Specialty Stores Pet Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 68.86 Billion |

| Market Size (2031) | USD 98.07 Billion |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specialty Stores Pet Food Market Analysis by Mordor Intelligence

Market Analysis by Mordor Intelligence

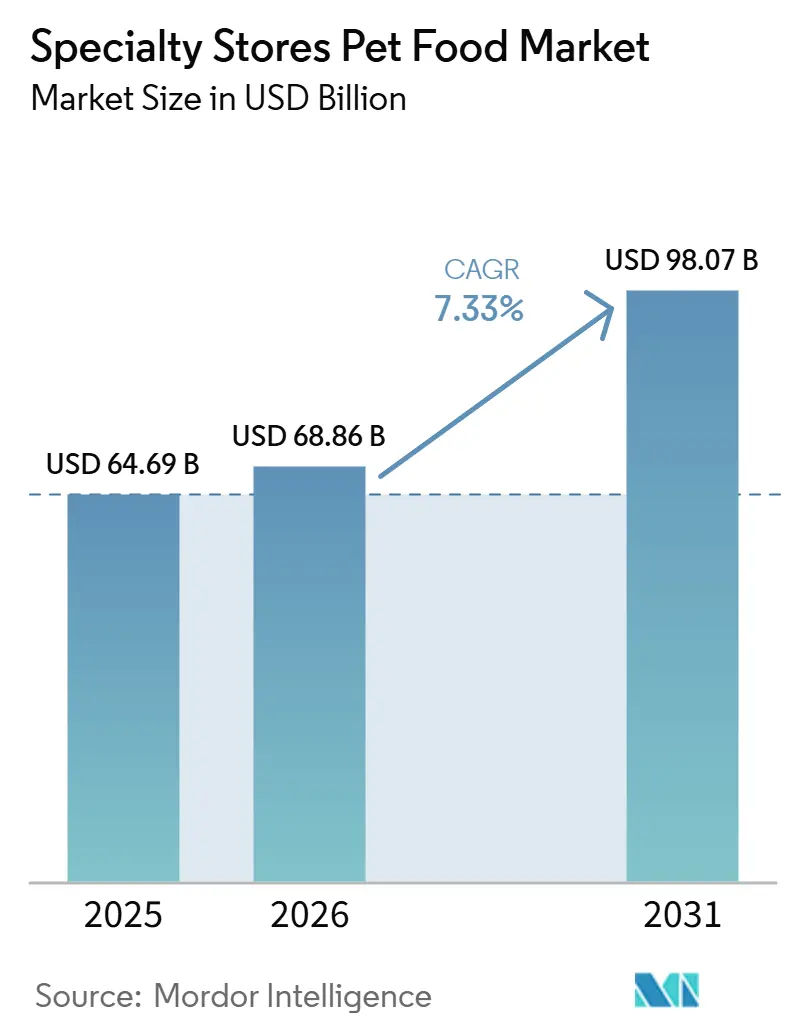

The specialty store pet food market was valued at USD 64.69 billion in 2025 and is forecast to grow from USD 68.86 billion in 2026 to USD 98.07 billion by 2031, at a CAGR of 7.33% during the forecast period (2026–2031). The specialty store pet food market holds a distinct position within pet retail, as trained staff, broader product assortments, and the ability to carry refrigerated, freeze-dried, and therapeutic products support larger basket sizes and stronger repeat purchases compared to mass retail formats. This advantage is most pronounced in premium and functional nutrition, where veterinary-backed diets and fresh products benefit from in-store guidance and consumer trust. Companion animal humanization is shifting food purchasing toward health management, directing spending into the specialty store pet food market rather than grocery or discount channels. Fresh and refrigerated formats are altering store economics due to cold-chain investment requirements, while supplements, therapeutic diets, and cross-selling are increasing visit value within the specialty store pet food market.

Key Report Takeaways

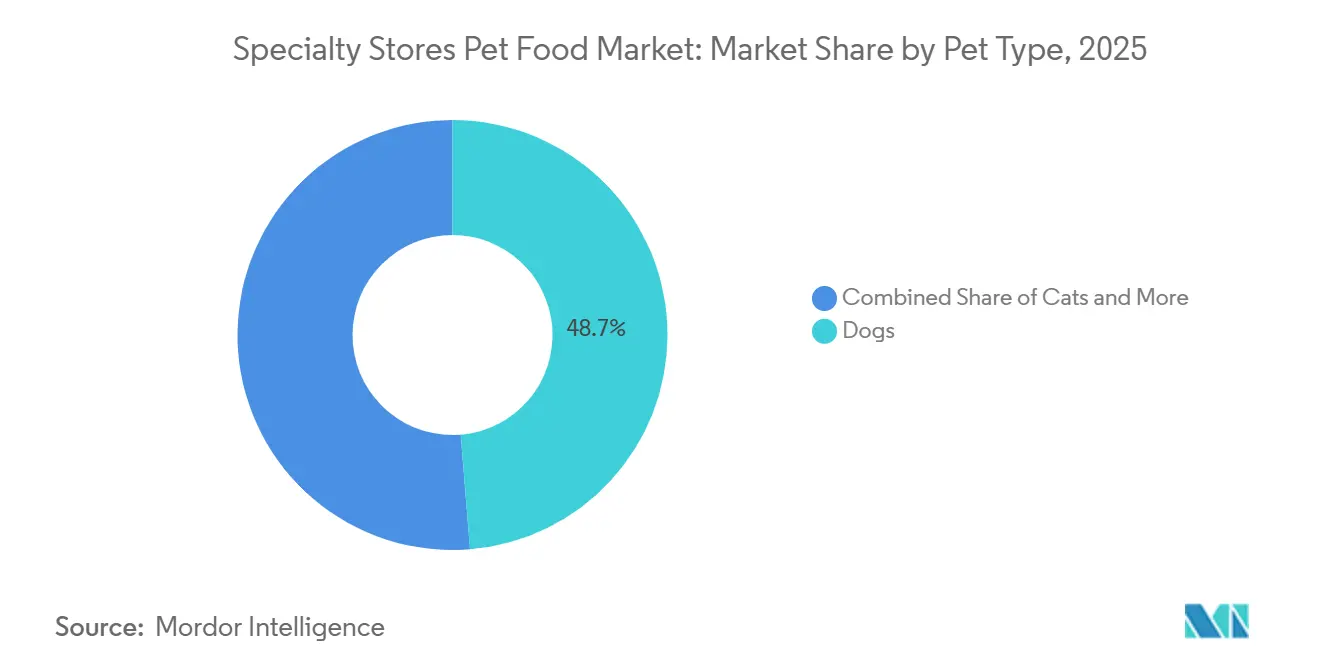

- By pet type, dogs were the largest segment and accounted for 48.7% of the specialty stores pet food market share in 2025, and are anticipated to expand at an 8.5% CAGR between 2026 and 2031.

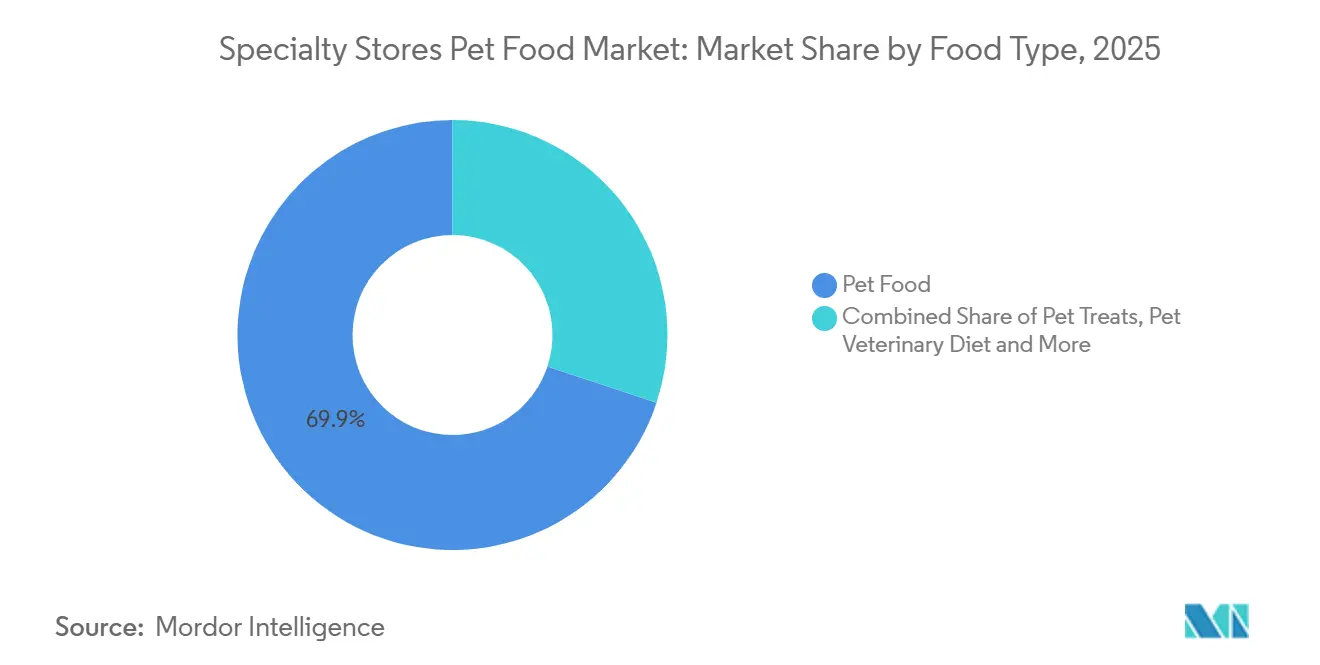

- By food type, pet food was the largest segment and held 69.9% of the specialty stores pet food market size in 2025, while pet nutraceuticals and supplements are the fastest-growing segment and are anticipated to expand at an 8.3% CAGR between 2026 and 2031.

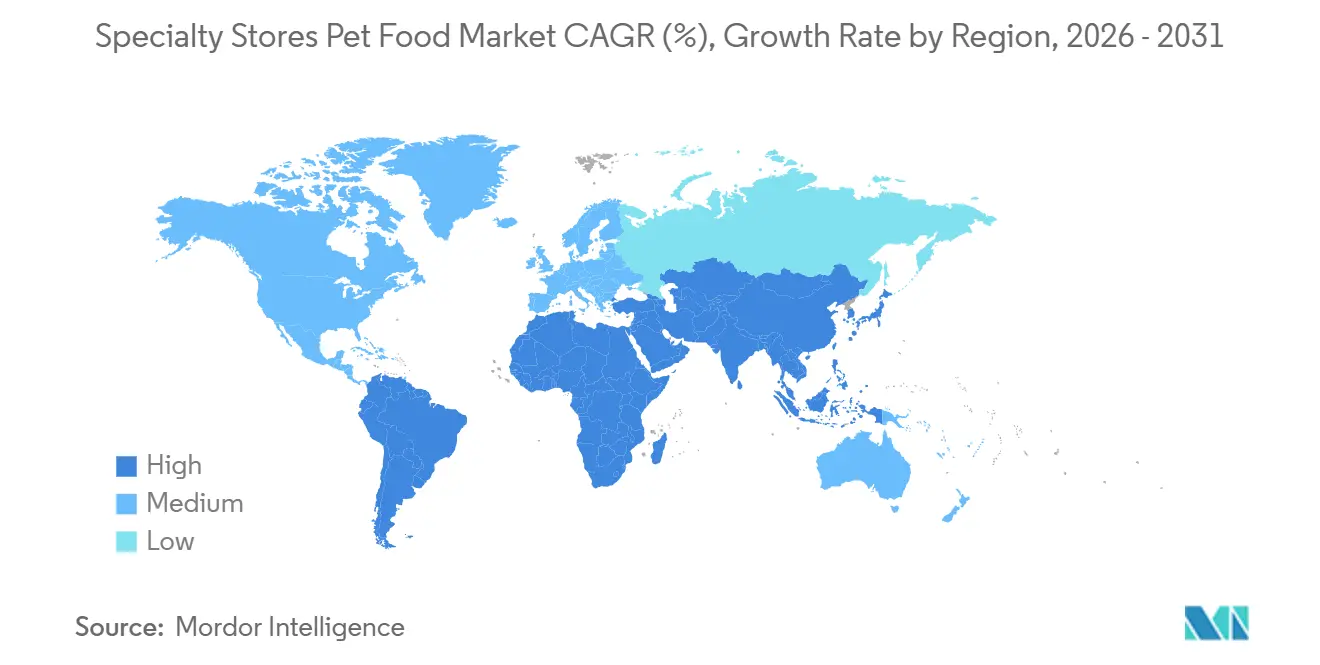

- By geography, North America was the largest segment, and held 42.5% of the market size in 2025, while Africa is the fastest-growing segment and is anticipated to expand at a 10.1% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Specialty Stores Pet Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Veterinary-endorsed premium diet adoption | +1.8% | North America and Europe core, spillover to Asia-Pacific | Medium term (2-4 years) |

| Rising demand for fresh, frozen, and therapeutic pet food | +1.5% | North America, expanding to Europe and Australia | Medium term (2-4 years) |

| Higher conversion through in-store guidance and assisted selling | +1.2% | Global, strongest in developed specialty markets | Short term (≤ 2 years) |

| Specialty retailer private label expansion | +0.9% | Europe and North America primarily | Medium term (2-4 years) |

| Loyalty programs driving repeat basket frequency | +0.8% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Growth in cross-selling of treats, supplements, and functional add-ons | +0.7% | North America and Europe, spillover to South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Veterinary-Endorsed Premium Diet Adoption

Veterinary endorsement is one of the strongest trust signals in the specialty store pet food market, as it reduces hesitation about premium, science-based formulations. In April 2025, Hill's Pet Nutrition introduced ActivBiome+ Multi-Benefit technology into its Science Diet adult and senior portfolio, with the rollout covering pet specialty stores and veterinary clinics globally [1]Source: News Article, “HILL'S PET NUTRITION ENHANCES HILL'S SCIENCE DIET PORTFOLIO WITH GAME-CHANGING MICROBIOME INNOVATION,” prnewswire.com. This is relevant to specialty outlets because they are better positioned than mass channels to explain digestive, microbiome, and life-stage claims in person. It also supports repeat purchase cycles, as feeding trials for therapeutic or functional diets typically run over several weeks, bringing shoppers back into the store more regularly. The specialty store pet food market benefits when local veterinary clinics and specialty retailers align product recommendations with in-store availability.

Rising Demand for Fresh, Frozen, and Therapeutic Pet Food

Fresh, frozen, and therapeutic products continue to reshape the specialty store pet food market, as these formats combine premium pricing with a greater need for shelf explanation. In June 2025, General Mills launched Blue Buffalo Love Made Fresh in the United States and introduced Edgard and Cooper at PetSmart stores nationwide, demonstrating how major suppliers are using the specialty channel to build premium visibility. This shift also increases infrastructure requirements, as fresh products depend on refrigerated handling from manufacturer to shelf. In the United States, the Food Safety Modernization Act (FSMA) requirements impose formal temperature-control and traceability obligations on the movement and storage of animal food. These factors make the specialty-store pet food market more accessible to larger suppliers and better-capitalized retailers that can support fresh assortments with cold-chain discipline.

Higher Conversion Through In-Store Guidance and Assisted Selling

In-store guidance gives the specialty store pet food market an advantage by converting interest in premium nutrition into actual purchases more effectively than self-serve retail formats. Data from the American Pet Products Association (APPA), cited in July 2025, showed that 54% of dog owners and 47% of cat owners were interested in premium pet food options in the United States[2]Source: News Article, “PetSmart Expands Premium Pet Nutrition Offerings Through Exclusive Partnership with Edgard & Cooper,” prnewswire.com. Specialty retail is better positioned to capture that interest because trained associates can connect product features to owner concerns during the same visit. This is particularly relevant for diets tied to breed, age, digestion, weight control, or ingredient sensitivity, as these needs often require explanation before a purchase decision is made. The specialty store pet food market benefits from this assisted-selling model because it creates a recommendation layer that supermarkets and many third-party online platforms do not replicate.

Specialty Retailer Private Label Expansion

Private label is playing an increasingly premium role in the specialty store pet food market, particularly where retailers seek stronger margins and a more differentiated assortment. At Interzoo 2026 in Nuremberg (Germany), VAFO Group showcased private-label services covering recipe development, novel proteins, and marketing support for specialty retail partners. This offering indicates that private label in specialty retail is no longer limited to entry-level alternatives and is now part of premium shelf strategy. It also gives retailers a way to build store loyalty rather than reliance on a single national brand. In the specialty store pet food market, successful premium private label can therefore improve shelf productivity while making branded access more selective.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain handling and short shelf-life losses | -0.8% | Global, acute in Africa, South America, and Southeast Asia | Long term (≥ 4 years) |

| High SKU complexity and inventory rationalization challenges | -0.6% | Global, largest chains in North America and Europe most exposed | Medium term (2-4 years) |

| Price competition from mass retail and online channels | -0.9% | North America and Europe primarily | Medium term (2-4 years) |

| Dependence on physical foot traffic in mature specialty corridors | -0.5% | North America and Europe, urban fringe markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain Handling and Short Shelf-Life Losses

Cold-chain handling is a significant operational barrier in the specialty store pet food market, as fresh and refrigerated products require strict temperature control from production to point of sale. In United States, the Food Safety Modernization Act (FSMA) regulations mandate documented temperature control and traceability for animal food, adding cost and process requirements across transport, receiving, and storage. This burden is more pronounced in emerging markets where power reliability and refrigeration access are inconsistent. Smaller specialty operators in developed markets are also affected, as refrigerated less-than-truckload distribution is difficult to manage without sufficient scale. Consequently, the specialty store pet food market tends to favor larger chains and nationally distributed brands as fresh formats expand beyond niche placement.

Price Competition from Mass Retail and Online Channels

Price pressure from mass retail and online platforms continues to challenge the specialty store pet food market, particularly in mature regions where consumers can quickly compare replenishment options. Competing channels are expanding their premium sections, exclusive online formulas, and subscription offerings, reducing one of specialty retail's earlier advantages. While in-store expertise retains its value, the need for clear differentiation at the store level has increased. Retailers that rely primarily on broad assortment face greater pressure than those that use exclusive products, staff training, and loyalty programs to support repeat purchases. The specialty store pet food market remains more resilient where service, trust, and channel-specific assortment are sufficient to offset price comparison.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Dog Segment Anchors Premium Assortment Economics

Dogs accounted for 48.7% of the specialty store pet food market share in 2025, making them the largest pet type in the channel. This position reflects higher basket values, as dog owners are more likely to purchase dry, wet, and fresh products, as well as treats, in a single visit. The specialty store pet food market also benefits from stronger referral-driven purchasing in dog nutrition, particularly for veterinary-backed and breed-specific products. Dogs are also the fastest-growing pet type and are anticipated to expand at an 8.5% CAGR between 2026 and 2031, keeping them central to premium assortment planning.

The dog segment opportunity is further supported by life-stage and size-specific feeding, as large-breed and senior products are occupying more shelf space in specialty outlets. These ranges align well with the specialty store pet food market, which relies on explanation, trust, and repeat purchases rather than price-driven impulse buying. Cat nutrition remains strategically important as household penetration rises and fresh cat food remains less developed than fresh dog food, leaving room for assortment expansion. Other pets, including birds, small mammals, and reptiles, continue to support the specialty store pet food market, as their feeding needs are more specialized and less suited to mainstream grocery retail. Association of American Feed Control Officials (AAFCO) standards support trust across pet types by providing a recognized nutritional baseline for formulas sold in specialty channels.

By Food Type: Nutraceuticals Lead Growth While Pet Food Anchors Volume

Pet food accounted for 69.9% of the specialty store pet food market in 2025, maintaining its position as the primary volume driver within the channel. Growth within this segment is being shaped more by premiumization and format mix than by unit expansion alone. High-protein dry kibble continues to anchor everyday demand, while life-stage-specific and breed-specific formulas are gaining share against general-purpose products. Pet treats remain a valuable adjacent category, as they increase basket value and support frequent assortment refreshes in the specialty-store pet food market.

Pet nutraceuticals and supplements are the fastest-growing food type and are anticipated to grow at a CAGR of 8.3% between 2026 and 2031. This segment of the specialty store pet food industry benefits from staff-led explanation, as ingredient functions and health claims often require interpretation before purchase. Pet veterinary diets also hold a strong position within the channel, combining two of its established strengths: veterinary credibility and assisted consultation. In Brazil, specialty stores held a major share of pet nutraceutical distribution in 2025, reflecting how staff training and guided selling improve conversion in health-oriented categories. This dynamic supports a broader shift toward preventive health and condition-specific nutrition within the specialty store pet food market.

Geography Analysis

North America held the largest share of the specialty store pet food market at 42.5% in 2025. The region is supported by a dense specialty retail network, high spending per pet, and strong demand for premium and therapeutic nutrition. The United States held the major market, where chains such as PetSmart and Petco have developed consultative store models that support higher-value purchases. PetSmart's Treat Rewards program reached 75 million members in 2025, and more than 90% of transactions were linked to a member account, reflecting how loyalty systems continue to support retention in this region. South America and Europe also remain important regional contributors, as both regions have established specialty retail channels and a solid base for premium pet nutrition demand.

Africa is anticipated to expand at a 10.1% CAGR between 2026 and 2031, making it the fastest-growing regional market. Growth is centered in South Africa, Egypt, Nigeria, and Kenya, where urbanization, rising disposable income, and improving access to formal retail are supporting the development of a more structured specialty pet food channel. The region is still at an earlier stage than developed markets, but expanding veterinary networks and a gradual shift toward packaged nutrition are improving the long-term outlook. Demand in Africa is building alongside retail infrastructure rather than through an already scaled channel, which distinguishes it from mature regional markets.

Asia-Pacific is supported by India, South Korea, and Southeast Asia, where pet ownership formalization and specialty retail expansion are progressing together. Specialty stores across the region are maintaining relevance by offering grooming, consultation, and product sampling that online channels cannot easily replicate. In South America, Brazil continues to anchor the region through its broad independent specialty store base. In Europe, Germany remained a key market after Zentralverband der Heimtierbranche (ZZF) and Industrieverband Heimtierbedarf (IVH) reported USD 7.6 billion (EUR 7 billion) in pet industry revenue in 2025, with specialist trade retaining a 76% channel share in accessories and specialty pet products[3]Source: News Article, “The German Pet Market 2025,” presseportal.de. In the Middle East, Gulf Cooperation Council (GCC) demand and Mars, Incorporated's January 2026 appointment of The Petshop Group as its exclusive specialty retail distribution partner in the United Arab Emirates (UAE) are supporting market activity. In Russia, geopolitical disruption and trade restrictions continue to weigh on premium imported products, driving expansion in the domestic specialty channel.

Competitive Landscape

The specialty store pet food market remains moderately consolidated. Mars, Incorporated and Nestlé S.A. continue to shape competitive dynamics through scale, broad portfolios, and channel reach. Colgate-Palmolive Company leverages Hill's Pet Nutrition to strengthen veterinary credibility, while General Mills, Inc. is expanding its presence in fresh nutrition and The J. M. Smucker Company maintains a meaningful position in treats and mainstream pet food sold through specialty retail. This competitive balance allows regional players and focused premium brands to defend profitable positions within the market.

Large suppliers are treating specialty retail as a distinct commercial channel rather than an extension of grocery distribution. In January 2026, Mars, Incorporated appointed The Petshop Group as its exclusive specialty retail distribution partner in the United Arab Emirates, reflecting a channel-specific approach to market access. In February 2025, Hill's Pet Nutrition agreed to acquire Prime100 in Australia, adding a refrigerated and shelf-stable fresh product line for specialty retailers. In June 2025, General Mills, Inc. launched Blue Buffalo Love Made Fresh in the United States and introduced Edgard and Cooper into PetSmart stores nationwide, linking premium product innovation to specialty shelf presence. These moves indicate that product innovation, veterinary credibility, and exclusive distribution arrangements remain central competitive factors in the specialty store pet food market.

The competitive landscape also includes specialists such as VAFO Group, Wellness Pet Company, and Freshpet, Inc., each building positions in targeted segments of the channel. VAFO is expanding its reach in Central and Eastern Europe through branded and private-label support for specialty partners. Wellness Pet Company continues to refresh its premium cat and dog offerings aimed at specialty retail buyers. Fresh-format expansion, microbiome-focused nutrition, and private-label support are raising the capability threshold across the market, increasingly rewarding suppliers and retailers that can combine product depth with effective channel execution.

Specialty Stores Pet Food Industry Leaders

Mars, Incorporated

Purina PetCare (Nestlé S.A.)

Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

General Mills, Inc.

The J. M. Smucker Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mars, Incorporated completed a USD 133 million (CAD 180 million) investment , across four Ontario manufacturing facilities in Canada, including a 50% production capacity increase for Temptations cat treats at the Bolton site and a 12% capacity expansion at Royal Canin’s Guelph facility.

- July 2025: VAFO Group acquired AZAN, one of the largest pet food distributors in Poland, deepening specialty channel access in Central and Eastern Europe and converting a long-standing distribution relationship into owned channel infrastructure.

- February 2025: Colgate-Palmolive’s Hill’s Pet Nutrition agreed to acquire Care TopCo, owner of the Prime100 fresh pet food brand in Australia, giving Hill’s its first refrigerated and shelf-stable fresh product line for specialty retailers and strengthening its presence in the regional Asia-Pacific channel.

Global Specialty Stores Pet Food Market Report Scope

The specialty store pet food market refers to pet nutrition products sold through dedicated pet retail formats, including national pet specialty chains, independent pet stores, and premium pet boutiques. These stores provide pet owners with trained staff guidance, curated assortments spanning dry food, wet food, fresh and freeze-dried formats, pet treats, veterinary diets, and nutraceuticals, along with personalized nutrition recommendations tailored to individual pet needs.

The Specialty Stores Pet Food Market Report is Segmented by Pet Type (Dogs, Cats and Other Pets), by Food Type (Pet Food, Pet Treats, Pet Veterinary Diet, and Pet Nutraceuticals and Supplements), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Dogs |

| Cats |

| Other Pets |

| Pet Food |

| Pet Treats |

| Pet Veterinary Diet |

| Pet Nutraceuticals and Supplements |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Poland | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Philippines | |

| Taiwan | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Pet Type | Dogs | |

| Cats | ||

| Other Pets | ||

| By Food Type | Pet Food | |

| Pet Treats | ||

| Pet Veterinary Diet | ||

| Pet Nutraceuticals and Supplements | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| Philippines | ||

| Taiwan | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecasted value of the Specialty store pet food market by 2031?

The specialty store pet food market is forecasted to reach USD 98.1 billion by 2031, rising from USD 68.9 billion in 2026 at a 7.33% CAGR between 2026 and 2031.

Which pet type leads specialty pet food sales?

Dogs lead the channel with 48.7% share in 2025 and also represent the fastest growing pet type at an anticipated 8.5% CAGR between 2026 and 2031.

Which region is expanding the fastest?

Africa is the fastest growing region with an anticipated 10.1% CAGR between 2026 and 2031, supported by formal retail expansion and wider veterinary access.

What is driving premium growth in specialty pet food retail?

Veterinary-backed diets, fresh and therapeutic products, assisted selling, and premium private-label expansion are the main forces supporting channel growth.

Page last updated on: