Online Language Learning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

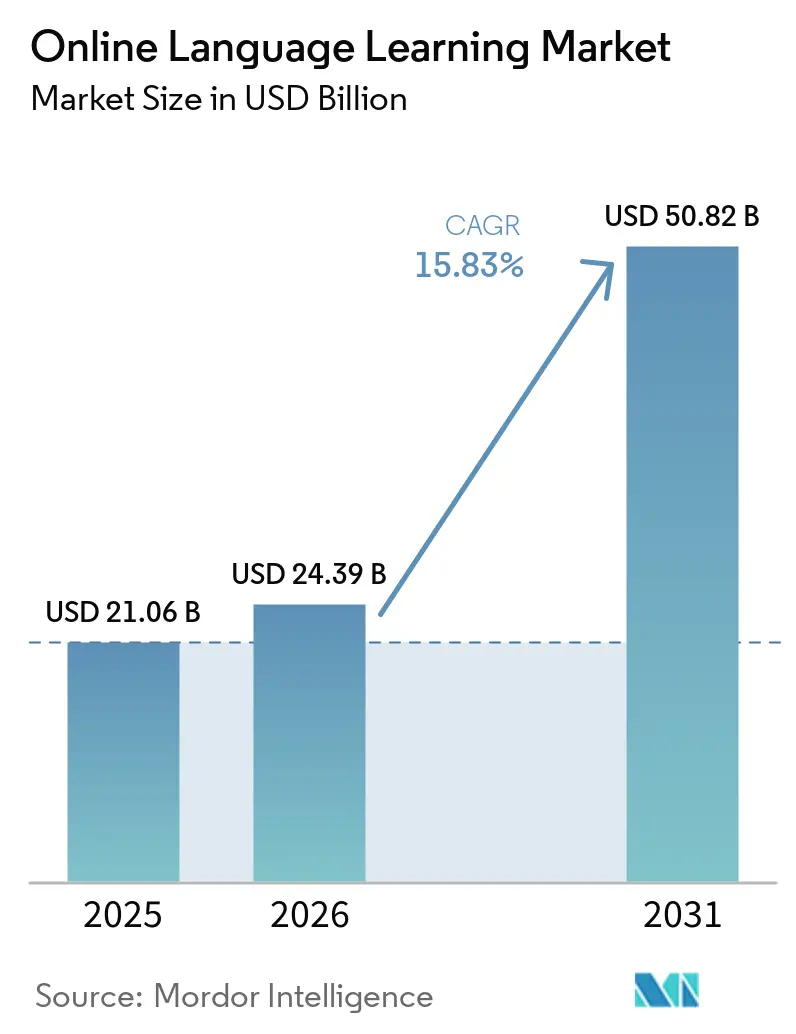

| Market Size (2026) | USD 24.39 Billion |

| Market Size (2031) | USD 50.82 Billion |

| Growth Rate (2026 - 2031) | 15.83% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

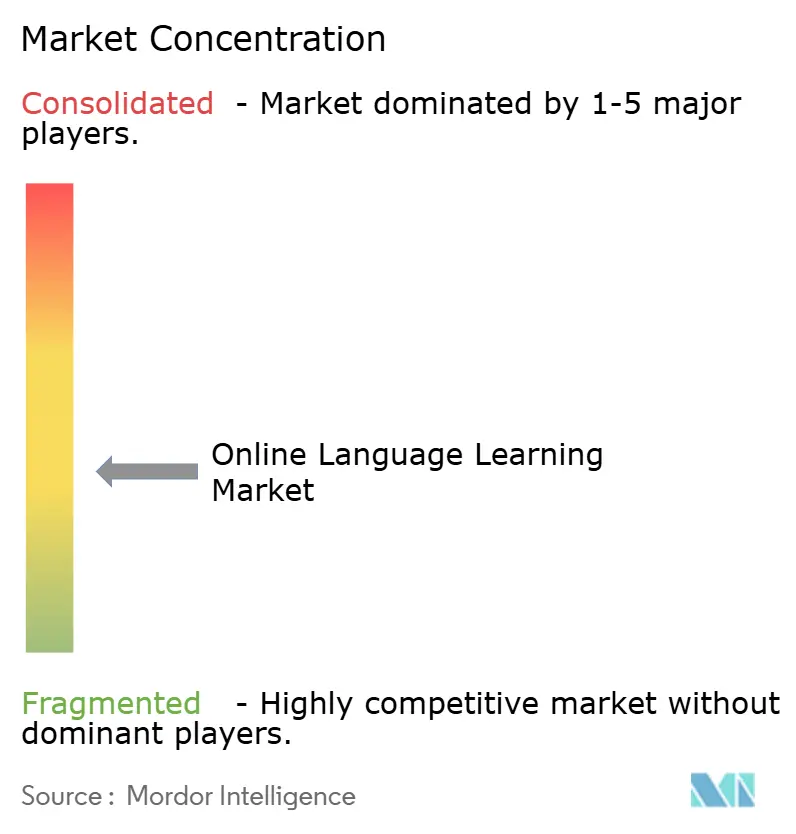

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Online Language Learning Market Analysis by Mordor Intelligence

The online language learning market size was valued at USD 21.06 billion in 2025 and estimated to grow from USD 24.39 billion in 2026 to reach USD 50.82 billion by 2031, at a CAGR of 15.83% during the forecast period (2026-2031). Growing cross-border trade, demographic shifts, and rapid mobile adoption keep demand high, while AI-driven personalization and immersive technologies strengthen learning effectiveness. Platforms deliver ever-larger course catalogues and adaptive paths that improve retention, a key differentiator in an increasingly competitive landscape. Corporates accelerate spending on workforce language skills to meet ESG and DEI goals, and public-sector budgets for multilingual programs further expand the accessible learner base. Meanwhile, strict data-privacy regimes in Europe and rising user-acquisition costs in saturated freemium channels temper growth, encouraging platforms to refine monetization strategies and diversify revenue streams.

Key Report Takeaways

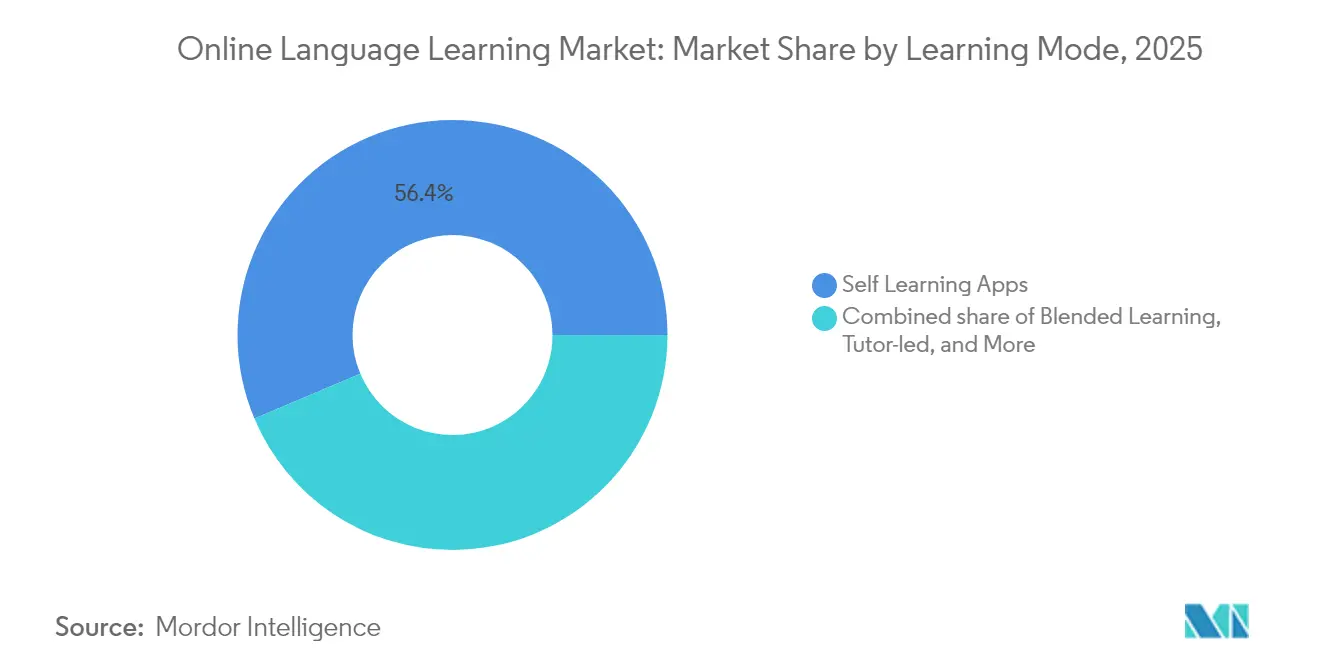

- By learning mode, self-learning apps led with 56.35% of online language learning market share in 2025, whereas tutor-led live instruction is set to grow at a 21.25% CAGR through 2031.

- By end-user, the individual segment accounted for 47.35% of online language learning market size in 2025; corporate learners are expanding at 23.70% CAGR to 2031.

- By language, English captured 54.85% of 2025 revenue, while Spanish is poised for a 20.20% CAGR through 2031.

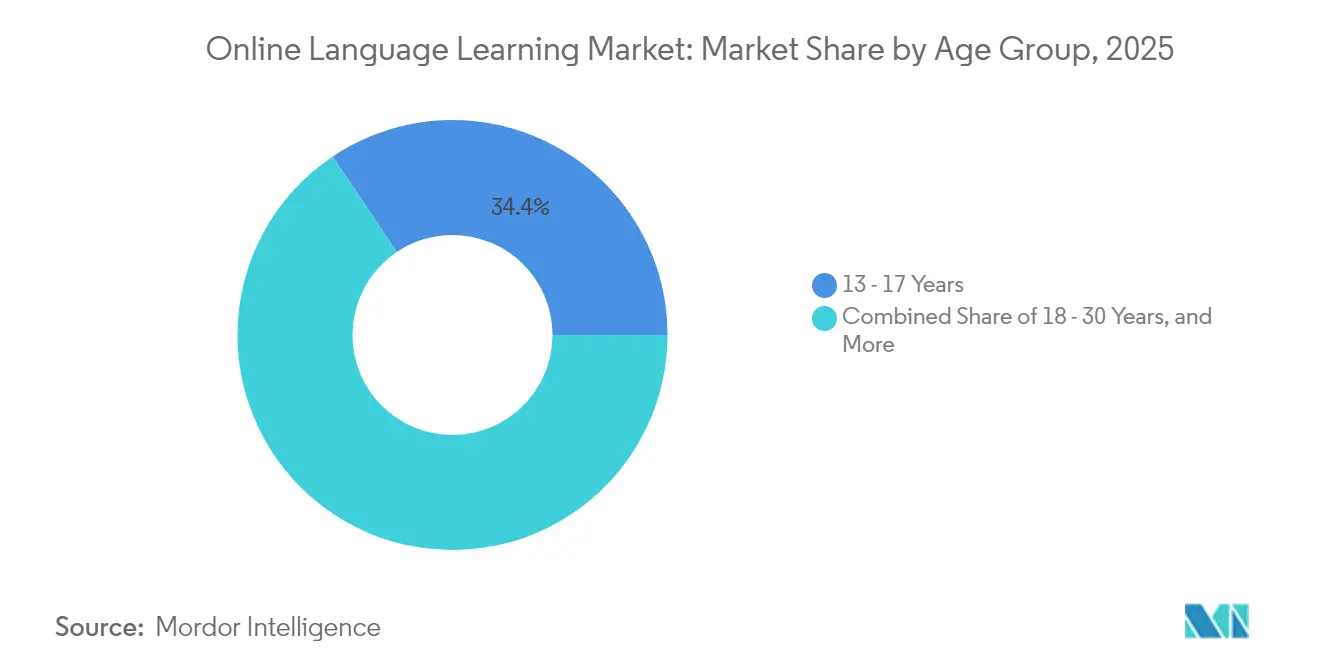

- By age group, learners aged 13-17 held 34.40% of 2025 revenue; the 18-30 cohort is progressing at a 19.12% CAGR up to 2031.

- By technology platform, mobile applications represented 62.05% of online language learning market size in 2025, and VR/AR tools are on track for 31.10% CAGR growth.

- By geography, Asia-Pacific commanded 45.75% revenue in 2025; South America is forecast to post a 21.90% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Language Learning Market Trends and Insights

Driver Impact Analyis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Globalisation-driven cross-border communication demand | +4.2% | Global; strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| AI-powered adaptive learning penetration | +3.8% | Global; led by North America and Europe | Short term (≤ 2 years) |

| Mobile-first uptake in emerging economies | +3.1% | Asia-Pacific, South America, Africa | Medium term (2-4 years) |

| Corporate ESG and DEI language-upskilling mandates | +2.4% | North America, Europe; expanding in Asia-Pacific | Long term (≥ 4 years) |

| Early-age language mandates in K-12 curricula | +1.8% | Europe, Asia-Pacific; now global | Long term (≥ 4 years) |

| Voice-assistant ecosystem skill marketplaces | +1.5% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Globalisation-driven cross-border communication demand

Intensifying international trade turns language proficiency into a core competitiveness lever. Enterprises across technology, tourism, and finance invest in scalable online language programs to remove communication bottlenecks. Providers like Open English have broadened Latin American access by marketing English skills as an economic mobility enabler. Regional trade blocs also lift demand for Portuguese and Spanish, underscoring multi-directional growth beyond English [1] University of Louisville, “Portuguese Language Demand in South America,” louisville.edu.

AI-powered adaptive learning penetration

Artificial-intelligence engines now adjust content sequencing, difficulty, and feedback in real time, raising completion rates and upsell potential. Duolingo integrates generative AI to personalize review loops and pronunciation drills, an investment detailed in its 2024 SEC filing [2]Duolingo Inc., “Form 10-K FY 2024,” sec.gov. Venture funding echoes this trend: Speak’s valuation surpassed USD 1 billion after proving conversational AI can support a billion spoken sentences and premium adoption. Platforms that align AI with privacy-by-design guidelines build durable differentiation under Europe’s strict data regime.

Mobile-first uptake in emerging economies

Smartphone growth neutralizes infrastructure gaps in India, Indonesia, and Colombia, letting learners access bite-sized lessons during idle moments. Academic reviews show mobile-assisted language learning heightens verbal practice opportunities for rural students, further widening the addressable base. Freemium apps exploit app-store discoverability but face higher acquisition costs; sustained engagement architecture is now essential for viable unit economics.

Corporate ESG and DEI language-upskilling mandates

Large employers embed language training budgets within inclusion scorecards and supplier audits. The U.S. federal allocation of USD 1.2 billion for English Language Acquisition highlights policy tailwinds supporting workplace multilingualism. Speak for Business secured 200+ enterprise clients with an 85% rollout rate, demonstrating that outcome-linked dashboards and LMS integrations unlock longer contracts and lower churn.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and privacy concerns | -2.1% | Global; peak impact in Europe and North America | Short term (≤ 2 years) |

| Low course-completion and high churn rates | -1.8% | Global; freemium strongly affected | Medium term (2-4 years) |

| Freemium-model revenue saturation | -1.3% | Mature markets worldwide | Medium term (2-4 years) |

| AI copyright / ethics regulatory barriers | -0.9% | North America, Europe; rising in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-security and privacy concerns

GDPR rules prohibit unchecked voice-data transfers to third-party AI processors, forcing platforms to build costly private speech-recognition pipelines. New localization mandates further raise overhead, compressing smaller entrants’ margins and nudging the market toward scale players with in-house compliance teams.

Low course-completion and high churn rates

Industry reports place first-week churn above 60% for many freemium apps, eroding lifetime value and inflating marketing spend. Richer feedback loops, gamified streaks, and social accountability tools are now critical to stabilize cohorts—yet over-gamification risks trivializing learning, creating a delicate optimization challenge for product managers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Learning Mode: Self-learning apps maintain scale while live tutoring accelerates

Self-learning apps generated 56.35% of 2025 revenue, underpinning the online language learning market’s largest delivery channel. This dominance relies on always-on accessibility, micro-lesson design, and algorithmic personalization that lower per-learner cost. However, tutor-led live instruction is advancing at 21.25% CAGR, reflecting heightened demand for real-time conversation that algorithms still only partially simulate. Hybrid pathways—recorded modules plus weekly tutor sessions—emerge as the retention sweet-spot, helping platforms defend subscription pricing. Preply’s marketplace illustrates the financial upside of such blended delivery, with session bookings rising alongside subscription upgrades. Continued innovation in scheduling automation and pay-per-minute billing is expected to pull more independent instructors onto aggregated platforms, deepening supply and compressing lesson prices to learners’ benefit.

Rising broadband quality in emerging markets further boosts live tutoring uptake by mitigating latency that previously hindered synchronous video practice. Conversely, self-learning incumbents invest in AI voice partners to replicate tutor feedback. The dual strategy indicates the online language learning market will not polarize; rather, integrated workflows will dominate. Providers that dynamically route learners between self-study and live conversation based on progress signals could see higher lifetime value and lower churn.

By End-user: Corporates unlock premium ARPU even as consumers remain the volume anchor

Individuals held 47.35% of 2025 revenue—a foundational pillar of the online language learning market. Price-sensitive consumers gravitate toward freemium models, forcing platforms to balance ad loads and feature gating. In contrast, corporate clients, expanding at 23.70% CAGR, purchase bulk licences bundled with analytics dashboards and single-sign-on integrations that command 6-8× higher ARPU. Speak for Business reports 85% internal adoption within client firms, reinforcing the stickiness of enterprise rollouts.

Public-sector allocations strengthen demand from schools and workforce-integration programs. U.S. English Language Acquisition grants, for instance, stimulate district-level procurement of adaptive solutions, thereby funneling learners into long-term online ecosystems . The cross-subsidy effect allows vendors to reinvest in consumer feature development, illustrating the symbiotic revenue model spanning consumer and B2B sub-markets within the broader online language learning market.

By Language: English supremacy persists while Spanish growth reshapes portfolios

English retained 54.85% revenue share in 2025, consolidating its role as the default L2 target across corporate and academic contexts. Yet Spanish, clocking a 20.20% CAGR, is inducing major platforms to localize course flows and marketing assets for bilingual U.S. and Latin American audiences. Dual-direction demand—English-Spanish and Spanish-English—expands total addressable hours of instruction without content duplication, improving content ROI.

Portuguese uptake in Brazil highlights a regional dimension often underserved by global apps. University of Louisville research notes rising Portuguese acquisition among neighboring Spanish-speaking professionals. For the online language learning market, tailoring cultural references and regional dialect options becomes decisive for engagement metrics, pushing content teams toward modular authoring systems that support rapid localization.

By Age Group: Teens still lead but young professionals set monetization pace

Learners aged 13-17 contributed 34.40% of 2025 revenue, reflecting curriculum mandates and parental subscription support. Gamified progress tracking matches teen motivation profiles, helping vendors maximize daily active users. Simultaneously, the 18-30 demographic advances at 19.12% CAGR as career-oriented learners seek certified proficiency to secure remote work and international assignments. Their willingness to pay for accelerated pathways allows premium tiers—priority tutor slots, exam prep courses, and professional certificates—to flourish.

Retention signals show young professionals exceed average lesson streaks when progression maps to career KPIs such as TOEIC or IELTS scores. This group’s feedback has sparked condensed “sprint” course formats that fit work schedules, broadening the online language learning market’s product architecture. Higher retention among professional cohorts could rebalance revenue mix toward premium subscriptions, partially offsetting teen cohort seasonality.

By Technology Platform: Mobile leads while VR/AR adds immersive depth

Mobile apps captured 62.05% of 2025 revenue and remain the on-ramp for most new users. Push notifications and offline modes keep engagement high during commutes, cementing mobile as the fulcrum of the online language learning market. However, VR/AR tools racing at 31.10% CAGR introduce situational context—ordering food, attending meetings—that accelerates speaking confidence. Portfolio examples such as Mondly VR transport learners into cafés and airports, giving spontaneous dialogue practice that flat-screen interfaces cannot match.

Hardware affordability and content authoring toolkits will dictate adoption speed. Meanwhile, privacy constraints limit voice-assistant features that depend on cloud-based speech analysis, impeding feedback quality in smart-speaker environments. Platform roadmaps therefore foreground on-device inference models to reconcile immersive feedback with regulatory compliance.

Geography Analysis

Asia-Pacific, with 45.75% of 2025 revenue, remains the engine of the online language learning market. China’s urban learners pay for premium English tracks that facilitate overseas study, while India’s young mobile-native population leans on freemium tiers to supplement exam preparation. Government multilingual policies in Indonesia and Vietnam mandate early exposure, broadening the K-12 funnel. Corporate-sector demand grows as regional firms court foreign investment, pushing vendors to launch HR dashboards that log skill progression for compliance reporting.

South America posts the fastest 21.90% CAGR outlook, propelled by Brazil’s massive user base and Mexico’s near-shoring boom that values bilingual staff. Subsidized smartphone plans and improved 4G coverage widen distribution channels, letting platforms bundle English courses with telecom loyalty programs. Local cultural references in content—sports idioms, regional slang—have proven to lift completion rates, a critical insight for the online language learning market’s course-design strategy.

North America and Europe exhibit high per-capita spend yet slower learner-base expansion. North America benefits from immigration-driven heritage-language niches and enterprises’ DEI budgets. Europe’s GDPR compliance costs elevate entry barriers, tilting competitive advantage toward established providers with in-house legal and infosec teams. Nevertheless, both regions act as innovation testbeds—features perfected here, like real-time dysfluency analytics, later scale into Asia-Pacific and South America, reinforcing a global RandD diffusion cycle inside the online language learning market.

Competitive Landscape

The online language learning market is moderately fragmented but trending toward consolidation. Duolingo, Babbel, and Busuu dominate consumer self-learning installs, leveraging broad language catalogs and brand recognition. Yet rising customer-acquisition costs force all three to diversify: Duolingo released a math app to cross-sell, while Babbel expanded corporate bundles featuring analytics dashboards. Niche challengers such as Speak focus on AI-led conversational fluency, courting venture capital to finance deep-learning models that ingest millions of anonymized dialogue lines.

Marketplace operators like Preply and italki scale supply by onboarding freelance tutors, then use algorithmic matching to raise booking frequency. Tutor retention hinges on transparent commission structures; Preply’s dynamic pricing engine allocates higher visibility to high-engagement tutors, lifting overall session quality. In corporate training, Berlitz and EF Education First leverage legacy classroom partnerships to cross-sell SaaS dashboards, whereas cloud-born rivals differentiate by offering self-paced microlessons that sync with company LMS systems in real time.

Immersive-tech specialists, including Mondly VR and ImmerseMe, build strategic alliances with headset makers to pre-install demo courses, expanding addressable audiences as hardware penetration rises. Data-privacy leadership is becoming a competitive moat: platforms that obtained ISO 27001 certification early report easier B2B conversions in Europe and North America. Over the forecast horizon, MandA is expected as scale players acquire AI startups to secure proprietary models and defend margin in a market where user expectations now include personalized feedback, immersive scenarios, and seamless cross-device syncing.

Online Language Learning Industry Leaders

-

Duolingo, Inc.

-

Babbel GmbH

-

Rosetta Stone LLC

-

Busuu Ltd.

-

EF Education First Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Native Camp launched unlimited on-demand English tutoring in Brazil, extending its 3 million-learner footprint to South America.

- April 2025: Duolingo rolled out 148 new language courses powered by generative AI, doubling its catalog.

- December 2024: Speak raised USD 78 million in Series C funding at a USD 1 billion valuation to expand AI conversational learning.

- November 2024: Lingawa secured USD 1.1 million pre-seed to build native-language apps for the African diaspora.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the online language learning market as all revenues generated through internet-enabled platforms, web, mobile, or mixed-reality, that deliver live tutoring, self-paced lessons, adaptive assessments, or blended models aimed at second-language acquisition for consumers, institutions, and corporate learners.

Scope exclusion: purely classroom programs that do not employ a digital delivery layer are left outside the model.

Segmentation Overview

-

By Learning Mode

- Self-Learning Apps

- Tutor-Led

- Blended Learning

- AI-Adaptive Platforms

-

By End-user

- Individual Learners

- Corporate Learners

- Educational Institutions (K-12 and Higher-Ed)

- Government and Non-profit Bodies

-

By Language

- English

- Mandarin Chinese

- Spanish

- French

- German

- Japanese

- Other Languages

-

By Age Group

- < 13 Years

- 13 - 17 Years

- 18 - 30 Years

- 31 - 45 Years

- > 45 Years

-

By Technology Platform

- Mobile Applications

- Web-based Platforms

- VR and AR Tools

- Conversational Voice Assistants

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

-

Middle East

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed EdTech founders, K-12 digital curriculum officers across Asia and Europe, HR learning managers in North America, and freelance online tutors active on major platforms. Their inputs clarified active user-to-subscriber conversion ratios, average course completion rates, and region-specific pricing spreads that cannot be gauged from public datasets alone.

Desk Research

Analysts gathered foundational data from open repositories such as UNESCO Institute for Statistics, World Bank EdStats, Eurostat continuing education tables, and U.S. Bureau of Labor Statistics time-use surveys, which benchmark learning hours and technology access. Industry context was enriched with white papers from organizations like OECD, ACTFL, and China's Ministry of Education, plus company filings and press releases that reveal subscriber counts and pricing pivots. Select paid repositories, Dow Jones Factiva for deal tracking and D&B Hoovers for revenue splits, supported competitive intelligence. The sources cited above illustrate, not exhaust, the wider desk research pool tapped during validation.

Market-Sizing & Forecasting

A top-down learning population pool was built using data on internet penetration, foreign-language enrollment, and smartphone access, which is then pressure tested with sampled average selling price multiplied by paid user counts reported by listed providers. Key variables like monthly active users, paid conversion, corporate seat licenses, government e-learning budgets, and premium app pricing ladders drive the model. Multivariate regression links these factors to historical revenue, producing a five-year projection adjusted through scenario analysis for policy or exchange-rate shocks. Gaps where bottom-up checks fell short were bridged by sensitivity ranges reviewed with interviewed experts.

Data Validation & Update Cycle

Outputs flow through variance checks against third-party enrollment surveys, analyst peer reviews, and leadership sign-off. Mordor refreshes the dataset annually and issues mid-cycle updates when material moves, major M&A, regulatory shifts, or currency swings occur.

Why Mordor's Online Language Learning Baseline Earns Trust

Published estimates seldom align because publishers pick differing revenue streams, user definitions, and update rhythms.

Key gap drivers include whether ad-supported free tiers are counted, how aggressively foreign-exchange gains are booked, disparate pricing ladders for institutional licenses, and refresh cadences that leave some figures two years old while Mordor updates yearly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.06 B (2025) | Mordor Intelligence | - |

| USD 22.12 B (2024) | Global Consultancy A | Includes offline digital labs and bundles courseware with devices |

| USD 22.86 B (2025) | Industry Association B | Rolls ad-supported free usage into revenue via CPM equivalents |

| USD 14.20 B (2024) | Regional Consultancy C | Excludes corporate seat-license contracts and uses 2022 pricing assumptions |

Taken together, the comparison shows how our disciplined scope choices, current-year price tracking, and annual refresh cycle provide a balanced, transparent baseline that decision-makers can replicate and defend.

Key Questions Answered in the Report

How large is the online language learning market in 2026?

The market stands at USD 24.39 billion in 2026.

What growth rate is forecast for the online language learning market between 2026 and 2031?

Revenue is projected to rise at a 15.83% CAGR during the 2026-2031 period.

Which learning mode generates the biggest share of revenue?

Self-learning apps lead with 56.35% of 2025 revenue.

Which geographic region contributes the most to market revenue today?

Asia-Pacific accounts for 45.75% of global revenue.

Which language segment is expanding the fastest?

Spanish courses are advancing at a 20.20% CAGR through 2031.

Why are corporations increasing spending on language training

ESG and DEI objectives push companies to upgrade employee language skills, making corporate learners the fastest-growing end-user group at a 23.70% CAGR.

Page last updated on: