Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

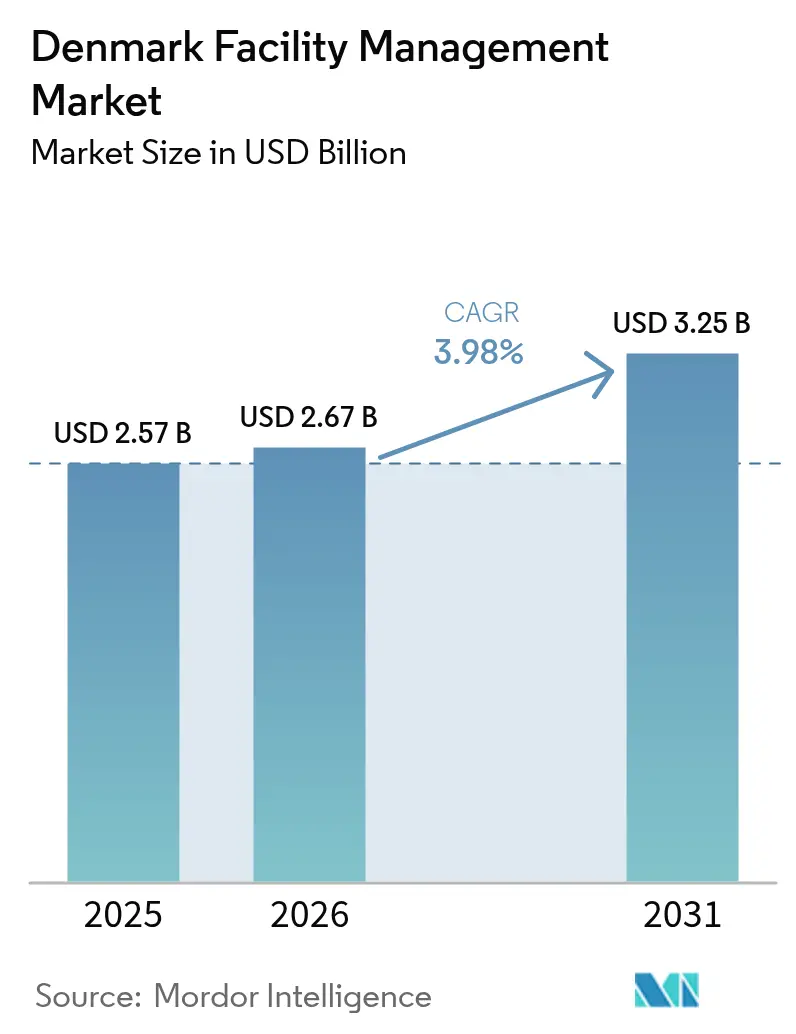

| Base Year Market Size (2025) | USD 2.57 Billion |

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 3.25 Billion |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Facility Management Market Analysis by Mordor Intelligence

The Denmark facility management market size is expected to grow from USD 2.57 billion in 2025 to USD 2.67 billion in 2026 and is forecast to reach USD 3.25 billion by 2031 at 3.98% CAGR over 2026-2031. The Denmark facility management market benefits from tight commercial real-estate fundamentals; national office vacancy now stands at 6.7% below the long-run average, which drives recurring demand for integrated hard and soft services. Demand is further lifted by mandatory energy-performance upgrades linked to EU directives that push building owners toward outsourced, technology-enabled solutions. The outsourced delivery model already commands 70% of the Denmark facility management market and continues to widen its lead because organisations prefer to focus resources on core activities while relying on specialist partners for regulatory compliance, IoT deployment, and carbon-footprint tracking. Nordic incumbents strengthen competitive positions through AI, robotics, and sensor analytics that help offset Denmark’s elevated labour costs. Over the forecast period, public spending tied to the Recovery and Resilience Plan and a 60% green-allocation rule is expected to channel significant capital toward energy-efficient retrofits, further underpinning service uptake across institutional and infrastructure assets.

Key Report Takeaways

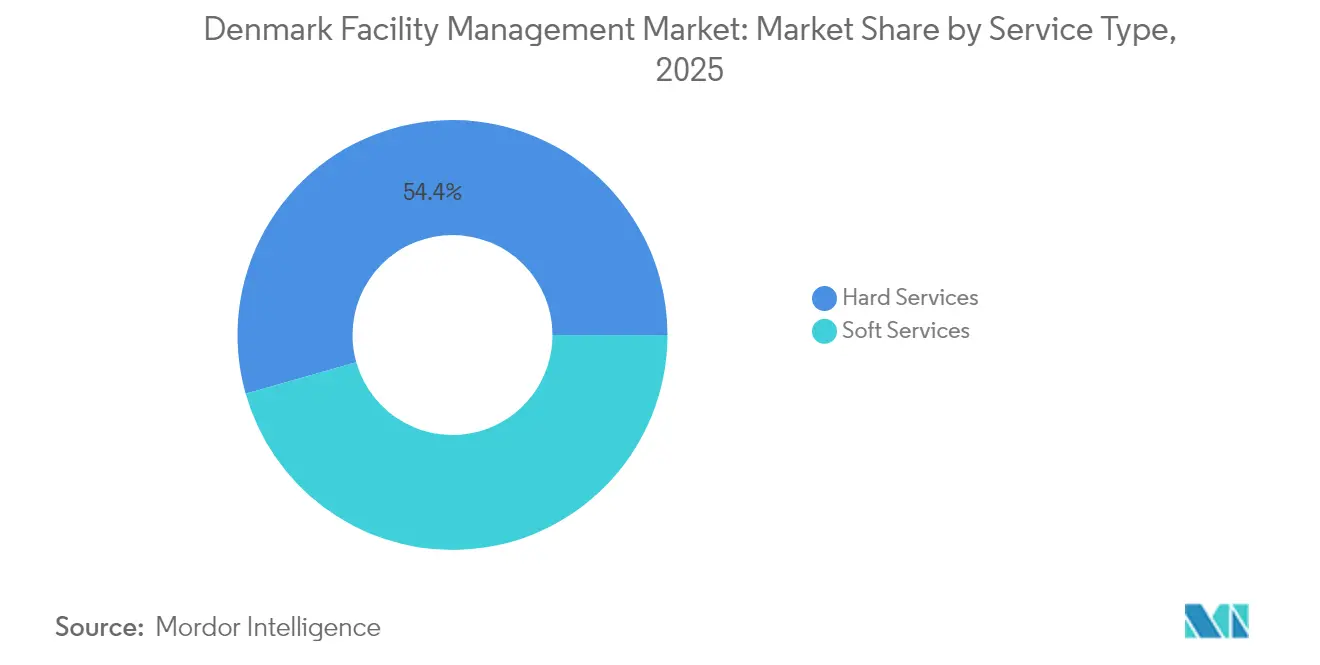

- By service type, hard services retained 54.40% Denmark facility management market share in 2025, while soft services are set to expand at a 5.95% CAGR through 2031.

- By offering type, outsourcing accounted for 69.20% of the Denmark facility management market size in 2025 and is projected to grow at 5.38% CAGR to 2031.

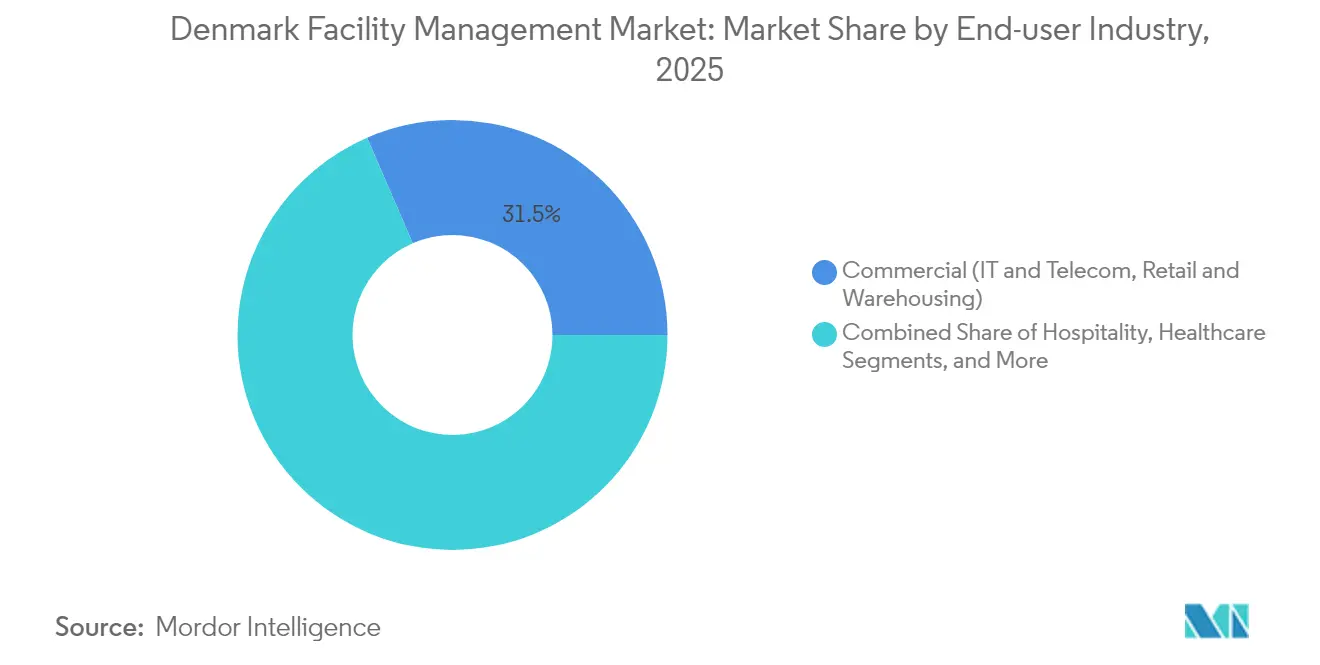

- By end-user, the commercial segment led with 31.50% of 2025 revenue; institutional and public infrastructure facilities hold the highest growth outlook at 4.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Current Occupancy Rates Drive Service Expansion | +1.2% | National, with concentration in Copenhagen, Aarhus, Odense | Short term (≤ 2 years) |

| Profitability Benchmarks Reshape Service Portfolios | +0.8% | National, stronger in commercial hubs | Medium term (2-4 years) |

| Labor Market Dynamics Accelerate Automation | +1.5% | National, early adoption in urban centers | Medium term (2-4 years) |

| Urbanization Patterns Reshape Service Distribution | +0.6% | Copenhagen, Aarhus, Odense, Aalborg, Esbjerg | Long term (≥ 4 years) |

| Public-sector Digitalisation and Rising Defence Outlays | +0.9% | National, concentrated in government facilities | Medium term (2-4 years) |

| Mandatory ESG Reporting (CSRD) Spurs Sustainable FM Demand | +1.1% | National, EU-wide compliance requirements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Current Occupancy Rates Drive Service Expansion

Office utilisation in Copenhagen, Aarhus, and Odense has rebounded strongly, with vacancy now 6.7% below the historical mean.[1]EjendomDanmark, “Kontorudlejning i USA og Danmark: Som at sammenligne pærer og bananer,” ejd.dkHigher daily footfall forces landlords to increase cleaning frequency, security staffing, and indoor-air quality monitoring. Integrated providers capable of bundling these hard and soft services command price premiums as asset owners seek one-stop coverage. Rising density also elevates energy-use intensity, leading owners to sign performance-based contracts that link reimbursements to measurable efficiency gains. The result is accelerating contract value in the Denmark facility management market for both preventive maintenance and workplace-experience add-ons. Occupancy-driven expansion is expected to remain the single largest short-term catalyst because Denmark continues to encourage on-site collaboration rather than fully remote work models.

Labor Market Dynamics Accelerate Automation

Denmark’s unemployment rate remains below 3% and union agreements keep wages elevated relative to continental peers. Facility managers, therefore, deploy cleaning robots, automated scheduling algorithms, and IoT-enabled predictive maintenance to protect margins. AI-driven rostering tools have cut manual supervisory hours by up to 20%, freeing scarce labour for higher-value tasks. Automation also helps large providers comply with Denmark’s strict worker-safety statutes by reducing exposure to routine hazards. Early adopters of robotics have secured multi-year extensions from retail and transport clients, illustrating the competitive edge technology confers within the Denmark facility management market. Over the medium term, AI and robotics are forecast to shave 1.5 percentage points off labour-line cost growth, thereby broadening outsourcing’s value proposition.

Mandatory ESG Reporting (CSRD) Spurs Sustainable FM Demand

The Corporate Sustainability Reporting Directive forces Danish organisations with over 250 employees or EUR 40 million (USD 46.59 million) to publish detailed environmental metrics from 2025. This regulatory trigger has turned carbon-monitoring dashboards, energy analytics services, and waste-segregation audits into core contract deliverables rather than optional extras. Providers able to document cradle-to-gate emissions now win tenders at a 15-20% higher success rate, according to bid-evaluation data compiled by market leaders. Demand is surging for sustainability consulting, carbon accounting, and circular-economy advisory bundled with traditional hard-services execution. The Denmark facility management market, therefore, gains both volume and value uplift, as ESG compliance fees are typically priced at a 5-10% premium to baseline maintenance.

Public-sector Digitalisation and Rising Defence Outlays

Central government agencies automate administrative workflows and modernise property portfolios under Denmark’s joint procurement framework. The Ministry of Defence recently awarded ISS a DKK 3 billion (USD O.47 billion) integrated services contract that extends to canteens, cleaning, security, and technical maintenance across 500 locations.[2]ISS World, “Intelligent Solutions,” issworld.com Similar multi-site contests are expected from the Ministry of Taxation and the Police Service, each specifying sensor-based monitoring and cyber-secure building-management systems. In parallel, defence real-estate spending increases with NATO readiness targets, boosting long-term demand for specialised services such as high-grade access control and on-site energy generation. These developments give the Denmark facility management market a stable pipeline of publicly funded opportunities, insulated from short-term economic volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Complexity Raises Entry Barriers | -0.7% | National, EU-wide compliance requirements | Medium term (2-4 years) |

| Macroeconomic Headwinds Constrain Discretionary Spending | -0.9% | National, with spillover effects from European markets | Short term (≤ 2 years) |

| Stringent Labour Regulations Inflate Operating Costs | -0.8% | National, particularly affecting labor-intensive services | Long term (≥ 4 years) |

| Up-front Capital Needed for Advanced IoT / AI Platforms | -0.6% | National, concentrated in technology-intensive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity Raises Entry Barriers

Multiple compliance layers building energy certification, ISO 9001:2015 for energy labelling, worker-safety audits, and GDPR requirements, add significant cost and administrative friction for new entrants. [3]Danish Energy Agency, “Energikonsulenter,” ens.dk Achieving full certification can take 18 months and consume up to 8% of annual revenue for smaller providers, limiting competitive churn and reinforcing incumbent dominance. EU-wide sustainability directives further complicate reporting, especially for foreign firms unfamiliar with Danish municipal codes. While this environment secures quality and safety, it also restricts supplier diversity and may slow innovation at the fringes of the Denmark facility management market.

Macroeconomic Headwinds Constrain Discretionary Spending

Inflation and energy-price volatility diminish tenant budgets for elective facility upgrades. Many SMEs postpone IoT retrofits and experiential office enhancements, focusing only on essential maintenance and statutory compliance. Providers struggle to pass through rising wages and material costs under fixed-price contracts, squeezing margins. Some clients renegotiate service scopes mid-contract, particularly within retail and light-manufacturing estates exposed to consumer-demand swings. This restraint depresses short-term spend in the Denmark facility management market, though it simultaneously motivates efficiency-oriented innovations that lower lifecycle cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft Services Gain Digital Edge

Soft services delivered the fastest revenue trajectory with a 5.95% CAGR outlook to 2031, even though hard services retained 54.40% denmark facility management market share in 2025. Cleaning, security, and front-of-house support have become data-rich operations managed through AI scheduling and real-time quality dashboards. Occupier demand for wellness-centred work environments pushes providers to embed sensors that monitor air quality, foot-traffic patterns, and temperature comfort. Catering extends into nutrition analytics and contactless payment ecosystems, reinforcing its strategic role in employee-experience programmes. This digital repositioning elevates soft-service average contract value by 8-10% and cements its status as the fastest-growing pillar of the Denmark facility management market.

Hard services remain indispensable because mechanical, electrical, and plumbing infrastructure must comply with tightening energy-efficiency benchmarks. Asset managers accelerate the adoption of predictive analytics by fitting HVAC equipment with vibration and temperature sensors that trigger intervention before breakdown. In 2024, more than 60% of hard-service contracts included remote-monitoring clauses, up from 42% in 2022. Fire-safety regulations now require integrated evacuation-simulation tools during annual audits, expanding the advisory element within technical maintenance. Accordingly, the sub-segment adds incremental revenue through compliance consultancy even as core maintenance margins compress.

By Offering Type: Outsourcing Dominance Accelerates

The outsourced model commanded 69.20% of the Denmark facility management market size in 2025 and is slated for 5.38% CAGR growth through 2031. Integrated facility management, where a single provider delivers bundled hard and soft services under outcome-based KPIs, represents the fastest-scaling contract form. These arrangements often run five to seven years and include capital project management alongside routine operations, enabling clients to consolidate vendor portfolios and unlock 8-12% total-cost reductions. Bundled facility management appeals to the mid-market cohort that seeks service consolidation but retains selective internal oversight. Single-service outsourcing continues to serve specialised technical needs such as critical-power maintenance in data centres.

In-house management retained a 30.80% share in 2025, concentrated in healthcare, defence, and select manufacturing plants where security or process continuity is viewed as mission-critical. Yet even these sectors increasingly adopt hybrid models that keep strategic oversight internal while subcontracting execution. DSB’s announced USD 90.45 million 2024 profit was accompanied by more than USD 6.0 billion capital earmarked for rolling-stock upgrades, a financial burden that encourages partial outsourcing of depot maintenance and facilities supervision. Over the long term, labour shortages and technology capital requirements will erode the practicality of standalone in-house operations.

By End-user Industry: Institutional Sector Accelerates Growth

Institutional and public-infrastructure estates will post a 4.72% CAGR to 2031, outpacing all other verticals as municipal and central authorities channel Recovery and Resilience funds into green retrofits. Government campuses now embed digital twins for energy optimisation, and military installations require high-grade perimeter security, catering, and equipment-maintenance solutions. Education facilities demand smart-classroom support and student-experience analytics, broadening service scope beyond custodial routines.

Commercial real estate still generated 31.50% of 2025 revenue and remains the largest slice of the Denmark facility management market. Corporate tenants prioritise agile workspace configurations and occupancy analytics that accommodate hybrid working, reinforcing demand for sensor-enabled desk management and wellness-certified cleaning regimes. Retail and warehousing turn to flexible staffing models tied to foot-traffic data, while IT and telecom switch to uptime-driven service-level agreements for cooling and critical power. Industrial facilities leverage predictive maintenance to cut unplanned downtime by up to 15%, sustaining hard-service spend growth above inflation.

Geography Analysis

The Copenhagen metropolitan area accounted for the highest absolute spend in 2024, supported by the headquarters of multinational corporations, embassy clusters, and ministerial buildings. Office density in the capital exceeds the national average by 23%, driving premium demand for front-of-house, concierge, and wellness-related soft services. Aarhus and Odense post faster unit growth as companies decentralise operations in search of lower rents and access to regional talent pools; these cities now host a combined 18% of national Grade-A office stock. Aalborg and Esbjerg contribute steady expansion anchored to logistics, maritime, and energy supply chains, which require specialised hard services focused on corrosion control and hazard-class maintenance.

Nationwide, the Recovery and Resilience Plan funnels more than EUR 1.5 billion (USD 1.75 billion) into building renovations and energy optimisation projects. Because at least 60% of funds carry a green-transition mandate, municipalities across Jutland and Funen accelerate tenders for heat-pump retrofits, façade insulation, and solar-integrated roofs. Facility managers equipped with energy-performance contracting capabilities secure multi-year deals that bundle capex financing, installation oversight, and ongoing maintenance.

Geographic diversity gives rise to a dual-provider landscape. National full-service players operate central command centres that monitor thousands of properties, leveraging scale economies for helpdesk and analytics functions. Regional specialists compete successfully by offering hyper-local technician response times and cultural familiarity, particularly in small-city healthcare and elderly-care facilities. This mix ensures that the Denmark facility management market delivers tailored solutions across urban and peri-urban catchment areas.

Competitive Landscape

Nordic heavyweights dominate revenue share yet face intensifying rivalry from tech-centric entrants. ISS A/S leverages Microsoft-powered AI platforms to optimise task allocation and deliver predictive analytics across 10,000 Danish sites. Coor Service Management executes a pan-Nordic sustainability roadmap that targets net-zero emissions by 2050 and has already rolled out climate-adaptation measures across 15 million m² of managed property. Compass Group Denmark captures first-time outsourcing wins in catering, supported by digital recipe-management tools that cut food waste by 26% and meet CSRD reporting needs.

Emerging competitors deploy cloud-native building-management systems capable of 35% energy savings. Venture-funded start-ups specialise in SaaS carbon-accounting modules that integrate directly with legacy CAFM suites, appealing to mid-market clients seeking cost-effective ESG compliance. Consolidation continues as larger players acquire HVAC and security boutiques to fill technical capability gaps; Apleona’s purchase of Air for All underlines this trend and is expected to boost cross-sell potential in Denmark once post-merger integration completes.

Barriers to entry remain moderate because incumbents possess entrenched customer relationships and nationwide technician networks. However, digital disruption lowers switching costs for clients, making service quality and data transparency pivotal competitive levers. Over the next five years, the Denmark facility management market is likely to witness a convergence between FM-as-a-service models and proptech platforms, compelling all providers to broaden skill sets beyond traditional facilities upkeep.

Denmark Facility Management Industry Leaders

Coor Service Management A/S

Compass Group Denmark A/S

Sodexo Facilities Management Denmark A/S

G4S Facilities Management Denmark A/S

Apleona GmbH (Nordic Operations)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ISS announced a strategic partnership with a Nordic proptech start-up to integrate AI-driven energy dashboards across 2,000 Danish commercial buildings.

- August 2024: DSB confirmed a USD 6.0 billion rolling-stock investment programme through 2030, including new depot facilities requiring advanced maintenance and asset-lifecycle management.

- October 2024: The European Parliament ratified revisions to the Energy Performance of Buildings Directive, mandating 16% average energy-consumption cuts by 2030, which expands mandatory auditing work for certified FM contractors.

- August 2024: DSB confirmed a USD 6.0 billion rolling-stock investment programme through 2030, including new depot facilities requiring advanced maintenance and asset-lifecycle management.

Denmark Facility Management Market Report Scope

Facility management (FM) includes management methods and techniques for building management, infrastructure management for an organization, and the means of overall harmonization of the work environment in an organization. This system standardizes services and streamlines processes for an organization.

The Denmark facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehousing) |

| Hospitality (Hotels, Eateries and Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transport) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehousing) | |

| Hospitality (Hotels, Eateries and Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transport) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Denmark facility management market?

The Denmark facility management market size is USD 2.67 billion in 2026.

How fast is the market expected to grow?

It is projected to record a 3.98% CAGR between 2026 and 2031.

Which service category is expanding the quickest?

Soft services, including cleaning, security, and catering, are forecast to grow at a 5.95% CAGR through 2031.

Why is outsourcing preferred over in-house management?

Outsourcing delivers 8-12% total-cost savings and gives clients access to advanced IoT and ESG-reporting capabilities without heavy upfront investment.

What role does ESG regulation play in market demand?

Mandatory CSRD reporting now makes carbon monitoring and energy-efficiency services essential contract components, driving premium pricing for compliant providers.

Page last updated on: