Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

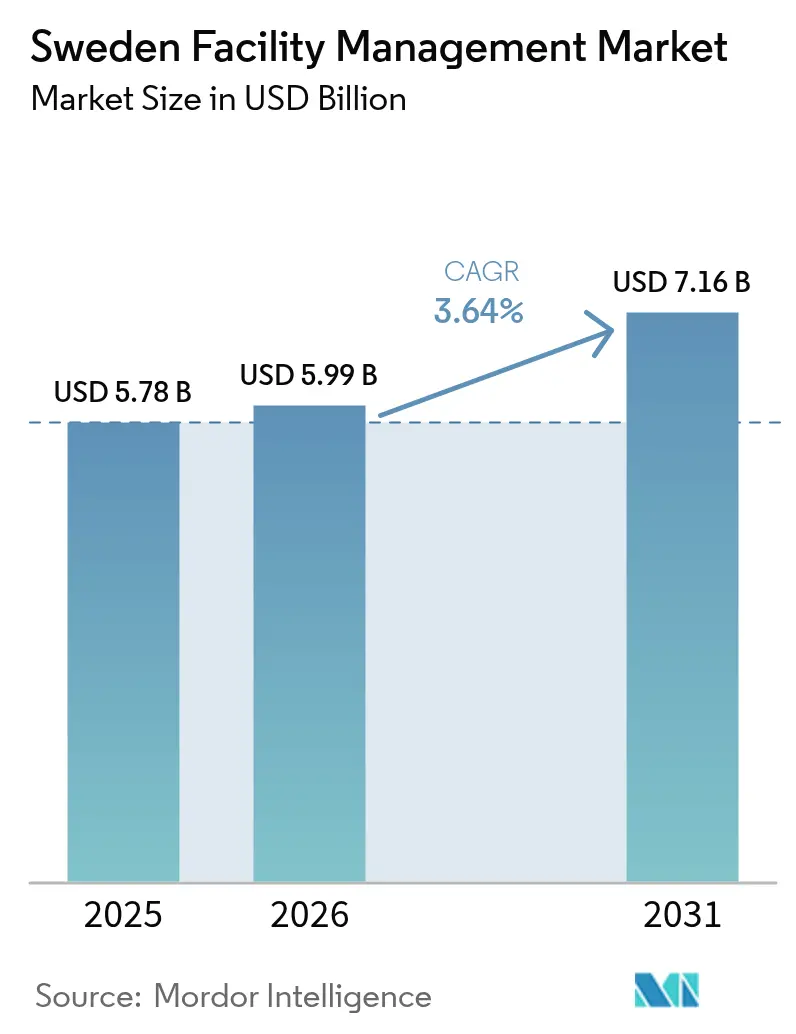

| Base Year Market Size (2025) | USD 5.78 Billion |

| Market Size (2026) | USD 5.99 Billion |

| Market Size (2031) | USD 7.16 Billion |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Facility Management Market Analysis by Mordor Intelligence

The Sweden facility management market size is expected to grow from USD 5.78 billion in 2025 to USD 5.99 billion in 2026 and is forecast to reach USD 7.16 billion by 2031 at 3.64% CAGR over 2026-2031. Market fundamentals hinge on the country’s strict energy-efficiency rules that require 14,000 commercial assets to stay below the 174 kWh/m²/year threshold, a move that continues to fuel hard-service demand. Workplace-wellness programs, digital twin adoption and Brookfield’s planned hyperscale data-center roll-out broaden the service opportunity set for providers with deep technology benches. Outsourcing momentum remains a central growth lever as organisations seek sharper focus on core activities, while sustainability mandates act as a catalytic driver for bundled energy and asset-performance contracts. Competition is vibrant, with ISS Facility Services, Coor Service Management and Securitas anchoring a field of regional specialists that leverage IoT, video support and AI for service differentiation.

Key Report Takeaways

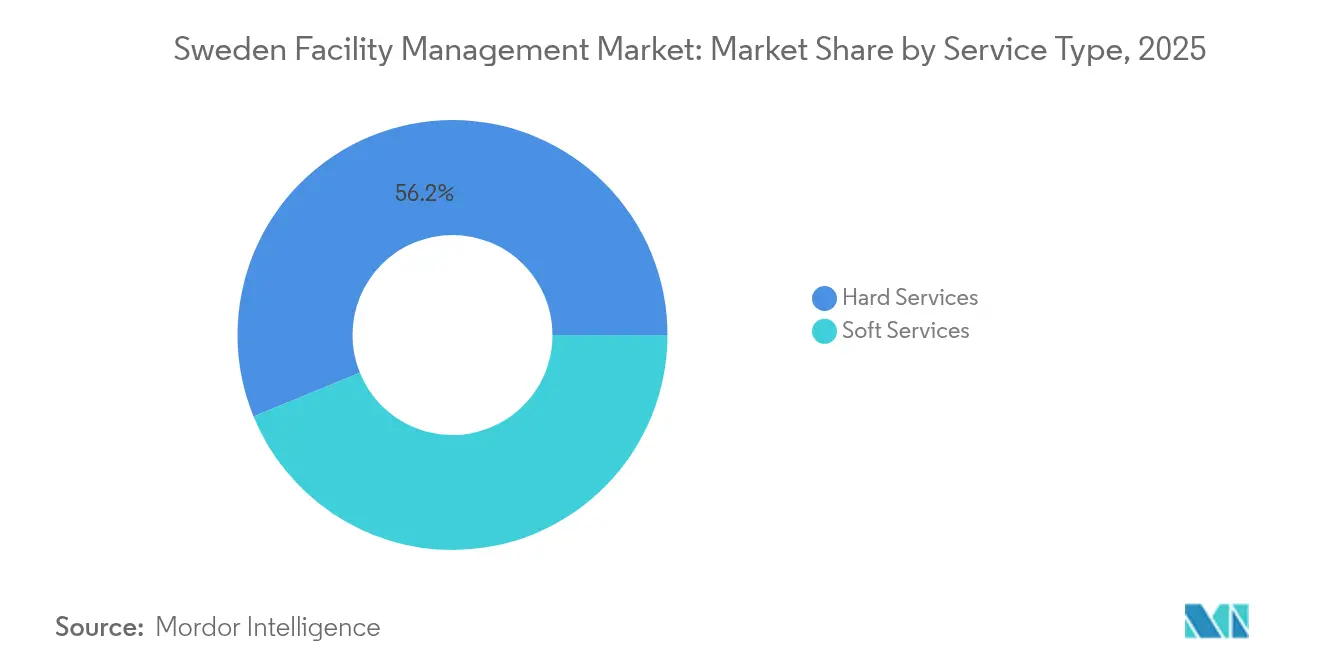

- By service type, hard services commanded 56.18% of Sweden facility management market share in 2025, whereas soft services are projected to advance at a 3.69% CAGR between 2026-2031.

- By offering, outsourced models captured 67.95% of Sweden facility management market size in 2025 and the integrated sub-segment is expected to expand at a 3.82% CAGR through 2031.

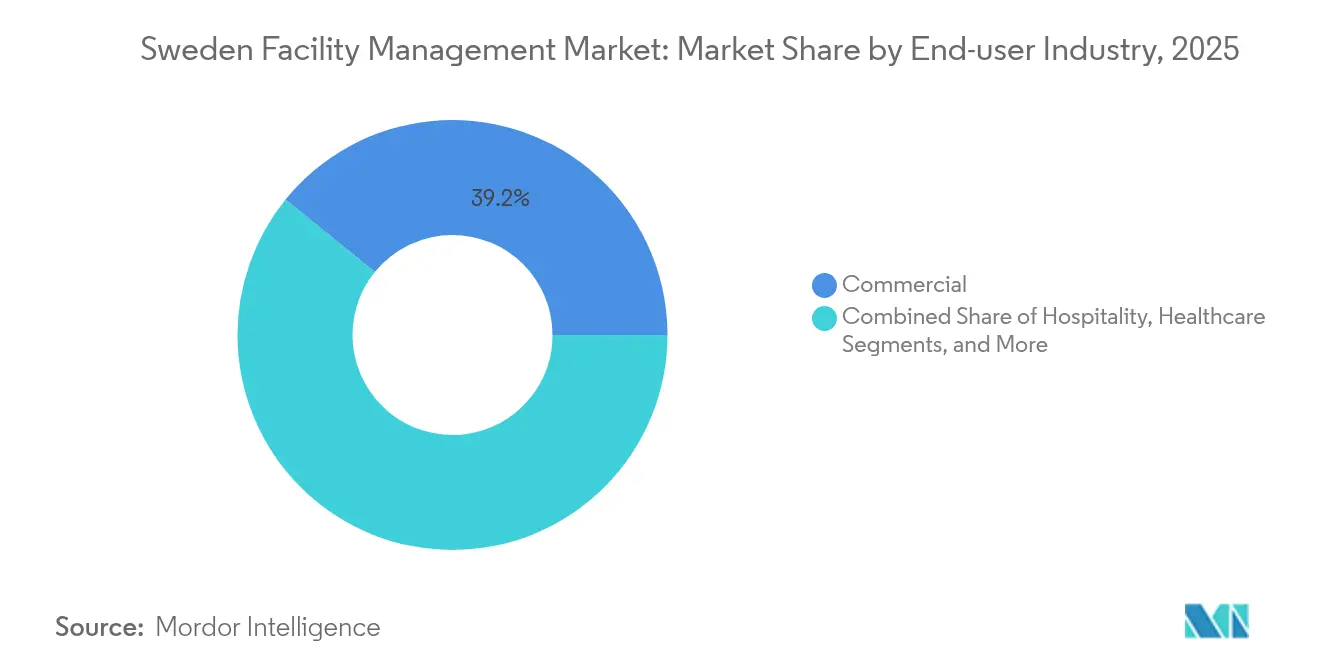

- By end-user, the commercial segment led with 39.15% revenue share in 2025; institutional and public infrastructure is set to grow the fastest at a 3.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Outsourcing of Non-core Functions | +0.8% | National, with concentration in Stockholm, Gothenburg, Malmö | Medium term (2-4 years) |

| Rising Demand for Integrated Facility Management | +0.7% | National, particularly strong in commercial and institutional sectors | Long term (≥ 4 years) |

| Growing Focus on Workplace Experience and Wellness | +0.6% | National, with emphasis on urban centers and knowledge economy hubs | Medium term (2-4 years) |

| Technological Advancements in Building Management | +0.5% | National, with early adoption in major metropolitan areas | Long term (≥ 4 years) |

| Government-backed Energy-Efficiency Performance Contracts | +0.4% | National, with priority on public sector buildings | Short term (≤ 2 years) |

| Digital Twin-Enabled Lifecycle FM Solutions Adoption | +0.3% | National, concentrated in large-scale commercial and industrial facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing outsourcing of non-core functions

Swedish companies view facility services as strategic enablers rather than operating costs, illustrated by Coor’s SEK 155 million (USD 16.02 million) annual PostNord renewal that consolidates cleaning, maintenance and logistical support under one roof. [1]Coor Service Management, “Financial Update for the Fourth Quarter,” coor.com Deep regulation on energy use coupled with mounting ESG disclosures intensifies the need for providers that can guarantee compliance, economies of scale and continuous innovation. Long-term leases such as Atea’s 3,200 m² Stockholm commitment underscore the preference for specialist operators who leverage predictive analytics to maintain uptime and extend asset life. The outsourcing narrative now extends well beyond cost optimisation, integrating risk transfer and data-driven performance outcomes to secure multi-year relationships.

Rising demand for integrated facility management

Clients increasingly fold hard and soft scopes into single contracts to simplify supplier governance and unlock unified data streams. Coor’s multi-service bundles—covering property, catering, cleaning and workplace experience exemplify the depth of value unlocked when one operator commands cross-functional insights. Hospitals provide a clear showcase: Karolinska University Hospital uses automated guided vehicles to handle 1,600 daily deliveries, integrating logistics, waste and sterile-goods flows under one digital command platform. [2]Skanska Group, “Stockholm County’s Innovative New Hospital – Robots and Much More,” skanska.com Integrated models empower continuous energy-performance tracking, immediate issue resolution and consolidated KPI dashboards that align with Sweden’s carbon-cut objective of net-zero by 2045.

Growing focus on workplace experience and wellness

Hybrid working makes the physical office a deliberate destination, shifting evaluation criteria from square-metre efficiency to human-centred value. Only 60% of Swedish employees take advantage of existing wellness benefits, prompting facility managers to embed biophilic design, circadian lighting and on-site fitness to foster behaviour change. [3]Oskar Ullberg, “Workplace Health Promotion to Facilitate Physical Activity Among Swedish Office Workers,” European Journal of Public Health, academic.oup.com Sweden also records Europe’s highest share of five-day in-office mandates, amplifying the need for experiential upgrades that raise talent retention thresholds. Air-quality monitoring, sit-stand desks and rapid service response times have become competitive differentiators, raising the bar for soft-service innovation.

Technological advancements in building management

AI, IoT and robotics move from pilot projects to revenue-scale deployments. Volvo Group’s AI-guided transporters reduce human-robot collision risk while maximising internal-logistics throughput at manufacturing plants. Husqvarna’s generative-AI facility companion slashes machine-fault diagnosis times by 60%, directly lowering downtime costs. Digital twins enable condition-based maintenance, decreasing system-failure incidents by up to 70% and curbing maintenance outlays by 30%. Such gains deliver measurable ROI that continues to pull FM budgets from reactive interventions to predictive service contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic Fluctuations and Cost Pressures | -0.9% | National, with particular impact on cost-sensitive sectors | Short term (≤ 2 years) |

| Workforce Challenges and Skill Gaps | -0.7% | National, with acute shortages in technical specialties | Medium term (2-4 years) |

| Escalating Cybersecurity Compliance Costs for Cloud-Based FM | -0.4% | National, concentrated in digitally advanced facilities | Medium term (2-4 years) |

| Contract Fragmentation from Municipal Procurement Decentralization | -0.3% | Regional and municipal levels, varying by administrative structure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Economic fluctuations and cost pressures

Inflation and rising energy tariffs are forcing providers to trim overhead while preserving service-level agreements. Coor’s SEK 120 million (USD 12.40 million) cost-containment programme illustrates the magnitude of margin pressure borne even by market leaders. Real-estate landlords pass higher utility and financing costs to occupiers, who respond by delaying non-essential refurbishments, directly stunting discretionary FM spend. Providers must therefore map variable-cost structures, emphasise continuous efficiency and demonstrate direct opex savings to retain contracts during procurement cycles.

Workforce challenges and skill gaps

Digital controls, smart meters and cyber-hardened building systems demand technicians with convergent IT-mechanical skillsets. Yet Sweden’s aging labour pool and acute competition from high-profile tech sectors create a recruitment shortfall that elevates wage bills and churn risk. Decision makers in municipal elder-care facilities report that welfare-technology adoption lags due to limited staff training capacity. Providers invest heavily in apprenticeship schemes, AR-supported troubleshooting and cross-skilling programmes to safeguard service quality despite labour scarcity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard-service dominance amid soft-service velocity

Hard services captured 56.18% revenue in 2025, propelled by mandatory retrofits and Sweden facility management market share gains from MEP, HVAC and fire-safety upgrades demanded by the new 174 kWh/m²/year ceiling. In value terms, hard services contributed USD 3.25 billion to Sweden facility management market size in 2025. Demand intensifies as asset owners fast-track energy-efficiency performance contracts, securing predictable returns through guarantee-backed savings.

Soft services, though smaller, are slated for a 3.69% CAGR to 2031, outpacing hard services as employers recalibrate offices for wellness, flexible occupancy and heightened hygiene expectations post-pandemic. Catering pivots to low-carbon menus, while cleaning adopts enzymatic, low-chemical processes that align with Swedish Green Building Council requirements. Security services integrate video analytics and mobile access management, underscoring a gradual shift toward outcome-based performance metrics.

By Offering Type: Outsourced and integrated surge

Outsourced solutions represented 67.95% of 2025 revenue or USD 3.93 billion of Sweden facility management market size, reflecting corporate preference for risk transfer and single-supplier accountability. Integrated facility management leads growth with a 3.82% CAGR, leveraging unified BMS dashboards and comprehensive SLA frameworks to deliver continuous improvement loops.

Single-service outsourcing remains relevant for niche functions such as vertical transport maintenance, yet bundling triggers measurable synergies in energy analytics and vendor coordination. In-house models persist in mission-critical public-safety facilities where security clearance drives make-or-buy decisions, but overall share inches downward as cost transparency and performance benchmarking mature.

By End-user Industry: Commercial reigns, institutional accelerates

Commercial premises spanning IT parks, retail flagship stores and omni-channel warehouses formed 39.15% of 2025 revenue. High-spec data centres financed by Brookfield and local operators heighten demand for resilient, AI-enabled FM contracts that guarantee 99.999% uptime.

Institutional and public infrastructure, benefitting from Sweden’s SEK 799 billion (USD 82.60 billion) national infrastructure plan, is on track for the fastest 3.86% CAGR as municipalities deploy smart-city street-lighting, energy-positive schools and hospital automation. Healthcare modernisation, highlighted by Karolinska University Hospital’s 1,600 daily AGV deliveries, spotlights the need for cross-disciplinary FM teams versed in clinical logistics and biomedical compliance. Industrial sites integrate IoT sensors to link production targets with facility uptime, while hospitality operators like Scandic pursue zero-waste certifications that pivot FM focus to circular resource flows.

Geography Analysis

Stockholm, Gothenburg and Malmö anchor over two-thirds of total market value thanks to dense commercial activity and the highest concentration of class-A real estate. Stockholm alone houses an expanding cluster of hyperscale data-centre projects that underpin critical-infrastructure FM contracts with stringent redundancy KPIs. Regional manufacturing hubs such as Västra Götaland rely on specialised technical FM to protect precision equipment from thermal drift and air-particle contamination.

Northern municipalities see heightened demand for remote-monitoring solutions as harsh climates shorten maintenance windows; IoT-enabled sensors transmit performance data to central control rooms, overcoming geographic isolation. University cities Uppsala and Umeå invest heavily in energy-renovation projects, pushing FM providers to guarantee stepwise kWh reductions aligned with Akademiska Hus’ 50% energy-delivery cutback target versus 2000 levels. Decentralised procurement means providers must adapt bids to varied contract volumes and service-quality benchmarks, but local governance also offers footholds for agile regional players.

Competitive Landscape

ISS leverages global purchasing power and a USD 12.1 billion 2024 revenue base to standardise processes, winning a five-year Barclays global extension that includes Swedish operations. Coor focuses on Nordic specialisation, expanding its portfolio through the SEK 155 million (USD 16.02 million) PostNord renewal and continuous facility-digitalisation initiatives that provide real-time SLA dashboards. Securitas, now offering converged guarding, remote video and IoT sensors, broadens client reliance on bundled security-FM accords.

Technology disruption breeds new entrants. Vallmo’s video-enabled remote-support model reduces on-site technician call-outs, while Kiona’s AI-driven energy-optimisation platform integrates legacy BMS equipment into a cloud edge that delivers double-digit energy savings. Consolidation remains measured, yet multi-service providers continue to snap up niche technical firms to gain advanced analytics, HVAC optimisation or green-cleaning IP.

Regulation-driven services such as EU Taxonomy reporting create added moat for incumbents with compliance credentials. Nevertheless, low switching costs in soft services keep pricing discipline tight, necessitating relentless innovation and contract-performance transparency to defend margins.

Sweden Facility Management Industry Leaders

Krohne Messtechnik GmbH

Kurita Water Industries Ltd

Durr Systems Inc.

Light House World Wide Solutions

Itasca Internationl Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Scandic confirmed a 236-room Uppsala Södra City hotel slated for Q2 2028 opening, designed to achieve Nordic Swan Ecolabel certification.

- April 2025: Volvo Group posted SEK 121.8 billion (USD 12.59 billion) Q1 2025 sales and reaffirmed AI-enabled internal-logistics deployment across Swedish sites.

- March 2025: ISS A/S launched a DKK 2.5 billion (USD 0.39 billion) share repurchase while maintaining CAPEX for FM-platform innovation.

- February 2025: Coor renewed its integrated FM mandate with PostNord, continuing to cover logistics hubs nationwide.

Sweden Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through their responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation. The objective of professional FM as an interdisciplinary business function is to coordinate the demand and supply of facilities and services in both public and private organizations.

The Sweden facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Sweden facility management market?

The market is valued at USD 5.99 billion in 2026 and is projected to expand to USD 7.16 billion by 2031, reflecting a 3.64% CAGR.

Which service type generates the most revenue?

Hard services dominate with 56.18% share in 2025 owing to mandatory energy-retrofit and safety-system upgrades.

Why is outsourcing growing so quickly?

Swedish organisations prefer outsourcing to focus on core competence, meet strict energy-efficiency rules and tap provider know-how, pushing outsourced models to 67.95% share in 2025.

Which segment is forecast to grow the fastest?

Institutional and public-infrastructure facilities are poised for a 3.86% CAGR through 2031 on the back of government smart-city and healthcare modernisation spend.

How is technology reshaping facility management in Sweden?

Providers deploy AI, digital twins and robotics for predictive maintenance, energy optimisation and automated logistics, cutting downtime and costs while meeting ESG targets.

Who are the leading companies in the Sweden facility management industry?

ISS Facility Services, Coor Service Management and Securitas headline the competitive landscape, together holding roughly one-fifth of national market revenue.

Page last updated on: