Omega-3 Prescription Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.46 Billion |

| Market Size (2030) | USD 1.98 Billion |

| Growth Rate (2025 - 2030) | 6.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

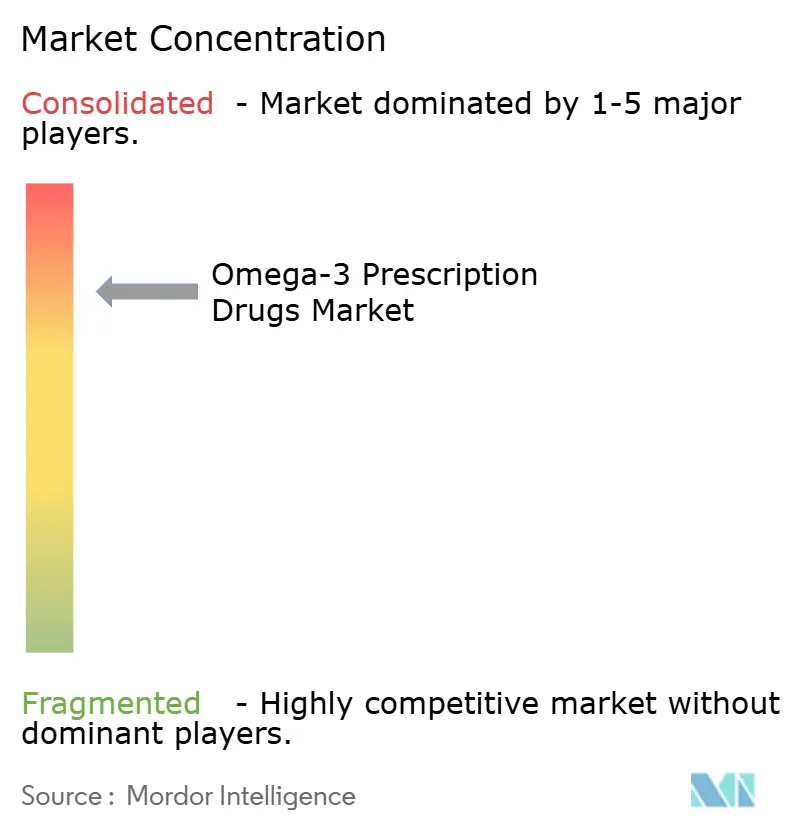

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Omega-3 Prescription Drugs Market Analysis by Mordor Intelligence

The Omega-3 prescription drugs market size reached USD 1.46 billion in 2025 and is on track to achieve USD 1.98 billion in 2030, reflecting a 6.3% CAGR during the forecast period. Clinical practice is rapidly migrating from over-the-counter fish-oil supplements toward regulated, ultra-pure formulations that deliver proven 25% cardiovascular event reduction when combined with statins, as demonstrated in the REDUCE-IT study. The U.S. Food and Drug Administration’s 2024 update that lets higher-fat fish carry a “healthy” claim has further raised physician confidence in long-chain omega-3s as cardioprotective agents. Pipeline introductions of high-concentration eicosapentaenoic acid (EPA) capsules, falling acquisition costs driven by generics, and expanded payer coverage are widening access to prescription therapy in both mature and emerging markets. At the same time, first-time approvals in China, upgrades in marine-oil refining capacity, and supportive dietary-guideline revisions position the Omega-3 prescription drugs market for sustained double-digit volume gains through 2030.

Key Report Takeaways

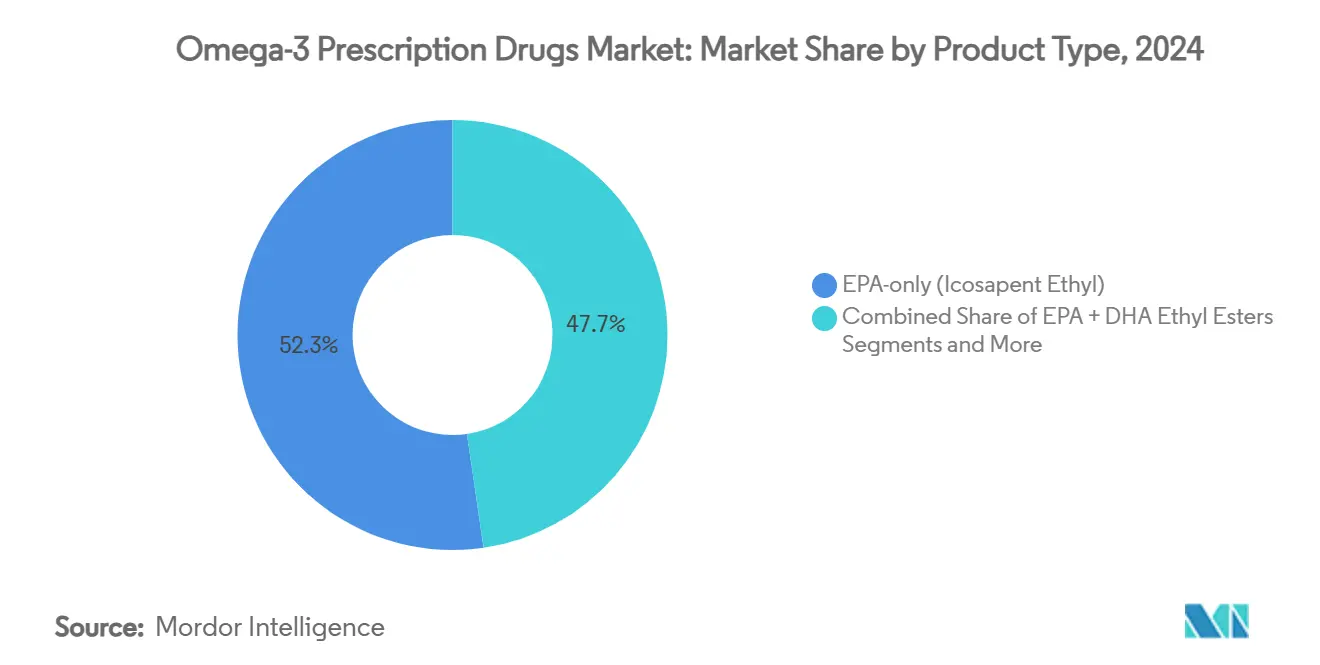

- By product type, EPA-only formulations commanded 52.3% of the Omega-3 prescription drugs market share in 2024, establishing a clinically differentiated class.

- By indication, severe hypertriglyceridemia represented 62.7% of the Omega-3 prescription drugs market size in 2024, while cardiovascular risk reduction led growth with an 18.2% CAGR.

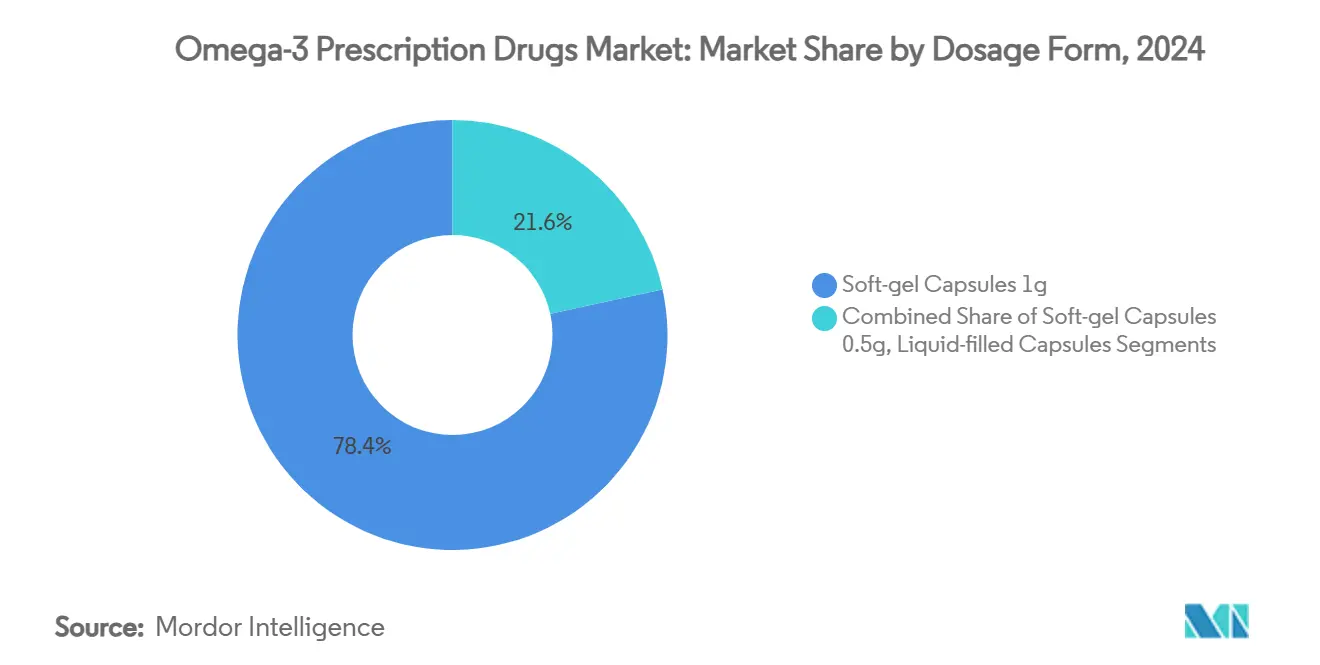

- By dosage form, 1 g soft-gel capsules captured 78.4% of 2024 sales, although smaller 0.5 g gels are expanding rapidly.

- By distribution channel, retail and specialty pharmacies held 68.3% revenue in 2024, whereas online and mail-order outlets exhibit the highest projected CAGR at 11.3% through 2030.

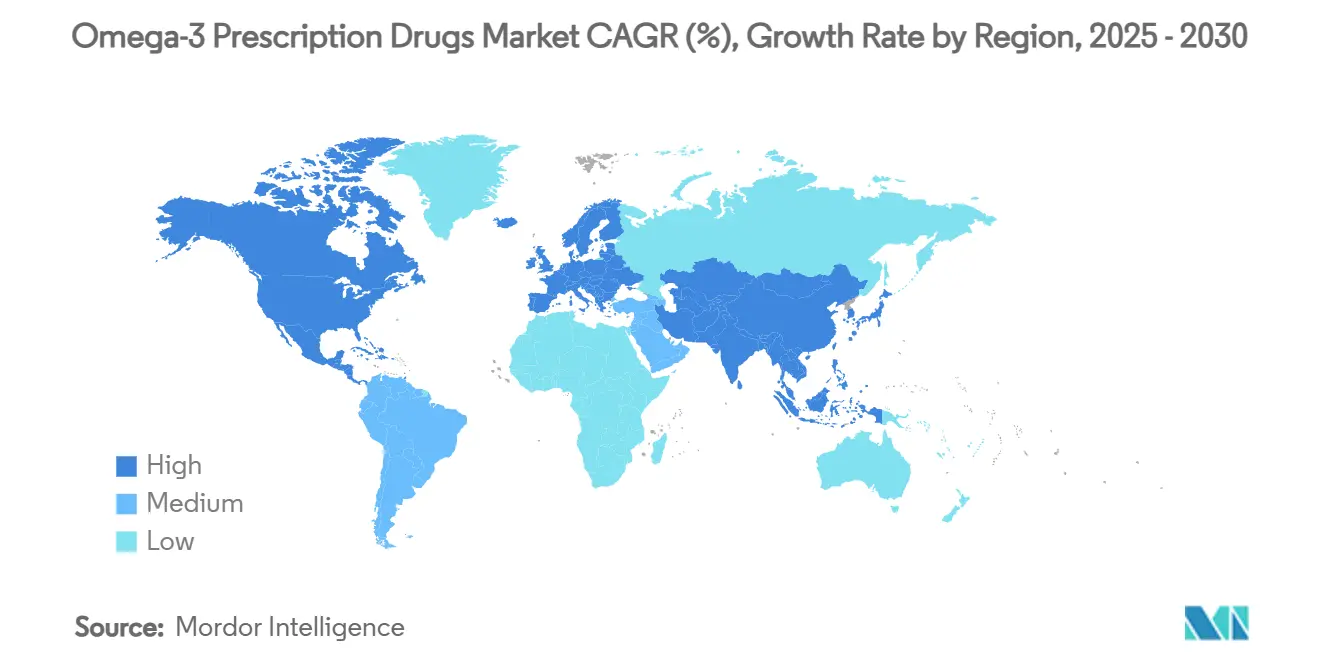

- By geography, North America contributed 45.6% of global revenue in 2024, and Asia Pacific shows the fastest regional CAGR at 12.5% through 2030.

Global Omega-3 Prescription Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA cardiovascular-risk label expansion for EPA-only drugs | +1.20% | North America & EU | Medium term (2–4 years) |

| Rising prevalence of severe hypertriglyceridemia & mixed dyslipidemia | +0.80% | Global | Long term (≥ 4 years) |

| Strong REDUCE-IT outcomes data boosting clinician confidence | +1.00% | Global | Short term (≤ 2 years) |

| Generic entry driving price-sensitive adoption in emerging markets | +0.60% | APAC core; spill-over to MEA | Medium term (2–4 years) |

| First-mover approvals in China & other untapped markets | +0.40% | APAC with early gains in China & India | Medium term (2–4 years) |

| Scaling of specialised soft-gel capacity for ultra-pure EPA/DHA | +0.30% | Global manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FDA Cardiovascular-Risk Label Expansion for EPA-Only Drugs

The U.S. label that now authorizes icosapent ethyl for broad cardiovascular risk reduction instantly enlarged the eligible pool by nearly 8 million adults and triggered Medicare Part D coverage without prior authorization for more than 90% of beneficiaries.[1]J. Bhatt et al., “National and State Estimates of SELECT Trial Eligibility,” jamanetwork.orgEuropean regulators have begun adopting parallel indications, and guideline committees in Japan and Australia are reviewing similar revisions. Product managers are accelerating once-daily, 4 g capsule programs to enhance adherence, while contract manufacturers ramp high-vacuum distillation lines that achieve ≥96% EPA purity. Insurers increasingly waive step therapy for EPA-only prescriptions when triglycerides remain ≥150 mg/dL despite maximized statin dosing, signaling reimbursement tailwinds across developed markets.

Rising Prevalence of Severe Hypertriglyceridemia & Mixed Dyslipidemia

Sedentary lifestyles, refined-carbohydrate diets, and metabolic syndrome have raised severe hypertriglyceridemia incidence worldwide. The 2024 Omega-3 World Map analysis of 342,864 subjects across 48 countries reported critically low mean omega-3 index values below 4% in India, Iran, and Egypt, correlating with elevated triglycerides and residual cardiovascular risk.[2]Omega-3 World Map Study Group, “Global Omega-3 Index Status 2024,” sciencedirect.comEpidemiologists link this deficiency to rising type 2 diabetes and non-alcoholic steatohepatitis, conditions that frequently co-present with dyslipidemia. National payers in Brazil, Indonesia, and Saudi Arabia now recognize that statins alone leave substantial residual risk, opening procurement budgets for prescription omega-3 therapy. Pharmaceutical detailers stress the combination treatment’s additive effect on high-sensitivity C-reactive protein reduction, which resonates with cardiologists managing inflammatory cardiometabolic profiles.

Strong REDUCE-IT Outcomes Data Boosting Clinician Confidence

The 8,179-patient REDUCE-IT trial recorded a 25% relative reduction in first cardiovascular events and a 30% drop in total ischemic events when EPA therapy was added to statins.[3]American College of Cardiology, “Reduction of Cardiovascular Events With Icosapent Ethyl–REDUCE-IT,” acc.org Subsequent subgroup analyses confirmed consistent benefit irrespective of baseline LDL-C, age, or renal function, thereby eliminating clinical hesitation around selective patient targeting. Real-world registry data from the United States, Germany, and Japan align closely with trial outcomes, reinforcing daily practice relevance. Treatment algorithms from the American Heart Association and European Society of Cardiology now recommend 4 g EPA daily for high-risk adults with triglycerides in the 150–499 mg/dL band. Pharmacy and therapeutics committees interpret these findings as high-quality evidence, accelerating formulary inclusion across large integrated-delivery networks.

Generic Entry Driving Price-Sensitive Adoption in Emerging Markets

Teva introduced the first generic omega-3-acid ethyl esters in early 2024 at a 60% discount to the brand, and by year-end, Hikma, Dr. Reddy’s, and Camber launched competing generic icosapent ethyl capsules. Cost reductions have stimulated multi-month prescriptions in Mexico, South Africa, and the Philippines, and insurers in Thailand now reimburse EPA therapy as a preferred adjunct to statins. Local active-pharmaceutical-ingredient (API) manufacturing in India and China shortens lead times and mitigates freight inflation, encouraging governments to add prescription omega-3 drugs to national essential-medicines lists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent cliffs & litigation eroding branded profitability | -1.40% | North America & EU | Short term (≤ 2 years) |

| LDL-C elevation concerns with DHA-containing formulations | -0.60% | Global | Medium term (2–4 years) |

| Volatile marine-oil supply chain & sustainability regulation | -0.40% | Global supply chains | Long term (≥ 4 years) |

| Payer focus shift to GLP-1 & PCSK9 drugs | -0.80% | North America & EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Patent Cliffs & Litigation Eroding Branded Profitability

The U.S. Supreme Court’s refusal to reinstate Vascepa patents in 2021 opened the floodgates to generics, wiping more than 95% off Amarin’s market value by 2024 and forcing headcount reductions. Teva and Hikma accuse Amarin of locking up the excipient supply to stall the generic launch, underscoring persistent legal friction. Brand manufacturers now lean on incremental innovation, such as pro-drug conjugates and soft-gel micro-emulsions, rather than intellectual-property exclusivity to defend their share.

LDL-C Elevation Concerns With DHA-Containing Formulations

Randomized studies attribute a 3–7% rise in LDL-C to docosahexaenoic acid, prompting cardiologists to prefer pure EPA for residual risk management. Payers sometimes decline reimbursement for mixed EPA+DHA products beyond severe hypertriglyceridemia, narrowing the addressable volume. Drug makers attempt to mitigate the issue by formulating EPA-dominant blends, yet scientific messaging remains challenging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: EPA-Only Formulations, Cement Leadership

The Omega-3 prescription drugs market size for EPA-only products reached 52.3% market share in 2024, equivalent to 52.3% revenue. Mixed EPA+DHA capsules contributed USD 574 million, while omega-3 carboxylic acids occupied the remainder. Pure EPA avoids the LDL-C uptick linked to DHA, allowing cardiologists to address residual risk without jeopardizing LDL benchmarks [JCLINLIPIDOL.ORG]. Pipeline candidates deliver 1.2–1.4 g EPA per capsule, promising once-daily therapy that simplifies multimerization regimens for secondary-prevention patients.

Growth prospects hinge on expanding awareness among primary-care physicians who manage most dyslipidemia cases. Medical education programs highlight real-world evidence showing similar event-reduction magnitude to REDUCE-IT, which resonates with clinicians wary of trial-practice gaps. Manufacturers pair such data with rebate contracts to persuade pharmacy-benefit managers. Assuming continued formulary support, the EPA-only subsegment is forecast to post a 15.4% CAGR, solidifying its majority share within the broader Omega-3 prescription drugs market.

By Indication: Cardiovascular Risk Reduction Surges

Severe hypertriglyceridemia captured 62.7% of the Omega-3 prescription drugs market share in 2024, as payers long reimbursed therapy solely for ≥500 mg/dL triglyceride levels. After label expansion, cardiovascular risk reduction now records the steepest growth, with revenue forecast to treble by 2030. Prescription volume in this category already exceeds 3.4 million monthly fills in the United States after Medicare relaxed quantity limits for eligible statin-treated patients.

International societies increasingly classify triglycerides between 150–499 mg/dL as modifiable residual risk, transforming EPA into a guideline-mandated option. Electronic-medical-record prompts in Canadian primary-care clinics improved prescription rates by 22% following integrated risk-score calculators. The shift reflects a proactive, rather than reactive, stance on dyslipidemia, moving therapy upstream toward prevention. The Omega-3 prescription drugs market size allocated to cardiovascular application is thus projected to outpace every other sub-segment through the decade.

By Dosage Form: High-Potency Soft-Gels Reshape Compliance

Classic 1 g soft-gels generated 78.4% of market shares in 2024, but a compliance audit indicated that 18% of patients found the capsules too large, leading to early discontinuation. Consequently, high-potency 0.5 g soft-gels with 600 mg EPA show a 9.0% CAGR. The reformats leverage novel micro-emulsion technology that packs more API per gram and eliminates fish-oil aftertaste. Liquid-filled syrups and suspensions represent a <2% share, catering to pediatric epilepsy cases and geriatric dysphagia.

Manufacturers also test plant-based capsule materials to address religious and vegan preferences, broadening demographic reach. Contract moulders in Canada and Spain are trialing fully recyclable blister packs to satisfy hospital group-purchasing-organization sustainability metrics. These innovations strengthen adherence and bolster lifetime therapy value, vital in chronic cardiovascular management paradigms.

By Distribution Channel: Digital Dispensing Gains Momentum

Retail and specialty pharmacies managed 68.3% of global turnover in 2024, partly because cardiovascular-risk scripts often require counselling on fasting triglyceride testing and dose titration. Yet online and mail-order pharmacies are expanding fast, spurred by 90-day supply incentives under Medicare and National Health Service cost-saving initiatives. Hospital pharmacies retain importance for patients discharged after acute coronary syndrome, where EPA therapy is started before release to improve continuity.

Digital platforms harness biometric data integration from connected home cholesterol meters, sending refill reminders based on personalized lipid trends. This value-added monitoring differentiates them from mortar outlets, appealing to tech-savvy cohorts. As payers reward outcome-based contracts, telemetry-enabled dispensing should further drive the Omega-3 prescription drug market penetration.

Geography Analysis

North America generated 45.6% of 2024 sales, reflecting early FDA endorsements, guideline alignment, and commercial insurance coverage that now approaches 95% of statin-treated high-triglyceride lives. The Omega-3 prescription drugs market size in the region is expected to rise at 4.7% CAGR as generics stimulate volume despite unit-price erosion. Canada’s public formulary added icosapent ethyl to all provinces by mid-2024, while Mexico listed EPA generics under Seguro Popular for secondary prevention, improving affordability in lower-income segments.

Europe ranks second by revenue, though growth is uneven. Germany and the United Kingdom have integrated EPA therapy into quality-outcome frameworks, accelerating adoption. In contrast, Italy and Spain impose stricter cost-effectiveness thresholds, slowing hospital access. Sustainability regulation adds complexity because the European Commission’s common fisheries policy caps industrial anchovy harvests. KD Pharma’s marine-lipid acquisition thus secures regional supply and underpins product launches that target value-based purchasing groups.

Asia Pacific shows the most dynamic trajectory with a 12.5% CAGR forecast. China’s 2024 approval unlocked a huge moderate-triglyceride population underserved by existing therapies. Local partner EddingPharm plans to leverage social-commerce channels such as JD Health to reach remote counties, while provincial tenders could add EPA to reimbursement formularies by 2026. India’s tighter scrutiny of nutraceutical claims may channel demand toward prescription products, especially among urban diabetic cohorts. Japan, South Korea, and Australia maintain stable growth through systematic dyslipidemia screening and rapid ageing demographics that elevate cardiovascular-disease risk.

Competitive Landscape

Patent expiration shifted the Omega-3 prescription drugs market from high to moderate concentration. Amarin, GlaxoSmithKline, and AstraZeneca still wield strong physician mindshare, but their combined share fell below 50% after multiple generic launches. Teva, Hikma, Dr. Reddy’s, and Camber compete on aggressive pricing and local manufacturing footprints that shorten supply chains. Contract development players Catalent and Thermo Fisher emerge as critical enablers by offering turnkey micronization, molecular distillation, and soft-gel encapsulation services to newcomers.

Strategic consolidation is accelerating. KD Pharma’s July 2024 purchase of DSM-Firmenich’s marine-lipids business secured MEG-3 capacity in Peru and Canada, ensuring raw-oil supply while capturing dietary-supplement scale efficiencies. Yield10’s USDA clearance for EPA-producing Camelina provides a terrestrial alternative to volatile fisheries, and several pharma companies are negotiating offtake agreements aimed at derisking ESG exposure. Litigation remains fierce: Teva accuses Amarin of anticompetitive manipulation over excipient suppliers, underscoring ongoing legal jockeying for advantageous cost positions.

Marketing strategies increasingly emphasise differentiation beyond simple triglyceride lowering. Branded manufacturers invest in head-to-head trials versus GLP-1 drugs to highlight complementarity rather than substitution. Generics focus on real-world evidence that demonstrates parity with reference products, easing prescriber adoption. As health systems transition to value-based care, companies that pair clinical data with digital adherence solutions are likely to secure preferred-provider contracts.

Omega-3 Prescription Drugs Industry Leaders

Amarin Corporation plc

GlaxoSmithKline plc

Teva Pharmaceutical Industries Ltd.

Hikma Pharmaceuticals PLC

AstraZeneca plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DSM-Firmenich introduced Life’s DHA B54-0100, a high-potency DHA ingredient that enables smaller capsule formats.

- July 2024: KD Pharma Group acquired DSM-Firmenich’s marine-lipids division, including MEG-3 facilities in Peru and Canada.

- July 2024: Amarin partner EddingPharm received NMPA approval for Vascepa in mainland China, triggering a USD 15 million milestone payment.

- March 2024: Yield10 Bioscience obtained USDA-APHIS clearance for Camelina varieties producing EPA and DHA, paving a sustainable land-based supply route.

Global Omega-3 Prescription Drugs Market Report Scope

| EPA-only (Icosapent Ethyl) |

| EPA + DHA Ethyl Esters |

| Omega-3 Carboxylic Acids |

| Pipeline High-Concentrate Formulations |

| Severe Hypertriglyceridemia (?500 mg/dL) |

| Cardiovascular Risk Reduction (?150 mg/dL on statin) |

| Other Dyslipidemias |

| Soft-gel Capsules 1 g |

| Soft-gel Capsules 0.5 g |

| Liquid-filled Capsules / Suspensions |

| Hospital Pharmacies |

| Retail & Specialty Pharmacies |

| Online & Mail-order Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | EPA-only (Icosapent Ethyl) | |

| EPA + DHA Ethyl Esters | ||

| Omega-3 Carboxylic Acids | ||

| Pipeline High-Concentrate Formulations | ||

| By Indication | Severe Hypertriglyceridemia (?500 mg/dL) | |

| Cardiovascular Risk Reduction (?150 mg/dL on statin) | ||

| Other Dyslipidemias | ||

| By Dosage Form | Soft-gel Capsules 1 g | |

| Soft-gel Capsules 0.5 g | ||

| Liquid-filled Capsules / Suspensions | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail & Specialty Pharmacies | ||

| Online & Mail-order Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Omega-3 prescription drugs market?

The market is valued at USD 1.46 billion in 2025 and is projected to reach USD 1.98 billion by 2030.

Which formulation dominates sales?

EPA-only products lead with 52.3% of 2024 revenue due to their favourable cardiovascular outcomes profile.

Why is Asia Pacific considered the fastest-growing region?

China’s 2024 regulatory approval of icosapent ethyl and expanding healthcare coverage across emerging economies drive a 12.5% regional CAGR forecast.

What key factor fuels prescription growth beyond severe hypertriglyceridemia?

Expanded cardiovascular-risk labelling now covers statin-treated adults with triglycerides as low as 150 mg/dL, greatly enlarging the addressable population.

How are sustainability issues being tackled in supply chains?

Companies invest in algal fermentation and USDA-approved Camelina crops that produce EPA and DHA, reducing dependence on wild-catch fisheries.

Do generic entries threaten branded market share?

Generics exert price pressure, but brands retain advantages through superior outcomes data, high-potency formulations and adherence-support programs.

Page last updated on: