Online Music Education Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

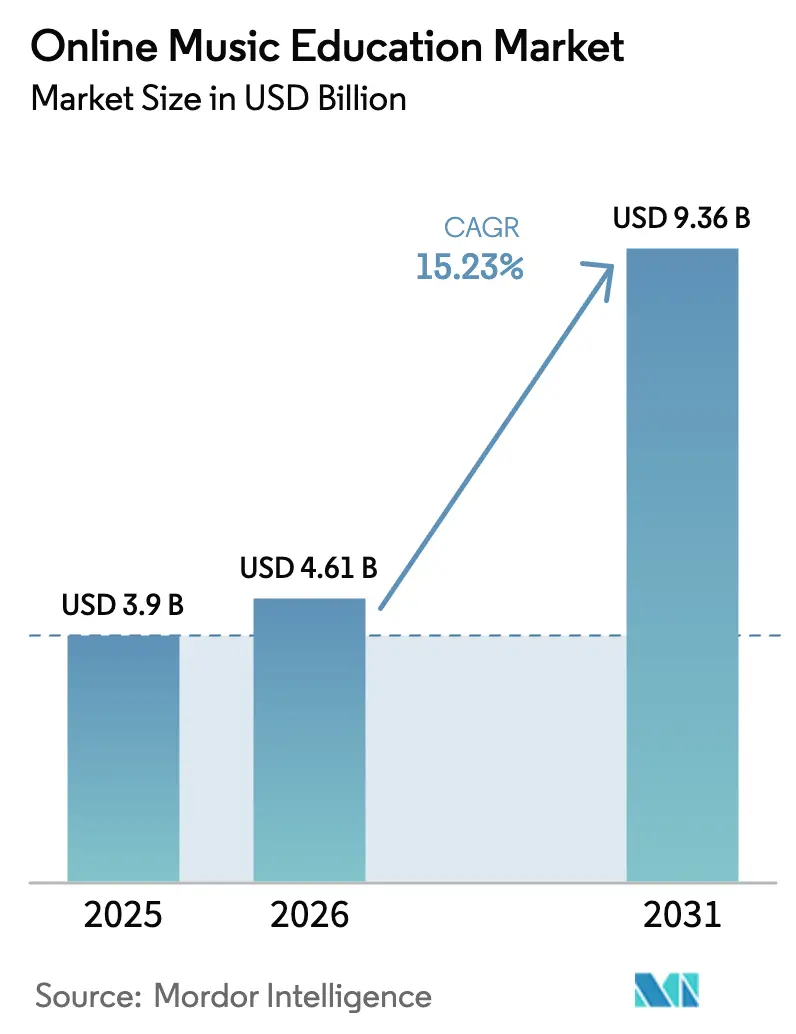

| Market Size (2026) | USD 4.61 Billion |

| Market Size (2031) | USD 9.36 Billion |

| Growth Rate (2026 - 2031) | 15.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Music Education Market Analysis by Mordor Intelligence

The Online Music Education Market size is expected to grow from USD 3.9 billion in 2025 to USD 4.61 billion in 2026 and is forecast to reach USD 9.36 billion by 2031 at 15.23% CAGR over 2026-2031. Adoption continues to accelerate as AI-powered teaching tools, rising smartphone penetration, and demand for flexible learning schedules converge to remove long-standing access barriers. Platforms that integrate real-time feedback, gamification, and adaptive lesson paths are capturing learners who expect interactive digital experiences comparable to leading consumer apps. Consolidation among content libraries and technology specialists is reshaping competitive dynamics, while tariff-related supply shocks on physical instruments threaten to lift acquisition costs for entry-level learners. Premium pricing power is gravitating toward providers that bundle instructor talent, extensive song catalogs, and proprietary AI assessment engines—capabilities that collectively boost completion rates and subscriber loyalty.

Key Report Takeaways

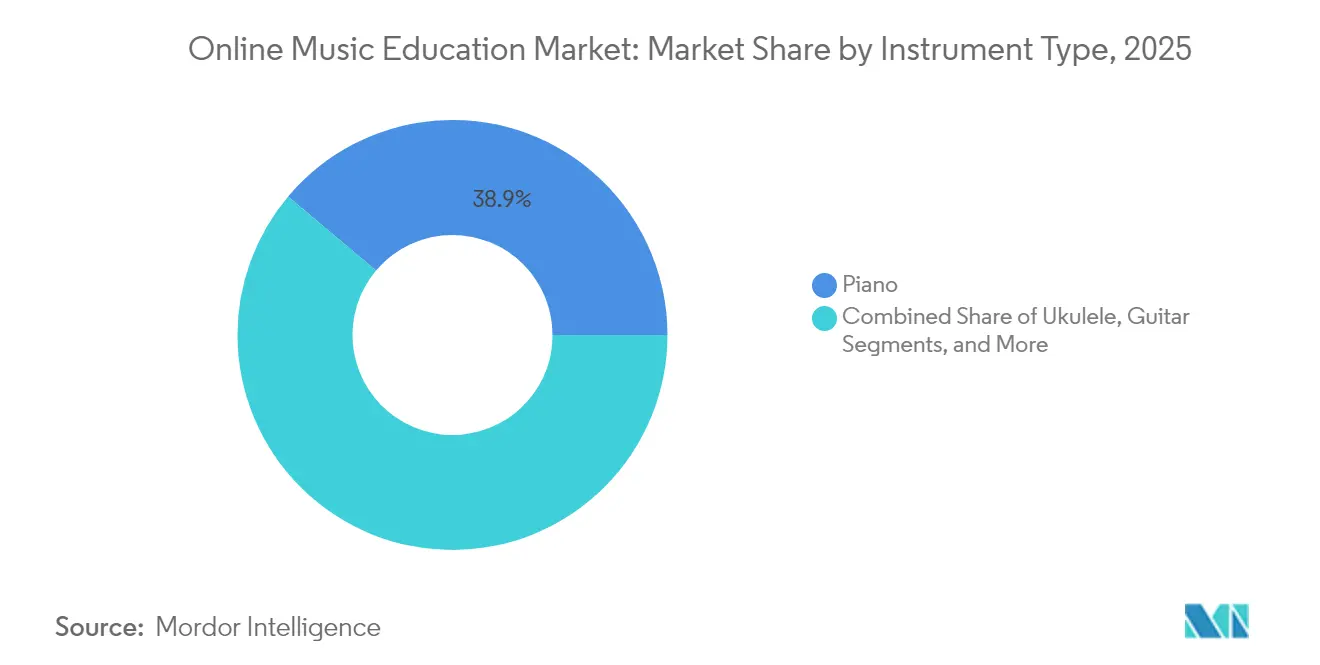

- By instrument type, piano led with 38.85% of the online music education market share in 2025; ukulele is projected to expand at a 15.55% CAGR through 2031.

- By platform, app-based solutions accounted for 50.75% revenue in 2025, while hybrid offerings are expected to grow at 16.6% CAGR to 2031.

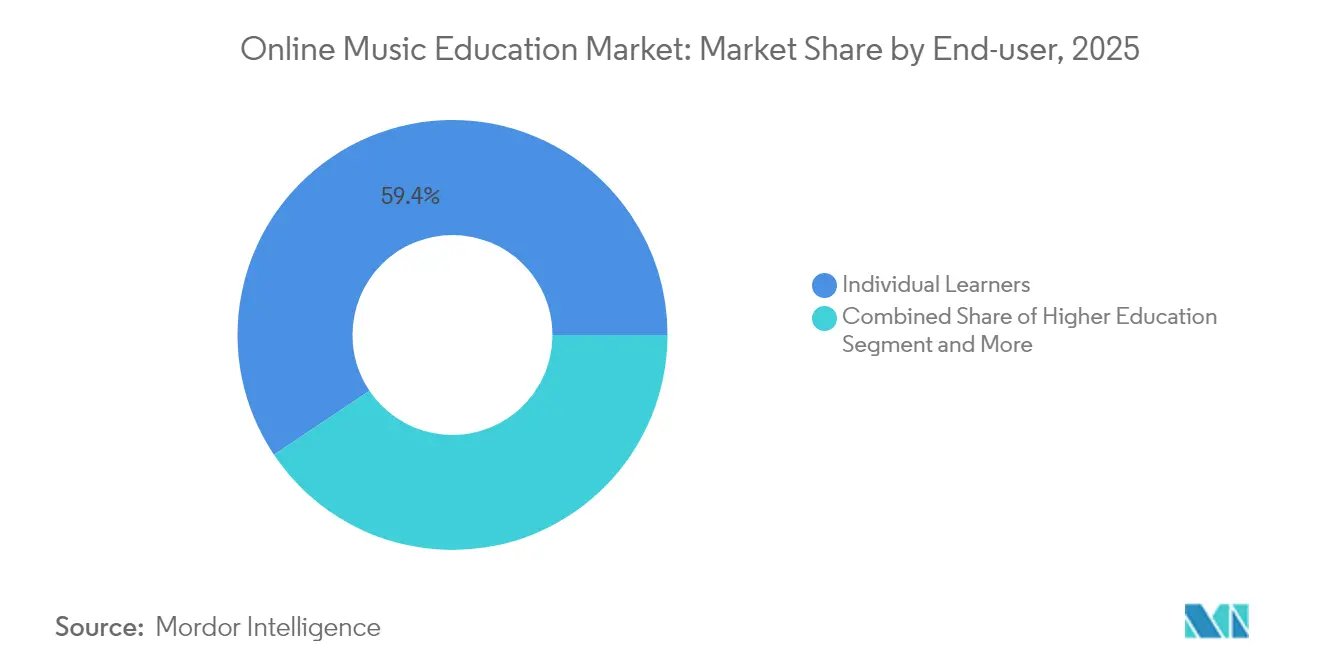

- By end-user, individual learners captured 59.40% of 2025 revenue; corporate and professional development is on track for a 16.45% CAGR through 2031.

- By learning model, self-paced courses represented 49.05% of 2025 spending as the largest slice of the online music education market size; live one-to-one instruction is advancing at a 16.1% CAGR between 2026-2031.

- By session format, one-to-one lessons contributed 47.10% of 2025 revenue, whereas masterclass and workshop formats are poised for a 16.3% CAGR to 2031.

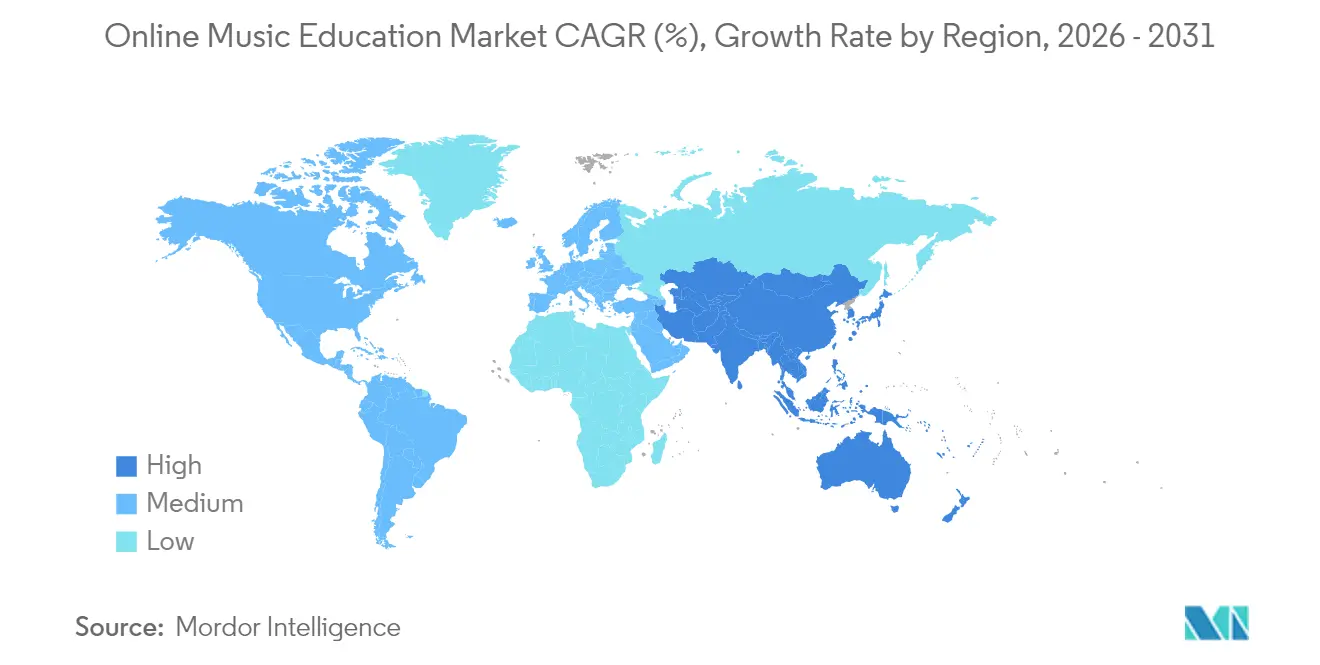

- By geography, North America controlled 35.05% revenue in 2025; Asia-Pacific will expand quickest at 16.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Music Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of interactive e-learning platforms | +3.2% | Global, with stronger adoption in North America and APAC | Medium term (2-4 years) |

| Rising demand for personalized, adaptive learning experiences | +2.8% | Global, led by developed markets | Long term (≥ 4 years) |

| Expansion of high-speed internet and smartphone penetration | +2.1% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Post-COVID normalization of remote skill-building | +1.6% | Global, with sustained impact in developed markets | Medium term (2-4 years) |

| AI-enabled real-time feedback accelerating practice efficiency | +2.4% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Corporate creator up-skilling programs fueling B2B demand | +1.9% | North America and EU, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Interactive E-Learning Platforms

Interactive ecosystems that reward practice streaks, display progress dashboards, and offer instant audio-based corrections now underpin user loyalty. Yousician’s community of 20 million monthly active users confirms that gamified loops translate into sustained practice frequencies. [1]Yousician, “About Yousician | Company Overview,” yousician.com Across six-month trials, students inside interactive cohorts recorded elevated emotional-intelligence scores relative to static-video peers. Bidirectional LSTM models evaluating pitch and rhythm with 91.9% accuracy enable automated scoring once reserved for human instructors. Self-paced segments benefit most, as algorithmic grading bridges feedback gaps inherent in asynchronous study and further cements the online music education market as a primary pathway for new learners.

Rising Demand for Personalized, Adaptive Learning Experiences

Learners increasingly expect lessons to adjust in real time to pace, genre preference, and skill deficiencies. Artie, ArtMaster’s AI piano tutor funded with EUR 800,000, delivers customized finger-position drills tuned to user error patterns. [2]Vestbee, “Czech startup ArtMaster raises €800k to launch and develop Artie,” vestbee.com Corporate programs mirror this trend; Samsung’s leadership cohort logged measurable emotional-intelligence gains after bespoke music sessions. Subscription churn declines when platforms push user-specific repertoire choices, underscoring personalization as a retention lever inside the broader online music education market.

Expansion of High-Speed Internet and Smartphone Penetration

Enterprises in Asia-Pacific scale fastest because smartphone adoption outruns fixed broadband in populous economies. India’s 891 billion streams in 2024 signal a cultural shift in which on-demand music becomes a gateway into structured lessons. App-based interfaces exploiting device-native microphones already own 51.3% revenue, proof that connectivity drives the online music education market toward mobile-first UX paradigms. Hybrid cloud syncing then lets learners pick up progress on larger desktop screens without friction.

AI-Enabled Real-Time Feedback Accelerating Practice Efficiency

Ultimate Guitar’s Practice Mode analyzes pitch and rhythm against 23,000 official tabs, delivering corrective hints within milliseconds. Patent filings from Sony outline ambisonic soundfield engines that immerse players in spatial audio, enhancing ear-training accuracy. As accuracy rates approach instructor parity, platforms compress time-to-competency, reinforcing the premium learners place on digital feedback loops across the online music education industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and privacy concerns on cloud lesson archives | -1.8% | Global, with heightened sensitivity in EU and North America | Short term (≤ 2 years) |

| Freely available tutorial content diluting paid platform value | -2.3% | Global, particularly impacting premium subscription models | Medium term (2-4 years) |

| Latency and audio-quality limits hamper nuanced instruction | -1.5% | Emerging markets with limited infrastructure | Short term (≤ 2 years) |

| Instructor income volatility under revenue-share models | -1.1% | Global, affecting platform sustainability | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Security and Privacy Concerns on Cloud Lesson Archives

General Data Protection Regulation enforcement and emerging US state-level privacy laws intensify compliance expenses for mid-tier providers. Continuous microphone monitoring records intimate practice sessions that, if breached, would erode trust quickly. Institutional buyers hesitate to onboard platforms until encryption audits pass, slowing B2B uptake that otherwise could broaden the online music education market.

Freely Available Tutorial Content Diluting Paid Platform Value

YouTube channels and social platforms release high-quality beginner courses at zero cost, compressing entry-level price points. Paid services must therefore out-innovate with AI feedback, celebrity masterclasses, or accredited pathways to defend margins. Development budgets rise in parallel, shrinking profitability for smaller players and raising break-even thresholds inside the online music education industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Instrument Type: Piano Dominance Drives Traditional Learning

Piano courses anchored 38.85% of revenue in 2025 and continue to define foundational pedagogy within the online music education market. Virtual keyboards render visual note-on timing, simplifying harmonic instruction and enabling automated scoring engines to detect finger placement mistakes. The segment benefits from decades of digital-piano penetration so that learners can practice silently with MIDI connectivity, a feature widely exploited by app-based tutors.

Ukulele enrollments rise on a 15.55% CAGR, reflecting consumer gravitation toward low-cost, fast-gratification instruments. Learners often complete their first song within days, which heightens motivation and builds positive feedback loops that strengthen overall subscriber stickiness. Guitar remains a large secondary pillar, aided by expansive song libraries and social cachet across pop genres. Violin, drums, and wind-brass categories remain niche but are gaining as mixed-reality prototypes promise haptic bowing or breath-pressure analytics that will widen addressable audiences.

By Platform: App-Based Solutions Lead Digital Transformation

App ecosystems captured 50.75% revenue in 2025 thanks to mobile ubiquity, single-tap onboarding, and push-notification nudges that reinforce practice habits. Real-time audio ingestion on-device paired with cloud AI inference lowers latency and operating costs while safeguarding intellectual property. Hybrid deployments are accelerating at a 16.6% CAGR, signaling demand for seamless transitions between small-screen convenience and large-screen notation workspaces.

Web platforms hold relevance for advanced composition and multi-track editing, where panoramic screen real estate is critical. Providers embed MIDI editors and multichannel recording features unavailable on smartphones. As broadband speeds climb, progressive-web-app architectures narrow the distinction between downloaded apps and browser experiences, tightening competition across distribution formats inside the online music education market.

By End-user: Individual Learners Drive Market Foundation

Self-funded hobbyists and aspiring musicians controlled 59.40% of 2025 spending, validating the direct-to-consumer thesis that underpins early platform scaling strategies. This cohort values 24/7 access, bite-sized lessons, and community leaderboards. K-12 and higher-education channels adopt more slowly due to curriculum alignment needs, but bring larger seat counts once integrated into learning-management systems.

Corporate and professional development bookings outpace all other end-users at 16.45% CAGR as firms integrate music modules into wellness or creativity workshops. Evidence from Samsung’s executive cohorts shows measurable emotional-intelligence lift, encouraging HR budgets to allocate toward musical training as a soft-skills lever. Music schools and conservatories leverage online modules to supplement in-person ensemble practice, extending reach to international applicants and buoying brand visibility.

By Learning Model: Self-Paced Dominance Reflects Flexibility Demand

Self-paced courses own 49.05% of revenue and illustrate the centrality of asynchronous video lessons, interactive quizzes, and AI grading against uploaded playbacks. Busy adults appreciate pausing and rewinding at will, a factor that cements user satisfaction scores. The online music education market size for live one-to-one instruction is poised to swell due to a 16.1% CAGR, supported by HD low-latency video conferencing APIs that bridge geographic gaps between students and master performers.

Blended models mix prerecorded curriculum with periodic live check-ins, combining scale efficiencies with motivational boosts from human coaching. Group classes, although price-friendly, face retention challenges when learner skill dispersion widens. Adaptive scheduling powered by AI forecasting of practice trends is emerging as a differentiator, nudging students toward optimal lesson cadences.

By Session Format: One-to-One Instruction Maintains Premium Position

Personal lessons captured 47.10% of spending in 2025, underlining the willingness of learners to pay for bespoke critique and rapid skill correction. AI diagnostics augment instructors by flagging micro-timing issues, letting tutors focus on musical interpretation instead of basic error spotting. Small group cohorts prosper where peer accountability encourages practice while retaining cost efficiency.

Masterclass and workshop enrollments, forecast to grow 16.3% annually, illustrate a rising appetite for short, high-intensity sessions with headline artists. Platforms curate limited-seat events, integrate moderated Q&A, and leverage multi-camera production values to replicate backstage environments. Webinars targeting theory fundamentals tap larger audiences at lower price points, broadening the online music education market without cannibalizing premium private-lesson segments.

Geography Analysis

North America delivered 35.05% of 2025 revenue for the online music education market and benefits from entrenched broadband infrastructure, high device ownership, and a mature subscription economy that smooths recurring-revenue adoption. Venture funding levels sustain rapid feature rollouts, while university and K-12 pilots legitimize online modalities. Tariff hikes on Chinese instruments from 11% to 145% present a headwind that platforms mitigate by partnering with rental services or embedding virtual instrument simulators.

Asia-Pacific records the fastest expansion at 16.55% CAGR, tied to surging smartphone ownership and cultural emphasis on extracurricular music training. India’s status as the second-largest streaming nation with 891 billion annual streams underscores the funnel opportunity into structured lessons. Chinese growth in paid digital music surpassed 28.4% during 2024, driving domestic platforms to localize curricula and integrate traditional instruments such as guzheng and erhu.

Europe shows steady but lower-velocity uptake given already high baseline music literacy and stringent privacy rules. Providers that align with multilingual content needs and comply with GDPR garner institutional contracts. South America, the Middle East, and Africa trail in revenue contribution yet post double-digit gains as 4G networks blanket urban centers and cashless micro-payment systems reduce friction for monthly subscriptions. Government-backed digital-literacy drives further embolden adoption across these regions, nudging the global online music education market toward a more balanced geographic revenue mix by decade's end.

Competitive Landscape

The market remains moderately concentrated. The merger between Hal Leonard and Muse Group pools 5.5 million scores and instructional assets, allowing algorithmic recommendation engines to draw from unmatched catalogs. [4]Muse Group, “Hal Leonard joins Muse Group: Uniting two content leaders on a shared mission,” mu.se Yousician leverages network effects from 20 million monthly active users, positioning its freemium funnel as an asset for upselling multi-instrument pathways. Flowkey specializes in premium piano arrangements with synchronous sheet-music scrolling, capturing higher average revenue per user.

Technology innovation is the principal moat. Sony’s ambisonic patents and Yamaha’s acoustic-parameter editors raise experiential bars that smaller rivals struggle to meet. Ultimate Guitar embeds real-time feedback across 23,000 licensed tabs, cementing guitarist loyalty. Regional startups such as Artium Academy in India localize Bollywood repertoire and Hindi-language instruction, carving niches outside Western-centric catalogs. Corporate training and mixed-reality instruments remain fertile white spaces likely to spur further alliances and acquisitions in the online music education industry.

Online Music Education Industry Leaders

Yousician Ltd.

JoyTunes Ltd.

Flowkey GmbH

Skoove GmbH

Lessonface Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Muse Group unified Hal Leonard US and Europe operations, launching MuseClass for educators with AI-driven classroom tools.

- April 2025: Splice purchased Spitfire Audio for USD 50 million to fuse AI composition features with education-focused sample libraries.

- March 2025: ArtMaster raised USD 872,000 to build Artie, an AI piano tutor slated for iOS release in English-speaking markets.

- February 2025: Ultimate Guitar rolled out Practice Mode that evaluates pitch and rhythm in real time for UG PRO subscribers.

- January 2025: Conduction secured USD 265,000 to scale its digital songwriting curriculum targeting schools without music programs.

Global Online Music Education Market Report Scope

The online music education sector encompasses a diverse array of digital solutions and services crafted to support the instruction and acquisition of musical skills via the internet. These solutions are tailored to individuals of varying ages and proficiency levels, ranging from novices to accomplished musicians.

The online music education market is segmented by instrument type (piano, guitar, banjo, violin, other types), by platform (web based, app based), by end-user (individual learners, institutions, music schools, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Piano |

| Guitar |

| Violin |

| Ukulele |

| Drums and Percussion |

| Wind and Brass |

| Other Instruments |

| App-Based |

| Web-Based |

| Hybrid (App + Web) |

| Individual Learners |

| K-12 Institutions |

| Higher Education |

| Music Schools and Conservatories |

| Corporate/Professional Development |

| Self-Paced Asynchronous Courses |

| Live Instructor-Led One-to-One |

| Live Instructor-Led Group Classes |

| Blended (Live + Self-Paced) |

| One-to-One |

| Small Group (2–5 Learners) |

| Large Group/Webinar |

| Masterclass/Workshop |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Instrument Type | Piano | ||

| Guitar | |||

| Violin | |||

| Ukulele | |||

| Drums and Percussion | |||

| Wind and Brass | |||

| Other Instruments | |||

| By Platform | App-Based | ||

| Web-Based | |||

| Hybrid (App + Web) | |||

| By End-user | Individual Learners | ||

| K-12 Institutions | |||

| Higher Education | |||

| Music Schools and Conservatories | |||

| Corporate/Professional Development | |||

| By Learning Model | Self-Paced Asynchronous Courses | ||

| Live Instructor-Led One-to-One | |||

| Live Instructor-Led Group Classes | |||

| Blended (Live + Self-Paced) | |||

| By Session Format | One-to-One | ||

| Small Group (2–5 Learners) | |||

| Large Group/Webinar | |||

| Masterclass/Workshop | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the online music education market?

The online music education market size is USD 4.61 billion in 2026.

How fast is the market expected to grow?

Revenue is projected to rise at a 15.23% CAGR, reaching USD 9.36 billion by 2031.

Which region is expanding the quickest?

Asia-Pacific leads with a forecast 16.55% CAGR due to rising smartphone adoption and larger middle-class demand for extracurricular learning.

Which instrument category dominates online lessons?

Piano courses account for 38.85% of 2025 revenue, reflecting their foundational role in digital pedagogy.

Why are hybrid platforms gaining popularity?

Hybrid models allow learners to switch seamlessly between mobile convenience and desktop-level notation features, explaining their 16.6% projected CAGR.

How are AI tools changing online music instruction?

Machine-learning engines now deliver 91.9% accurate real-time feedback on pitch and rhythm, reducing dependence on human instructors and improving practice efficiency.

Page last updated on: