Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.37 Billion |

| Market Size (2026) | USD 2.47 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Norway Facility Management Market Analysis by Mordor Intelligence

Norway facility management market size in 2026 is estimated at USD 2.47 billion, growing from 2025 value of USD 2.37 billion with 2031 projections showing USD 3.03 billion, growing at 4.16% CAGR over 2026-2031. This growth outlook reflects resilient demand across private and public real-estate portfolios, the country’s strict energy-efficiency mandates, and a decisive pivot toward integrated service models. Norway’s universal fiber connectivity underpins rapid PropTech integration, while mandatory ESG disclosure under the Climate Act accelerates adoption of data-rich facility management platforms. Oslo’s dominance in office transactions and infrastructure investment funnels a large share of new contracts into the capital region, yet Bergen, Stavanger, and a cluster of secondary cities are closing the gap by capitalizing on offshore energy projects, university expansion, and smart-building grants. Competitive intensity has sharpened after Compass Group’s 2025 purchase of 4Service, a move that triggered capability upgrades and price realignments among incumbents seeking Nordic scale. Providers able to demonstrate measurable carbon reductions and verifiable cost savings now command premium, multi-year integrated facility management agreements.

Key Report Takeaways

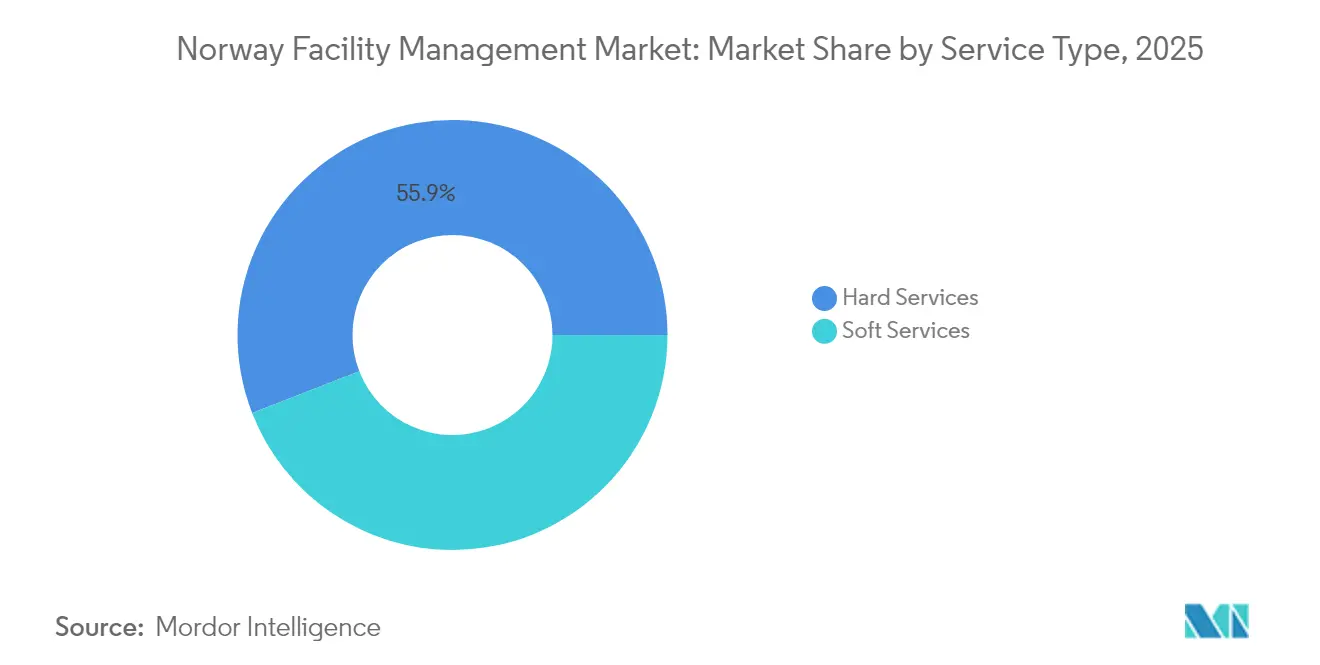

- By service type, hard services captured 55.90% of Norway facility management market share in 2025, whereas soft services are advancing at a 4.92% CAGR through 2031.

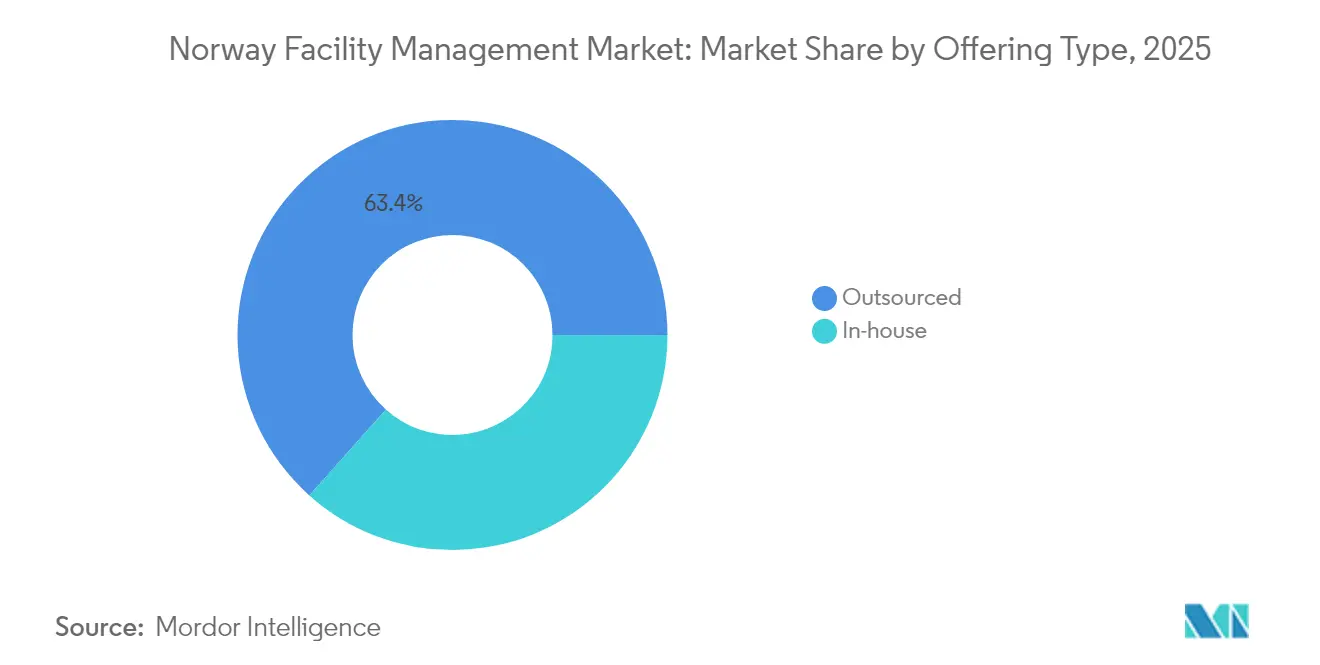

- By offering type, the outsourced model accounted for 63.40% of Norway facility management market size in 2025, while integrated FM contracts are projected to expand at 4.62% CAGR between 2026 and 2031.

- By end-user industry, the institutional and public-infrastructure segment is expanding at the fastest 4.73% CAGR to 2031; the commercial sector retained a 39.20% revenue share in 2025.

- ISS, Coor, and Compass Group collectively held just above 40% of the domestic revenue pool in 2024, underscoring a moderately concentrated competitive structure.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Norway Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in retrofit demand to meet Norway’s 2030 energy-efficiency directive targets | +1.2% | National; strongest in Oslo, Bergen, Stavanger | Medium term (2-4 years) |

| Government “Nye Veier” & Statsbygg outsourcing policies fuel large public-sector IFM contracts | +0.8% | National; major infrastructure corridors | Long term (≥ 4 years) |

| Mandatory ESG & carbon reporting under Norway’s Climate Act boosts data-driven FM services | +0.7% | National; priority in urban centers | Short term (≤ 2 years) |

| Tight labour market & high wage levels accelerate FM outsourcing for cost control | +0.9% | National; acute in Oslo, Stavanger | Medium term (2-4 years) |

| PropTech adoption enabled by nationwide fiber connectivity & smart-building grants | +0.6% | Urban centers, spreading to secondary cities | Medium term (2-4 years) |

| Integrated FM demand from offshore oil & gas platforms seeking single-vendor HSE compliance | +0.4% | Stavanger, Bergen, offshore installations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Retrofit Demand to Meet Norway's 2030 Energy-Efficiency Directive Targets

Norway’s legally binding goal of cutting greenhouse-gas emissions 55% by 2030 has unleashed unprecedented demand for building retrofit projects, and this demand feeds directly into the Norway facility management market.[1]Statsbygg, "Slik kan bygg og eiendom bli grønnere," statsbygg.no.Government-funded initiatives spotlight digital monitoring and space optimization to trim the building sector’s sizeable energy footprint. Facility managers increasingly deploy building-automation control systems, delivering up to 24% energy savings when paired with comprehensive envelope and plant upgrades. Urban projects favor such digital retrofits because dense sites impose physical limits on deep envelope interventions. Oslo and Bergen commercial landlords report shorter payback periods when automation is layered onto mechanical, electrical, and plumbing (MEP) upgrades, making energy retrofits a core driver of hard-service revenues.

Government “Nye Veier” & Statsbygg Outsourcing Policies Fuel Large Public-Sector IFM Contracts

Nye Veier’s EUR 25 billion, 20-year infrastructure pipeline and Statsbygg’s wholesale shift to outsourced non-core operations are reshaping public-sector procurement toward bundled and integrated contracts. [2]Nye Veier, “About Us,” nyeveier.noMunicipalities collectively direct more than NOK 500 billion of annual procurement, and recent tender specifications stress ESG scorecards and circular-economy compliance. Vendors that document CO₂ avoidance, waste diversion, and social-impact metrics gain scoring advantages. Integrated facility management agreements with performance-based clauses now replace fragmented single-service deals, especially along new highway corridors and in government office clusters. These policies lengthen contract tenors and raise lifetime revenue visibility for service providers capable of delivering end-to-end solutions.

Mandatory ESG & Carbon-Reporting Under Norway's Climate Act Boosts Data-Driven FM Services

The Climate Act and the Transparency Act require large Norwegian companies to furnish detailed ESG disclosures, driving a surge in demand for IoT-enabled carbon-tracking solutions. Facility managers have responded by installing sensor arrays across lighting, HVAC, and metering systems, capturing granular consumption data for automated compliance reporting. Deployments such as Sundvolden Hotel’s 1 GWh energy-saving program illustrate real-time analytics’ ability to translate data into clear cost and carbon reductions. Early adopters cite faster audit cycles and improved tenant engagement as additional benefits, reinforcing data-driven FM models as a competitive necessity.

Tight Labour Market & High Wage Levels Accelerate FM Outsourcing for Cost Control

Norway’s unemployment rate of just above 2% and average monthly salaries nearing 60,000 NOK translate into some of Europe’s highest facility payroll costs.[3]Statistics Norway, "Highest real wage growth in over ten years," ssb.no.Union density and collectively bargained overtime premiums further inflate budgets, making internally managed soft and technical services cost-prohibitive for many occupiers. Real wage growth of 1.9% in 2024 intensified these pressures, prompting corporations to pass responsibility for staffing, scheduling, and technology investment to specialist providers. Outsourcing also mitigates recruitment challenges in scarce technical disciplines, supporting the long-term shift toward bundled and integrated FM contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent tender regulations (Public Procurement Act) raise bid costs & lengthen sales cycles | -0.5% | National; applies to all public contracts | Long term (≥ 4 years) |

| Cap-ex freeze in commercial real-estate amid high interest rates curtails new FM contracts | -0.3% | Oslo and Bergen CBDs | Short term (≤ 2 years) |

| Volatility in offshore oil & gas maintenance budgets creates revenue swings for technical FM providers | -0.4% | National; applies to all public contracts | Long term (≥ 4 years) |

| High unionisation rates limit flexible workforce allocation and inflate overtime expenses | -0.2% | National, acute in Oslo, Stavanger | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Tender Regulations Raise Bid Costs & Lengthen Sales Cycles

Norway’s Public Procurement Act prescribes exhaustive documentation, transparent evaluation criteria, and appeal windows that often stretch bid cycles for public-sector FM contracts. Providers must invest in detailed ESG documentation, life-cycle cost analyses, and digital reporting frameworks even before shortlist selection. The rigorous process disadvantages smaller domestic firms lacking dedicated bid teams and lifts compliance costs for larger incumbents. Delays between tender issue and contract award can exceed 12 months, compressing near-term revenue visibility, particularly where incumbent agreements expire during the evaluation phase.

Cap-Ex Freeze in Commercial Real Estate Amid High Interest Rates Curtails New FM Contracts

A rapid rise in interest rates during 2024 increased capital costs for real-estate investors, leading many Oslo and Bergen landlords to defer new-build and major retrofit projects. With pipeline developments postponed, contract generation for construction-phase facility services slowed, translating into a short-term drag on Norway facility management market growth. Landlords now prioritize operating-expense optimization over expansion, heightening price competition in soft-service tenders until financing conditions ease.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Market Share Despite Soft-Service Growth Acceleration

Hard services commanded a dominant 55.90% Norway facility management market share in 2025 due to aging infrastructure, severe climatic stress on building envelopes, and mandatory energy audits that favor sophisticated MEP and HVAC upgrades. Fire-safety systems form a critical sub-segment in offshore platforms where nonstop monitoring is compulsory. Owners increasingly request asset-management overlays to extend equipment life, a trend reinforced by rising financing costs. Soft services, by contrast, controlled 44.10% of 2025 revenues yet are projected to scale at a brisk 4.92% CAGR through 2031 as occupiers embrace wellness-oriented workplace strategies. Digital work-order apps, ESG-compliant cleaning protocols, and app-based user-experience features position soft-service providers for rapid expansion inside bundled and integrated delivery models.

Across both categories, integrated packages that merge technical maintenance with hospitality-style amenity management are gaining traction, especially in high-rise multi-tenant assets where occupants demand seamless service experiences. Providers that blend certified Nordic Swan cleaning, AI-led space analytics, and energy-performance guarantees are closing larger, longer contracts, underscoring cross-selling potential between hard and soft domains.

By Offering Type: Outsourced Models Dominate as Integration Complexity Increases

The outsourced delivery model accounted for 63.40% of Norway facility management market size in 2025 and is on track to grow at 4.62% CAGR to 2031 as organizations double down on core-business focus and labor-cost risk transfer. Single-service contracts are receding, particularly in corporate headquarter campuses where fragmented vendors hamper portfolio-wide ESG reporting. Mid-market occupiers gravitate toward bundled FM because it balances coordination gains with manageable contract complexity, while larger groups push straight to fully integrated deals.

Integrated FM is delivering double digit pipeline growth, bolstered by ISS extending its Barclays mandate and Coor’s PostNord renewal. Providers leverage self-perform platforms for high-volume soft services and strategic sub-contractor ecosystems for specialist technical tasks, enabling flexible cost structures. The 36.60% in-house segment remains material in petrochemical, defense, and high-security sites where statutory or operational constraints limit third-party access, but even these holdouts increasingly carve out non-core tasks for external partners.

By End-User Industry: Commercial Sector Leadership Challenged by Institutional Growth

The commercial estate cluster retained 39.20% of 2025 revenue, powered by Oslo’s thriving technology scene and omnichannel retail networks that demand temperature-controlled warehousing and resilient data-center infrastructure. Operators such as Bulk Infrastructure have rolled out energy-efficient colocation sites, generating a steady stream of technical FM assignments. Yet the institutional and public-infrastructure segment is accelerating at a 4.73% CAGR, propelled by steady public expenditure and systematic outsourcing under Nye Veier and Statsbygg frameworks.

Hospitals, universities, and transport hubs leverage building-information-modeling workflows to enforce asset-performance warranties, nudging facility management vendors into data-centric service delivery. Industrial campuses, while cyclical, continue to require predictive-maintenance packages that minimize unplanned downtime for energy and process equipment. Meanwhile the hospitality sector adopts IoT-driven climate and occupancy controls that simultaneously cut utility bills and elevate guest comfort, signaling additional upside for solution-rich FM providers.

Geography Analysis

Greater Oslo, home to roughly 1.4 million residents, constitutes the single largest addressable cluster for the Norway facility management market. Prime CBD offices command rents near EUR 500/m², and 2023 absorption reached 870,000 m², generating a large volume of high-spec technical and soft-service contracts. The city’s data-center corridor amplifies demand for mission-critical maintenance and 24/7 monitoring. Second in momentum, Bergen recorded 13.1% property-value growth in 2024 and channels offshore-sector synergies into FM requirements for supply bases, crew accommodation, and maritime logistics.Stavanger’s energy heritage produces a deep pool of brown-field platform-support work, while several floating wind and carbon-capture pilots add specialist service opportunities.

Trondheim and Tromsø deliver steady institutional demand backed by university estates, student housing, and government northern-development programs. Ubiquitous fiber connectivity allows these secondary markets to adopt the same IoT-rich facility standards as the capital, shrinking the service-quality gap and expanding the reachable client base for national FM providers. Further afield, coastal towns with strong aquaculture and shipping activity require tailored HSE-focused FM solutions for hatcheries, cold-storage plants, and harbors, adding niche diversification opportunities for agile vendors. Collectively, these geographic dynamics reinforce a moderately concentrated yet regionally balanced growth profile for the Norway facility management market.

Competitive Landscape

ISS, Coor, and the newly enlarged Compass Group-4Service entity account for just over 40% of national revenues, defining a market structure that is neither oligopolistic nor highly fragmented. ISS has funneled investment into AI-guided workflow engines and an employee-experience app suite, winning multi-country deals such as the Barclays renewal that alone represents 2.5% of group turnover. Coor pursues a Nordic regional-scale thesis, integrating sustainability dashboards across its PostNord contract to prove emissions savings. Compass Group’s 2025 acquisition of 4Service grants instant soft-service density plus a digital ordering platform that scales efficiently across pan-European accounts.

Below the top tier, regional champions such as GK and Multiconsult exploit deep engineering know-how and local compliance mastery to defend technical niches. PropTech start-ups including Soundsensing and Sensorita supply modular, API-ready solutions that incumbents white-label inside integrated offerings, raising the technological bar for market entry. Competitive differentiators increasingly revolve around closed-loop sustainability reporting, predictive-maintenance accuracy, and contractual risk-sharing models that tie vendor remuneration to energy- and labour-cost savings.

Norway Facility Management Industry Leaders

-

ISS Facility Services

-

Toma Facility Services AS

-

Coor Service Management

-

Ability FM

-

Sodexo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Compass Group finalized its purchase of 4Service AS, adding an app-enabled soft-service platform and solidifying Nordic coverage.

- January 2025: Coor extended its Nordic IFM agreement with PostNord, securing SEK 155 million in annual revenue and embedding cross-border ESG dashboards.

- September 2024: ISS landed a 7-year, DKK 1.2 billion-per-year UK government contract, reinforcing its integrated FM credentials.

- August 2024: ISS reported 5.8% organic growth for Q2 2024 and renewed key contracts, underlining margin resilience in a high-wage environment.

Norway Facility Management Market Report Scope

Facility management (FM) services involve building upkeep, utilities, maintenance operations, waste services, security, etc. Hard facility management services and soft facility management services further segment these services. The adoption of FM solutions and services is likely to be driven by several factors, including an increase in demand for cloud-based FM solutions and a rise in demand for FM systems linked to intelligent software.

The Norway facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehousing) |

| Hospitality (Hotels, Eateries and Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transport) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehousing) | |

| Hospitality (Hotels, Eateries and Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transport) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Norway facility management market?

The market is valued at USD 2.47 billion in 2026 and is projected to reach USD 3.03 billion by 2031, reflecting a 4.16% CAGR over the 2026-2031 forecast period.

Which service category dominates market revenue?

Hard services account for 55.90% of 2025 revenue, driven by mandatory energy-efficiency upgrades and aging infrastructure.

Why are integrated facility management (IFM) contracts gaining traction?

Clients prefer single-vendor models to streamline ESG reporting, cut coordination costs, and secure long-term performance guarantees, especially on large public-sector projects under Nye Veier and Statsbygg frameworks.

How is Norway’s tight labour market influencing outsourcing decisions?

Unemployment near 2% and high unionised wage levels raise in-house staffing costs, encouraging organisations to outsource both soft and technical services for cost control.

Which geographic areas offer the fastest growth opportunities?

Bergen leads regional growth with 13.1% property-value gains in 2024, while secondary cities such as Trondheim and Tromsø are ramping up smart-building deployments aided by nationwide fibre connectivity.

What key technologies are reshaping facility management service delivery?

IoT sensors, AI-driven predictive maintenance, and cloud-based analytics platforms (for example, ClevAir and GK Cloud) are enabling 24%–40% energy savings and improving asset performance reporting.

Page last updated on: