Cytotoxic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

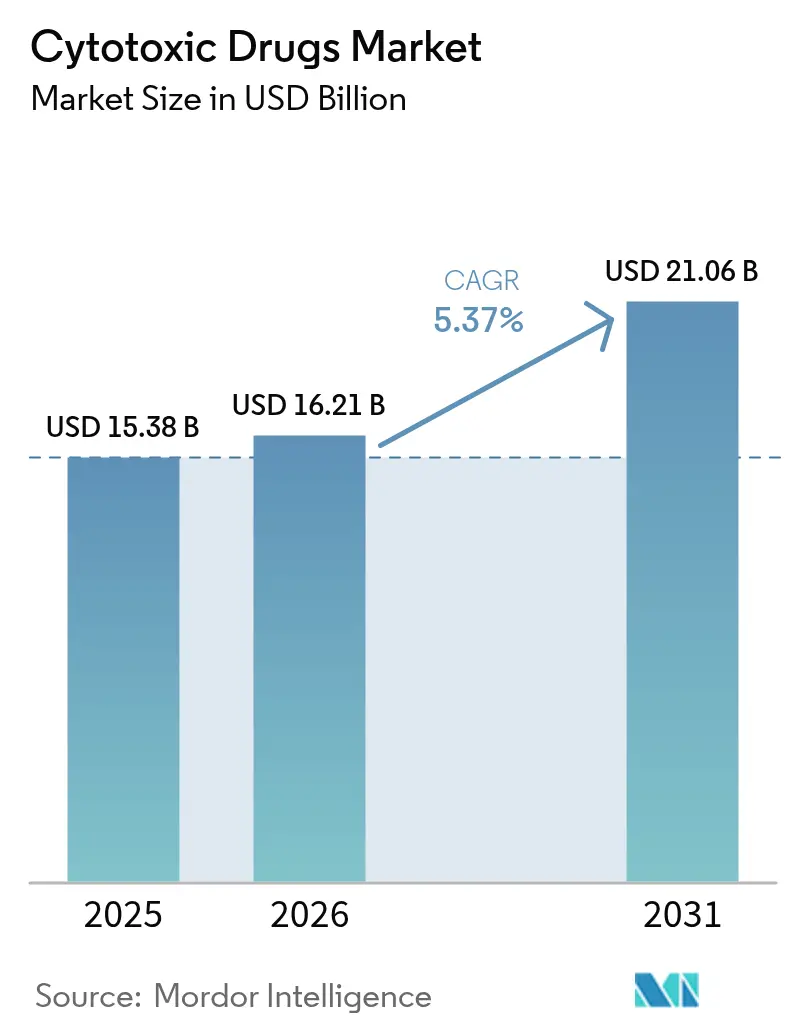

| Market Size (2026) | USD 16.21 Billion |

| Market Size (2031) | USD 21.06 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

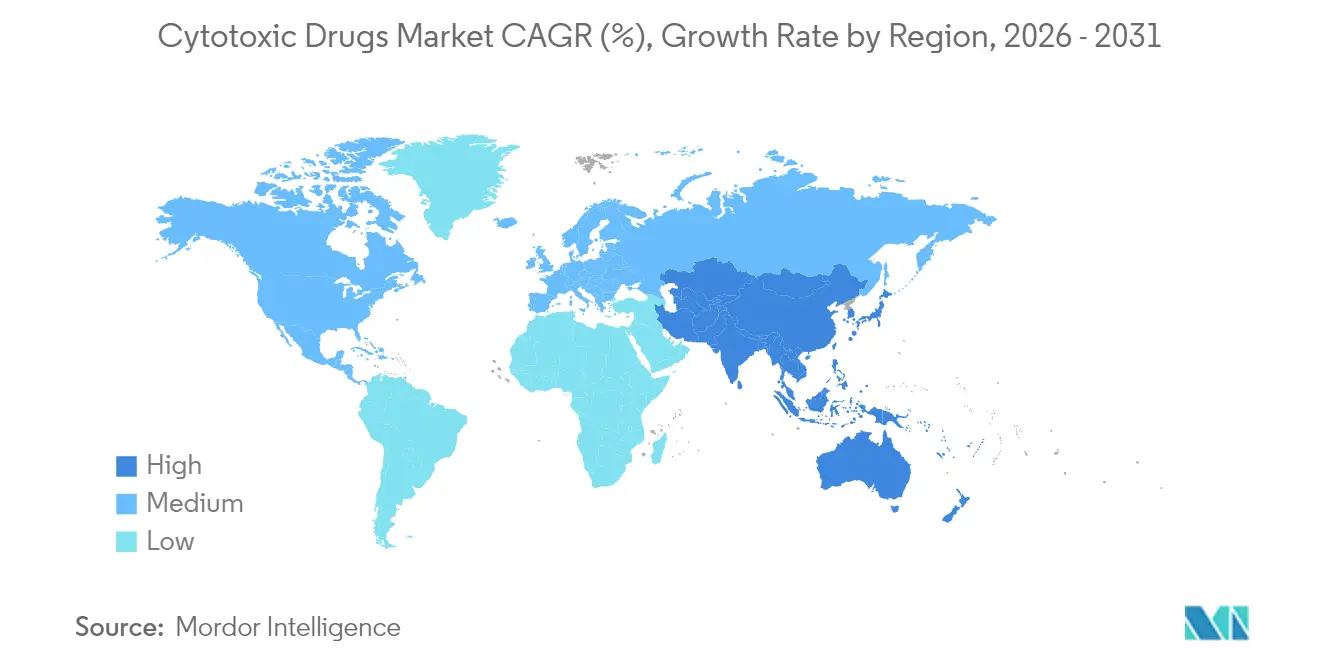

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cytotoxic Drugs Market Analysis by Mordor Intelligence

The cytotoxic drugs market size in 2026 is estimated at USD 16.21 billion, growing from 2025 value of USD 15.38 billion with 2031 projections showing USD 21.06 billion, growing at 5.37% CAGR over 2026-2031. Rising cancer diagnoses, sustained clinical reliance on chemotherapy backbones, and swift regulatory approvals underpin this steady outlook. Adoption accelerates where next-generation delivery platforms improve therapeutic indices, while expanded reimbursement frameworks in high-income countries lower financial barriers for combination regimens. Oral formulations, improved sustained-release injectables, and antibody-drug conjugates (ADCs) illustrate how established cytotoxic mechanisms adapt to precision-medicine paradigms. Simultaneously, manufacturing investments in Asia-Pacific elevate supply resilience and trim costs, positioning the region as the growth engine of the cytotoxic drugs market. Environmental compliance and adherence limitations continue to temper growth, yet pipeline momentum and broader geographic access outweigh these constraints.

Key Report Takeaways

- By route of administration, parenteral products retained 68.87% of cytotoxic drugs market share in 2025, whereas oral formulations record a 8.79% CAGR to 2031.

- By drug type, alkylating agents led with 30.10% revenue share in 2025; antimetabolites expand at a 7.02% CAGR through 2031.

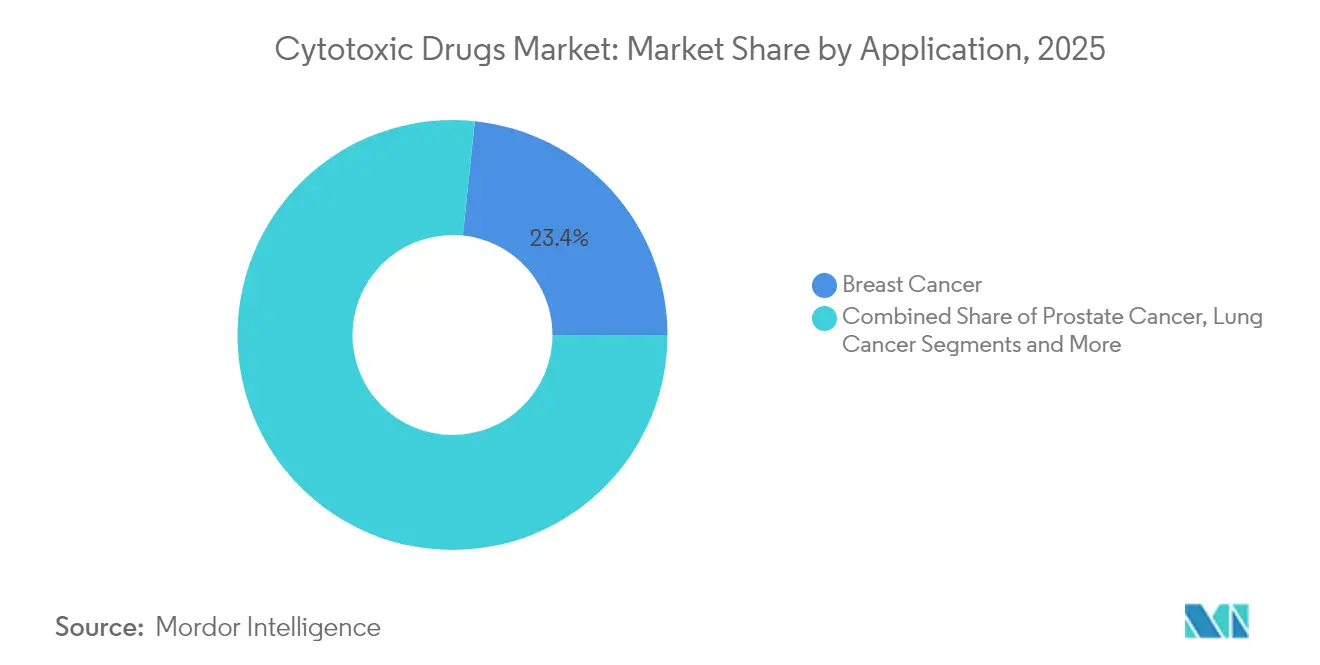

- By application, breast cancer commanded 23.35% of the cytotoxic drugs market size in 2025, while pancreatic cancer treatments rise at an 7.78% CAGR to 2031.

- By geography, North America held 42.15% share of the cytotoxic drugs market in 2025, yet Asia-Pacific grows the fastest at 10.07% CAGR to 2031.

- By distribution channel, retail pharmacies led with 40.65% share in 2025, whereas online pharmacies post a 9.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cytotoxic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cancer incidence & earlier diagnosis | +1.2% | Global with emphasis on APAC and North America | Medium term (2-4 years) |

| Expanding reimbursement for chemotherapy regimens | +0.8% | North America and EU extending into select APAC markets | Short term (≤ 2 years) |

| Pipeline approvals of next-gen cytotoxic formulations | +0.9% | Global led by US FDA and China NMPA approvals | Medium term (2-4 years) |

| Surging demand across low- and middle-income countries | +1.1% | APAC core, Latin America, MEA | Long term (≥ 4 years) |

| AI-driven drug-repurposing accelerating cytotoxic combos | +0.6% | North America and EU research hubs | Long term (≥ 4 years) |

| ADC payload demand for cytotoxics | +0.7% | Global, concentrated in major pharmaceutical markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cancer Incidence & Earlier Diagnosis

The number of newly diagnosed cancer cases crossed 2.04 million in the United States for the first time in 2025, reinforcing a large treatment pool for cytotoxic agents[1]American Cancer Society, “Cancer Facts & Figures 2025,” cancer.org. Improved imaging, AI-enabled screening, and aging demographics bring malignancies to clinical attention at stages where cytotoxics remain standard of care. Emerging nations roll out population-wide screening that uncovers earlier-stage tumors and unlocks demand for cost-effective chemotherapy. These factors collectively raise treatment volumes and extend therapy durations, strengthening baseline growth for the cytotoxic drugs market.

Expanding Reimbursement For Chemotherapy Regimens

Medicare’s 2025 introduction of a USD 2,000 annual cap on patient out-of-pocket drug costs slashes financial barriers for multi-agent chemotherapy. Private insurers increasingly mirror this ceiling, smoothing access to high-dose and combination protocols that previously strained household budgets. Similar reforms appear in China, where the national medical insurance list now includes recently approved cytotoxics, while European payers sustain comprehensive oncology packages. The resulting reimbursement expansion translates into higher treatment adherence, broader use of supportive care drugs, and faster uptake of newly launched cytotoxics.

Pipeline Approvals Of Next-Gen Cytotoxic Formulations

Regulators accelerated clearances for optimized cytotoxic regimens in 2024–2025; the FDA sanctioned treosulfan with fludarabine for allogeneic stem-cell conditioning, demonstrating survival benefits over busulfan. China’s NMPA approved more than 80 antineoplastic chemical entities during 2024 alone[2]Nature, “Approvals by the China NMPA in 2024,” nature.com. These decisions underscore confidence in reformulated payloads that integrate sustained-release technologies, oral bioavailability gains, or antibody targeting. Each approval enlarges the addressable market while signaling continued relevance of cytotoxic modes of action in precision-therapy settings.

Surging Demand Across Low- And Middle-Income Countries

Over 75% of projected cancer deaths will occur in low- and middle-income countries (LMICs) within a decade. Health ministries and global partnerships direct resources toward affordable chemotherapy, often via locally manufactured generics that cut import costs. India’s NexCAR19 development illustrates domestic innovation that reduces advanced therapy cost burdens by more than 90% compared with Western CAR-T analogues. As oncology infrastructure matures, volume growth from LMICs offsets price pressure and supports continued expansion of the cytotoxic drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe adverse-effect profile limits dosage adherence | −0.9% | Global with greater impact in aging populations | Short term (≤ 2 years) |

| High cost of HPAPI containment & compliance | −0.7% | North America and EU manufacturing hubs | Medium term (2-4 years) |

| Shift of R&D budgets toward targeted & immuno-oncology drugs | −1.1% | Global pharmaceutical R&D centers | Long term (≥ 4 years) |

| Environmental regulations on cytotoxic effluent disposal | −0.5% | Developed markets with stringent oversight | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Adverse-Effect Profile Limits Dosage Adherence

Toxicity-driven discontinuation persists, with dropout rates ranging from 27% to 53% in colorectal cancer treatments. Shortages of cornerstone agents such as cisplatin in 2023 amplified reliance on alternative drugs and spotlighted the narrow therapeutic margins of many chemotherapies. Although supportive care and pharmacist-led adherence programs mitigate some challenges, the core toxicity profile constrains broader application and affects real-world outcomes.

Shift Of R&D Budgets Toward Targeted & Immuno-Oncology Drugs

Capital flows increasingly favor immunotherapies and precision modalities, diverting funds from traditional cytotoxic discovery. High-potency API containment demands and environmental obligations under EPA and EMA rules elevate cost structures[3]Environmental Protection Agency, “Settlement with Stericycle for Hazardous Waste Violations,” epa.gov. This mix of budgetary preference and compliance expense narrows the pool of new cytotoxic entrants, even as reformulated legacy agents secure approvals. While ADCs realign attention to cytotoxic payloads, standalone chemotherapy innovation faces competitive pressure in investor portfolios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Oral Formulations Challenge Injectable Dominance

Parenteral drugs dominated with 68.87% market share in 2025, anchored by clinician confidence in controlled dosing for acute and combination regimens. Oral cytotoxics, however, record the segment’s quickest expansion at 8.79% CAGR through 2031 as patient-centric care models pivot toward home administration. The cytotoxic drugs market size for oral treatments is projected to outgrow hospital-exclusive volumes when improved bioavailability formulations reach widespread reimbursement. Advances such as sustained-release tablets reduce peak plasma toxicity while maintaining efficacy, driving oncologists to integrate oral options into long-term combination plans.

Convenience bolsters adherence when pharmacists monitor dosing schedules through telehealth platforms that flag missed pills and manage side effects. Injectables remain critical in induction and salvage protocols where rapid cytoreduction is essential, yet broader patient acceptance of tablets and capsules shifts revenue momentum toward oral formats. As e-prescription ecosystems mature, online pharmacy distribution further accelerates uptake of at-home regimens, creating fresh competitive angles for formulation innovators.

By Drug Type: Antimetabolites Accelerate Despite Alkylating Leadership

Alkylating agents commanded 30.10% share in 2025 owing to their broad mechanistic reach and longstanding physician familiarity. The cytotoxic drugs market share attributed to this class underscores its entrenched role in foundation regimens for hematologic and solid tumors. Antimetabolites, featuring refined toxicity and combination potential, outpace all other types at a 7.02% CAGR. AI-enabled drug repurposing identifies synergistic antimetabolite partners that enhance outcomes in resistant cancers.

Development pipelines increasingly leverage ADCs that carry topoisomerase inhibitors and plant alkaloid derivatives into antigen-expressing tumors, breathing new commercial life into underutilized payloads. FDA endorsement of treosulfan demonstrates regulators’ confidence in optimized alkylators even as antimetabolites seize growth momentum. The interplay of incremental innovation and novel conjugation strategies reshapes competitive dynamics across the drug-type spectrum.

By Application: Pancreatic Cancer Momentum Outstrips Breast Cancer Scale

Breast cancer interventions led revenue with 23.35% slice of 2025 demand, reflecting large patient volumes and embedded use of combination chemotherapy alongside targeted agents. Pancreatic cancer indications, while smaller in absolute terms, exhibit an 7.78% CAGR as machine-learning screens generate 300-plus validated synergistic drug pairs that overcome historical resistance. The cytotoxic drugs market size for pancreatic therapy is thus on course for the segment’s highest proportional increase through 2031.

Lung, colorectal, and prostate cancers stay central to revenue diversification as emerging ADCs combine veterinary proven payloads with precision antibodies that lower systemic toxicity. Regulatory nods for agents like datopotamab deruxtecan in HR-positive breast cancer reaffirm the commercial case for payload innovation that reinvigorates cytotoxic classes. Multimodal regimens integrating radioligands and checkpoint inhibitors further widen demand footprints across tumor types.

By Distribution Channel: Digital Platforms Redefine Access

Retail pharmacies captured 40.65% of 2025 revenue owing to in-person counseling and established reimbursement billing. Online channels, however, post the fastest 9.11% CAGR as telehealth normalizes drug delivery straight to patient homes. The cytotoxic drugs market size driven by e-pharmacy orders is expanding when Medicare’s out-of-pocket caps prompt comparison shopping across digital portals that also support adherence tracking. Hospital pharmacies keep a pivotal role in intensive regimens and investigational therapy dispensing yet collaborate with specialty providers that manage complex cold-chain and hazardous-drug logistics.

Centralized compounding hubs tied to large online franchises reduce wastage and elevate safety compliance under USP-800, appealing to payers and providers looking to curtail handling costs. As blockchain-enabled track-and-trace proves supply authenticity, digital channels will progressively standardize across oncology practices.

Geography Analysis

North America led revenue with 42.15% share in 2025, propelled by comprehensive insurance coverage and robust clinical trial activity. Medicare’s cost-sharing cap beginning in 2025 widens the addressable patient base for multi-agent cycles and supports higher therapy adherence. Venture investment and favorable orphan-drug incentives keep the United States at the forefront of ADC and oral formulation breakthroughs. Canada adds analytical depth through machine-learning incidence forecasts that allow provincial health authorities to budget accurately for chemotherapy inventories.

Asia-Pacific registers a vigorous 10.07% CAGR and now anchors global manufacturing scaleouts that lower finished-dose costs. China’s NMPA clearance of 228 drugs in 2024, with 37% classified as antineoplastics, signals regulatory momentum supporting domestic innovators. India’s localization drive exemplified by NexCAR19 and large API parks, Japan’s conditional nods for isatuximab in multiple myeloma, and Korea’s bioconjugate trials collectively form a vibrant ecosystem that accelerates both clinical adoption and export potential.

Europe maintains balanced progress through harmonized EMA procedures that give companies a single pathway to 27 markets. The agency’s approval of Roche’s Alecensa as adjuvant therapy highlights precision oncology leadership in integrating cytotoxic payloads into early disease settings. Contract development giants such as Lonza expand Swiss conjugation suites to serve escalating ADC demand. Public healthcare frameworks secure broad patient access yet heighten price scrutiny, pressing suppliers to justify incremental benefits.

Middle East and Africa plus South America are smaller in absolute terms yet register double-digit upticks where multilateral health initiatives lift chemotherapy availability. Infrastructure projects, such as oncology centers co-funded by Gulf sovereign wealth funds, facilitate region-specific supply networks. The Access to Oncology Medicines Coalition channels technical assistance and pooled procurement tools that shorten supply timelines, solidifying emerging-market contributions to the cytotoxic drugs market.

Competitive Landscape

Industry concentration is moderate. Pfizer’s USD 43 billion purchase of Seagen advances its ADC portfolio and affirms the rationale for marrying legacy cytotoxic compounds with antibody precision. ONO Pharmaceutical’s USD 2.4 billion agreement for Deciphera shows mid-cap players seeking pipeline diversity through bolt-on deals in specialized cytotoxic niches. Contract manufacturers expand high-potency suites as demand surges for commercial-scale conjugations.

Product strategy centers on payload innovation, oral reformulation, and digital patient-support ecosystems that mitigate toxicity and reinforce adherence. Biocon’s bevacizumab biosimilar approval and Novartis’ radioligand expansions illustrate how adjacent technology families enter combination protocols that include cytotoxic backbones. Disruptors leverage AI to map drug-interaction networks, guiding co-formulation decisions that lengthen product life cycles while differentiating safety profiles.

Regional manufacturers in China and India scale cost-effective generics, raising competitive thresholds for pricing in LMICs and pushing multinationals toward premium, targeted-delivery spaces. Strategic collaborations, such as Sanofi’s radioligand venture with Orano, highlight cross-disciplinary synergies that can complement cytotoxic assets. As large portfolios tilt to mixed-modality regimens, suppliers that bundle cytotoxic, targeted, and immunologic assets gain holistic contracting leverage with payers and providers.

Cytotoxic Drugs Industry Leaders

Roche Holding AG

Novartis AG

Pfizer Inc.

Johnson & Johnson

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Deciphera Pharmaceuticals received full FDA approval for ROMVIMZA (vimseltinib) in symptomatic tenosynovial giant cell tumor, showing superior objective response versus placebo.

- January 2025: FDA approved treosulfan (Grafapex) with fludarabine for conditioning in allogeneic HSCT patients with AML or MDS, citing improved survival metrics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cytotoxic drugs market as all prescription, small-molecule chemotherapeutic agents, branded or generic, delivered orally or parenterally to destroy malignant cells by interrupting DNA replication or mitosis. According to Mordor Intelligence, sales tracked span hospital, retail, and online channels across North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

We exclude antibody-drug conjugates, targeted kinase inhibitors, veterinary preparations, and pipeline molecules lacking regulatory approval.

Segmentation Overview

- By Route of Administration

- Parenteral

- Oral

- By Drug Type

- Alkylating Agents

- Antitumor Antibiotics

- Antimetabolites

- Plant Alkaloids

- Topoisomerase Inhibitors

- Others

- By Application

- Breast Cancer

- Prostate Cancer

- Lung Cancer

- Pancreatic Cancer

- Colorectal Cancer

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Pharmacies

- Other Distribution Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with oncologists, hospital pharmacists, and regional distributors in the United States, Germany, India, Brazil, and the Gulf. Insights on dose intensity, tender discounts, and patient co-pays helped us refine uptake curves and validate secondary findings.

Desk Research

We began by mining Tier-1 public datasets such as WHO GLOBOCAN incidence tables, UN Comtrade trade codes for antineoplastics, FDA and EMA approval archives, and health-ministry expenditure series; these sources fixed epidemiological baselines and price corridors. Our team next reviewed company 10-Ks, investor decks, and reputable press, then cross-checked financials through D&B Hoovers and news flow through Dow Jones Factiva to gauge branded-to-generic switch timing and average selling price erosion. The sources cited are illustrative; many additional public records were consulted.

Market-Sizing & Forecasting

Our model applies a top-down prevalence-to-treated-patient build, using variables such as new cancer cases, treatment penetration, average cycles per patient, branded versus generic mix, regulatory approval pipeline, and regional reimbursement ceilings. Select bottom-up supplier roll-ups for key agents like paclitaxel and capecitabine act as sense checks. Forecasts to 2030 employ multivariate regression complemented by scenario analysis around biosimilar launch dates; gaps in distributor data are bridged with historical substitution ratios.

Data Validation & Update Cycle

We compare outputs with pharmacy audits, import shipments, and oncology budget statements; variances above five percent trigger re-work. Reports refresh annually, with interim updates after major approvals or price caps, and a final analyst review before release.

Why Mordor's Cytotoxic Drugs Baseline Earns Stakeholder Trust

Published estimates often diverge because firms vary scope, price-erosion curves, and refresh cadence, a reality we address upfront.

Key gaps arise when other publishers bundle targeted biologics with classical chemo, freeze list prices across regions, or miss rapid generic entry; Mordor Intelligence separates therapy classes, applies region-specific blended ASPs, and revisits models each year, giving decision-makers a figure they can lean on.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.38 B (2025) | Mordor Intelligence | - |

| USD 14.8 B (2023) | Global Consultancy A | Branded sales only, limited geography mix |

| USD 16.2 B (2023) | Industry Association B | Combines biologics with cytotoxics, uses list prices |

| USD 17.16 B (2024) | Trade Journal C | Static incidence growth, three-year update cycle |

We believe that, once definitions, price assumptions, and update frequency are aligned, our balanced figure sits near the midpoint, offering a transparent baseline that users can replicate and defend with confidence.

Key Questions Answered in the Report

What is the current value of the cytotoxic drugs market?

The market is valued at USD 16.21 billion in 2026 and is forecast to reach USD 21.06 billion by 2031.

Which region is growing the fastest in the cytotoxic drugs market?

Asia-Pacific records the highest CAGR at 10.07% through 2031, driven by regulatory modernization and manufacturing investments.

Which drug type shows the quickest growth?

Antimetabolites expand at a 7.02% CAGR, outpacing other classes as formulation upgrades boost therapeutic indices.

How are reimbursement changes affecting market demand?

A USD 2,000 Medicare out-of-pocket cap introduced in 2025 lowers financial hurdles, increasing patient access to multi-agent chemotherapy.

Why are oral cytotoxic formulations gaining traction?

Patients favor home dosing, while sustained-release technologies and digital adherence tools improve efficacy and convenience, resulting in a 8.79% CAGR for oral products.

Page last updated on: