Hashimotos Thyroiditis Drug Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

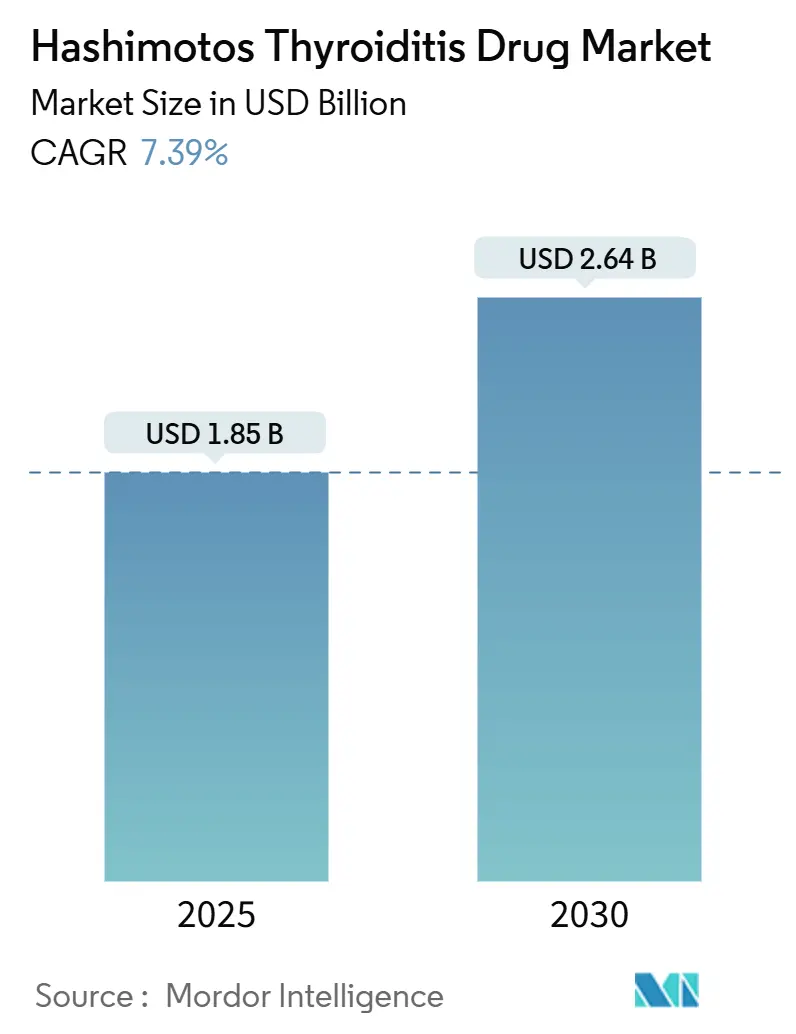

| Market Size (2025) | USD 1.85 Billion |

| Market Size (2030) | USD 2.64 Billion |

| Growth Rate (2025 - 2030) | 7.39% CAGR |

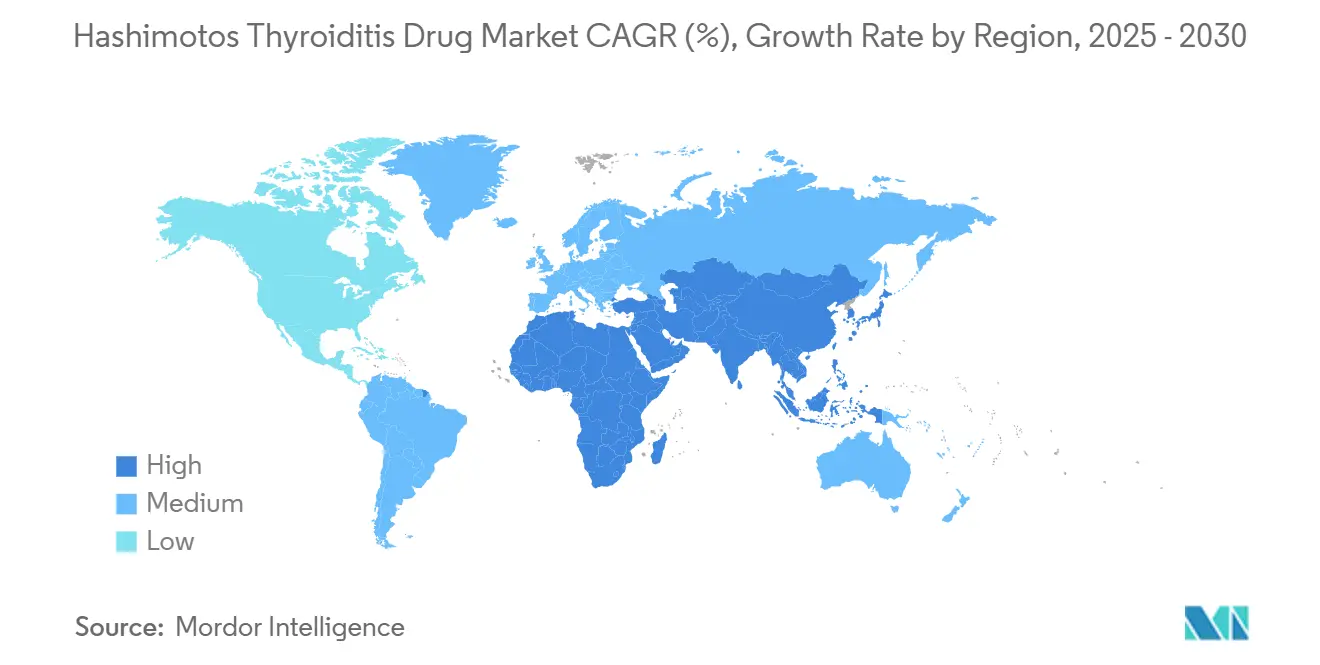

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hashimotos Thyroiditis Drug Market Analysis by Mordor Intelligence

The global Hashimoto's thyroiditis drug market size stood at USD 1.85 billion in 2025 and is forecast to reach USD 2.64 billion by 2030, reflecting a 7.39% CAGR over the period. Demand is expanding as autoimmune thyroid disorders become more common, clinicians adopt novel LT4 + LT3 combinations, and new thyroid hormone–receptor modulators enter the therapeutic toolbox. Persistent patient symptoms despite normalized TSH are encouraging trials of targeted drugs that can fine-tune peripheral T3 levels, opening white-space for differentiated mechanisms of action. Supply disruptions in 2024–2025 exposed vulnerabilities in levothyroxine manufacturing and prompted physicians to consider liquid LT4, soft-gel capsules and desiccated thyroid extract, each commanding premium prices. At the same time, direct-to-consumer telehealth models, paired with app-based adherence monitoring, are lifting prescription refill rates and expanding international access. Finally, regulator-backed real-world evidence confirming generic therapeutic equivalence is easing payer pressure yet has only modestly dented brand loyalty, preserving value for incumbents.

Key Report Takeaways

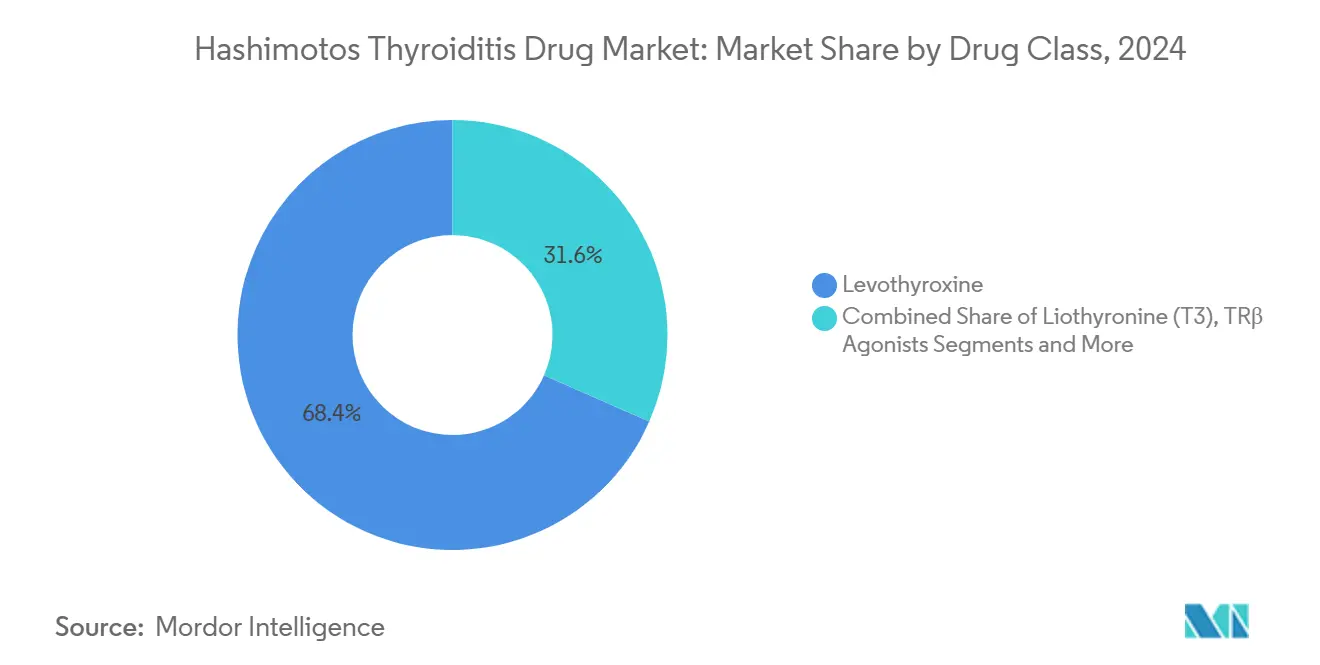

- By drug class, levothyroxine led with 68.41% of the Hashimoto's thyroiditis drug market share in 2024, while TRβ agonists are advancing at a 10.47% CAGR through 2030.

- By formulation, tablets accounted for 61.23% of the Hashimoto's thyroiditis drug market size in 2024 and liquid solutions are rising at an 11.46% CAGR.

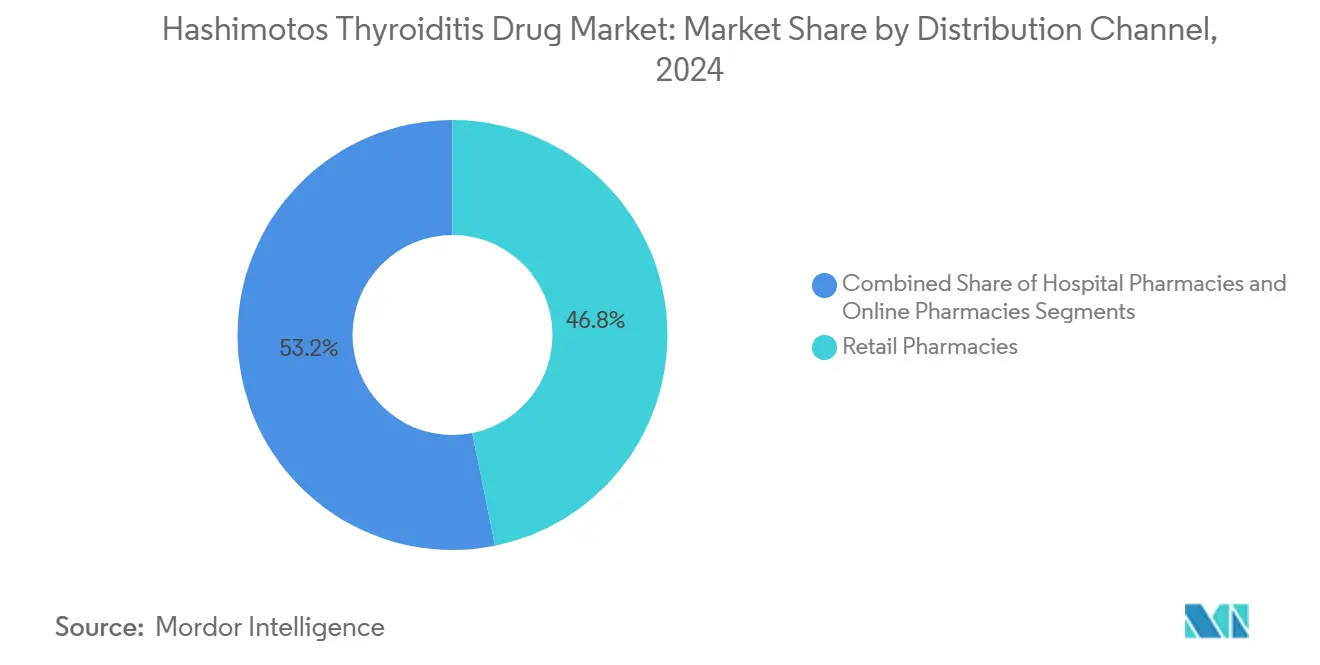

- By distribution channel, retail pharmacies held 46.84% revenue share in 2024, whereas online pharmacies post the fastest growth at 11.94% CAGR.

- By patient demographics, adults captured 67.31% share of the Hashimoto's thyroiditis drug market in 2024 and the pediatric segment is progressing at a 10.48% CAGR.

- By geography, North America remained dominant with 38.52% share in 2024, but Asia-Pacific exhibits the fastest 9.41% CAGR through 2030.

Global Hashimotos Thyroiditis Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of autoimmune thyroid disorders | +1.8% | Global; strongest in North America & Europe | Long term (≥ 4 years) |

| High prescription volume of levothyroxine (T4) | +1.5% | Worldwide, led by North America | Medium term (2-4 years) |

| Increasing awareness & national screening programs | +1.2% | Core Asia-Pacific, spill-over to MEA | Medium term (2-4 years) |

| Shift toward individualized LT4 + LT3 combination therapy | +1.0% | North America & Europe; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Liquid & soft-gel T4 formulations boosting adherence | +0.9% | Global; early uptake in developed markets | Short term (≤ 2 years) |

| TRβ-selective agonists repurposed for comorbidities | +0.8% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Autoimmune Thyroid Disorders

Cancer immunotherapy has unintentionally spotlighted the thyroid: 98% of checkpoint-inhibitor recipients who develop thyroid irAEs actually present with Hashimoto pathology, adding a new influx of patients to endocrinology practices.[1]Wenwen Gong, “Risk Factors and Outcomes of Thyroid Immune-Related Adverse Events Following PD-1/PD-L1 Inhibitors Treatment,” BMC Endocrine Disorders, biomedcentral.com Population aging in developed economies is widening this base because immune dysregulation intensifies with age. Meanwhile, AI-driven pattern-recognition tools now flag subtle TSH shifts in primary care, shortening diagnostic latency and expanding the treated population.[2]Mohammad H. Dabbaghmanesh, “Illuminating the Path to Thyroid Disorder Management Using Artificial Intelligence,” Shiraz E-Med J., semj.sums.ac.ir These advances collectively enlarge the Hashimoto's thyroiditis drug market as more subclinical cases move into active pharmacologic management. They also heighten demand for therapies that minimize long-term bone and cardiac risks associated with over-replacement. Finally, epidemiologic registries integrating oncology and endocrinology data provide real-world evidence that guides payers toward earlier intervention, sustaining drug utilization growth.

High Prescription Volume of Levothyroxine (T4)

Levothyroxine’s status as the 4th most dispensed drug in the United States—82.4 million annual prescriptions serving 18.1 million patients—restates the medicine’s outsized footprint. Because titration is lifelong, each patient generates repeated fills, reinforcing stable cash flows that entice branded and authorized-generic launches. Synthroid alone still commands roughly 82% of U.S. prescriptions, illustrating how perceived consistency trumps price in a narrow-therapeutic-index landscape. The dense monitoring burden—TSH checks every 6–12 weeks during dose adjustment—also inflates laboratory and consultation revenue tied to pharmacotherapy. Collectively these factors consolidate levothyroxine’s dominance, yet they simultaneously expose unmet needs for alternatives that curb pill burden and reduce visit frequency. This duality keeps the Hashimoto's thyroiditis drug market dynamic, blending legacy prescription volumes with space for differentiated entrants.

Increasing Awareness & National Screening Programs

Governments in China, India and several Gulf states have embedded thyroid-function testing into routine health checkups, spurred by digital diagnostics able to analyze large datasets in primary care. Clinical-trial registries from China list 65 active thyroid studies between 2009 and 2022, 21 of which target non-tumorous disorders including Hashimoto's thyroiditis. Early detection platforms integrate genetic screening for D2 Thr92Ala variants, informing whether LT4 monotherapy is likely to leave residual symptoms. As screening penetrates rural Asia, incidence appears to climb, yet the true driver is case discovery rather than disease explosion. This surveillance translates into earlier prescriptions, moving revenue forward in the patient journey and swelling total treated prevalence. Interactive public-health dashboards reporting regional hypothyroidism burden further galvanize funding for medicines on national formularies, bolstering volumes inside the Hashimoto's thyroiditis drug market.

Shift Toward Individualized LT4 + LT3 Combination Therapy

Patient-reported outcome surveys show 52% of hypothyroid adults favor combination therapy even when clinicians consider their TSH “normalized,” underscoring a gap between biochemical control and symptom relief. Sustained-release liothyronine candidates now smooth the T3 profile, lessening palpitations that limited older regimens.[3]Fereidoun Azizi, “Combined Preparation of Levothyroxine Plus Sustained-Release Liothyronine,” BMC Endocrine Disorders, springeropen.com An estimated 400,000 U.S. patients—double the level a decade ago—already rely on some LT4 + LT3 protocol, creating an anchor market for new entrants. Regulators have begun referencing combination therapy in guidelines for persistent symptomatic patients, lending legitimacy that unlocks reimbursement. For drug makers, the appeal lies in premium pricing justified by quality-of-life gains and compelling real-world evidence. These factors propel combination products into one of the fastest expanding niches within the Hashimoto's thyroiditis drug market.

Restraints Impact Analysis*

| Restraint | (-) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bioequivalence concerns dampening generic substitution | -1.2% | Global; pronounced in North America | Medium term (2-4 years) |

| Stringent potency-stability regulations for thyroid drugs | -0.8% | Worldwide; stricter in developed markets | Long term (≥ 4 years) |

| Fragile supply chain for porcine-derived DTE APIs | -0.6% | North America & Europe | Short term (≤ 2 years) |

| Rising uptake of nutraceutical & lifestyle interventions | -0.4% | Global; led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bioequivalence Concerns Dampening Generic Substitution

Despite FDA data proving therapeutic equivalence, brand-to-generic or generic-to-generic switching can induce TSH variability that alarms physicians, leading to repeat lab tests and dosage adjustments. Warning letters issued in 2024 against facilities manufacturing levothyroxine further erode prescriber confidence. Hospitals often instruct pharmacists to maintain patients on a single manufacturer, diminishing volume for low-cost entrants and constraining price competition. This barrier protects branded revenues but suppresses wider cost-driven adoption, tempering overall volume growth in the Hashimoto's thyroiditis drug market. Payers remain caught between higher brand spend and the clinical risk of hormonal fluctuations, resulting in cautious substitution policies that perpetuate restraint.

Stringent Potency-Stability Regulations for Thyroid Drugs

Both USP and EP require levothyroxine batches to retain 95–105% potency through expiry, a specification tightened in 2024 after multiple recalls. Manufacturers must overfill tablets to hedge degradation, inflating API consumption and costs. Extended validation studies for heat, light and humidity stress elongate development timelines and deter smaller entrants. Regulatory harmonization via ICH M13A bioequivalence guidance, while streamlining dossier formats, simultaneously enforces uniform high-bar criteria, raising compliance expenditure. Collectively, rigorous stability mandates depress near-term competitive intensity yet curtail supply flexibility, limiting rapid price declines in the Hashimoto's thyroiditis drug market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Innovation Beyond Traditional Hormones

Levothyroxine controlled 68.41% of the 2024 Hashimoto's thyroiditis drug market share, underlining its entrenchment as first-line replacement therapy. Nevertheless, the TRβ agonist cohort posts a 10.47% CAGR, signaling a paradigm shift toward receptor-selective modulation and metabolic comorbidity management. This segment’s fast clip enlarges the overall Hashimoto's thyroiditis drug market size, adding high-value prescriptions that complement rather than cannibalize LT4 volumes.

Combination LT4 + LT3 therapies occupy a growing niche where residual symptoms persist, and their uptake is underpinned by sustained-release T3 formulations that mitigate cardiovascular concerns. Desiccated thyroid extract, though limited by supply reliability, retains a loyal user base that values qualitative symptom relief over biochemical targets. Liothyronine monotherapy remains constrained to special scenarios such as thyroid cancer suppression. Taken together, drug-class diversification transforms the competitive landscape, but levothyroxine’s bulk volume continues to anchor the Hashimoto's thyroiditis drug market.

By Formulation: Liquid Solutions Overcome Absorption Barriers

Tablets commanded a 61.23% share of the 2024 Hashimoto's thyroiditis drug market size, owing to decades-long physician familiarity and payer formulary placement. Yet liquid solutions are outperforming with an 11.46% CAGR because they circumvent gastric pH variability and dietary interference, allowing more flexible dosing schedules. The soft-gel capsule niche also prospers, targeting patients with lactose intolerance and celiac disease, further fragmenting demand.

Injectable levothyroxine is confined to hospital use for myxedema coma but is drawing R&D attention through subcutaneous depot systems now under IND review. Innovators position these novel delivery forms as adherence solutions, especially for populations with polypharmacy or dysphagia. As evidence accumulates, formulary committees weigh higher acquisition costs against down-stream savings from reduced hospitalizations, reinforcing liquid and soft-gel momentum inside the Hashimoto's thyroiditis drug market.

By Distribution Channel: Digital Access Redraws Fulfillment Patterns

Retail outlets controlled 46.84% of global revenues in 2024, sustained by pharmacist counseling and insurance integration. Nonetheless, online pharmacies are expanding at 11.94% CAGR, capitalizing on telemedicine consultations that issue e-prescriptions and arrange same-day shipping of thyroid medications. For chronic therapy requiring monthly refills, subscription models reduce friction and bolster compliance, translating into higher fill rates per patient.

Hospital pharmacies handle postpartum thyroiditis and in-patient titration, yet their growth lags amid outpatient care dominance. Hybrid distribution models, where manufacturers partner directly with digital clinics, are emerging: Acella’s collaboration with Paloma Health exemplifies a closed-loop system combining virtual endocrinology visits with doorstep delivery, framing a new competitive frontier for the Hashimoto's thyroiditis drug market.

By Patient Demographics: Early Intervention Shapes Lifetime Value

Adults aged 18–64 years generated 67.31% of 2024 revenue, reflecting peak disease incidence alongside active workforce participation that supports regular monitoring and premium formulations. Pediatric prescriptions, though smaller in volume, deliver a 10.48% CAGR because heightened awareness of growth impairment drives earlier screening. Pediatric dose flexibility favors liquid LT4, and potential expansion of LT4 + LT3 combinations in youths with persistent low-normal T3 could further raise value per patient.

Elderly patients confront polypharmacy, requiring careful dose titration to avoid atrial fibrillation, while pregnant women need trimester-specific dose escalations. Personalized algorithms integrating age, weight, genetic polymorphisms and comorbidities are under development to refine therapy across life stages, enhancing clinical outcomes and solidifying patient loyalty to specific brands. This demographic tailoring secures long-run utilization within the Hashimoto's thyroiditis drug market.

Geography Analysis

North America retained a 38.52% revenue share in 2024 as brand loyalty and insurance coverage offset generic erosion. Yet chronic levothyroxine shortages in both the United States and Canada demonstrated the fragility of supply chains, pushing clinicians toward imported alternatives and liquid formulations.

Asia-Pacific is winning the speed race with 9.41% CAGR thanks to broader insurance schemes, urbanized lifestyles fueling autoimmune incidence, and regulatory acceleration exemplified by Australia’s sequential generic approvals. China’s jump in thyroid clinical trials underscores domestic innovation, while India’s openness to advanced diabetes-thyroid cross-over drugs signals a sophisticated prescription base.

Europe exhibits mature, guideline-driven consumption with powerful arbitration of drug pricing, yet new bioequivalence harmonization can shorten time-to-market for pan-regional generics. In contrast, Middle East & Africa and South America remain volume-constrained by patchy insurance coverage, although telehealth penetration is slowly unlocking rural demand. Altogether, geographic heterogeneity ensures multiple growth vectors sustain the global Hashimoto's thyroiditis drug market.

Competitive Landscape

Intensity sits at a moderate level as branded levothyroxine, authorized generics, specialty thyroid players and metabolic-disease upstarts contest mindshare. Synthroid retains near-monopoly U.S. share by leveraging consistency messaging, sample programs and strong endocrinologist engagement.

Pipeline differentiation is visible among biotechs targeting TRβ with metabolic benefits; litigation victories have protected Viking Therapeutics’ intellectual property, discouraging fast-follower entrants and reinforcing investor confidence. Concurrently, Jerome Stevens Pharmaceuticals’ acquisition of Thyquidity expanded its endocrine franchise and mitigated prior liquid-formulation shortages, fortifying supply reliability.

Digital-first providers like Paloma Health introduce vertical integration, owning patient relationships from teleconsultation through drug shipping and digital follow-up. This service bundling threatens traditional pharmacy margins, compelling incumbents to explore omnichannel offerings. M&A and co-marketing alliances are likely as stakeholders vie for data, distribution and differentiation in the evolving Hashimoto's thyroiditis drug market.

Hashimotos Thyroiditis Drug Industry Leaders

AbbVie Inc.

Merck KGaA

Pfizer Inc.

Viatris

Lannett Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Jerome Stevens Pharmaceuticals acquired Thyquidity (levothyroxine sodium oral solution) from Azurity Pharmaceuticals to reinforce its liquid-formulation portfolio and stabilize national supply.

- March 2025: The Clayman Thyroid Center launched the annual Hashimoto's Disease Awareness Day, observed every second Wednesday of March, to improve early detection and patient education.

Global Hashimotos Thyroiditis Drug Market Report Scope

| Levothyroxine (T4) |

| Liothyronine (T3) |

| LT4 + LT3 Combination |

| Desiccated Thyroid Extract |

| TRβ Agonists |

| Others |

| Tablets |

| Soft-gel Capsules |

| Liquid Solution |

| Injectable |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Adults (18-64 yrs) |

| Pediatric (<18 yrs) |

| Pregnant Women |

| Elderly (≥65 yrs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Levothyroxine (T4) | |

| Liothyronine (T3) | ||

| LT4 + LT3 Combination | ||

| Desiccated Thyroid Extract | ||

| TRβ Agonists | ||

| Others | ||

| By Formulation | Tablets | |

| Soft-gel Capsules | ||

| Liquid Solution | ||

| Injectable | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Patient Demographics | Adults (18-64 yrs) | |

| Pediatric (<18 yrs) | ||

| Pregnant Women | ||

| Elderly (≥65 yrs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the global Hashimoto's thyroiditis drug market?

The market was valued at USD 1.85 billion in 2025 and is projected to hit USD 2.64 billion by 2030.

How fast is the market expected to grow?

The compound annual growth rate is forecast at 7.39% between 2025 and 2030.

Which drug class leads global sales?

Levothyroxine continues to dominate with a 68.41% market share in 2024.

Which region is expanding the quickest?

Asia-Pacific is the fastest-growing region, projected to register a 9.41% CAGR through 2030.

Why are liquid levothyroxine formulations gaining traction?

They allow flexible dosing around meals and acid-suppression therapy, improving adherence and TSH stability.

What drives interest in LT4 + LT3 combination therapy?

Around half of patients report persistent symptoms on monotherapy, and sustained-release T3 formulations now address previous safety concerns.

Page last updated on: