Argentina Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

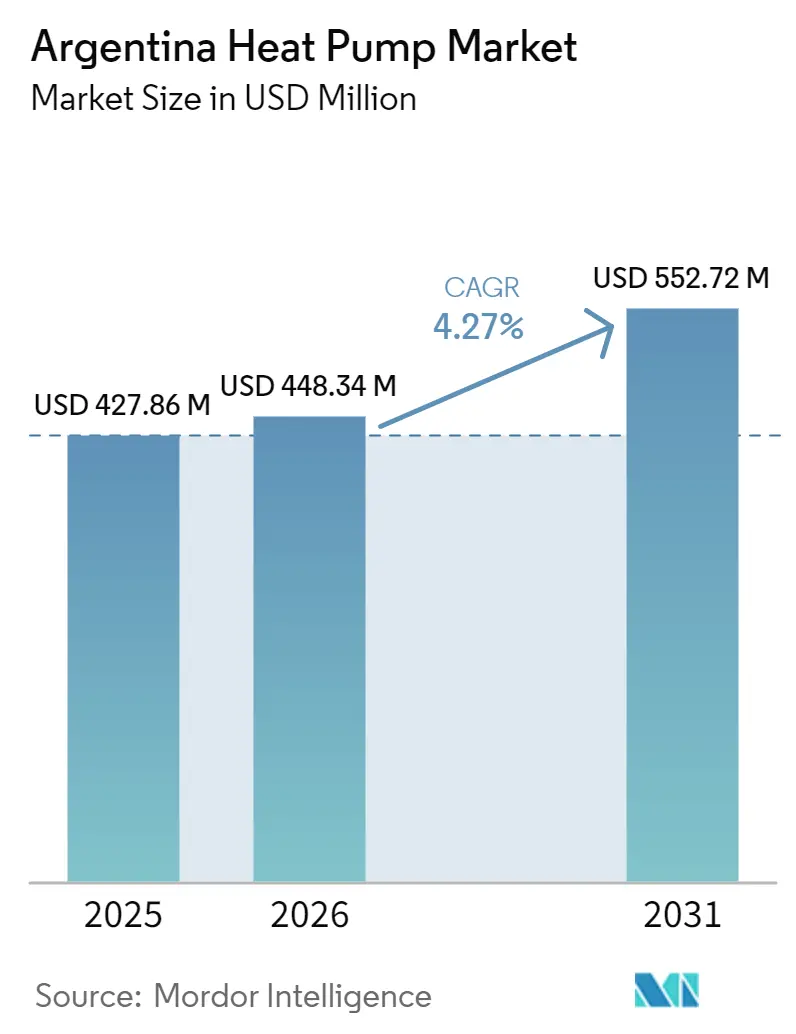

| Base Year Market Size (2025) | USD 427.86 Million |

| Market Size (2026) | USD 448.34 Million |

| Market Size (2031) | USD 552.72 Million |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

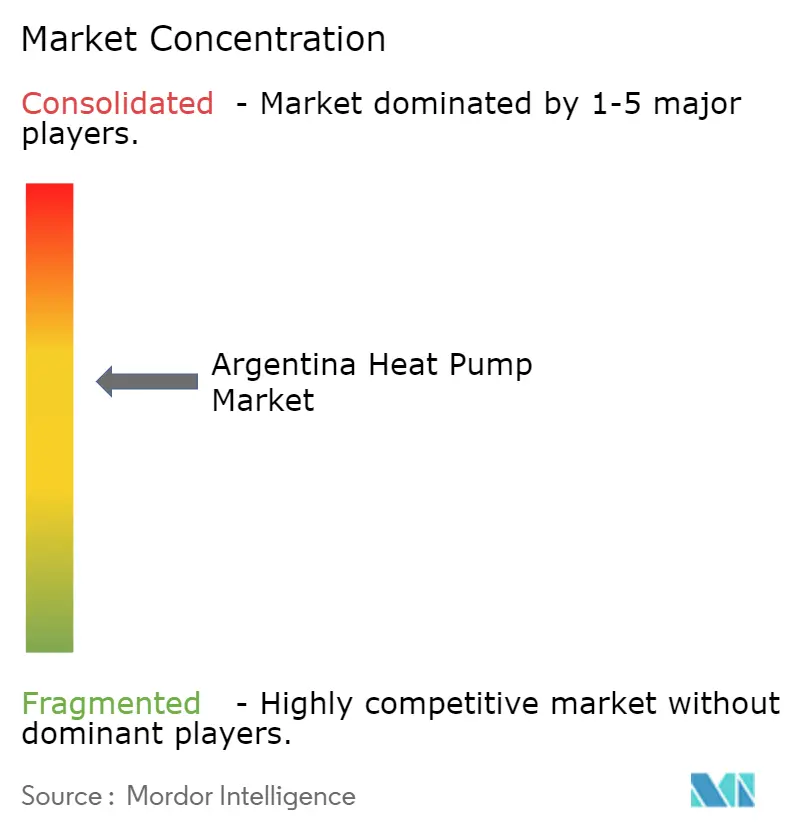

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Heat Pump Market Analysis by Mordor Intelligence

The Argentina heat pump market size is expected to grow from USD 427.86 million in 2025 to USD 448.34 million in 2026 and is forecast to reach USD 552.72 million by 2031 at a 4.27% CAGR over 2026-2031. Strong appliance-financing programs, tighter minimum energy-performance rules and a warm-temperate climate underpin demand, even while peso volatility and fossil-gas priorities temper near-term momentum. Manufacturers accelerate local assembly of R-32 inverter models, helping the Argentina heat pump market overcome import duties and expand residential retrofits. Provincial on-bill incentives broaden purchasing power, and updated building codes encourage developers to specify integrated heat-pump and photovoltaic packages. Competitive intensity remains moderate, with multinational brands leveraging training hubs and certified-installer networks to protect share against regional distributors that compete on flexible financing outside the Buenos Aires-Rosario-Córdoba axis.

Key Report Takeaways

- By installation, retrofit projects commanded 60.43% of the Argentina heat pump market in 2025, while new installations are projected to expand at a 4.57% CAGR through 2031.

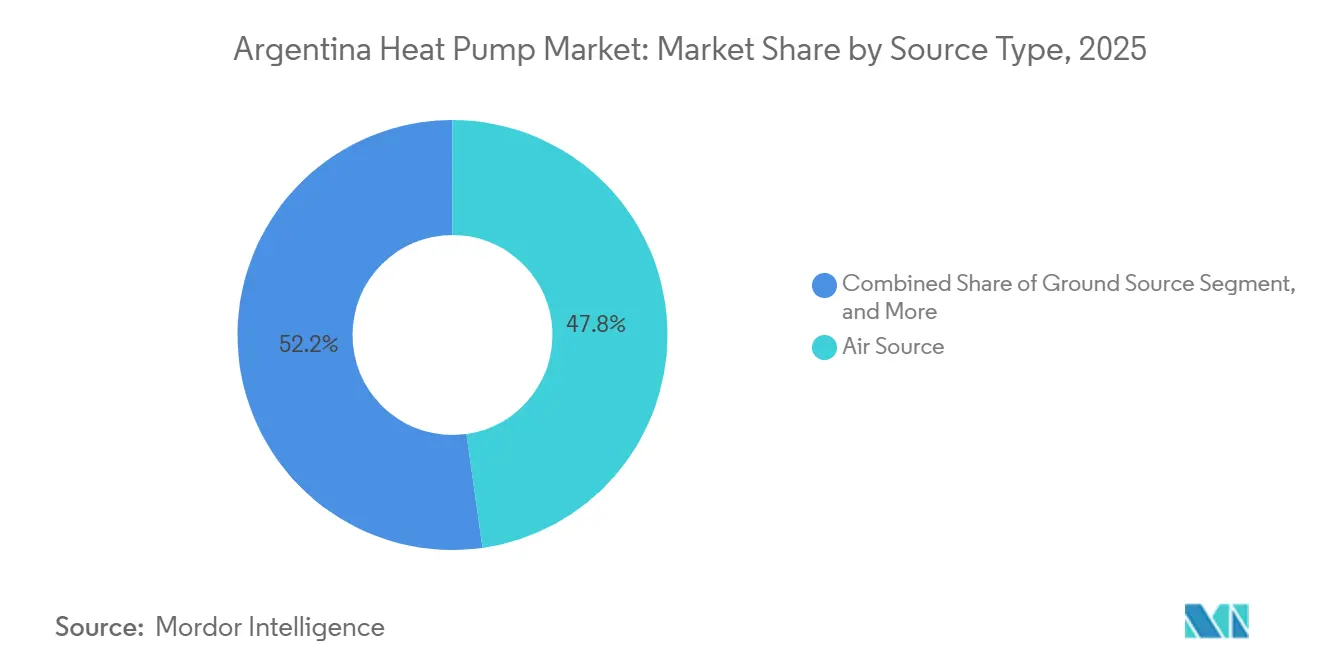

- By source type, air-source units held 47.78% of the Argentina heat pump market share in 2025, and hybrid systems are advancing at a 5.41% CAGR during 2026-2031.

- By technology, air-to-air systems led with 46.31% revenue share in 2025, whereas air-to-water is forecast to record a 5.02% CAGR to 2031.

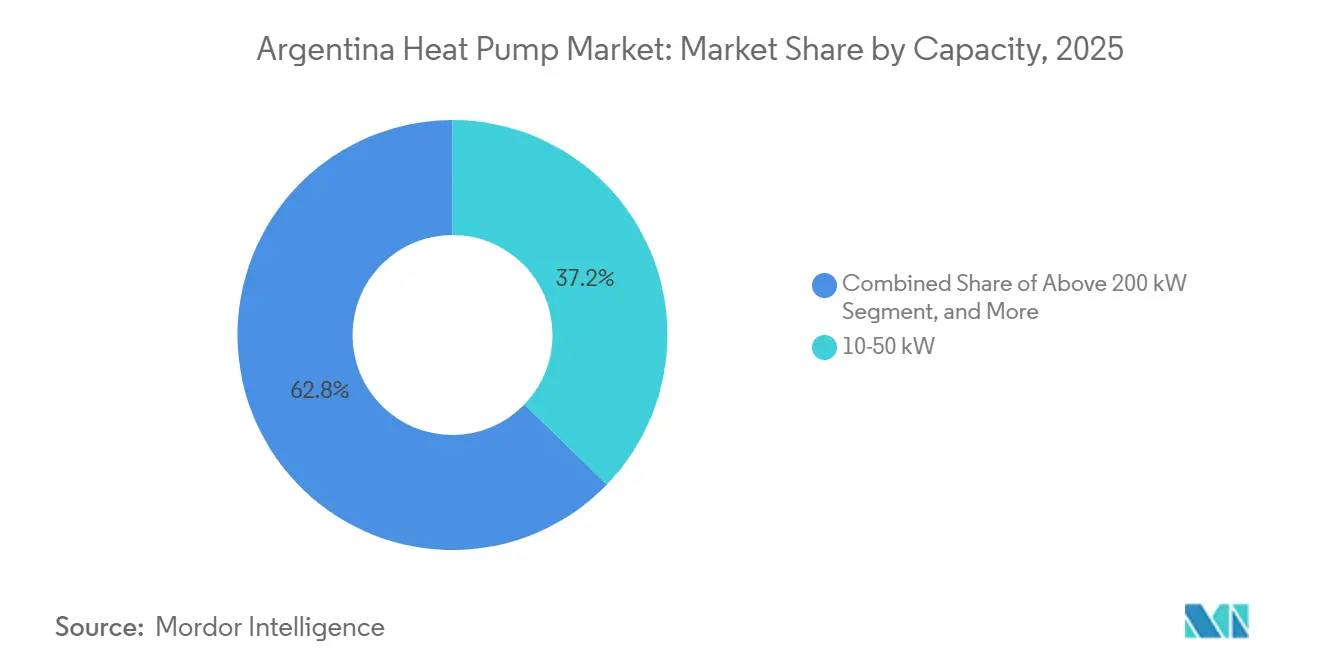

- By capacity, the below 10 kW bracket is set to grow at a 5.78% CAGR between 2026-2031, outpacing the overall Argentina heat pump market size.

- By application, domestic hot-water solutions are expected to expand at a 4.86% CAGR, even as space heating maintained 41.94% revenue share in 2025.

- By end user, industrial demand is projected to rise at a 4.38% CAGR, supported by mining and data-center investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives for Building-Sector Decarbonization | +1.2% | National, early gains in Buenos Aires, Córdoba, Santa Fe | Medium term (2-4 years) |

| Rapid HVAC Electrification in Warm-Temperate Zones | +0.9% | Buenos Aires-Rosario-Córdoba corridor, Litoral region | Short term (≤ 2 years) |

| Declining Heat-Pump Hardware Costs From Asian Scale Manufacturing | +0.7% | Import channels, Tierra del Fuego assembly | Medium term (2-4 years) |

| Surge in On-Bill Financing Programs From Provincial Utilities | +0.5% | Mendoza, Buenos Aires province, pilots in Córdoba and Santa Fe | Long term (≥ 4 years) |

| Advent of Heat-Pump-Ready Smart-Grid Tariffs by CAMMESA | +0.4% | National rollout starting Greater Buenos Aires | Long term (≥ 4 years) |

| Expanding EU Carbon-Border Adjustment Pressure on Exporters | +0.3% | Steel and aluminum hubs in Buenos Aires, Santa Fe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Building-Sector Decarbonization

Federal Resolution 202/2024 lets households spread payments for A+ inverter units over 24 zero-interest installments, shrinking the up-front gap versus gas-heater combinations.[1]SOMOS JUJUY, “El Gobierno lanzó créditos para bajar el consumo energético,” somosjujuy.com.ar Minimum COP and SEER thresholds introduced in 2025 accelerate the retirement of low-efficiency equipment, so certified inverter heat pumps become the default choice across the Argentina heat pump market.[2]BOLETINOFICIAL.GOB.AR, “Resolución 426/2025,” boletinoficial.gob.arProvincial grants, such as Mendoza’s Activa IV covering 40% of eligible costs up to ARS 15 million (USD 17,241), give wineries and cold-chain operators a practical route to hydronic retrofits.[3]GUAYMALLEN, “Eficiencia Energética - Financiamiento Guaymallén,” guaymallen.gob.ar Together, these measures lift unit sales and add a visible 1.2% to the long-term growth trajectory.

Rapid HVAC Electrification in Warm-Temperate Zones

Subsidized summer blocks of up to 550 kWh for very-hot NEA provinces cut marginal electricity cost, favoring air-source models that sustain seasonal COP above 3.4.[4]EL DESTAPE, “Nuevas tarifas eléctricas,” eldestape.com.ar Media cost-comparisons underline that a reversible inverter drawing 1 kWh delivers threefold heat output over resistance heaters, reinforcing consumer preference. Quick payback in Buenos Aires apartments propels word-of-mouth adoption, adding nearly a full point to forecast CAGR for the Argentina heat pump market.

Declining Heat-Pump Hardware Costs from Asian Scale Manufacturing

Local R-32 production started in 2024 and now retails at ARS 827,065-893,764 (USD 951-1,027) for a 3,000 frigorías split, undercutting imports despite an 82% tax burden.[5]ARQA EMPRESAS, “Midea pionero en la fabricación,” arqa.com UNIDO audits show inverter share already tops 70% at key Tierra del Fuego plants, proving that scaled Asian supply chains compress landed costs. This shift delivers a 0.7% uplift to the Argentina heat pump market CAGR by closing the affordability gap for first-time buyers.

Surge in On-Bill Financing Programs from Provincial Utilities

Mendoza’s non-reimbursable grant framework ties disbursements to documented energy savings, letting heat-pump projects qualify alongside efficient motors and solar heaters. World Bank indicators flag an absence of national on-bill programs, so provincial pilots become critical to mainstreaming finance for households without access to cheap bank credit. Over the forecast horizon, these mechanisms add 0.5% to sector growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Cost Versus Split-AC Plus Gas-Heater Combinations | -0.8% | Provinces with subsidized gas | Short term (≤ 2 years) |

| Elevated Grid-Carbon Intensity Reducing Net-Zero Credentials | -0.5% | Regions served by thermal generation | Medium term (2-4 years) |

| Peso Volatility Raising Import Component Prices | -0.4% | National | Short term (≤ 2 years) |

| Installer Shortage Outside Primary Metro Areas | -0.3% | NEA, NOA, Patagonia interiors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Cost Versus Split-AC Plus Gas-Heater Combinations

A cooling-only split paired with a gas heater costs ARS 500,000-1,250,000 (USD 575-1,437), whereas a reversible inverter of similar capacity starts near ARS 827,000 (USD 951) before installation. Labor and materials add USD 207-299, and copper shortages during exchange-rate spikes push quotes higher with 24-hour validity. Even with zero-interest loans, unbanked households face cash-flow hurdles, clipping 0.8% from the Argentina heat pump market growth outlook.

Elevated Grid-Carbon Intensity Reducing Net-Zero Credentials

Natural-gas generation still represents roughly two-thirds of national electricity, so the carbon advantage of heat pumps versus condensing boilers remains modest.[6]IEA, “Argentina - Countries & Regions,” iea.org Limited firm-capacity awards in CAMMESA’s 2025 renewable auction expose transmission bottlenecks, raising the chance that new electric demand is met by thermal peakers. This dynamic subtracts 0.5% from the potential CAGR, as ESG-minded commercial buyers delay conversion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air-Source Dominance Reflects Simple Installation

Air-source units secured 47.78% of 2025 revenue within the Argentina heat pump market, thanks to mild winters that keep efficiencies high and because rooftop or wall-mount installations require no excavation. Hybrids combining a heat pump with resistance or gas backup expand 5.41% a year, giving supermarkets and offices a safety net during peak-price evenings. Meanwhile, water-source remains niche for industrial plants with cooling towers, and ground-source trails due to drilling cost and urban space limits.

Air-source popularity is reinforced by factory-certified training hubs in Buenos Aires that standardize installation quality. Daikin’s proprietary leak-free pipe joints and LG’s Monobloc outdoor chassis shorten project timelines, a decisive factor for apartment retrofits. As tariff reform narrows gas subsidies, households view air-source as the least-cost all-season comfort option, keeping this configuration the volume engine of the Argentina heat pump market.

By Technology: Air-To-Water Gains Traction For Boiler Swaps

Air-to-air systems led with 46.31% share in 2025, yet air-to-water is projected to log a 5.02% CAGR, driven by hospitals, hotels and multifamily towers that can reuse hydronic loops. Retrofits avoid radiator replacement where low-temperature units suffice, containing capex and unlocking Banco Nación credit lines. Suppliers market pre-charged outdoor units that connect only water pipes indoors, so licensed plumbers can perform most tasks without refrigerant certification, easing the installer bottleneck beyond the core corridor.

Second-generation controls allow dual-temperature operation for underfloor heating and fan-coil cooling, matching developer demand for energy-label upgrades under PRONEV. With residential building codes edging toward electrified baselines, air-to-water technology positions itself as the boiler-replacement standard within the Argentina heat pump market.

By Capacity: Entry-Level Systems Propel Residential Uptake

Systems rated below 10 kW accounted for the highest unit shipments in 2025 and are projected to expand at a 5.78% CAGR through 2031 as apartments under 90 m² opt for single-room ductless units that qualify for zero-interest Banco Nación credit. Packages priced between ARS 500,000 and ARS 1,250,000 (USD 575-1,437) cover most middle-income budgets and include Wi-Fi controls that track power use within subsidy caps. The 10-50 kW range made up 37.23% of 2025 revenue because offices, clinics and schools deploy modular VRF arrays that scale up to 78 HP without structural changes.

Demand above 50 kW centers on hospitals, hotels and small industrial plants seeking simultaneous heating and cooling. The USD 116,092 retrofit at Hospital Pasteur illustrates how public agencies bundle multiple 60 kW units to cover intensive care wings without boiler downtime. Above 200 kW installations remain rare but large mining and data-center projects now ask vendors for ammonia or CO₂ heat pumps delivering 80 °C process water, signaling future growth for the top capacity tier. Product-line breadth across all brackets enables leading brands to preserve Argentina heat pump market share as building owners upgrade over time.

By Application: Domestic Hot Water Gains Momentum as Gas Prices Spike

Space heating generated 41.94% of 2025 revenue because split inverters double as heaters during mild winters. The gas-tariff surge above 1,000% in 2024 narrowed operating-cost gaps, prompting hotels and condominiums to embrace hybrid water heaters that slash energy use 70%.[7]RHEEM ARGENTINA, “Termotanque por bomba de calor,” rheem.com.ar Growth in domestic-hot-water projects at a 4.86% CAGR outpaces total Argentina heat pump market growth, reflecting urgent replacement of aging gas tanks.

Cooling remains the dominant summer need in NEA and NOA where the Secretaría de Energía raised subsidized caps to 550 kWh, encouraging reversible splits that handle both seasons. Industrial process-heat adoption, while smaller in absolute value, advances as lithium brine plants and dairy processors reuse waste heat to hit sustainability targets. Pool-heating retrofits such as the twin 80 kW rooftop units at AquaVida deliver 26% monthly savings and validate payback cases in leisure facilities.

By End User: Mining and Data Infrastructure Drive Industrial Upswing

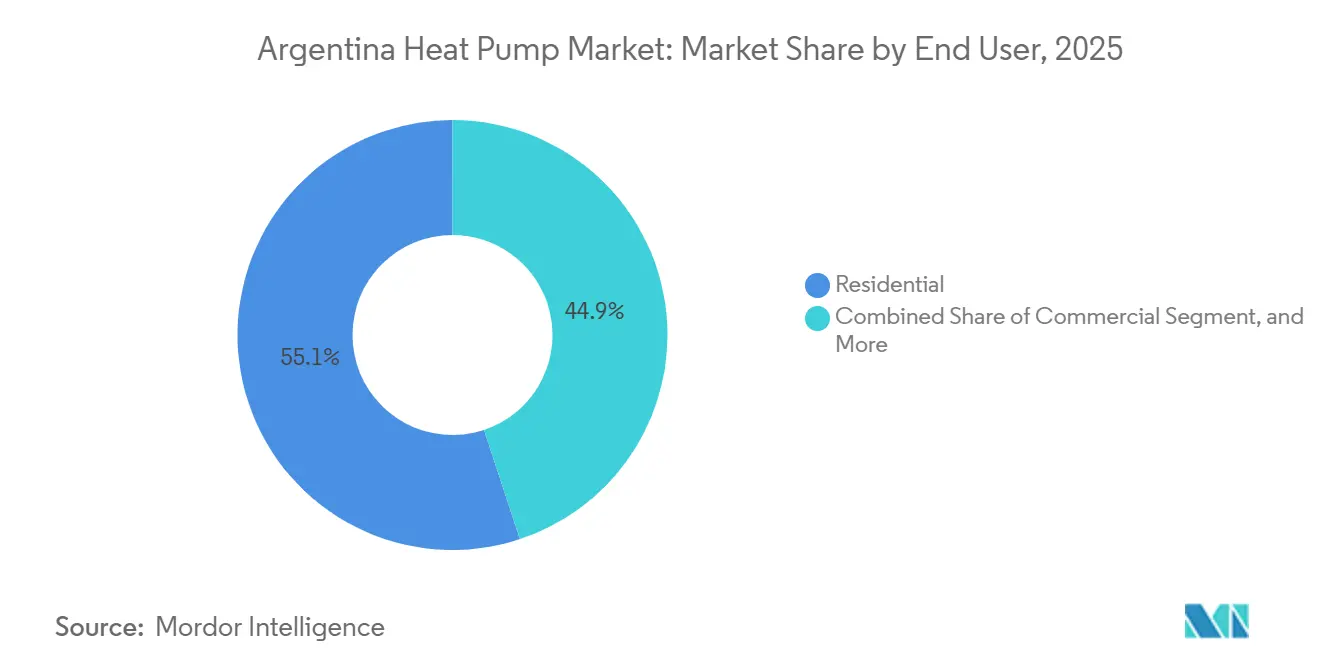

Residential customers contributed 55.09% of 2025 demand, yet an industrial CAGR of 4.38% through 2031 signals diversification. The Large Investment Incentive Programme draws Rio Tinto and Glencore into remote provinces where off-grid renewables pair with high-temperature heat pumps for ore processing. Commercial buildings adopt VRF systems to reduce energy bills during peso inflation, helping maintain the Argentina heat pump market size trajectory.

OpenAI’s USD 25 billion Stargate data-center plan in Patagonia will require high-capacity chillers that can also export waste heat to nearby towns, creating a showcase for multi-megawatt equipment. Public health ministries in Córdoba and Santa Fe pursue PRONEV-aligned retrofits, adding steady public-sector volume.[8]PEEB, “Revitalizing Healthcare in Argentina,” peeb.build Across segments, installer training programs by Daikin and LG ensure service quality and support repeat purchases.

By Installation: Retrofits Lead but Code-Driven New Builds Accelerate

Retrofit activity captured 60.43% of 2025 revenue because Argentina’s pre-2017 building stock still relies on separate cooling and gas appliances. Air-to-air swaps are the quickest path, with Monobloc options minimizing indoor work. Owners in Buenos Aires compress payback to four cooling seasons by applying electricity-subsidy caps and Banco Nación terms.

New-build penetration rises at a 4.57% CAGR as developers target higher PRONEV labels to unlock green mortgages. Pairing rooftop PV with heat pumps boosts the label score and limits tariff exposure, making integrated designs popular in gated communities around Córdoba. Code compliance and resale premiums will steadily lift the Argentina heat pump market share of new construction through 2031.

Geography Analysis

Greater Buenos Aires accounts for over half of national revenue because distributor hubs, financing offices and installer capacity are concentrated in the capital. Consumers benefit from Daikin’s Vicente López academy and Johnson Controls-Hitachi’s new USD 15 million training center that certifies 400 technicians yearly. Córdoba and Santa Fe anchor public-sector demand, as PEEB studies fund hydronic retrofits in provincial hospitals exposed to heatwaves. Their combined pipeline reinforces a balanced regional mix.

Mendoza leverages Activa IV grants covering 40% of energy-efficiency equipment to retrofit wineries and cold-storage rooms, proving that provincial incentives can spur project clusters outside the core corridor. NEA and NOA provinces, classified as “very hot,” gain higher subsidized kWh blocks, heightening affordability for reversible splits despite lower median income.

Patagonia remains a long-term hotspot due to abundant wind resources and the proposed Stargate data-center hub, yet transmission congestion limits near-term installations. Tierra del Fuego’s assembly zone grew inverter production above 70% at several plants, cutting logistics cost and anchoring supply for southern provinces. Interior regions suffer installer shortages, but nationwide Asociación Argentina del Frío programs begin to close the skills gap.

Competitive Landscape

Five multinationals, Daikin, Midea, Johnson Controls-Hitachi, LG and Carrier, command roughly 60-65% of the Argentina heat pump market, keeping concentration moderate. Daikin positions Tightfit piping for leak-free retrofits in vertical housing, while a showroom in Vicente López demos full-system solutions. Johnson Controls-Hitachi ships Mercosur-qualified VRF units from São Paulo exempt from 35% duties and pairs them with cloud commissioning apps that shrink site visits.

Midea’s R-32 line assembled in Tierra del Fuego retails below imported equivalents, winning price-sensitive households yet meeting COP 3.61 mandates. LG promotes R-290 Monoblocs and industrial ammonia units to differentiate on ultra-low GWP, targeting hotel chains that value ESG scores. Carrier, through BGH Fueguina, bundles financing with Banco Galicia to penetrate smaller cities.

Niche Chinese entrants such as SPRSUN secure leisure contracts by guaranteeing 12-month payback for pool heating. Local integrators offer turnkey solar plus heat-pump packages that hedge peso inflation by cutting grid reliance. Vendor competition now shifts from headline efficiency to financing creativity and installer loyalty, shaping Argentina heat pump market dynamics through 2031.

Argentina Heat Pump Industry Leaders

Daikin Industries Ltd.

Mitsubishi Electric Corporation

Carrier Global Corporation

Johnson Controls International plc

Bosch Thermotechnology (Robert Bosch GmbH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Córdoba installed 60 VRV heat-pump units at Hospital Regional Luis Pasteur under a USD 116,092 procurement, upgrading pediatrics and maternity wings.

- January 2026: Decreto 943/2025 unified power and gas subsidies, setting new consumption caps that steer households toward efficient electric heating.

- October 2025: Resolution 426/2025 raised minimum COP to 3.40 and SEER to 5.60 for splits up to 10.5 kW, accelerating low-efficiency phase-outs.

- September 2025: Johnson Controls won a 42 MW ammonia heat-pump order for Zürich’s district network, cutting emissions 60%.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Argentina's heat pump market as the annual value of new air-source, water-source, ground-source, hybrid, and exhaust-air units sold for space conditioning or sanitary hot water across residential, commercial, industrial, and institutional premises. Refurbished equipment, purely air-conditioning systems, aftermarket parts, and installation labor fees lie outside this scope.

Standalone chiller modules, fossil-fueled boilers, rooftop packaged AC units, and portable room heaters are not counted.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed regional distributors, installer guilds, and utility energy-efficiency officers spanning Buenos Aires, Cordoba, Mendoza, and Santa Fe. Dialogues validated typical selling prices, seasonal demand swings, refrigerant transition timelines, and the share of retrofit versus new-build projects.

Desk Research

We began by mapping Argentina's building stock, energy-use balance, and appliance trade through open datasets such as INDEC foreign-trade tables, Secretaria de Energia efficiency bulletins, IEA energy indicators, International Heat Pump Association shipment notes, and World Bank construction permits. Company filings accessed via D&B Hoovers, customs micro-data from Volza, and reputable press reports added price points and channel insights. These sources illustrate but do not exhaust the references our analysts reviewed.

Market-Sizing & Forecasting

A top-down 'device stock and heat demand' model begins with dwelling counts, floor-area growth, climatic degree-days, and prevailing penetration rates, which are then valued using average selling prices gathered from distributor quotes. Supplier roll-ups and installer channel checks act as a selective bottom-up control to fine-tune totals. Key variables include residential renovation pace, utility electricity-to-gas price spread, import tariff changes, urbanization, and inverter adoption rates. Forecasts deploy multivariate regression blended with scenario analysis to project each driver through 2030, and gap-filled bottom-up estimates where official data lag.

Data Validation & Update Cycle

Outputs face variance checks against historic trade volumes, IEA efficiency targets, and random distributor invoice audits before internal peer review. Mordor refreshes this dataset yearly, issuing interim adjustments when subsidy schemes, currency shocks, or major capacity additions materially shift the baseline.

Why Mordor's Argentina Heat Pump Baseline Inspires Confidence

Published figures often diverge because studies anchor on different scopes, reference years, or valuation layers.

By aligning device definitions with local tariff codes and reconciling factory-gate values with channel mark-ups, Mordor delivers a balanced picture users can replicate.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 428.4 million (2025) | Mordor Intelligence | - |

| USD 533 million (2024) | Regional Consultancy A | Includes pool and process chillers, excludes AC units, yet applies uniform 20 % importer margin, inflating value |

| USD 147 million (2023) | Trade Statistic B | Captures only declared imports, omits locally assembled output and in-country distribution mark-ups |

The comparison shows how broader equipment coverage or narrower import-only views skew totals. Mordor's disciplined scope selection, dual-angle modeling, and annual refresh cadence therefore provide the most dependable baseline for planners weighing manufacturing, policy, or investment moves.

Key Questions Answered in the Report

What is the forecast value of Argentina heat pump market by 2031?

It is projected to reach USD 552.72 million.

How fast will domestic hot-water projects grow to 2031?

They are projected to advance at a 4.86% CAGR as gas tariffs rise.

Which provinces benefit most from higher subsidized kWh caps?

NEA and NOA provinces such as Formosa and Chaco receive up to 550 kWh in summer.

What is driving industrial adoption of heat pumps?

Expansion of lithium and copper mines plus data-center cooling needs in Patagonia.

Who leads local assembly of R-32 inverter units?

Midea and Carrier Fueguina operate large-scale lines in Tierra del Fuego.

Why are air-to-water systems important for new construction?

They integrate with hydronic loops and raise PRONEV energy labels, unlocking green mortgages.

Page last updated on: