Kuwait Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

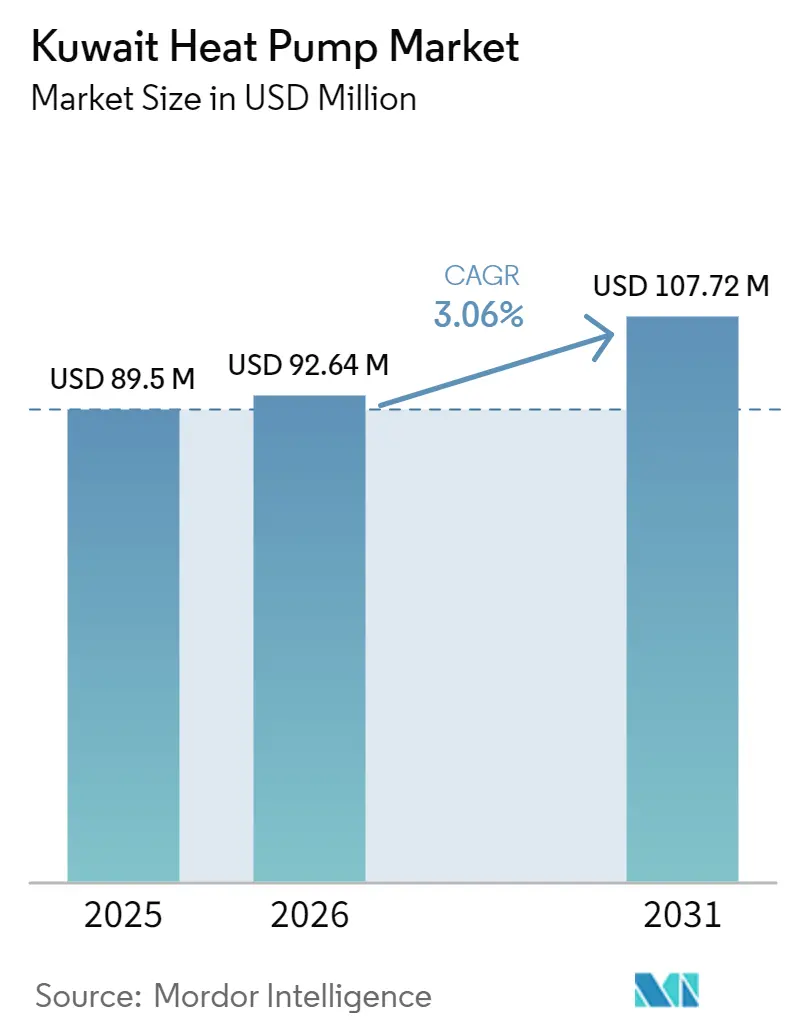

| Base Year Market Size (2025) | USD 89.5 Million |

| Market Size (2026) | USD 92.64 Million |

| Market Size (2031) | USD 107.72 Million |

| Growth Rate (2026 - 2031) | 3.06% CAGR |

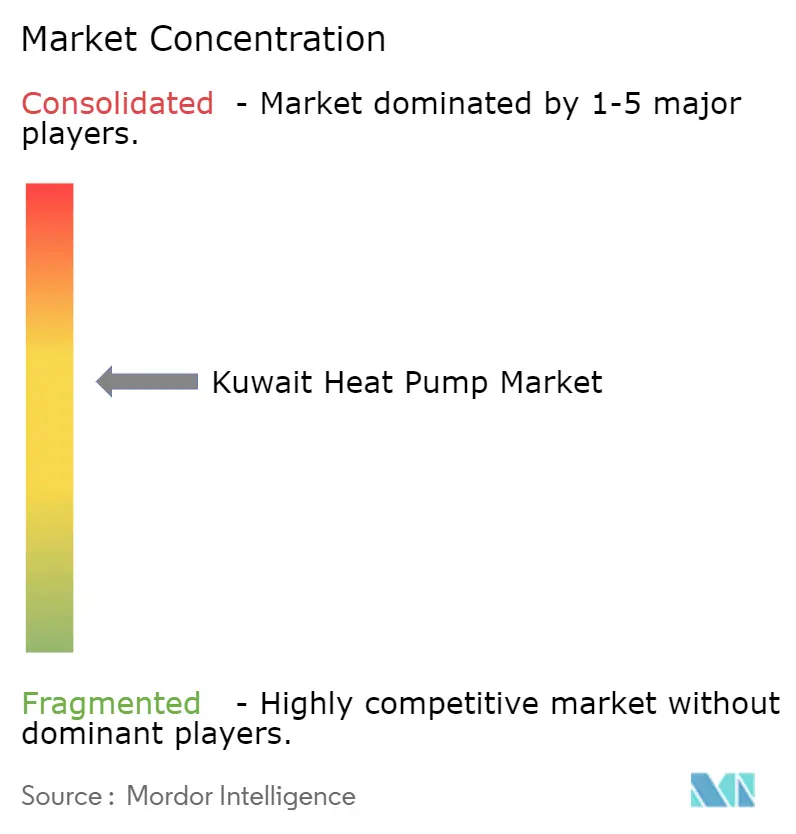

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait Heat Pump Market Analysis by Mordor Intelligence

The Kuwait heat pump market size is expected to increase from USD 89.5 million in 2025 to USD 92.64 million in 2026 and reach USD 107.72 million by 2031, growing at a CAGR of 3.06% over 2026-2031. Structural subsidy reforms, the Kigali-driven hydrochlorofluorocarbon (HCFC) phase-out, and mega-project procurement are gradually offsetting Kuwait’s legacy dependence on low-cost natural gas and ultracheap residential electricity. Corporate and public developers now specify reversible, high-coefficient-of-performance systems for new data centers, district-cooling networks, and petrochemical complexes, while expatriate households respond to differentiated tariffs by adopting small-capacity units. Original equipment manufacturers (OEMs) are localizing manufacturing in the Gulf Cooperation Council (GCC) to offer high-ambient-rated models, shorten lead times, and bundle lifecycle service contracts that de-risk ownership for commercial buyers. However, elevated upfront capital expenditure, technician shortages, and corrosion-intensive operating conditions still temper the pace at which the Kuwait heat pump market transitions away from traditional gas boilers.

Key Report Takeaways

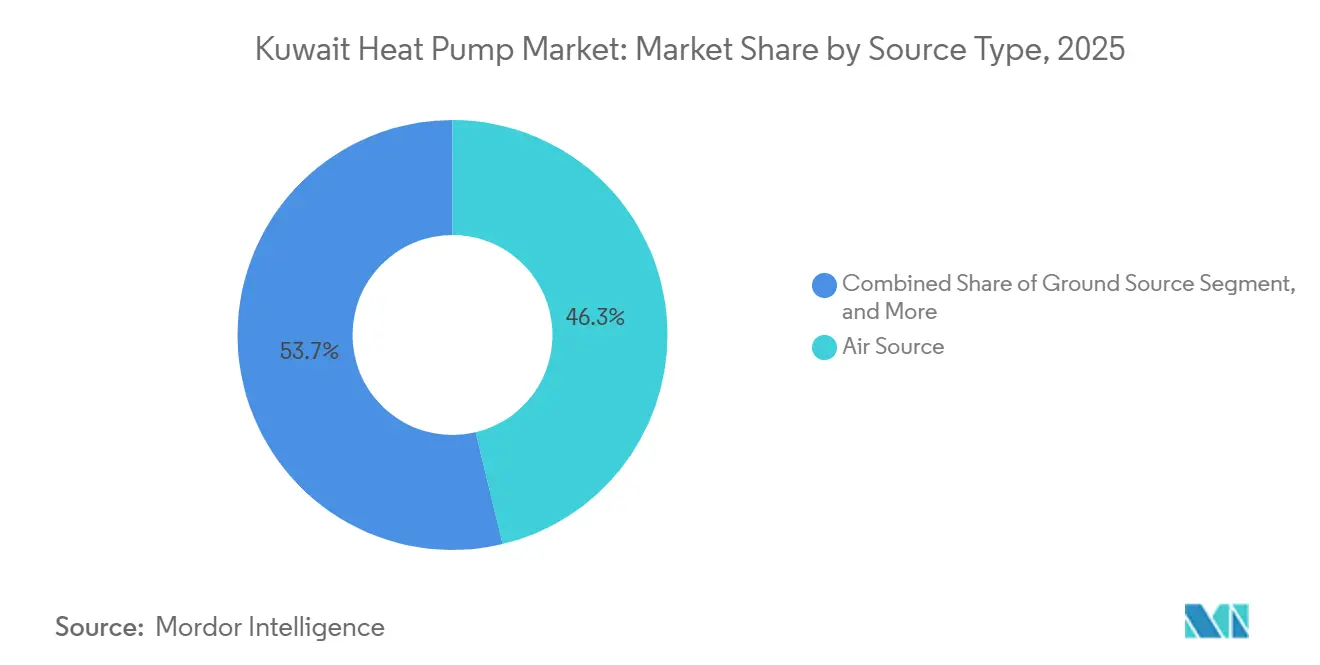

- By source type, air source held 46.27% of Kuwait heat pump market share in 2025, while hybrid systems are projected to expand at a 4.02% CAGR through 2031.

- By technology, air-to-air captured 37.93% Kuwait heat pump market size in 2025; ground-to-water is the fastest-growing technology at a 3.72% CAGR over 2026-2031.

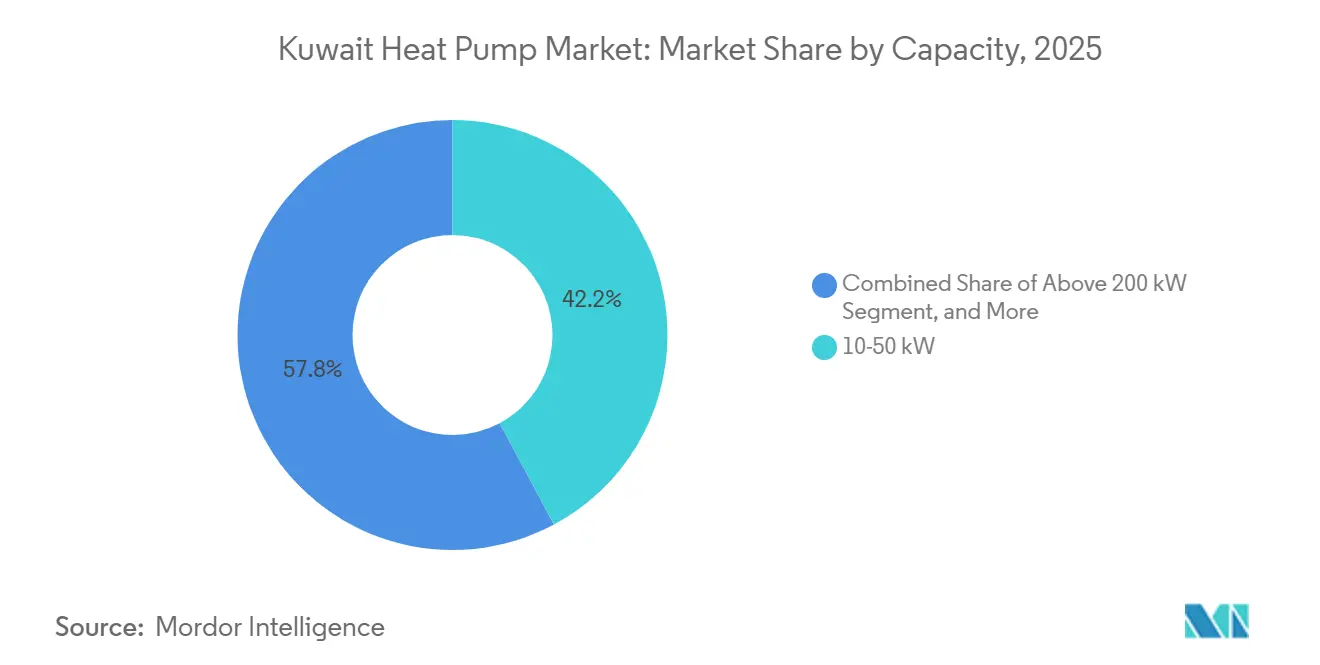

- By capacity, the 10-50 kW band accounted for 42.18% of Kuwait heat pump market share in 2025, whereas below-10 kW units lead growth at 3.37% CAGR through 2031.

- By application, space cooling dominated with 54.08% revenue in 2025; industrial and process heating is forecast to expand at a 3.86% CAGR to 2031.

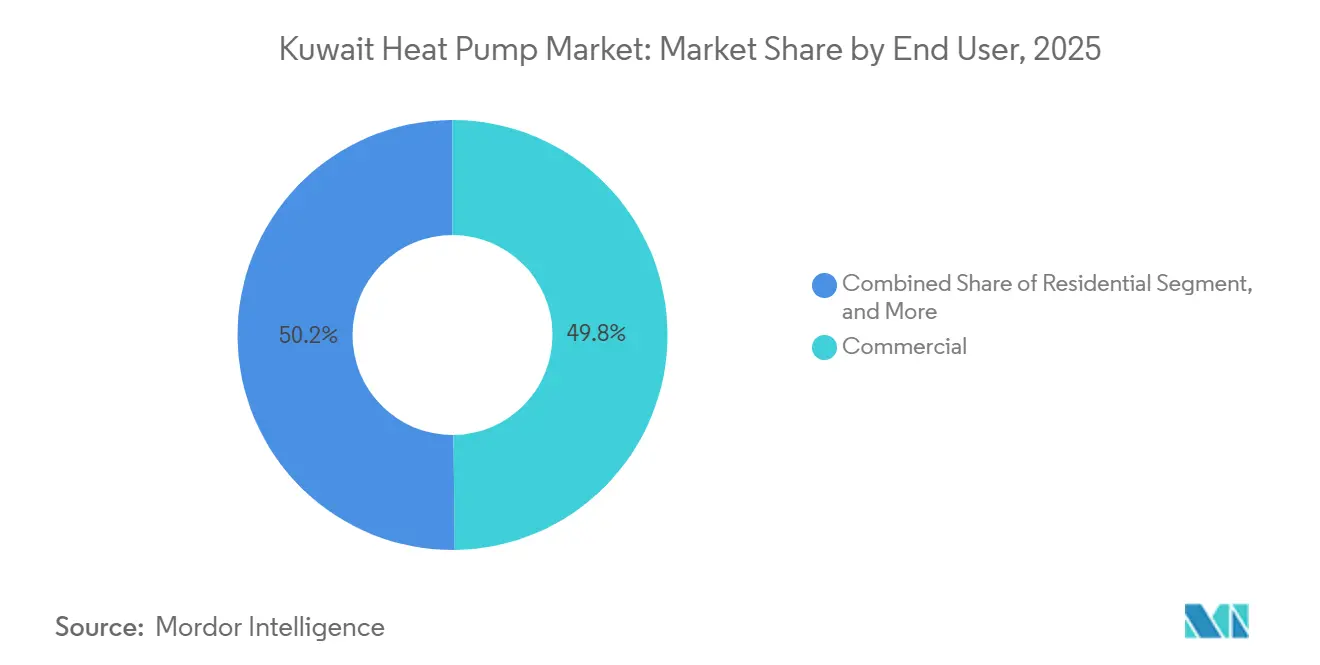

- By end user, commercial facilities commanded 49.83% share in 2025, yet industrial installations record the highest projected CAGR at 3.48% during 2026-2031.

- By installation, retrofit accounted for 52.77% of 2025 demand, while new installation is set to grow at 3.21% CAGR on the back of Silk City and Shagaya Phase III projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kuwait Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kuwait Vision 2035 clean-energy mandates accelerating heat-pump adoption | +0.8% | National, strongest in Silk City and Shagaya zones | Medium term (2-4 years) |

| Escalating data-center and petrochemical cooling loads demanding high-COP reversible systems | +0.7% | Industrial corridors and KNPC sites | Short term (≤ 2 years) |

| Higher expatriate electricity tariffs improving heat-pump lifecycle economics | +0.5% | Expatriate-dense residential districts | Short term (≤ 2 years) |

| HCFC-based chiller phase-out in 2026 triggering retrofit wave | +0.6% | Nationwide commercial and industrial stock | Short term (≤ 2 years) |

| Mega-hospitality projects fueling HVAC demand | +0.4% | Northern Economic Zone | Long term (≥ 4 years) |

| District-cooling subsidies tied to renewable targets | +0.3% | Kuwait Vision 2035 projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Kuwait Vision 2035 Clean-Energy Mandates Accelerating Heat-Pump Adoption

Kuwait Vision 2035 commits the country to source 15% of electricity from renewables by 2030 and achieve net-zero emissions by 2050. The resulting procurement standards favor electrically driven, desert-certified chillers and reversible systems able to shift loads when solar output peaks. The 500 MW Al Dibdibah solar tender issued in 2025 exemplifies how power-purchase-agreement structures embed heat-pump compatibility into greenfield plants.[1]Eurovent Certification, “Eurovent launches Desert Certification for HVAC systems in GCC region,” refindustry.com Developers also earn fast-track permitting if they specify high-coefficient-of-performance equipment that can shift load when midday photovoltaic output peaks. These policy carrots shorten payback for large-tonnage units even without new subsidies. As master plans move from concept to construction after 2027, the mandate effect will ripple across commercial, industrial, and mixed-use projects, anchoring steady demand through 2031.

Escalating Data-Center and Petrochemical Cooling Loads Demanding High-COP Reversible Systems

Hyperscale data hubs and the Kuwait National Petroleum Company’s (KNPC) integrated refining complexes need year-round, high-reliability cooling. OEMs such as LG have introduced oil-free magnetic-bearing compressors that improve part-load efficiency, while KNPC pilot projects capture low-grade waste heat for preheating feedstock, replacing auxiliary gas boilers. These industrial loads are less sensitive to retail tariff politics, giving the Kuwait heat pump market a stable demand anchor.[2]Kuwait National Petroleum Company, “Corporate Sustainability Report 2025,” knpc.com Petrochemical plants capture condenser waste heat and upcycle it for feedstock preheating, trimming natural-gas use in process heaters. Because these industrial buyers run captive maintenance teams, technician shortages pose less risk, enabling quicker procurement cycles than the commercial segment. The resulting anchor orders in the 50-200 kW and 200 kW-plus classes cushion market growth against any residential soft patch.

Higher Expatriate Electricity Tariffs Improving Heat-Pump Lifecycle Economics

Since 2017, expatriate households have faced higher electricity prices than Kuwaiti citizens, converting energy savings into tangible payback for below-10 kW and 10-50 kW units. Lifecycle analyses show a 5-7-year payback window, prompting residential installers to market heat-pump domestic-hot-water packages alongside air-conditioning retrofits. Installers now bundle financing, maintenance, and hot-water add-ons to sweeten the deal, and sales of below-10 kW units have begun to outpace standard air conditioners in expatriate districts. Although tariff reform is politically sensitive, every additional fils per kilowatt-hour widens the savings gap in favor of electric systems. This customer segment therefore delivers a predictable, retail-driven growth stream through 2031.

HCFC-Based Chiller Phase-Out in 2026 Triggering Retrofit Wave

Kuwait’s 2024 ratification of the Kigali Amendment bans HCFC chillers from 2026, forcing building owners to retire hundreds of aging machines simultaneously. OEMs responded with low-GWP models that drop into existing plant rooms, complete with factory-filled R-1234ze or R-515B refrigerants that clear compliance hurdles on day one. Because fines apply after the deadline, procurement teams accelerated tender timelines, front-loading spend that might have trickled into the next decade. Technician training remains a bottleneck, yet owners accept higher service fees to avoid penalties. The rush inflates near-term unit shipments and establishes a larger installed base that will eventually feed replacement and service revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidized Natural-Gas Boilers Undercutting Short-Term ROI | -0.6% | Citizen-majority homes and micro-businesses | Short term (≤ 2 years) |

| Saline Desert Environment Raising O&M Costs | -0.4% | Coastal and refinery zones | Medium term (2-4 years) |

| Shortage of Licensed Refrigeration Technicians | -0.3% | Commercial and industrial facilities | Short term (≤ 2 years) |

| High Upfront CAPEX Amid Subsidy Uncertainty | -0.2% | Residential and small commercial | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Subsidized Natural-Gas Boilers Undercutting Short-Term ROI

Citizens still pay only 0.7 cents per kilowatt-hour for electricity and enjoy below-cost natural-gas pricing, allowing a basic boiler-plus-air-conditioner package to win on first cost in most villas.[3]Baker Institute for Public Policy, “Kuwait’s Electricity Subsidy Reform,” bakerinstitute.org As long as this subsidy remains, payback on a reversible system stretches beyond a decade for citizen households, chilling demand in the largest residential segment. Small shops and cafés face the same math, so they often postpone upgrades until an existing unit fails. The split in tariff treatment therefore fragments the market, leaving OEMs to chase expatriate and industrial buyers while lobbying for broader reform. Unless pricing structures change, residential penetration will lag commercial and industrial adoption.

Saline Desert Environment Drives Up Ownership Costs

Ambient temperatures above 50 °C and salt-laden coastal air corrode coils and cabinets, shortening equipment life versus temperate markets. Eurovent’s 2025 Desert Certification tests at 46 °C and 52 °C and requires ISO 12944 C5-M coatings, but certified model availability is still limited. Operators budget for extra coil cleanings, refrigerant top-ups, and fan-motor replacements, adding roughly 10-15% to annual maintenance outlays. Higher service costs lengthen payback, especially for mid-sized commercial sites that lack in-house maintenance crews. Until locally built, desert-rated units dominate catalogs, corrosion will remain a drag on growth and a key variable in total-cost-of-ownership models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Configurations Hedge Infrastructure Transition

Air source units commanded 46.27% of Kuwait heat pump market share in 2025, mainly because they dovetail with rooftop and split-system layouts that dominate existing buildings. Facility owners appreciate the limited structural work, quick commissioning, and familiar maintenance profile that these units bring. Hybrid configurations, which pair an air-source compressor with a backup gas boiler or solar loop, are projected to register the fastest 4.02% CAGR through 2031. Their appeal rests on flexibility: operators can toggle fuels when grid prices spike or when solar generation peaks at midday. This fuel-switching capability aligns with Kuwait Vision 2035 procurement rules that reward projects able to track renewable output.

Water-source machines remain niche because saline feedwater rapidly corrodes exchangers, although a few coastal desalination plants run closed-loop variants. Ground-source pilots in Silk City leverage master-plan budgets to absorb drilling costs, and stable subsurface temperatures cushion coefficient-of-performance swings during 50 °C summers. The combined growth of hybrid and ground-coupled options shows buyers moving toward incremental rather than abrupt electrification. As more developers specify desert-certified equipment that withstands 52 °C ambient conditions, air-source dominance will gradually ease, yet the technology will retain a sizable installed base for at least one replacement cycle.

By Technology: Ground-to-Water Gains in Process-Heating Applications

Air-to-air products delivered 37.93% of Kuwait heat pump market size in 2025 and remain the go-to choice for villa and small-office retrofits where ductwork is already in place. Expatriate households favor the format because tariff differentials shorten payback. Ground-to-water units, however, are the fastest-growing technology at a 3.72% CAGR, supplying 60-90 °C hot water that petrochemical and hospitality operators require. The ability to lift low-grade waste heat with minimal performance loss gives these systems a clear industrial edge.

Air-to-water machines feed hydronic loops in district-cooling schemes, while water-to-water solutions stay peripheral due to Kuwait’s chronic water scarcity. Recent localization in Saudi Arabia and the United Arab Emirates allows factory acceptance testing at 46 °C and 52 °C, easing buyer concerns over high-ambient reliability. As desert-certified models proliferate, specifiers are expected to shift tenders away from direct-expansion packages toward ground-coupled or air-to-water lines. This change will broaden supplier portfolios and tighten competition around part-load efficiency guarantees.

By Capacity: Below-10 kW Residential Segment Responds to Tariff Differentials

Units rated 10-50 kW captured 42.18% of Kuwait heat pump market share in 2025, serving small commercial blocks, clinics, and villa clusters. These customers often replace aging direct-expansion air conditioners with drop-in reversible packages that fit existing electrical capacity. Below-10 kW equipment, though smaller in value, posts the briskest 3.37% CAGR because expatriate tenants retrofit bedrooms and kitchens with mini-splits that cover cooling and domestic hot water.

Vendors sweeten deals with financing and service bundles that hold payback under seven years despite higher upfront cost. Above-200 kW machines appear mainly in refinery loops where a single order can top 1 MW, creating lumpy but high-margin revenue. The bifurcated pattern forces manufacturers to span the gamut from wall-mounted splits to containerized megawatt skids. Over time, stronger enforcement of desert-performance ratings may tilt the Kuwait heat pump market size mix toward midsize modular units that balance scalability with manageable service loads.

By Application: Industrial Process Heating Accelerates on Waste-Heat Recovery Mandates

Space cooling dominated with 54.08% of Kuwait heat pump market size in 2025, a natural result of extreme summer temperatures that drive electricity demand peaks. Conventional chillers still account for most rooftop systems, but reversible units now replace them when Kigali-related retrofits come due. Industrial and process heating is projected to rise at a 3.86% CAGR through 2031, propelled by refinery waste-heat recovery mandates.

High-temperature compressors lift 30-35 °C waste streams to usable 80 °C levels, slashing natural-gas consumption in desalination preheaters and petrochemical feedstock lines. Hotels and hospitals within Silk City also specify modular air-to-water packs that provide chilled water in summer and hot water year-round, boosting utilization rates. As these projects proliferate, process-heating revenue will carve out a larger slice of future growth even while space cooling retains numerical dominance. The shift underscores Kuwait’s gradual pivot from single-function chillers to dual-service, high-efficiency platforms.

By End User: Industrial Buyers Capitalize on Scale and Renewable Integration

Commercial buildings, offices, malls, clinics, held 49.83% Kuwait heat pump market share in 2025, anchored in Kuwait City’s dense urban core. Building managers prize reliability and quick maintenance turnaround, so OEMs position service centers along major ring roads. Industrial plants, however, are projected to log a 3.48% CAGR as Kuwait National Petroleum Company folds 2 GW of solar into refinery complexes and demands flexible electric heating.

Internal maintenance crews and 24-hour operation give industrial managers confidence to specify large-tonnage reversible chillers even with technician shortages nationwide. Residential uptake stays bifurcated: expatriate villas electrify, while most citizen households cling to gas boilers. This two-tier pattern shapes product roadmaps, with vendors tailoring after-sales support separately for heavy-industry hubs and residential installers.

By Installation: New Greenfield Projects Shift Mix Toward Long-Term Efficiency

Retrofits made up 52.77% of 2025 sales because Kigali rules force owners to replace HCFC chillers before 2026. The backlog feeds short-cycle demand for drop-in air-source packages and drives near-term Kuwait heat pump market size.

From 2027 onward, the construction of Silk City, Shagaya Phase III, and 170,000 planned housing units will tilt the mix toward greenfield systems designed around variable-renewable grids. These master plans embed thermal storage, high-efficiency hydronic plants, and smart controls at the blueprint stage, favoring suppliers that bundle financing with multi-year performance contracts. Consequently, retrofit share will taper while long-cycle infrastructure work becomes the prime driver of Kuwait heat pump market growth through 2031.

Geography Analysis

Kuwait City presently anchors the bulk of installed capacity because its commercial towers, airports, and data hubs run high cooling loads year-round. The metropolitan area’s concentration means OEM service centers cluster along the Fifth Ring Road, ensuring four-hour response times that de-risk ownership for building managers. Northern Economic Zone demand will accelerate once Silk City’s first residential parcels hand over in 2028, with master-plan guidelines requiring desert-certified heat pumps in every district-cooling plant.

Coastal industrial corridors near Al-Zour and Shuaiba favor closed-loop ground or seawater systems to shield exchangers from salt spray. Inland desert sites, by contrast, lean on air-source models fitted with oversized condensers that expel dust through self-cleaning fan shrouds. Regional localization in Saudi Arabia and the United Arab Emirates trims delivery schedules by up to six weeks, allowing contractors to align unit arrival with compressed GCC construction calendars and keeping Kuwait heat pump market share competitive against imported alternatives.

Western interior regions adjacent to the 500 MW Al Dibdibah solar park will form Kuwait’s first large cluster of grid-tied renewable generation.[4]Kuwait Authority for Partnership Projects, “Al Dibdibah Solar PV Project Tender Documents,” kapp.gov.kw Developers there intend to couple photovoltaic output with reversible chillers that shift loads toward mid-day solar peaks, an operational pattern that spreads electric demand more evenly across the network. Collectively, these geographic pockets create a mosaic of technical requirements, from corrosion-proof coatings on the coast to sand-resistant louvers inland, compelling vendors to certify multiple build variants within a single product family.

Competitive Landscape

Global brands such as Daikin, Mitsubishi Electric, LG Electronics, Carrier, Trane Technologies, Samsung, Bosch, and Johnson Controls dominate public tenders, supplying more than half of all commercial and industrial units ordered in 2025. Each has moved to localize production or sub-assembly within the GCC to secure high-ambient testing credentials and qualify for government procurement scorecards. Daikin broke ground on a Jeddah plant focused on large air-cooled chillers in December 2025, while Carrier partnered with Saudi Arabia’s Public Investment Fund company Alat to build variable-refrigerant-flow lines aimed at upcoming NEOM and Shagaya projects.

Bosch’s USD 8 billion purchase of Johnson Controls’ residential and light-commercial business doubled its Home Comfort sales and added York and Hitachi licenses, giving the firm a deeper catalogue for Kuwait’s below-200 kW retrofit sweet spot. LG, which operates 62 HVAC academies, trains more than 30,000 engineers per year, positioning itself to mitigate Kuwait’s acute technician shortage through regional certification courses.

Chinese entrants Midea and Gree deploy cost leadership and rapid-delivery models but still trail on desert-performance references, a gap Eurovent’s 2025 Desert Certification may widen until additional test data become public. District-cooling giants Tabreed and Empower are expanding upstream by co-developing variable-speed centrifugal chillers with Johnson Controls, locking in volume discounts and performance guarantees that smaller suppliers struggle to match. Overall, the top five producers held roughly 60% Kuwait heat pump market share in 2025, signaling moderate concentration where localized engineering, corrosion-resistant materials, and bundled service contracts determine bidding success.

Kuwait Heat Pump Industry Leaders

Daikin Industries, Ltd.

Mitsubishi Electric Corporation

LG Electronics Inc.

Carrier Global Corporation

Trane Technologies plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Johnson Controls Arabia won a USD 90 million VRF contract for Egypt’s New Administrative Capital, underlining regional scalability of oil-free variable refrigerant flow chillers.

- March 2026: Empower ordered 56,250 refrigeration tons of Mitsubishi Heavy Industries water-cooled centrifugal chillers for Dubai projects, with options up to 100,000 tons.

- March 2026: Carrier released AquaForce 23XW and 23XQ heat pumps optimized for R-1234ze and R-515B refrigerants, targeting GCC retrofit mandates.

- December 2025: Daikin broke ground on a Jeddah plant producing large air-cooled chillers, with planned hydronic heat pump expansion.

Kuwait Heat Pump Market Report Scope

| Air Source |

| Water Source |

| Ground Source |

| Hybrid |

| Air-to-Air |

| Air-to-Water |

| Water-to-Water |

| Ground-to-Water |

| Below 10 kW |

| 10-50 kW |

| 50-200 kW |

| Above 200 kW |

| Space Heating |

| Space Cooling |

| Domestic and Sanitary Hot Water |

| Industrial and Process Heating |

| Other Applications |

| Residential |

| Commercial |

| Industrial |

| New Installation |

| Retrofit |

| By Source Type | Air Source |

| Water Source | |

| Ground Source | |

| Hybrid | |

| By Technology | Air-to-Air |

| Air-to-Water | |

| Water-to-Water | |

| Ground-to-Water | |

| By Capacity | Below 10 kW |

| 10-50 kW | |

| 50-200 kW | |

| Above 200 kW | |

| By Application | Space Heating |

| Space Cooling | |

| Domestic and Sanitary Hot Water | |

| Industrial and Process Heating | |

| Other Applications | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| By Installation | New Installation |

| Retrofit |

Key Questions Answered in the Report

How fast is the Kuwait heat pump market expected to grow between 2026 and 2031?

It is projected to expand at a 3.06% CAGR, rising from USD 92.64 million in 2026 to USD 107.72 million by 2031.

Which application segment will grow the quickest through 2031?

Industrial and process heating leads with a 3.86% CAGR as refineries and desalination plants prioritize waste-heat recovery.

What capacity range dominates current sales?

Units rated 10-50 kW captured 42.18% of 2025 revenues, serving small commercial buildings and villas.

Why are hybrid heat pumps gaining traction?

They hedge subsidy uncertainty by combining electric compression with backup gas or solar thermal sources, achieving the fastest 4.02% CAGR among source types.

How does Kuwait's climate influence product choice?

Extreme heat and saline air require desert-certified equipment with reinforced coatings and wide operating envelopes, favoring high-ambient-rated models produced in regional factories.

Which policy is driving the 2026 retrofit surge?

Kuwait's Kigali-aligned ban on HCFC-based chillers forces commercial and industrial owners to replace legacy equipment with low-GWP, high-efficiency heat pumps.

Page last updated on: