Denmark Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

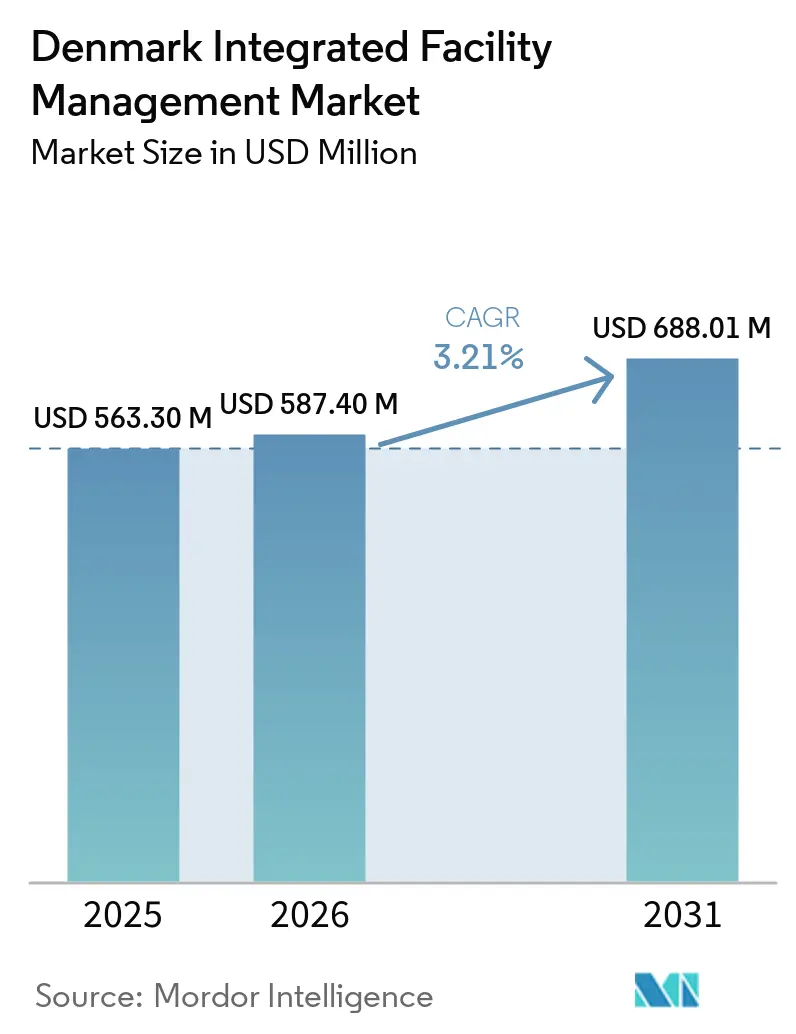

| Base Year Market Size (2025) | USD 563.30 Million |

| Market Size (2026) | USD 587.40 Million |

| Market Size (2031) | USD 688.01 Million |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

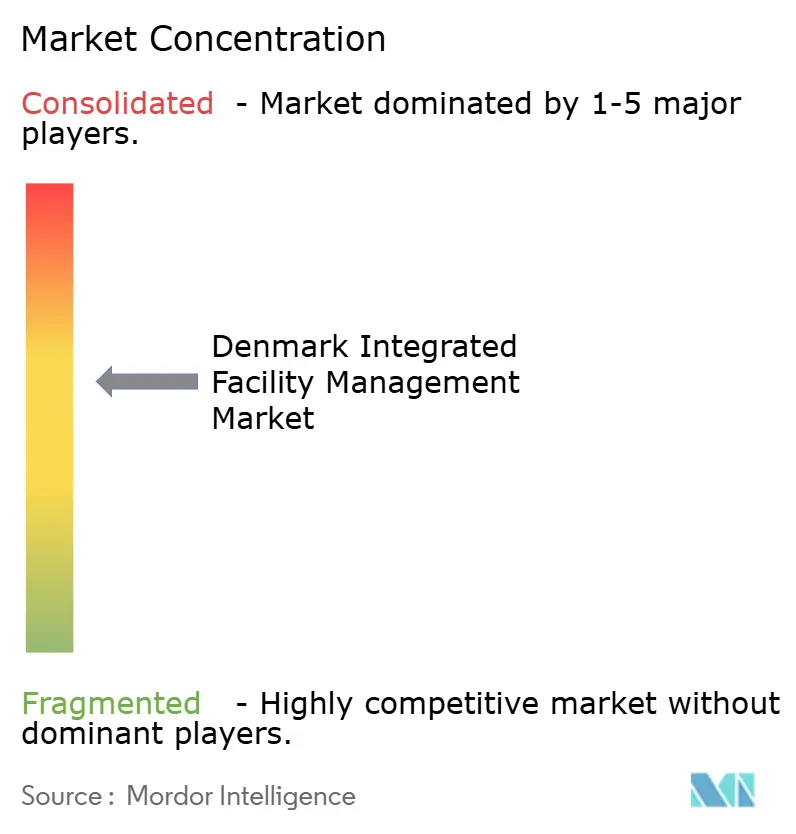

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Integrated Facility Management Market Analysis by Mordor Intelligence

The Denmark Integrated Facility Management Market size is projected to expand from USD 563.30 million in 2025 and USD 587.40 million in 2026 to USD 688.01 million by 2031, registering a CAGR of 3.21% between 2026 to 2031.

The Denmark integrated facility management market is expanding as buyers move away from single-service contracts and prefer bundled models that place cleaning, technical maintenance, catering, and workplace support under one governance structure. Contract values are also rising, as seen in the Statens FM 2026 agreement, a DKK 1.5 billion (USD 212 million) contract, that ISS now holds for more than 50 public institutions over 55 months. This shift supports larger providers because clients want fewer vendors, stronger reporting, and better operational control across sites. Sustainability rules, energy targets, and certification needs are also widening contract scope, especially where buyers now expect technical capability alongside soft services. At the same time, wage pressure and shortages in technical labour are limiting margin expansion, so success in the Denmark integrated facility management market depends as much on workforce depth and digital control as on demand growth.

Key Report Takeaways

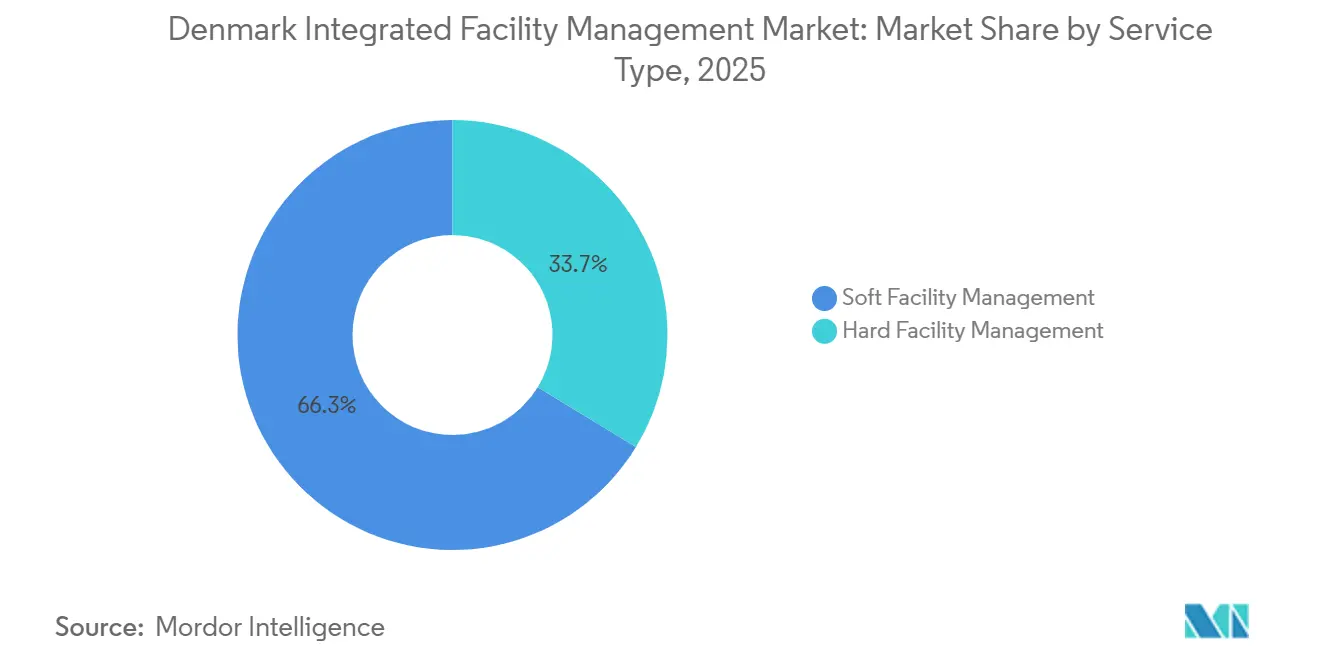

- By service type, soft facility management held 66.3% of the Denmark integrated facility management market share in 2025, while hard facility management is forecast to grow at 4.3% CAGR through 2031.

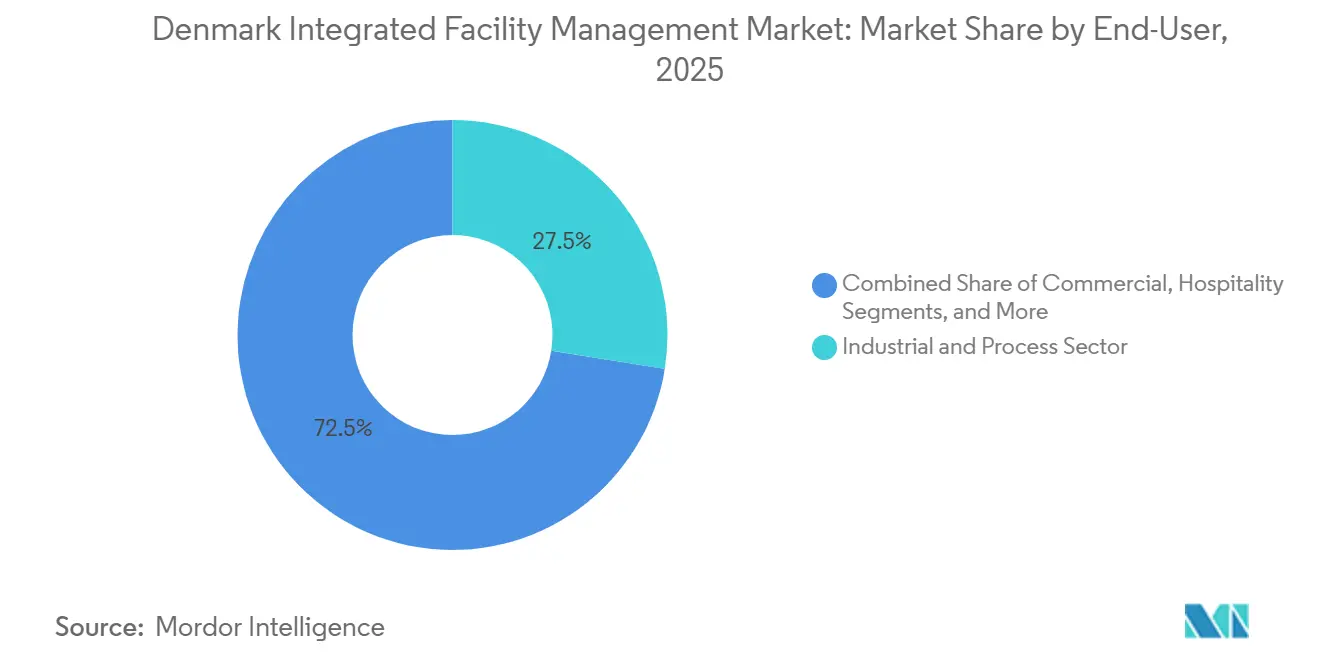

- By end-user, industrial held 27.5% share of the Denmark integrated facility management market in 2025, while commercial is forecast to grow at 4.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Denmark Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitalization Of Building Operations | +0.8% | National, with early concentration in Copenhagen, Aarhus, and Odense commercial districts | Short term (≤ 2 years) |

| Rising Demand for Sustainable FM Services | +0.7% | National, strongest in public-sector estate and corporate real estate in Greater Copenhagen | Medium term (2-4 years) |

| Emergence Of Performance-Based FM Contracts | +0.6% | National, with spill-over to regional industrial parks in Jutland | Medium term (2-4 years) |

| Growth In Investment in Critical Infrastructure | +0.5% | National, concentrated in Copenhagen metropolitan area and Northern Jutland energy corridors | Long term (≥ 4 years) |

| Workplace Wellness and Hybrid Work Models | +0.3% | Primarily Copenhagen metro and Aarhus urban commercial districts | Short term (≤ 2 years) |

| Growing Collaboration for Energy-Efficient Innovation | +0.2% | National, with cross-border Nordic spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digitalization Of Building Operations Is Redefining Real-Time FM Decision-Making

Digital tools are moving from support functions to core operating systems across the Denmark integrated facility management market. A February 2026 survey by Dansk Facilities Management reported that 94% of Danish FM organizations now use AI in their operations. The same work showed average AI maturity at 2.5 on a five-step scale, indicating broad adoption but still room to improve operating depth. That gap supports new spending on sensors, predictive maintenance, remote supervision, and automated workflow management. Procurement is also becoming more digital, and in June 2025, a linked FM and tendering workflow was introduced to reduce manual tender steps and improve documentation quality.[1]NTI Group, “NTI FM And NTI BIDCO Integration,” NTI Group Cybersecurity rules linked to connected building systems are now raising the minimum technical standard for suppliers, especially in public-sector work.[2]Dansk Facilities Management, “AI In Danish FM Organisations,” Dansk Facilities Management

Rising Demand for Sustainable FM Services Converts Regulatory Deadlines into Procurement Triggers

Sustainability requirements are now shaping how contracts are specified and renewed in the Denmark integrated facility management market. Building operations and heating accounted for 23% of Denmark’s total CO₂ emissions in 2025, underscoring the centrality of building services to national decarbonization efforts. The 2025 Klimarådet status framework also called for public-sector final energy consumption to fall by at least 1.9% each year against 2021 levels.[3]Klimarådet, “Status Report 2025,” Klimarådet It also set a yearly renovation requirement for at least 3% of public floor area above 250 m² with an energy label below B, which directly supports performance-oriented FM demand. Corporate occupiers are responding in the same direction because CSRD and ESG disclosures require auditable building data rather than general sustainability statements. Certification-linked upgrades are also causing more retendering activity when incumbent suppliers cannot support DGNB, BREEAM, or ISO 50001 workflows.

Emergence Of Performance-Based FM Contracts Rebalances Risk and Accelerates Innovation

Performance-based procurement is changing the commercial logic of the Denmark integrated facility management market. More buyers now want fees tied to uptime, energy use, and service quality rather than labour input alone. The state FM program has helped establish this direction by creating a clear public-sector template for larger buyers through phased tender structures with outcome accountability. This approach rewards providers with stronger data capture, better operating discipline, and more consistent reporting. It also tends to support longer contract periods because both client and supplier invest in baselines, measurement tools, and shared performance targets. Smaller operators remain at a disadvantage when they cannot fund the systems needed to verify results across a multi-site portfolio.

Growth In Investment in Critical Infrastructure Broadens the Hard FM Addressable Market

Investment in critical infrastructure is widening technical service demand within the Denmark integrated facility management market. Data centers, energy networks, large campuses, and advanced industrial facilities need constant oversight of MEP systems, HVAC assets, safety infrastructure, and energy performance. Copenhagen Municipality’s Climate Plan 2035 has added pressure by linking procurement and maintenance activity to lower emissions over time. This changes the FM role from routine upkeep to planned operational improvement across the asset base. It also increases the value of providers that can manage engineering-intensive scopes rather than rely solely on labor-heavy services. As buildings age and technical complexity rises, more contracts are bringing asset management and energy optimization into broader IFM packages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Skilled FM Workforce | -0.5% | National, most acute in Copenhagen and Aarhus, where labour market competition is highest | Medium term (2-4 years) |

| Limited Small Business Access to Data Protection Frameworks | -0.4% | National, disproportionately affecting SME FM operators in secondary cities | Short term (≤ 2 years) |

| Third-Party Coordination Among FM Service Providers | -0.3% | National | Medium term (2-4 years) |

| Cybersecurity Concerns in IoT-Enabled FM Platforms | -0.2% | National, strongest in public-sector and healthcare-adjacent FM | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity Of Skilled FM Workforce Constrains Contract Capacity and Service Quality

Labor availability remains one of the clearest operating limits across the Denmark integrated facility management market. The pressure affects both service operatives in cleaning and catering and technical specialists in MEP engineering, fire safety, and smart building systems. Survey work referenced by Dansk Facilities Management showed that unit-price contract structures are gaining favour, but those models depend on flexible staffing and fast deployment. DFM’s sustainability skills project also confirmed that the sector has a documented competence gap in the capabilities needed for greener building operations. Larger providers can absorb training costs and move specialists between contracts more easily than mid-sized competitors. This keeps competition tighter than demand alone would suggest and raises delivery risk when contract scopes expand during the service period.

Limited Small Business Access to Data Protection Frameworks Slows Market Digitalization for SME Operators

Data protection and cybersecurity requirements are also slowing digital adoption for smaller firms in the Denmark integrated facility management market. GDPR obligations, NIS2 requirements, and public tender rules increasingly require stronger access controls, secure storage, defined response processes, and formal governance. Smaller FM operators often lack these systems, which makes compliance a barrier to entry in integrated and data-intensive tenders. Many of these firms can still participate, but often as subcontractors rather than as prime contractors. This weakens diversity in service models because smaller providers often test niche approaches before larger groups scale them. As contracts become more digital, the compliance gap between large and small operators is becoming harder to close.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft Facility Management Services Lead While Technical Services Expand Faster

Soft Facility Management (FM) services held 66.3% of the Denmark integrated facility management (IFM) market share in 2025, which kept this group in the leading position by revenue. The large base reflects frequent outsourcing of cleaning, catering, workplace support, and security across commercial, institutional, and public buildings. Cleaning remained the highest-volume activity within Soft FM, while catering procurement became more selective, with buyers giving greater weight to sustainability credentials such as Nordic Swan Ecolabel standards in canteen operations. This steady service frequency gives Soft FM a scale advantage, as it is tied to daily building use rather than periodic technical interventions.

Hard FM is forecast to grow at a 4.3% CAGR through 2031, making it the fastest-growing segment of the Denmark IFM industry. Demand is improving because owners of complex sites need stronger coverage in MEP systems, HVAC assets, fire protection, and structured asset management. Heat-pump retrofits, district-cooling requirements, and more advanced operating needs in life sciences and data centers are raising the value of technical capability over basic reactive repair. Fire systems and safety remain more resilient than discretionary building services because compliance-driven spending cannot be delayed for long. DGNB and ISO 50001 requirements are also pulling technical services into broader IFM scopes that once focused mainly on cleaning and catering. This is gradually changing the mix of the Denmark integrated facility management market toward broader bundles with a stronger engineering component.

By End-User: Industrial Contracts Hold Scale While Commercial Demand Improves

Industrial end-users accounted for 27.5% of the Denmark IFM market in 2025, making this the largest end-user segment. Denmark’s concentration of pharmaceutical, cleantech, and precision manufacturing facilities supports this position because these sites need disciplined maintenance, safety control, and vendor qualification. Contract values also benefit from technical complexity, since regulated environments require more documentation, planned maintenance, and compliance support than standard office locations. That pattern was evident in December 2025, when Forenede Service entered a new integrated FM partnership with Topsoe across all four Danish locations, combining canteen, operations, safety, and employee experience under a single structure.

Commercial end-users are forecast to grow at a 4.0% CAGR through 2031, reflecting the redesign of office portfolios around hybrid work and tenant experience. Landlords and occupiers are using FM more actively to support flexible workplace use, front-of-house quality, digital workplace tools, and ESG-linked asset positioning. Healthcare remains a specialized area within the Denmark IFM industry because infection control, specialist cleaning, and non-clinical support create entry barriers that general providers cannot meet easily. Residential complexes, entertainment venues, and data centers are also adding new pockets of demand as building development becomes more varied. The rise of data centers is especially important because it brings 24/7 technical service needs that were less common in the older Danish FM mix.

Geography Analysis

Greater Copenhagen held the largest share of contracted volume in 2025 within the Denmark IFM market. The region has the highest concentration of offices, state institutions, hospitals, transport-linked assets, and corporate headquarters, which gives it a natural lead in outsourced FM demand. By May 2024, ISS was already serving nearly 100 state institutions and 34,000 daily users through the state FM relationship, which shows how strongly national portfolios still lean on the capital region and nearby administrative centers. Development activity in and around Copenhagen is also sustaining technical demand, including large campus-style projects where continuous monitoring and energy performance are part of the operating brief.

Aarhus and Odense are becoming more important secondary demand centers for the Denmark integrated facility management market. Their role is supported by university-linked campuses, logistics growth, advanced manufacturing, and a steady mix of public and private real estate investment. Jutland remains important because large exporters and industrial groups need consistent service delivery across several Danish locations rather than only in one city. That requirement favours providers with national coverage, stronger workforce planning, and enough technical depth to support multi-site contracts. Aalborg and Esbjerg add smaller but growing demand linked to port activity, offshore wind support, and infrastructure-adjacent facilities. These locations do not match Copenhagen in contract volume, but they do matter for Hard FM and other engineering-led scopes. Regional demand is therefore broadening, even though the capital area continues to set the pace for large integrated contracts.

Denmark’s wider Nordic setting also shapes supplier strategy and client expectations. Buyers often compare service quality, reporting discipline, and operating models across neighbouring Nordic markets, which encourages standardization in digital workflows and contract governance. Denmark’s small geography and strong digital infrastructure make national rollout easier than in larger European countries where distance and building dispersion raise operating complexity. That setting supports faster adoption of connected maintenance, remote oversight, and portfolio-wide performance tracking across the Denmark integrated facility management market.

Competitive Landscape

The Denmark integrated facility management market is moderately consolidated at the top, with a limited number of large providers leading major public and multinational contracts. ISS A/S, Coor Service Management, Forenede Service, and Caverion are the most visible names across integrated and technical scopes. ISS now holds the Statens FM 2026 agreement, which strengthens its position in state and institutional outsourcing and underlines the advantage of national delivery scale. Mid-tier and specialist firms still matter, especially in technical areas where engineering depth, certification, and local operating knowledge are more important than broad contract coverage alone.

Strategic moves in 2025 and 2026 show that leading firms are competing through contract breadth, digital execution, and service quality rather than price alone. Forenede Service expanded its position in industrial outsourcing through the new Topsoe partnership in December 2025, where multiple service streams were brought under one management model. ISS also renewed and extended its cleaning and catering agreement with Salling Group in January 2025, and the contract included robotics and digital solutions for service optimization across a large retail and logistics footprint. A June 2025 release of a linked FM and tendering workflow also points to a wider shift in the operating environment, since buyers now expect faster tendering, cleaner audit trails, and stronger documentation from FM partners. In practical terms, the Denmark integrated facility management market is rewarding providers that can show measurable control over service performance, procurement, and compliance.

Sustainability reporting is becoming a stronger selection factor because clients need auditable energy and carbon data from building operations. That benefits larger providers because digital platforms, reporting systems, and governance controls are easier to finance across a wide client base than on a small contract book. Specialist firms still have room in healthcare, fire systems, critical environments, and data-center-related services where narrow expertise matters more than broad bundling. The Denmark integrated facility management market therefore remains competitive, but access to the largest integrated mandates is narrowing toward firms with stronger digital, ESG, and governance capability.

Denmark Integrated Facility Management Industry Leaders

ISS A/S

Coor Service Management Holding AB

Sodexo S.A.

CBRE Group, Inc.

Compass Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Caverion and Danfoss formalised a five-year performance-based technical IFM agreement covering Campus Nordborg and Campus Gråsten, incorporating Caverion's SmartView digital monitoring platform for real-time building operations, energy optimisation, and shared performance data. The agreement represents a flagship case for performance-oriented contracting in Danish industrial FM and signals the mainstreaming of outcome-linked Hard FM delivery models.

- April 2026: ISS was awarded the Statens FM 2026 contract by Bygningsstyrelsen (Danish Building and Property Agency) for a 55-month term effective October 1, 2026, covering 50-plus state institutions, approximately 240 locations, and over 18,000 employees. The contract is valued at over DKK 300 million (USD 42 million) annually and approximately DKK 1.5 billion (USD 212 million) in total, covering canteen, cleaning, internal service, maintenance, waste management, and outdoor services. Notably, security services were carved out to a separate Securitas contract, marking a structural adjustment to the state's IFM model.

- December 2025: Forenede Service entered a new integrated FM partnership with Topsoe covering all four of the company's Danish locations, consolidating canteen, operations, safety, and employee experience services under a single management structure. The agreement includes a dedicated Experience Manager and a differentiated food concept (SANS!), signalling that industrial clients are elevating employee-experience outcomes alongside operational reliability in FM procurement.

- May 2025: ISS received Nordic Swan Ecolabel certification for 16 canteens operated at Bygningsstyrelsen locations, covering approximately 2,400 daily meals. The certification, assessed by an independent third party, validates operational sustainability practices including food-waste reduction, CO₂ minimisation, phase-out of single-use packaging, and increased organic meal content.

Denmark Integrated Facility Management Market Report Scope

The Denmark Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the current outlook for Denmark integrated facility management?

The Denmark integrated facility management market was valued at USD 563.3 million in 2025 and is forecast to reach USD 688.0 million by 2031, growing at a 3.2% CAGR over 2026-2031.

Which service category contributes the most revenue in Denmark?

Soft FM led the revenue mix with 66.3% share in 2025, supported by the high frequency of cleaning, catering, workplace support, and security services.

Which service area is growing the fastest through 2031?

Hard FM is forecast to grow at 4.3% CAGR through 2031, driven by technical maintenance, MEP systems, HVAC needs, fire safety, and energy-related compliance.

Which end-user group creates the largest demand base?

Industrial users held the largest share at 27.5% in 2025 because life sciences, cleantech, and advanced manufacturing sites require more complex maintenance and compliance support.

Why are Danish buyers shifting toward integrated contracts?

Buyers want fewer vendors, better reporting, stronger performance control, and easier coordination across cleaning, technical maintenance, catering, and workplace services.

What is the main operating challenge for providers?

The biggest constraints are skilled labour shortages and rising digital compliance demands, which raise delivery risk and make it harder for smaller firms to compete for integrated mandates.

Page last updated on: