Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.65 Billion |

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 3.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland Facility Management Market Analysis by Mordor Intelligence

The Finland facility management market size is expected to grow from USD 2.65 billion in 2025 to USD 2.74 billion in 2026 and is forecast to reach USD 3.27 billion by 2031 at 3.57% CAGR over 2026-2031. Growth rests on mandatory EU-taxonomy retrofits, accelerating smart-building adoption, and enterprises’ shift toward core-business focus. Aging infrastructure sustains demand for intensive mechanical, electrical, and plumbing upgrades, while 2035 carbon-neutrality goals bolster energy-efficiency services. Tight labor markets raise service pricing but also motivate automation investments and outcome-based contracts. Technology integration yields measurable owner returns, with documented smart-building projects delivering energy savings exceeding 10% and asset-value uplifts above EUR 10 million (USD 11.61 million).[1]Siemens, “Sello Shopping Center, Finland,” Siemens, siemens.com Competition remains moderate as Nordic leaders scale via mergers to offset wage inflation and digital-platform costs.

Key Report Takeaways

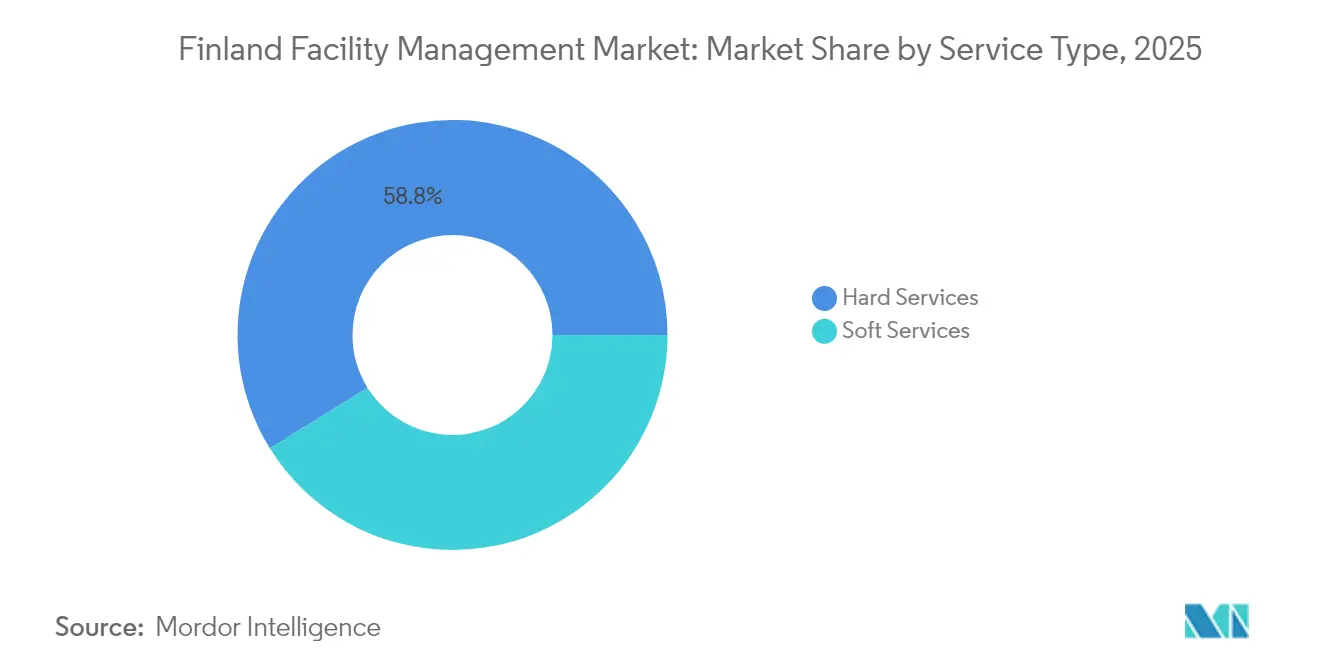

- By service type, hard services controlled 58.84% of the Finland facility management market share in 2025; soft services are forecast to expand at a 4.05% CAGR through 2031.

- By offering type, outsourced delivery accounted for 65.32% revenue share in 2025; integrated outsourcing solutions are projected to advance at 4.88% CAGR to 2031.

- By end-user industry, commercial facilities held 37.68% share of the Finland facility management market size in 2025; institutional and public infrastructure is growing fastest at 7.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Finland Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Current occupancy rates | +0.8% | Helsinki metropolitan area, Tampere, Turku | Short term (≤ 2 years) |

| Profitability of major providers | +0.6% | National, concentrated in urban centers | Medium term (2-4 years) |

| Labor-participation trends | +0.4% | National, acute in Western Finland | Long term (≥ 4 years) |

| Urbanisation in metro areas | +0.7% | Helsinki, Tampere, Turku, Oulu | Medium term (2-4 years) |

| Adaptive reuse of aging industrial spaces | +0.5% | Helsinki, Tampere industrial districts | Long term (≥ 4 years) |

| EU taxonomy–aligned green financing | +0.9% | National, emphasis on public sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Current Occupancy Rates

Premium office districts in Helsinki sustain high utilization even as hybrid work spreads, whereas suburban parks contend with structural vacancies that downshift maintenance intensity needs. This divergence pushes bundled contracts toward experience-centric services in prime zones and cost-optimization packages in secondary assets. At Sello Shopping Center, smart-building retrofits cut energy demand 40% while supporting 21 million annual visitors, underscoring how facility data analytics fine-tune service levels without eroding user comfort. Segmenting offerings by occupancy dynamics enables providers to protect margins in high-touch accounts while preserving competitiveness in price-sensitive portfolios.

Profitability of Major Providers

Escalating wages and cautious client budgeting squeeze operating margins. Coor’s Q4 2024 Nordic revenue hit SEK 3,192 million (USD 327.43 million) yet organic growth slipped 3%, producing a 3.3% margin.[2]Coor, “Q4 2024 Results,” Coor, news.cision.com Providers pivot toward integrated, outcome-based contracts that reward measurable performance, notably in healthcare, where downtime directly affects patient safety. Sodexo’s 1.7% global FM growth shows that pivot paying off, with healthcare upsides offsetting commodity-service softness. High-margin digital energy management, wellness programs, and compliance reporting now feature prominently in tenders, cushioning profitability as commodity cleaning rates tighten.

Labor-Participation Trends

Employment of 20-64-year-olds slipped to 75.8% in January 2025 and unemployment touched 9.5%, yet technical FM vacancies remain unfilled.[3]Statistics Finland, “More Unemployed Persons in January 2025,” Statistics Finland, stat.fi Skill mismatches push average service wages up 3.6%. Western Finland faces the steepest gaps, forcing providers to offer location premiums and cross-train recruits. Long-term unemployment of 106,000 highlights retraining needs, prompting industry-backed vocational programs in HVAC automation and low-carbon retrofits. Robotics for floor care and AI condition monitoring increasingly substitute labor, tempering cost escalation without sacrificing service quality.

EU Taxonomy–Aligned Green Financing

Financing availability reshapes the Finland facility management market. MuniFin allocated EUR 4.8 billion to green projects in 2024, 63% of its housing book. Kesko’s EUR 300 million green note illustrates corporate appetite for taxonomy-qualified upgrades. Lifecycle carbon metrics now inform tender scoring, favoring providers with certified energy-management systems. Energy-performance contracts convert capex retrofits into service revenues, lifting margins while aligning with national net-zero targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and legislative hurdles | -0.6% | National, acute in construction permits | Short term (≤ 2 years) |

| Macroeconomic headwinds | -0.8% | National, concentrated in discretionary spending | Short term (≤ 2 years) |

| Shortage of skilled FM labor and rising wage costs | -0.7% | National, severe in Western Finland | Medium term (2-4 years) |

| Cybersecurity liabilities from connected building systems | -0.4% | Urban centers with smart building adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled FM Labor and Rising Wage Costs

Scarcity of certified technicians inflates payrolls and jeopardizes service quality. Construction downturns displaced workers lacking IoT or predictive-maintenance competencies, amplifying the gap. Wage premiums have already expanded FM salary bands by 3.6%. Providers respond with automation—robotic cleaners now cover up to 1,800 m² per hour—and international recruitment. A leading case is Caverion’s apprenticeship alliance with Tampere University of Applied Sciences, which halves technician onboarding time and embeds digital-retrofit competencies.

Cybersecurity Liabilities from Connected Building Systems

The Vastaamo patient data breach exposed vulnerabilities in networked controls, heightening liability fears. Smart-building rollouts promise 36.8 kW average power savings, yet each new sensor expands the attack surface. Insurance premiums for connected facilities climbed 12% in 2025, and tender documents now mandate ISO 27001 compliance. Smaller providers lacking cyber resources risk exclusion from high-value digital-FM contracts, capping overall market upside until robust security standards diffuse industry-wide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Dominate Retrofit Momentum

Hard services retained 58.84% of Finland facility management market share in 2025, driven by mandatory MEP upgrades to reach 2035 neutrality goals. Predictive HVAC analytics optimize asset life and cut downtime, translating into 8-10% annual maintenance cost savings for property owners. A 2024 case study at Hospital Nova illustrates hard-service impact: integrating AI motor monitoring reduced unplanned chiller outages by 90% and saved EUR 2.1 million (USD 2.44 million) in replacement parts, shielding operating budgets during raw-material price volatility. Steel and copper price increases of 14% in 2024 pressured CAPEX, but long-term energy savings sustained retrofit ROI, bolstering demand for hard-service expertise.

Soft services, while smaller, are on a 4.05% CAGR path as hybrid work drives flexible security, cleaning, and hospitality solutions. Robotics and biodegradable cleaning chemicals mitigate wage and material-cost spikes. For example, Sodexo deployed autonomous UV disinfection robots that trim chemical usage 40% and enhance infection control in Mehiläinen clinics. Such innovation supports premium pricing and employee-wellness differentiation, maintaining the segment’s upward slope within the Finland facility management market.

By Offering Type: Outsourcing Captures Complexity Premium

Outsourced contracts represented 65.32% of the Finland facility management market size in 2025 and are expanding at 4.88% CAGR. Demand stems from rising regulatory complexity and the need for specialist digital platforms. Coor’s renewal with PostNord, worth SEK 155 million (USD 15.90 million) annually, consolidates mail centers, logistics hubs, and offices under one SLA, cutting client coordination costs 11% while ensuring compliance across 77 performance metrics. Outsourcing also blunts wage-inflation risk by shifting head-count fluctuations to service partners.

In-house FM still covers 34.68% of spend, mainly in mission-critical industrial sites that value direct control. Yet technology requirements erode the in-house model. Valmet’s 2025 restructuring targets EUR 80 million (USD 92.94 million) annual savings partly by moving non-core maintenance to integrated FM suppliers. Over the forecast horizon, bundled outsourcing will widen its lead as clients prioritize variable-cost structures and cradle-to-grave accountability.

By End-user Industry: Institutional Surge Rewrites Growth Map

Commercial real estate contributed 37.68% to the Finland facility management market in 2025, anchored by Helsinki’s prime offices and high-street retail. E-commerce logistics hubs dampen retail footfall, yet smart-warehouse retrofits preserve margins by trimming energy bills 14% despite diesel-price spikes. IT and telecom facilities demand Tier III uptime, enabling premium FM rates up to 35% above standard commercial contracts.

Institutional and public infrastructure posted the highest 7.16% CAGR, propelled by the hospital pipeline and municipal modernization. Hospital Nova’s “Hot Hospital” model bundles acute services around imaging suites, necessitating 24/7 MEP resilience and just-in-time sterile-supply logistics. Rising stainless-steel prices inflated construction outlays by 9%, but FM-enabled energy savings of 22% neutralize lifecycle cost spikes, proving the economic case for advanced institutional FM solutions within the Finland facility management market.

Geography Analysis

Helsinki metropolitan area generated around 44.62% of national FM revenues in 2025 thanks to headquarters clustering, transit investments, and Pasila’s redevelopment that elevated Class-A office rents 7%. The Finland facility management market share in the capital region aligns with high service-quality expectations and early adoption of AI predictive analytics, supporting vendor margins above the national average. Tampere and Turku jointly hold 25.34% share, underpinned by university expansions and tech-industry spillovers. Their 4.42% forecast CAGR outpaces the national rate, driven by new life-science campuses requiring GMP-compliant FM protocols.

Northern and Eastern Finland deliver 20.12% of value through industrial and healthcare facilities spread across large geographies. Remote monitoring reduces truck rolls by 15%, offsetting fuel-price volatility. Mining site FM—where hourly downtime exceeds USD 17,000—prioritizes predictive maintenance and rapid spare-parts logistics via drone deliveries tested in 2025 under a VTT-coordinated pilot. Western Finland, accounting for 9.92% of revenues, wrestles with the deepest labor shortages, pushing baseline service wages 4% above the national mean. Providers compensate through robotic cleaning fleets and mobile-first workforce apps that raise technician productivity 18%.

Regional FM demand now tracks sustainability investment flows more than traditional industrial clusters. The state’s EUR 294 billion (USD 341.5 billion) green-transition program funds public-building retrofits nationwide, widening geographic opportunity pools. Coastal municipalities allocate resilience budgets for flood-mitigation retrofits, creating niche FM demand in seawall pump maintenance and salt-air corrosion control—specialties that command premium rates.

Competitive Landscape

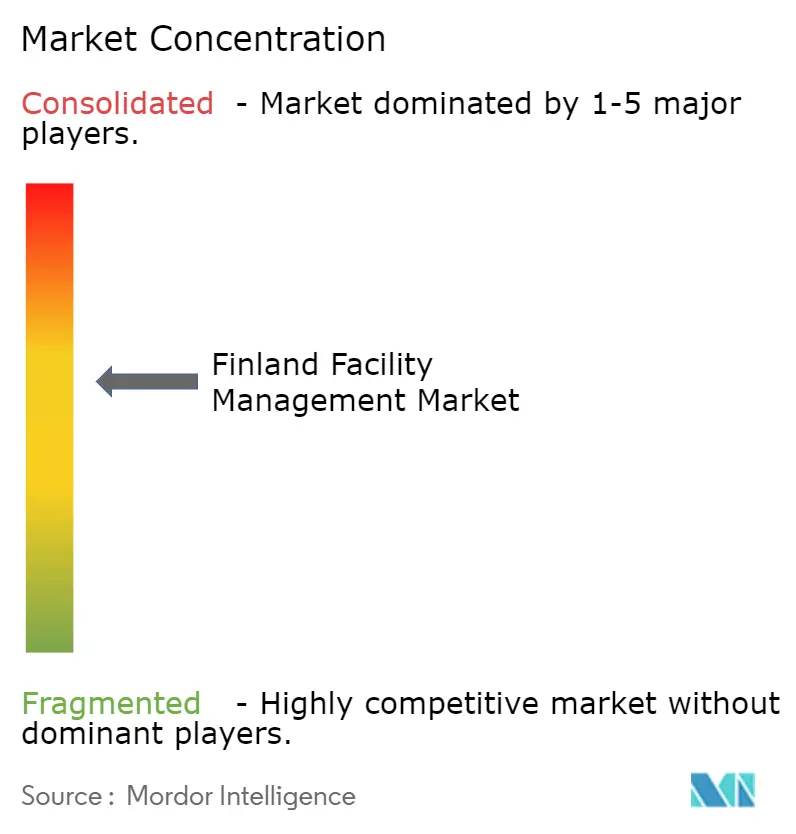

Market concentration remains moderate. Coor, Caverion, and Lassila & Tikanoja collectively capture an estimated 38% of Finland facility management market share, leveraging integrated portfolios and deep client relationships. The Caverion–Assemblin merger will create a Nordic giant with USD 5.2 billion combined turnover and broadened smart-building capabilities. Lassila & Tikanoja differentiates through circular-economy waste programs, while Lindström monetizes textile-service digitalization via RFID-tagged workwear that optimizes laundering cycles.

Technology investment shapes competitive edges. KONE applies AI to elevator sensor data, predicting 60% of failures before downtime and reducing technician dispatches by 15%. Smaller regionals survive through vertical specialization-such as Fidelix’s building-automation retrofits-often becoming acquisition targets for scale-seeking nationals. White-space opportunities persist in cybersecurity-centric FM offerings, with only 12% of tenders currently bundling IT security clauses despite growing liability exposures.

Finland Facility Management Industry Leaders

Lindstrom Group

PHM Group

Coor Group

Four FM

Palmia Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Coor extended its Nordic Integrated Facility Management deal with PostNord worth SEK 155 million annually, reinforcing multi-country outsourcing momentum.

- January 2025: Valmet unveiled restructuring affecting 1,150 positions to save EUR 80 million (USD 92.8 million) yearly by 2026, signaling cost-control focus among industrial FM clients.

- September 2024: Assemblin acquired Fidelix Group, boosting building-automation strength.

- July 2024: Sodexo partnered with UVD Robots for autonomous UV disinfection in Finnish hospitals.

Finland Facility Management Market Report Scope

The Finland facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Finland facility management market?

The Finland facility management market size is USD 2.74 billion in 2026.

How fast will the market grow through 2031?

The sector is forecast to expand at a 3.57% CAGR, reaching USD 3.27 billion by 2031.

Which segment is expanding the fastest?

Institutional and public infrastructure FM services are growing at 7.16% CAGR due to new hospital projects and municipal retrofits.

Why are outsourced contracts gaining share?

Outsourcing offers compliance expertise and spreads wage-inflation risk, driving its share to 65.32% in 2025 with a 4.88% CAGR outlook.

What is the main challenge for providers?

A shortage of skilled technicians coupled with rising wage costs is squeezing margins and driving automation investments.

How are sustainability regulations influencing the market?

EU-taxonomy rules are channeling billions of euros into green retrofits, boosting demand for energy-performance contracting and certified FM services.

Page last updated on: