Qatar Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

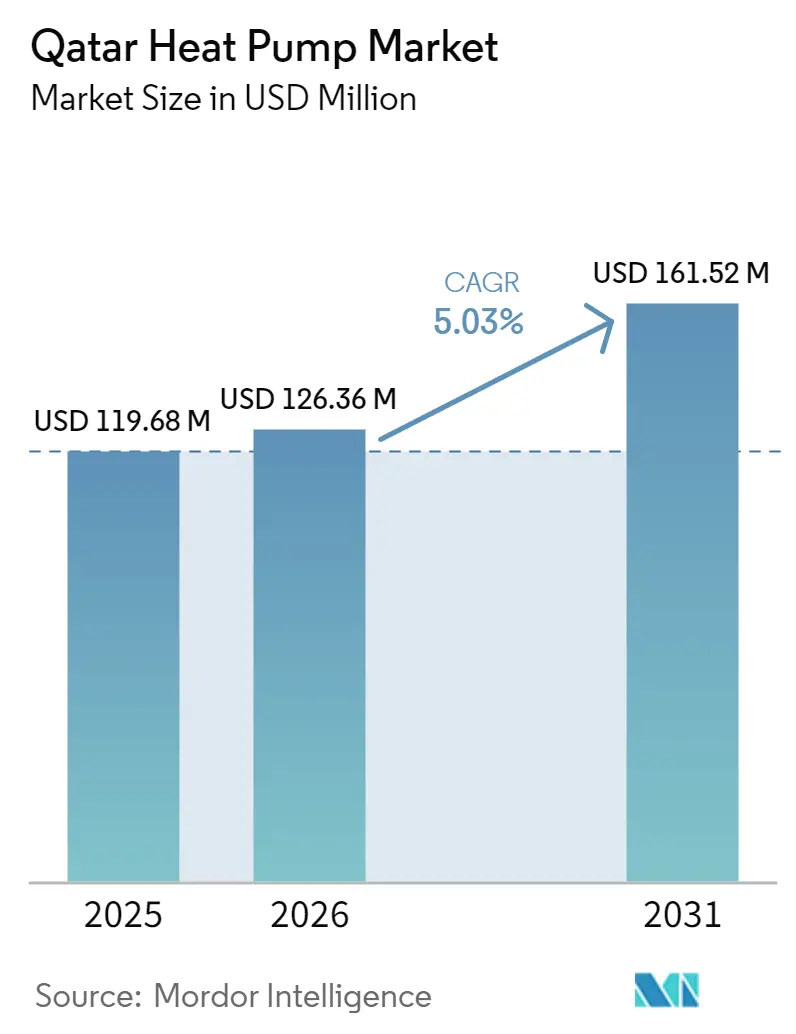

| Base Year Market Size (2025) | USD 119.68 Million |

| Market Size (2026) | USD 126.36 Million |

| Market Size (2031) | USD 161.52 Million |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

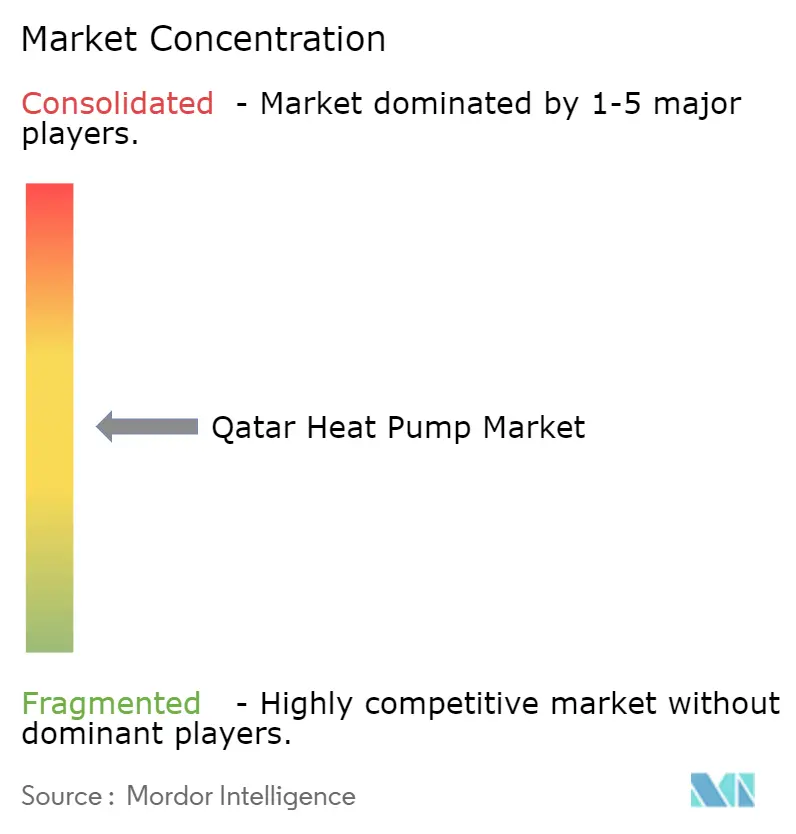

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Heat Pump Market Analysis by Mordor Intelligence

The Qatar heat pump market size is projected to expand from USD 119.68 million in 2025, USD 126.36 million in 2026, to USD 161.52 million by 2031, registering a CAGR of 5.03% over 2026-2031. Demand gains arise from mandatory energy-efficiency codes, hyperscale data-center construction, and the country’s extreme cooling climate, even as subsidized natural gas and free residential electricity temper the commercial payback case. Rapid progress on smart-city districts in Lusail and the Um Al Houl Economic Zone is pulling specification toward high-coefficient-of-performance equipment, while technology pivots—such as R-32 refrigerants with lower global-warming potential—are giving suppliers additional compliance hooks. Original-equipment manufacturers respond through exclusive distributor agreements that combine technician upskilling with multi-year service bundles, closing capability gaps in a market where fewer than 200 installers hold manufacturer credentials. Steady tariff rationalization for expatriate consumers is shortening payback horizons, positioning the Qatar heat pump market for sustained though disciplined growth.

Key Report Takeaways

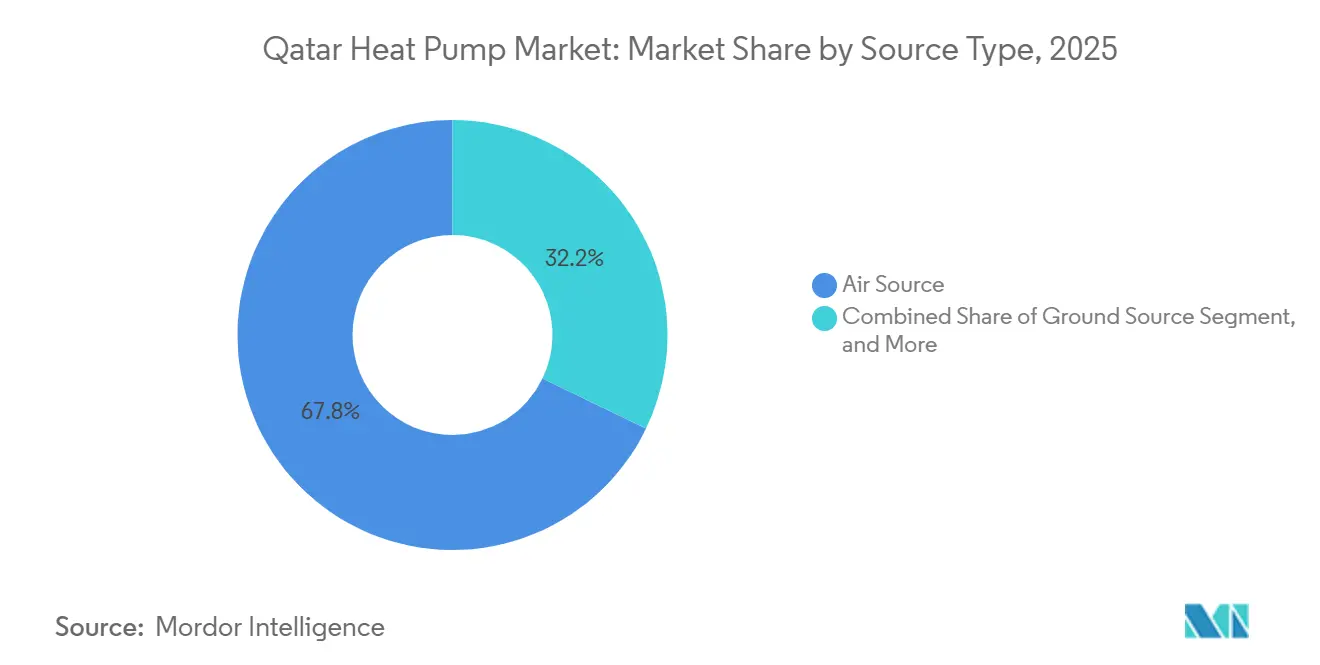

- By source type, Air Source systems led with 67.83% revenue share in 2025, whereas Ground Source systems are forecast to grow at a 5.72% CAGR through 2031.

- By technology, Air-to-Air configurations held 59.36% of the Qatar heat pump market share in 2025, while Ground-to-Water systems are set to expand at a 5.18% CAGR to 2031.

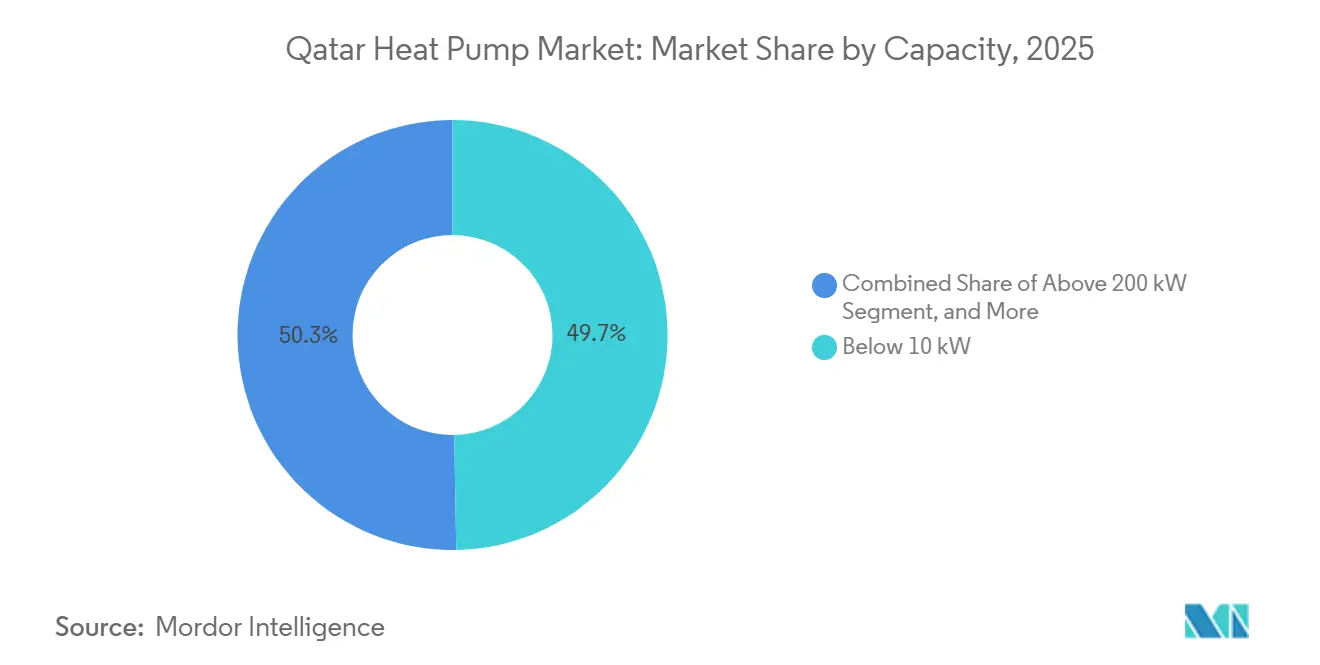

- By capacity, units below 10 kW captured 49.72% of the Qatar heat pump market size in 2025; the 50-200 kW bracket is projected to advance at a 5.51% CAGR between 2026-2031.

- By application, space cooling accounted for 71.64% of demand in 2025 and industrial and process heating is moving ahead at a 5.56% CAGR through 2031.

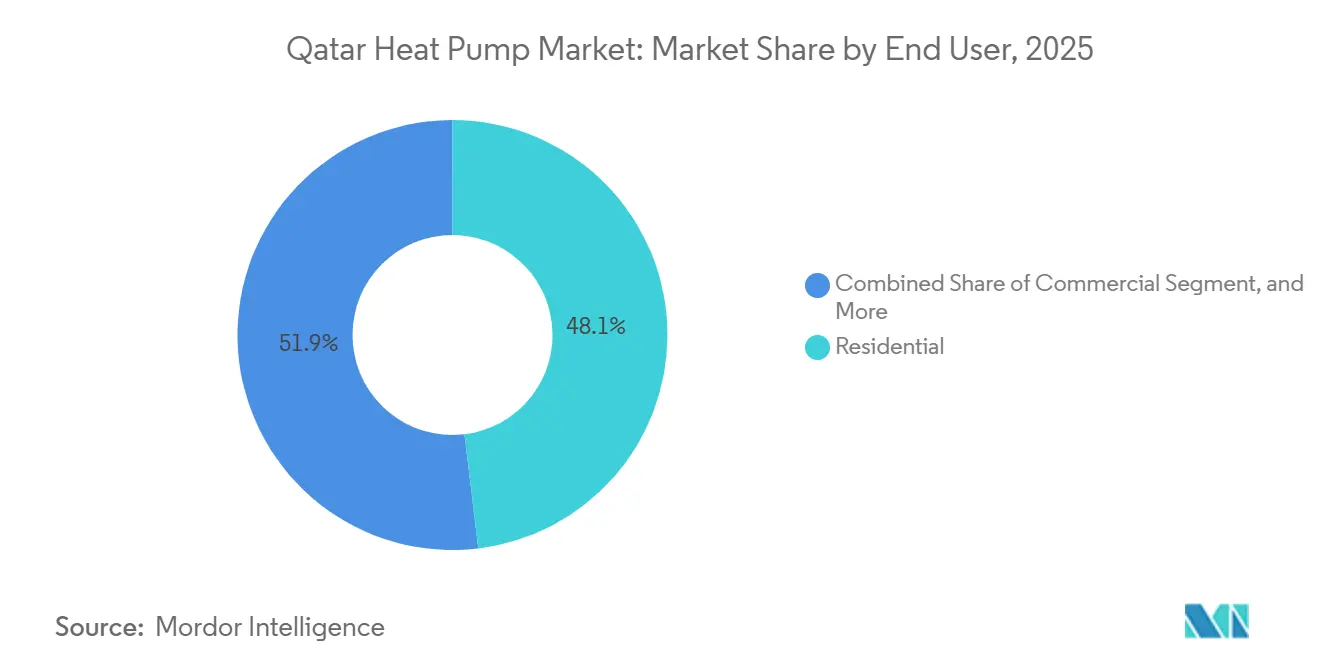

- By end user, residential customers represented 48.09% of 2025 revenue, while industrial adopters are expected to post the fastest growth at a 5.37% CAGR over 2026-2031.

- By installation type, retrofit activity dominated with 58.91% of 2025 shipments and is likely to grow at a 5.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | Impact on CAGR Forecast (%) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Qatar National Vision 2030 energy-efficiency targets accelerating heat-pump adoption | +1.2% | Doha, Lusail, Al Rayyan | Medium term (2-4 years) |

| Rapid expansion of hyperscale data centers requiring high-efficiency cooling and heating | +1.5% | Doha, Lusail, Qatar Science and Technology Park | Short term (≤ 2 years) |

| Extreme climatic conditions driving year-round reversible HVAC demand | +0.9% | National, coastal zones | Long term (≥ 4 years) |

| Gradual electricity-tariff rationalization improving payback | +0.7% | National, expatriate segments | Medium term (2-4 years) |

| Smart-city and mega-project construction pipeline | +1.0% | Lusail, Um Al Houl, West Bay | Medium term (2-4 years) |

| Low-GWP refrigerant regulations favoring next-generation systems | +0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Qatar National Vision 2030 Energy-Efficiency Targets Accelerate Adoption

Law 19-2024 obliges buildings above 10,000 m² to connect to district cooling or achieve equivalent performance, effectively mandating heat pumps with seasonal energy-efficiency ratios above 16.[1]Ministry of Environment and Climate Change, “Third Nationally Determined Contribution,” moecc.gov.qa Kahramaa’s 2025 net-billing scheme lets commercial owners offset up to 50% of consumption with rooftop solar, so pairing photovoltaics with heat pumps trims operating cost peaks.[2]Qatar General Electricity and Water Corporation, “Tariff Schedule,” kahramaa.qa Compliance systems, such as the Qatar Sustainability Assessment System, award extra points for heat-recovery designs, steering developers in West Bay toward reversible equipment. Together these rules compress decision cycles, making the Qatar heat pump market central to green-building certification strategies.

Rapid Expansion of Hyperscale Data Centers Requires High-Efficiency Cooling

Microsoft’s cloud campus and Ooredoo’s Syntys build-out are adding more than 25 MW of IT load that must be cooled year-round, even when winter temperatures drop to 15 °C.[3]Microsoft Corporation, “Regional Cloud Datacenter Investment,” microsoft.com, Ooredoo Group, “Syntys Data Center Expansion,” ooredoo.com Operators specify air-to-water heat pumps delivering 12 °C chilled water and 60 °C hot water for humidity control, a design that slashes compressor runtime by up to 40% through free-cooling economizers. New racks running artificial-intelligence workloads generate 30-40% more heat than older servers, so modular 500 kW heat-pump arrays can be dropped in without civil works. The cascading effect is an expanded addressable market for precision cooling equipment across adjacent office and colocation sites.

Extreme Climatic Conditions Drive Year-Round Reversible Demand

Doha logs 2 589 cooling-degree days at a 23 °C base, the Gulf’s highest, and climate models project a doubling of > 48 °C days by 2050. Cooling already uses 60% of national electricity, so equipment that holds capacity at 50 °C ambient, like Mitsubishi Electric’s City Multi systems, wins favor. January lows near 12 °C push occupants to seek efficient space heating, which resistance coils deliver at triple the operating cost of a reversible unit. This dual-season requirement cements heat pumps as the only practical path to whole-year comfort without outsized utility bills.

Gradual Electricity-Tariff Rationalization Improves Payback

Time-of-use rates for large expatriate accounts climbed to 4.5 US cents /kWh in 2025, and the Ministry of Finance signals further adjustments through 2028. Higher variable tariffs shrink heat-pump payback from seven to roughly five years when paired with rooftop solar, meeting the hurdle rate for most commercial investors. Developers now model tariff escalation as a top-line risk, making high-coefficient-of-performance equipment an insurance hedge. As subsidies narrow, the financial logic of heat pumps strengthens, reinforcing steady market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortage for design, installation, commissioning | -0.8% | Doha, Al Rayyan, Lusail | Short term (≤ 2 years) |

| High up-front costs for ground- and water-source installations | -0.6% | Commercial and industrial segments | Medium term (2-4 years) |

| Subsidized natural-gas pricing reducing industrial payback | -0.5% | Um Al Houl, Mesaieed, Ras Laffan | Long term (≥ 4 years) |

| Saline sandy soils increasing borehole drilling complexity | -0.3% | Coastal and desert zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortage Constrains Quality Installations

Only about 200 technicians possess manufacturer certifications, forcing contractors to import specialists at day rates above USD 500, a premium that inflates project budgets by up to 35%.[4]Qatar Foundation, “Technical Education Initiatives,” qf.org.qa Training-of-trainers programs launched in 2025 remain focused on traditional air-conditioning, leaving gaps in hydronic balancing and refrigerant-charge optimization. The shortage leads to installation errors, undersized buffer tanks and incorrect flow-switch wiring account for 40% of first-year service calls, denting confidence among early adopters.

High Up-Front Costs Slow Ground-Source Uptake

Ground-source projects cost USD 800-1,200 per installed kW because drilling saline sandy soils requires chlorideresistant grout and high-density polyethylene loops, with borehole costs averaging USD 150 per meter.[5]International Ground Source Heat Pump Association, “Design and Installation Standards,” igshpa.org Only two Qatari drilling firms own rigs equipped with real-time parameter sensors, limiting automation gains that could trim civil budgets by 14%. Banks demand 30% equity on green-finance loans, screening out speculative developers.[6]Qatar Development Bank, “Green-Finance Facility,” qdb.qa

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Ground Systems Gain Traction in Mega-Projects

Air Source units captured 67.83% of 2025 revenue, reflecting low capital cost and rooftop compatibility across villas and low-rise offices. Developers pursuing LEED Platinum certification now specify borehole arrays in Lusail and Um Al Houl, lifting Ground Source growth to a 5.72% CAGR through 2031. Hybrid air-ground schemes that employ shallow horizontal loops are being piloted to reduce drilling budgets and maintain high coefficients of performance during shoulder months.

Daikin’s planned hydronic-heat-pump plant in Jeddah aims to lower import duties by 10-15%, which should improve the landed price of Ground Source packages. Qatar Cool is testing geothermal pre-cooling at district plants, and success could translate to a 20% chiller draw reduction, freeing grid headroom for other loads. The resulting operational savings enhance the Qatar heat pump market value proposition for high-density precincts.

By Technology: Ground-to-Water Configurations Lead the Efficiency Race

Air-to-Air systems held 59.36% market share in 2025, favored for villa retrofits that rely on existing ducts. Ground-to-Water solutions, capable of delivering 7 °C chilled water and 55 °C hot water with seasonally adjusted energy-efficiency ratios above 20, are expanding at a 5.18% clip as district-cooling operators adopt closed-loop hydronic networks.

Johnson Controls’ YORK YVAM chiller with variable-speed screw compressors demonstrates part-load savings up to 35%, resonating with facilities that operate below full capacity for most of the year. Tabreed’s 2026 framework agreement underscores the shift toward high-efficiency centrifugal machines, a trend that aligns with broader Qatar heat pump market decarbonization goals.

By Capacity: Mid-Range Units Capture the Commercial Retrofit Wave

Units below 10 kW secured 49.72% of 2025 sales, driven by villa owners replacing aging split systems. Commercial landlords in West Bay and The Pearl are pivoting to centralized 50-200 kW arrays, projected to grow at 5.51% through 2031, to satisfy LEED thresholds and recover efficiency savings via tenant clauses.

Panasonic’s Aquarea high-temperature line, delivering 80 °C water, is being trialed in Mesaieed petrochemical plants to displace steam boilers. Kahramaa’s demand-response incentives, QAR 50 (USD 13.73) per curtailed kW, enable buildings with mid-range units to pre-cool thermal mass, strengthening retrofit economics and expanding the Qatar heat pump market size for centralized capacities.

By Application: Industrial Process Heating Emerges as a Frontier

Space cooling represented 71.64% of 2025 demand, reflecting electricity use that already tops 60% of national consumption. Industrial and process heating is forecast to grow at 5.56% as LNG exporters and petrochemical operators upcycle 40 °C waste heat to 90 °C steam, cutting gas use by 15%.

Alfa Laval is piloting ammonia-based systems that achieve Carnot efficiencies above 50% when lifting heat from 35 °C to 85 °C, trimming payback to under 4 years even with subsidized fuel. Meanwhile, space-cooling retrofits increasingly select desuperheaters to capture condenser energy for domestic hot water, raising overall system efficiency to beyond 450% on a primary-energy basis.

By End User: Industrial Buyers Accelerate for Carbon Compliance

Residential customers retained 48.09% market share in 2025 as villa retrofits surged, but industrial buyers are slated for 5.37% CAGR growth over 2026-2031, driven by ISO 50001 certification and looming carbon-border adjustment tariffs on exports.

LG’s partnership with Tadmur Trading includes technician training that mitigates the labor bottleneck in residential and small-commercial segments, while energy-service companies finance industrial upgrades by monetizing avoided fuel. Net-billing further sweetens residential economics, reinforcing the Qatar heat pump market’s dual-track expansion across household and heavy-industry users.

By Installation: Retrofit Projects Dominate an Aging Stock

Retrofits comprised 58.91% of 2025 activity and will continue to outpace new builds at a 5.26% CAGR, because most structures erected before 2015 lack hydronic loops and require packaged solutions. Smart-city districts in Lusail specify centralized heat-pump arrays during construction, but long project cycles and lump-sum procurement make year-to-year volumes volatile.

ST Engineering’s Lusail gateway enables grid-stress load shedding, preventing the need for an additional combined-cycle plant before 2028. Retrofit challenges include limited panel capacity and duct leakage, yet inverter-driven compressors improve part-load performance and extend service life, bolstering homeowner confidence in the Qatar heat pump market.

Geography Analysis

Doha, Lusail, and the industrial corridors of Mesaieed and Ras Laffan shape regional demand. Doha contains half of Qatar’s data centers, and offices in West Bay and The Pearl are installing modular water-source units that integrate with existing risers. The city’s 2,589 cooling-degree days ensure reversible systems operate profitably year-round, while winter lows of 12 °C create short yet critical heating windows.

Lusail’s USD 250 billion build-out mandates centralized systems with seasonal energy-efficiency ratios above 16, feeding multi-year procurement cycles. ST Engineering’s smart-city platform curtails compressor loads during grid stress, complementing Kahramaa’s strategy to delay new generation assets. Shallow horizontal loops are under evaluation to trim drilling budgets without sacrificing performance.

Um Al Houl and adjoining industrial zones pursue high-temperature heat pumps to displace up to 15% of subsidized gas in process heating, motivated by corporate emission targets rather than tariff savings. Inland Al Rayyan villas, averaging 34,000 kWh annually, face a replacement cliff, while coastal towers leverage seawater condensers albeit with higher corrosion-control costs. Collectively these sub-markets give the Qatar heat pump market a mosaic of drivers linked by extreme climate, tariff reform, and green-building mandates.

Competitive Landscape

Global brands, Daikin, Mitsubishi Electric, LG, Carrier, Trane, and Johnson Controls, compete through exclusive distributor deals that bundle training and service. Daikin’s 2024 agreement with Al Emadi Trading and LG’s 2025 pact with Tadmur Trading each pledge to certify 50-100 technicians by 2026, closing skill gaps that currently cap annual installations.

District-cooling incumbent Qatar Cool is vertically integrating by fitting heat-recovery chillers at plant level, an approach that cuts procurement expense yet limits technology diffusion beyond concession zones. Its West Bay command center opened in 2024, signaling a move toward real-time optimization that could treat packaged heat pumps as dispatchable grid resources.

White-space growth centers on hybrid air-ground systems and modular water-source units for mid-rise offices with constrained rooftops. Johnson Controls’ YORK YVAM chiller shows 35% part-load savings, while Tabreed’s 2026 centrifugal-drive framework confirms that variable speed is now table stakes. Energy-service companies further differentiate by offering performance contracts that monetize avoided fuel, nudging the Qatar heat pump market toward service-led value propositions.

Qatar Heat Pump Industry Leaders

Daikin Industries, Ltd.

Mitsubishi Electric Corporation

LG Electronics Inc.

Carrier Global Corporation

Trane Technologies plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Tabreed and Johnson Controls signed a framework to supply next-generation centrifugal chillers with variable-speed drives, targeting 30% energy cuts across Middle East district-cooling plants.

- January 2026: GENERAL Inc, now under Paloma Rheem, announced Middle East rollout of high-efficiency air-to-water pumps, leveraging Rheem’s network for Gulf-specific models.

- November 2025: Daikin broke ground on a Jeddah factory to build 50-200 kW hydronic heat pumps, intended to trim landed costs in Qatar by reducing duty and freight.

- November 2025: Johnson Controls unveiled YORK YVAM air-cooled chillers with variable-speed screws at HVACR World Dubai, highlighting 35% part-load savings.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Qatar heat pump market as the revenue earned from new sales, on-site installation, and aftermarket service of air, water, and ground-source electrically driven heat pumps that provide space conditioning or sanitary hot water in homes, commercial buildings, and light industrial facilities. Units factory-integrated inside reversible chillers are counted because the heat pump cycle is certified at origin.

Scope Exclusion: Stand-alone absorption chillers, pure cooling split ACs, and separately traded spare parts lie outside our scope.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with distributors, facility operators, ESCO contractors, and policy specialists across Doha, Al Khor, and Mesaieed. Insights on channel margins, retrofit share, and price dispersion were used to validate secondary findings and close data gaps.

Desk Research

We collected open data from Kahramaa load curves, Planning and Statistics Authority building completions, UN Comtrade codes 8418 and 841861, and GSAS green-building registers, and then matched those series with company filings via D&B Hoovers, news flow on Dow Jones Factiva, and patent signals on Questel. Peer-reviewed work from ASHRAE and the International Ground Source Heat Pump Association helped anchor technology efficiency bands. These examples are illustrative; numerous other publications supported fact checks.

Market-Sizing & Forecasting

A top-down demand pool model converts occupied floor area, cooling degree days, and average load per square meter into potential thermal demand, which is next aligned to typical coefficient of performance values to size equipment revenue. Bottom-up supplier roll-ups and installer channel checks then temper totals. Key variables include tariff slabs, GSAS registration counts, copper prices, import unit values, and cooling degree day trends. We apply multi-variable regression with scenario analysis to extend forecasts to 2030; missing channel data points are bridged with weighted moving averages from adjacent HVAC segments.

Data Validation & Update Cycle

Outputs pass variance checks, peer review, and senior analyst sign-off. Models refresh annually, with interim updates triggered by major policy shifts or giga project awards, ensuring clients always receive the latest view.

Why Our Qatar Heat Pump Baseline Commands Reliability

Published figures often diverge because each publisher picks different product scopes, revenue elements, and refresh cadences.

Key gap drivers center on the use of narrow customs codes, reliance on import value as a demand proxy, or omission of installation and service revenues.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 120.6 M (2025) | Mordor Intelligence | - |

| USD 3 M (2024) | Regional Consultancy A | Counts only 'heat pumps other than AC machines,' omits installation and service revenue |

| USD 35.6 M (2023) | Trade Statistics B | Uses import value alone, excludes local assembly, distributor margin, and retrofit activity |

The comparison shows that Mordor's balanced scope, mixed method modeling, and yearly refresh provide a dependable baseline that mirrors real equipment flows and spending patterns, giving decision makers clearer insight.

Key Questions Answered in the Report

What CAGR is projected for the Qatar heat pump market between 2026-2031?

The market is forecast to grow at a 5.03% CAGR over 2026-2031, reaching a value of USD 161.52 million in 2031.

Which source type is expected to be the fastest growing?

Ground Source systems are projected to expand at 5.72% annually through 2031.

Why are industrial buyers accelerating adoption of heat pumps?

LNG and petrochemical operators seek ISO 50001 compliance and aim to cut natural-gas consumption by 15%, driving a 5.37% CAGR in industrial demand.

How do electricity-tariff reforms influence payback?

Time-of-use hikes for expatriate accounts shorten typical payback from seven to about five years when heat pumps are paired with rooftop solar.

What is the major restraint for ground-source installations?

High up-front drilling costs, at USD 150 per meter in saline sandy soils, keep capital intensity roughly double that of air-source systems.

Page last updated on: