K-12 Education Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

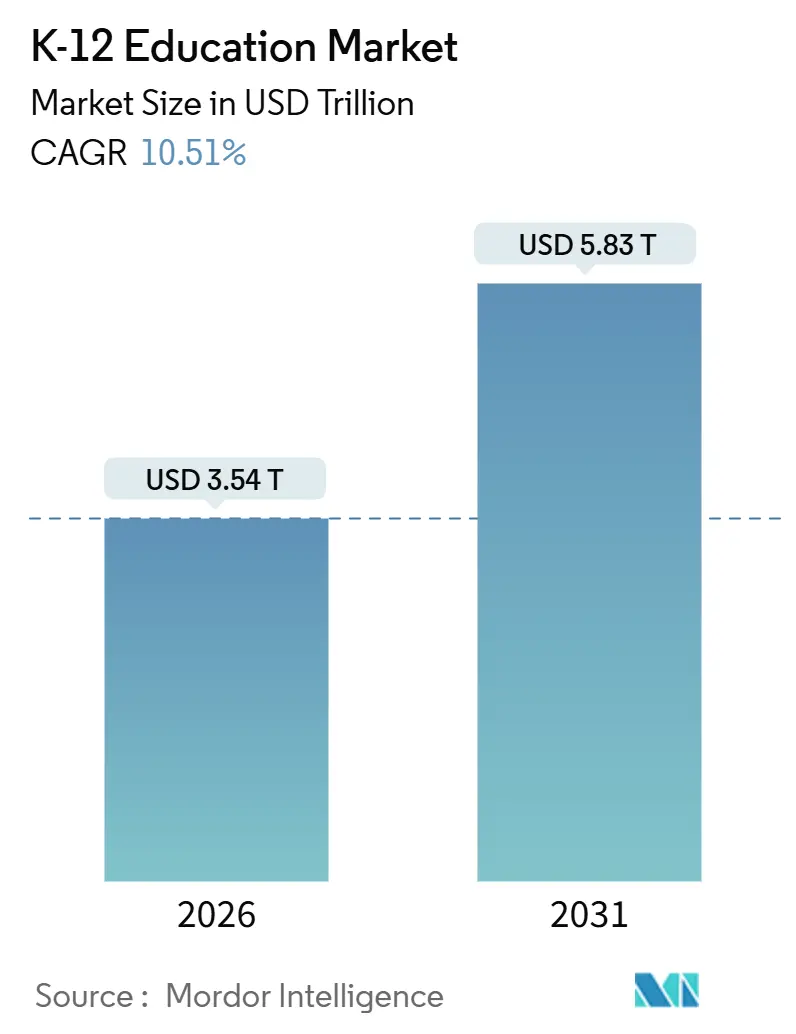

| Market Size (2026) | USD 3.54 Trillion |

| Market Size (2031) | USD 5.83 Trillion |

| Growth Rate (2026 - 2031) | 10.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

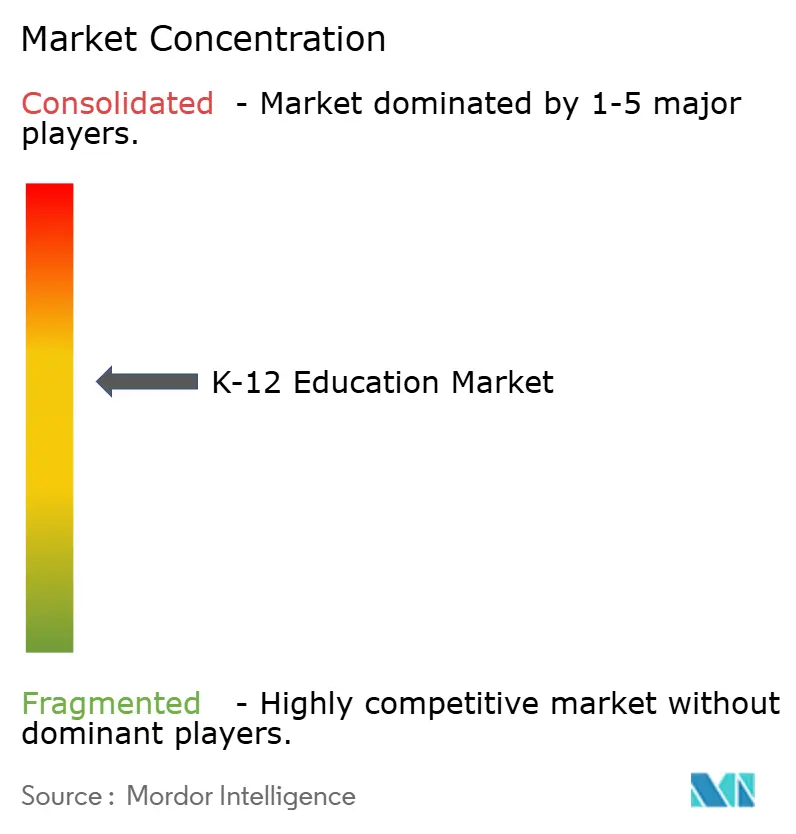

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

K-12 Education Market Analysis by Mordor Intelligence

The K-12 education market size stands at USD 3.54 trillion in 2026 and is projected to reach USD 5.83 trillion by 2031, expanding at a 10.51% CAGR. Rapid digitization is reshaping classroom experience, intertwining AI analytics, immersive simulation tools, and cloud-first infrastructure with daily instruction. Hardware prices are falling, broadband coverage is widening, and government mandates continue to underwrite device purchases, creating fertile ground for platform expansion. Incumbent technology vendors bundle zero-cost productivity suites with hardware subscriptions, eroding the long-standing dominance of traditional publishers. Meanwhile, open-source curriculum collaboratives are squeezing print margins, prompting textbook players to pivot toward direct-to-consumer micro-credential programs and adaptive e-textbooks. Adoption hurdles remain the digital divide, fragmented procurement, and teacher-training gaps but the medium-term outlook stays strongly upward as interoperability standards mature and outcome-based funding gains traction.

Key Report Takeaways

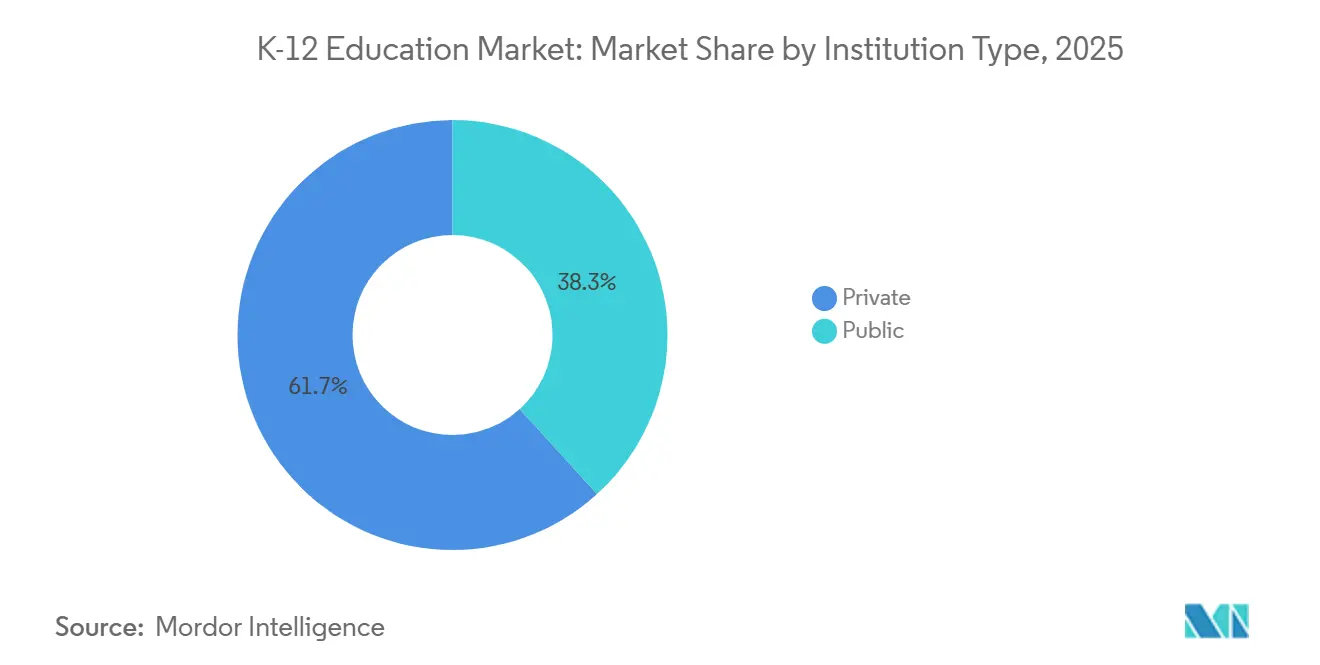

- By institution type, public schools led with 61.74% of the K-12 education market share in 2025, while private schools are forecast to expand at an 11.54% CAGR through 2031.

- By learning model, in-person instruction accounted for 60.32% of 2025 revenue, whereas fully online and virtual schools are advancing at an 11.47% CAGR to 2031.

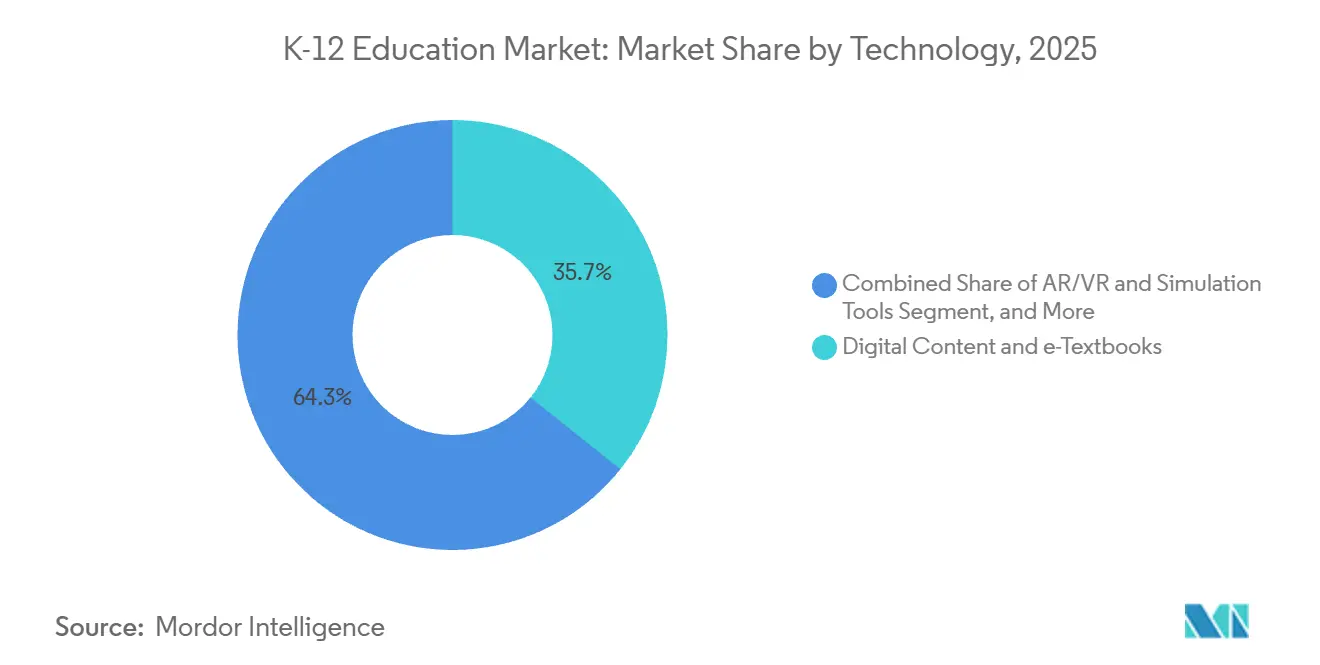

- By technology, digital content and e-textbooks claimed 35.74% of 2025 spending, yet AR/VR and simulation tools are projected to grow at an 11.83% CAGR.

- By application, high-school programs represented 39.59% of 2025 value, while the pre-primary and primary segment is on pace for an 11.61% CAGR.

- By geography, North America contributed 40.14% of global revenue in 2025, whereas Asia-Pacific is predicted to surge at an 11.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global K-12 Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Powered Learning Analytics | +2.1% | Global, early adoption in North America, China, India | Medium term (2-4 years) |

| Government Mandates for Classroom Digitisation | +1.9% | North America, Europe, Asia-Pacific (China, India, South Korea) | Short term (≤ 2 years) |

| Growing Penetration of Digital Devices and Broadband Access | +1.7% | Global, accelerating in Asia-Pacific and South America | Medium term (2-4 years) |

| Rising Demand for Personalised and Adaptive Learning Platforms | +1.5% | North America, Europe, Australia, urban Asia-Pacific | Medium term (2-4 years) |

| Emergence of Micro-Credentialing for Career Readiness | +0.8% | North America, Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| District-Level Open-Source Curriculum Collaborations | +0.6% | North America, Europe, select South American cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Powered Learning Analytics Enhancing Student Outcomes

Predictive dashboards now surface mastery gaps in near real time, enabling timely intervention that lifts quarterly pass rates. U.S. districts using early-warning models flagged at-risk students with 78% accuracy in 2025, raising proficiency by 12 points. China followed suit, mandating adaptive assessments in 50,000 middle schools that year. India earmarked INR 50 billion (USD 600 million) for AI infrastructure, and pilots in Karnataka improved math scores 15% by the end of 2025. Vendors offering closed-loop systems diagnostics that feed automated lesson plans are capturing multi-year contracts, pressuring publishers that rely on static test banks. As training ramps and data standards settle, this driver will add the greatest boost to mid-term growth.

Government Mandates for Classroom Digitisation

Funding is increasingly tied to connectivity benchmarks and device penetration ratios. The U.S. Infrastructure Investment and Jobs Act steered USD 7.2 billion into school broadband upgrades, catalyzing cloud-platform adoption.[1]Federal Communications Commission, “E-Rate Program Funding for Schools and Libraries,” fcc.gov Europe’s Digital Education Action Plan committed EUR 10 billion (USD 11.3 billion) for interactive displays, with compliance audits by the European Commission in 2026. South Korea, Australia, and other early movers imposed deadlines for digital textbooks, unleashing multi-billion-dollar procurement waves. While the spending bolsters short-term revenue, districts must budget for recurring software renewals to sustain the gains.

Growing Penetration of Digital Devices and Broadband Access

Affordable rugged tablets and sub-USD 200 Chromebooks pushed education device shipments to 47 million units in 2025. BharatNet connected 250,000 Indian village schools to fiber, bridging gaps where teacher vacancies topped 20%. Brazil’s 4G rollout reached 35,000 campuses, unlocking demand for streaming video lessons. The U.K. issued 1.3 million laptops to disadvantaged learners, narrowing the homework gap. As infrastructure improves, platform stickiness and content consumption rise, adding sustained lift to the growth curve.

Rising Demand for Personalised and Adaptive Learning Platforms

Districts now gravitate toward software that automatically calibrates difficulty, rewarding outcomes over seat-license counts. U.S. adoption jumped to 18 million students in 2025, with subscription revenue up 22%. DreamBox users gained 1.5 grade levels after weekly 60-minute sessions, persuading 450 districts to renew. European competency-based models issue micro-credentials upon mastery, and pilots in New South Wales cut remediation 18%. Demonstrated efficacy will keep districts spending, underpinning medium-term momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Divide in Rural and Low-Income Districts | -1.3% | Global, acute in South America, Africa, rural Asia-Pacific and North America | Short term (≤ 2 years) |

| Student-Data Privacy Litigations Constraining Roll-Outs | -1.1% | North America, Europe (GDPR jurisdictions) | Short term (≤ 2 years) |

| Teacher Resistance to Technology Adoption | -0.7% | Global, pronounced in Europe and parts of Asia-Pacific | Medium term (2-4 years) |

| Fragmented Procurement Processes Lengthening Sales Cycles | -0.5% | North America, Germany, Brazil, decentralized systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Divide in Rural and Low-Income Districts

Infrastructure gaps threaten to widen achievement inequities. In 2024, 9.7 million U.S. students lacked reliable home broadband, mostly in Appalachia, tribal lands, and the Mississippi Delta. Sub-Saharan Africa saw only 28% of schools electrified, rendering online tools impractical.[2]UNESCO, “School Connectivity in Sub-Saharan Africa,” unesco.org India’s rural device ratios reached 40:1 in 2025, forcing chalkboard fallback. Brazilian Northeast districts still trail urban adoption by 50%. Until subsidies and device-donation schemes scale, the digital divide will shave 1.3 points off near-term growth.

Student-Data Privacy Litigations Constraining Roll-Outs

Regulatory fines and class actions are forcing platform pauses and expensive redesigns. The U.S. Federal Trade Commission levied a USD 6 million penalty on a vendor in 2024 for unauthorized geolocation tracking.[3]Federal Trade Commission, “COPPA Enforcement Actions 2024,” ftc.gov Three European LMS providers faced EUR 12 million (USD 13.6 million) in GDPR penalties during 2025, prompting district moratoria. California’s updated student privacy law now requires annual security audits, raising vendor compliance costs 18%. Australia introduced opt-in rules for behavioral tracking, slowing AI roll-outs. Until privacy-by-design frameworks become the norm, legal uncertainty will weigh on short-term adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Institution Type: Private Schools Outpace Public Sector

Public schools accounted for 61.74% of the K-12 education market in 2025, reflecting enrollment scale and federal device subsidies. Private institutions, however, are growing at an 11.54% pace as they bundle premium adaptive-learning subscriptions, AR/VR labs, and micro-credential programs that justify rising tuition. The K-12 education market size for private schools is widening fastest in India, where chains such as Delhi Public School spent USD 4.2 billion on EdTech in 2025. Charter schools bridge both worlds, blending public funding with agile procurement to test competency-based progression. Vendors targeting this segment enjoy larger contract values, shorter sales cycles, and less bureaucracy than in the public sector.

Budget pressures constrain many public districts, pushing them toward open-source textbooks and one-time hardware grants rather than multi-year SaaS licenses. Even so, their massive user bases are critical for platform scale. Suppliers must therefore offer interoperable, standards-aligned solutions and patient financing models to win tenders. Overall, private-school momentum should continue lifting revenue while public districts remain the volume anchor of the K-12 education market.

By Learning Model: Virtual Schools Gain Traction

In-person classrooms held 60.32% share in 2025, yet virtual academies are expanding at an 11.47% CAGR as families prioritize flexibility and districts tackle teacher shortages. K12-branded virtual schools enrolled 185,000 students and produced USD 1.6 billion in 2025 revenue. The K-12 education market share of fully online models rises quickest in China, where policy shifts redirected after-school tutoring budgets into daytime digital curricula. Hybrid formats add synchronous video labs to local classrooms, maximizing scarce certified teachers across large geographies.

Early-grade socialization needs and affluent district preferences sustain the brick-and-mortar core, but secondary-grade demand for AP courses and niche electives fuels digital enrollment. Virtual providers must therefore invest in live engagement, peer collaboration, and robust counseling to stave off isolation risks and meet accountability metrics.

By Technology: AR/VR as Growth Leader

Digital content and e-textbooks captured 35.74% of technology spending in 2025, yet slowing growth exposes these categories to price erosion. In parallel, AR/VR and simulation solutions are accelerating at an 11.83% CAGR, buoyed by headsets such as Meta Quest 3 that lower hardware cost thresholds. The K-12 education market size for AR/VR platforms is rising sharply as retention gains of 18-24% outshine static textbook outcomes. European schools purchased 85,000 ClassVR headsets in 2025, bundling curriculum-aligned content that trims teacher prep time.

Legacy learning-management and assessment suites remain indispensable, but competitive differentiation is shifting toward AI-driven grading and predictive analytics. Vendors that integrate immersive modules with LMS data streams will command premium pricing, while pure-play e-textbook suppliers risk commoditization.

By Application (Grade Level): Early Education Surges

High-school programs still dominated spending with 39.59% share in 2025, supported by career-readiness platforms, dual-credit courses, and college-prep tools. Nevertheless, the pre-primary and primary cohort is advancing at an 11.61% CAGR as neuroscience validates gamified phonics and numeracy apps. Waterford.org programs delivered 1.8 months of extra reading growth for Title I students, attracting new grants. The K-12 education market size allocated to early-education software is scaling quickly in China, where regulators approved 47 preschool apps in 2025.

Middle-school demand grows mainly in South Asia and Sub-Saharan Africa, where demographics remain favorable. Secondary-grade tools now compete on breadth of electives and integration with transcript services, exemplified by recent LMS-credential mergers. Vendors must therefore balance age-appropriate UX, parental controls, and standards alignment across disparate grade ranges.

Geography Analysis

North America retained 40.14% of 2025 revenue, underpinned by USD 7.2 billion in E-Rate connectivity grants and robust state mandates for digital content. U.S. districts allocate large line items to cloud subscriptions, analytics dashboards, and device refresh cycles, cementing incumbent vendor dominance. Canada invested CAD 1.2 billion (USD 880 million) in 2025 to extend smart-classroom access to Indigenous communities.

Asia-Pacific is the fastest-growing region at an 11.97% CAGR, propelled by China’s nationwide AI-tutoring rollout and India’s rural fiber program. The K-12 education market size in Asia-Pacific will eclipse North America before 2031 if current policy momentum endures. Governments continue subsidizing hardware and mandating adaptive-assessment platforms to mitigate teacher shortages.

Europe progresses more slowly due to stringent data-sovereignty rules that favor locally hosted or open-source systems, stretching procurement cycles. Germany’s DigitalPakt Schule injected EUR 6.5 billion (USD 7.3 billion) through 2024, yet district implementation still lags 18 months behind funding awards. The United Kingdom improved device ownership among low-income households to 81% in 2025, aided by GBP 1.8 billion (USD 2.3 billion) investments.

South America and the Middle East and Africa remain fragmented. Brazil accounts for 55% of Latin American EdTech spending, though connectivity gaps persist in rural Northeast states. In the Middle East and Africa, smart-classroom pilots flourish in the United Arab Emirates and Saudi Arabia under Vision 2030, whereas South Africa and Nigeria grapple with infrastructure shortfalls. Vendors seeking regional growth must adapt pricing to variable purchasing power and offer off-line functionality where bandwidth remains scarce.

Competitive Landscape

The sector is moderately fragmented. Google Workspace for Education served 170 million students in 2025, pairing Chromebooks that represent 52% of U.S. K-12 device shipments. Microsoft Teams for Education counted 200 million active users, integrating AI-reading progress and video conferencing. Apple positions iPads as premium, privacy-centric solutions, strengthened by ClassKit 2.0 rollouts that attracted 120 partner apps.

Pearson+ for K-12 attracted 1.2 million users within six weeks, signaling appetite for direct-to-parent models. McGraw-Hill linked GPT-powered tutoring to its ALEKS system, delivering 19% algebra gains in pilots. OpenStax, meanwhile, distributed 3.8 million free digital textbooks, increasing price pressure on legacy content providers.

Specialist disruptors seize niches. Squirrel AI scaled adaptive tutoring to 3.2 million Chinese students, while ClassDojo’s communication app connects 50 million users and is branching into SEL content. Google is exploring AI-enabled disengagement detection; Microsoft focuses on multilingual translation.

To survive, mid-tier vendors must either integrate horizontally, offering full-stack ecosystems, or drill vertically into high-value niches such as special education analytics or competency-based credentials. Distribution reach, interoperability, and privacy compliance will decide long-term winners in the K-12 education market.

K-12 Education Industry Leaders

McGraw-Hill Education (Platinum Equity)

Pearson plc

Cengage Group

Stride Inc.

TAL Education Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft Education unveiled a USD 500 million plan to extend AI reading and math tutors to 15,000 U.S. Title I schools over three years.

- December 2025: Google for Education partnered with India to equip 25,000 public schools in Uttar Pradesh and Bihar with Chromebooks and Workspace, valued at USD 320 million.

- November 2025: Pearson launched Pearson+ for K-12 at USD 9.99 per month, amassing 1.2 million subscriptions in six weeks.

- October 2025: Instructure bought credential service Parchment for USD 275 million, integrating transcripts into Canvas LMS.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the K-12 education market as all public and private spending that delivers formal schooling from kindergarten through twelfth grade, spanning tuition, staffing, physical facilities, curriculum materials, and digital learning infrastructure worldwide. Values are stated in constant 2025 US dollars and cover government allocations, household out-of-pocket expenses, and commercial service revenues.

Scope exclusion: short-cycle vocational programs delivered after grade 12 are outside this analysis.

Segmentation Overview

- By Institution Type

- Public

- Private

- By Learning Model

- Traditional In-Person

- Hybrid

- Fully Online / Virtual Schools

- By Technology

- Learning Management Systems (LMS)

- Digital Content and e-Textbooks

- Assessment and Analytics Tools

- Collaboration and Communication Platforms

- AR/VR and Simulation Tools

- Other Technologies

- By Application (Grade Level)

- Pre-Primary and Primary School (K-5)

- Middle School (6-8)

- High School (9-12)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed district superintendents, state education technology directors, private school bursars, and EdTech distributors across North America, Europe, Asia-Pacific, and the Middle East. These conversations tested subsidy assumptions, captured device refresh cycles, and gauged likely shifts toward hybrid timetables, helping us reconcile disparate secondary indicators.

Desk Research

We began with finance ministries, UNESCO Institute for Statistics, the World Bank Education Finance dataset, and national budget papers, which reveal per-pupil outlays, enrollment shifts, and digital device procurements. Trade associations such as the National School Boards Association, EdTech UK, and the Asia-Pacific Smart Learning Council supplied adoption benchmarks for learning management systems and broadband ratios. Annual reports of listed textbook publishers and large school operators clarified average selling prices and fee trajectories, while Dow Jones Factiva and D&B Hoovers provided verified revenue trails for private school chains. The sources quoted here illustrate our desk research pool and are not exhaustive.

Market-Sizing & Forecasting

We anchored a top-down model that rolls national education budgets and household fee data into regional spending baselines, which are then validated through selective bottom-up checks such as textbook unit shipments and sampled tuition times enrollment tallies. Key variables include gross enrollment ratios, average teacher salary growth, device penetration per student, cloud LMS adoption rates, and public-to-private enrollment migration. Forecasts draw on multivariate regression that links spending to GDP per capita, school-age population, and digital equipment price curves, with scenario analysis for fiscal stimulus shocks. Coverage gaps in bottom-up samples are bridged using three-year moving averages from comparable districts.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance checks against historic elasticity ranges, and backcasts versus prior years before sign-off. Reports refresh annually, and interim updates trigger when policy shifts or macro swings move any input beyond a preset tolerance band.

Why Mordor's K-12 Education Baseline Inspires Confidence

Published figures often diverge because firms pick dissimilar spending buckets, currency bases, and update cadences.

By tracing every dollar to clearly documented budget lines and real-world price points, Mordor Intelligence offers a baseline that decision-makers can audit with minimal effort.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.23 Trillion (2025) | Mordor Intelligence | - |

| USD 2.79 Trillion (2024) | Regional Consultancy A | Omits private tutoring flows and provincial subsidies outside the OECD set, relying on one government dataset |

| USD 130.6 Billion (2024) | Trade Journal B | Counts only online learning platform revenue, excludes classroom salaries and facility upkeep |

| USD 153.4 Billion (2024) | Industry Platform C | Focuses on EdTech hardware and software, leaving out core instructional and capital expenditure |

The comparison shows how narrower scopes or single-source models compress spend estimates. By combining verified fiscal data, live enrollment inputs, and periodic primary checks, Mordor delivers a balanced, transparent baseline that users can trace, replicate, and trust.

Key Questions Answered in the Report

How large is the K-12 education market in 2026?

It totals USD 3.54 trillion, with a projected 10.51% CAGR through 2031.

Which segment is growing fastest within K-12 EdTech spending?

AR/VR and simulation tools, expanding at an 11.83% CAGR as headset prices fall and immersive curricula gain traction.

Why are private schools adopting technology faster than public schools?

Tuition flexibility allows private institutions to fund premium adaptive platforms and AR/VR labs, driving an 11.54% growth pace to 2031.

Which region will contribute the most new revenue by 2031?

Asia-Pacific, forecast to grow at 11.97% annually as China and India scale AI tutoring and rural broadband.

What is the biggest barrier to digital adoption in K-12?

Persistent digital divides in rural and low-income districts, which currently shave 1.3 percentage points off overall growth until infrastructure gaps close.

How are privacy regulations affecting EdTech vendors?

GDPR and U.S. state laws have triggered fines and contract pauses, raising compliance costs and delaying roll-outs, reducing near-term growth by about 1.1 percentage points.

Page last updated on: