Prescription Dermatology Therapeutics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

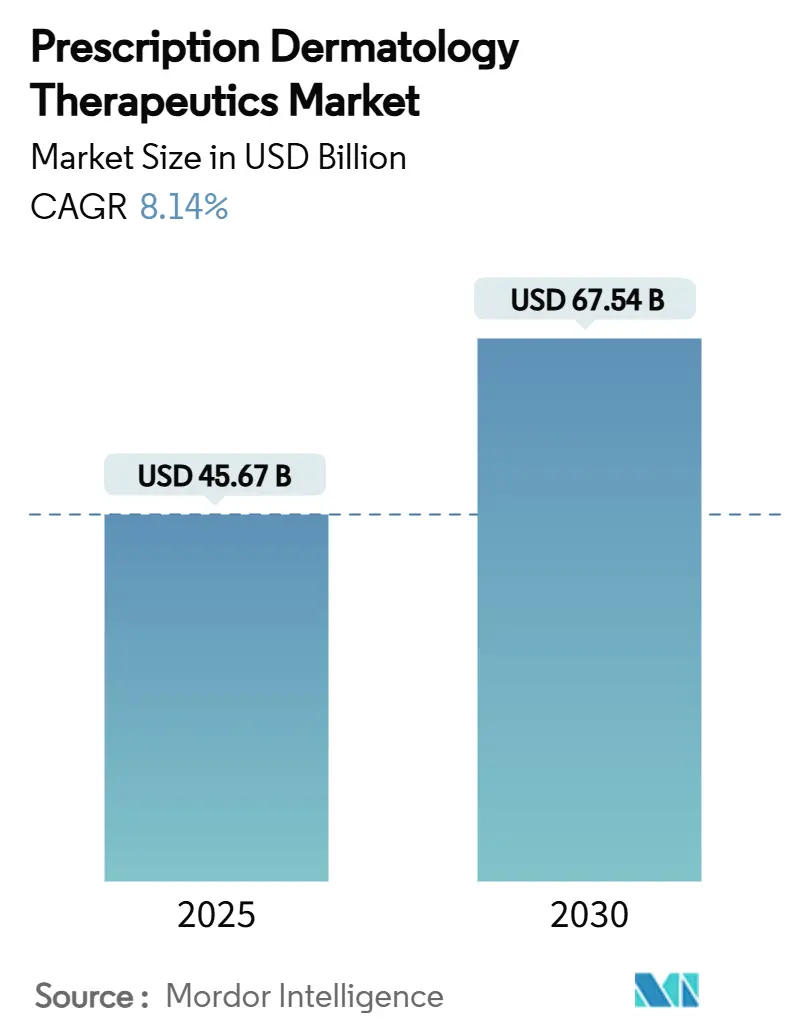

| Market Size (2025) | USD 45.67 Billion |

| Market Size (2030) | USD 67.54 Billion |

| Growth Rate (2025 - 2030) | 8.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prescription Dermatology Therapeutics Market Analysis by Mordor Intelligence

The prescription dermatology therapeutics market size was USD 45.67 billion in 2025 and is on track to reach USD 67.54 billion by 2030, reflecting an 8.14% CAGR. Demand is rising as climate-linked flare-ups of chronic dermatoses push patients and physicians toward targeted biologics and small-molecule immunomodulators. Regulatory fast-tracking of new mechanisms, coupled with simultaneous biosimilar launches, is reshaping competitive pricing. Digital care models that join tele-dermatology to e-prescribing are widening access, while cold-chain advances are easing geographic bottlenecks for injectable biologics. In emerging economies, higher discretionary income and broader insurance coverage are expanding the treated population.

Key Report Takeaways

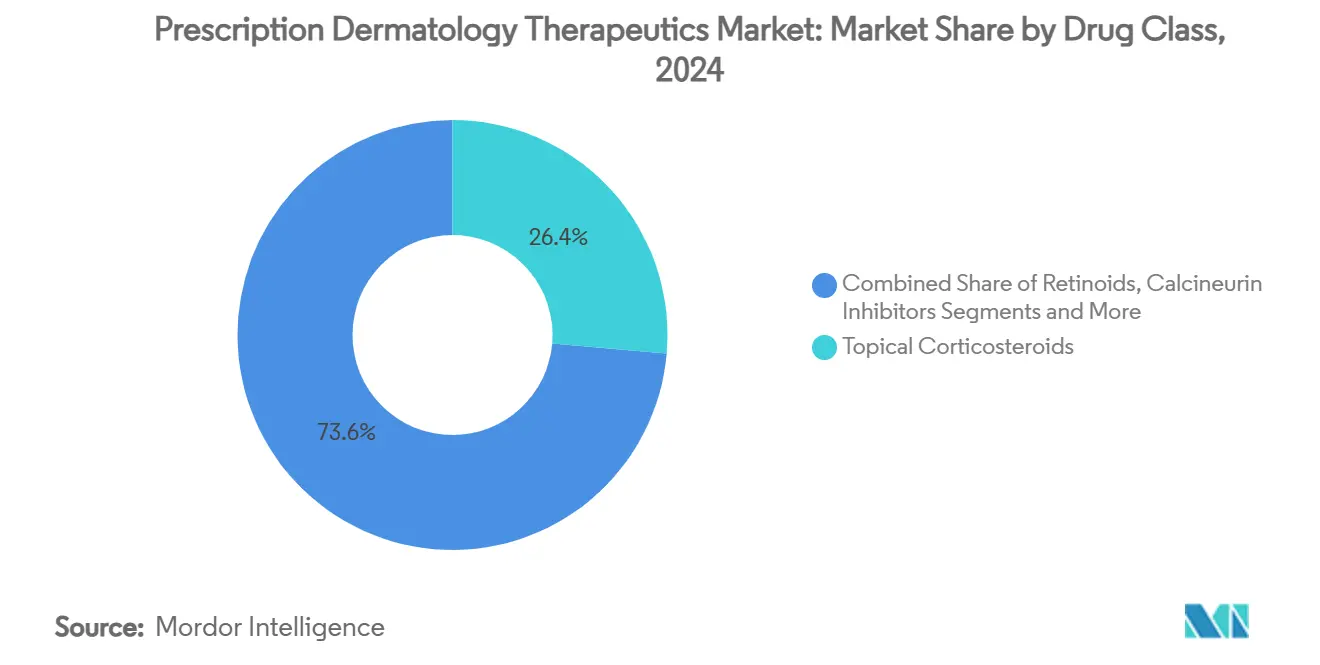

- By drug class, topical corticosteroids led with 26.37% of the prescription dermatology therapeutics market share in 2024, while JAK inhibitors are projected to record the fastest 12.45% CAGR through 2030.

- By disease indication, psoriasis accounted for 32.33% of the prescription dermatology therapeutics market size in 2024; alopecia therapies are expected to expand at an 11.56% CAGR over the same period.

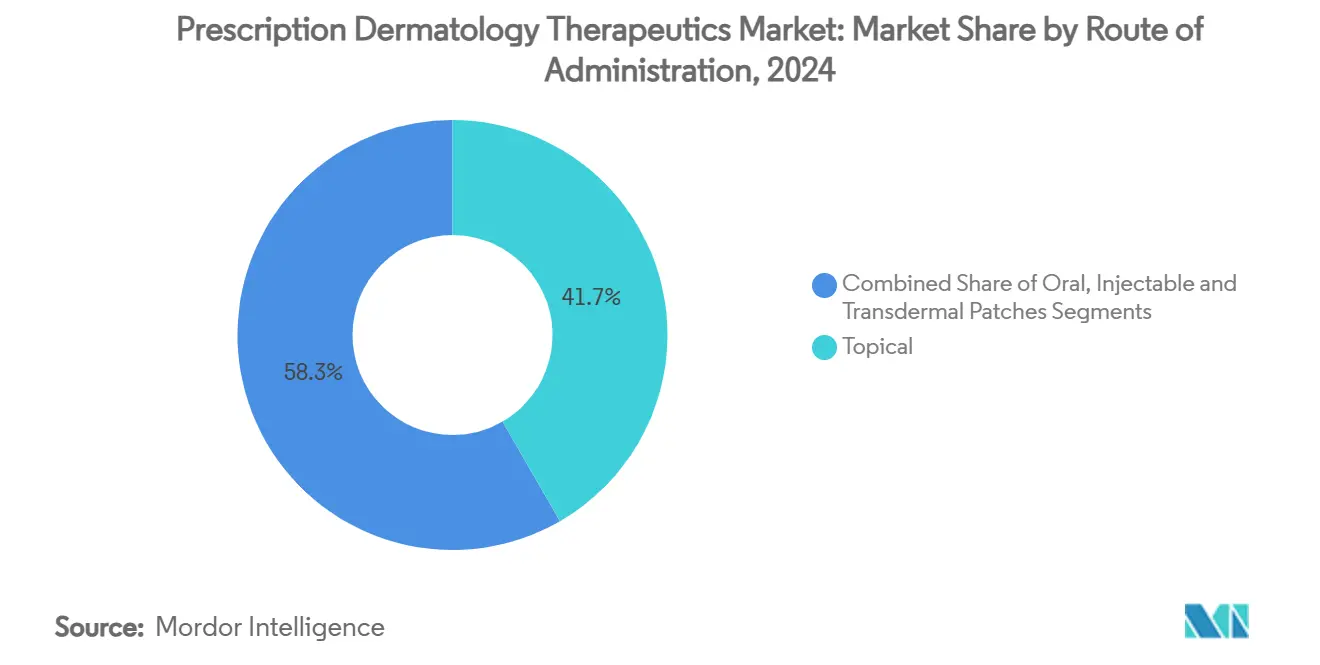

- By route of administration, topical formulations held 41.66% of the prescription dermatology therapeutics market share in 2024, whereas injectables are forecast to advance at a 10.69% CAGR.

- By distribution channel, hospital pharmacies captured 36.84% of the prescription dermatology therapeutics market size in 2024, while online pharmacies are set to grow at a 12.89% CAGR through 2030.

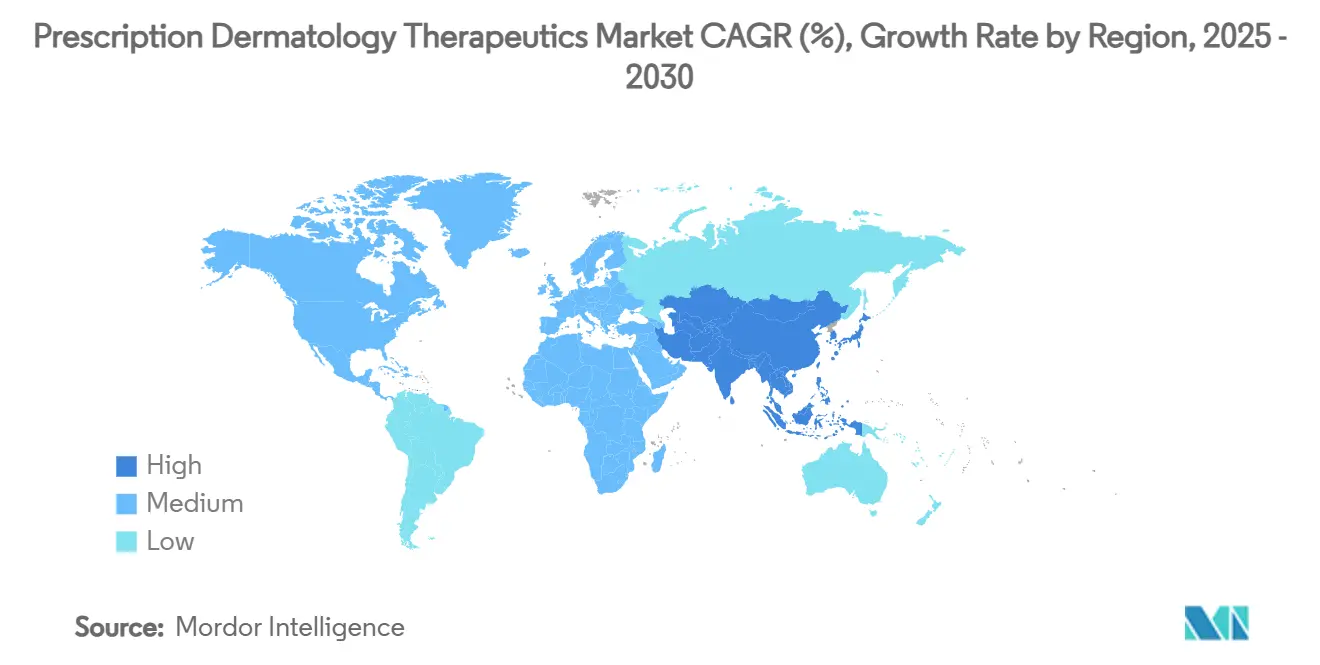

- By geography, North America dominated with 33.68% of the prescription dermatology therapeutics market share in 2024, and Asia-Pacific is anticipated to post the fastest 10.46% CAGR to 2030.

Global Prescription Dermatology Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Chronic Skin Diseases | +1.8% | Global, with highest impact in Asia-Pacific and emerging economies | Long term (≥ 4 years) |

| Accelerated Approvals Of Novel Biologics & Biosimilars | +2.1% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Expansion Of Tele-Dermatology & E-Prescription Platforms | +1.4% | Global, with early gains in North America, Europe, Australia | Short term (≤ 2 years) |

| Increasing Healthcare Spending In Emerging Economies | +1.2% | APAC core, Latin America, MEA emerging markets | Long term (≥ 4 years) |

| AI-Enabled Diagnostic Tools Boosting Prescription Volumes | +0.9% | North America & EU, expanding to developed APAC markets | Medium term (2-4 years) |

| Climate Change–Linked Surge In Inflammatory Skin Disorders | +0.6% | Global, with acute impact in wildfire-prone regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Skin Diseases

Urban pollution and an aging population are driving a steady rise in psoriasis, atopic dermatitis, and other inflammatory dermatoses. Fine-particle exposure below current guideline levels has been tied to persistent cytokine activation that extends well past initial contact.[1]R.W. Kim et al., “Air Pollution and Inflammatory Skin Disease—Can Clinicians Make Recommendations to Reduce Risk?,” JAMA Network Open, jamanetwork.com The International Eczema Council cataloged ten separate climate hazards that now aggravate atopic dermatitis, eroding the seasonality once typical of flare patterns.[2]Sheng-Pei Wang, “Impact of Climate Change on Atopic Dermatitis,” Allergy, wiley.com Rising disease burden increases lifetime prescription cycles, strengthening the long-run revenue base for advanced therapies.

Accelerated Approvals of Novel Biologics & Biosimilars

Breakthrough designations and priority reviews have shortened U.S. approval timelines for first-in-class agents like nemolizumab, the inaugural IL-31 receptor blocker for atopic dermatitis.[3]Galderma, “FDA Approval for Nemluvio,” galderma.com At the same time, clustered biosimilar launches—three ustekinumab copies debuted within weeks—are compressing price premiums sooner after patent expiry. Together, the twin tracks of innovation and commoditization are recasting budget impact forecasts across payer systems.

Expansion of Tele-Dermatology & E-Prescription Platforms

Remote care tools now deliver same-day diagnoses for thousands of skin conditions, then route scripts directly to online pharmacies. Integrated video consults and e-prescriptions simplify follow-up, improving adherence and enlarging the treated base outside metro hubs. Regulatory reciprocity compacts among U.S. states have eased cross-border tele-practice, and similar provisions are emerging in the EU and Australia.

Increasing Healthcare Spending in Emerging Economies

Insurance expansion and public-sector initiatives in India, China, and Brazil are elevating demand for branded dermatology agents. China’s IPO pipeline for home-grown vitiligo drugs signals growing investor confidence in regional R&D. Multinationals are responding with tiered pricing and local fill-finish partnerships to preserve margins while widening access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Biologic Therapies | -1.5% | Global, with acute impact in emerging markets and uninsured populations | Medium term (2-4 years) |

| Safety Concerns Around Long-Term Corticosteroid Use | -0.8% | Global, with regulatory focus in North America & EU | Short term (≤ 2 years) |

| OTC Microbiome Products Cannibalising Prescriptions | -0.6% | North America & EU core, expanding to developed APAC markets | Medium term (2-4 years) |

| Cold-Chain Logistics Bottlenecks For Specialty Injectables | -0.4% | Global, with acute impact in emerging markets and rural areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologic Therapies

Complex cell-culture processes and multi-phase trials keep biologic costs high, forcing payers to impose prior authorization hurdles and step-therapy mandates. While biosimilars lower list prices, physician reluctance to switch entrenched patients tempers immediate savings.

Safety Concerns Around Long-Term Corticosteroid Use

Adverse events such as dermal atrophy and hypothalamic-pituitary suppression restrict chronic use durations. Tougher labeling and monitoring raise compliance costs even as steroid-sparing creams like tapinarof gain favor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Versatile JAK Inhibitors Accelerate Adoption

JAK inhibitors posted a 12.45% CAGR and are broadening beyond atopic dermatitis into alopecia and vitiligo. The July 2024 U.S. approval of deuruxolitinib for severe alopecia areata demonstrated 80% scalp-hair recovery in roughly one-third of patients after 24 weeks. Topical corticosteroids still command the largest slice of the prescription dermatology therapeutics market but are losing momentum as safety-first guidelines prioritize steroid-sparing regimens. Biologics and biosimilars are filling that void with differentiated mechanisms and cost-relief options, while PDE-4 inhibitors such as roflumilast cream extend targeted therapy to pediatric cohorts.

Pharmacoeconomic models suggest that early use of higher-cost biologics offsets long-run hospitalization risks, an argument that is resonating with payers in North America and parts of Europe. Pipeline activity leans toward combination molecules that interrupt multiple inflammatory cascades. This approach aims to deliver durable remission while simplifying dosing schedules, a key adherence booster for chronic conditions.

By Disease Indication: Alopecia Gains Momentum

Alopecia therapies are projected to grow 11.56% annually, propelled by fresh JAK approvals and rising public awareness of the psychosocial load of hair loss. Ritlecitinib and deuruxolitinib have set a precedent for oral, once-daily regimens that produce cosmetically meaningful hair regrowth. Psoriasis retains dominance within the prescription dermatology therapeutics market, undergirded by a crowded biologic class that includes IL-17, IL-23, and TNF inhibitors. Atopic dermatitis sits close behind, leveraging IL-31 blockade and extended-half-life antibodies to improve convenience.

Under-served disorders such as chronic hand eczema and prurigo nodularis are attracting targeted R&D funding after regulatory precedents for special designations lowered hurdle rates. For acne, triple-combination topicals like Cabtreo offer multi-pathway control in a single tube, thereby capturing compliance value.

By Route of Administration: Injectables Outpace Topicals

Injectable agents are advancing at a 10.69% CAGR, buoyed by extended-half-life antibodies that reduce dosing to two injections per year—a win for adherence and cold-chain efficiency. Though topicals remain first-line for localized disease, their 41.66% share of the prescription dermatology therapeutics market is slowly eroding as systemic options deliver deeper clearance with convenient schedules. Oral small-molecule agents occupy a middle ground, offering whole-body coverage but requiring ongoing liver-function monitoring.

Innovation in microneedle patches promises a hybrid of topical ease and injectable pharmacokinetics, but high production costs keep commercial rollout years away. Route choice now hinges on disease severity, patient lifestyle, and insurance formulary positioning.

By Distribution Channel: Online Pharmacies Scale Rapidly

Digital pharmacies are projected to expand 12.89% per year, anchored by seamless tele-consults that convert video diagnoses into doorstep delivery. Hospital pharmacies, holding a 36.84% share of the prescription dermatology therapeutics market size, remain essential for biologic initiation under specialist oversight.

Retail chains face margin compression from mail-order rivals but retain foot-traffic advantages for acute prescription fills. Compounding pharmacies cater to niche allergen-free or customized-dose needs yet operate under stricter regulatory guardrails after recent sterility incidents.

Geography Analysis

North America captured 33.68% of global revenue in 2024 thanks to high biologic uptake, favorable reimbursement, and robust tele-health networks. The FDA’s priority-review pathway, illustrated by the December 2024 approval of nemolizumab, enables rapid commercial rollout across U.S. payers. Canada is gradually aligning safety assessments to accelerate parallel adoption, while Mexico leverages regional trade pacts to import biosimilars at discounted rates.

Europe’s cost-effectiveness frameworks restrain list prices yet reward durable remission data. February 2025 EU approval of nemolizumab for both atopic dermatitis and prurigo nodularis illustrates consolidated indication reviews. Germany, France, and the UK spearhead biologic penetration, whereas Southern Europe leans on biosimilar discounts. Sustainability directives influence formulary choices, favoring agents with lower carbon-footprint packaging.

Asia-Pacific is the fastest-growing region at a 10.46% CAGR through 2030. China’s domestic innovators are floating IPOs on vitiligo candidates, a sign of rising scientific depth and capital availability. Japan’s timely endorsement of VTAMA cream indicates regulatory agility, while India’s dermatology roadmap stresses international research alliances and manufacturing self-reliance. Diverse climates and pollutant profiles across APAC spur demand for tailored regimens that address both UV exposure and particulate stress.

Competitive Landscape

Market structure is moderately fragmented, yet consolidation is quickening as firms seek end-to-end portfolios spanning multiple pathways and delivery modes. Organon’s USD 1.2 billion acquisition of Dermavant secured VTAMA, a nonsteroidal aryl hydrocarbon receptor modulator with multi-indication potential. Johnson & Johnson, facing biosimilar erosion of Stelara, is counter-balancing with Skyrizi extensions into Crohn’s disease. AbbVie remains aggressive, leveraging dual-asset synergies between Rinvoq and Skyrizi to chase multiple inflammatory indications.

AI-enabled diagnostics and e-pharmacies are lowering the prescription barrier, allowing agile biotech firms to sidestep traditional detailing and scale rapidly through digital channels. Manufacturing prowess in cold-chain handling becomes a competitive moat, as reliable 2–8 °C delivery is now pivotal for blockbuster injectables.

White-space areas such as epidermolysis bullosa demonstrate how orphan-drug routes can yield premium pricing: the January 2024 approval of birch-triterpene gel Filsuvez validated small-population economics. Extended half-life antibodies that promise twice-yearly dosing are set to redraw patient adherence curves, a feature incumbents must emulate or risk share erosion.

Prescription Dermatology Therapeutics Industry Leaders

AbbVie Inc.

Johnson & Johnson

Pfizer Inc.

Amgen Inc.

Eli Lilly & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: LEO Pharma acquired global rights to Spevigo for EUR 90 million upfront plus milestones, adding the first targeted therapy for generalized pustular psoriasis.

- June 2025: FDA approved Dupixent for adults with bullous pemphigoid.

- May 2025: FDA cleared ZORYVE topical foam 0.3% for scalp and body plaque psoriasis in patients ≥ 12 years.

Global Prescription Dermatology Therapeutics Market Report Scope

| Topical Corticosteroids |

| Retinoids |

| Calcineurin Inhibitors |

| Phosphodiesterase-4 (PDE4) Inhibitors |

| Biologics & Biosimilars |

| Janus Kinase (JAK) Inhibitors |

| Other Drug Classes |

| Psoriasis |

| Atopic Dermatitis |

| Acne Vulgaris |

| Rosacea |

| Alopecia (Alopecia Areata & Androgenetic) |

| Vitiligo |

| Other Dermatological Disorders |

| Topical |

| Oral |

| Injectable |

| Transdermal Patches |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| Compounding Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Topical Corticosteroids | |

| Retinoids | ||

| Calcineurin Inhibitors | ||

| Phosphodiesterase-4 (PDE4) Inhibitors | ||

| Biologics & Biosimilars | ||

| Janus Kinase (JAK) Inhibitors | ||

| Other Drug Classes | ||

| By Disease Indication | Psoriasis | |

| Atopic Dermatitis | ||

| Acne Vulgaris | ||

| Rosacea | ||

| Alopecia (Alopecia Areata & Androgenetic) | ||

| Vitiligo | ||

| Other Dermatological Disorders | ||

| By Route of Administration | Topical | |

| Oral | ||

| Injectable | ||

| Transdermal Patches | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| Compounding Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What will the prescription dermatology therapeutics market be worth in 2030?

The market is forecast to reach USD 67.54 billion, expanding at an 8.14% CAGR from 2025.

Which drug class is growing the fastest?

Janus kinase (JAK) inhibitors are projected to post the strongest growth at a 12.45% CAGR through 2030.

Which disease area is showing the highest growth momentum?

Alopecia therapies are expected to rise 11.56% annually, driven by recent JAK inhibitor approvals.

Why are online pharmacies gaining traction?

Seamless links between tele-dermatology consults and home delivery support a 12.89% CAGR for this channel.

What limits broader biologic adoption in dermatology?

High acquisition costs and strict cold-chain requirements continue to restrict access, especially in emerging markets.

Which region will expand the quickest?

Asia-Pacific is set to grow at a 10.46% CAGR, propelled by rising healthcare spending and improved treatment access.

Page last updated on: