Oman Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

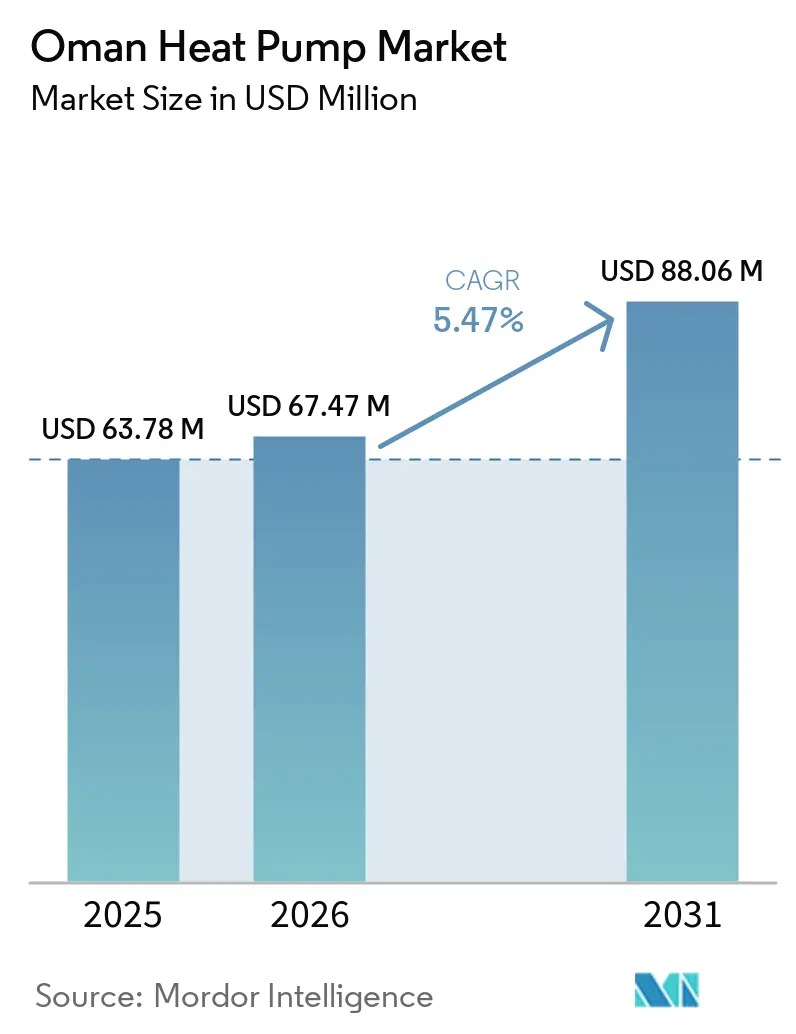

| Base Year Market Size (2025) | USD 63.78 Million |

| Market Size (2026) | USD 67.47 Million |

| Market Size (2031) | USD 88.06 Million |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

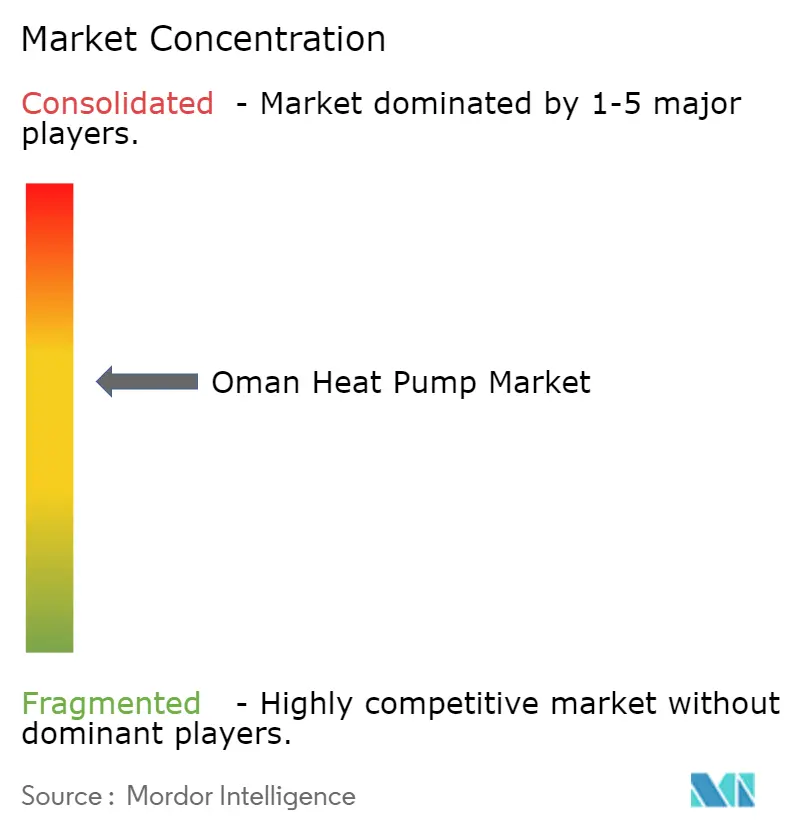

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Heat Pump Market Analysis by Mordor Intelligence

The Oman heat pump market size is projected to expand from USD 63.78 million in 2025 and USD 67.47 million in 2026 to USD 88.06 million by 2031, registering a CAGR of 5.47% between 2026 to 2031. Recent electricity-tariff reforms, a hotel construction surge, and district-cooling roll-outs are reshaping end-user economics, prompting developers to weigh lifecycle efficiency over first cost. Policy tailwinds tied to Oman Vision 2040 and the Kigali Amendment are nudging commercial buyers toward low-GWP and natural-refrigerant systems, even as subsidized natural gas still tempers industrial uptake. Global brands are strengthening local service footprints, while Energy Service Company (ESCO) financing is enlarging retrofit demand. Collectively, these forces position the Oman heat pump market for steady, policy-backed growth that aligns cooling-intensive development with the sultanate’s net-zero timeline.

Key Report Takeaways

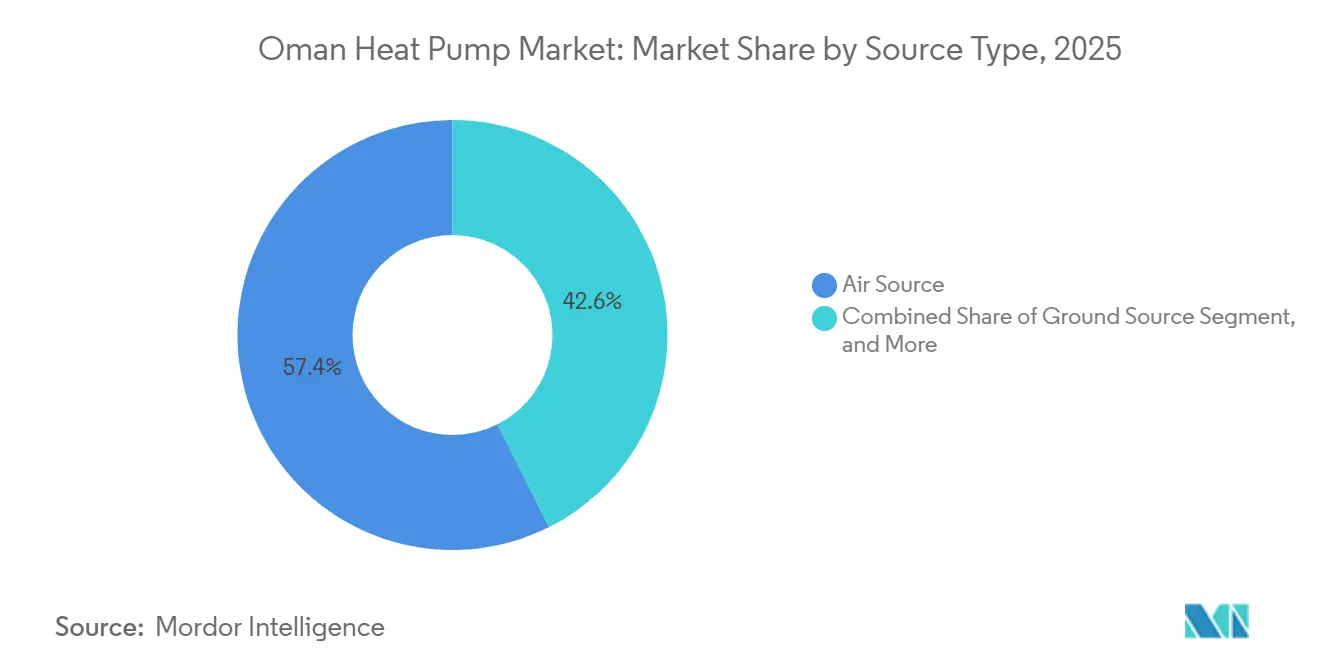

- By product type, air-source systems led with 57.42% revenue share in 2025, while water-source configurations are advancing at a 6.31% CAGR through 2031.

- By technology, air-to-air systems commanded 54.76% of installations in 2025, whereas water-to-water units are projected to post the fastest 6.02% CAGR to 2031.

- By application, domestic and sanitary hot water represented 44.61% of demand in 2025; space cooling is forecast to expand at a 6.06% CAGR through 2031.

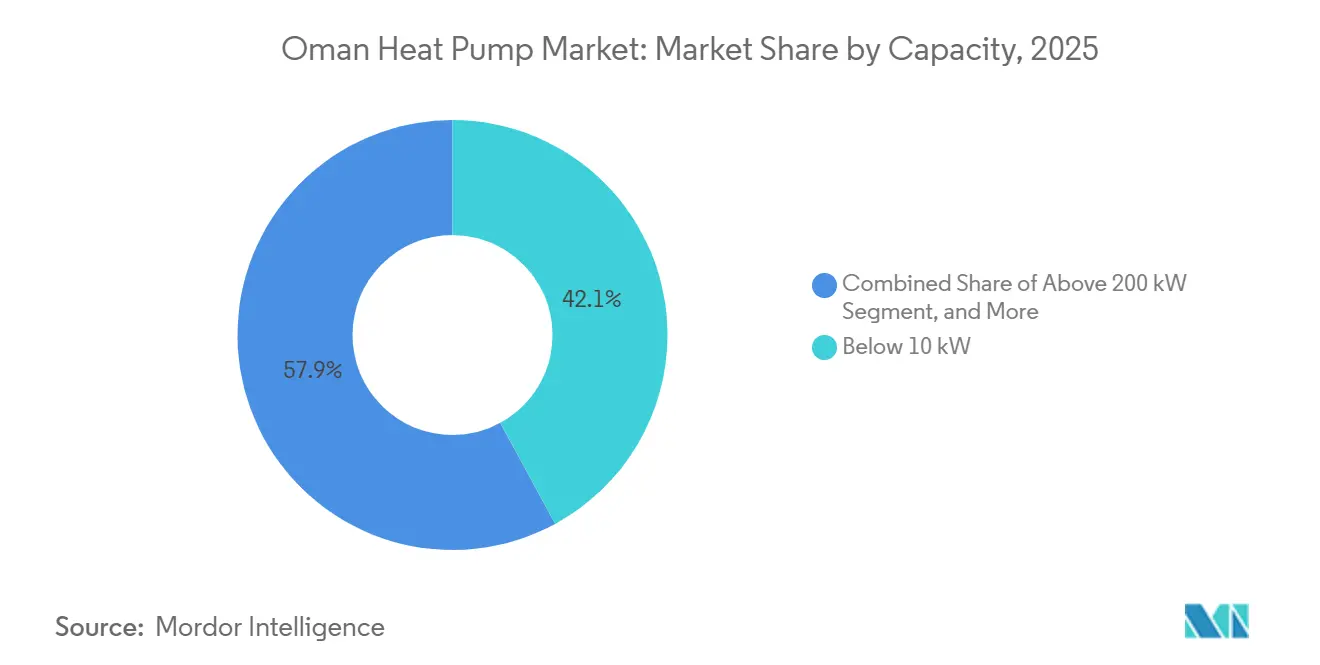

- By capacity, below-10 kilowatt units captured 42.08% of the Oman heat pump market share in 2025, while 50-kilowatt-to-200-kilowatt units are set to grow at 5.86% annually.

- By installation, new builds accounted for 61.13% of the Oman heat pump market size in 2025, yet retrofits are expanding at a 6.11% CAGR to 2031.

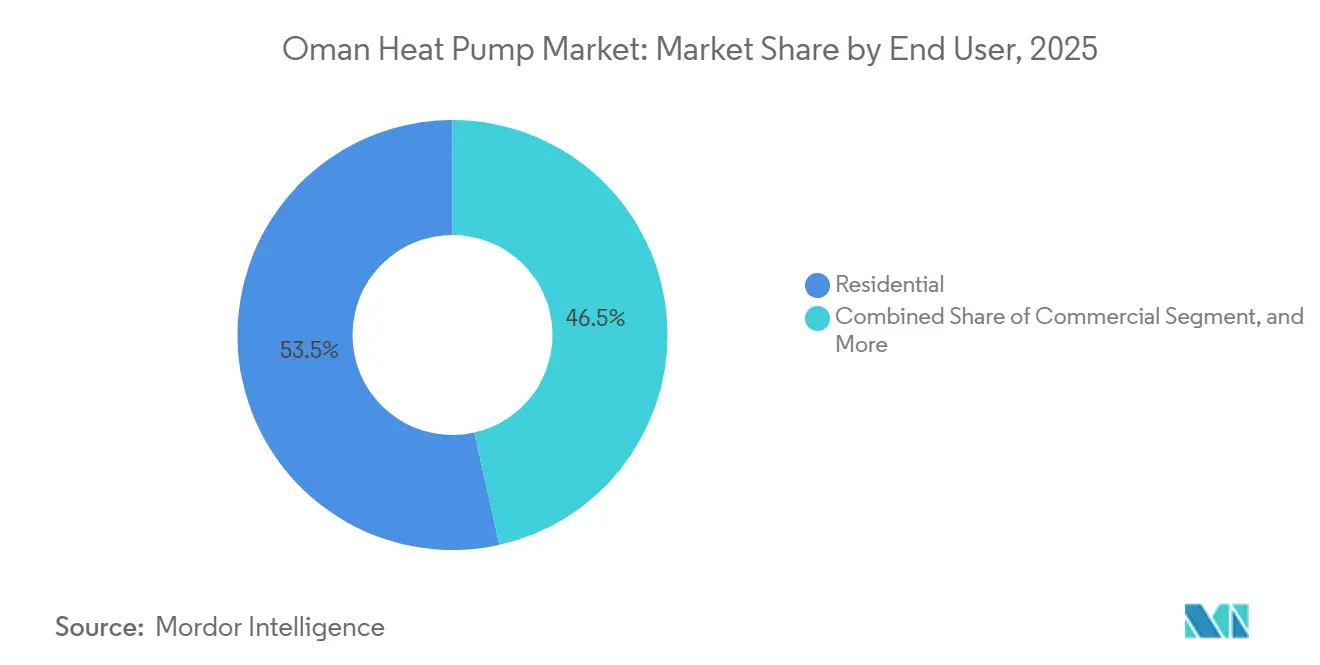

- By end user, residential held 53.49% of 2025 revenue, whereas the industrial segment records the highest 5.86% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Oman Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial Decarbonization Initiatives Under Oman Vision 2040 | +1.2% | Sohar, Duqm, Muscat industrial zones | Long term (≥ 4 years) |

| Hospitality-Led Construction Boom Driving HVAC Demand | +1.5% | Muscat, Salalah, coastal tourism corridors | Medium term (2-4 years) |

| Integration With Smart Building and IoT Energy-Management Platforms | +0.8% | Muscat commercial and government buildings | Medium term (2-4 years) |

| Rising Electricity Tariffs Elevating Total-Cost-of-Ownership Focus | +1.3% | Commercial and industrial users nationwide | Short term (≤ 2 years) |

| District-Cooling Roll-Outs in Duqm SEZ Using Seawater-Source Heat Pumps | +0.9% | Duqm, with spillover to Sohar and Muscat | Long term (≥ 4 years) |

| Royal Navy Retrofits Creating Defense-Sector Reference Projects | +0.4% | Defense facilities countrywide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial Decarbonization Initiatives Under Oman Vision 2040

Oman Vision 2040 sets a 30% renewable-energy target by 2030 and carbon neutrality by 2050, creating a binding framework that elevates electrified heat recovery in petrochemical and desalination hubs. Fewer than 10% of heavy-industry sites employed waste-heat capture in 2024, leaving sizable headroom for 10 MW-to-50 MW industrial heat pumps now offered by global suppliers.[1]Atlas Copco, “Heat Pumps,” atlascopco.com The inaugural SuperESCO pilot at OQ Refineries promises 22.5 GWh annual savings and 9.4 kt CO₂ avoidance, demonstrating a pay-from-savings model that removes upfront-capital friction. As the Ministry of Energy and Minerals prepares to scale the scheme, industrial buyers gain a proven template that links compliance targets with attractive internal rates of return. These dynamics make large-capacity units a credible pathway for deep-carbon cuts in Oman’s process industries.

Hospitality-Led Construction Boom Driving HVAC Demand

Twenty-seven hotel projects totaling 4,709 keys moved through the pipeline in Q2 2025, and January 2026 saw marquee openings such as a Hilton trio and the Four Seasons Marina Bandar A'Rawdha Developers specify chilled-water backbones sized for future heat-pump hot-water retrofits, slashing auxiliary heating costs by up to 75% versus resistance elements. Commercial tariffs rose 18% in 2025, so operators now focus on total ownership cost, favoring units with coefficients of performance above 4.0 that qualify for accelerated depreciation. High-ambient air-to-water heat pumps also deliver simultaneous cooling and domestic hot water, trimming mechanical-room footprints in land-constrained resorts. These economics cement the hospitality sector as the most immediate outlet for premium-efficiency products.

Integration With Smart Building and IoT Energy-Management Platforms

Cloud-linked platforms such as Syncrow’s SyncOS, launched in July 2025, pool data streams from HVAC, lighting, and plug loads, achieving 22% peak-demand cuts during Muscat pilots.[2]Syncrow, “SyncOS Launch,” syncrow.com Siemens Demand Flow delivered 36% annual energy savings at German University of Technology in Oman by modulating chiller staging through machine-learning algorithms.[3]German University of Technology in Oman, “Energy Efficiency and Sustainability,” gutech.edu.om Government retrofits now mandate open-protocol IoT sensors, creating a reference stack that private owners increasingly mirror. Predictive maintenance improves uptime and halves emergency-repair outlays, strengthening the business case for high-capacity heat pump integration. Vendor-lock challenges persist, yet open-platform adoption is rising as building owners seek cross-brand interoperability.

Rising Electricity Tariffs

Industrial electricity prices climbed 12%-to-15% when subsidies narrowed in January 2025, pressuring energy-intensive users to reexamine cooling economics.[4]Times of Oman, “Oman announces new electricity tariff structure effective January 2025,” timesofoman.com Heat pumps with energy-efficiency ratios of 4.0-to-5.0 outperform legacy chillers by roughly 60%, translating to six-year paybacks in ESCO-financed government retrofits. Electricity supply reached 38,711 GWh in 2023 and will approach 20.3 GW of capacity by 2030, yet demand-side efficiency remains untapped relative to technical potential.[5]Oman Authority for Public Services Regulation, “Electricity Sector Statistics 2023,” apsr.om Forward-looking tariff schedules heighten uncertainty, so hedging through high-performance systems is gaining board-level attention, catalyzing accelerated procurement cycles across offices, malls, and logistics hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Capital Cost for Small-Scale Residential Users | -0.9% | Nationwide villas and small shops | Short term (≤ 2 years) |

| Shortage of Skilled Installers and Service Technicians | -0.7% | Rural and secondary cities | Medium term (2-4 years) |

| Five Percent Import Tariff Plus High Freight Costs for Bulky Units | -0.5% | All segments except U.S. FTA items | Short term (≤ 2 years) |

| Subsidized Natural-Gas Prices Undermine Industrial Business Case | -1.1% | Petrochemical and manufacturing zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital Cost for Small-Scale Residential Users

Below-10 kilowatt units retail for USD 3,000-to-USD 8,000, a 150%-to-200% premium over split ACs, deterring middle-income households despite 20-year lifecycle savings. Green-loan products are scarce, and consumer-side ESCO models are absent, so uptake hinges on self-financing. Residential tariffs, although higher than pre-2025 levels, remain insufficiently punitive to guarantee attractive paybacks for homes consuming under 10,000 kWh annually. Manufacturers now promote hybrid cooling-and-water-heating packages that shave installed cost by up to 30%, yet penetration still trails 5% of annual residential HVAC sales. Without credit mechanisms or rebates, broad-based household adoption will remain subdued.

Shortage of Skilled Installers and Service Technicians

Complex water- and ground-source systems demand refrigerant charging, hydronic balancing, and smart-controller commissioning beyond the scope of typical split-AC mechanics. Only 150 Omani technicians joined a 2,500-person regional training initiative in 2025, illustrating limited local capacity.[6]Johnson Controls, “Middle East HVAC Training Initiative,” johnsoncontrols.com National Training Institute programs face enrollment bottlenecks as certified technicians earn minimal wage premiums over general HVAC labor. Kafa'a upskilled 56 professionals for Association of Energy Engineers credentials, but demand far outstrips supply. Until a licensing framework emerges and wage signals improve, installer scarcity will cap complex-system diffusion, especially outside Muscat and Salalah.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Coastal Zones Favor Water-Source Configurations

Water-source heat pumps, though smaller in installed base, are growing at a 6.31% CAGR as Duqm and Sohar deploy seawater loops that maintain 24 °C-to-30 °C inlet temperatures, enabling coefficients of performance above 4.0 compared with 3.1 for air-source units braving 50 °C summer peaks. Air-source systems still held 57.42% of 2025 revenue thanks to swift installation and retrofit suitability across Muscat villas and interior towns where groundwater is scarce.

Large petrochemical operators now pilot hybrid air-to-water units married to variable-refrigerant-flow modules, providing discharge temperatures above 80 °C for cleaning-in-place and pasteurization processes. Ground-source remains a boutique choice in institutional campuses willing to absorb USD 150-to-USD 250 per-meter drilling costs that deliver 25-year borehole life and minimal annual maintenance. Oman's Kigali ratification is accelerating the shift from R-410A to R-32 and propane, with propane units posting 15% efficiency gains in regional pilots, though building-code fire-safe revisions are still pending.

By Technology: Air-to-Water Gains in Multi-Family and Hospitality

Air-to-air technology comprised 54.76% of 2025 installations, thriving in small offices and split-system retrofits where ducting is absent. Water-to-water units anchor district-cooling nodes like Innovation Park Muscat, whose 10,000 RT plant leverages thermal storage to shave 30% off electricity bills.

Air-to-water modules are displacing separate chiller and boiler racks in hotels, improving whole-building system efficiency by up to 25% while reclaiming mechanical-room space for revenue-generating amenities. Ground-to-water remains marginal but instructive; Siemens Demand Flow at German University of Technology modulates borehole temperature with live occupancy data, achieving 36% annual savings and 642 t-CO₂ abatement. The 2025 Oman Building Code, moving from voluntary trial to mandatory status by 2030, is expected to tighten minimum Energy Efficiency Ratio thresholds, implicitly favoring water-based and high-temperature heat-pump designs.

By Capacity: Mid-Range Units Serve Commercial Retrofits

The 50 kilowatt-to-200 kilowatt band, although smaller in shipment count, already delivers roughly one-quarter of installed kilowatt-hours and is expanding at a 5.86% annual clip inside the Oman heat pump market. Projects such as the Civil Services Pension Fund headquarters in Muscat rely on four modular chillers totaling 5,120 kilowatts, each outfitted with high-ambient kits that keep coefficients of performance from cascading during 48 °C summer peaks . Commercial landlords choose these mid-range packages because cranes or service elevators can place them on rooftops without street closures, trimming installation lead time by two weeks compared with single large tonnage machines. Energy-services contractors overlay remote monitoring, enabling operators to modulate staging once overnight humidity drops, which further compresses payback periods.

Below-10 kilowatt units retain 42.08% share of the Oman heat pump market share in villas and convenience stores, yet penetration growth slows as tariffs make lifecycle economics less compelling for households consuming below 10,000 kWh. Above-200 kilowatt systems remain a niche at under 10 % of unit sales, but feasibility studies around Sohar and Duqm petrochemical clusters keep them visible in future demand models for the Oman heat pump market. Industrial customers continue to stress-test turbocompressor designs that reach 50 megawatts thermal, but subsidized gas tempers near-term conversion. ESCO pilots that verified 22.5 GWh yearly savings in refinery campuses nevertheless illustrate that scale installations can clear the 15 % internal-rate-of-return hurdle when coupled with performance contracting.

By Application: Space Cooling Overtakes Hot-Water Demand

Domestic and sanitary hot-water systems commanded 44.61 % of 2025 demand inside the Oman heat pump market size, reflecting the country’s legacy of electric-resistance heaters in hotels and multifamily towers. Rheem and Ariston units registering coefficients of performance above 4.0 replace those elements with 20-year assets that reduce utility spend by up to 75%, which resonates among hospitality operators affected by an 18 % tariff hike in 2025. The Ministry of Housing retrofit showed that coupling heat-pump water heaters with smart controls yielded a verified six-year payback even without rebates.

Space-cooling demand is projected to rise at a 6.06 % CAGR, making it the fastest growth vector of the Oman heat pump market. Mega-projects such as the USD 18-20 billion Great Blue City embed chilled-water backbones sized for future air-to-water upgrades that can simultaneously generate process hot water. Industrial and process heating remains under 8 % of units but generates the most inbound inquiries from desalination plants striving to elevate brine feed temperatures with waste-heat recovery. Space heating stays negligible because winter lows hover at 18 °C except in high-altitude interiors, so vendors seldom stock dual-mode European models.

By End User: Industrial Segment Accelerates on ESCO Financing

Residential customers preserved a 53.49 % revenue share of the Oman heat pump market in 2025, anchored in owner-occupied villas that prize silent operation and Wi-Fi thermostats. Uptake plateaus as sticker shock outweighs long-term savings, a dynamic that underscores why industry watchers classify the Oman heat pump industry as policy-sensitive rather than purely price-elastic.

Commercial buildings, encompassing offices and malls, raised their share to roughly 38 %, while the industrial slice, though still under 9 %, books the steepest 5.86 % growth trajectory thanks to SuperESCO pilots. OQ Alternative Energy’s refinery program illustrates how verified-savings contracts let corporate treasurers record off-balance-sheet assets, a structure now replicated in government portfolios. The Oman heat pump market therefore finds its most reliable uplift where fuel-switching aligns with carbon-credit accrual and corporate sustainability targets.

By Installation: Retrofit Projects Unlock Existing Building Stock

New-build integration remained dominant at 61.13% of the Oman heat pump market size during 2025 because contractors could optimize piping and electrical risers before handover. Developers of Sultan Haitham City specified fused-header plumbing that eases future integration of water-source heat pumps once seawater intakes come online.

Retrofit activity, expanding at 6.11 % a year, turns older stock into a demand well for the Oman heat pump market. The HASA Energy contract that sliced ministerial energy use by 39 % in six years solidifies investor confidence in pay-from-savings mechanics. Energy audits at Sultan Qaboos University revealed 37.6 % possible reduction, most of which stems from right-sizing chillers and adding variable frequency drives, both complementary to heat-pump retrofits. As Kafa’a certifies more professionals, measurement-and-verification rigor improves, unlocking commercial loans for mid-size owners.

Geography Analysis

Muscat Governorate concentrates about 55 % of installations within the Oman heat pump market because it hosts the highest number of grade-A towers and hotel keys. Coastal humidity paired with 50 °C highs challenges air-source performance, so designers adopt seawater loops that keep entering-water temperatures near 28 °C, boosting system efficiency by roughly 30%. Muscat’s Civil Services Pension Fund tower demonstrated four-chiller redundancy that keeps compressor lift under control during peak load hours. Code compliance also starts earlier in Muscat, where municipal approvals already align with the forthcoming mandatory Oman Building Code.

Dhofar, anchored by Salalah, now secures 15 % of the Oman heat pump market. The USD 208 million tourism complex and a new RO 4.62 million (USD 12.0 million) manufacturing plant that can assemble 70,000 units yearly both stimulate local demand and shorten delivery cycles. Salalah’s cooler micro-climate allows air-source systems to maintain coefficients of performance above 3.5 even in summer, which reduces reliance on water-source variants. Because the plant earned the Gulf Standardisation Mark, engineers in the wider Middle East and Africa view Dhofar as an emerging export hub, further embedding the Oman heat pump market in regional supply chains.

Sohar and Duqm industrial corridors together hold about 20 % share and form the growth frontier for the Oman heat pump market. Petrochemical sites there evaluate turbocompressor heat pumps that deliver 10 MW-to-50 MW thermal at up to 300 °C discharge, aiming to harness waste heat from compressors and desalination brine. District-cooling rollouts in Duqm Special Economic Zone already integrate seawater-source designs that achieve coefficients of performance beyond 4.0, offering a living lab for coastal industrial clusters. Interior regions such as Nizwa and Ibri collectively sit near 10 % share, encumbered by limited installer density and higher freight costs, yet training programs under Kafa’a slowly chip away at capacity gaps.

Competitive Landscape

Five global brands, Daikin, Mitsubishi Electric, LG Electronics, Carrier Global, and Trane Technologies, hold around 60-to-65 % combined stake in the Oman heat pump market, which yields a moderate concentration profile. Each vendor couples showroom displays with on-site technical teams, letting consulting engineers witness variable-refrigerant-volume performance in Muscat’s 48 °C coastal conditions. LG’s 2026 Muscat showroom accelerates bid specifications for high-ambient VRF units, while Daikin Solution Plaza doubles as a training academy that certifies installers on charge-optimization best practices.

Competition now hinges less on hardware differentiation and more on bundled energy-services portfolios that mirror ESCO financing norms inside the Oman heat pump industry. Johnson Controls packages performance guarantees with digital twins that benchmark building operation against international peers. Trane’s remote-monitoring center in Dubai absorbs Muscat telemetry and dispatches corrective instructions, cutting unscheduled downtime by 40 %. Atlas Copco searches for first-mover advantage in process-heat recovery, pitching turbocompressor designs that could dislodge natural-gas boilers once subsidies taper.

Local players seed white-space niches. Engineering Industries Company, by inaugurating its Salalah factory, positions itself to fill quick-turn orders and avoid five-percent import duties that still apply to most Asian-sourced equipment. Syncrow, a Muscat start-up, allies with chilled-water plant operators to layer predictive analytics atop legacy building-management systems, an approach that elevates stickiness for whichever hardware brand wins the chiller tender. As the Oman Building Code tightens efficiency thresholds, natural-refrigerant adoption will likely sort winners from laggards, with propane-based portfolios giving early movers a compliance cushion.

Oman Heat Pump Industry Leaders

Daikin Industries Ltd.

Mitsubishi Electric Corporation

LG Electronics Inc.

Carrier Global Corporation

Trane Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sohar University issued a tender covering design, supply, installation, testing, and commissioning of a 17,457 m² HVAC system for its Innovation Centre Phase I building, further signaling institutional demand for the Oman heat pump market.

- February 2026: Oman Observer reported that the Ministry of Energy and Minerals will scale the SuperESCO program after the OQ Alternative Energy pilot recorded 22.5 GWh yearly savings and 9.4 kt CO₂ avoidance.

- January 2026: Engineering Industries Company began production at its OMR 4.62 million (USD 12.0 million) air-conditioning plant in Salalah Free Zone, adding 70,000-unit annual capacity and targeting Gulf Cooperation Council exports.

- January 2026: LG Electronics opened a dedicated commercial air-conditioning showroom in Muscat, showcasing variable-refrigerant-flow solutions adapted to high-ambient Gulf climates.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Oman heat pump market as sales revenue from newly installed air-source, water-source, and ground-source heat-pump units rated up to one megawatt that deliver space cooling, space heating, or domestic hot water across residential, commercial, industrial, and institutional premises in the Sultanate. Systems integrated inside large chillers or district-cooling plants and portable room coolers are kept outside this frame.

Equipment whose primary function is vapor-compression air-conditioning without heat-pump reversal is excluded.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Omani HVAC contractors, distributor principals in Muscat and Sohar, property developers, and policymakers overseeing Vision 2040 energy goals. These conversations tested import-volume assumptions, validated typical installed costs, and calibrated adoption triggers across housing tiers and light-industry clusters.

Desk Research

We began with regulatory datasets from bodies such as Oman's Authority for Public Services Regulation, Nama Group's tariff filings, the Ministry of Housing and Urban Planning's building-permit bulletins, trade invoices in UN Comtrade, and population projections from the National Center for Statistics & Information. Market context was enriched through trade-association briefs from the Gulf HVAC Society, peer-reviewed articles on Gulf climate loads, and installer price lists that circulate on open manufacturer portals. To verify corporate footprints and shipment values, analysts mined D&B Hoovers and Dow Jones Factiva. The named sources illustrate the mix; several other public and subscription holdings informed cross-checks throughout the study.

Market-Sizing & Forecasting

A top-down construct starts with dwelling and commercial floor-space inventories, peak-cooling degree days, and tariff-driven technology penetration rates, which are then monetized through average selling prices backed by customs data. Select bottom-up rollups of large distributor shipments and sampled installer invoices act as guardrails that adjust totals when deviations exceed five percent. Key variables include new housing completions, retrofit share of electricity-subsidy segments, unit ASP movements, peak-period tariff premiums, and Vision 2040 rebate uptake. Five-year projections rely on exponential smoothing layered with scenario analysis that reflects electricity-price bands and construction-cycle swings.

Data Validation & Update Cycle

Outputs pass a two-stage peer review, after which anomalies against import statistics or power-sector forecasts trigger re-runs. Reports refresh every twelve months, with mid-cycle updates when subsidy reforms or building-code revisions materially shift inputs.

Why Mordor's Oman Heat Pump Baseline Commands Reliability

Published figures often diverge because publishers adopt different geographic cuts, technology mixes, or refresh cadences.

Key gap drivers include wider regional scopes, omission of tariff elasticity, or reliance on unvetted shipment proxies. Mordor pairs country-specific policy trackers with shipment audits and updates the model annually, so users receive figures anchored to current on-ground variables rather than regional averages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 63.8 million (2025) | Mordor Intelligence | - |

| USD 42 million (2024) | Regional Consultancy A | Excludes water-source and ground-source units; omits retrofit segment |

| USD 669.1 million (2024) | Trade Journal B | Covers entire Middle East; treats Saudi volumes as proxy for Oman without tariff adjustment |

In sum, Mordor's disciplined country scope, variable transparency, and annual refresh cadence deliver a balanced baseline that decision-makers can retrace and replicate with confidence.

Key Questions Answered in the Report

How large will the Oman heat pump market be by 2031?

The Oman heat pump market size is forecast to reach USD 88.06 million by 2031, expanding at a 5.47% CAGR from 2026.

Which capacity segment is growing fastest?

Units rated between 50 kilowatts and 200 kilowatts are advancing at a 5.86% yearly pace as commercial retrofits accelerate.

What drives industrial adoption of heat pumps in Oman?

SuperESCO financing aligned with Oman Vision 2040 decarbonization goals lets refineries and petrochemical sites install 10 MW-plus heat pumps without upfront capital.

How are electricity tariffs influencing purchasing decisions?

The 12%-to-15% industrial tariff increase in 2025 sharpened total-cost-of-ownership focus, pushing building owners toward systems with coefficients of performance above 4.0.

Which geography outside Muscat shows strong future demand?

Duqm Special Economic Zone is emerging as a high-growth pocket due to district-cooling networks that favor seawater-source heat pump designs.

What constraint most limits residential uptake?

A 150%-to-200% upfront price premium over split ACs, combined with scarce green-loan products, continues to slow household conversions.

Page last updated on: