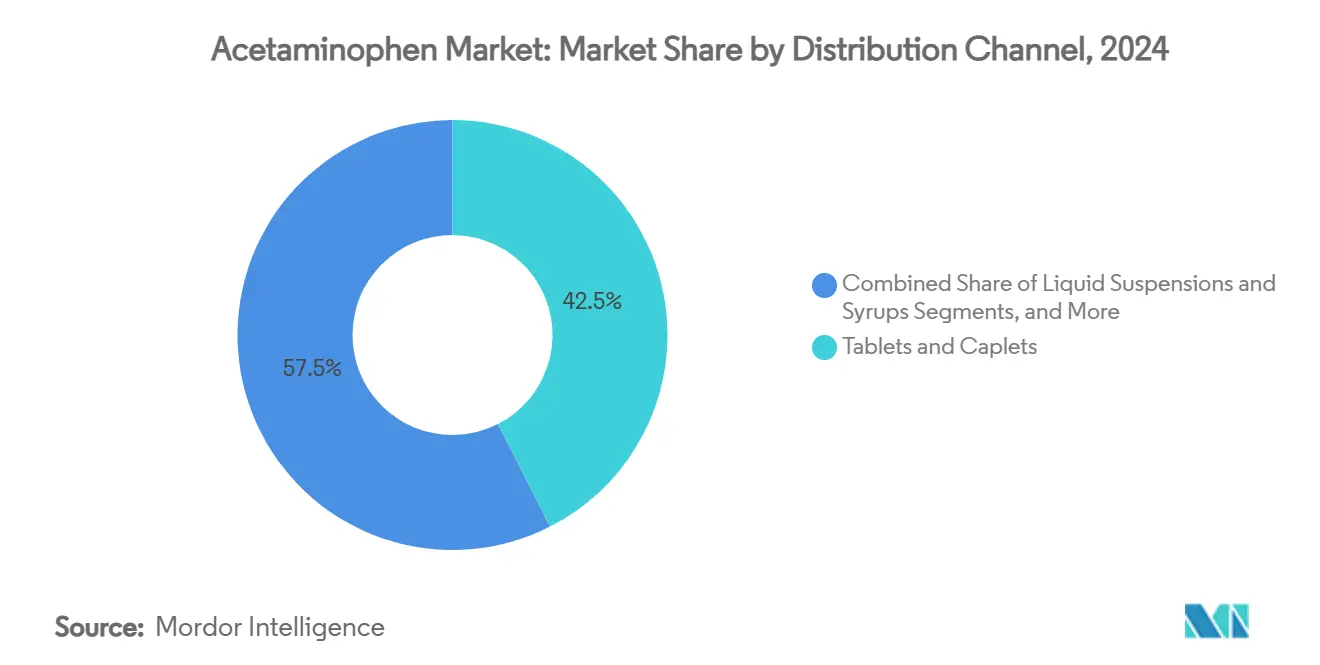

- By distribution channel, retail pharmacies held 54.8% revenue share in 2024, whereas e-commerce platforms are set to progress at a 6.2% CAGR to 2030.

- By region, North America led with 33.7% of the acetaminophen market size in 2024, yet Asia-Pacific is advancing at a 7.3% CAGR due to rising self-medication rates.

Global Acetaminophen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Chronic Pain & Febrile Ailments | +1.20% | Global, with concentration in aging populations of North America & Europe | Long term (≥ 4 years) |

| Growing OTC Self-Medication Trend In Emerging Economies | +0.80% | APAC core, spill-over to Latin America & MEA | Medium term (2-4 years) |

| Regulatory Crack-Down On Opioids Boosting Non-Opioid Demand | +0.70% | North America & EU, expanding to Australia | Short term (≤ 2 years) |

| Expansion Of Generic API Capacity In India & China | +0.50% | Global supply chains, primary impact in APAC | Medium term (2-4 years) |

| Surge In Fixed-Dose Pediatric Cold-&-Flu Combinations | +0.40% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Adoption Of Continuous-Flow Chemistry Lowering API Cost & Footprint | +0.30% | Manufacturing hubs in India, China, and select EU facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Pain and Febrile Ailments

An aging demographic profile across developed economies is propelling long-term acetaminophen usage as seniors manage arthritis, neuropathic discomfort, and post-surgical pain. The World Health Organization’s essential-medicine designation reinforces its indispensability in first-line therapy worldwide. Clinical studies confirm that acetaminophen, in concert with adjuvant non-opioid agents, delivers effective relief while avoiding opioid-related adverse events.[1]Olga L. Elvir-Lazo, “Role of Acetaminophen in Chronic Pain Management: Benefits, Risks, and Considerations,” Journal of Surgery and Research, fortunejournals.com Oncology and palliative-care protocols increasingly integrate the drug for baseline pain control, reducing morphine requirements and lowering treatment costs for stretched hospital budgets. These factors collectively add more chronic prescriptions to the acetaminophen market, extending average treatment duration and unit volumes. Payers value its favorable cost-utility profile, particularly as health-system spending faces macroeconomic pressure through the decade.

Growing OTC Self-Medication Trend in Emerging Economies

Government decentralization of primary healthcare in markets such as India, Indonesia, and Brazil is fostering consumer reliance on easily available analgesics. Indian surveys show 52% of the population self-medicate for minor ailments, directly benefiting acetaminophen uptake.[2]Prashant Narang, “Regulatory, Safety and Economic Considerations of Over-the-Counter Medicines in the Indian Population,” Springer Nature, springer.comRecent regulatory blueprints carve out clear OTC schedules, allowing community pharmacists to recommend branded or generic 500 mg tablets without prescriptions. Smartphone-enabled drug-delivery apps deepen rural reach, and promotional campaigns underline correct dosage, reinforcing responsible use. Price sensitivity remains a determinant of choice; hence, local manufacturers that backward-integrate to para-aminophenol production gain margin headroom to sustain competitive retail price points. COVID-19 experience further ingrained household stockpiling habits that now persist in seasonal influenza waves, elevating baseline retail sales across Asia-Pacific.

Regulatory Crackdown on Opioids Boosting Non-Opioid Demand

Across the United States, new state prescription-monitoring laws and federal prescribing-limit guidelines have reduced opioid volumes, compelling clinicians to embrace safer analgesic regimens. Acetaminophen fixed-dose combinations with ibuprofen demonstrate comparable analgesic potency to low-dose opioids in dental and musculoskeletal indications, according to randomized trials. Policymaker endorsement of such regimens is accelerating hospital formulary inclusion. Pharmaceutical innovators are investing in novel non-opioid molecules like suzetrigine that complement acetaminophen, highlighting a strategic pivot in pain-management pipelines. Insurers also incentivize non-opioid dispensing via lower co-pays, enhancing patient adherence and reinforcing volume growth within the acetaminophen market.

Expansion of Generic API Capacity in India and China

India’s Production Linked Incentive program allocates subsidies for domestic para-aminophenol plants, aiming to curtail reliance on 28,000-30,000 tonnes of annual imports from China.[3]Chaitanya Ghoroi, “Process Design and Economics of Production of p-Aminophenol,” arXiv, arxiv.org Concurrently, Chinese producers are modernizing to meet tougher wastewater standards, which could modestly elevate conversion costs but improve long-term supply stability. Diversified sourcing arrangements are enabling multinational formulators to secure multi-year contracts at predictable pricing, buffering against the recent raw-material price swings reported in 2025. Continuous-flow synthesis is gaining industrial traction, lowering energy inputs and trimming batch variability, thereby strengthening the cost competitiveness of Asian bulk manufacturers. Collectively, these developments underpin a modest positive contribution to the global acetaminophen market CAGR by constraining future input shocks and broadening supplier choice.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hepatotoxicity Concerns Prompting Dosage Caps & Warning Labels | -0.90% | Global, with strictest enforcement in North America & EU | Short term (≤ 2 years) |

| Volatile Prices Of Key Raw Material Para-Aminophenol (PAP) | -0.60% | Global supply chains, acute impact in manufacturing hubs | Medium term (2-4 years) |

| Competition From NSAID Blends & Novel Analgesics | -0.40% | North America & EU primarily, expanding to developed APAC markets | Medium term (2-4 years) |

| EU "Green Chemistry" Procurement Rules Against High-Toxicity APIs | -0.30% | European Union, with potential spillover to other developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hepatotoxicity Concerns Prompting Dosage Caps and Warning Labels

The FDA now limits prescription combinations to 325 mg acetaminophen per dosage unit and mandates boxed liver-injury warnings, a response to data showing the drug as a leading cause of acute liver failure in the United States. Roughly 48% of such cases stem from inadvertent overdosing, spurring consumer-education drives that advise strict adherence to the 4,000 mg daily maximum. These interventions dampen per-capita consumption and compel manufacturers to reformulate legacy products, incurring incremental development and packaging expenses. European regulators have adopted analogous dosage guidance, further tightening the global safety envelope. Although these measures safeguard public health, they temporarily curb volume growth until lower-dose SKUs achieve full market penetration and patient confidence stabilizes.

Volatile Prices of Key Raw Material Para-Aminophenol (PAP)

Sharp swings in para-aminophenol pricing during early 2025, stemming from feedstock disruptions and Chinese export controls, squeezed gross margins for finished-dose manufacturers. Short-term price spikes ripple across procurement budgets because PAP accounts for a significant share of acetaminophen tablet cost of goods. The Indian National Pharmaceutical Pricing Authority documented subsequent pass-through attempts that met resistance in price-capped domestic markets, highlighting profitability pressure in low-income geographies. While additional capacity coming on-stream in Gujarat and Jiangsu is easing supply tightness, the concentration of PAP production heightens exposure to geopolitical or environmental shocks. Persistent volatility constitutes a structural headwind restraining the acetaminophen market expansion rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tablets Retain Primacy while IV Therapies Scale Up

Tablets and caplets dominated the acetaminophen market at 42.5% revenue share in 2024, reflecting production efficiency, brand familiarity, and broad indication coverage. Household recognition of 500 mg and 650 mg strengths ensures continued shelf-space priority in chain pharmacies, while pediatric chewables and flavored suspensions secure caregiver loyalty. Liquid syrups capture a significant share in the sub-12-year demographic, leveraging weight-based dosing convenience. Niche delivery forms such as effervescent or orally disintegrating tablets open differentiation avenues for companies targeting patients with dysphagia or rapid-onset needs.

IV acetaminophen represents the fastest-growing product group with 5.9% CAGR through 2030, buoyed by rising hospital adoption for post-operative analgesia and neonatal patent ductus arteriosus therapy. Clinical meta-analyses reveal 80.7% ductus closure in very-low-birth-weight infants, comparable to indomethacin but with fewer gastrointestinal or renal complications. Hospitals also appreciate the opioid-sparing properties of peri-operative IV acetaminophen, which shorten recovery times and reduce antiemetic consumption. Continuous-flow crystallization advances achieve 47% drug loading, shrinking unit production costs and improving vial affordability. As supply reliability strengthens, formulators are poised to expand their peri-operative care portfolios, driving incremental volume growth within this segment of the acetaminophen market.

By Route of Administration: Oral Supremacy Faces Targeted Clinical Challenges

Oral administration held 88.7% of global revenue in 2024 owing to cost-effective mass manufacture, broad consumer acceptance, and versatile strength options. Immediate-release 500 mg tablets fulfill the bulk of intermittent fever treatment, whereas extended-release 650 mg formats cater to overnight pain control. Flavor-masked pediatric suspensions enhance dosing compliance, especially in markets where self-medication rates are burgeoning. Rectal suppositories remain valuable in post-operative or vomiting scenarios, though limited by slower absorption and caregiver reluctance.

IV delivery is steadily gaining share at a projected 5.8% CAGR. Post-surgical pain management protocols increasingly incorporate scheduled IV acetaminophen to curtail opioid requirements, an approach validated across orthopedic, gynecological, and colorectal procedures. Emerging IV fixed-dose combinations pairing 1 g of acetaminophen with 100 mg of ibuprofen show synergistic efficacy, prompting formulary evaluations. Hospitals appreciate the predictable pharmacokinetics and lack of first-pass metabolism, crucial for intensive-care patients with impaired gastric motility. Manufacturers investing in ready-to-use plastic-bag formats and extended shelf-life formulations are well-positioned to capture this clinically driven growth pocket inside the broader acetaminophen market.

By Distribution Channel: Retail Dominance Meets E-Commerce Momentum

Brick-and-mortar pharmacies and drugstores delivered 54.8% of 2024 sales, underpinned by pharmacist counsel, immediate availability, and insurance reimbursement infrastructure for prescription combinations. Seasonal demand spikes during influenza waves showcase the channel’s inventory agility, while loyalty programs anchor repeat purchases of private-label 500 mg packs. Hospital pharmacies maintain an essential, albeit smaller, slice of distribution tied to inpatient IV administration and high-strength prescription blends.

E-commerce is the fastest-expanding outlet with 6.2% CAGR, catalyzed by mobile app penetration and improved cold-chain logistics for temperature-controlled shipments. Contactless delivery preferences formed during the pandemic remain intact, and same-day fulfillment in metropolitan areas now rivals the speed of walk-in retail. Digital platforms apply algorithmic recommendations based on browsing patterns to upsell complementary cough-and-cold SKUs, elevating basket value. Regulatory frameworks in the United States and India that authenticate online pharmacy licenses enhance consumer trust, further embedding e-commerce in the acetaminophen market’s long-term channel mix.

Geography Analysis

North America accounted for 33.7% of global consumption in 2024, anchored by physician trust in branded products and payer acceptance of lower-dose prescription combinations. Kenvue’s flagship Tylenol maintains top-of-mind recall among pediatricians, bolstering premium pricing power despite generic competition. The region benefits from comprehensive pharmacovigilance systems that quickly disseminate safe-use messaging, preserving consumer confidence amid hepatotoxicity debates. Ongoing litigation around opioid manufacturers has enhanced the reputational standing of non-opioid options, supporting robust unit sales across retail chains and hospitals.

Europe preserves a sizeable share through stringent quality standards and expanding hospital IV utilization. The European Parliament’s strategic push for domestic API production incentivizes regional manufacturers to reshore para-aminophenol synthesis, potentially buffering currency and freight cost swings. Green-procurement rules that reward low-solvent, low-emission synthesis routes could advantage continuous-flow adopters. Pharmaceutical majors such as GSK reported GBP 31.4 billion in 2024 sales, with general medicines climbing 6%, demonstrating the resilience of mature portfolios that include acetaminophen formats.

Asia-Pacific is the fastest-growing territory with 7.3% CAGR through 2030, fueled by rising disposable incomes, urbanization, and policy support for self-care. India’s OTC market value hit USD 3.9 billion in 2021 and is scaling further as state governments streamline pharmacy regulations. Indigenous para-aminophenol production investments promise raw-material self-sufficiency, which could cut landed costs and elevate local formulators’ competitiveness. China continues to dominate API exports yet faces stricter environmental compliance, prompting select facilities to relocate inland where utilities are cheaper and regulatory enforcement is evolving. Multinationals such as Lotus Pharmaceuticals leverage acquisitions to gain footholds in Southeast Asian retail networks, positioning themselves for sustained growth within the regional acetaminophen market.

Competitive Landscape

The acetaminophen market displays moderate concentration; branded incumbents wield strong visibility yet do not command overwhelming share, creating space for agile generics. Perrigo controls more than half of the United States'' private-label tablet volumes, leveraging FDA approval of a 250 mg acetaminophen plus 125 mg ibuprofen dual-action tablet to cement retailer partnerships. Kenvue’s mid-2025 leadership overhaul signals potential portfolio pruning as it prioritizes higher-margin skin-care assets, possibly leading to divestitures in the analgesic line. Such moves could shift brand-equity dynamics and invite consolidation bids from regional producers seeking instant scale.

Technological differentiation is emerging as a competitive lever. Continuous-flow crystallization, pioneered at Massachusetts Institute of Technology, achieves double-digit efficiency gains and lowers solvent usage, an attribute increasingly valued under European green-chemistry procurement standards. Teva underscores the trend with a pipeline pivot toward complex generics and biosimilars, while its API division returned to 3% growth in 2024, underscoring the strategic value of vertical integration. Smaller specialists focus on pediatric or clean-label niches, as illustrated by Genexa’s vegan, filler-free infant suspension launch that resonates with ingredient-conscious consumers.

Supply-chain resilience remains a boardroom priority after pandemic-era shortages underscored dependence on Chinese para-aminophenol. Manufacturers that lock in dual-source contracts or co-invest in upstream facilities mitigate risk and gain negotiating leverage. Overall, the competitive field rewards scale economies, regulatory agility, and process innovation, factors that collectively shape future share redistribution inside the acetaminophen market.

Acetaminophen Industry Leaders

Mallinckrodt plc

Farmson Pharmaceutical Gujarat Pvt. Ltd.

Granules India Ltd.

Johnson & Johnson

GlaxoSmithKline plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teva launched the acceleration phase of its Pivot to Growth plan, forecasting over USD 5 billion from innovative medicines by 2030 and renewed emphasis on generic acetaminophen output.

- March 2025: Perrigo secured FDA clearance for a store-brand acetaminophen and ibuprofen tablet, strengthening its private-label leadership in the United States.

- January 2025: Genexa introduced a clean-label infant acetaminophen suspension free from artificial fillers, gluten, and animal derivatives.

Global Acetaminophen Market Report Scope

| Tablets & Caplets |

| Liquid Suspensions & Syrups |

| Suppositories |

| Intravenous Injection |

| Others (Effervescent, ODT, Chewable) |

| Oral |

| Rectal |

| Intravenous |

| Transdermal |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| E-commerce & Online Pharmacies |

| Wholesalers & Distributors |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Tablets & Caplets | |

| Liquid Suspensions & Syrups | ||

| Suppositories | ||

| Intravenous Injection | ||

| Others (Effervescent, ODT, Chewable) | ||

| By Route of Administration | Oral | |

| Rectal | ||

| Intravenous | ||

| Transdermal | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| E-commerce & Online Pharmacies | ||

| Wholesalers & Distributors | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What was the global acetaminophen market size in 2025?

The acetaminophen market size stood at USD 10.34 billion in 2025 and is projected to reach USD 12.45 billion by 2030.

Which region leads global demand for acetaminophen?

North America held 33.7% of worldwide sales in 2024, supported by entrenched brand loyalty and strict opioid-reduction policies.

Which product segment is growing the fastest?

Intravenous acetaminophen is forecast to expand at 5.9% CAGR through 2030 on the strength of hospital adoption for post-operative pain and neonatal PDA therapy.

How are regulators affecting acetaminophen formulations?

The FDA cap of 325 mg per dosage unit for prescription combinations is forcing reformulation of legacy products and encouraging lower-dose offerings with enhanced labeling.

What supply-chain developments are shaping future pricing?

Indias incentive program for domestic para-aminophenol plants and Chinas process-efficiency upgrades are improving raw-material security while moderating price volatility.

Which distribution channel shows the highest growth potential?

E-commerce pharmacies are advancing at 6.2% CAGR, driven by contactless delivery preferences and regulatory recognition of licensed online platforms.

Page last updated on: