Canada Online Grocery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

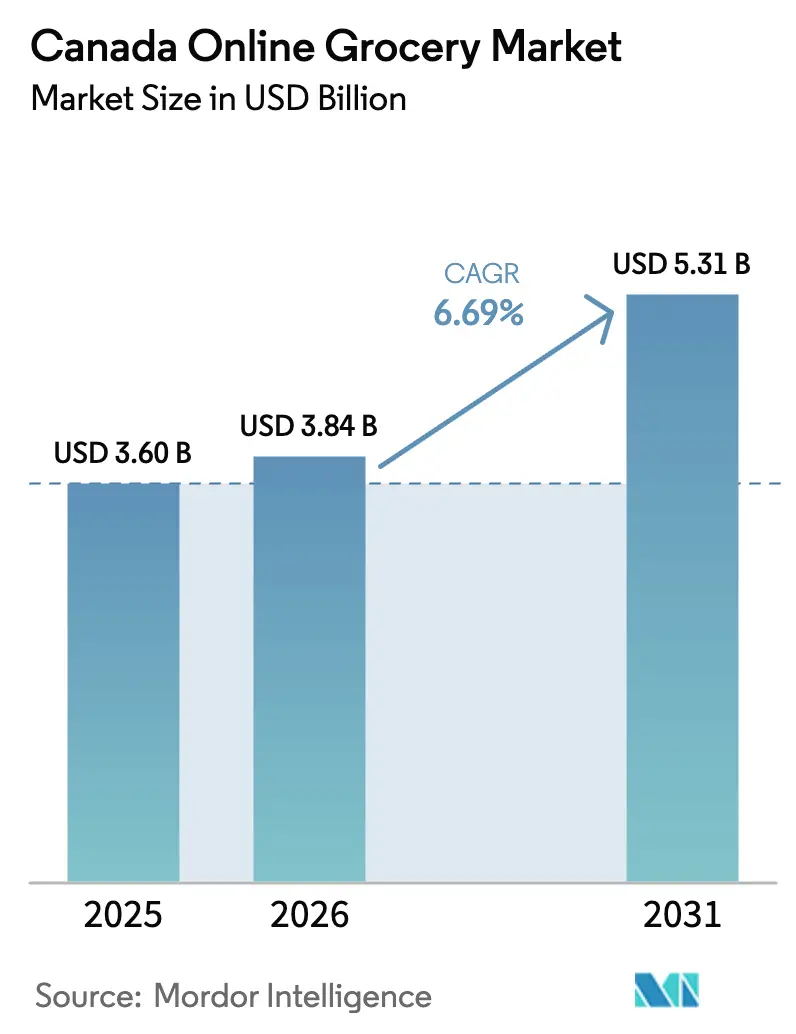

| Base Year Market Size (2025) | USD 3.6 Billion |

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 6.69% CAGR |

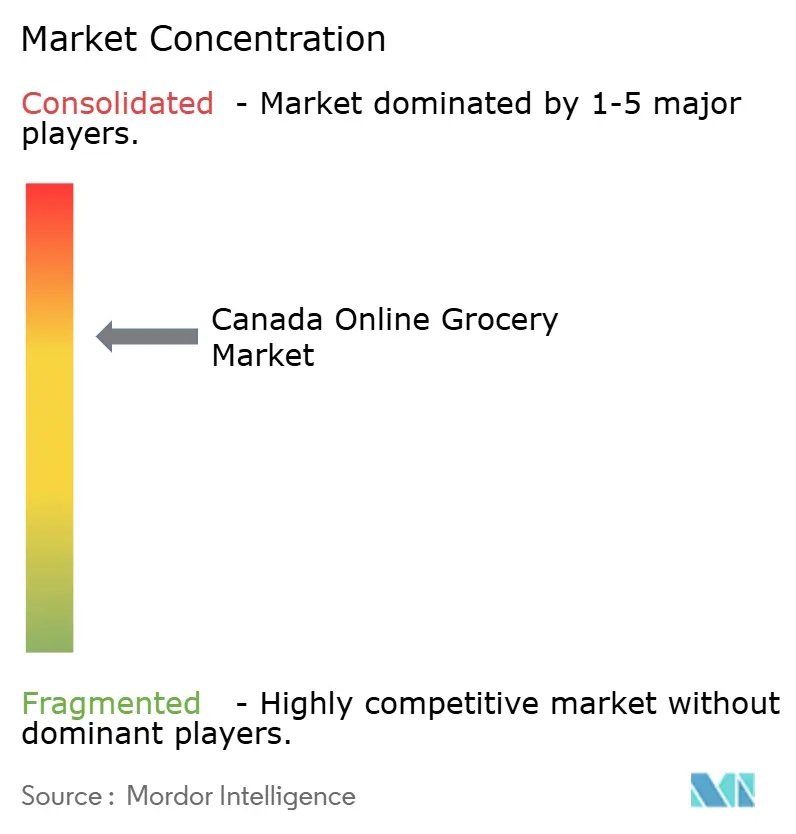

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Online Grocery Market Analysis by Mordor Intelligence

Market Analysis

The Canada online grocery market size in 2026 is estimated at USD 3.84 billion, growing from 2025 value of USD 3.6 billion with 2031 projections showing USD 5.31 billion, growing at 6.69% CAGR over 2026-2031. Momentum stems from continued digital adoption, tier-1 grocers’ omnichannel investments, and rising consumer comfort with remote shopping preferences. Aggressive capital expenditure programs, including Loblaw’s USD 1.55 billion outlay, expand automated distribution capacity and same-day coverage nationwide. Persistent urbanization and loyalty-program integration drive frequency and basket values, while third-party marketplaces broaden consumer choice and create incremental demand. Ongoing automation offers cost gains, yet high last-mile expenses and labor shortages pressure margins, particularly in low-density territories of the Canada online grocery market.

Key Report Takeaways

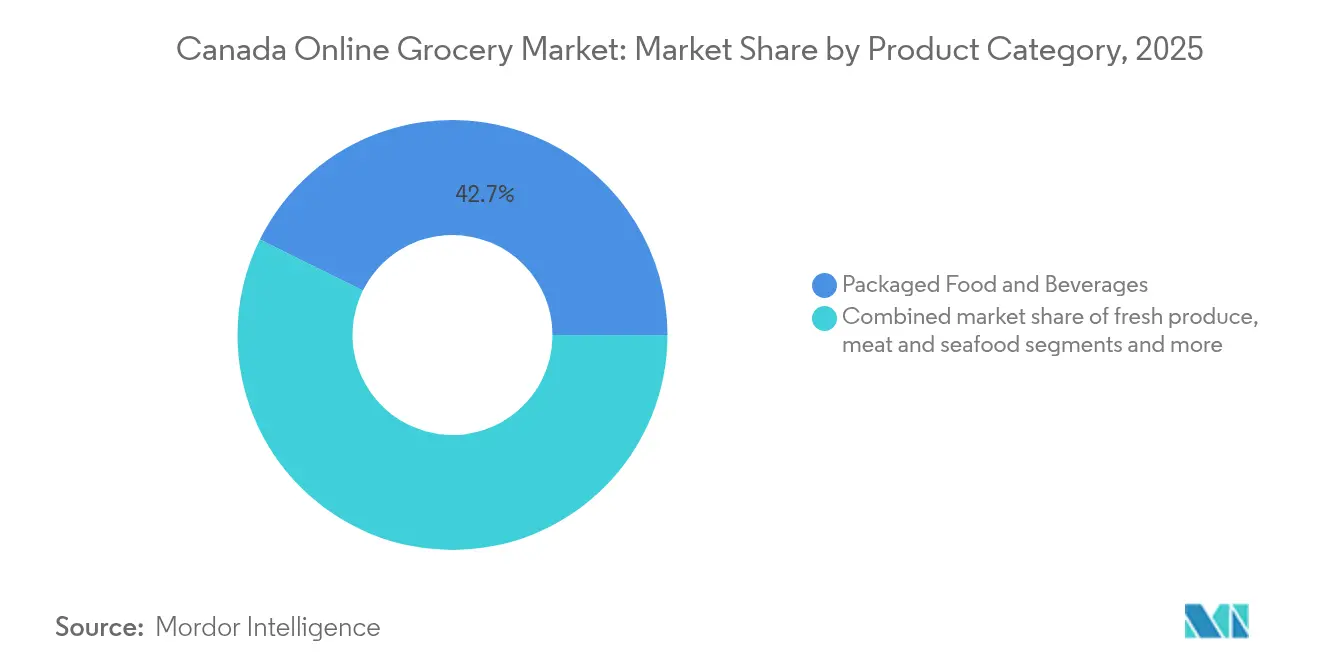

- By product category, Packaged Food & Beverages led with 42.68% revenue share in 2025; Fresh Produce is projected to expand at a 9.93% CAGR to 2031.

- By fulfilment model, Click & Collect accounted for 46.02% of the Canada online grocery market size in 2025; Rapid Delivery (≤ 1 hour) is growing at a 12.12% CAGR through 2031.

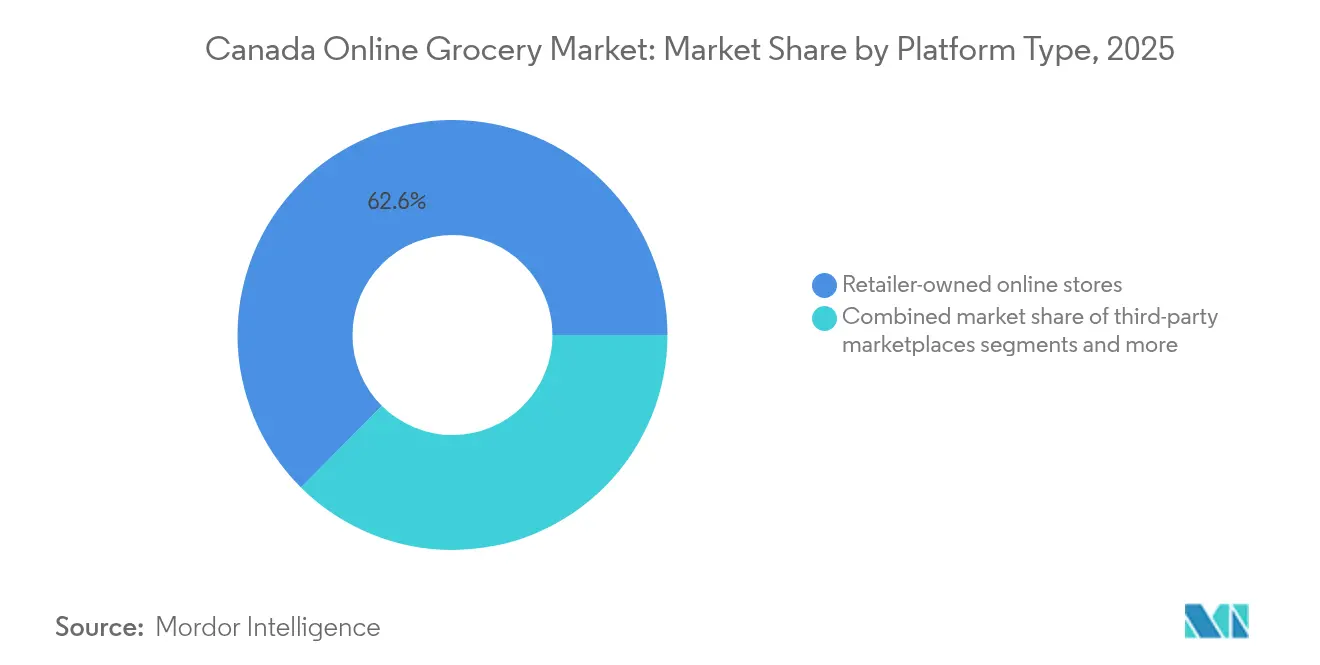

- By platform type, retailer-owned sites held a 62.55% share in 2025, while third-party marketplaces are registering the fastest growth at an 10.96% CAGR.

- By geography, Central Canada captured 53.88% of the Canada online grocery market share in 2025, while the Prairie Provinces are advancing at a 9.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Canada representing one among them. The global report on online grocery market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Canada Online Grocery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating omni-channel CAPEX by Tier-1 grocers | +1.8% | National, with concentration in Ontario & Quebec | Medium term (2-4 years) |

| Rising consumer adoption of click-and-collect post-pandemic | +0.9% | Urban centers nationwide, strongest in GTA & Montreal | Short term (≤ 2 years) |

| Expansion of same-day delivery networks into secondary cities | +0.7% | Prairie Provinces, Atlantic Canada, secondary BC markets | Medium term (2-4 years) |

| Boom in discount banners fueling online private-label demand | +0.5% | National, with emphasis on price-sensitive regions | Long term (≥ 4 years) |

| Government subsidies to improve food access in remote communities | +0.3% | Northern territories, isolated Indigenous communities | Long term (≥ 4 years) |

| AI-powered personalized nutrition driving higher basket values | +0.2% | Tech-forward urban markets, early adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Omnichannel CAPEX by Tier-1 Grocers

Canadian market leaders are synchronizing physical expansion with automated e-commerce infrastructure. Walmart Canada earmarked USD 4.51 billion over five years for new Supercenters and robotic distribution upgrades, matching Metro’s CAD 1 billion automation program that overlays Toronto and Quebec hubs [1]Metro Inc., “Supply Chain Modernization Update,” metro.ca. Loblaw intends to open 80 stores in 2025—half of them discount formats—using back-of-store staging zones to speed order picking. These roll-outs deepen nationwide coverage and reinforce scale advantages, elevating the Canada online grocery market beyond pandemic-era peaks by embedding e-commerce in every store renovation.

Rising Consumer Adoption of Click-and-Collect Post-Pandemic

Click-and-collect usage stabilizes at 46.65% of orders and remains sticky because it eliminates delivery fees and provides pickup time control. Loblaw’s PC Express slots drive loyalty point accrual, encouraging weekly baskets while minimizing last-mile expense on the retailer’s side. Shoppers in Greater Toronto and Montréal cite product inspection and on-time reliability as key reasons for returning to curbside pickup, distinguishing Canadian preferences from U.S. markets where doorstep delivery dominates. Expansion into Maritime provinces demonstrates viability in smaller population centers, because curbside hubs leverage existing parking lots rather than costly micro-fulfillment facilities.

Expansion of Same-Day Delivery Networks into Secondary Cities

Empire Company’s Instacart alliance now covers over 250 stores, placing 90% of Canadian households within same-day reach. Automated Ocado sheds in Calgary and Edmonton feed the Prairies, where delivery density rises with ongoing immigration. Local operators such as GroceryXpress.ca use regional driver pools to serve communities that national couriers overlook, picking up an incremental share in the Canada online grocery market. Improved route-planning software compresses drop-off windows, while consolidated dark-store inventory protects fresh-food quality.

Discount Banners Fuel Online Private-Label Demand

Loblaw’s No Frills and No Name digital assortments headline weekly flyers; Metro converts legacy stores to discount formats to capture price-sensitive traffic. Online catalogues spotlight private-label innovation, such as plant-based proteins and eco-packaged staples, lifting margins within the Canada online grocery market. A surge in discount traffic also widens data sets, enabling machine-learning engines to cross-sell higher-margin convenience meals. Private-label momentum boosts negotiating power with branded suppliers and fortifies retailer ecosystems against third-party platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile logistics & cold-chain costs in low-density areas | -0.6% | Northern territories, rural Atlantic Canada, remote BC | Long term (≥ 4 years) |

| Persistent consumer scepticism over fresh-produce quality online | -0.4% | National, particularly among older demographics | Medium term (2-4 years) |

| Stricter inter-provincial alcohol shipping regulations | -0.3% | National, with varying provincial enforcement | Medium term (2-4 years) |

| Fulfilment-center labor shortages & union pressures | -0.5% | Urban centers, particularly GTA, Montreal, Vancouver | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Logistics & Cold-Chain Costs in Low-Density Areas

Canada’s vast geography forces couriers to travel long distances to sparsely populated communities, driving per-order delivery expense above average basket values. Nutritional subsidy programs in 103 northern communities illustrate the structural cost gap as commercial players hesitate to build temperature-controlled lanes [2]Government of Canada, “Nutrition North Program Overview,” canada.ca. Severe winter storms regularly disrupt Nova Scotia highway links, causing produce spoilage and reinforcing cost volatility risks. Agriculture and Agri-Food Canada traces 40% of distribution wastage to cold-chain breakdowns, raising the hurdle rate for fresh-food e-commerce [3]Agriculture and Agri-Food Canada, “Annual Food Waste Report,” agr.gc.ca.. Retailers respond with zone-based pricing and modular refrigerated lockers, yet break-even horizons remain distant, tempering the growth runway for the Canada online grocery market in remote regions.

Persistent Consumer Scepticism Over Fresh-Produce Quality Online

Tactile assessment remains central to Canadian produce buying habits, making quality assurance the pivotal deterrent to online conversion. Temperature excursions during suburban van routes can bruise berries and wilt greens, feeding social media images that deter first-time users. IoT trackers from RiverCity Innovations now alert pickers to cold-chain breaches in real time, but behavioral change is gradual. Retailers test “delivered fresh or free” guarantees and image-based AI sorting, yet many consumers continue to reserve fresh items for in-store missions. Consequently, packaged staples still account for most baskets, restraining category mix elevation within the Canada online grocery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Fresh Produce Lifts Premium Growth

Packaged Food & Beverages held 42.68% of the Canada online grocery market in 2025, underpinned by standardized packaging that streamlines ambient shipping. Fresh Produce, though smaller, records a 9.93% CAGR and anchors long-term volume upside as automation improves shelf-life visibility. Metro’s CAD 1 billion network of automated fresh hubs in Toronto and Quebec illustrates capital redeployment toward perishables. Premiumization trends steer consumers toward organic berries and pre-washed salad kits, raising average basket revenue. Meanwhile, frozen entrées and bakery items benefit from stay-at-home meal planning, buffering margin pressures.

With cold-chain reliability rising, Fresh Produce captures incremental wallet share and elevates frequency by necessitating repeat orders for replenishment. Meat & Seafood sees steady demand thanks to portion-controlled, vacuum-sealed packaging that travels well across short-haul same-day services. Household and personal-care products round out larger baskets, creating cross-category promotions that drive economies of scale in the Canada online grocery market. Overall, rising produce penetration positions grocers to upsell complementary items, lifting gross profit dollars per order.

By Order Fulfilment Model: Rapid Delivery Gains Urban Traction

Click-and-collect remains the workhorse, claiming 46.02% of order volume by leveraging existing parking lots and eliminating courier fees. Loblaw’s PC Express slots now blanket more than 700 sites, while Real Canadian Superstore extends pickup windows into Maritime towns. The modality’s low capital requirement shields margins and builds perceived reliability among cost-conscious families within the Canada online grocery market.

Rapid Delivery, defined as sub-one-hour arrival, delivers the strongest 12.12% CAGR as urban consumers pay premiums for convenience. Instacart and Uber Eats plug into Sobeys and Walmart stores, turning aisle stock into quasi-dark-store inventory during off-peak hours and unlocking incremental cash flow. Dense downtown zones enable five-drop batches per hour, compressing delivery cost curves. As average delivery fees normalize around CAD 3.99, competitive differentiation shifts toward substitution accuracy and driver professionalism, further refining customer expectations in the Canada online grocery market.

By Platform Type: Marketplaces Expand Wallet Share

Retailer-owned channels control 62.55% of 2025 sales, anchored by powerful loyalty ecosystems such as PC Optimum, which issued more than CAD 1 billion in rewards last year. Proprietary data lakes inform predictive replenishment engines that lift unit per transaction count. Grocers also bypass third-party commissions, preserving margins in the Canada online grocery market.

Third-party marketplaces, however, accelerate at an 10.96% CAGR by aggregating inventory across multiple grocers and adding adjunct categories such as meal kits. Instacart’s penetration into 90 retail banners offers one-stop convenience for shoppers seeking assortment breadth. Promotional cross-retailer price comparisons appeal to younger demographics, enabling marketplaces to capture incremental baskets. An emerging hybrid model sees grocers syndicate private-label lines onto marketplaces to widen reach while safeguarding core SKUs for their own portals, reflecting channel coexistence in the Canada online grocery market.

Geography Analysis

Central Canada drives more than half of the nationwide online grocery share of about 53.88%, reflecting dense urban corridors from Windsor to Québec City and robust fulfillment-center clustering. Loblaw and Metro deploy automated warehouses outside Toronto, accelerating last-mile velocity to large suburban catchments that underpin profitability for the Canada online grocery market. Population growth, high broadband penetration, and loyalty program engagement sustain volume stability.

Western expansion vectors sharpen in Alberta and Saskatchewan as migration fuels mid-sized city formation. Prairie Provinces post a 9.47% CAGR on the back of Empire’s Ocado-powered Voilà network, which offers next-day and same-day windows in Calgary and Edmonton. Localized services adapt to dispersed addresses by employing locker pickup at gas stations, breaking delivery density barriers without compromising chilled chain rigor.

Atlantic Canada remains comparatively small yet unlocks upside through ferry-linked micro-fulfillment hubs. Ports such as Halifax facilitate inbound produce consolidation, shortening restock cycles and enabling same-day coverage for urban clusters. Northern territories still represent challenging economics because per-stop transport costs eclipse basket value even after federal subsidies. Pilot drone routes are being trialed for medical and high-value food items, though scale commercialization remains at least four years away for the Canada online grocery market.

Mordor Intelligence provides coverage of the online grocery market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Market concentration remains high: Loblaw, Sobeys, Metro, Costco, and Walmart collectively hold major market share in 2024, providing formidable buying leverage and media reach. Sobeys leverages Ocado robotics to promise one-hour cut-offs on frozen items, differentiating on accuracy rather than mere speed. Metro’s supply-chain overhaul automates 240,000 picks per day, raising throughput by 80% and freeing labor to focus on fresh QC checkpoints in the Canada online grocery market.

Costco extends Canada's online grocery market reach through member-only bulk assortments that compress cost per unit, while Walmart counters with everyday-low-price messaging paired with optional membership for free delivery. Instacart cements partnerships with Empire and Walmart to anchor growth while experimenting with micro-fulfillment centers in Vancouver to reduce driver dwell time. Uber Eats integrates grocery items into its core prepared-food interface, capturing incremental late-night baskets and eroding traditional day-part delineations.

Labor dynamics add complexity: Metro Toronto distribution staff voted to strike in 2024, pressuring wage formats and forcing contingency routing that briefly extended delivery windows in the Canada online grocery market. Retailers increasingly promote automation for heavy-lift tasks, channeling freed capacity toward quality control in fresh aisles. Collectively, these strategic initiatives solidify incumbents’ defensive moats even as marketplaces nibble peripheral share.

Canada Online Grocery Industry Leaders

Loblaw Companies Limited

Sobeys Inc. (Empire Company Limited)

Metro Inc.

Costco Wholesale Canada Ltd.

Walmart Canada Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Loblaw earmarked USD 1.55 billion in capital for store modernizations and automated fulfillment expansion.

- October 2024: Empire Company extended Instacart same-day delivery to 250 locations, reaching 90% household coverage nationwide.

Canada Online Grocery Market Report Scope

| Fresh Produce |

| Packaged Food & Beverages |

| Meat & Seafood |

| Dairy & Eggs |

| Frozen Foods |

| Bakery & Prepared Meals |

| Household & Personal Care |

| Click & Collect (Curb-side) |

| Same-Day Home Delivery |

| Next-Day / Standard Delivery |

| Rapid (≤1-hour) Delivery |

| Retailer-Owned Online Stores |

| Third-Party Marketplaces (Instacart, Uber Eats etc.) |

| Meal-Kit & Subscription Services |

| Atlantic Region |

| Central Canada |

| Prairie Provinces |

| West Coast |

| North (Territories) |

| By Product Category | Fresh Produce |

| Packaged Food & Beverages | |

| Meat & Seafood | |

| Dairy & Eggs | |

| Frozen Foods | |

| Bakery & Prepared Meals | |

| Household & Personal Care | |

| By Order Fulfilment Model | Click & Collect (Curb-side) |

| Same-Day Home Delivery | |

| Next-Day / Standard Delivery | |

| Rapid (≤1-hour) Delivery | |

| By Platform Type | Retailer-Owned Online Stores |

| Third-Party Marketplaces (Instacart, Uber Eats etc.) | |

| Meal-Kit & Subscription Services | |

| By Region | Atlantic Region |

| Central Canada | |

| Prairie Provinces | |

| West Coast | |

| North (Territories) |

Key Questions Answered in the Report

What is the current value of the Canada online grocery market?

The market is valued at USD 3.84 billion in 2026 and is projected to reach USD 5.31 billion by 2031.

Which region holds the largest share in the Canada online grocery market?

Central Canada accounts for 53.88% of national revenue, reflecting dense urban populations and advanced fulfillment infrastructure.

Which fulfilment model is most popular with Canadian consumers?

Click-and-collect leads with 46.02% of orders because it offers fee-free pickup and reliable scheduling.

Who are the leading companies in the Canada online grocery market?

Loblaw, Sobeys, Metro, Costco, and Walmart collectively command almost three-quarters of sales.

What category is growing fastest in the Canada online grocery market?

Fresh Produce is expanding at a 9.93% CAGR as cold-chain automation improves quality assurance.

How fast are third-party marketplaces growing?

Platforms such as Instacart and Uber Eats are registering an 10.96% CAGR, gaining ground among younger, convenience-focused shoppers.

Page last updated on: