Anti Inflammatory Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

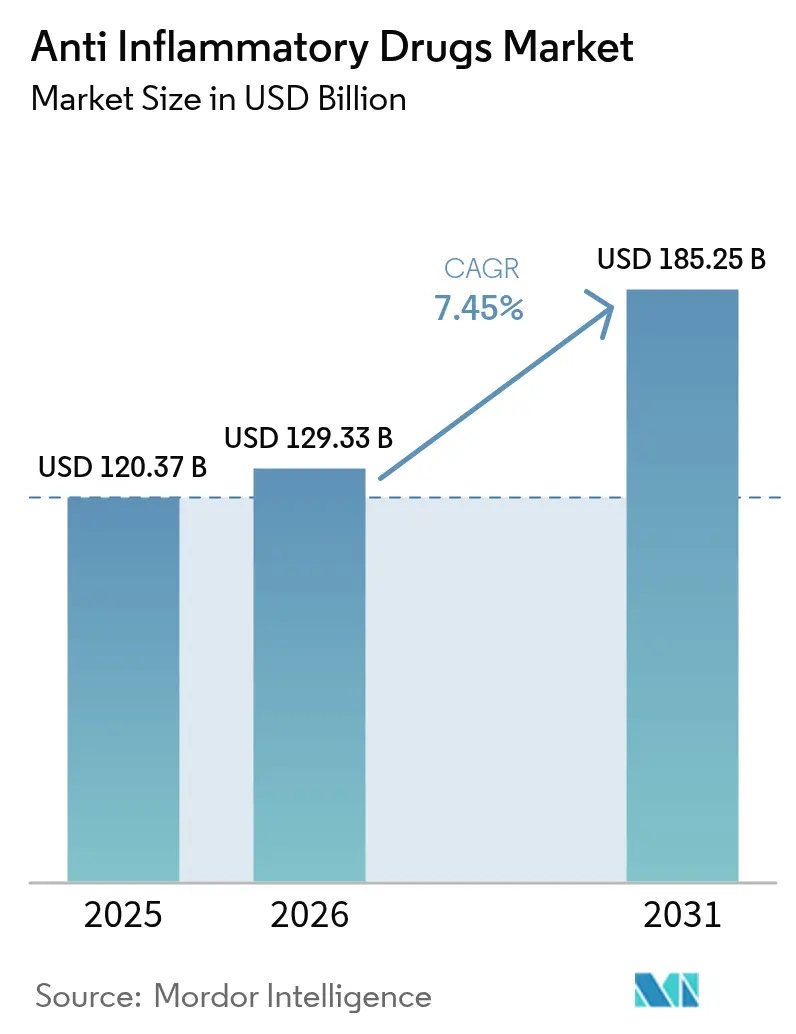

| Market Size (2026) | USD 129.33 Billion |

| Market Size (2031) | USD 185.25 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti Inflammatory Drugs Market Analysis by Mordor Intelligence

Anti-inflammatory drugs market size in 2026 is estimated at USD 129.33 billion, growing from 2025 value of USD 120.37 billion with 2031 projections showing USD 185.25 billion, growing at 7.45% CAGR over 2026-2031. Growth is anchored in global population aging, higher chronic disease incidence, and faster biologics discovery enabled by artificial intelligence. Demand is further supported by broader over-the-counter access to topical non-steroidal anti-inflammatory drugs (NSAIDs), expanding adoption of JAK inhibitors after unified safety labeling, and continued investment in precision medicine. Competitive activity remains moderate, with large pharmaceutical groups defending share through pipeline diversification, while biosimilar entrants narrow price gaps and expand patient access. Persistent concerns over COX-2 cardiovascular safety and active-pharmaceutical-ingredient (API) supply chain exposure to Asia temper momentum, yet novel indications such as colchicine for cardiovascular disease reveal new clinical and revenue pathways. The anti-inflammatory drugs market therefore balances steady base-therapy consumption with waves of innovation that raise therapeutic value.

Key Report Takeaways

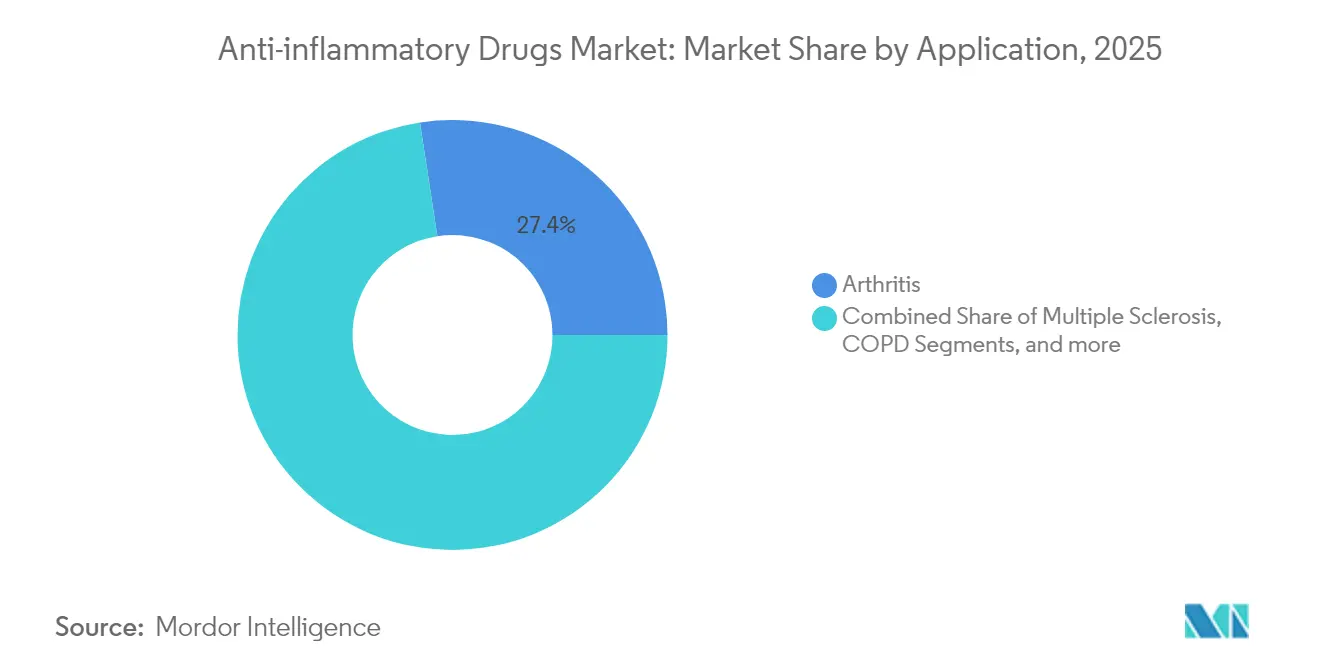

- By application, arthritis commanded 27.42% of anti-inflammatory drugs market share in 2025; tendonitis is projected to grow quickest at an 8.05% CAGR through 2031.

- By drug class, biologics led with 32.10% revenue share in 2025, while the segment is advancing at an 8.12% CAGR to 2031.

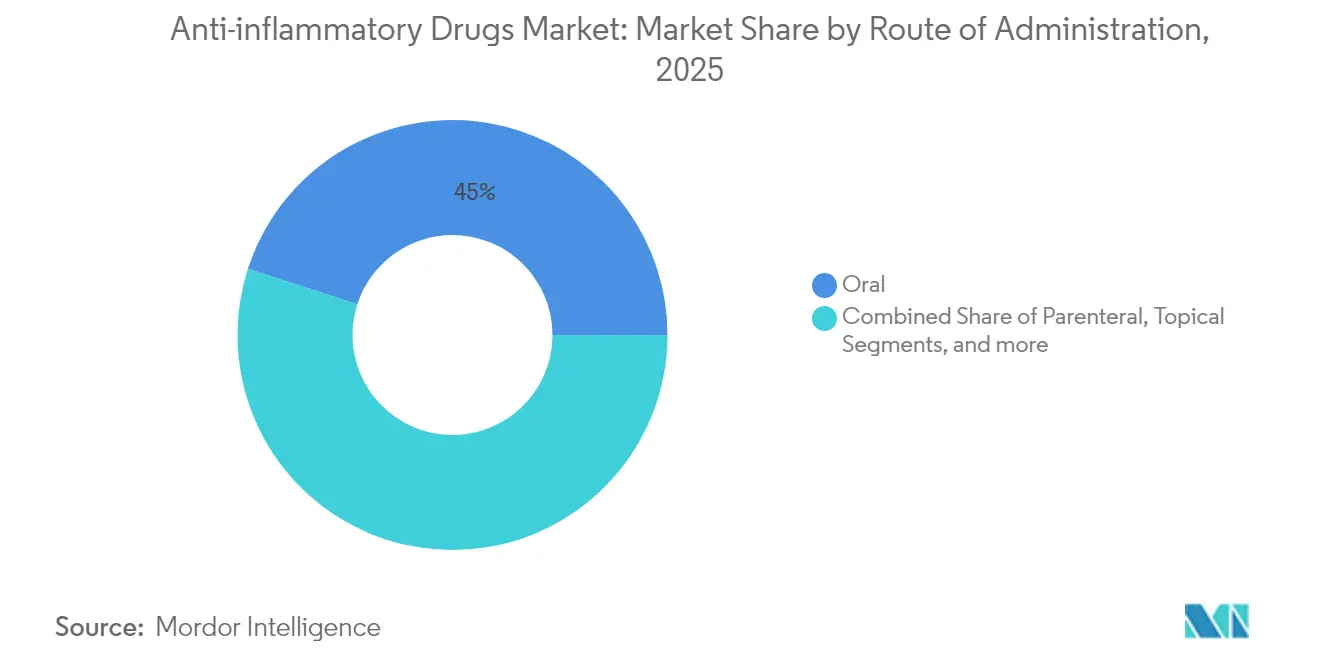

- By route of administration, oral formulations accounted for 45.02% of the anti-inflammatory drugs market size in 2025 and are expected to expand at an 8.01% CAGR through 2031.

- By sales channel, prescription distribution held 69.10% share of the anti-inflammatory drugs market size in 2025; the OTC channel is forecast to record the fastest 8.18% CAGR.

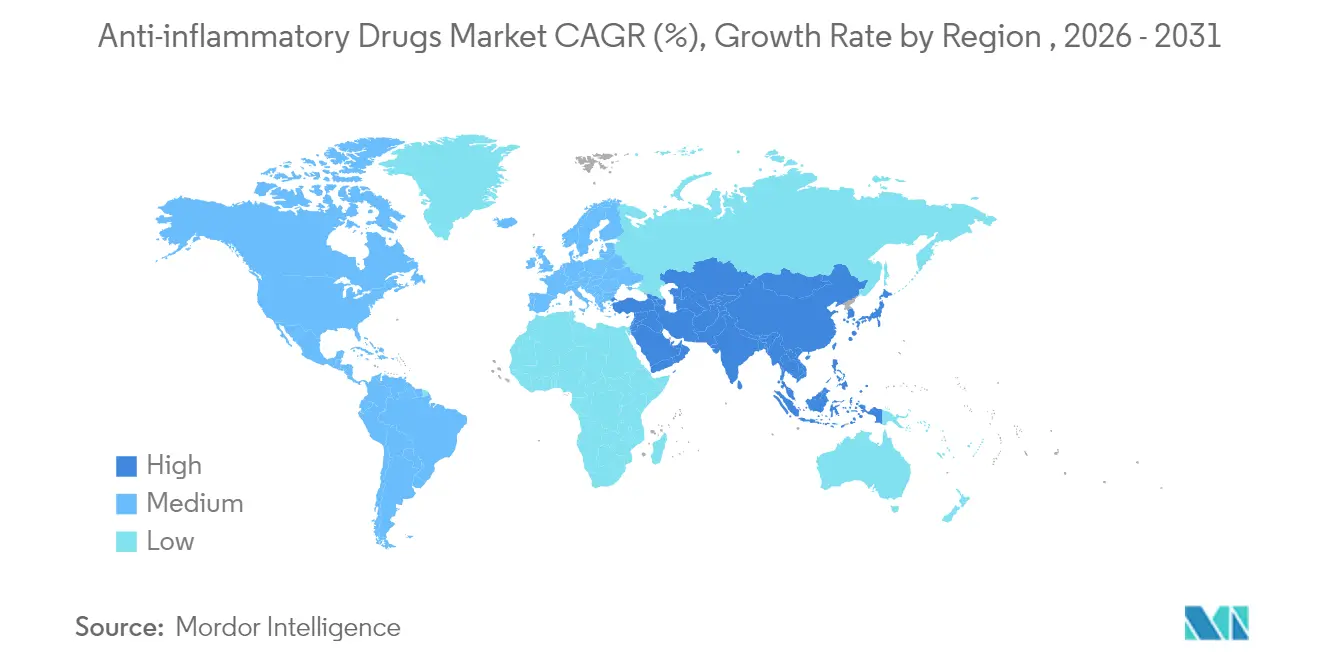

- Geographically, North America maintained 38.35% share of the anti-inflammatory drugs market in 2025, while Asia-Pacific is poised for an 8.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti Inflammatory Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating prevalence of obesity-linked osteoarthritis | +1.2% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Biologics pipeline acceleration due to AI-enabled target discovery | +1.8% | Global, concentrated in US and EU innovation hubs | Long term (≥ 4 years) |

| Expansion of OTC topical NSAID switches in Europe & U.S. | +0.9% | North America & EU | Short term (≤ 2 years) |

| Uptake of JAK inhibitors after safety-label harmonisation | +1.4% | Global, led by developed markets | Medium term (2-4 years) |

| Growing demand for once-weekly depot corticosteroid injectables | +0.7% | Global, early adoption in hospital systems | Medium term (2-4 years) |

| Hospital antimicrobial-stewardship programs favouring steroid-sparing regimens | +0.5% | Global, concentrated in developed healthcare systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of Obesity-Linked Osteoarthritis

Growing obesity and longevity are jointly raising osteoarthritis caseloads, stimulating the anti-inflammatory drugs market. Mechanical strain and low-grade systemic inflammation accelerate cartilage loss, driving sustained demand for safe analgesia. Observational studies indicate topical diclofenac gel yields symptom relief with 74.2% of users reporting no adverse events, a meaningful safety edge for obese patients with cardiovascular comorbidity[1]Pain Therapy, “Long-Term Safety of Topical Diclofenac in Obese Osteoarthritis Patients,” link.springer.com. Payers endorse weight-neutral therapeutics and integrated metabolic-inflammation regimens, expanding formularies for topical NSAIDs and glucosamine combinations. Device-coupled drug delivery and single-visit depot corticosteroid injections further heighten adherence. Collectively, obesity-driven osteoarthritis provides a long-run volume anchor for the anti-inflammatory drugs market.

Biologics Pipeline Acceleration Through AI-Enabled Discovery

Generative algorithms shorten target identification, optimize binding affinity and de-risk lead candidates, enabling faster biologic entry. Insilico Medicine progressed ISM5411 for inflammatory bowel disease from in-silico concept to Phase 1 inside 30 months. Big Pharma now pairs internal libraries with AI platforms to refresh immunology portfolios, enhancing the anti-inflammatory drugs market with differentiated mechanisms. Companion diagnostics derived from genomics refine patient selection, bolstering trial success rates and payer acceptance. The virtuous cycle of data, modeling and clinical validation promises sustained biologics innovation through 2030. Regions with strong digital infrastructure, notably the United States, Germany and the United Kingdom, capture much of this activity, but strategic partnerships extend capacity into China and Singapore research hubs.

Prescription-to-OTC Switches for Topical NSAIDs

Health agencies continue approving OTC status for topical NSAIDs after extensive safety reviews. The FDA concluded prior withdrawals of diclofenac solution were non-safety related, opening pathways for generics[2]FDA, “Post-marketing Safety Evaluation of Topical Diclofenac,” fda.gov. European regulators broadened non-prescription access, citing favorable benefit-risk profiles. Meta-analysis shows diclofenac patches provide the fastest early pain relief among topical forms[3]BMC Musculoskeletal Disorders, “Efficacy of Diclofenac Patch Versus Gel and Solution,” bmcmusculoskeletdisord.biomedcentral.com. Consumers value self-directed care, and pharmacists provide frontline triage, reducing physician visits. Manufacturers benefit from brand recognition and incremental revenue while offloading rebate negotiation burdens. These developments widen the anti-inflammatory drugs market footprint in community settings.

Wider Uptake of JAK Inhibitors After Unified Safety Labels

Regulators harmonized boxed warnings for JAK inhibitors in 2024, clarifying thromboembolic and cancer risks relative to TNF blockers. Registry data from BIOBADASER confirmed comparable safety and similar one-year persistence at 68%. The 2025 EULAR congress reported no higher malignancy incidence across 53,169 treatment starts, restoring prescriber confidence. Upadacitinib achieved 24.6% clinical remission versus 18.7% for adalimumab after five years. Convenience of once-daily oral dosing and rapid onset spur adoption in rheumatoid arthritis, ulcerative colitis and atopic dermatitis. Sustained uptake injects higher-margin therapies into the anti-inflammatory drugs market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cardiovascular boxed-warnings on COX-2 NSAIDs | -1.1% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Biologic price erosion from biosimilars in EU5 | -0.8% | EU5 markets, with spillover to other regions | Short term (≤ 2 years) |

| Rising litigation over proton-pump-inhibitor co-prescriptions | -0.6% | Global | Medium term (2-4 years) |

| Supply-chain vulnerability of API precursors sourced from China | -0.5% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cardiovascular Boxed-Warnings on COX-2 NSAIDs

Although the PRECISION trial positioned celecoxib as non-inferior to naproxen or ibuprofen for major adverse cardiac events, prescriber caution persists. FDA advisory committees considered but did not remove celecoxib warnings, sustaining perception hurdles Arthritis Foundation. Korean insurance data on ankylosing spondylitis indicated dose-dependent cardiovascular risk with adjusted hazard ratio of 1.12 for heart failure Annals of the Rheumatic Diseases. Clinicians therefore limit high-dose or long-term COX-2 NSAID use, especially in older or high-risk patients. The restraint caps systemic NSAID growth and shifts volume toward topical NSAIDs and biologics, marginally slowing the anti-inflammatory drugs market.

Biologic Price Erosion From Biosimilars in EU5

Europe’s robust biosimilar framework accelerates reference-product substitution. Adalimumab biosimilars reached 53% unit share in 2024, cutting average prices 7%. Polish etanercept experienced price rebounds once competition lapsed, highlighting volatility. Across EU insulin glargine markets, biosimilar entry trimmed median prices 21.6%. Intensifying tenders pressure manufacturer margins, obliging originators to bundle support services or pivot to next-generation agents. While patient access rises, headline revenue growth slows, curbing the anti-inflammatory drugs market expansion in cost-controlled regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Arthritis Dominance Drives Tendonitis Innovation

Arthritis applications command 27.42% market share in 2025, reflecting the segment's established treatment protocols and large patient population requiring chronic management. However, tendonitis emerges as the fastest-growing application at 8.05% CAGR through 2031, driven by evolving treatment paradigms that emphasize early intervention and targeted anti-inflammatory approaches. Recent preclinical research demonstrates that both local and oral NSAIDs provide effective short-term relief for tendon overuse-related pain, with particular efficacy in acute shoulder tendonitis and bursitis. Multiple sclerosis and inflammatory bowel disease applications are experiencing robust growth as new targeted therapies expand treatment options, while COPD applications benefit from steroid-sparing regimens that reduce long-term complications.

The application landscape is being reshaped by precision medicine approaches that match specific inflammatory pathways to targeted interventions. Tendon-bone healing research emphasizes the critical role of inflammatory modulation, with emerging therapies focusing on macrophage polarization and cytokine regulation to optimize repair processes. Asthma applications are witnessing significant innovation with JAK inhibitors demonstrating efficacy across multiple inflammatory cascades, while other treatment categories benefit from combination approaches that address both acute symptoms and underlying disease progression. The shift toward application-specific biomarkers and companion diagnostics is enabling more precise treatment selection, particularly in complex conditions where multiple inflammatory pathways contribute to disease pathology.

By Drug Class: Biologics Leadership Accelerates Innovation

Anti-inflammatory biologics maintain market leadership with 32.10% share in 2025 and drive growth at 8.12% CAGR through 2031, reflecting continued innovation in targeted immunomodulation and expanding indication approvals. The class benefits from AI-accelerated drug discovery, with generative platforms enabling more precise target identification and molecular optimization that reduces development timelines and improves success rates. Non-steroidal anti-inflammatory drugs remain essential for acute management, while corticosteroids face pressure from steroid-sparing alternatives that offer comparable efficacy with reduced adverse effect profiles. Immune-selective anti-inflammatory derivatives represent an emerging category that promises more precise inflammatory modulation with fewer systemic effects.

Recent regulatory approvals demonstrate the biologics segment's momentum, with upadacitinib receiving its eighth indication for giant cell arteritis and demonstrating 46.4% sustained remission rates compared to 29.0% for placebo. The segment is also benefiting from novel mechanisms of action, including TL1A inhibitors that are showing superior efficacy in inflammatory bowel disease, with Merck's PRA-023 achieving 49.1% remission rates in Crohn's disease patients. Other drug classes are evolving toward combination approaches and sustained-release formulations that improve patient compliance and therapeutic outcomes while reducing dosing frequency and systemic exposure.

By Route of Administration: Oral Convenience Meets Topical Innovation

The oral route commands 45.02% market share in 2025 and leads growth at 8.01% CAGR through 2031, driven by patient preference for convenient administration and expanding once-daily formulations that improve compliance. Parenteral administration serves critical roles in acute care settings and for biologics that require injection, while topical applications are gaining traction through improved formulation technologies that enhance skin penetration and localized delivery. Inhalation routes serve specialized applications in respiratory inflammatory conditions, with novel delivery systems improving drug deposition and reducing systemic exposure.

Topical delivery innovations are reshaping the route landscape, with advanced formulations including solid lipid nanoparticles and hydrogels demonstrating enhanced therapeutic efficacy and reduced systemic side effects. The FDA approval of novel topical treatments like ZORYVE (roflumilast) cream for plaque psoriasis and atopic dermatitis demonstrates the potential for phosphodiesterase 4 inhibitors in localized anti-inflammatory therapy. Parenteral routes are benefiting from long-acting formulations that reduce injection frequency, while inhalation delivery is advancing through smart inhaler technologies that optimize drug deposition and monitor patient adherence. The convergence of route optimization with personalized medicine approaches is enabling more precise therapeutic interventions tailored to individual patient needs and disease characteristics.

By Sales Channel: OTC Expansion Transforms Access Patterns

Prescription channels maintain dominance with 69.10% market share in 2025, reflecting the complex nature of chronic inflammatory conditions that require physician oversight and monitoring. However, over-the-counter channels represent the fastest-growing segment at 8.18% CAGR through 2031, driven by regulatory switches of proven therapies and consumer demand for accessible pain management solutions. This channel expansion is particularly pronounced for topical NSAIDs, where extensive safety data supports broader patient access without prescription requirements.

The OTC transformation is being accelerated by real-world evidence demonstrating the safety and efficacy of self-administered treatments, with studies showing that 74.2% of patients using topical diclofenac sodium gel experience no adverse events over extended periods. Digital health platforms are enhancing OTC channel effectiveness by providing patient education, symptom tracking, and guidance on appropriate use, while pharmacist consultation services bridge the gap between prescription oversight and self-care. The channel evolution is also being shaped by healthcare cost containment efforts, as OTC access reduces physician consultation requirements and enables more efficient resource allocation within healthcare systems.

Geography Analysis

North America retained 38.35% of global revenue in 2025, underpinned by advanced reimbursement, rapid uptake of novel agents and rigorous clinical research capacity. The United States approved JOURNAVX, the first non-opioid NaV1.8 blocker for acute pain, reinforcing therapeutic leadership. Biosimilar penetration, including adalimumab alternatives, aligns with payer cost-containment goals, slightly moderating net sales growth. Federal incentives to reshore key APIs and diversify sourcing address supply vulnerabilities exposed during 2024 logistics disruptions. Canada expands real-world evidence requirements, enhancing post-marketing surveillance and driving formulary refinement.

Asia-Pacific records the highest 8.2% CAGR through 2031. China’s centralized procurement lowers biologic prices and accelerates hospital uptake, while domestic manufacturers scale TNF inhibitor biosimilars. India’s Ayushman Bharat insurance scheme enlarges patient coverage and boosts retail OTC demand. Japan remains a bellwether for aging-related inflammatory disease, supporting steady biologic utilization. Southeast Asian markets invest in clinical trial infrastructure, attracting multinational sponsors. Collectively, rising income, urbanization and chronic disease prevalence fuel anti-inflammatory drugs market expansion in the region.

Europe holds meaningful share but faces intensified price erosion from biosimilars. Germany’s early access pathways and digital therapeutics pilots demonstrate commitment to innovation, yet health technology assessments demand robust cost-effectiveness evidence. The United Kingdom’s Medicines and Healthcare products Regulatory Agency (MHRA) post-Brexit flexibility expedites approvals, balancing competition with patient access. The Middle East and Africa invest in tiered formulary systems and biosimilar adoption to widen therapy reach, while Latin America modernizes regulatory frameworks, encouraging multinationals to localize production. Those developments collectively sustain global momentum for the anti-inflammatory drugs market while highlighting regional nuances.

Competitive Landscape

The anti-inflammatory drugs market remains moderately consolidated. AbbVie, Johnson & Johnson, Novartis, Pfizer and Amgen controlled majority of 2024 revenue, leveraging broad immunology portfolios, biologic manufacturing scale and multi-channel marketing. AbbVie generated USD 17.7 billion from Skyrizi and Rinvoq in 2024, offsetting Humira biosimilar erosion. Johnson & Johnson’s Stelara and Tremfya maintained franchise strength, while impending biosimilar competition spurs pipeline diversification. Novartis advanced Vanrafia, a selective endothelin A antagonist, extending immunology reach into renal inflammation. Pfizer integrates digital monitoring with etanercept to defend market share.

Biosimilar manufacturers—Samsung Bioepis, Fresenius Kabi and Sandoz—expand tender coverage, especially in Europe, exerting pricing pressure on reference biologics. Chinese firms produce cost-competitive adalimumab and infliximab biosimilars, entering Latin America and Middle East markets. AI-native companies such as Insilico Medicine and BenevolentAI partner with incumbents to co-develop next-generation therapeutics, threatening traditional discovery timelines. Digital health start-ups deliver companion diagnostics and remote monitoring, adding non-pharmacologic differentiation. Mergers and acquisitions focus on mid-phase assets in inflammatory bowel disease and dermatology, reflecting appetite for incremental mechanism diversity within the anti-inflammatory drugs market.

Strategic responses include outcome-based contracts, co-pay assistance and real-world evidence generation to reinforce value propositions. Manufacturers invest in continuous bioprocessing to cut costs and secure supply. Patient-centric initiatives—such as self-injector training apps and community nurse programs—strengthen adherence. Looking ahead, competitive intensity will hinge on biosimilar uptake rates, AI-enabled discovery output and payer tolerance for premium pricing.

Anti Inflammatory Drugs Industry Leaders

Johnson & Johnson

Pfizer Inc.

AbbVie Inc

F. Hoffmann-La Roche AG

AstraZeneca PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AbbVie won FDA approval for RINVOQ (upadacitinib) in giant cell arteritis, with 46.4% of patients achieving sustained remission versus 29.0% on placebo.

- March 2025: Novartis secured FDA accelerated approval for Vanrafia (atrasentan) in primary IgA nephropathy after showing a 36.1% proteinuria reduction.

- January 2025: Vertex gained FDA clearance for JOURNAVX (suzetrigine), the first NaV1.8 sodium-channel blocker for moderate-to-severe acute pain.

- June 2023: AGEPHA Pharma USA announced the FDA approval of Lodoco (colchicine) as the first anti-inflammatory cardiovascular therapy, reducing composite events 31% when added to standard care.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the anti-inflammatory drugs market as the global sales value of prescription-strength and over-the-counter medicines whose primary mechanism lowers inflammatory pathways, including biologics (e.g. TNF or IL inhibitors), non-steroidal anti-inflammatory drugs (NSAIDs), corticosteroids, and newer immune-selective derivatives. Products formulated for human use across oral, parenteral, topical, or inhalation routes are in scope.

Scope Exclusions. We exclude adjunct analgesics with no direct anti-inflammatory effect, ophthalmic-only NSAIDs, veterinary drugs, and active pharmaceutical ingredient contract revenues.

Segmentation Overview

- By Application

- Arthritis

- Chronic Obstructive Pulmonary Disease (COPD)

- Multiple Sclerosis

- Inflammatory Bowel Disease (IBD)

- Asthma

- Tendonitis

- Other Applications

- By Drug Class

- Anti-Inflammatory Biologics

- Non-steroidal Anti-Inflammatory Drugs (NSAIDs)

- Corticosteroids

- Immune-selective Anti-inflammatory Derivatives (ImSAIDs)

- Other Drug Classes

- By Route of Administration

- Oral

- Parenteral

- Topical

- Inhalation

- By Sales Channel

- Prescription

- Over-the-Counter (OTC)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed hospital pharmacists across North America, rheumatologists in Europe, pulmonologists in Asia-Pacific, and procurement managers at large retail chains to validate volume splits, typical course pricing, and uptake of biosimilars. Short on-the-floor surveys with patients' advocacy groups clarified out-of-pocket patterns and OTC substitution, enabling us to fine-tune elasticity assumptions.

Desk Research

We began by mapping demand pools through publicly available tier-1 statistics such as WHO Global Health Estimates, CDC arthritis prevalence dashboards, OECD Health Expenditure, and UN Population Prospects, supported by trade association notes from the European Medicines Agency and Arthritis Foundation. Company 10-Ks, drug approval dossiers, and investor decks helped us capture brand-level revenue signals, which were then cross-checked on D&B Hoovers and Dow Jones Factiva for consistency. Patent trend snapshots from Questel (illustrating biologic biosimilar waves) offered forward cues. These sources are illustrative only; numerous additional publications informed our evidence base.

Market-Sizing & Forecasting

Market sizing started with a top-down prevalence-to-treatment build. Arthritis, asthma, COPD, IBD, and tendonitis cohorts were sized country by country, multiplied by treatment penetration and average annual therapy cost; supplier roll-ups of sampled brand revenues offered a bottom-up reasonableness check. Key variables feeding the model included diagnosed arthritis incidence, biologic penetration rates, median biologic versus NSAID prices, generic erosion curves, patent-expiry calendars, and retail versus hospital channel mix.

For forecasting, multivariate regression combined with scenario analysis projected how aging population growth, biosimilar discount depth, and pipeline approvals translate into value CAGR, while ARIMA smoothing handled seasonality in OTC sales. Data gaps, especially in emerging markets, were bridged by regional analog proxies and expert-agreed adjustment factors.

Data Validation & Update Cycle

Before sign-off, our analysts run variance tests against prescription audit snapshots and quarterly company earnings; anomalies trigger re-checks with original respondents. The model is refreshed every twelve months, and an interim update is issued when material events such as blockbuster launches or major safety recalls occur. A final real-time sweep is completed just prior to client delivery.

Why Mordor's Anti-Inflammatory Drugs Baseline Commands Reliability

Published estimates often differ, and buyers ask why. Divergences usually stem from how firms slice the product universe, pick base years, convert currencies, or apply list versus net price assumptions.

Key gap drivers emerge when other publishers blend symptomatic analgesics with anti-inflammatory therapeutics or adopt a single-source top-down view without primary cross-checks; some also lock forecasts for three-year cycles, whereas we update annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 120.37 B (2025) | Mordor Intelligence | - |

| USD 136.86 B (2024) | Global Consultancy A | Includes broader pain-management drugs and applies list prices without net-discount validation |

| USD 122.32 B (2024) | Trade Journal B | Utilizes limited primary interviews and a three-year refresh cadence, causing outdated epidemiology inputs |

The comparison shows that, by selecting a precise scope, layering contemporaneous payer and prescriber insights, and employing yearly revisions, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to verifiable variables and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the anti-inflammatory drugs market?

The anti-inflammatory drugs market generated USD 129.33 billion in 2026 and is projected to reach USD 185.25 billion by 2031.

Which application segment is growing fastest?

Tendonitis is forecast to expand at an 8.05% CAGR through 2031, outpacing other applications due to earlier diagnosis and targeted therapies.

How dominant are biologics within the market?

Biologics held 32.10% revenue share in 2025 and are growing at an 8.12% CAGR, driven by AI-accelerated discovery and multiple new indications.

Why are topical NSAIDs moving to OTC status?

Extensive safety data and regulator support have prompted prescription-to-OTC switches, improving patient access and lowering healthcare costs.

Which region shows the highest growth potential?

Asia-Pacific leads with an 8.2% CAGR through 2031, benefiting from rising healthcare spending, broader insurance coverage and local production capacity.

How are biosimilars affecting market pricing?

In Europe, adalimumab biosimilars captured 53% share in 2024, reducing average prices by 7% and pressuring originator profit margins.

Page last updated on: