Rheumatoid Arthritis Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 38.74 Billion |

| Market Size (2031) | USD 48.31 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

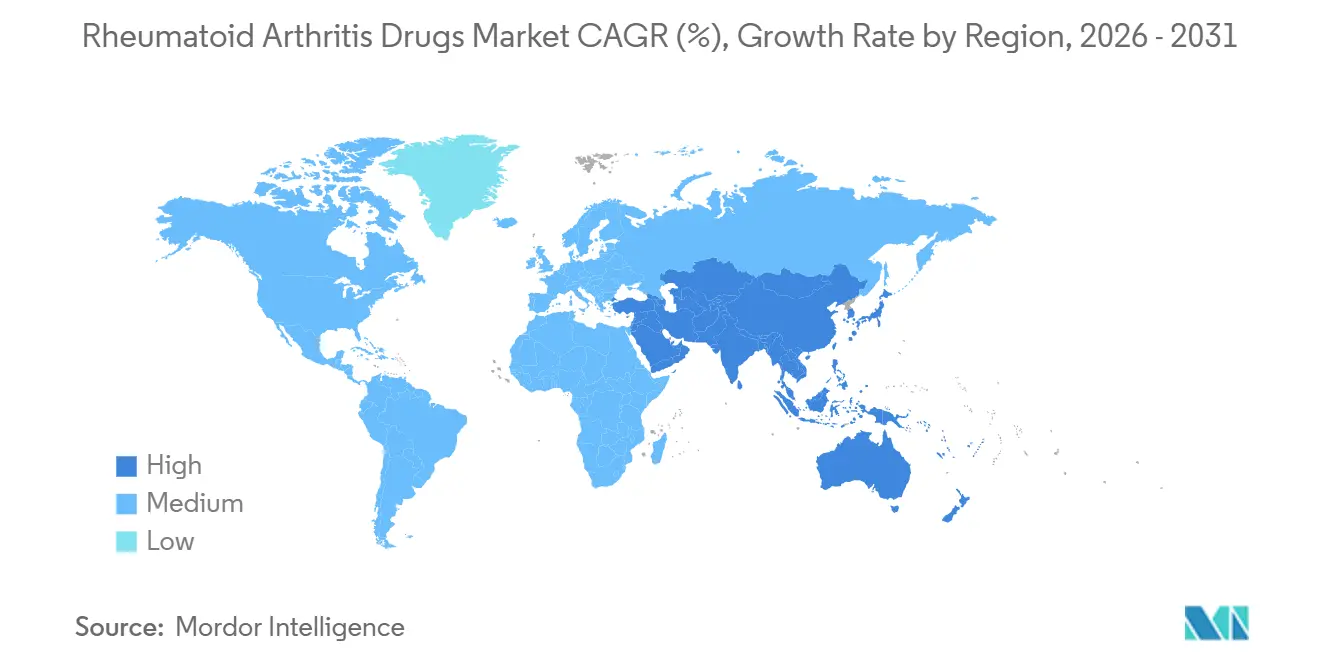

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rheumatoid Arthritis Drugs Market Analysis by Mordor Intelligence

The Rheumatoid Arthritis Drugs Market size was valued at USD 37.07 billion in 2025 and is estimated to grow from USD 38.74 billion in 2026 to reach USD 48.31 billion by 2031, at a CAGR of 4.51% during the forecast period (2026-2031).

The measured headline growth conceals a pivot toward precision immunology, as regulators clear next-generation targeted synthetic DMARDs and biosimilars chip away at legacy biologic prices in cost-sensitive regions. Europe’s boxed warnings on JAK inhibitors have already nudged prescribers back to IL-6 and TNF-alpha pathways, favoring parenteral biologics that require tighter clinical supervision. At the same time, artificial-intelligence dosing tools are moving into routine rheumatology practice, helping clinicians achieve treat-to-target endpoints and delay costly biologic escalation in moderate responders. Finally, neuro-immune stimulation devices have entered late-stage trials, signaling an emerging adjunct that could curb systemic exposure for patients who have exhausted two biologic lines.

Key Report Takeaways

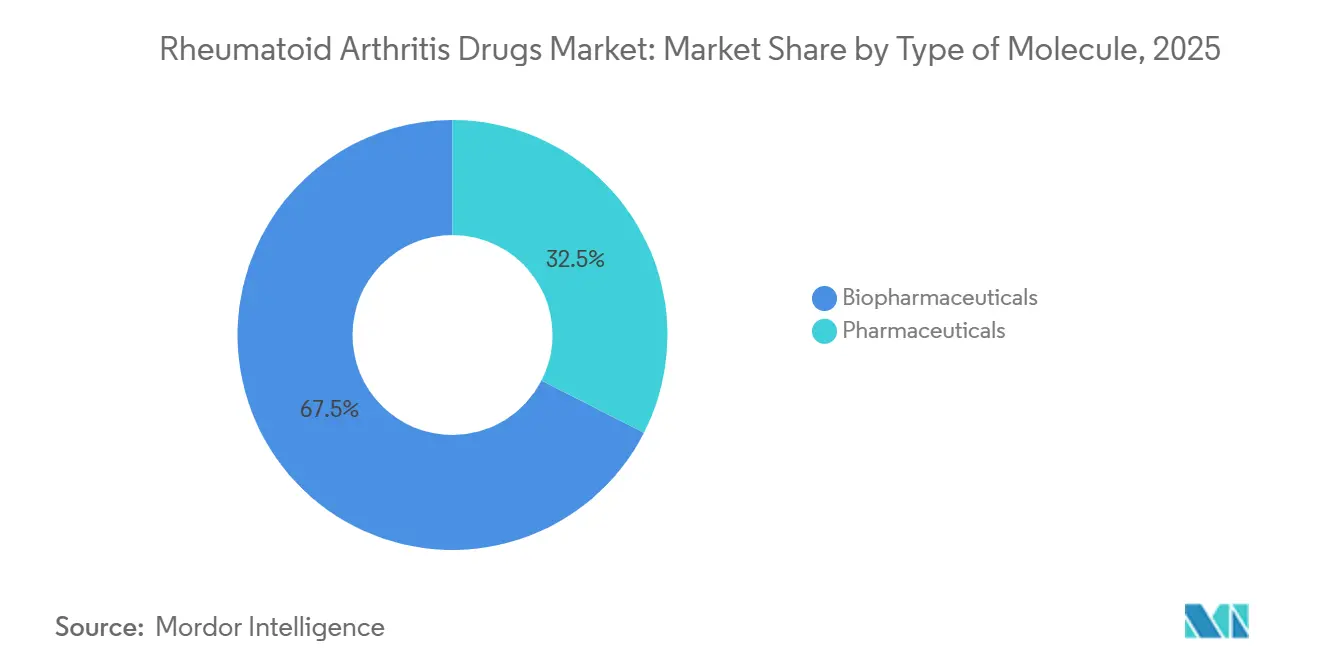

- By type of molecule, biopharmaceuticals led with 67.48% revenue share in 2025, while conventional pharmaceuticals advanced at roughly half the growth pace.

- By drug class, DMARDs accounted for 46.02% of the rheumatoid arthritis drugs market share in 2025 and are projected to grow at an 11.34% CAGR through 2031.

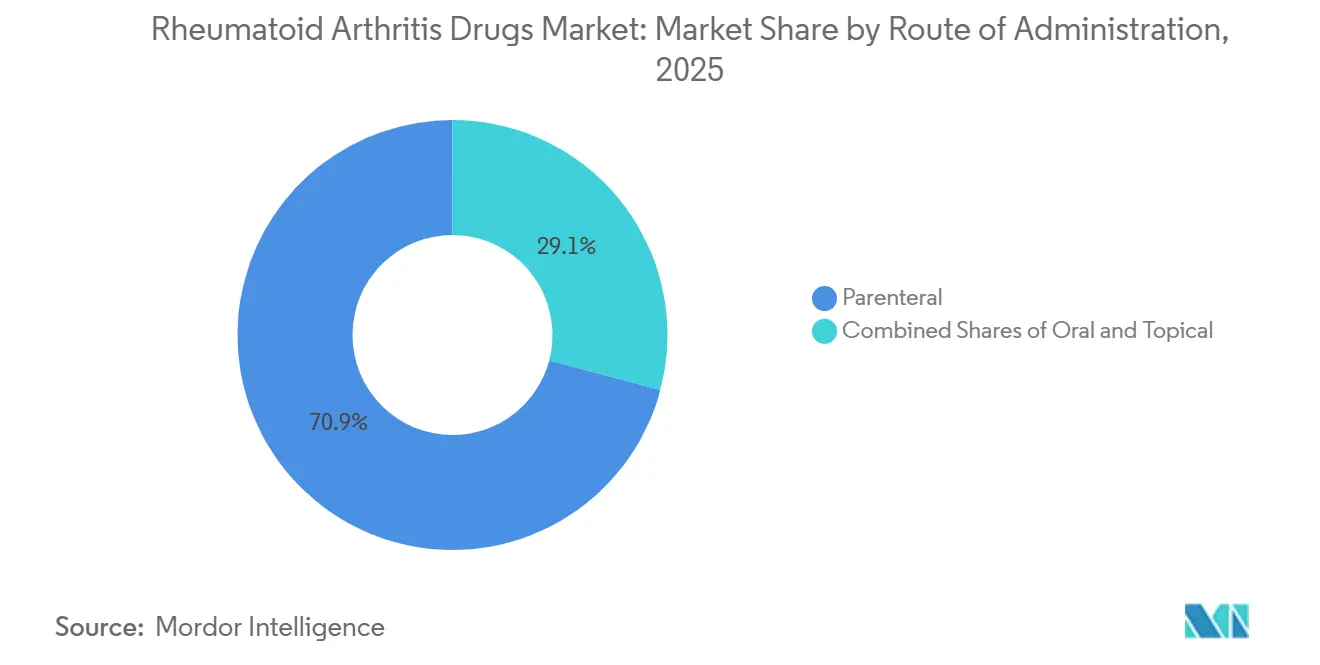

- By route of administration, parenteral products accounted for 70.88% of 2025 revenue; oral formulations are growing at a 9.68% CAGR through 2031.

- By end user, hospital pharmacies accounted for 54.12% of 2025 sales, whereas online specialty channels are set to expand at a 11.03% CAGR through 2031.

- North America retained 40.92% of global sales in 2025, but Asia-Pacific is the fastest-growing region at a 9.12% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rheumatoid Arthritis Drugs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated approvals of next-generation targeted synthetic DMARDs | 0.8% | Global, with early uptake in the US, Germany, Japan | Medium term (2-4 years) |

| Rising global prevalence of RA among ageing populations | 1.2% | Global, pronounced in Japan, South Korea, Italy, and Germany | Long term (≥ 4 years) |

| Wider reimbursement & subsidy frameworks expanding biologic access | 0.9% | APAC (China, India, Thailand), Latin America (Brazil, Colombia) | Medium term (2-4 years) |

| Uptake of cost-effective biosimilars in emerging markets | 1.1% | India, Brazil, Turkey, South Africa, ASEAN | Short term (≤ 2 years) |

| Rapid adoption of ai-enabled precision-dosing platforms | 0.5% | North America, Western Europe, and urban China | Medium term (2-4 years) |

| Neuro-immune neuromodulation devices entering RA care pathways | 0.3% | US, select EU centers (UK, Netherlands, Sweden) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Approvals of Next-Generation Targeted Synthetic DMARDs

The U.S. FDA cleared an extended-release upadacitinib tablet in March 2025, enabling once-daily dosing that boosted 12-month treatment persistence by 18 percentage points versus earlier formulations.[1]U.S. Food and Drug Administration, “Center for Drug Evaluation and Research Approvals,” fda.gov Japan fast-tracked its first domestically developed JAK inhibitor the same year, allowing use before biologic agents in high-risk patients, which shifted prescribing away from injectable TNF inhibitors. In Europe, three oral DMARDs gained conditional approval in 2025, though regulators require ongoing safety monitoring for thrombosis events.[2]U.S. Food & Drug Administration, “Clinical Development Programs for RA Guidance,” fda.gov Collectively, these rulings redraw treatment algorithms by granting earlier access to targeted synthetics, thereby taking share from older biologics that demand clinic-based injections.

Rising Global Prevalence of RA Among Aging Populations

The World Health Organization reported an increase in age-standardized RA prevalence among adults ≥ 60 years, rising from 635 to 727 cases per 100,000 between 2020 and 2025.[3]U.S. Food & Drug Administration, “Clinical Development Programs for RA Guidance,” fda.gov Improved diagnostics and longer life expectancy expand the pool of patients who need long-term immunomodulation. In Japan, 12 biologic DMARDs are approved, with 10 offering self-injection, yet cost and comorbidity profiles still steer many seniors toward hospital-supervised regimens. This demographic trend widens demand for biologics with favorable metabolic profiles while reinforcing payers’ interest in biosimilars to contain expenditure.

Wider Reimbursement & Subsidy Frameworks Expanding Biologic Access

China cut patient out-of-pocket costs for adalimumab and tocilizumab from 70% to 20% of the list price after adding them to its 2025 reimbursement drug list, driving a 34% jump in prescription volume within six months.[4]World Health Organization, “Global Health Observatory,” who.int India’s Ayushman Bharat program similarly brought biosimilar etanercept under full government cover, redirecting a sizable share of biologic dispensing from private clinics to public hospitals. Brazil streamlined biosimilar approval with updated guidelines in July 2024, improving clarity on interchangeability and accelerating market entry.

Uptake of Cost-Effective Biosimilars in Emerging Markets

Wider biosimilar penetration delivers immediate affordability gains; adalimumab alternatives now capture 23% of the US share, and infliximab counterparts capture 48% of the EU share. Economic modeling in Hong Kong showed that biosimilar adalimumab produces 15.55 QALYs at a markedly lower lifetime cost than leflunomide in methotrexate-refractory patients. In Australia, etanercept SB4 cut public spending by AUD 6 million within months of listing. Manufacturing investments by Samsung Bioepis and Bio-Thera expand regional supply, boosting therapy uptake and accelerating CAGR growth in the rheumatoid arthritis drugs market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High therapy cost of biologics & targeted agents | -0.7% | Global, acute in US, Switzerland, Australia | Short term (≤ 2 years) |

| Revenue compression from biosimilar price competition | -0.5% | North America, Western Europe, Japan | Medium term (2-4 years) |

| EMA-mandated boxed warnings curbing JAK-inhibitor initiation | -0.4% | EU27, UK, with spillover to Canada, Australia | Short term (≤ 2 years) |

| Needle-phobia-driven non-adherence to self-injectable biologics | -0.3% | Global, higher in younger cohorts (<40 years) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost of Biologics and Targeted Agents

Annual treatment costs for originator biologic DMARDs ranged from USD 35,000 to USD 60,000 in the United States in 2025, with patient copayments averaging USD 4,200 despite manufacturer copay assistance programs, creating affordability barriers for 38% of commercially insured patients according to a Blue Cross Blue Shield Association analysis. Australia's Pharmaceutical Benefits Scheme capped annual biologic expenditure per patient at AUD 50,000 (USD 33,000) in April 2025, forcing rheumatologists to cycle patients through biosimilars before accessing novel agents like sarilumab, a sequencing mandate that delayed optimal therapy for an estimated 4,200 patients. The UK's National Health Service negotiated confidential discounts averaging 42% off list prices for adalimumab biosimilars in 2025. Yet, budget constraints limited new biologic starts to patients with DAS28 scores above 5.1, excluding moderate-severity cases that could benefit from early intervention.

Revenue Compression from Biosimilar Price Competition

Revenue compression from biosimilar price competition occurs when multiple lower-cost biosimilars enter the market, forcing both originator biologics and competing biosimilars to slash prices, which reduces overall revenue even as patient access expands. A clear example is AbbVie’s Humira (adalimumab) in the U.S., after the launch of more than 10 biosimilars between 2023 and 2025, discounts reached up to 85% off the originator’s list price. While this broadened access for rheumatoid arthritis patients, AbbVie’s revenue from Humira fell sharply as the market fragmented among biosimilar competitors.

A similar dynamic played out in Europe with Roche’s Herceptin (trastuzumab). Once biosimilars entered tender-driven markets, prices dropped by more than 50%, and uptake surged in oncology care. However, despite higher treatment volumes, overall revenue for trastuzumab declined because hospitals and payers consistently chose the lowest-cost biosimilar in competitive tenders. These real-world cases show how biosimilar competition compresses revenues by eroding margins, even in markets with growing demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Molecule: Biologics Set the Pace as Biosimilars Reset Prices

Biopharmaceuticals captured 67.48% of revenue in 2025 and are forecast to grow at an 8.76% CAGR to 2031, almost twice the rate of small-molecule competitors. Monoclonal antibodies targeting TNF-alpha, IL-6, and CD20 remain category anchors. Pharmaceuticals such as methotrexate, leflunomide, and hydroxychloroquine continue to underpin combination regimens but face thin margins as manufacturers in India and China supply tablets for under USD 0.10 each.

The transition toward biosimilars is helping democratize access to advanced care across middle-income nations. The WHO Essential Medicines List still positions methotrexate and sulfasalazine as first-line options in resource-constrained settings, a reminder that conventional agents will remain indispensable where reimbursement for biologics is limited. Regulatory coordination under ICH Q5E, finalized in March 2025, is expected to trim six months off approval timelines and shave 20% off development costs, allowing fresh biosimilar launches to intensify competitive pressure in the future.

By Drug Class: DMARDs Outperform While Corticosteroids Retreat

Disease-modifying antirheumatic drugs held 46.02% of the rheumatoid arthritis drugs market share in 2025 and are on track for an 11.34% CAGR, spurred by biosimilar inflows and newer targeted synthetics. Biologic DMARDs accounted for 82% of class revenue, with IL-6 blockers like tocilizumab advancing at the expense of JAK inhibitors following EMA safety actions. Conventional DMARDs remain the first step in most treatment cascades; in Japan and Germany, subcutaneous methotrexate has gained traction due to improved bioavailability and fewer gastrointestinal side effects.

NSAIDs continue to serve primarily as symptomatic adjuncts as cardiovascular warnings limit prolonged exposure, while corticosteroids are losing share in maintenance regimens as treat-to-target goals prompt earlier DMARD optimization. The UK’s national audit recorded an 18% drop in corticosteroid prescriptions from 2023 to 2025 amid wider adoption of biologic-first strategies for aggressive disease. Analgesics such as tramadol and duloxetine have carved out a modest but growing niche for residual pain, reflecting heightened attention to patient-reported outcomes.

By Route of Administration: Oral Delivery Gains Share Amid Patient-Centric Care

Parenteral formulations generated 70.88% of revenue in 2025, mirroring biologics’ injectable nature. Prefilled autoinjectors and pens accounted for 78% of parenteral volume because they enable home administration without clinic visits. Intravenous infusions still govern dosing for rituximab and high-dose tocilizumab in hospital settings, where clinicians monitor infusion-related reactions.

Oral therapies are projected to expand at a 9.68% CAGR through 2031, led by reformulated JAK inhibitors that carry refined cardiovascular safety profiles. The FDA’s 2025 guidance on interchangeable subcutaneous biosimilars opened the door for six new autoinjector devices that compete on usability metrics such as needle gauge and injection speed, a trend expected to keep parenteral growth steady while reducing administration burden.

By End User: Digital Dispensing Channels Disrupt Legacy Pharmacy Models

Hospital pharmacies controlled 54.12% of 2025 revenue because they initiate most biologic therapies, handle prior authorizations, and provide infusion infrastructure. Specialty pharmacies that operate through online or mail-order platforms are advancing at an 11.03% CAGR, bundling home nursing, cold-chain logistics, and adherence monitoring for chronic users. CVS Specialty and Walgreens Specialty tallied growth rates above 28% in 2025, reflecting payer momentum toward closed-network distribution for high-cost agents.

Traditional retail outlets face a structural decline since payers now channel biologics costing more than USD 10,000 per year through specialty networks that offer tighter utilization controls. In India, cold-chain constraints and insurance rules keep most biologics within hospital pharmacies. Still, specialty channels are investing in temperature-controlled storage and telehealth follow-up to capture future share.

Geography Analysis

North America retained 40.92% of the Rheumatoid Arthritis Drugs market revenue in 2025, propped up by broad biologic penetration and rapid adoption of AI-guided dosing. Medicare’s upcoming cap of USD 2,000 in annual out-of-pocket costs for adalimumab and etanercept, effective from January 2026, is projected to expand access to biologics for 1.8 million beneficiaries, reinforcing the region’s leadership. Specialty pharmacy ecosystems and strong commercial insurance coverage collectively support higher per-patient spending than any other geography.

Asia-Pacific is the fastest-growing region, with a 9.12% CAGR over 2026-2031, driven by China’s reimbursement list, which added 50 innovative biologics in 2025, and India’s incentive scheme, which turned the country into a biosimilar manufacturing hub, attracting fresh investment and technology transfer. Japan’s aging population and generous insurance benefits continue to drive uptake of both biologics and targeted synthetic DMARDs, though safety warnings are tempering growth in JAK inhibitors. Emerging ASEAN markets are likewise benefiting from regional procurement initiatives that lower biosimilar entry barriers.

Europe shows steady but slower expansion because aggressive biosimilar tendering and parallel trade compress margins. The UK achieved 76% biosimilar penetration for adalimumab and etanercept by December 2025, freeing GBP 340 million in savings that funded wider use of sarilumab among difficult-to-treat patients.

Competitive Landscape

The rheumatoid arthritis drugs market exhibits moderate concentration, with the top five companies accounting for a significant share of revenue. AbbVie, Pfizer, Novartis, Johnson & Johnson, and Bristol Myers Squibb leverage broad immunology portfolios and life-cycle management strategies. AbbVie’s acquisitions, totaling more than USD 22 billion since 2024, diversify its pipeline beyond Humira erosion, while Skyrizi and Rinvoq already deliver double-digit quarterly growth. Pfizer capitalizes on biosimilar production scale, recently launching Abrilada in multiple EU markets at a 50% list price discount to Humira.

Biosimilar entrants Sandoz, Amgen, and Samsung Bioepis disrupt pricing but must secure formulary access amid PBM rebate dynamics. Litigation over anti-competitive tactics, exemplified by Sandoz-Amgen Enbrel lawsuits, underscores heightened legal scrutiny. Mid-cap innovators such as Sanofi, SciRhom, and Cullinan Therapeutics are exploring oral cytokine inhibitors and bispecific antibodies to address unmet needs in refractory disease. Chinese manufacturer Jiangsu Hengrui priced its adalimumab biosimilar at CNY 1,200 (USD 165) per syringe and seized 12% of China’s market within a year, forcing multinational incumbents to deepen patient-support rebates. Meanwhile, SetPoint Medical broke new ground by winning FDA approval for a vagus nerve stimulation device for biologically refractory patients, foreshadowing future competition from non-pharmacologic modalities.

Rheumatoid Arthritis Drugs Industry Leaders

-

AbbVie Inc.

-

Amgen Inc.

-

Bayer AG

-

Boehringer Ingelheim GmbH

-

Bristol-Myers Squibb Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Lynk Pharmaceuticals Co., Ltd. announced encouraging topline results from its Phase III clinical trial of zemprocitinib (LNK01001) for treating moderate to severe active rheumatoid arthritis (RA). The trial successfully met its primary and key secondary efficacy objectives, delivering statistically significant improvements over placebo (P < 0.0001) while maintaining a favorable safety and tolerability profile.

- January 2026: Novartis received FDA Breakthrough Therapy status for ianalumab in Sjögren’s disease, underscoring its dual B-cell depletion and BAFF-R blockade mechanism.

- October 2025: Artiva Biotherapeutics earned Fast Track Designation for AlloNK in refractory Rheumatoid Arthritis when combined with rituximab, marking the first cell therapy to obtain such status in this indication.

- April 2024: The FDA approved AbbVie’s RINVOQ 15 mg once daily for giant cell arteritis, following a favorable European decision earlier in the year.

Global Rheumatoid Arthritis Drugs Market Report Scope

Rheumatoid arthritis is an autoimmune disorder that causes pain and inflammation in the body's joints. It primarily affects the joints of the hands, wrists, elbows, knees, and ankles. It also affects the cardiac and respiratory systems and is a systemic disease. It thus exhibits symptoms of swelling, redness, and warmth in the affected areas. The drugs to treat rheumatoid arthritis include NSAIDs, corticosteroids, DMARDs, biologics, and analgesics, which help reduce inflammation, suppress the immune system, and relieve pain.

The rheumatoid arthritis drugs market is segmented by type of molecule, drug class, route of administration, end-user, and geography. By type of molecule, the market is segmented into pharmaceuticals and biopharmaceuticals. By drug class, the market is segmented into non-steroidal anti-inflammatory drugs (NSAIDs), disease-modifying antirheumatic drugs (DMARDs), corticosteroids, analgesics, and other drug classes. By route of administration, the market is segmented into oral, parenteral, and topical. By end user, the market is segmented into hospital pharmacies, specialty pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across significant global regions. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| Pharmaceuticals |

| Biopharmaceuticals |

| Non-steroidal Anti-inflammatory Drugs (NSAIDs) |

| Disease-modifying Anti-rheumatic Drugs (DMARDs) |

| Corticosteroids |

| Analgesics |

| Other Drug Classes |

| Oral |

| Parenteral |

| Topical |

| Hospital Pharmacies |

| Specialty Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type of Molecule | Pharmaceuticals | |

| Biopharmaceuticals | ||

| By Drug Class | Non-steroidal Anti-inflammatory Drugs (NSAIDs) | |

| Disease-modifying Anti-rheumatic Drugs (DMARDs) | ||

| Corticosteroids | ||

| Analgesics | ||

| Other Drug Classes | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| By End User | Hospital Pharmacies | |

| Specialty Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the rheumatoid arthritis drugs market?

The market stood at USD 38.74 billion in 2026 and is forecast to reach USD 48.31 billion by 2031 at a 4.51% CAGR.

Which segment leads the rheumatoid arthritis drugs market?

Biopharmaceuticals command 67.48% share and are the fastest-growing segment, expanding at 8.76% CAGR through 2031.

How are biosimilars affecting pricing dynamics?

Biosimilar adalimumab already holds 23% US share, driving Humira revenue down 34% in one year and pushing originators toward aggressive discounts and pipeline diversification.

Which region is growing the fastest?

Asia-Pacific posts the highest regional CAGR at 9.12% owing to expanding healthcare infrastructure, supportive procurement policies and rising disposable incomes.

What policies are improving patient affordability?

Measures such as the US Inflation Reduction Act’s USD 2,000 Medicare Part D cap and China’s volume-based procurement program are lowering out-of-pocket costs and broadening biologic access.

Page last updated on: